193. In 2014, Creative Design, Inc., instituted a quality improvement program. At the end of 2015, the

management of the corporation requested a report to show the amount saved by the measures taken during the

year. The actual sales and actual quality costs for 2014 and 2015 are as follows:

2014

2015

Sales

$125,000

$150,000

Scrap

3,750

3,750

Rework

5,000

2,500

Training program

1,250

1,500

Consumer complaints

2,500

1,250

Lost sales, incorrect labeling

2,000

—

Test labor

3,000

2,000

Inspection labor

6,250

6,000

Supplier evaluation

3,750

3,250

Required:

a.

Classify each cost as variable or fixed with respect to sales and compute the variable cost ratio for 2014. Be careful—costs may change

because of quality improvement, not cost behavior.

b.

How much did profits increase because of quality improvements made in 2015, assuming all reductions in quality costs are attributable to

quality improvements?

c.

Prepare an interim trend quality costs report for Creative Design, Inc.

a.

Scrap:

variable 3%

Rework:

variable 4%

Training program:

fixed

Lost sales, incorrect labeling:

variable 1.6%

Test labor:

variable 2.4%

Inspection labor:

variable 5%

Supplier evaluation:

fixed

194. At the beginning of the year, Alejandro Corporation initiated a quality improvement program. The program

was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement

program, the following data were collected for the current and preceding years:

2014

2015

2016

2017

Reliability engineering

$8,000

$10,000

$15,000

$25,000

Quality training

1,000

2,000

5,000

8,000

Packaging inspections

2,000

3,000

5,000

5,000

Product Acceptance

12,000

10,000

9,000

7,000

Rework

30,000

25,000

18,000

12,000

Reinspection

75,000

65,000

48,000

29,000

Customer complaints

100,000

85,000

62,000

51,000

Warranty and Repair

70,000

50,000

40,000

25,000

Required:

