CHAPTER 13

STATEMENT OF CASH FLOWS

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

True-False Statements

1.

1

K

9.

2

K

17.

2

C

a25.

5

K

sg33.

2

K

2.

1

K

10.

2

K

18.

3

C

a26.

5

C

sg34.

3

C

3.

1

K

11.

2

C

19.

3

C

a27.

5

K

a,sg35.

5

K

4.

1

K

12.

2

C

20.

3

C

a28.

5

K

a,sg36.

6

K

5.

1

K

13.

2

C

21.

3

C

a29.

6

C

6.

1

C

14.

2

C

22.

3

C

a30.

7

K

7.

1

C

15.

2

C

23.

4

K

a31.

7

K

8.

2

K

16.

2

C

24.

4

K

sg32.

2

K

Multiple Choice Questions

37.

1

K

62.

2

K

87.

3

K

112.

3,5

C

a137.

5

AP

38.

1

K

63.

2

K

88.

3

C

113.

3,5

C

a138.

5

C

39.

1

C

64.

2

K

89.

3

C

114.

3,5

C

a139.

5

AP

40.

1

C

65.

2

AP

90.

3

K

115.

3,5

C

a140.

5

AP

41.

1

C

66.

2

AP

91.

3

K

116.

3,5

C

a141.

5

C

42.

1

K

67.

2

AP

92.

3

C

117.

3,5

C

a142.

6

C

43.

1

K

68.

2

AP

93.

3

C

118.

3,5

C

a143.

6

C

44.

1

C

69.

2

AP

94.

3

C

119.

4

K

a144.

6

C

45.

1

K

70.

3

AP

95.

3

C

120.

4

C

a145.

6

C

46.

2

K

71.

3

AP

96.

3

C

121.

4

AP

sg146.

2

K

47.

2

K

72.

3

AP

97.

3

C

122.

4

AN

sg147.

2

K

48.

2

C

73.

3

AP

98.

3

C

123.

4

C

st148.

2

K

49.

2

K

74.

3

AP

99.

3

C

a124.

5

AP

sg149.

2

K

50.

2

C

75.

3

AP

100.

3

AP

a125.

5

AP

sg150.

1

C

51.

2

C

76.

3

K

101.

3

C

a126.

5

AP

sg151.

3

K

52.

2

C

77.

3

K

102.

3

C

a127.

5

AP

sg152.

3,5

AP

53.

2

C

78.

3

AP

103.

3

K

a128.

5

AP

a,sg153.

5

AP

54.

2

C

79.

3

K

104.

3

AP

a129.

5

C

a,sg154.

5

AP

55.

2

K

80.

3

C

105.

3

AP

a130.

5

K

a.sg155.

8

K

56.

2

C

81.

3

C

106.

3

AP

a131.

5

AP

156.

8

K

57.

2

K

82.

3

C

107.

3

AP

a132.

5

AP

157.

8

K

58.

2

C

83.

3

C

108.

3

AP

a133.

5

AP

158.

8

K

59.

2

C

84.

3

C

109.

3

AP

a134.

5

AP

159.

8

K

60.

2

C

85.

3

AP

110.

3,5

AP

a135.

5

AP

160.

8

K

61.

2

K

86.

3

AP

111.

3,5

C

a136.

5

AP

Brief Exercises

161.

2

C

163.

3

AP

165.

3

K

167.

3

AP

a169.

5

AP

162.

3

AP

164.

3

AP

166.

3

K

168.

4

AP

a170.

5

AP

sg This question also appears in the Study Guide.

st This question also appears in a self-test at the student companion website.

a This topic is dealt with in an Appendix to the chapter.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 2

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Exercises

171.

2

C

177.

3

C

183.

3

AP

a189.

5

AP

a195.

5

AP

172.

2

C

178.

3,4

AP

184.

3

AN

a190.

5

AP

a196.

5

AP

173.

2

C

179.

3

AP

185.

3,4

AP

a191.

5

AP

174.

2

AP

180.

3

AP

186.

3,4

AP

a192.

5

AP

175.

3

AP

181.

3

AP

187.

4

AP

a193.

5

AP

176.

3

AP

182.

3

AP

a188.

6

AP

a194.

5

AP

Completion Statements

197.

2

K

200.

3

K

203.

3

K

a206.

5

K

a209.

5

K

198.

2

K

201.

3

K

204.

4

K

a207.

5

AN

199.

3

K

202.

3

K

a205.

5

K

a208.

5

K

Matching Statements

210.

3

K

211.

5

K

Short-Answer Essay

212.

2

K

214.

1

K

216.

1

K

218.

1

K

213.

1

K

215.

1

K

217.

1

K

sg This question also appears in the Study Guide.

st This question also appears in a self-test at the student companion website.

a This topic is dealt with in an Appendix to the chapter.

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

5.

TF

38.

MC

42.

MC

46.

MC

215.

SA

2.

TF

6.

TF

39.

MC

43.

MC

150.

MC

216.

SA

3.

TF

7.

TF

40.

MC

44.

MC

213.

SA

217.

SA

4.

TF

37.

MC

41.

MC

45.

MC

214.

SA

218.

SA

Learning Objective 2

8.

TF

16.

TF

49.

MC

57.

MC

65.

MC

149.

MC

212.

SA

9.

TF

17.

TF

50.

MC

58.

MC

66.

MC

161.

BE

10.

TF

31.

TF

51.

MC

59.

MC

67.

MC

171.

Ex

11.

TF

32.

TF

52.

MC

60.

MC

68.

MC

172.

Ex

12.

TF

33.

TF

53.

MC

61.

MC

69.

MC

173.

Ex

13.

TF

46.

MC

54.

MC

62.

MC

146.

MC

174.

Ex

14.

TF

47.

MC

55.

MC

63.

MC

147.

MC

197.

C

15.

TF

48.

MC

56.

MC

64.

MC

148.

MC

198.

C

Learning Objective 3

18.

TF

22.

TF

72.

MC

76.

MC

80.

MC

84.

MC

88.

MC

19.

TF

34.

TF

73.

MC

77.

MC

81.

MC

85.

MC

89.

MC

20.

TF

70.

MC

74.

MC

78.

MC

82.

MC

86.

MC

90.

MC

21.

TF

71.

MC

75.

MC

79.

MC

83.

MC

87.

MC

91.

MC

Continued on the next page.

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 3

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Learning Objective 3 (Cont.)

92.

MC

100.

MC

108.

MC

116.

MC

165.

BE

180.

Ex

200.

C

93.

MC

101.

MC

109.

MC

117.

MC

166.

BE

181.

Ex

201.

C

94.

MC

102.

MC

110.

MC

118.

MC

167.

BE

182.

Ex

202.

C

95.

MC

103.

MC

111.

MC

151.

MC

175.

Ex

183.

Ex

203.

C

96.

MC

104.

MC

112.

MC

152.

MC

176.

Ex

184.

Ex

210.

SA

97.

MC

105.

MC

113.

MC

162.

BE

177.

Ex

185.

Ex

98.

MC

106.

MC

114.

MC

163.

BE

178.

Ex

186.

Ex

99.

MC

107.

MC

115.

MC

164.

BE

179.

Ex

199.

C

Learning Objective 4

23.

TF

119.

MC

121.

MC

123.

MC

178.

Ex

186.

Ex

204.

C

24.

TF

120.

MC

122.

MC

168.

BE

185.

Ex

187.

Ex

Learning Objective a5

a25.

TF

a113.

MC

a126.

MC

a134.

MC

a152.

MC

a192.

Ex

a208.

C

a26.

TF

a114.

MC

a127.

MC

a135.

MC

a153.

MC

a193.

Ex

a209.

C

a27.

TF

a115.

MC

a128.

MC

a136.

MC

a154.

MC

a194.

Ex

a28.

TF

a116.

MC

a129.

MC

a137.

MC

a169.

BE

a195.

Ex

a35.

TF

a117.

MC

a130.

MC

a138.

MC

a170.

BE

a196.

Ex

a110.

MC

a118.

MC

a131.

MC

a139.

MC

a189.

Ex

a205.

C

a111.

MC

a124.

MC

a132.

MC

a140.

MC

a190.

Ex

a206.

C

a112.

MC

a125.

MC

a133.

MC

a141.

MC

a191.

Ex

a207.

C

Learning Objective a6

a29.

TF

a142.

MC

a143.

MC

a144.

MC

a145.

MC

a155.

MC

a188.

Ex

a36.

TF

Learning Objective a7

a30.

F

a31.

T

Learning Objective a8

a156.

MC

a157.

MC

a158.

MC

a159.

MC

a160.

MC

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise

CHAPTER LEARNING OBJECTIVES

1. Indicate the usefulness of the statement of cash flows. The statement of cash flows

provides information about the cash receipts, cash payments, and net change in cash

resulting from the operating, investing, and financing activities of a company during the

period.

2. Distinguish among operating, investing, and financing activities. Operating activities

include the cash effects of transactions that enter into the determination of net income.

Investing activities involve cash flows resulting from changes in investments and long-term

asset items. Financing activities involve cash flows resulting from changes in long-term

liability and stockholders’ equity items.

3. Prepare a statement of cash flows using the indirect method. The preparation of a

statement of cash flows involves three major steps: (1) Determine net cash provided/used by

operating activities by converting net income from an accrual basis to a cash basis. (2)

Test Bank for Financial Accounting, Ninth Edition

13 – 4

Analyze changes in noncurrent asset and liability accounts and record as investing and

financing activities, or disclose as noncash transactions. (3) Compare the net change in cash

on the statement of cash flows with the change in the Cash account reported on the balance

sheet to make sure the amounts agree.

4. Analyze the statement of cash flows. Free cash flow indicates the amount of cash a

company generated during the current year that is available for the payment of additional

dividends or for expansion.

a5. Prepare a statement of cash flows using the direct method. The preparation of the

statement of cash flows involves three major steps. (1) Determine net cash provided/used by

operating activities by converting net income from an accrual basis to a cash basis. (2)

Analyze changes in noncurrent asset and liability accounts and record as investing and

financing activities, or disclose as noncash transactions. (3) Compare the net change in cash

on the statement of cash flows with the change in the Cash account reported on the balance

sheet to make sure the amounts agree. The direct method reports cash receipts less cash

payments to arrive at net cash provided by operating activities.

a6. Explain how to use a worksheet to prepare the statement of cash flows using the

indirect method. When there are numerous adjustments, a worksheet can be a helpful tool

in preparing the statement of cash flows. Key guidelines for using a worksheet are as follows

(1) List accounts with debit balances separately from those with credit balances. (2) In the

reconciling columns in the bottom portion of the worksheet, show cash inflows as debits and

cash outflows as credits. (3) Do not enter reconciling items in any journal or account, but use

them only to help prepare the statement of cash flows.

