Chapter 15 – Statement of Cash Flows

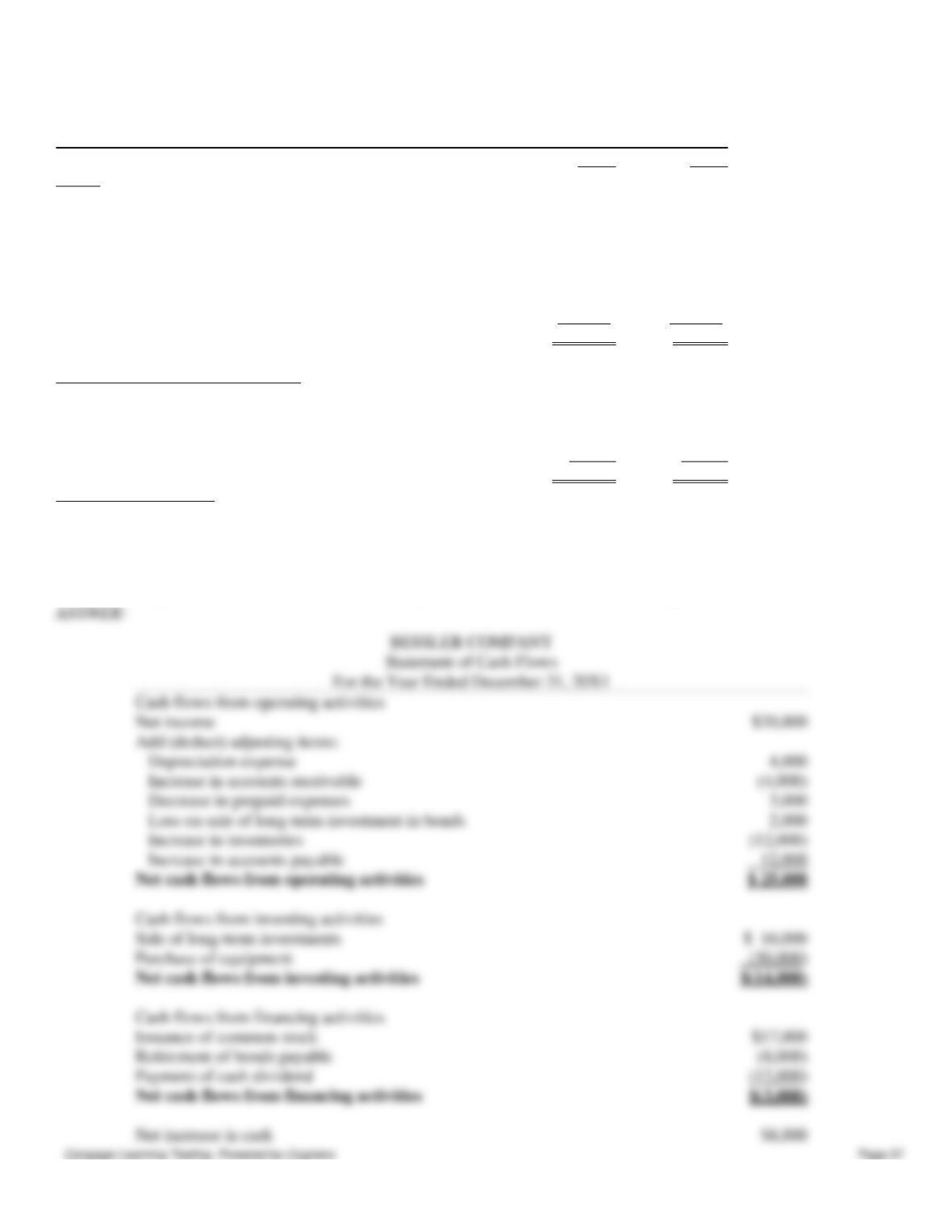

Bessler Company

Comparative Balance Sheet

20X1

20X0

Assets

Cash

$ 23,000

$15,000

Accounts receivable

18,000

14,000

Prepaid expenses

6,000

9,000

Inventory

27,000

15,000

Long-term investments

-0-

18,000

Equipment

60,000

30,000

Accumulated depreciation—equipment

(18,000)

(14,000)

Total assets

$116,000

$87,000

Liabilities and Stockholders’ Equity

Accounts payable

$ 21,000

$ 9,000

Bonds payable

37,000

45,000

Common stock

40,000

23,000

Retained earnings

18,000

10,000

Total liabilities and stockholders’ equity

$116,000

$87,000

Additional information:

1.

Net income for the year ending December 31, 20X1, was $20,000.

2.

Cash dividends of $12,000 were declared and paid during the year.

3.

Long-term investments that had a book value of $18,000 were sold for $16,000.

4.

Sales for 20X1 are $120,000.

Required: Prepare a statement of cash flows for the year ended December 31, 20X1, using the indirect method.

Cash flows from operating activities

Net income

$20,000

Add (deduct) adjusting items:

Depreciation expense

4,000

Increase in accounts receivable

Decrease in prepaid expenses

3,000

Loss on sale of long-term investment in bonds

2,000

Increase in inventories

(12,000)

