Chapter 14 – Financial Statement Analysis

121. The following information pertains to Newman Company. Assume that all balance sheet amounts represent both

average and ending balance figures and that all sales were on credit.

Assets

Cash and short-term investments

$ 40,000

Accounts receivable (net)

30,000

Inventory

25,000

Property, plant, and equipment

215,000

Total Assets

$310,000

Liabilities and Stockholders’ Equity

Current liabilities

$ 60,000

Long-term liabilities

95,000

Stockholders’ equity—Common

155,000

Total liabilities and stockholders’ equity

$310,000

Income Statement

Sales

$90,000

Cost of goods sold

45,000

Gross margin

$45,000

Operating expenses

20,000

Net income

$25,000

Number of shares of common stock

6,000

Market price of common stock

$40

Dividends per share

$1.00

Cash provided by operations

$40,000

What is the return on total assets for this company?

a.

8.1%

b.

6.8%

c.

10.5%

d.

16.1%

Chapter 14 – Financial Statement Analysis

122. The following information pertains to Dallas Company. Assume that all balance sheet amounts represent both

average and ending balance figures and that all sales were on credit.

Assets

Cash and short-term investments

$ 40,000

Accounts receivable (net)

30,000

Inventory

25,000

Property, plant, and equipment

280,000

Total assets

$375,000

Liabilities and Stockholders’ Equity

Current liabilities

$ 60,000

Long-term liabilities

95,000

Stockholders’ equity—Common

220,000

Total liabilities and stockholders’ equity

$375,000

Income Statement

Sales

$90,000

Cost of goods sold

45,000

Gross margin

$45,000

Operating expenses

15,000

Net income

$30,000

Number of shares of common stock

6,000

Market price of common stock

$20

Dividends per share

$1.00

Cash provided by operations

$40,000

What is the return on stockholders’ equity?

a.

7.3%

b.

13.6%

c.

20.5%

d.

40.9%

Chapter 14 – Financial Statement Analysis

123. A company reports the following:

Net income

$160,000

Preferred dividends

$10,000

Shares of common stock outstanding

20,000

Market price per share of common stock

$35

The company’s earnings per share on common stock is

a.

$13.33

b.

$8.50

c.

$7.50

d.

$35.00

124. Corporate annual reports typically do not contain

a.

management discussion and analysis

b.

an SEC statement expressing an opinion

c.

accompanying notes

d.

an auditor’s report

125. The independent auditor’s report

a.

describes which financial statements are covered by the audit

b.

gives the auditor’s opinion regarding the fairness of the financial statements

c.

summarizes what the auditor did

d.

states that the financial statements were presented on time

Chapter 14 – Financial Statement Analysis

126. The purpose of an audit is to

a.

determine whether or not a company is a good investment

b.

render an opinion on the fairness of the statements

c.

determine whether or not a company complies with corporate social responsibility

d.

determine whether or not a company is a good credit risk

127. Which of the following is required by the Sarbanes-Oxley Act?

a.

a price-earnings ratio

b.

a report on internal control

c.

a vertical analysis

d.

a common-sized statement

128. All of the following are typically included in the management’s discussion and analysis in annual reports except

a.

explanations of any significant changes between the current and prior years’ financial statements

b.

management’s assessment of liquidity

c.

journal entries

d.

off-balance-sheet arrangements

Chapter 14 – Financial Statement Analysis

129. Which of the following would appear as an unusual item on the income statement?

a.

loss resulting from the sale of fixed assets

b.

gain resulting from the disposal of a segment of the business

c.

presentation of earnings per share

d.

stock split

130. A loss on disposal of a segment would be reported in the income statement as a(n)

a.

administrative expense

b.

other expense

c.

deduction from income from continuing operations

d.

selling expense

131. Which of the following is not an unusual item?

a.

a segment of the business being sold

b.

corporate income tax being paid

c.

a change from one accounting method to another acceptable accounting method

d.

closure of all outlet stores

Chapter 14 – Financial Statement Analysis

132. Which of the following is considered an unusual item affecting the prior period’s income statement?

a.

a change in accounting principles

b.

fixed asset impairments

c.

sale of company stores in Florida

d.

discontinued operations

133. A loss due to a discontinued operation should be reported on the income statement

a.

above income from continuing operations

b.

without related tax effect

c.

below income from continuing operations

d.