The steps in preparing the worksheet are as follows (1) Enter beginning and ending balances

of balance sheet accounts. (2) Enter debits and credits in reconciling columns. (3) Enter the

increase or decrease in cash in two places as a balancing amount.

a7. Use the T-account approach to prepare a statement of cash flows. To use T-accounts to

prepare the statement of cash flows: (1) prepare a large Cash T-account with sections for

operating, investing, and financing activities; (2) prepare smaller T-accounts for all other

noncash accounts; (3) insert beginning and ending balances for all accounts; and (4) follow

the steps in illustration 13-3 (page 654), entering debit and credit amounts as needed.

TRUE-FALSE STATEMENTS

1. The statement of cash flows is a required statement that must be prepared along with an

income statement, balance sheet, and retained earnings statement.

2. For external reporting, a company must prepare either an income statement or a

statement of cash flows, but not both.

3. A primary objective of the statement of cash flows is to show the income or loss on

investing and financing transactions.

Statement of Cash Flows

13 – 5

4. A statement of cash flows indicates the sources and uses of cash during a period.

5. A statement of cash flows should help investors and creditors assess the entity’s ability to

generate future income.

6. The information in a statement of cash flows helps investors and creditors assess the

company’s ability to pay dividends and meet obligations.

7. Financial statement readers can determine future investing and financing transactions by

examining a company’s statement of cash flows.

8. In preparing a statement of cash flows, the issuance of debt should be reported separately

from the retirement of debt.

9. Noncash investing and financing activities must be reported in the body of a statement of

cash flows.

10. The statement of cash flows classifies cash receipts and payments as operating,

nonoperating, financial, and extraordinary activities.

11. The sale of land for cash would be classified as a cash inflow from an investing activity.

12. Cash flow from investing activities is considered the most important category on the

statement of cash flows because it is considered the best measure of expected income.

13. The receipt of dividends from long-term investments in stock is classified as a cash inflow

from investing activities.

14. The payment of interest on bonds payable is classified as a cash outflow from operating

activities.

15. Any item that appears on the income statement would be considered as either a cash

inflow or cash outflow from operating activities.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 6

16. The acquisition of a building by issuing bonds would be considered an investing and

financing activity that did not affect cash.

17. All major financing and investing activities affect cash.

18. Cash provided by operations is generally equal to operating income.

19. Using the indirect method, an increase in accounts receivable during a period is deducted

from net income in calculating cash provided by operations.

20. Using the indirect method, an increase in accounts payable during a period is deducted

from net income in calculating cash provided by operations.

21. A loss on sale of equipment is added to net income in determining cash provided by

operations under the indirect method.

22. In preparing a statement of cash flows, an increase in the Common Stock and Treasury

Stock accounts during a period would be an investing activity.

23. Cash provided by operating activities fails to take into account that a company must invest

in new fixed assets just to maintain its current level of operations.

24. Free cash flow equals cash provided by operations less capital expenditures and cash

dividends.

a25. Operating expenses + an increase in prepaid expenses – a decrease in accrued

expenses payable = cash payments for operating expenses.

a26. During the year, Income Tax Expense amounted to $30,000 and Income Taxes Payable

increased by $4,000; therefore, the cash paid for income taxes was $26,000.

a27. In preparing net cash flow from operating activities using the direct method, each item in

the income statement is adjusted from the accrual basis to the cash basis.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 7

a28. During a period, cost of goods sold + an increase in inventory + an increase in accounts

payable = cash paid to suppliers.

a29. The use of a worksheet to prepare a statement of cash flows is optional.

FSA

a30. The change in cash is equal to the change in liabilities less the change in equity plus the

change in noncash assets.

a31. Analysis of the changes in all of the noncash balance sheet accounts will explain the

change in the Cash account.

32. The statement of cash flows classifies cash receipts and cash payments into two

categories: operating activities and nonoperating activities.

33. Financing activities include the obtaining of cash from issuing debt and repaying the

amounts borrowed.

34. Under the indirect method, retained earnings is adjusted for items that affected reported

net income but did not affect cash.

a35. Under the direct method, the formula for computing cash collections from customers is

sales revenues plus the increase in accounts receivable or minus the decrease in

accounts receivable.

a36. The reconciling entry for depreciation expense in a worksheet is a credit to Accumulated

Depreciation and a debit to Operating-Depreciation Expense.

Answers to True-False Statements

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Test Bank for Financial Accounting, Ninth Edition

13 – 8

MULTIPLE CHOICE QUESTIONS

37. The statement of cash flows should help investors and creditors assess each of the

following except the

a. entity’s ability to generate future income.

b. entity’s ability to pay dividends.

c. reasons for the difference between net income and net cash provided by operating

activities.

d. cash investing and financing transactions during the period.

38. The statement of cash flows

a. must be prepared on a daily basis.

b. summarizes the operating, financing, and investing activities of an entity.

c. is another name for the income statement.

d. is a special section of the income statement.

39. Which one of the following items is not generally used in preparing a statement of cash

flows?

a. Adjusted trial balance

b. Comparative balance sheets

c. Current income statement

d. Additional information

40. The primary purpose of the statement of cash flows is to

a. provide information about the investing and financing activities during a period.

b. prove that revenues exceed expenses if there is a net income.

c. provide information about the cash receipts and cash payments during a period.

d. facilitate banking relationships.

41. If a company reports a net loss, it

a. may still have a net increase in cash.

b. will not be able to pay cash dividends.

c. will not be able to get a loan.

d. will not be able to make capital expenditures.

42. In addition to the three basic financial statements, which of the following is also a required

financial statement?

a. the “Cash Budget”

b. the Statement of Cash Flows

c. the Statement of Cash Inflows and Outflows

d. the “Cash Reconciliation”

Statement of Cash Flows

13 – 9

43. The statement of cash flows will not report the

a. amount of checks outstanding at the end of the period.

b. sources of cash in the current period.

c. uses of cash in the current period.

d. change in the cash balance for the current period.

44. The statement of cash flows reports each of the following except

a. cash receipts from operating activities.

b. cash payments from investing activities.

c. the net change in cash.

d. cash sales.

45. Each of the following are particularly interested in the statement of cash flows except

a. creditors.

b. employees.

c. shareholders.

d. government agencies.

46. Lending money and collecting the loans are

a. operating activities.

b. investing activities.

c. financing activities.

d. Non-cash investing and financing activities.

47. The cash effects of transactions that create revenues and expenses are

a. financing activities.

b. investing activities.

c. operating activities.

d. processing activities.

48. The acquisition of land by issuing common stock is

a. a noncash transaction which is not reported in the body of a statement of cash flows.

b. a cash transaction and would be reported in the body of a statement of cash flows.

c. a noncash transaction and would be reported in the body of a statement of cash flows.

d. only reported if the statement of cash flows is prepared using the direct method.

49. The order of presentation of activities on the statement of cash flows is

a. operating, investing, and financing.

b. operating, financing, and investing.

c. financing, operating, and investing.

d. financing, investing, and operating.

Test Bank for Financial Accounting, Ninth Edition

13 – 10

50. Financing activities involve

a. lending money.

b. acquiring investments.

c. issuing debt.

d. acquiring long-lived assets.

51. Investing activities include

a. collecting cash on loans made.

b. obtaining cash from creditors.

c. obtaining capital from owners.

d. repaying money previously borrowed.

52. Generally, the most important category on the statement of cash flows is cash flows from

a. operating activities.

b. investing activities.

c. financing activities.

d. significant noncash activities.

53. The category that is generally considered to be the best measure of a company’s ability to

continue as a going concern is

a. cash flows from operating activities.

b. cash flows from investing activities.

c. cash flows from financing activities.

d. usually different from year to year.

54. Cash receipts from interest and dividends are classified as

a. financing activities.

b. investing activities.

c. operating activities.

d. either financing or investing activities.

55. Each of the following is an example of a significant noncash activity except

a. conversion of bonds into common stock.

b. exchanges of plant assets.

c. issuance of debt to purchase assets.

d. stock dividends.

56. If a company has both an inflow and outflow of cash related to property, plant, and

equipment, the

a. two cash effects can be netted and presented as one item in the investing activities

section.

b. cash inflow and cash outflow should be reported separately in the investing activities

section.

c. two cash effects can be netted and presented as one item in the financing activities

section.

d. cash inflow and cash outflow should be reported separately in the financing activities

section.

Statement of Cash Flows

13 – 11

57. Of the items below, the one that appears first on the statement of cash flows is

a. noncash investing and financing activities.

b. net increase (decrease) in cash.

c. cash at the end of the period.

d. cash at the beginning of the period.

58. Which of the following transactions does not affect cash during a period?

a. Write-off of an uncollectible account

b. Collection of an accounts receivable

c. Sale of treasury stock

d. Exercise of the call option on bonds payable

59. Significant noncash transactions would not include

a. conversion of bonds into common stock.

b. asset acquisition through bond issuance.

c. treasury stock acquisition.

d. exchange of plant assets.

60. In preparing a statement of cash flows, a conversion of bonds into common stock will be

reported in

a. the financing section.

b. the “extraordinary” section.

c. a separate schedule or note to the financial statements.

d. the stockholders’ equity section.

61. Indicate where the payment of income taxes would appear, if at all, on the statement of

cash flows.

a. Operating activities section

b. Investing activities section

c. Financing activities section

d. Does not represent a cash flow

62. Indicate where the issuance of common stock issued for cash would appear, if at all, on

the indirect statement of cash flows.

a. Operating activities section

b. Investing activities section

c. Financing activities section

d. Does not represent a cash flow

63. Indicate where the purchase of land for cash would appear, if at all, on the indirect

statement of cash flows.

a. Operating activities section

b. Investing activities section

c. Financing activities section

d. Does not represent a cash flow

Test Bank for Financial Accounting, Ninth Edition

13 – 12

64. Indicate where the event purchase of land and a building with a mortgage would appear, if

at all, on the indirect statement of cash flows.

a. Operating activities section

b. Investing activities section

c. Financing activities section

d. Does not represent a cash flow

65. Jean’s Vegetable Market had the following transactions during 2014:

1. Issued $50,000 of par value common stock for cash.

2. Repaid a 6 year note payable in the amount of $22,000.

3. Acquired land by issuing common stock of par value $50,000.

4. Declared and paid a cash dividend of $7,000.

5. Sold a long-term investment (cost $3,000) for cash of $6,000.

6. Acquired an investment in IBM stock for cash of $10,000.

What is the net cash provided by financing activities?

a. $21,000

b. $67,000

c. $28,000

d. $0

66. Jean’s Vegetable Market had the following transactions during 2014:

1. Issued $50,000 of par value common stock for cash.

2. Repaid a 6 year note payable in the amount of $22,000.

3. Acquired land by issuing common stock of par value $100,000.

4. Declared and paid a cash dividend of $2,000.

5. Sold a long-term investment (cost $3,000) for cash of $8,000.

6. Acquired an investment in IBM stock for cash of $15,000.

What is the net cash provided (used) by investing activities?

a. $15,000

b. $33,000

c. ($7,000)

d. $8,000

67. Vision Company purchased treasury stock with a cost of $16,000 during 2014. During the

year, the company paid dividends of $20,000 and issued bonds payable for proceeds of

$860,000. Cash flows from financing activities for 2014 total

a. $840,000 net cash inflow.

b. $856,000 net cash inflow.

c. $860,000 net cash outflow.

d. $824,000 net cash inflow.