Increase in accounts payable

12,000

Cash flows from investing activities

Sale of long-term investments

Purchase of equipment

Cash flows from financing activities

Issuance of common stock

$17,000

Retirement of bonds payable

Net increase in cash

$8,000

Chapter 15 – Statement of Cash Flows

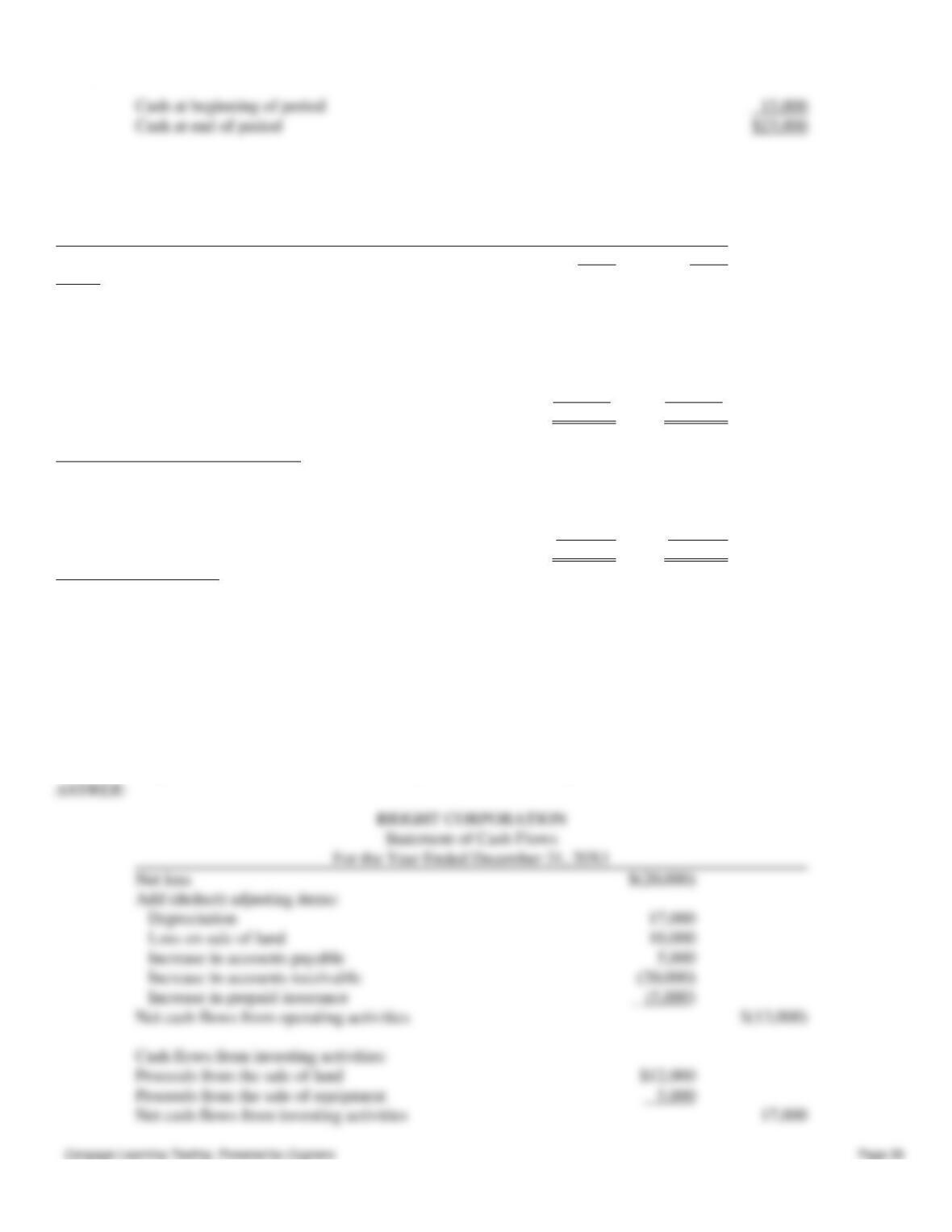

146. A comparative balance sheet for the Bright Corporation is presented below:

BRIGHT CORPORATION

Comparative Balance Sheet

20X1

20X0

Assets

Cash

$ 39,000

$ 31,000

Accounts receivable (net)

80,000

60,000

Prepaid insurance

22,000

17,000

Land

18,000

40,000

Equipment

70,000

60,000

Accumulated depreciation

(20,000)

(13,000)

Total assets

$209,000

$195,000

Liabilities and Stockholders’ Equity

Accounts payable

$ 11,000

$ 6,000

Bonds payable

27,000

19,000

Common stock

140,000

115,000

Retained earnings

31,000

55,000

Total liabilities &stockholders’ equity

$209,000

$195,000

Additional information:

1.

Net loss for 20X1 is $20,000. Net sales for 20X1 are $250,000.

2.

Cash dividends of $4,000 were declared and paid in 20X1.

3.

Land was sold for cash at a loss of $10,000. This was the only land transaction during the

year.

4.

Equipment with a cost of $15,000 and accumulated depreciation of $10,000 was sold for

$5,000 cash.

5.

$12,000 of bonds were retired during the year at carrying (book) value.

6.

Equipment was acquired for common stock. The fair market value of the stock at the time of

the exchange was $25,000.

Required: Prepare a statement of cash flows for the year ended 20X1 using the indirect method.

BRIGHT CORPORATION

Net loss

Add (deduct) adjusting items:

Depreciation

Loss on sale of land

Increase in accounts payable

Increase in accounts receivable

(20,000)

Increase in prepaid insurance

(5,000)

Net cash flows from operating activities

Cash flows from investing activities:

Proceeds from the sale of equipment

Net cash flows from investing activities

17,000

Cash at beginning of period

15,000

Cash at end of period

$23,000

Chapter 15 – Statement of Cash Flows

147. The following information is available for the Benning Corporation for the year ended Dec. 31, 20X1:

Collection of principal on long-term loan to a supplier

$35,000

Acquisition of equipment for cash

10,000

Proceeds from sale of long-term investment at book value

27,000

Issuance of common stock for cash

20,000

Depreciation expense

25,000

Redemption of bonds payable at carrying (book) value

24,000

Payment of cash dividends

9,000

Net income

35,000

Purchase of land by issuing bonds payable

40,000

In addition, the following information is available from the comparative balance sheet for Benning at the end of 20X1 and

20X0:

20X1

20X0

Cash

$107,000

$14,000

Accounts receivable (net)

20,000

15,000

Prepaid insurance

17,000

13,000

Total current assets

$144,000

$42,000

Accounts payable

$ 25,000

$19,000

Salaries payable

4,000

7,000

Total current liabilities

$ 29,000

$26,000

Required: Prepare Benning’s statement of cash flows for the year ended Dec. 31, 20X1, using the indirect method.