as an operating expense

134. A change from one acceptable accounting method to another is reported

a.

on the statement of retained earnings, as a correction to the beginning balance

b.

on the income statement, below income from continuing operations

c.

on the income statement, above income tax expense

d.

through a retroactive restatement of prior-period earnings

Chapter 14 – Financial Statement Analysis

135. Which of the following items should be classified as an unusual item on an income statement?

a.

gain on the retirement of a bond payable

b.

gain on a sale of a long-term investment

c.

loss due to a discontinued operation in Colorado

d.

selling treasury stock for more than the company paid for it

136. Which of the following items appear on the corporate income statement before income from continuing operations?

a.

cumulative effect of a change in accounting principle

b.

income tax expense

c.

presentation of earnings per share

d.

loss on discontinued operations

137. The price-earnings ratio on common stock is calculated as:

a.

market price per share of common stock, divided by earnings per share on common stock.

b.

earnings per share of common stock, divided by market price per share of common stock.

c.

market price per share of common stock, divided by dividends per share of common stock.

d.

dividends per share of common stock, divided by earnings per share on common stock.

138. Dividend yield on common stock is calculated as:

a.

dividends on common stock, divided by shares of common stock outstanding.

b.

net income minus preferred dividends, divided by shares of common stock outstanding.

c.

dividends per share of common stock, divided by earnings per share.

d.

dividends per share of common stock, divided by market price per share of common stock.

Chapter 14 – Financial Statement Analysis

139. Select the correct presentation for other comprehensive income on the financial statements of Puma Company.

a.

Puma Company

Income Statement

For the Year Ended December 31, 20Y3

Sales

$625,000

Cost of goods sold

350,000

Gross profit

$275,000

Operating expenses

135,000

Net income

$140,000

Other comprehensive income

20,000

Comprehensive income

$160,000

b.

Puma Company

Statement of Comprehensive Income

For the Year Ended December 31, 20Y3

Net income

$140,000

Other comprehensive income

20,000

Comprehensive income

$160,000

c.

Both are correct

d.

Neither is correct

140. Manx Company owns one investment, purchased several years ago for $20,000. As of the end of the year two years

ago, the investment had increased in value to $26,000. As of the end of the current year, the investment had decreased

somewhat in value, to $24,000. Manx anticipates selling the investment in the coming year and expects to receive

$28,000. Under fair value accounting, what would be the value of the investments account on the current year’s

December 31 balance sheet?

a.

$24,000

b.

$20,000

c.

$26,000

d.

$28,000

Chapter 14 – Financial Statement Analysis

(current) value at the balance sheet date.

141. Accumulated other comprehensive income is presented in the financial statements:

a.

either on the income statement or in a separate statement of comprehensive income.

b.

on the balance sheet as part of stockholders’ equity.

c.

on the income statement only.

d.

in a separate statement only.

comprehensive income.

FNMN.WARR.17.14-APP2 – LO: 14–APP2

BUSPROG – Analytic

Match each definition that follows with the term (a–h) it defines.

a.

solvency

b.

leverage

c.

times interest earned

d.

horizontal analysis

e.

vertical analysis

f.

common-sized financial statements

g.

current position analysis

h.

profitability analysis

DIFFICULTY:

Bloom’s: Remembering

Easy

LEARNING OBJECTIVES:

FNMN.WARD.17.14-01 – LO: 14–01

FNMN.WARD.17.14-02 – LO: 14–02

FNMN.WARD.17.14-03 – LO: 14–03

FNMN.WARD.17.14-04 – LO: 14–04

FNMN.WARD.17.14-05 – LO: 14–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.02 – GAAP

ACCT.ACBSP.APC.23 – Financial Statement Analysis

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

Chapter 14 – Financial Statement Analysis

142. a percentage analysis of increases and decreases in related items on comparative financial statements

143. use debt to increase the return on an investment

144. an analysis of a company’s ability to pay its current liabilities

145. the percentage analysis of the relationship of each component in a financial statement to a total within the statement

146. a company’s ability to make interest payments and repay debt at maturity

147. focuses on a company’s ability to generate net income

148. useful for comparing one company to another or to industry averages

149. measures the risk that interest payments will not be made if earnings decrease

Match each ratio that follows to its use (items a–h). Items may be used more than once.

a.

assess the profitability of the assets

b.

assess how effectively assets are used

c.

indicate the ability to pay current liabilities

d.