Statement of Cash Flows

13 – 13

68. Kanet Company issued common stock for proceeds of $386,000 during 2014. The

company paid dividends of $80,000 and issued a long-term note payable for $95,000 in

exchange for equipment during the year. The company also purchased treasury stock that

had a cost of $15,000. The financing section of the statement of cash flows will report net

cash inflows of

a. $291,000.

b. $481,000.

c. $306,000.

d. $371,000.

69. In Jude Company, land decreased $150,000 because of a cash sale for $150,000, the

equipment account increased $60,000 as a result of a cash purchase, and Bonds Payable

increased $120,000 from issuance for cash at face value. The net cash provided by

investing activities is

a. $150,000.

b. $210,000.

c. $90,000.

d. $270,000.

70. Accounts receivable arising from sales to customers amounted to $86,000 and $77,000 at

the beginning and end of the year, respectively. Income reported on the income statement

for the year was $290,000. Exclusive of the effect of other adjustments, the cash flows

from operating activities to be reported on the statement of cash flows is

a. $290,000.

b. $299,000.

c. $213,000.

d. $280,000.

71. Accounts receivable arising from sales to customers amounted to $40,000 and $55,000 at

the beginning and end of the year, respectively. Income reported on the income statement

for the year was $180,000. Exclusive of the effect of other adjustments, the cash flows

from operating activities to be reported on the statement of cash flows is

a. $180,000.

b. $195,000.

c. $220,000.

d. $165,000.

Test Bank for Financial Accounting, Ninth Edition

13 – 14

72. Bush Company reported net income of $60,000 for the year. During the year, accounts

receivable decreased by $8,000, accounts payable increased by $4,000 and depreciation

expense of $5,000 was recorded. Net cash provided by operating activities for the year is

a. $48,000.

b. $77,000.

c. $59,000.

d. $55,000.

73. Adama Company reported a net loss of $6,000 for the year ended December 31, 2014.

During the year, accounts receivable increased $15,000, merchandise inventory

decreased $12,000, accounts payable decreased by $20,000, and depreciation expense

of $12,000 was recorded. During 2014, operating activities

a. used net cash of $17,000.

b. used net cash of $29,000.

c. provided net cash of $24,000.

d. provided net cash of $21,000.

74. The net income reported on the income statement for the current year was $220,000.

Depreciation recorded on plant assets was $35,000. Accounts receivable and inventories

increased by $2,000 and $8,000, respectively. Prepaid expenses and accounts payable

decreased by $2,000 and $12,000 respectively. How much cash was provided by

operating activities?

a. $200,000

b. $235,000

c. $220,000

d. $255,000

75. The net income reported on the income statement for the current year was $245,000.

Depreciation was $40,000. Account receivable and inventories decreased by $12,000 and

$35,000, respectively. Prepaid expenses and accounts payable increased, respectively,

by $1,000 and $8,000. How much cash was provided by operating activities?

a. $296,000

b. $339,000

c. $323,000

d. $311,000

Statement of Cash Flows

13 – 15

76. If a gain of $12,000 is incurred in selling (for cash) office equipment having a book value

of $110,000, the total amount reported in the cash flows from investing activities section of

the statement of cash flows is

a. $98,000.

b. $122,000.

c. $110,000.

d. $12,000.

77. If a loss of $25,000 is incurred in selling (for cash) office equipment having a book value of

$90,000, the total amount reported in the cash flows from investing activities section of the

statement of cash flows is

a. $65,000.

b. $90,000.

c. $115,000.

d. $25,000.

78. Wilson Company reported net income of $105,000 for the year ended December 31,

2014. During the year, inventories decreased by $15,000, accounts payable decreased

by $20,000, depreciation expense was $18,000 and a gain on disposal of equipment of

$9,000 was recorded. Net cash provided by operating activities in 2014 using the indirect

method was

a. $101,000.

b. $109,000.

c. $120,000.

d. $118,000.

79. The third (final) step in preparing the statement of cash flows is to

a. analyze changes in noncurrent asset and liability accounts.

b. compare the net change in cash with the change in the cash account reported on the

balance sheet.

c. determine net cash provided by operating activities.

d. list the noncash activities.

80. Which one of the following items is not necessary in preparing a statement of cash flows?

a. Determine the change in cash

b. Determine the cash provided by operations

c. Determine cash from financing and investing activities

d. Determine the cash in all bank accounts

Test Bank for Financial Accounting, Ninth Edition

13 – 16

81. If accounts receivable have increased during the period,

a. revenues on an accrual basis are less than revenues on a cash basis.

b. revenues on an accrual basis are greater than revenues on a cash basis.

c. revenues on an accrual basis are the same as revenues on a cash basis.

d. expenses on an accrual basis are greater than expenses on a cash basis.

82. If accounts payable have increased during a period,

a. revenues on an accrual basis are less than revenues on a cash basis.

b. expenses on an accrual basis are less than expenses on a cash basis.

c. expenses on an accrual basis are greater than expenses on a cash basis.

d. expenses on an accrual basis are the same as expenses on a cash basis.

83. Which one of the following affects cash during a period?

a. Recording depreciation expense

b. Declaration of a cash dividend

c. Write-off of an uncollectible account receivable

d. Payment of an accounts payable

84. In calculating cash flows from operating activities using the indirect method, a gain on the

sale of equipment is

a. added to net income.

b. deducted from net income.

c. ignored because it does not affect cash.

d. not reported on a statement of cash flows.

85. Rubble Company reported net income of $70,000 for the year. During the year, accounts

receivable increased by $6,000, accounts payable decreased by $5,000 and depreciation

expense of $8,000 was recorded. Net cash provided by operating activities for the year is

a. $67,000.

b. $89,000.

c. $63,000.

d. $70,000.

86. Pare Company reported a net loss of $30,000 for the year ended December 31, 2014.

During the year, accounts receivable decreased $15,000, merchandise inventory

increased $25,000, accounts payable increased by $30,000, and depreciation expense of

$20,000 was recorded. During 2014, operating activities

a. used net cash of $10,000.

b. used net cash of $25,000.

c. provided net cash of $10,000.

d. provided net cash of $25,000.

Statement of Cash Flows

13 – 17

87. Starting with net income and adjusting it for items that affected reported net income but

which did not affect cash is called the

a. direct method.

b. indirect method.

c. working capital method.

d. cost-benefit method.

88. In calculating net cash provided by operating activities using the indirect method, an

increase in prepaid expenses during a period is

a. deducted from net income.

b. added to net income.

c. ignored because it does not affect income.

d. ignored because it does not affect expenses.

89. Using the indirect method, patent amortization expense for the period

a. is deducted from net income.

b. causes cash to increase.

c. causes cash to decrease.

d. is added to net income.

90. In developing the cash flows from operating activities, most companies in the U. S.

a. use the direct method.

b. use the indirect method.

c. present both the indirect and direct methods in their financial reports.

d. prepare the operating activities section on the accrual basis.

91. Each of the following is added to net income in computing net cash provided by operating

activities except

a. amortization expense.

b. an increase in accrued expenses payable.

c. a gain on sale of equipment.

d. a decrease in inventory.

92. Which of the following would be subtracted from net income using the indirect method?

a. Depreciation expense

b. An increase in accounts receivable

c. An increase in accounts payable

d. A decrease in prepaid expenses

93. Which of the following would be added to net income using the indirect method?

a. An increase in accounts receivable

b. An increase in prepaid expenses

c. Depreciation expense

d. A decrease in accounts payable

Test Bank for Financial Accounting, Ninth Edition

13 – 18

94. Which of the following would not be an adjustment to net income using the indirect

method?

a. Depreciation Expense

b. An increase in Prepaid Insurance

c. Amortization Expense

d. An increase in Land

95. In calculating cash flows from operating activities using the indirect method, a loss on the

sale of equipment will appear as a(n)

a. subtraction from net income.

b. addition to net income.

c. addition to cash flow from investing activities.

d. subtraction from cash flow from investing activities.

96. Which of the following adjustments to convert net income to net cash provided by

operating activities is correct?

Add to Net Income Deduct from Net Income

a. Accounts Receivable increase decrease

b. Prepaid Expenses increase decrease

c. Inventory decrease increase

d. Taxes Payable decrease increase

97. Which of the following adjustments to convert net income to net cash provided by

operating activities is incorrect?

Add to Net Income Deduct from Net Income

a. Accounts Receivable decrease increase

b. Prepaid Expenses increase decrease

c. Inventory decrease increase

d. Accounts Payable increase decrease

98. Which of the following adjustments to convert net income to net cash provided by

operating activities is not added to net income?

a. Gain on Sale of Equipment

b. Depreciation Expense

c. Patent Amortization Expense

d. Depletion Expense

99. Using the indirect method, if equipment is sold at a gain, the

a. sale proceeds received are deducted in the operating activities section.

b. sale proceeds received are added in the operating activities section.

c. amount of the gain is added in the operating activities section.

d. amount of the gain is deducted in the operating activities section.

Statement of Cash Flows

13 – 19

100. A company had net income of $210,000. Depreciation expense is $27,000. During the

year, Accounts Receivable and Inventory increased $17,000 and $42,000, respectively.

Prepaid Expenses and Accounts Payable decreased $5,000 and $6,000, respectively.

There was also a loss on the sale of equipment of $2,000. How much cash was provided

by operating activities?

a. $175,000

b. $179,000

c. $241,000

d. $271,000

101. On the statement of cash flows using the indirect method, patent amortization expense will

a. be added to net income in the operating section.

b. be deducted from net income in the operating section.

c. appear as an inflow of cash in the investing section.

d. appear as an outflow of cash in the investing section.

