Firms in Competitive Markets 3591

89.

In the transition from the short run to the long run, the number of firms in a competitive industry is

a.

fixed.

b.

increasing at a constant rate.

c.

decreasing.

d.

able to adjust to market conditions.

90.

The long-run supply curve for a competitive industry

a.

may be horizontal if entry into the industry lowers average total cost.

b.

may be upward-sloping if higher–cost firms enter the industry.

c.

will be horizontal if there is free entry into the industry.

d.

will be upward-sloping if there are barriers to entry into the industry.

91.

The long–run supply curve for a competitive industry may be upward sloping if

a.

there are barriers to entry.

b.

firms that enter the industry are able to do so at lower average total costs than the existing

firms in the

industry.

c.

some resources are available only in limited quantities.

d.

accounting profits are positive.

92.

If all existing firms and all potential firms have the same cost curves, there are no inputs in limited

quantities, and

the market is characterized by free entry and exit, then the long-run market supply

curve

a.

is horizontal and equal to the minimum of long-run marginal cost for each firm.

b.

must slope downward.

c.

must slope upward.

d.

is horizontal and equal to the minimum of long–run average cost for each firm.

93.

When all firms and potential firms in a market have the same cost curves, the long-run equilibrium

of a competitive

market with free entry and exit will be characterized by firms

a.

earning small but positive economic profits.

b.

facing the prospect of future losses.

c.

operating at the efficient scale.

d.

that work together to raise market prices.

94.

When entry and exit behavior of firms in an industry does not affect a firm‘s cost structure,

a.

the long-run market supply curve must be horizontal.

b.

the long-run market supply curve must be upward-sloping.

c.

the long-run market supply curve must be downward-sloping.

d.

we do not have sufficient information to determine the shape of the long–run market supply

curve.

95.

When some resources used in production are only available in limited quantities, it is likely that the

long–run supply

curve in a competitive market is

a.

downward sloping.

b.

upward sloping.

c.

horizontal.

d.

vertical.

96.

When a competitive market experiences an increase in demand that increases production costs for

existing firms

and potential new entrants, which of the following is most likely to arise?

a.

The long-run market supply curve will be upward sloping.

b.

The condition of free entry into the market will be violated.

c.

Producer profits will fall in the long run.

d.

The long–run market supply curve will be horizontal as new firms enter and drive the price

downward.

97.

When firms in a competitive market have different costs, it is likely that

a.

free entry and exit in the market will be violated.

b.

the market will no longer be considered competitive.

c.

long–run market supply will be downward sloping.

d.

some firms will earn positive economic profits in the long run.

98.

A long-run supply curve is flatter than a short-run supply curve because

a.

firms can enter and exit a market more easily in the long run than in the short run.

b.

long-run supply curves are sometimes downward sloping.

c.

competitive firms have more control over demand in the long run.

d.

firms in a competitive market face identical cost structures.

99.

A market might have an upward-sloping long-run supply curve if

a.

firms have different costs.

b.

consumers exercise market power over producers.

c.

all factors of production are essentially available in unlimited supply.

d.

the entry of new firms into the market has no effect on the cost structure of firms in the

market.

100.

When new entrants into a competitive market have higher costs than existing firms,

a.

accounting profits will be the primary determinant of entry into the market.

b.

sunk costs become an important determinant of the short-run entry strategy.

c.

market price will rise.

d.

long–run supply is constant.

101.

Suppose a competitive market has a horizontal long-run supply curve and is in long-run

equilibrium. If demand

decreases, we can be certain that in the short-run,

a.

at least some firms will shut down.

b.

price will fall below marginal cost for some firms.

c.

price will fall below average total cost for some firms.

d.

at least some firms will enter the industry.

102.

The long-run market supply curve in a competitive market will

a.

always be horizontal.

b.

be the portion of the MC that lies above the minimum of AVC for the marginal firm.

c.

typically be more elastic than the short-run supply curve.

d.

be above the competitive firm’s efficient scale.

103.

In the long run the market supply

a.

must always be horizontal.

b.

could be upward sloping if the cost of production falls as new firms enter the market.

c.

could be upward sloping if the cost of production rises as new firms enter the market.

d.

could be upward sloping if technological improvements lower the cost of producing in the

market.

104.

Suppose that a competitive market is initially in equilibrium. Then demand increases. If some

resources used in

production are not available in sufficient quantities for entering firms,

a.

the long-run market supply curve will be upward sloping.

b.

the long-run market supply curve will be perfectly elastic.

c.

in the long run firms will suffer economic losses, leading them to exit the industry.

d.

the number of firms will decrease, and the market will become a monopoly.