Cash flows from operating activities

Net income

$35,000

Adjustments to reconcile net income to net cash provided

Depreciation

25,000

Increase in accounts receivable

Increase in prepaid insurance

Increase in accounts payable

6,000

Cash flows from financing activities:

Retirement of bonds payable

Issuance of bonds payable

20,000

Payment of dividends

Net cash flows from financing activities

4,000

Increase in cash

$ 8,000

Cash at beginning of period (12−31−20X0)

31,000

Cash at end of period (12−31−20X1)

$ 39,000

Noncash investing and financing activities:

Purchase of equipment through issuance of common stock

$ 25,000

increase of $20,000.

Chapter 15 – Statement of Cash Flows

148. Assuming a statement of cash flows is prepared, indicate the reporting of the transactions and events listed below by

major categories on the statement. Use the following code letters to indicate the appropriate category under which the item

would appear on the statement of cash flows.

Code

Cash Flows From Operating Activities

Add to Net Income

A

Deduct from Net Income

D

Cash Flows From Investing Activities

IA

Cash Flows From Financing Activities

FA

Category

1.

Common stock is issued for cash at an amount above par value.

_____

2.

Merchandise inventory increased during the period.

_____

3.

Depreciation expense recorded for the period.

_____

4.

Building was purchased for cash.

_____

5.

Bonds payable were acquired and retired at their carrying value.

_____

6.

Accounts payable decreased during the period.

_____

7.

Prepaid expenses decreased during the period.

_____

8.

Treasury stock was acquired for cash.

_____

9.

Land is sold for cash at an amount equal to book value.

_____

10.

Patent amortization expense recorded for a period.

_____

Category

1.

Common stock is issued for cash at an amount above par value.

FA

2.

Merchandise inventory increased during the period.

D

3.

Depreciation expense recorded for the period.

A

4.

Building was purchased for cash.

IA

5.

Bonds payable were acquired and retired at their carrying value.

FA

6.

Accounts payable decreased during the period.

D

7.

Prepaid expenses decreased during the period.

A

Decrease in salaries payable

Cash flows from investing activities:

Collection of long-term loan

Proceeds from the sale of investments

Purchase of equipment

Cash flows from financing activities:

Issuance of common stock

Redemption of bonds

Payment of dividends

Increase in Cash

Cash at beginning of period

Cash at end of period

Noncash investing and financing activities

Purchase of land by issuing bonds

Chapter 15 – Statement of Cash Flows

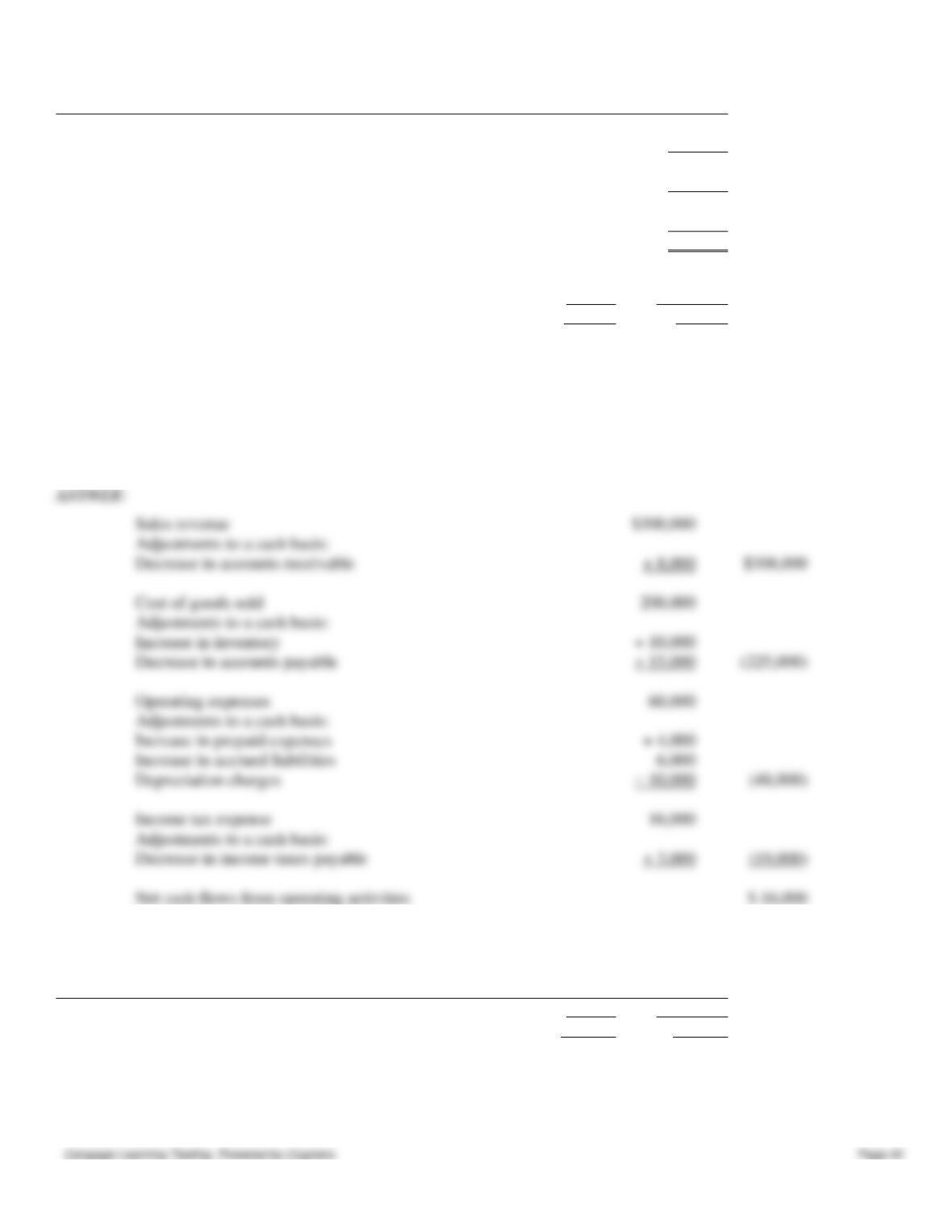

149. Playtown Company’s income statement for last year appears below:

Playtown Company

Income Statement

Sales

$100,000

Less: Cost of goods sold

60,000

Gross margin

$ 40,000

Less: Operating expenses

25,000

Income before income taxes

$ 15,000

Less: Income taxes

6,000

Net income

$ 9,000

The beginning and ending balances for last year are available for the following selected accounts:

Ending

balance

Beginning

balance

Accounts receivable

$15,000

$10,000

Inventory

29,000

25,000

Prepaid expenses

6,000

9,000

Accumulated depreciation

(35,000)

(30,000)

Accounts payable

27,000

20,000

Accrued liabilities

3,000

5,000

Income taxes payable

4,000

1,000

Required: Using the direct method, prepare the operating activities section of the statement of cash flows.

