20) Refer to Figure 13-4. At the profit-maximizing output level the firm will

A) earn a profit of $176.

B) break even.

C) earn a profit of $88.

D) earn a profit of $60.

21) Refer to Figure 13-4. Based on the diagram, one can conclude that

A) some existing firms will exit the market.

B) new firms will enter the market.

C) the industry is in long-run equilibrium.

D) firms achieve productive efficiency.

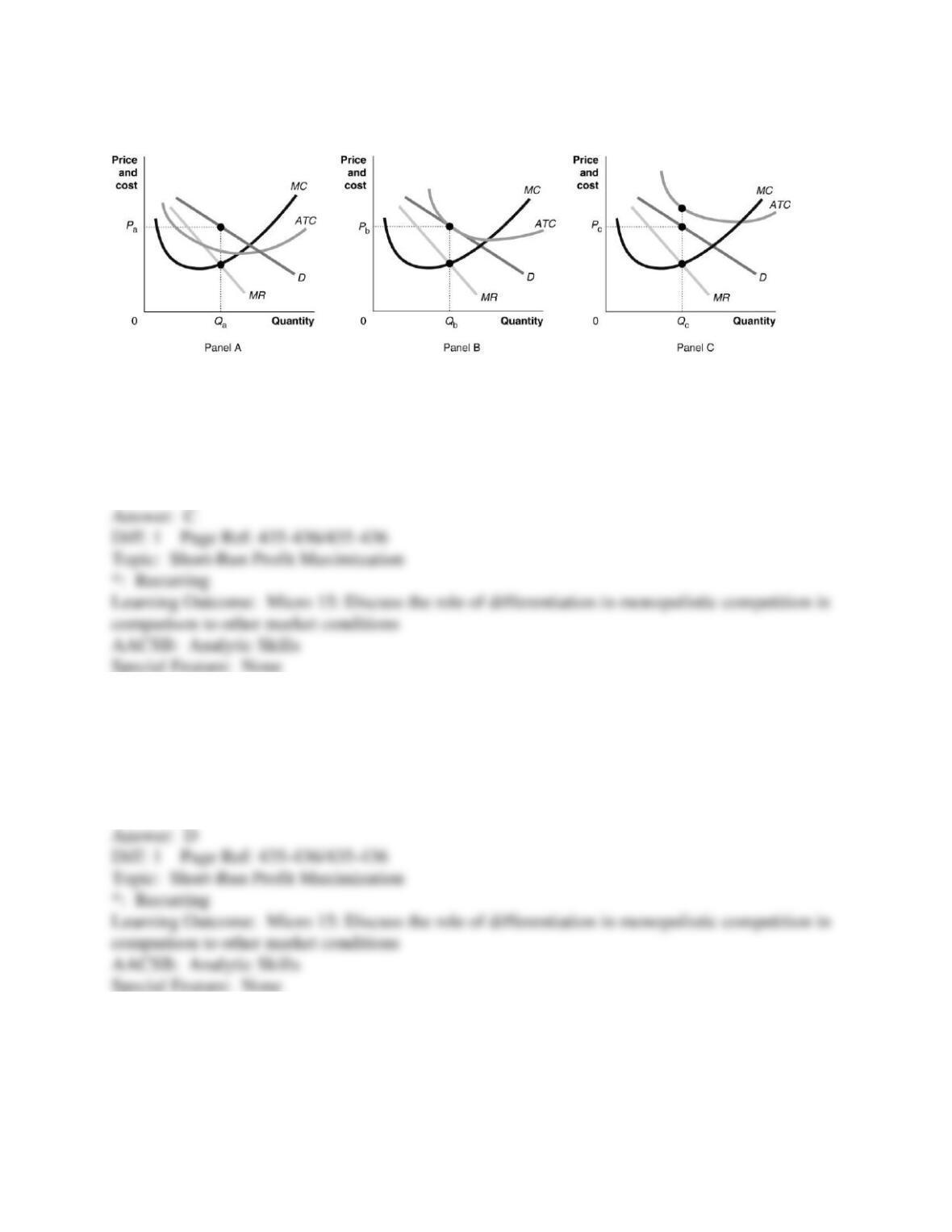

Figure 13-5

22) Refer to Figure 13-5. Which of the graphs in the figure depicts a monopolistically

competitive firm that is minimizing its losses?