indicate how much of the company is financed by debt and equity

e.

indicate instant debt-paying ability

f.

assess the profitability of the investment by common stockholders

g.

indicate future earnings prospects

h.

indicate the extent to which earnings are being distributed to common stockholders

DIFFICULTY:

Bloom’s: Remembering

Moderate

LEARNING OBJECTIVES:

FNMN.WARD.17.14-03 – LO: 14–03

FNMN.WARD.17.14-04 – LO: 14–04

FNMN.WARD.17.14-05 – LO: 14–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.23 – Financial Statement Analysis

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

150. price-earnings (P/E) ratio

151. working capital

Chapter 14 – Financial Statement Analysis

152. return on total assets

153. ratio of liabilities to stockholders’ equity

154. quick ratio

155. return on common stockholders’ equity

156. current ratio

157. asset turnover ratio

158. dividends per share

159. earnings per share (EPS) on common stock

160. Cash and accounts receivable for Adams Company are provided below:

Current Year

Prior Year

Cash

$70,000

$50,000

Accounts receivable (net)

70,400

80,000

What is the amount and percentage of increase or decrease that would be shown with horizontal analysis?

Cash

$20,000 increase ($70,000 – $50,000) or 40%

Accounts receivable

$9,600 decrease ($80,000 – $70,400) or (12%)

Chapter 14 – Financial Statement Analysis

161. The following items were taken from the financial statements of Tilden, Inc., over a three-year period:

Item

Year 3

Year 2

Year 1

Sales

$360,000

$335,000

$290,000

Cost of goods sold

225,000

205,000

185,000

Gross profit

$135,000

$130,000

$105,000

Compute the following for each of the items listed.

(a)

The amount and percentage change from Year 2 to Year 3.

(b)

The amount and percentage change from Year 1 to Year 2.

Round percentages to one decimal place.

Sales

Cost of goods sold

Gross profit

162. Comparative information taken from the Friction Company’s financial statements is shown below:

Year 2

Year 1

(a)

Notes receivable

$ 25,500

$ 30,000

(b)

Accounts receivable

106,200

90,000

(c)

Retained earnings

77,000

70,000

(d)

Sales

654,000

600,000

(e)

Operating expenses

160,000

200,000

(f)

Income taxes payable

28,000

20,000

Using horizontal analysis, show the percentage change and direction (increase or decrease) from Year 1 to Year 2 with

Year 1 as the base year.

(a)

$4,500 ÷ $30,000 = 15% decrease

(b)

$16,200 ÷ $90,000 = 18% increase

(c)

$7,000 ÷ $70,000 = 10% increase

(d)

$54,000 ÷ $600,000 = 9% increase

(e)

$40,000 ÷ $200,000 = 20% decrease

(f)

$8,000 ÷ $20,000 = 40% increase

Chapter 14 – Financial Statement Analysis

163. Revenue and expense data for Young Technologies Inc. are as follows:

Year 2

Year 1

Sales

$500,000

$440,000

Cost of goods sold

325,000

242,000

Selling expenses

70,000

79,200

Administrative expenses

75,000

70,400

Income tax expense

10,500

16,400

(a)

Prepare an income statement in comparative form, stating each item for both years as an

amount and as a percent of sales. Round to the nearest whole percent.

(b)

Comment on the significant changes disclosed by the comparative income statement.

Sales

Cost of goods sold

Gross profit

Selling expenses

Administrative expenses

Total expenses

Income from operations

Income tax expense

3%.

164. Cash and accounts receivable for Ashfall Co. are provided below:

Current Year

Prior Year

Cash

$62,400

$58,000

Accounts receivable (net)

42,000

50,000

Based on this information, what is the amount and percentage of increase or decrease that would be shown on a balance

sheet with horizontal analysis? Round percentages to one decimal place.

Cash

$4,400 increase ($62,400 – $58,000) or 7.6%

Accounts receivable

$8,000 decrease ($42,000 – $50,000) or (16%)

Chapter 14 – Financial Statement Analysis

165. Income statement information for Lucy Company is provided below:

Sales

$175,000

Cost of goods sold

105,000

Gross profit

$ 70,000

Prepare a vertical analysis of the income statement for Lucy Company.

Sales

Cost of goods sold

Gross profit

166. Why would you or why wouldn’t you compare an organization like Ford Motor Company to the local car dealer

“Johnson City Ford/Lincoln/Mercury” using vertical and horizontal analysis?