Sales revenue

$100,000

Adjustments to a cash basis:

Increase in accounts receivable

$95,000

Cost of goods sold

$ 60,000

Adjustments to a cash basis:

Increase in inventory

Increase in accounts payable

(57,000)

Operating expenses

$ 25,000

Adjustments to a cash basis:

Decrease in prepaid expenses

Decrease in accrued liabilities

Depreciation expense

(19,000)

Income tax expense

Adjustments to a cash basis:

Increase in income taxes payable

Net cash flows from operating activities

$16,000

150. Freeport Company’s income statement for last year appears below:

Treasury stock was acquired for cash.

Land is sold for cash at an amount equal to book value.

Patent amortization expense recorded for a period.

A

Chapter 15 – Statement of Cash Flows

Income Statement

Sales

$300,000

Less: Cost of goods sold

200,000

Gross margin

100,000

Less: Operating expenses

60,000

Income before income taxes

40,000

Less: Income taxes

16,000

Net income

$ 24,000

The beginning and ending balances for last year are available for the following accounts:

Ending

Beginning

balance

balance

Accounts receivable

$32,000

$40,000

Inventory

60,000

50,000

Prepaid expenses

12,000

8,000

Accumulated depreciation

(40,000)

(30,000)

Accounts payable

30,000

45,000

Accrued liabilities

16,000

10,000

Income taxes payable

2,000

5,000

Required: Using the direct method, prepare the operating activities section of the statement of cash flows.

Sales revenue

$300,000

Adjustments to a cash basis:

Decrease in accounts receivable

$308,000

Cost of goods sold

200,000

Adjustments to a cash basis:

Decrease in accounts payable

Operating expenses

60,000

Adjustments to a cash basis:

Increase in prepaid expenses

Increase in accrued liabilities

Depreciation charges

(48,000)

Income tax expense

16,000

Adjustments to a cash basis:

Decrease in income taxes payable

(19,000)