A) Panel A

B) Panel B

C) Panel C

D) Panel A and Panel C

23) Refer to Figure 13-5. Which of the graphs in the figure depicts a monopolistically

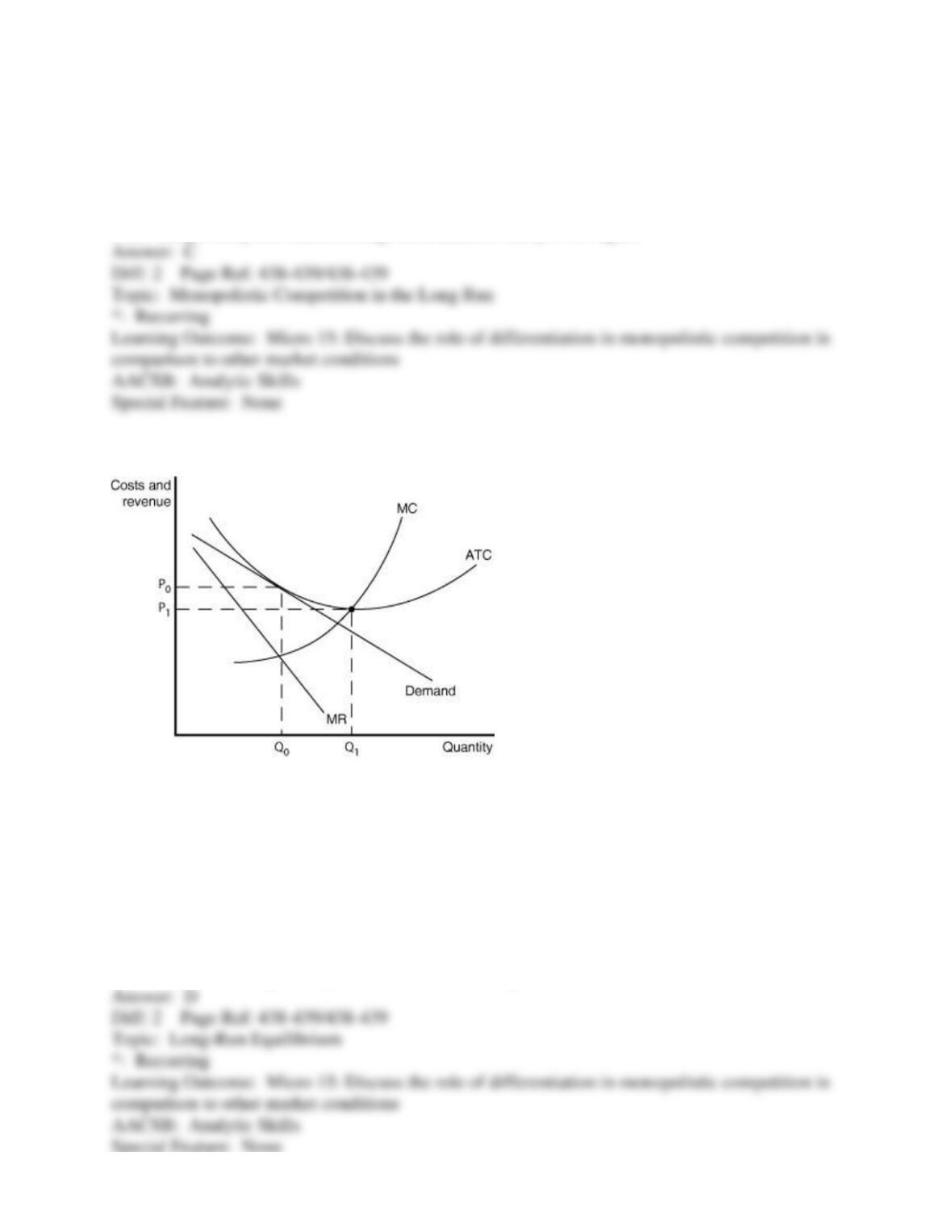

competitive firm that is earning economic profits?