102. The indirect and direct methods of preparing the statement of cash flows are identical

except for the

a. significant noncash activity section.

b. operating activities section.

c. investing activities section.

d. financing activities section.

103. Land acquired from the issuance of common stock is reported

a. as a financing activity.

b. as an investing activity.

c. as an operating activity.

d. in a separate schedule at the bottom of the statement of cash flows.

104. In Ramon Company, Treasury Stock increased $20,000 from a cash purchase, and

Retained Earnings increased $80,000 as a result of net income of $120,000 and cash

dividends paid of $40,000. Net cash used by financing activities is:

a. $20,000.

b. $40,000.

c. $120,000.

d. $60,000.

Test Bank for Financial Accounting, Ninth Edition

13 – 20

105. In Alona Company, net income is $285,000. If accounts receivable increased $140,000

and accounts payable decreased $40,000, net cash provided by operating activities using

the indirect method is:

a. $105,000.

b. $185,000.

c. $385,000.

d. $465,000.

106. In Lynne Company, there was an increase in the land account during the year of $43,000.

Analysis reveals that the change resulted from a cash sale of land at cost $115,000, and a

cash purchase of land for $158,000. In the statement of cash flows, the change in the land

account should be reported in the investment section:

a. as a net purchase of land, $43,000.

b. only as a purchase of land $158,000.

c. as a purchase of land $158,000 and a sale of land $115,000.

d. only as a sale of land $115,000.

107. The following data are available for Sampson Corporation.

Net income $200,000

Depreciation expense 60,000

Dividends paid 90,000

Loss on sale of land 15,000

Decrease in accounts receivable 30,000

Decrease in accounts payable 45,000

Net cash provided by operating activities is:

a. $140,000.

b. $260,000.

c. $160,000.

d. $240,000.

108. The following data are available for Alamo Corporation.

Sale of land $225,000

Sale of equipment $130,000

Issuance of common stock 140,000

Purchase of equipment 70,000

Payment of cash dividends 120,000

Net cash provided by investing activities is:

a. $285,000.

b. $260,000.

c. $305,000.

d. $425,000.

Statement of Cash Flows

13 – 21

109. The following data are available for Two-off Company.

Increase in accounts payable $120,000

Increase in bonds payable 300,000

Sale of investments 150,000

Issuance of common stock 160,000

Payment of cash dividends 90,000

Net cash provided by financing activities is:

a. $180,000.

b. $370,000.

c. $360,000.

d. $420,000.

110. If $250,000 of bonds are issued during the year but $130,000 of old bonds are retired

during the year, the statement of cash flows will show a(n)

a. net increase in cash of $120,000.

b. net decrease in cash of $120,000.

c. increase in cash of $250,000 and a decrease in cash of $130,000.

d. net gain on retirement of bonds of $120,000.

111. Which of the following changes in retained earnings during a period will be reported in the

financing activities section of the statement of cash flows?

1. Declaration and payment of a cash dividend during the period.

2. Net income for the period.

a. 1

b. 2

c. Neither 1 nor 2.

d. Both 1 and 2.

112. The statement of cash flows

a. is prepared instead of an income statement under generally accepted accounting

principles.

b. is used to assess an entity’s ability to pay dividends and meet obligations.

c. is prepared from comparative income statements.

d. reflects earnings per share figures on a cash basis and on an accrual basis in the

body of the statement.

113. In preparing the statement of cash flows, determining the net increase or decrease in cash

requires the use of

a. the adjusted trial balance.

b. the current period’s balance sheet.

c. a comparative balance sheet.

d. a comparative income statement.

Test Bank for Financial Accounting, Ninth Edition

13 – 22

114. To determine the net cash provided (used) by operating activities, it is necessary to analyze

a. the current year’s income statement.

b. a comparative balance sheet.

c. additional information.

d. All of these answers are correct.

115. Which of the following would not be needed to determine net cash provided by operating

activities?

a. Depreciation expense

b. Change in accounts receivable

c. Payment of cash dividends

d. Change in prepaid expenses

116. When equipment is sold for cash, the amount received is reflected as a cash

a. inflow in the operating section.

b. inflow in the financing section.

c. inflow in the investing section.

d. outflow in the operating section.

117. The statement of cash flows will not provide insight into

a. why dividends were not increased.

b. whether cash flow is greater than net income.

c. the exact proceeds of a future bond issue.

d. how the retirement of debt was accomplished.

118. Which of the following transactions would not be classified as a financing activity?

a. Purchase of treasury stock

b. Payment of dividends

c. Issuance of bonds at a discount

d. Purchase of a long-term investment in bonds

119. A measure that describes the cash remaining from operations after adjustment for capital

expenditures and dividends is

a. adjusted cash from operations.

b. cash provided by operations.

c. free cash flow.

d. net cash provided by operating activities.

120. Free cash flow equals cash provided by

a. operations less capital expenditures and cash dividends.

b. operations less cash dividends.

c. investing activities less capital expenditures and cash dividends.

d. operations less capital expenditures.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 23

121. Tomas Pest Control Products has the following information available:

Net Income $25,000

Cash Provided by Operations 33,000

Cash Sales 65,000

Capital Expenditures 10,000

Dividends Paid 2,000

What is Tomas’ free cash flow?

a. $27,000

b. $23,000

c. $21,000

d. $10,000

122. During 2014, Harvey Industries reported cash provided by operations of $670,000, cash

used in investing of $1,039,000, and cash used in financing of $145,000. In addition, cash

spent for fixed assets during the period was $404,000. No dividends were paid. Based on

this information, what was Harvey’s free cash flow?

a. ($369,000)

b. $1,450,000

c. $266,000

d. ($918,000)

123. All of the following statements about free cash flow are false except:

a. Significant free cash flow indicates less potential to finance new investments.

b. Free cash flow is most commonly calculated by subtracting capital expenditures from

cash provided by operations and then adding cash dividends.

c. Free cash flow is not reported on the statement of cash flows.

d. Significant free cash flow indicates less potential to pay additional dividends.

a124. The cost of goods sold during the year was $183,000. Merchandise inventory decreased

by $8,000 during the year and accounts payable decreased by $4,000 during the year.

Using the direct method of reporting cash flows from operating activities, cash payments

for merchandise total

a. $187,000.

b. $179,000.

c. $171,000.

d. $195,000.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 24

a125. Gonzo Company reports a $25,000 increase in inventory and a $12,000 decrease in

accounts payable during the year. Cost of Goods Sold for the year was $185,000. Using

the direct method of reporting cash flows from operating activities, cash payments made

to suppliers were

a. $185,000.

b. $197,000.

c. $222,000.

d. $148,000.

a126. During 2015, Zuma Company had $150,000 in cash sales and $1,240,000 in credit sales.

The accounts receivable balances were $180,000 and $215,000 at December 31, 2014

and 2015, respectively. Using the direct method of reporting cash flows from operating

activities, what was the total cash collected from all customers during 2015?

a. $1,205,000

b. $1,425,000

c. $1,390,000

d. $1,355,000

a127. Lager Company has other operating expenses of $260,000. There has been an increase

in prepaid expenses of $20,000 during the year, and accrued liabilities are $15,000 lower

than in the prior period. Using the direct method of reporting cash flows from operating

activities, what were Lager’s cash payments for operating expenses?

a. $255,000

b. $265,000

c. $225,000

d. $295,000

128. In the Papyrus Corporation, cash receipts from customers were $136,000, cash payments

for operating expenses were $102,000, and one-third of the company’s $9,300 income

taxes were paid during the year. Net cash provided by operating activities is:

a. $34,000.

b. $24,700.

c. $30,900.

d. $27,800.

a129. Each of the following would be reported under operating activities except cash receipts

a. from sales of goods.

b. from sales of investments.

c. of interest on loans.

d. of dividends from investments.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 25

a130. Which of the following statements concerning the statement of cash flows is true?

a. The statement of cash flows is usually more accurate when using the indirect method.

b. If the direct method is used, a supplementary schedule reconciling the net income to

net cash from operating activities must still be provided.

c. The statement of cash flows reflects both earnings per share and cash per share.

d. The statement of cash flows is an optional financial statement for external reporting

purposes.

a131. Squeeze Company reports the following:

End of Year Beginning of Year

Inventory $25,000 $42,000

Accounts Payable 22,000 12,000

If cost of goods sold for the year is $220,000, the amount of cash paid to suppliers is

a. $227,000.

b. $205,000.

c. $193,000.

d. $247,000.

a132. During the year, Salaries Payable decreased by $5,000. If Salary Expense amounted to

$174,000 for the year, the cash paid to employees (including deductions from gross pay) is

a. $179,000.

b. $174,000.

c. $169,000.

d. $184,000.

a133. Ale Company reports a $16,000 increase in inventory and a $8,000 increase in accounts

payable during the year. Cost of Goods Sold for the year was $150,000. The cash

payments made to suppliers were

a. $150,000.

b. $158,000.

c. $126,000.

d. $174,000.

a134. LRRP Company had credit sales of $650,000. The beginning accounts receivable balance

was $15,000 and the ending accounts receivable balance was $140,000. What were the

cash collections from customers during the period?

a. $775,000

b. $650,000

c. $525,000

d. $665,000

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 26

a135. Marke Inc. had cash sales of $400,000 and credit sales of $1,150,000. The accounts

receivable balance increased $30,000 during the year. How much cash did Marke receive

from its customers during the year?

a. $1,520,000

b. $1,120,000

c. $1,550,000

d. $780,000

a136. Ware Company had purchases of $260,000. The comparative balance sheet analysis

revealed a $15,000 decrease in inventory and a $25,000 increase in accounts payable.