Net cash flows from operating activities

$ 16,000

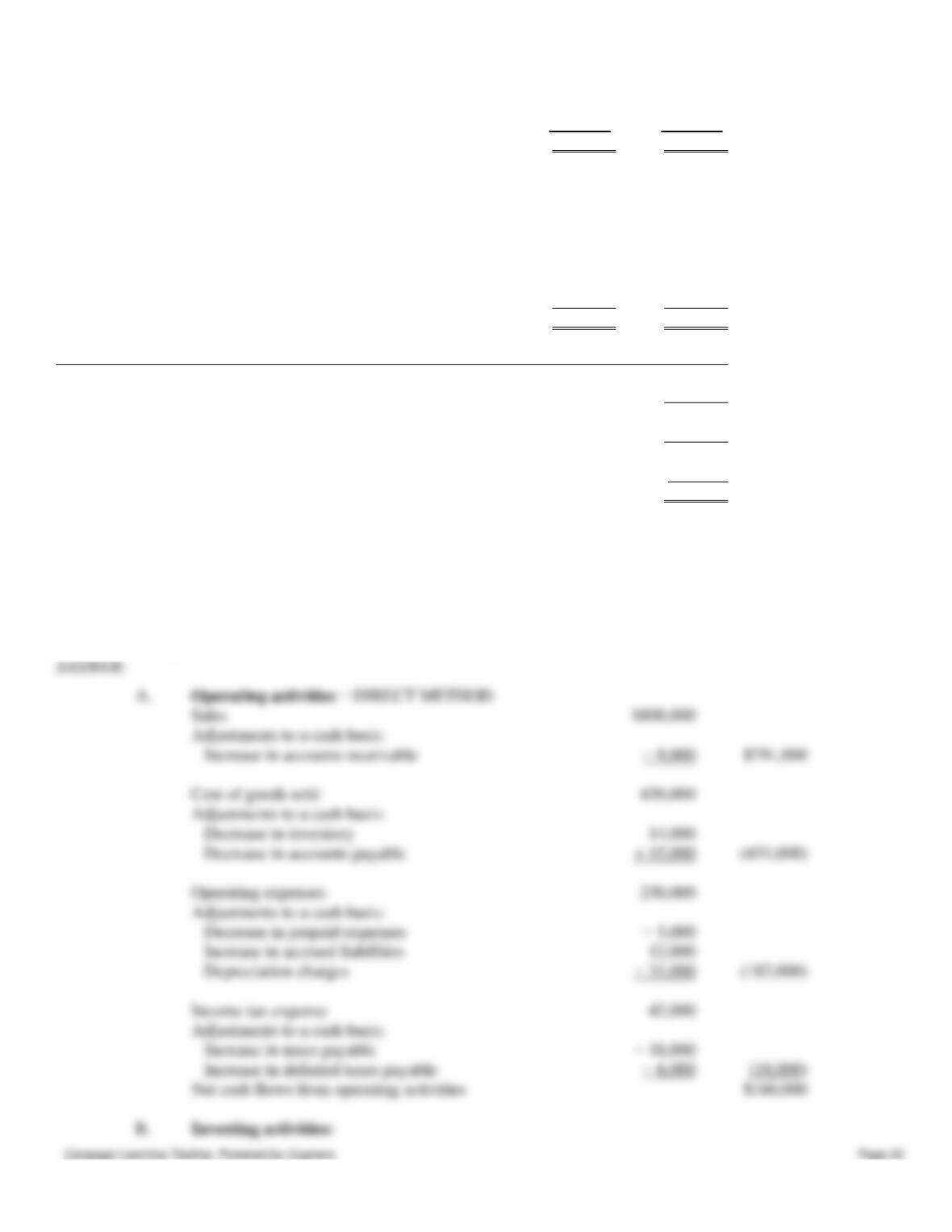

151. Gingerich Company’s comparative balance sheet and income statement for last year appear below:

Balance Sheet

Ending

Beginning

Balance

Balance

Cash

$ 45,000

$ 27,000

Accounts receivable

39,000

30,000

Inventory

30,000

44,000

Prepaid expenses

14,000

19,000

Long-term investments

280,000

200,000

Chapter 15 – Statement of Cash Flows

Plant and equipment

600,000

600,000

Accumulated depreciation

(322,000)

(291,000)

Total assets

$686,000

$629,000

Accounts payable

$ 19,000

$ 34,000

Accrued liabilities

37,000

25,000

Taxes payable

32,000

14,000

Deferred taxes payable

28,000

22,000

Bonds payable

100,000

150,000

Common stock

100,000

70,000

Retained earnings

370,000

314,000

Total liabilities and stockholders’ equity

$686,000

$629,000

Income Statement

Sales

$800,000

Less: Cost of goods sold

430,000

Gross margin

370,000

Less: Operating expenses

230,000

Net operating income

140,000

Less: Income taxes

42,000

Net income

$ 98,000

The company declared and paid $42,000 in cash dividends during the year.

Required: Using the direct method, prepare each of the following activities sections of the company’s statement of cash

flows for the year:

A.

Operating activities section.

B.

Investing activities section.

C.

Financing activities section.

A.

Sales

$800,000

Adjustments to a cash basis:

Increase in accounts receivable

Cost of goods sold

430,000

Adjustments to a cash basis:

Decrease in inventory

Decrease in accounts payable

Operating expenses

230,000

Adjustments to a cash basis:

Decrease in prepaid expenses

Increase in accrued liabilities

Depreciation charges

(182,000)

Income tax expense

42,000

Adjustments to a cash basis:

Increase in taxes payable

Net cash flows from operating activities

$160,000

B.

Chapter 15 – Statement of Cash Flows

152. The following information is available for Snider Company:

Receipts from customers

$180,000

Dividends from stock investments

3,000

Proceeds from sale of equipment

18,000

Proceeds from issuance of stock

90,000

Payments for goods

100,000

Payments for operating expenses

70,000

Interest paid

5,000

Taxes paid

4,000

Dividends paid

20,000

Required: Based on the preceding information, compute the net cash provided by operating activities.

Receipts from customers

$180,000

Dividends from stock investments

3,000

183,000

Payments for goods

$100,000

Payments for operating expenses

70,000

Interest paid

5,000

Taxes paid

4,000

153. Dolan Company’s income statement showed revenues of $250,000 and operating expenses of $160,000. Accounts

receivable decreased by $60,000 and accounts payable increased by $40,000 during the year.

Required: Compute (A) cash receipts from customers and (B) cash payments for operating expenses using the direct

method.

Cash receipts from customers = $310,000 ($250,000 + $60,000)

Cash payments for operating expenses = $120,000 ($160,000 − $40,000)

154. The general ledger of Lopez Company provides the following information:

Beginning

End of Year

of Year

Accounts Receivable

$ 55,000

$ 94,000

Inventory

350,000

210,000

Accounts Payable

40,000

65,000

Net sales for the year were $2,100,000 and cost of goods sold were $1,500,000.

Increase in long-term investments

Decrease in bonds payable

Increase in common stock

Cash dividends

Chapter 15 – Statement of Cash Flows

Required: Compute the following:

A.

Cash receipts from customers.

B.

Cash payments to suppliers.

A.

Cash receipts from customers

Sales + Decrease in Accounts Receivable

$2,100,000 + $39,000 = $2,139,000

B.

Cash payments to suppliers

First calculate the amount of purchases:

Beginning inventory

Add:

Purchases

Goods Available for sale

Less:

Ending inventory

Cost of goods sold

=

$1,640,000 + $25,000 = $1,665,000

155. The income statement of Stuart Company is shown below:

STUART COMPANY

Income Statement

For the Year Ended December 31, 20X0

Sales

$8,200,000

Cost of goods sold

5,400,000

Gross profit

$2,800,000

Operating expenses

Selling expenses

$500,000

Administrative expense

700,000

Depreciation expense

90,000

Amortization expense

30,000

1,320,000

Net income

$1,480,000

Additional information:

1.

Accounts receivable increased $400,000 during the year.

2.

Inventory increased $250,000 during the year.

3.

Prepaid expenses increased $200,000 during the year.

4.

Accounts payable to merchandise suppliers increased $100,000 during the year.

5.

Accrued expenses payable increased $180,000 during the year.

Required: Prepare the operating activities section of the statement of cash flows for the year ended December 31, 20X0,

for Stuart Company, using the direct method.

Chapter 15 – Statement of Cash Flows

156. The income statement of Bingham Inc. for the year ended December 31, 20X1, reported the following condensed

information:

Service revenue

$600,000

Operating expenses

360,000

Income from operations

$240,000

Income tax expense

60,000

Net income

$180,000

Bingham’s balance sheet contained the following comparative data at December 31:

20X1

20X0

Accounts receivable

$50,000

$40,000

Accounts payable

35,000

50,000

Income taxes payable

6,000

3,000

Bingham has no depreciable assets. Accounts payable pertains to operating expenses.

Require: Prepare the operating activities section of the statement of cash flows using the direct method.