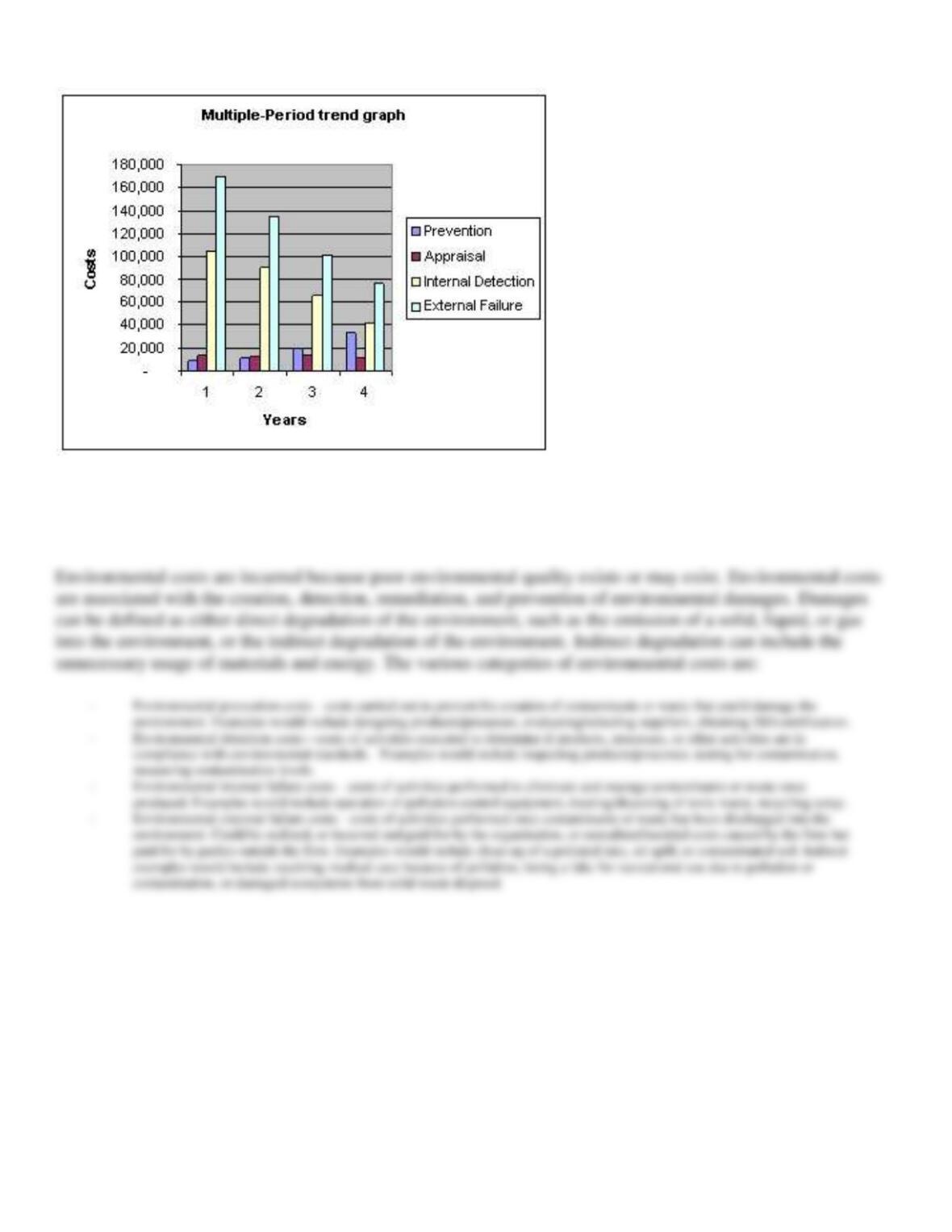

a. Prepare a multiple-year trend report for overall costs of quality.

b. Prepare a multiple-year trend report for each category of quality costs.

c. Graph the results.

2014

2015

2016

2017

Reliability engineering

8,000

10,000

15,000

25,000

Quality training

1,000

2,000

5,000

8,000

Packaging inspections

2,000

3,000

5,000

5,000

Product Acceptance

12,000

10,000

9,000

7,000

Rework

30,000

25,000

18,000

12,000

Reinspection

75,000

65,000

48,000

29,000

Customer complaints

100,000

85,000

62,000

51,000

Warranty and Repair

70,000

50,000

40,000

25,000

Overall Quality Costs

$298,000

$250,000

$202,000

$162,000

2011

2012

2013

2014

Prevention Costs

$9,000

$12,000

$20,000

$33,000

Appraisal Costs

14,000

13,000

14,000

12,000

Internal Failure Costs

105,000

90,000

66,000

41,000

External Failure Costs

170,000

135,000

102,000

76,000

Overall Costs

$298,000

$250,000

$202,000

$162,000

c.

195. Define environmental costs and identify the four categories of environmental costs. Give an example of

each category.

196. Using the abbreviations listed below, indicate for each of the costs whether the cost should be classified as:

P

=

Prevention

D

=

Detection

I

=

Internal Failure

E

=

External Failure

N

=

none of the above

1.

Cleaning up contaminated soil

2.

Designing processes

3.

Recycling scrap

4.

Auditing environmental activities

5.

Testing for contamination

6.

Losing a lake for recreational use

7.

Measuring contamination levels

8.

Recycling products

9.

Maintaining pollution equipment

10.

Evaluating and selecting suppliers

E

1.

Cleaning up contaminated soil

P

2.

Designing processes

I

3.

Recycling scrap

D

4.

Auditing environmental activities

D

5.

Testing for contamination

E

6.

Losing a lake for recreational use

D

7.

Measuring contamination levels

P

8.

Recycling products

I

9.

Maintaining pollution equipment

P

10.

Evaluating and selecting suppliers

197. Using the abbreviations listed below, indicate for each of the costs whether the cost should be classified as:

P

=

Prevention

D

=

Detection

I

=

Internal Failure

E

=

External Failure

N

=

none of the above

1.

Inspecting products and processes

2.

Verifying supplier environmental performance

3.

Testing for contamination

4.

Obtaining ISO 14001 certification

5.

Carrying out environmental studies

6.

Operating pollution control equipment

7.

Cleaning up a polluted lake

8.

Recycling scrap

9.

Recycling products

10.

Cleaning up oil spills

D

1.

Inspecting products and processes

D

2.

Verifying supplier environmental performance

D

3.

Testing for contamination

P

4.

Obtaining ISO 14001 certification

P

5.

Carrying out environmental studies

I

6.

Operating pollution control equipment

E

7.

Cleaning up a polluted lake

I

8.

Recycling scrap

P

9.

Recycling products

E

10.

Cleaning up oil spills

198. At the beginning of the year, Michelina, Inc., initiated an environmental cost reduction program. To help

assess the impact of the environmental cost reduction improvement program, the following data was collected

for the current and preceding year:

Preceding Year

Current Year

Operating costs

$4,000,000

$4,000,000

Designing products

18,000

20,000

Auditing environmental activities

40,000

64,000

Recycling scrap

200,000

180,000

Restoring land to natural state

360,000

320,000

Operating pollution control equipment

250,000

240,000

Testing for contamination

80,000

80,000

Required:

a.

Compute each category of environmental quality costs as a percentage of operating costs for each year.

Prevention costs

Detection costs

Internal failure costs

External failure costs

b.

How much has profit increased as a result of the environmental cost reduction improvements?