What were Ware‘s cash payments to suppliers?

a. $235,000

b. $220,000

c. $275,000

d. $300,000

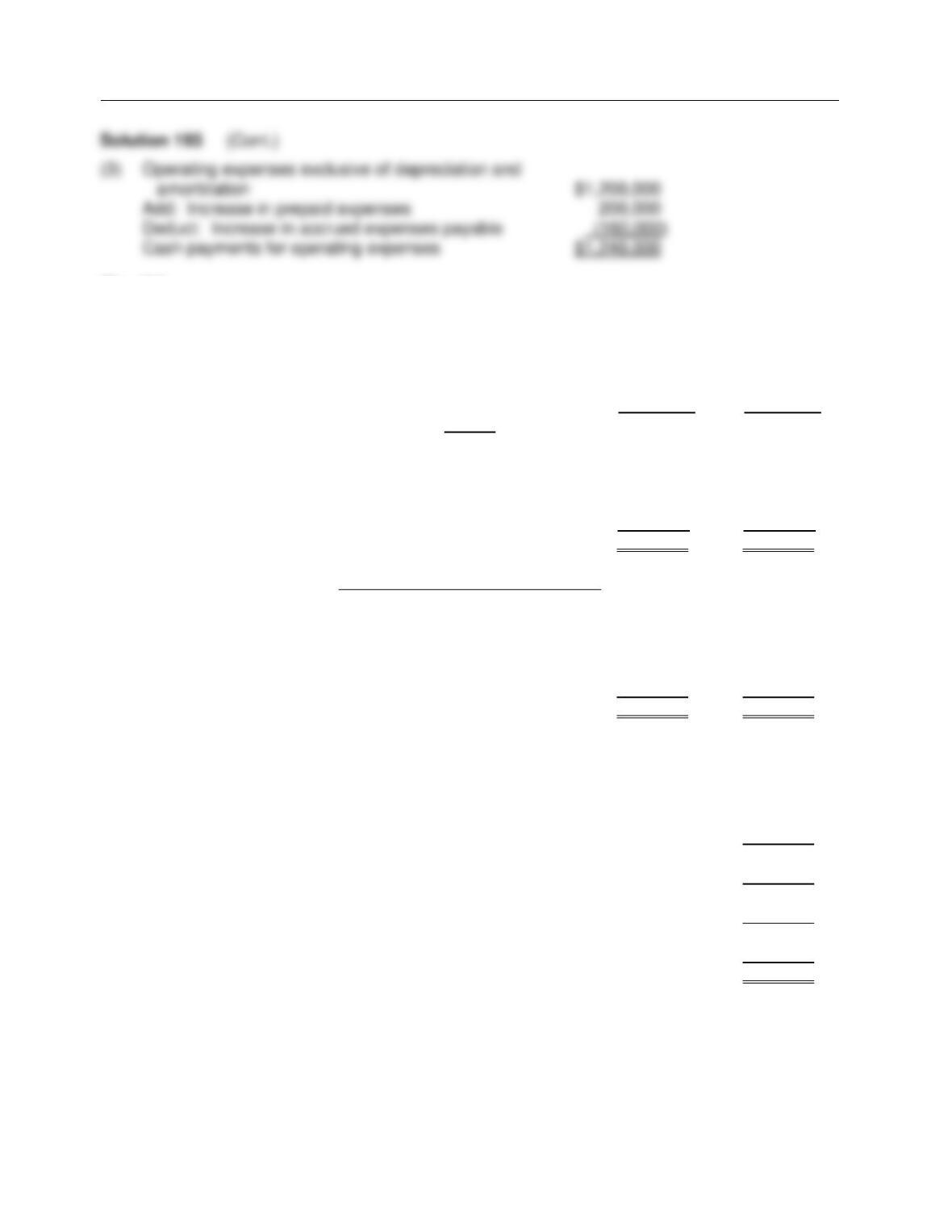

a137. Christine Company had an increase in inventory of $55,000. The cost of goods sold was

$95,000. There was a $6,000 decrease in accounts payable from the prior period. What

were Christine’s cash payments to suppliers?

a. $156,000

b. $61,000

c. $144,000

d. $101,000

Solution; $95,000 + $55,000 + $6,000 = $156,000

a138. Which of the following items does not appear in the statement of cash flows under the

direct method?

a. Cash payments to suppliers

b. Cash collections from customers

c. Depreciation Expense

d. Cash from the sale of equipment

a139. Ale Company has other operating expenses of $80,000. There has been a decrease in

prepaid expenses of $6,000 during the year, and accrued liabilities are $5,000 larger than

in the prior period. What were Ale’s cash payments for operating expenses?

a. $81,000

b. $82,000

c. $69,000

d. $80,000

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 27

a140. Beane Corporation shows income tax expense of $82,000. There has been a $6,000

decrease in federal income taxes payable and a $7,000 increase in state income taxes

payable during the year. What was Beane’s cash payment for income taxes?

a. $82,000

b. $81,000

c. $76,000

d. $95,000

a141. Which of the following would not appear in the operating activities section of a statement

of cash flows prepared under the direct method?

a. Cash receipts from customers

b. Cash paid for income taxes

c. Gain on sale of equipment

d. Cash paid to employees

a142. In the Garnet Company, the beginning and ending balances in Land were $198,000 and

$240,000 respectively. During the year, land costing $50,000 was sold for $50,000 cash,

and land costing $92,000 was purchased for cash. The entries in the reconciling columns

of the worksheet will include a:

a. credit to Land $50,000 and a debit to Sale of Land $50,000 under investing activities.

b. debit to Land $92,000 and a credit to Purchase of Land $92,000 under financing

activities.

c. net debit to Land $42,000 and a credit to Purchase of Land $42,000 under investing

activities.

d. credit to Land $50,000 and a debit to Sale of Land $50,000 under financing activities.

a143. When listing accounts in the statement of cash flows worksheet, the accumulated

depreciation account is shown

a. with accounts that have credit balances.

b. with accounts that have debit balances.

c. as a credit under the reconciling items.

d. as a debit under the reconciling items.

a144. In the bottom portion of the statement of cash flows worksheet,

a. inflows of cash are debits in the reconciling columns.

b. outflows of cash are debits in the reconciling columns.

c. information pertaining to investing and financing activities only is entered.

d. only significant noncash transactions are entered.

Test Bank for Financial Accounting, Ninth Edition

13 – 28

a145. On the statement of cash flows worksheet,

a. significant noncash investing and financing activities are not entered in the reconciling

columns.

b. a decrease in cash will be offset by a debit in the reconciling items columns at the

bottom of the worksheet.

c. an increase in cash will be offset by a debit in the reconciling items column at the

bottom of the worksheet.

d. income statement accounts are listed after balance sheet accounts in the top half of

the worksheet under the indirect method.

146. Which of the following steps is not required in preparing the statement of cash flows?

a. Determine the net change in cash.

b. Determine the net cash provided by operating activities.

c. Determine cash from investing and financing activities.

d. Determine the change in current assets.

147. Financing activities involve

a. lending money to other entities and collecting on those loans.

b. cash receipts from sales of goods and services.

c. acquiring and disposing of productive long-lived assets.

d. long-term liability and stockholders’ equity items.

148. The information to prepare the statement of cash flows usually comes from each of the

following except

a. the comparative balance sheet.

b. the prior year’s income statement.

c. additional information.

d. the current income statement.

149. The statement of cash flows is prepared from all of the following except

a. the adjusted trial balance.

b. comparative balance sheets.

c. selected transaction data.

d. the current income statement.

150. The information in a statement of cash flows will not help investors to assess the entity’s

ability to

a. generate future cash flows.

b. obtain favorable borrowing terms at a bank.

c. pay dividends.

d. pay its obligations when they become due.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 29

151. In converting net income to net cash provided by operating activities, under the indirect

method:

a. decreases in accounts receivable and increases in prepaid expenses are added.

b. decreases in inventory and increases in accrued liabilities are added.

c. decreases in accounts payable and decreases in inventory are deducted.

d. increases in accounts receivable and increases in accrued liabilities are deducted.

152. In the Buans Company, land decreased $80,000 because of a cash sale for $80,000, the

equipment account increased $35,000 as a result of a cash purchase, and Bonds Payable

increased $60,000 from an issuance for cash at face value. The net cash provided by

investing activities is

a. $80,000.

b. $165,000.

c. $45,000.

d. $25,000.

a153. Hogan Company uses the direct method in determining net cash provided by operating

activities, During the year, operating expenses were $295,000, prepaid expenses

increased $23,000, and accrued expenses payable increased $33,000. Cash payments

for operating expenses were

a. $39,000.

b. $51,000.

c. $305,000.

d. $285,000.

a154. Spa Company uses the direct method in determining net cash provided by operating

activities. The income statement shows income tax expense $85,000. Income taxes

payable were $35,000 at the beginning of the year and $20,000 at the end of the year.

Cash payments for income taxes are

a. $70,000.

b. $85,000.

c. $100,000.

d. $140,000.

a155. When a worksheet is used, all but one of the following statements is correct. The

incorrect statement is

a. Reconciling items on the worksheet are not journalized or posted.

b. The bottom portion of the worksheet shows the statement of cash flows effects.

c. The balance sheet accounts portion of the worksheet is divided into two parts: assets,

and liabilities and stockholders’ equity.

d. Each line pertaining to a balance sheet account should foot across.

Test Bank for Financial Accounting, Ninth Edition

13 – 30

156. Under IFRS, the cash flow statement can be prepared using

a. the direct method only.

b. the indirect method only.

c. either the direct or indirect method.

d. the T-account method only.

157. Under IFRS, bank overdrafts are classified as

a. operating activities.

b. investing activities.

c. financing activities.

d. cash and cash equivalents.

158. Which of the following activities is excluded from the statement of cash flows under IFRS?

a. Financing activities

b. Investing activities

c. Noncash investing and financing activities

d. Operating activities

FSA

159. Each of the following items may be classified as operating or financing activities under

IFRS except

a. dividends paid.

b. dividends received.

c. interest paid.

d. All of these answers are correct.

FSA

160. Under IFRS, some companies present which section of the cash flow statement as a

single line item?

a. Operating activities

b. Investing activities

c. Financing activities

d. Noncash investing and financing activities

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 31

Answers to Multiple Choice Questions

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

BRIEF EXERCISES

BE 161

Selected transactions for the Ecker Company are listed below.

1. Collected accounts receivable.

2. Declared and paid dividends on common stock.

3. Sold long-term investments for cash.

4. Issued stock for equipment.

5. Repaid five year note payable.

6. Paid employee wages.

7. Converted bonds payable to common stock.

8. Acquired long-term investment with cash.

9. Sold buildings and equipment for cash.

10. Sold merchandise to customers.

Instructions

Classify each transaction as either (a) an operating activity, (b) an investing activity, (c) a

financing activity, or (d) a noncash investing and financing activity.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 32

BE 162

Garton Company had net income of $195,000 in 2014. Depreciation expense for the year is

$50,000. During the year, Accounts Receivable increased $8,000 and Prepaid Expenses

decreased $1,000. The company also sold equipment at a loss of $3,000.

Instructions

Calculate net cash flows from operating activities using the indirect method.

BE 163

During 2014, Blaine Company sold a building with a book value of $145,000 for proceeds of

$175,000. The company also sold long-term investments for proceeds of $32,000. The company

purchased land and a new building for $320,000 by signing a long-term note payable. No other

transactions impacted long-term asset accounts during 2014.