Cash flows from operating activities

Cash receipts from customers ($600,000 − $10,000)

$590,000

For operating expenses ($360,000 + $15,000)

$375,000

For income taxes ($60,000 − $3,000)

57,000

Net cash provided by operating activities

$158,000

Cash flows from operating activities

Adjustments to Cash Basis:

Cost of Goods Sold

Operating expenses

Net cash provided by operations

Deduct: Increase in accounts receivable

Cost of goods sold

Add: Increase in inventory

250,000

Deduct: Increase in accounts payable

Operating expenses exclusive of depreciation and amortization

Add: Increase in prepaid expenses

200,000

Deduct: Increase in accrued expenses payable

Chapter 15 – Statement of Cash Flows

157. The income statement of Grimes Company is shown below:

GRIMES COMPANY

Income Statement

For the Year Ended December 31, 20X1

Sales

$ 8,000,000

Cost of goods sold

5,400,000

Gross profit

$ 2,600,000

Operating expenses

Selling expenses

$500,000

Administrative expense

700,000

Depreciation expense

90,000

Amortization expense

30,000

(1,320,000)

Net income

$ 1,280,000

Additional information:

1.

Accounts receivable increased $500,000 during the year.

2.

Inventory increased $250,000 during the year.

3.

Prepaid expenses increased $200,000 during the year.

4.

Accounts payable to merchandise suppliers increased $150,000 during the year.

5.

Accrued expenses payable increased $180,000 during the year.

Required: Prepare the operating activities section of the statement of cash flows for the year ended

December 31, 20X1, for Grimes Company, using the direct method.

Cash flows from operating activities

Cash receipts from customers

Cash payments:

To suppliers

$(5,500,000)

For operating expenses

(6,720,000)

Net cash provided by operations

(1)

Sales

Deduct: Increase in accounts receivable

Cash receipts from customers

(2)

Cost of goods sold

Add: Increase in inventory

250,000

Purchases

Deduct: Increase in accounts payable

Cash payments to suppliers

(3)