Preceding Year

Current Year

Prevention costs

0.45%

0.50%

[$18,000/$4,000,000]

[$20,000/$4,000,000]

Detection costs

3.00%

3.60%

Internal failure costs

11.25%

10.50%

[$360,000/$4,000,000]

[$320,000/$4,000,000]

$44,000 =

$948,000 – $904,000

199. Amenities Corporation reported the following operating costs and environmental quality costs for the past

four years. Assume that all environmental quality costs are variable and that all changes in the quality cost

ratios are due to an environmental cost reduction program.

Environmental Costs as

Year

Operating Cost

Percent of Operating Costs

1

$2,000,000

23.0

2

2,200,000

20.0

3

2,200,000

16.0

4

2,400,000

12.0

Required:

a.

Compute the environmental quality costs for all four years.

b.

How much did net income increase from Year 1 to Year 2 because of quality improvements? From Year 2 to Year 3? From Year 3 to Year

4?

a.

Environmental quality costs:

Year 1: $460,000

Year 2: $440,000

Year 3: $352,000

Year 4: $288,000

Net income increases:

Year 1: $460,000 – $440,000 = $20,000

Year 2: $440,000 – $352,000 = $88,000

Year 3: $352,000 – $288,000 = $64,000

200. At the beginning of the year, Heathrow, Inc., initiated an environmental cost reduction program. To help

assess the impact of the environmental cost reduction improvement program, the following data was collected

for the current and preceding year:

Preceding Year

Operating costs

$2,500,000

Cost reduction, contaminants (ongoing)

187,500

Designing products

10,000

Auditing environmental risks

12,500

Recycling scrap

62,500

Recycling income

125,000

Restoring land to natural state

75,000

Operating pollution control equipment

62,500

Packaging cost reductions ( current year)

150,000

Testing for contamination

100,000

Required:

a.

Prepare an environmental financial statement for the year.

Environmental Benefits:

Income Sources:

Recycling income

$125,000

Ongoing Savings:

Cost reduction, contaminants (ongoing)

187,500

Current Savings

Packaging cost reductions ( current year)

150,000

Environmental Costs:

Prevention costs

$12,500

Designing products

10,000

Detection costs

Testing for contamination

100,000

Internal failure costs

Operating pollution control equipment

62,500

Recycling scrap

62,500

External failure costs

Restoring land to natural state

75,000

Total environmental costs

$322,500

201. Maldovar Chemical produces a number of chemical products, two of which are Product A and Product B.

The controller and environmental manager have identified the following environmental activities and costs

associated with the two products:

Product A

Product B

Pounds produced

1,000,000

2,500,000

Packaging materials (pounds)

300,000

150,000

Energy usage (kilowatt hours)

100,000

50,000

Toxic releases (pounds into air)

250,000

50,000

Pollution control (machine hours)

40,000

10,000

Costs of activities:

Using packaging materials

$450,000

Using energy

120,000

Releasing toxins (fines)

60,000

Operating pollution control equipment

140,000

Required:

a.

Calculate the environmental cost per pound for each product.

b.

Which of the two appears to cause the most degradation to the environment?

a.

Using packaged materials: $450,000/450,000 = $1 per lb.

Using energy: $120,000/150,000 = $0.80 per kwh

Releasing toxins (fines): $60,000/300,000 = $0.20 per lb.

Operating pollution control equipment: $140,000/50,000 = $2.80 per MH

Product A

Product B

Packaging materials

$ 150,000

Energy usage

80,000

40,000

Toxic releases

50,000

10,000

Pollution control

112,000

28,000

Total costs

$ 542,000

$ 228,000

Units

1,000,000

2,500,000

Cost per unit

$ 0.542

$ 0.0912

b.

Product A

202. Growfast Fertilizer Company produces a number of chemical products, two of which are Product X and

Product Y. The controller and environmental manager have identified the following environmental activities

and costs associated with the two products:

Product X

Product Y

Gallons produced

312,500

781,250

Energy usage (kilowatt hours)

31,250

15,625

Pollution control (machine hours)

12,500

3,125

Toxic releases (pounds into air)

78,125

15,625

Packaging materials (pounds)

93,750

46,875

Costs of activities:

Using packaging materials

$281,250

Using energy

75,000

Releasing toxins (fines)

37,500

Operating pollution control equipment

87,500

Required:

a.

Calculate the environmental cost per pound for each product.

b.

Which of the two appears to cause the most degradation to the environment?

a.

Using packaged materials: $281,250/140,625 = $2.00 per lb.

Using energy: $75,000/46,875 = $1.60 per kwh

Releasing toxins (fines): $37,500/93,750 = $0.40 per lb.

Operating pollution control equipment: $87,500/15,625 = $5.60 per MH

Product X

Product Y

Packaging materials

$187,500

$ 93,750

Energy usage

50,000

25,000

Toxic releases

31,250

6,250

Pollution control

70,000

17,500

Total costs

$338,750

$142,500

Units

312,500

781,250

Cost per unit

$ 1.084

$ 0.1824

b.

Product X