105.

Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering

firms face the same

costs as existing firms and sufficient resources are available for entering

firms,

a.

the long-run market supply curve will be upward sloping.

b.

the long-run market supply curve will be perfectly elastic.

c.

in the long run firms will suffer economic losses, leading them to exit the industry.

d.

the number of firms will decrease, and the market will become a monopoly.

106.

In a market with a fixed number of firms, as long as price is above average

a.

variable cost, each firm’s marginal-cost curve is its supply curve.

b.

variable cost, each firm’s average-total-cost curve is its supply curve.

c.

total cost, each firm’s marginal-cost curve is its supply curve.

d.

total cost, each firm’s average-total-cost curve is its supply curve.

107.

Suppose the long-run supply curve for a good is upward-sloping. The upward slope could be

explained by

a.

increases in production costs resulting from more firms coming into the market.

b.

a breakdown of the “free entry and exit” feature of competition.

c.

a breakdown of the “price taking” feature of competition.

d.

a stable demand curve for the good, that is, a demand curve that never shifts.

108.

Suppose the long-run supply curve for a good is upward-sloping. The upward slope could be

explained by

a.

decreases in production costs resulting from more firms coming into the market.

b.

a breakdown of the “free entry and exit” feature of competition.

c.

a breakdown of the “price taking” feature of competition.

d.

the fact that a resource used in the production of the good is available only in limited quantities.