Operating expenses exclusive of depreciation and amortization

Add: Increase in prepaid expenses

200,000

Deduct: Increase in accrued expenses payable

Cash payments for operating expenses

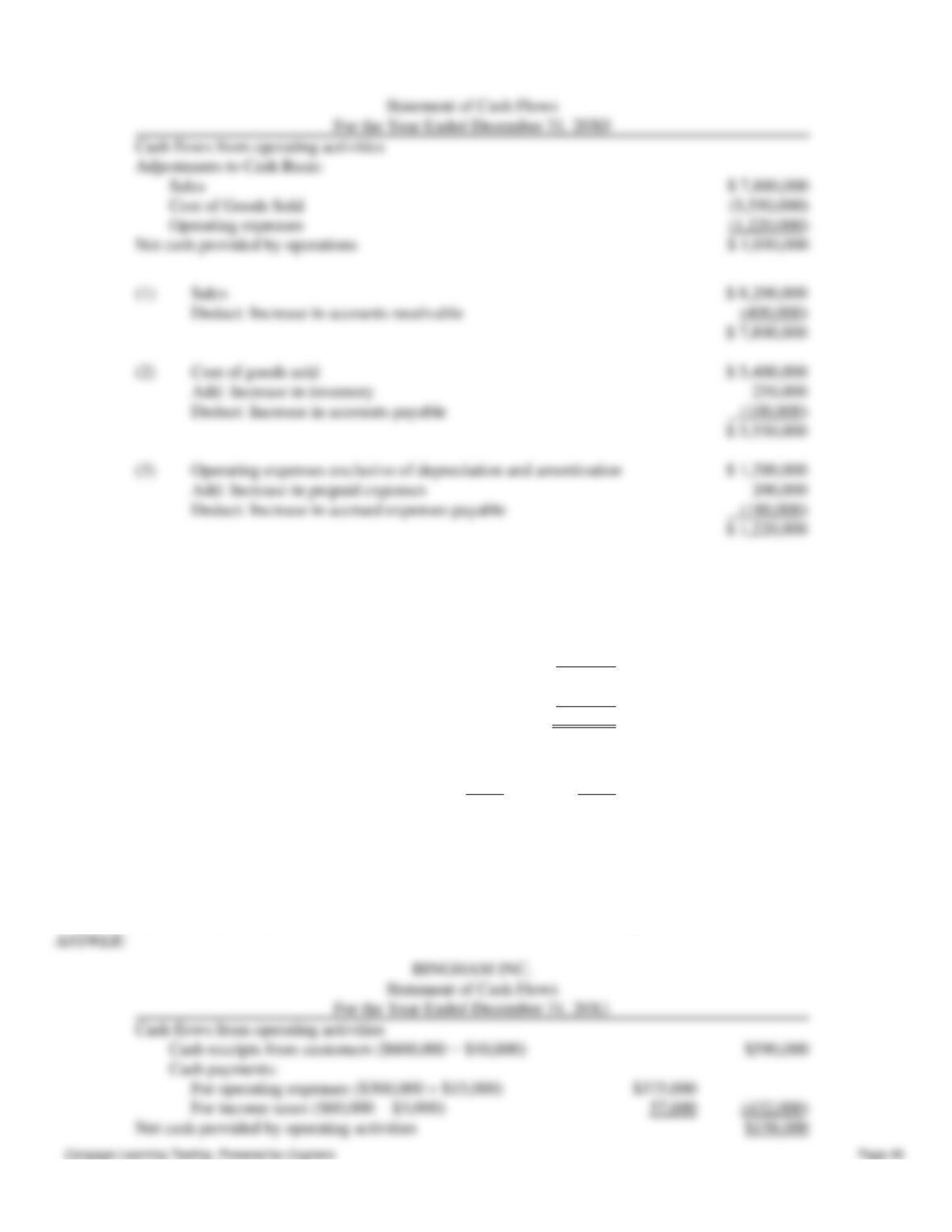

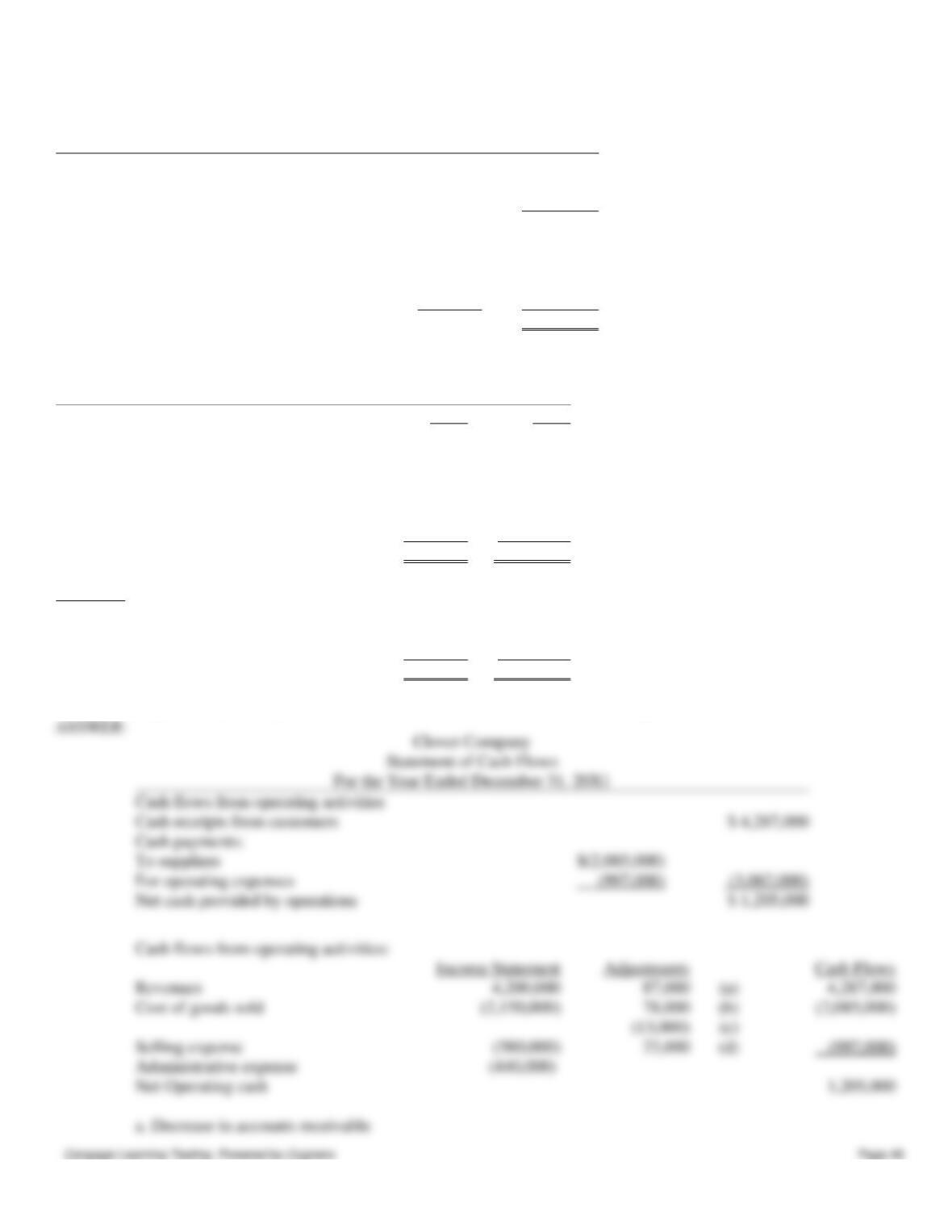

158. Clover Company had the following information for the years 20X1 and 20X0:

Chapter 15 – Statement of Cash Flows

Clover Company

Income Statement

For the Year Ended December 31, 20X1

Sales

$4,200,000

Cost of goods sold

2,150,000

Gross profit

$2,050,000

Operating expense:

Selling expense

$580,000

Administrative expense

440,000

Depreciation expense

40,000

1,060,000

Net income

$ 990,000

Clover Company

Balance Sheet

December 31, 20X1

20X1

20X0

Assets

Cash

$ 16,000

$ 22,000

Accounts receivable

325,000

412,000

Inventory

127,000

205,000

Property, plant and equipment

300,000

300,000

Accumulated depreciation

120,000

100,000

Total assets

$888,000

$1,039,000

Liabilities

Accounts payable

$ 46,000

$ 59,000

Accrued expenses

65,000

42,000

Stockholders’ equity

777,000

938,000

Total liabilities and equity

$888,000

$1,039,000

Required: Prepare the operating activities section of the statement of cash flows using the direct method.

Cash flows from operating activities

Cash receipts from customers

Cash payments:

For operating expenses

Net cash provided by operations

Cash flows from operating activities:

Revenues

Cost of goods sold

Selling expense

(580,000)