Instructions

Compute net cash flows from investing activities.

BE 164

Madisun Company issued common stock for proceeds of $20,000 during 2014. The company

paid dividends of $5,000. The company also issued a long-term note payable for $35,000 in

exchange for equipment during the year. The company sold treasury stock that had a cost of

$3,000 for $9,000.

Instructions

Compute net cash flows from financing activities.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 33

BE 165

At January 1, 2014, Benny Enterprises reported a balance in the Equipment account of $45,000.

During the year the company purchased equipment with a cost of $60,000 and sold equipment

with a book value of $30,000. The company reported a loss on the sale of equipment of $4,000.

Assume the indirect method is used.

Instructions

Determine what amount will be reported in (a) the operating activities section and (b) the

investing activities section with regard to the purchase and sale of equipment.

BE 166

Assume the indirect method is used to compute cash flows from operations. For each item listed

below, indicate the effect on net income in arriving at cash flows from operations by choosing one

of the following code letters.

Code

Cash Flows From Operating Activities

Add to Net Income A

Deduct from Net Income D

1. Increase in accounts receivable

2. Increase in inventory

3. Decrease in prepaid expenses

4. Decrease in accounts payable

5. Increase in accrued liabilities

6. Increase in income taxes payable

7. Depreciation expense

8. Loss on sale of investment

9. Gain on disposal of equipment

10. Amortization expense

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 34

BE 167

Doctor Company prepared the tabulation below at December 31, 2015.

Net Income ……………………………………………………………………………………………… $307,000

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation expense, $32,000 ………………………………………………………….. ______

Decrease in accounts receivable, $50,000 …………………………………………… ______

Increase in inventory, $12,000 ……………………………………………………………. ______

Decrease in accounts payable, $8,600 ………………………………………………… ______

Increase in income taxes payable, $1,500 ……………………………………………. ______

Loss on sale of land, $5,000 ………………………………………………………………. ______

Net cash provided (used) by operating activities ……………………………………. ______

Instructions

Show how each item should be reported in the statement of cash flows. Use parentheses for

deductions.

BE 168

Hogan Enterprises reported cash flow from operations of $275,000. The company made capital

expenditures of $110,000 and paid dividends of $35,000.

Instructions

Compute free cash flow.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 35

aBE 169

Small Company reported cost of goods sold of $179,000 on its 2014 income statement. The

company’s beginning inventory was $35,000. The ending inventory was valued at $40,000. The

Accounts Payable balance at January 1 was $25,000. The December 31 balance in Accounts

Payable was $22,000.

Instructions

Compute cash payments to suppliers.

aBE 170

Show Company had total operating expenses of $153,000 in 2014, which included Depreciation

Expense of $30,000. Also during 2014, prepaid expenses decreased by $9,500 and accrued

expenses increased by $8,500.

Instructions

Calculate the amount of cash payments for operating expenses in 2014 using the direct method.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 36

EXERCISES

Ex. 171

Classify each of the following as a(n):

A. Operating Activity

B. Investing Activity

C. Financing Activity

_____ 1 Issuance of bonds.

_____ 2. Sale of equipment.

_____ 3. Amortization expense.

_____ 4. Purchase of treasury stock.

_____ 5. Receipt of dividends on investment.

_____ 6. Purchase of land.

Ex. 172

Selected transactions of Alton Company are listed below.

1. Common stock is sold for cash above par value.

2. Bonds payable are issued for cash at a discount.

3. Interest receivable on a short-term note receivable is collected.

4. Land is sold for cash at book value.

5. Accounts payable are paid in cash.

6. Equipment is purchased by signing a 3-year, 10% note payable.

7. Cash dividends on common stock are declared and paid.

8. 100 shares of XYZ common stock are purchased for cash.

9. Merchandise is sold to customers for cash.

10. Bonds payable are converted into common stock.

Instructions

Classify each transaction as either (a) an operating activity, (b) an investing activity, (c) a

financing activity, or (d) a noncash investing and financing activity.

Statement of Cash Flows

13 – 37

Ex. 173

(a) Identify several alternatives for presenting significant noncash activities in financial

statements.

(b) Give three examples of significant noncash transactions.

Ex. 174

The following information is available for Redcands Company:

Receipts from customers $215,000

Dividends from stock investments 3,000

Proceeds from sale of equipment 18,000

Proceeds from issuance of stock 90,000

Payments for inventory 100,000

Payments for operating expenses 78,000

Interest paid 6,000

Taxes paid 4,000

Dividends paid 20,000

Instructions

Based on the preceding information, compute the net cash provided by operating activities.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 38

Ex. 175

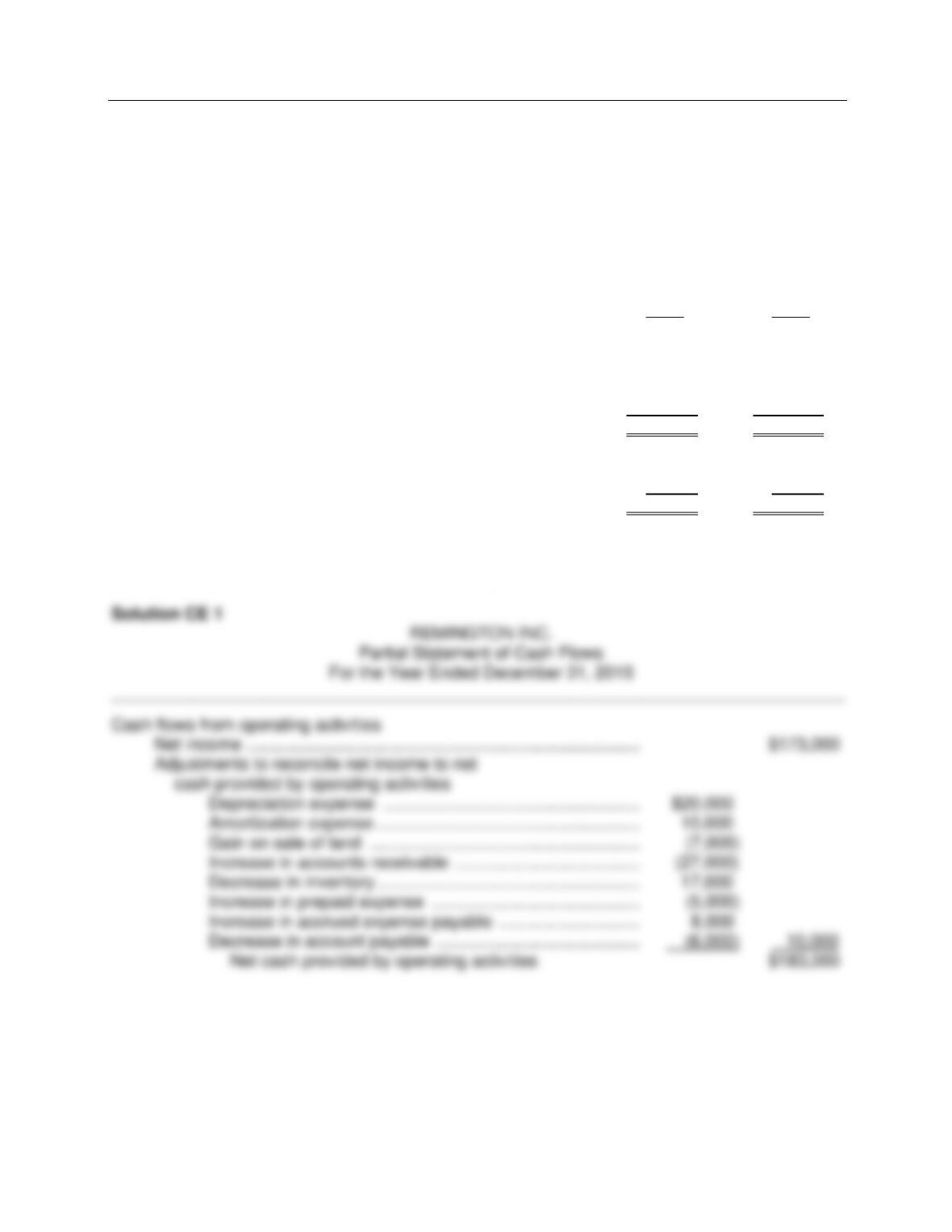

Plough Company reported net income of $180,000 for the current year. Depreciation recorded on

buildings and equipment amounted to $80,000 for the year. Balances of the current asset and

current liability accounts at the beginning and end of the year are as follows:

End of Year Beginning of Year

Cash $20,000 $15,000

Accounts receivable 24,000 32,000

Inventories 50,000 65,000

Prepaid expenses 9,500 5,000

Accounts payable 12,000 18,000

Income taxes payable 1,600 1,200

Instructions

Prepare the cash flows from the operating activities section of the statement of cash flows using

the indirect method.

Ex. 176

Plexis Company reported net income of $148,000. For 2014, depreciation was $45,000, and the

company reported a gain on sale of investments of $12,000. Accounts receivable increased

$25,000 and accounts payable decreased $23,000.

Instructions

Compute net cash provided by operating activities using the indirect method.

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 39

Ex. 177

Assuming a statement of cash flows is prepared, indicate the reporting of the transactions and

events listed below by major categories on the statement. Use the following code letters to indicate

the appropriate category under which the item would appear on the statement of cash flows.