A) Panel A

B) Panel B

C) Panel C

D) Panel A and Panel B

24) A monopolistically competitive firm should lower its price if its marginal revenue exceeds its

marginal cost.

25) If a perfectly competitive firm maximizes short-run profits, its marginal revenue will be

positive and less than its price.

26) A profit-maximizing monopolistically competitive firm produces and sells an allocatively

efficient quantity of output.

27) Unlike a perfectly competitive firm, a monopolistic competitor does not have a short-run

shut-down point.

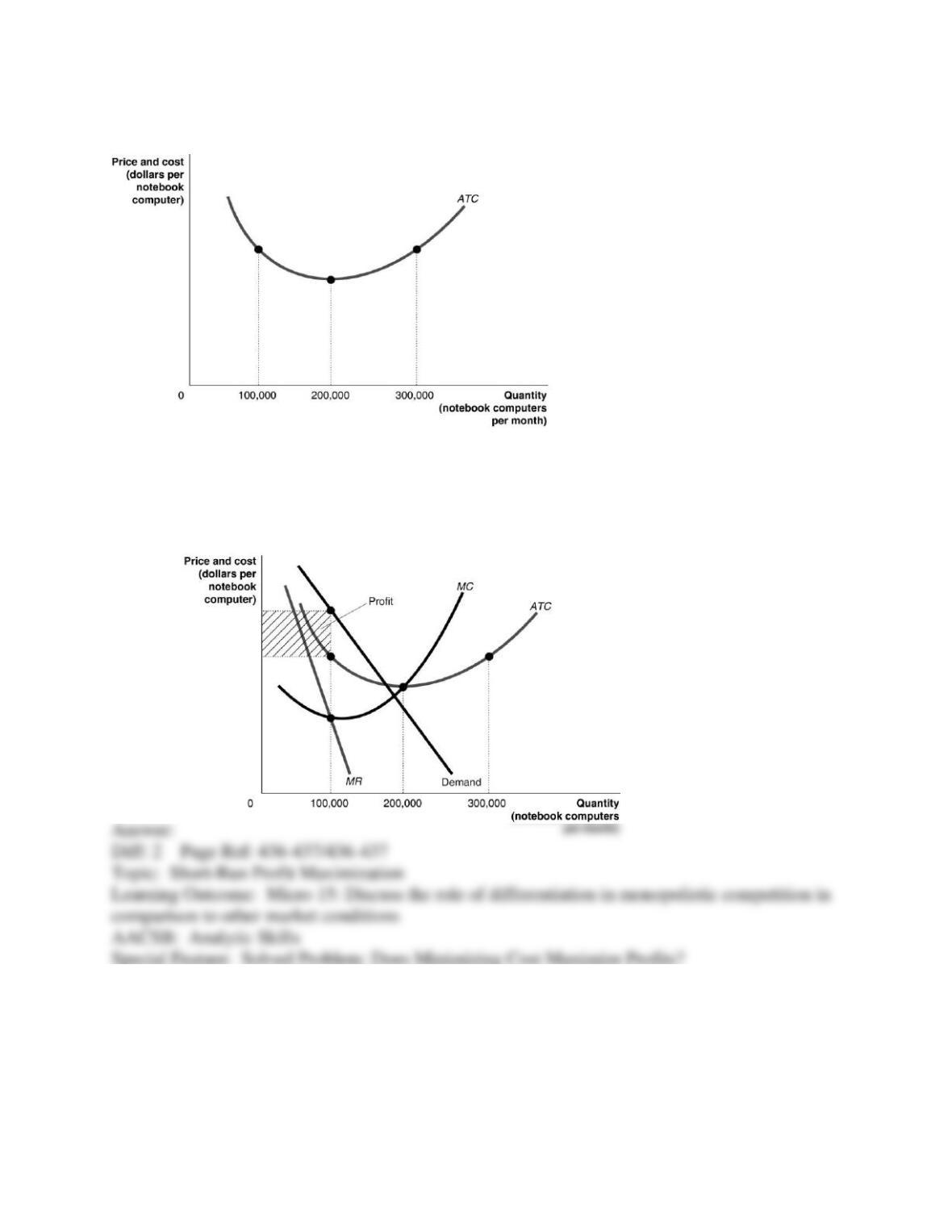

Figure 13-6

28) Refer to Figure 13-6. Suppose the above graph represents the relationship between the

average total cost of producing notebook computers and the quantity of notebook computers

produced by Dell. On a graph, illustrate the demand, MR, MC, and ATC curves which would

represent Dell maximizing profits at a quantity of 100,000 per month and identify the area on the

graph which represents the profit.