Administrative expense

Net Operating cash

Chapter 15 – Statement of Cash Flows

b. Decrease in inventory

c. Decrease in accounts payable

d. Increase in accrued expenses

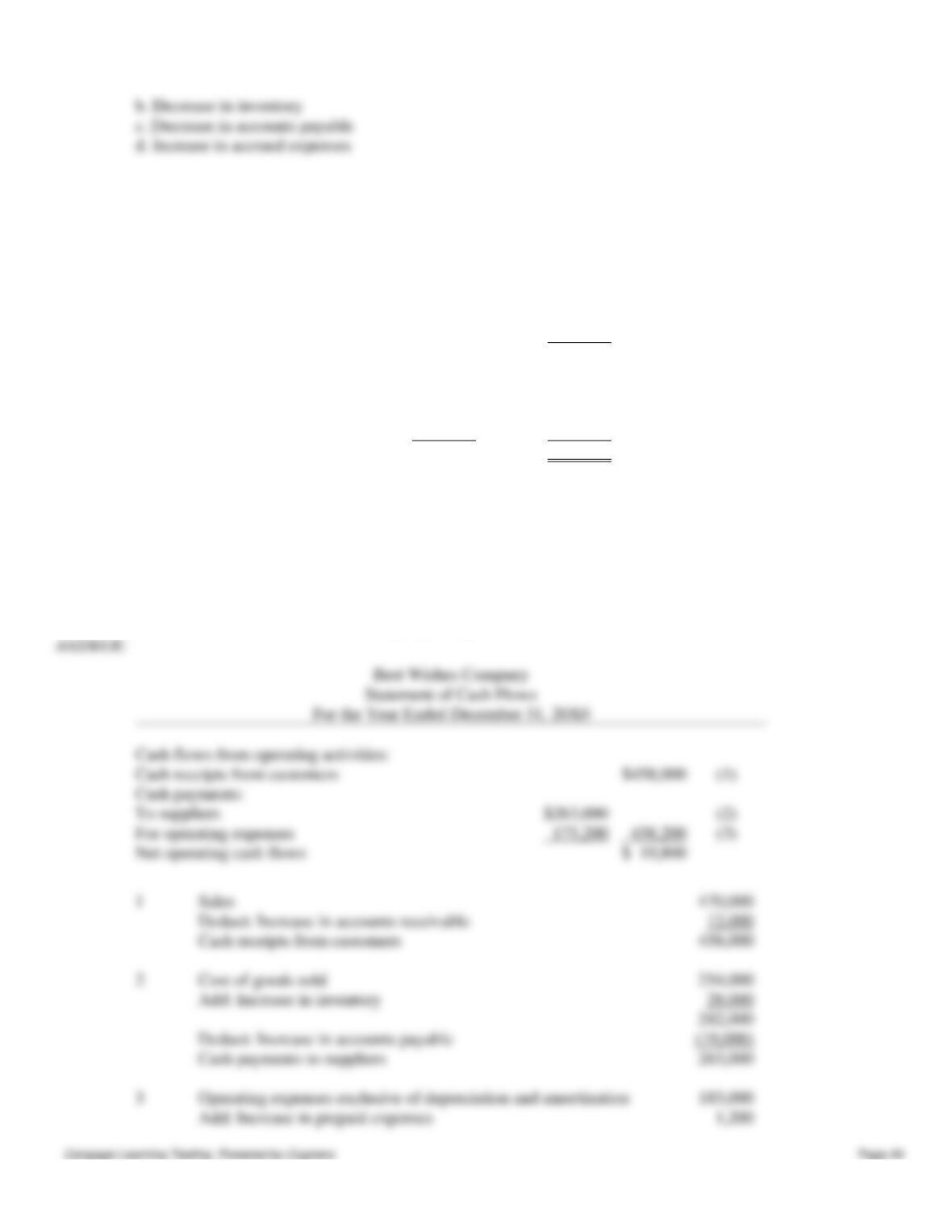

159. Best Wishes Company had the following information for the year ended December 31, 20X0:

Best Wishes Company

Income Statement

For the Year Ended December 31, 20X0

Sales

$470,000

Cost of goods sold

254,000

Gross profit

$216,000

Operating expenses

Selling expense

$110,000

Administrative expense

73,000

Amortization expense

14,000

197,000

Net income

$ 19,000

Additional information:

a. Accounts receivable increased by $12,000.

b. Inventories increased by $28,000.

c. Prepaid expenses increased by $1,200.

d. Accounts payable to merchandise suppliers increased by $19,000.

e. Accrued expenses payable increased by $9,000.

Required: Prepare the operating activities section of the statement of cash flows for the year

ended December 31, 20X0, for Best Wishes Company, using the direct method.

Cash flows from operating activities:

Cash receipts from customers

Cash payments:

For operating expenses

Net operating cash flows

Sales

Deduct: Increase in accounts receivable

Cash receipts from customers

Cost of goods sold

Add: Increase in inventory

Deduct: Increase in accounts payable

Cash payments to suppliers

Operating expenses exclusive of depreciation and amortization

Add: Increase in prepaid expenses

Chapter 15 – Statement of Cash Flows

160. The statement of cash flow classifies the cash flows into three categories. Describe each of these categories.

161. When preparing a statement of cash flows using the indirect method, why is depreciation added back to net income

within the operating activities section?

162. How is it possible for a company to suffer a net loss for a given year, yet produce a positive net cash flow from

operating activities?

163. If an asset is sold at a gain, why is the gain deducted from net income when computing the net cash flows from

operating activities under the indirect method?

You decide

164. There are five basic steps that are followed in preparing a statement of cash flows. List the five steps and briefly

describe what takes place in each step.

165. Cash flows from operating activities can be calculated using the indirect or direct method. Briefly describe how the

two methods differ yet arrive at the same information about the net cash flows from operating activities.

Chapter 15 – Statement of Cash Flows

Use the following major cash flow activities to classify the activities listed below:

a.

Operating Activity, Source of Cash

b.

Operating Activity, Use of Cash

c.

Investing Activity, Source of Cash

d.

Investing Activity, Use of Cash

e.

Financing Activity, Source of Cash

f.

Financing Activity, Use of Cash

g.

Non-cash Investing & Financing Activity

166. Land is exchanged for common stock

167. Reported profitable operations (Net Income)

a

168. Issued long-term debt

e

169. Payment of cash dividends

170. Sold equipment used in the business for cash

c

171. Payment of Operating Expenses

172. Collection of Sales Revenue

a

173. Purchased land for cash

174. Issued Common Stock for cash

e

175. Paid off long-term debt

Chapter 15 – Statement of Cash Flows

For each of the following items, indicate by using the appropriate code letter, how the item should be reported in the

statement of cash flows, using the indirect method.

a.

Added to net income

b.

Deducted from net income

c.

Cash outflow—investing activity

d.

Cash inflow—investing activity

e.

Cash outflow—financing activity

f.

Cash inflow—financing activity

g.

significant noncash investing and financing activity

176. Decrease in accounts payable during a period.

177. Declaration and payment of a cash dividend.

178. Loss on sale of land.

179. Decrease in accounts receivable during a period.

180. Redemption of bonds for cash.

181. Proceeds from sale of equipment at book value.

182. Issuance of common stock for cash.

183. Purchase of a building for cash.

184. Acquisition of land in exchange for common stock.

185. Increase in merchandise inventory during a period.