Code

Cash Flows From Operating Activities

Add to Net Income A

Deduct from Net Income D

Cash Flows From Investing Activities IA

Cash Flows From Financing Activities FA

Category

1. Common stock is issued for cash at an amount above par value. _____

2. Merchandise inventory increased during the period. _____

3. Depreciation expense recorded for the period. _____

4. Building was purchased for cash. _____

5. Bonds payable were acquired and retired at their carrying value. _____

6. Accounts payable decreased during the period. _____

7. Prepaid expenses decreased during the period. _____

8. Treasury stock was acquired for cash. _____

9. Land is sold for cash at an amount equal to book value. _____

10. Patent amortization expense recorded for a period. _____

Test Bank for Financial Accounting, Ninth Edition

13 – 40

Ex. 178

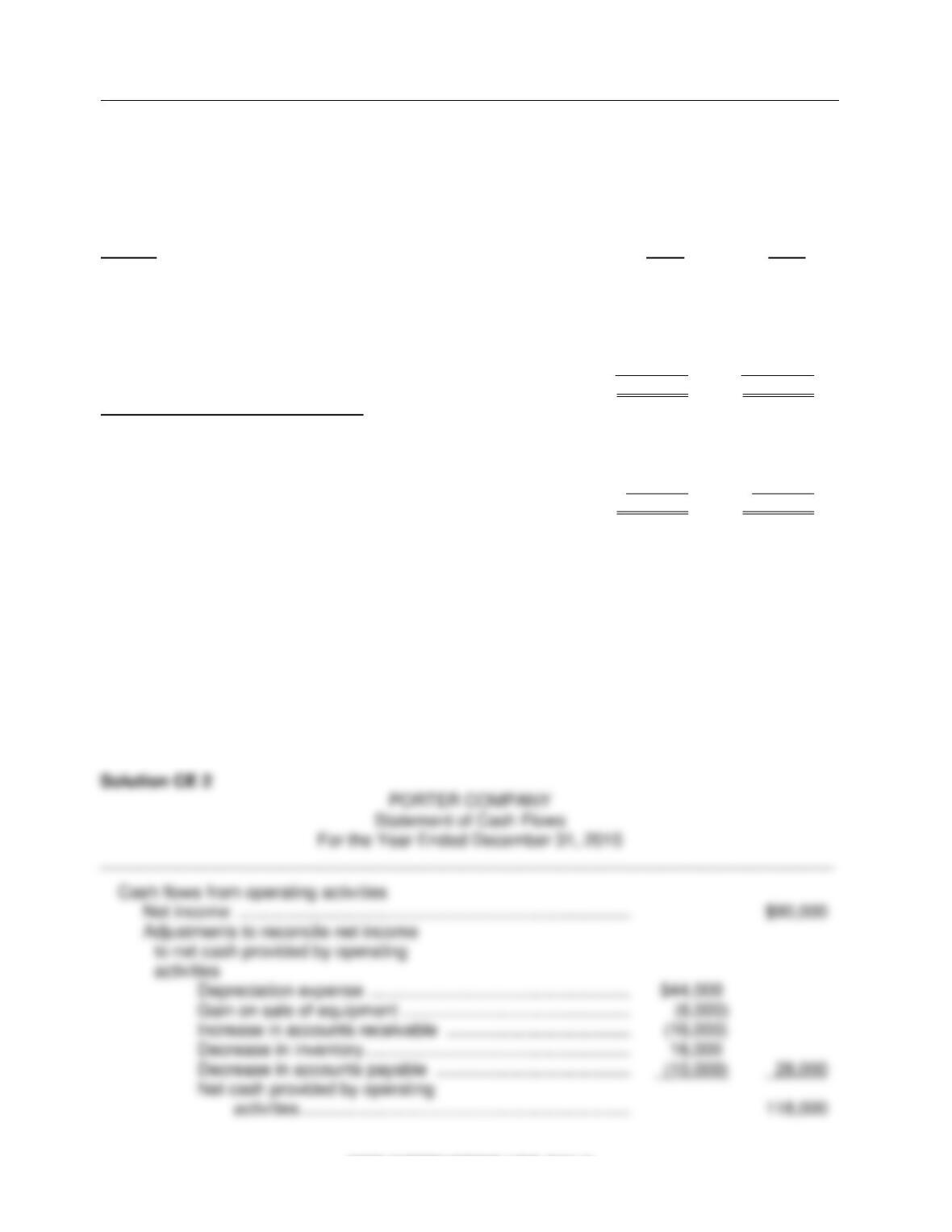

A comparative balance sheet for Rocker Company appears below:

ROCKER COMPANY

Comparative Balance Sheet

Dec. 31, 2015 Dec. 31, 2014

Assets

Cash $ 34,000 $11,000

Accounts receivable 18,000 13,000

Inventory 25,000 17,000

Prepaid expenses 6,000 9,000

Long-term investments -0- 17,000

Equipment 60,000 33,000

Accumulated depreciation—equipment (20,000) (15,000)

Total assets $123,000 $85,000

Liabilities and Stockholders’ Equity

Accounts payable $ 17,000 $ 7,000

Bonds payable 36,000 45,000

Common stock 40,000 23,000

Retained earnings 30,000 10,000

Total liabilities and stockholders’ equity $123,000 $85,000

Additional information:

1. Net income for the year ending December 31, 2015 was $35,000.

2. Cash dividends of $15,000 were declared and paid during the year.

3. Long-term investments that had a cost of $17,000 were sold for $14,000.

4. Sales for 2015 were $120,000.

Instructions

Prepare a statement of cash flows for the year ended December 31, 2015, using the indirect

method.

Statement of Cash Flows

13 – 41

Solution 178 (Cont.)

Ex. 179

A comparative balance sheet for Halpern Corporation is presented below:

HALPERN CORPORATION

Comparative Balance Sheet

2015 2014

Assets

Cash $ 36,000 $ 31,000

Accounts receivable (net) 70,000 60,000

Prepaid insurance 25,000 17,000

Land 18,000 40,000

Equipment 70,000 60,000

Accumulated depreciation (20,000) (13,000)

Total Assets $199,000 $195,000

Liabilities and Stockholders’ Equity

Accounts payable $ 11,000 $ 6,000

Bonds payable 27,000 19,000

Common stock 140,000 115,000

Retained earnings 21,000 55,000

Total liabilities and stockholders’ equity $199,000 $195,000

Additional information:

1. Net loss for 2015 is $20,000.

2. Cash dividends of $14,000 were declared and paid in 2015.

3. Land was sold for cash at a loss of $4,000. This was the only land transaction during the year.

4. Equipment with a cost of $15,000 and accumulated depreciation of $10,000 was sold for

$5,000 cash.

5. $22,000 of bonds were retired during the year at carrying (book) value.

6. Equipment was acquired for common stock. The fair value of the stock at the time of the

exchange was $25,000.

Instructions

Prepare a statement of cash flows for the year ended 2015, using the indirect method.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