While they both sell Ford cars, they are not comparable companies.

Chapter 14 – Financial Statement Analysis

167. The balance sheet data of Randolph Company for two recent years appears below:

Assets:

Year 2

Year 1

Current assets

$ 445

$280

Plant assets

680

520

Total assets

$1,125

$800

Liabilities and stockholders’

equity:

Current liabilities

$ 285

$120

Long-term debt

255

160

Common stock

325

320

Retained earnings

260

200

Total liabilities and

stockholders’ equity

$1,125

$800

(a)

Using horizontal analysis, show the percentage change for each balance sheet item

using Year 1 as a base year.

(b)

Using vertical analysis, prepare a comparative balance sheet.

Round percentages to one decimal place.

(a)

(Decrease)

Current assets

Plant assets

Total assets

Current liabilities

Long-term debt

Common stock

Retained earnings

Total liabilities and stockholders’

(b)

Current assets

Long-term debt

Common stock

Retained earnings

Total liabilities and stockholders’ equity

Chapter 14 – Financial Statement Analysis

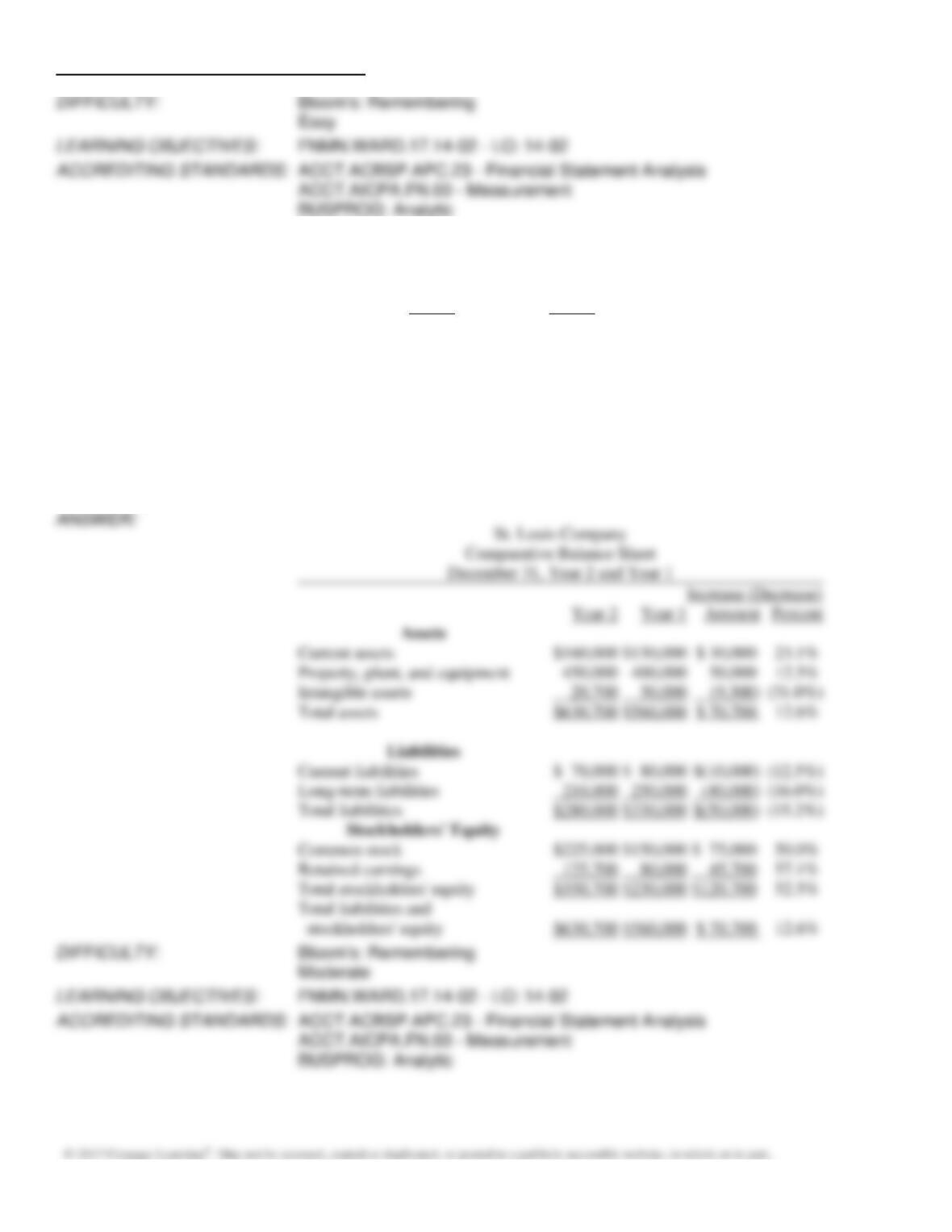

168. Condensed data taken from the ledger of St. Louis Company at December 31, for the current and preceding years, are

as follows:

Year 2

Year 1

Current assets

$160,000

$130,000

Property, plant, and equipment

450,000

400,000

Intangible assets

20,700

30,000

Current liabilities

70,000

80,000

Long-term liabilities

210,000

250,000

Common stock

225,000

150,000

Retained earnings

125,700

80,000

Prepare a comparative balance sheet, with horizontal analysis, for December 31, Year 2 and Year 1. (Round percents to

one decimal point.)

Increase (Decrease)

Current assets

Property, plant, and equipment

Intangible assets

Total assets

Current liabilities

Long-term liabilities

Total liabilities

Common stock

Retained earnings

Total stockholders’ equity

Total liabilities and

Chapter 14 – Financial Statement Analysis

169. Revenue and expense data for Bluestem Company are as follows:

Year 2

Year 1

Administrative expenses

$ 37,000

$ 20,000

Cost of goods sold

350,000

320,000

Income tax

40,000

32,000

Sales

800,000

700,000

Selling expenses

150,000

110,000

(a)

Prepare a comparative income statement, with vertical analysis, stating each item for both

years as a percent of sales.

(b)

Comment upon significant changes disclosed by the comparative income statement.

Round percentages to one decimal place.

Sales

Cost of goods sold

Gross profit

Selling expenses

Administrative expenses

Total operating expenses

Income before income tax

Income tax

170. What is a major advantage of using percentages rather than dollar changes in doing horizontal and vertical analysis?

Chapter 14 – Financial Statement Analysis

171. The following items are reported on a company’s balance sheet:

Cash

$230,000

Marketable securities

50,000

Accounts receivable

200,000

Inventory

240,000

Accounts payable

300,000

Determine the (a) current ratio, and (b) quick ratio. Round your answer to one decimal place.

Current ratio = ($230,000 + $50,000 + $200,000 + $240,000)/$300,000

Current ratio = 2.4

Quick ratio = ($230,000 + $50,000 + $200,000)/$300,000

Quick ratio = 1.6

172. The following items are reported on a company’s balance sheet:

Cash

$400,000

Marketable securities

50,000

Accounts receivable

150,000

Inventory

200,000

Accounts payable

250,000

Determine the (a) current ratio, and (b) quick ratio. Round your answer to one decimal place.

Current ratio = ($400,000 + $50,000 + $150,000 + $200,000)/$250,000

Current ratio = 3.2

Quick ratio = ($400,000 + $50,000 + $150,000)/$250,000

Quick ratio = 2.4

Chapter 14 – Financial Statement Analysis

173. The following items are reported on Denver Company’s balance sheet:

Cash

$190,000

Marketable securities

160,000

Accounts receivable (net)

240,000

Inventory

350,000

Accounts payable

600,000

Determine (a) the current ratio and (b) the quick ratio. Round to one decimal place.

(a)

Current ratio = Current assets ÷ Current liabilities

Current ratio = ($190,000 + $160,000 + $240,000 + $350,000) ÷ $600,000

Current ratio = 1.6

(b)

Quick ratio = Quick assets ÷ Current liabilities

Quick ratio = ($190,000 + $160,000 + $240,000) ÷ $600,000

Quick ratio = 1.0

174. For Garrison Corporation, the working capital at the end of the current year is $10,000 more than the working capital

at the end of the preceding year, reported as follows:

Year 2

Year 1

Current assets:

Cash, marketable securities, and receivables

$ 80,000

$ 84,000

Inventories

120,000

66,000

Total current assets

$200,000

$150,000

Current liabilities

100,000

60,000

Working capital

$100,000

$ 90,000

Has the current position of Garrison Corporation improved? Explain.

Working capital

Current ratio

Quick ratio

and the quick ratio has fallen from 1.4 to 0.8.