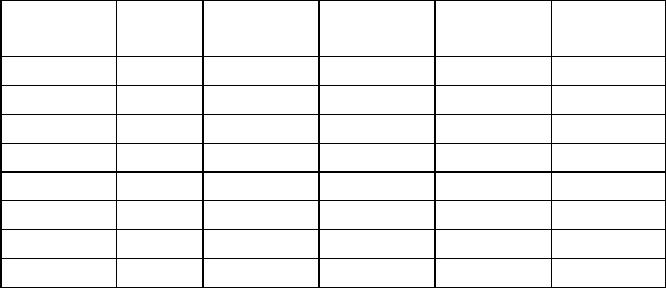

29) Central Grocery in New Orleans is famous for its muffaletta, a large round sandwich filled

with deli meats and topped with a tangy olive salad. Suppose the following table represents cost

and revenue data for Central Grocery. Fill in the columns for TR, MR, MC, ATC, and profit. If

Central Grocery wants to maximize profits, what price should it charge for a muffaletta, what

quantity should it sell, and what will be the amount of its total profit?

Muffaletta

s Sold per

Day

Price

(P)

Total

Revenue

(TR)

Marginal

Revenue

(MR)

Total

Cost

(TC)

Marginal

Cost (MC)

Average

Total

Cost

(ATC)

Profit

0

$15

$12

1

14

18

2

13

20

3

12

21

4

11

23

5

10

26

6

9

30

7

8

35

8

7

42

9

6

52

10

5

78

13.3 What Happens to Profits in the Long Run?

1) Tony’s Italian Ice is a monopolistically competitive firm. If Tony’s earns a profit in the short

run, which of the following is most likely to occur?

A) New firms that sell Italian ice will enter the market and Tony’s cost curves will shift to the

left.

B) New firms that sell Italian ice will enter the market and Tony’s demand curve will shift to the

left.

C) New firms that sell Italian ice will enter the market and Tony’s demand curve will shift to the

right.

D) New firms that sell Italian ice will enter the market and Tony’s demand curve will become

more inelastic.

2) Which of the following describes the relative positions of the demand curve and the average

total cost (ATC) curve of a monopolistically competitive firm that earns a profit in the short run?

A) In the short run, the firm’s demand curve will lie above its ATC curve. The demand curve will

be tangent to the ATC curve in the long run.

B) In the short run, the firm’s demand curve will lie below its ATC curve. The demand curve will

be tangent to the ATC curve in the long run.

C) In the short run, the firm’s demand curve will cross its ATC curve at the ATC curve’s lowest

point. The demand curve will be above the ATC curve in the long run.

D) In the short run, the firm’s ATC curve will cross the demand curve at the profit maximizing

level of output. The demand curve will be tangent to the ATC curve in the long run.

3) If firms in a monopolistically competitive industry are making profits in the short run,

A) barriers to entry will be erected to keep out rivals.

B) some firms will ultimately exit the industry.

C) they will resort to advertising wars to help sustain these profits.

D) new firms will enter the market.

4) A monopolistically competitive firm that earns an accounting profit in the short run

A) must also earn an economic profit in the short run.

B) does not earn enough to earn an economic profit in the short run.

C) could earn an economic profit, break even or suffer an economic loss in the short run.

D) could earn an economic profit or break even, but could not suffer an economic loss in the

short run.

5) In the long run, if the demand curve of a monopolistically competitive firm is tangent to its

average total cost curve then

A) the firm would break even.

B) the firm would shut down temporarily.

C) the firm would earn enough revenue to cover its variable costs, but not its fixed costs.

D) the firm would earn an economic profit.

6) Which of the following would not occur as a result of a monopolistically competitive firm

suffering a short-run economic loss?

A) The firm could exit the industry in the long run.