13 – 42

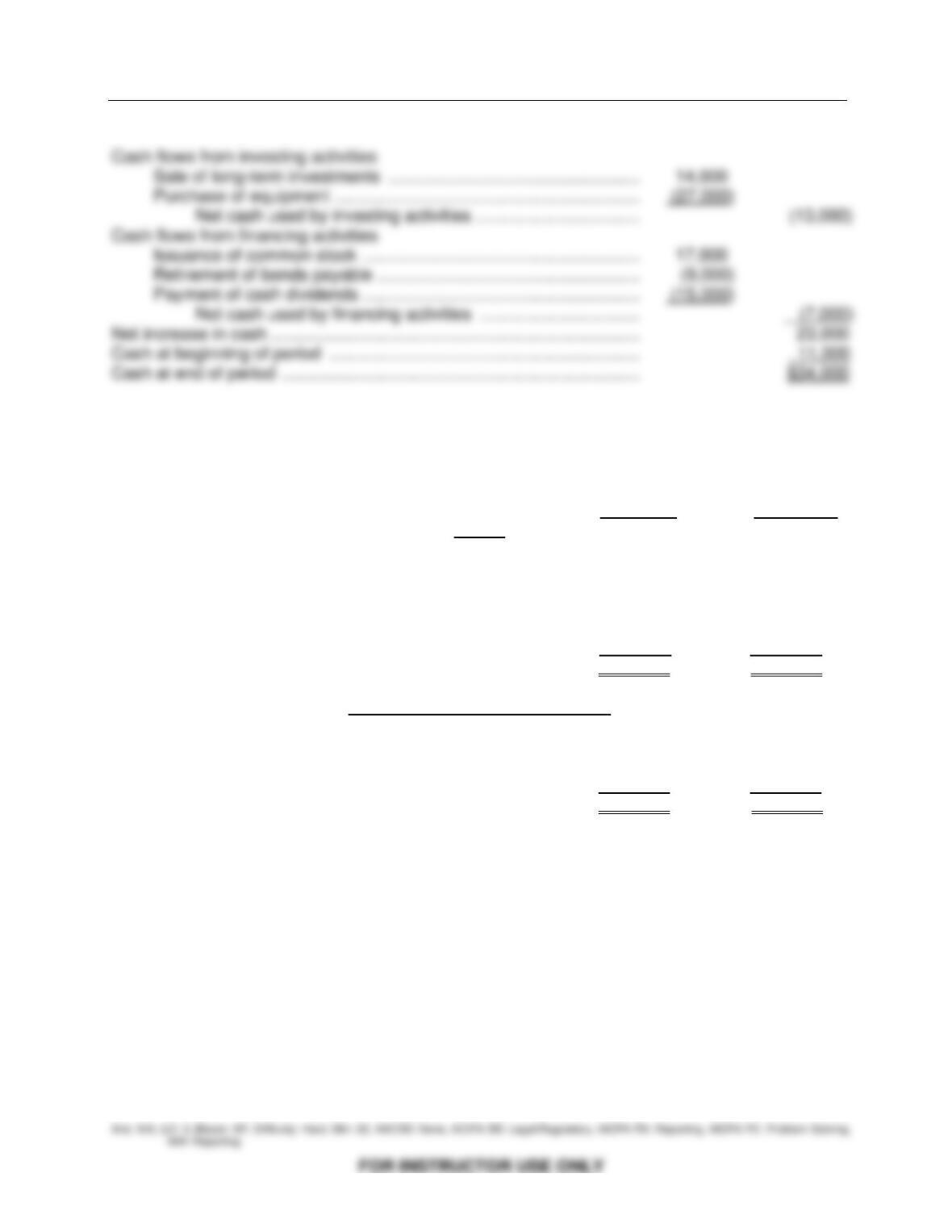

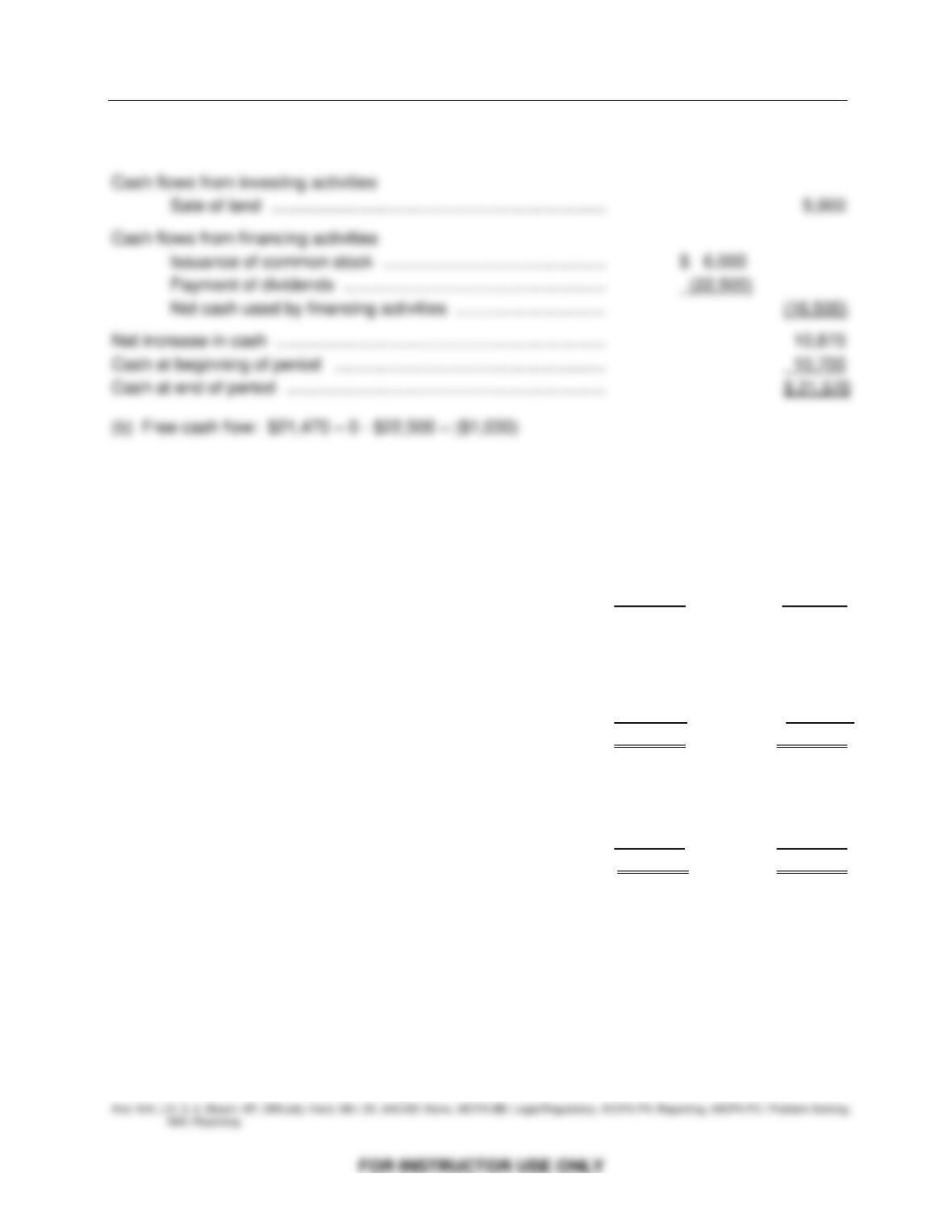

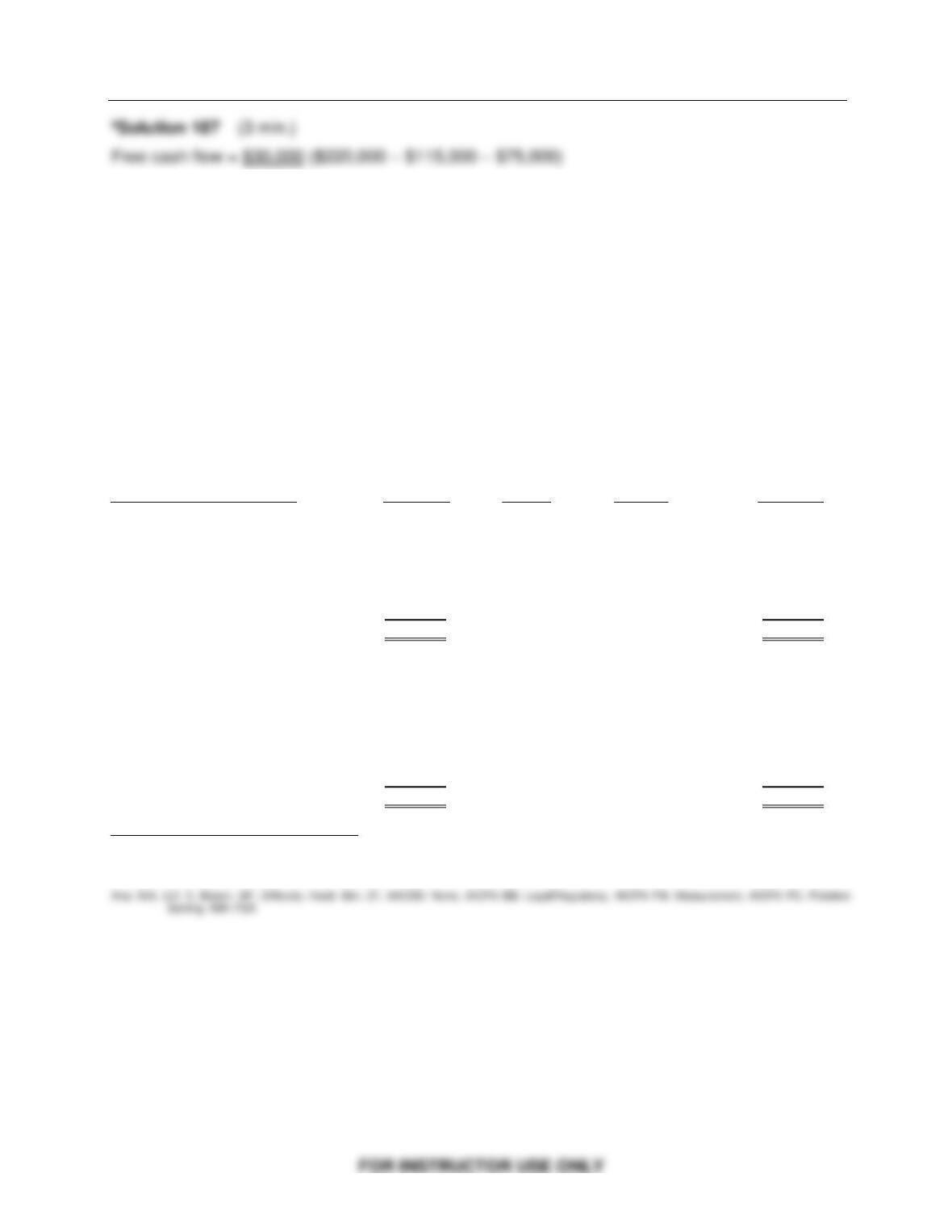

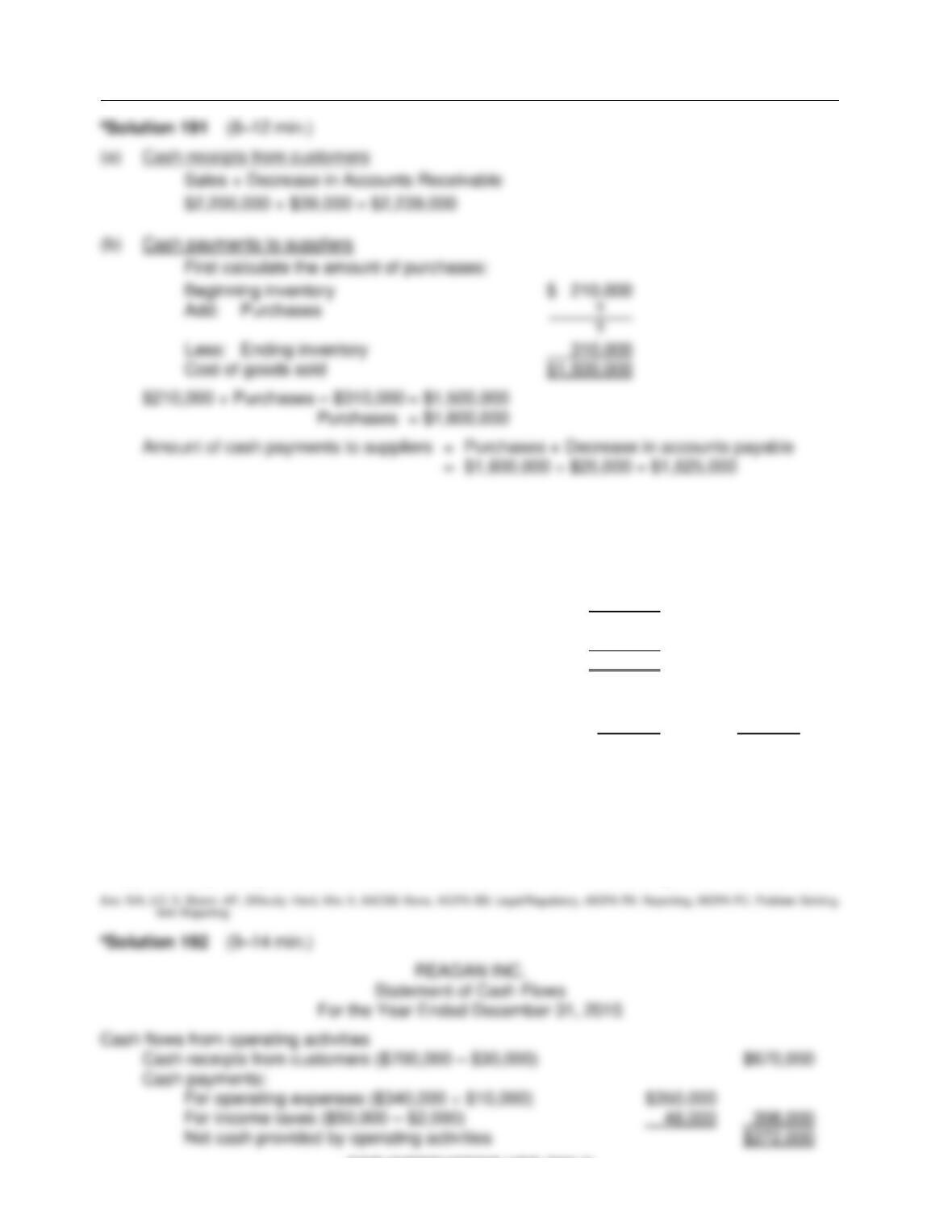

Statement of Cash Flows

FOR INSTRUCTOR USE ONLY

13 – 43

Ex. 180

The following information is available for Sally Corporation for the year ended December 31,

2015:

Collection of principal on long-term loan to a supplier $15,000

Acquisition of equipment for cash 10,000

Proceeds from the sale of long-term investment at book value 20,000

Issuance of common stock for cash 27,000

Depreciation expense 28,000

Redemption of bonds payable at carrying (book) value 35,000

Payment of cash dividends 15,000

Net income 25,000

Purchase of land by issuing bonds payable 45,000

In addition, the following information is available from the comparative balance sheet for Sally at

the end of 2014 and 2015:

2015 2014