B) If the firm does not exit the industry in the long run its demand curve will shift to the left.

C) If the firm does not exit the industry in the long run its demand curve will shift to the right.

D) If the firm remains in the industry in the long run it will break even.

7) One reason Starbucks experienced a decline in sales in the late 2000s is because

A) the product they offered was becoming less differentiated from their competitors’ products.

B) the coffeehouse market transitioned from being monopolistically competitive to perfectly

competitive.

C) barriers to entry became more restrictive in the coffeehouse market.

D) the number of competitors in the market declined dramatically.

8) The entry and exit of firms in a monopolistically competitive market guarantee that

A) marginal revenue equals marginal cost and average total cost is minimized.

B) firms can earn economic profits in the long run.

C) price equals average total cost in the long run.

D) firms can earn economic profits in the short run.

9) When new firms are encouraged to enter a monopolistically competitive market

A) some existing firms must be earning economic profits.

B) they do so because there is insufficient product differentiation.

C) the demand curve facing an existing firm shifts to the right.

D) the marginal cost curve facing an existing firm shifts downwards.

10) If firms in a monopolistically competitive market are earning economic profits, which of the

following scenarios best reflects the change a representative firm experiences as the market

adjusts to its long-run equilibrium?

A) Demand decreases and becomes less elastic.

B) Demand decreases and becomes more elastic.

C) Demand increases and becomes less elastic.

D) Demand increases and becomes more elastic.

11) Long-run equilibrium under monopolistic competition and perfect competition is similar in

that

A) firms produce at the minimum point of their average cost curves.

B) price equals marginal cost.

C) firms break even.

D) price equals marginal revenue.

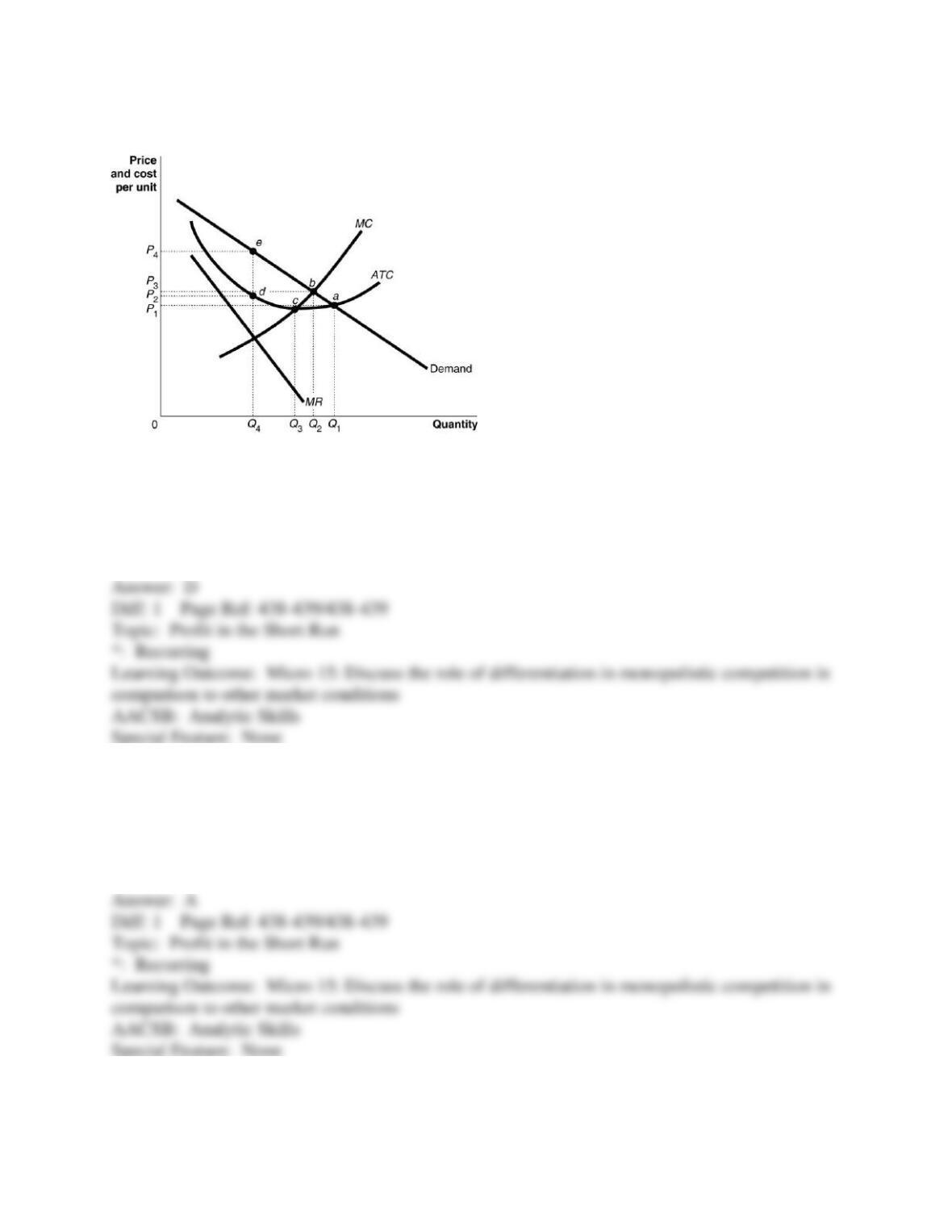

Figure 13-7

12) Refer to Figure 13-7. What is the profit maximizing output level?

A) Q1 units

B) Q2 units

C) Q3 units

D) Q4 units

13) Refer to Figure 13-7. What is the output price?

A) P4

B) P3

C) P2

D) P1

14) Refer to Figure 13-7. What is the area that represents the firm’s profit?

A) profit = 0

B) P4edP2

C) P4eaP1

D) P3baP2

15) Refer to Figure 13-7. Economies of scale are exhausted at which output level?

A) Q1 units

B) Q2 units

C) Q3 units

D) more than Q1 units

16) Refer to Figure 13-7. If the diagram represents a typical firm in the market, what is likely to

happen in the long run?

A) Some firms will exit the market causing the demand to increase for firms remaining in the

market.

B) New firms will enter the market causing the demand to decrease for existing firms.

C) Inefficient firms will exit the market and new cost-efficient firms will enter the market.

D) Competition will be intensified as firms strive to make long-run profits.

17) Refer to Figure 13-7. If the diagram represents a typical firm in the market, what is likely to

happen to its average cost of production in the long run?

A) It will probably fall since the firm must be cost efficient to remain competitive.

B) It will probably fall since the firm will be selling less than its current amount.

C) It will probably rise since the firm will be producing less than its current amount.

D) It will probably rise since its long-run demand is likely to be higher.

Figure 13-8

Figure 13-8 illustrates a monopolistically competitive firm.

18) Refer to Figure 13-8. Which of the following statements describes the firm depicted in the

diagram?

A) The firm is making no economic profit and will exit the industry.

B) The firm is suffering an economic loss by producing at Q0 but will break even it increases its

output to Q1.

C) The firm achieves productive efficiency by producing at Q0.

D) The firm is in long-run equilibrium and is breaking even.

19) Refer to Figure 13-8. It is possible to lower the average cost of production by expanding

output beyond Q0 to Q1. Why wouldn’t a firm expand its output to Q1?

A) The firm wants to maximize accounting profit rather than economic profit.

B) The firm would suffer an economic loss at Q1 while it would break even at Q0.

C) The firm’s marginal revenue would be negative at Q1.

D) Demand is not sufficient for consumers to buy Q1.

20) Which of the following is true for a monopolistically competitive firm in long-run

equilibrium?

A) P = ATC and MR = MC.

B) P = ATC and P = MC.

C) P > ATC and P > MR.

D) P > MR and MC = ATC.

21) Which of the following will not happen as a consequence of a monopolistically competitive

firm suffering economic losses in the short run?

A) The firm’s demand curve will shift to the right if it stays in business in the long run.

B) The firm will exit the industry if it continues to suffer economic losses.

C) The firm will break even if its stays in business in the long run.

D) In the long run the firm will be able to charge a price that is greater than its average total cost.

22) If a store like hhgregg has higher costs than a comparable Best Buy store, the only way it can

have higher profits is if

A) it has more locations than Best Buy.

B) its marginal revenue is lower than Best Buy’s.

C) the demand for its goods is higher than Best Buy’s.

D) it sells the quantity associated with its minimum average total cost.

23) A monopolistically competitive firm that is profitable in the short run will face competition

that will eventually eliminate the firm’s profits in the long run. But the firm can stave off

competition and continue to earn economic profits if

A) it can successfully sue its competitors for copyright infringement.

B) it can move to another country where there is less competition.

C) it can lobby the government to establish a price floor for its product.

D) it can find new ways to differentiate its product.

24) The economic analysis of monopolistic competition shows that market forces eliminate

profits in the long run. However, it is possible for a firm to continue to earn economic profits if

the firm

A) expands its marketing budget.

B) adopts new technologies that enable it to lower its cost of production.

C) expands its product offerings to appeal to a wider range of consumers.

D) reduces its price to expand its market.

25) Despite being in a market with ________, from the mid-1990s to the mid-2000s Starbucks

was able to significantly differentiate its products from the products of its competitors.

A) few barriers to entry

B) significant barriers to entry

C) blocked entry

D) no barriers to entry

26) When a monopolistically competitive firm breaks even in the long run, this is equivalent to

earning a zero accounting profit.

27) A monopolistically competitive firm can increase its profits beyond the long-run equilibrium

break-even level by deliberately lowering its price to force some of its competitors out of the

market.

28) If some monopolistically competitive firms exit their market after suffering short-run losses,

the demand curves of remaining firms will shift to the right.

29) What effect does the entry of new firms in a monopolistically competitive market have on

the economic profits of existing firms in the market? How might existing firms attempt to

counteract this effect?

30) Sparkle, one of many firms in the market for toothpaste, is in long-run equilibrium. Sparkle

has a small market share and has been in business for a long time.

a. Identify the market structure in which Sparkle operates. Explain your answer.

b. What is Sparkle’s profit or loss? Explain your answer. If you cannot determine the profit or

loss, explain what information is missing.

c. Draw a diagram showing Sparkle’s demand curve, marginal revenue curve, average total cost

curve and marginal cost curve. Label your diagram.

31) The table below shows the demand and cost data facing “Velvet Touches,” a

monopolistically competitive producer of velvet throw pillows.

Quantity

Price

Total

Revenue

Marginal

Revenue

Total Cost

Marginal

Cost

1

$30

$32

2

28

43

3

26

53

4

24

64

5

22

76

6

20

90

7

18

106

8

16

126

Use the data to answer the following questions.

a. Complete the Total Revenue (TR), Marginal Revenue (MR) and Marginal Cost (MC) columns

above.

b. What are the profit-maximizing price and quantity for Velvet Touches?

c. Is the firm making a profit or a loss? How much is the profit or loss? Show your work.

d. Is this firm operating in the long run or in the short run? Explain your answer.

e. If the firm’s profit or loss is typical of all firms in the market for throw pillows, what is likely

to happen in the future? Will there be more firms or will some existing firms leave the industry?

Explain your answer.

f. What will happen to the typical firm’s profit or loss after all entry/exit adjustments?

13.4 Comparing Monopolistic Competition and Perfect Competition

1) In both monopolistically competitive and perfectly competitive industries

A) firms produce products for which there are no close substitutes.

B) there are high barriers to entry.

C) there are many buyers and sellers.

D) firms are price takers.

2) In the long run firms in both monopolistically competitive markets and perfectly competitive

markets earn zero economic profits, but unlike perfectly competitive firms in the long run,

monopolistically competitive firms

A) charge a price that is greater than average revenue.

B) charge a price that is equal to marginal cost.

C) do not produce at minimum average total cost.

D) charge a price that is equal to average total cost.

3) Compared to a perfectly competitive firm, the demand curve facing a monopolistically

competitive firm is

A) more elastic because there are many close substitutes for the product of a monopolistically

competitive firm.

B) less elastic because monopolistically competitive firms produce similar, but not identical,

products.

C) just as elastic because there are many sellers in both markets.

D) more elastic because in the long run, the demand curve is tangent to the firm’s average total

cost curve.