Firms in Competitive Markets 3601

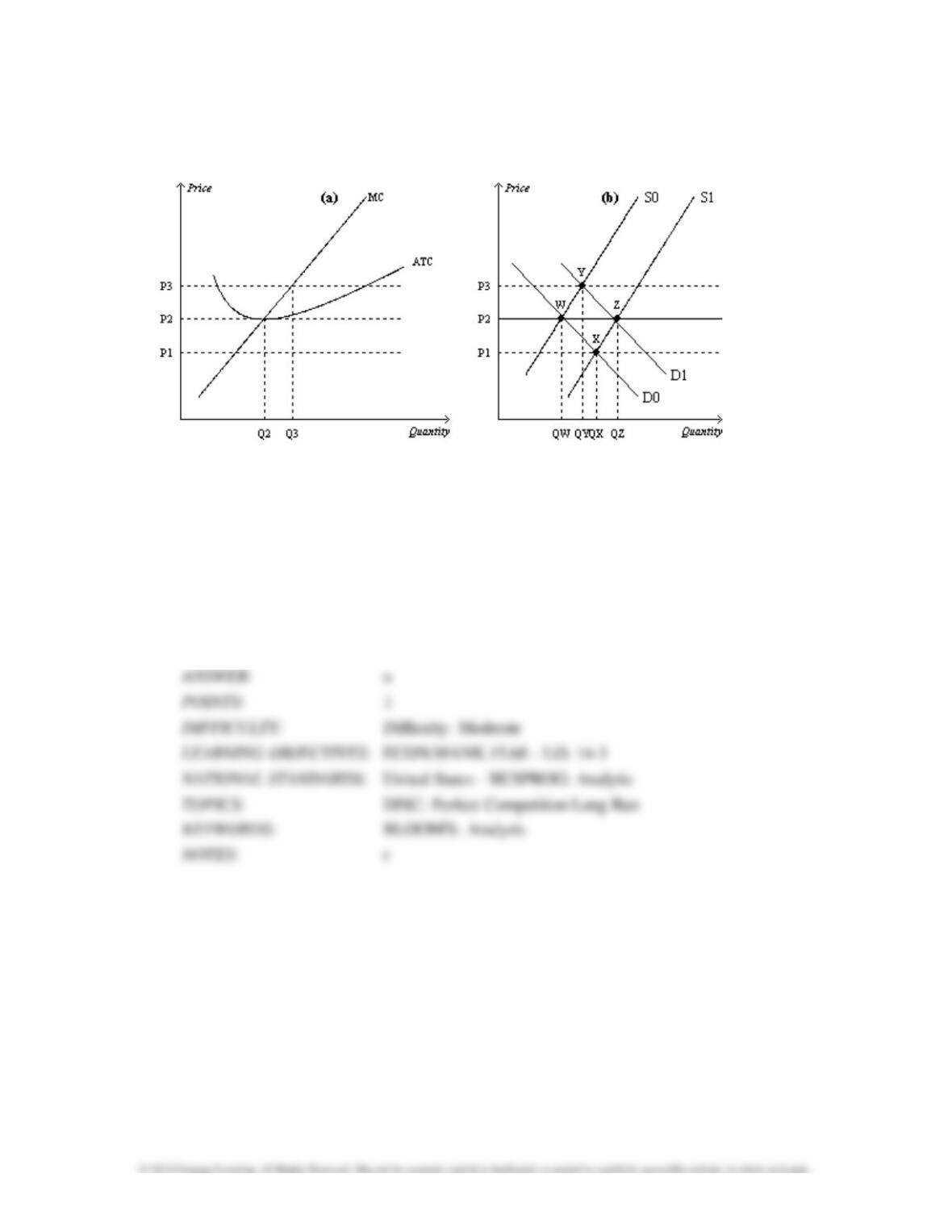

Figure 14–14

109.

Refer to Figure 14-14. When the market is in long-run equilibrium at point W in panel (b), the

firm represented in

panel (a) will

a.

have a zero economic profit.

b.

have a negative accounting profit.

c.

exit the market.

d.

choose to increase production to increase profit.

110.

Refer to Figure 14-14. Assume that the market starts in equilibrium at point W in panel (b).

An increase in

demand from D0 to D1 will result in

a.

a new market equilibrium at point X.

b.

an eventual increase in the number of firms in the market and a new long-run equilibrium at

point Z.

c.

rising prices and falling profits for existing firms in the market.

d.

falling prices and falling profits for existing firms in the market.

111.

Refer to Figure 14-14. Assume that the market starts in equilibrium at point W in panel (b)

and that panel (a)

illustrates the cost curves facing individual firms. Suppose that demand

increases from D0 to D1. Which of the

following statements is correct?

a.

Points W, Y, and Z represent both short–run and long-run equilibria.

b.

Points W, Y, Z, and X represent short-run equilibria.

c.

Points W, Y, and Z represent long-run equilibria.

d.

Points W and Z represent long-run equilibria.

112.

Refer to Figure 14-14. Assume that the market starts in equilibrium at point W in panel (b)

and that panel (a)

illustrates the cost curves facing individual firms. Suppose that demand

increases from D0 to D1. Which of the

following statements is not correct?

a.

Point W is a long-run equilibrium point.

b.

Points W, Y, and Z are short-run equilibria points.

c.

Point Y is a long-run equilibrium point.

d.

Point Z is a long-run equilibrium point.

113.

Refer to Figure 14-14. If the market starts in equilibrium at point Z in panel (b), a decrease in

demand will

ultimately lead to

a.

more firms in the industry but lower levels of output for each firm.

b.

fewer firms in the market.

c.

a new long–run equilibrium at point X in panel (b).

d.

lower prices once the new long-run equilibrium is reached.

114.

Refer to Figure 14-14. Suppose a firm in a competitive market, like the one depicted in panel

(a), observes

market price rising from P1 to P2. Which of the following could explain this

observation?

a.

The entry of new firms into the market.

b.

The exit of existing consumers from the market.

c.

An increase in market supply from S0 to S1.

d.

An increase in market demand from D0 to D1.

Multiple Choice – Section 04: Behind the Supply Curve

1.

The production decisions of perfectly competitive firms follow one of the Ten Principles of

Economics, which states

that rational people

a.

consider sunk costs.

b.

equate prices to the average costs of production.

c.

prefer to purchase products from smaller rather than larger firms.

d.

think at the margin.

2.

If firms are competitive and profit maximizing, the price of a good equals the

a.

marginal cost of production.

b.

fixed cost of production.

c.

total cost of production.

d.

average total cost of production.

3.

Profit maximizing firms in competitive industries with free entry and exit face a price equal to the

lowest possible

a.

marginal cost of production.

b.

fixed cost of production.

c.

total cost of production.

d.

average total cost of production.

3606 Firms in Competitive Markets

True/False and Short Answer

1.

For a firm operating in a perfectly competitive industry, total revenue, marginal revenue, and

average revenue are all

equal.

a.

True

b.

False

2.

For a firm operating in a perfectly competitive industry, marginal revenue and average revenue are

equal.

a.

True

b.

False

3.

If a firm notices that its average revenue equals the current market price, that firm must be

participating in a

competitive market.

a.

True

b.

False

4.

For a firm operating in a competitive market, both marginal revenue and average revenue exceed

the market price.

a.

True

b.

False

5.

A profit-maximizing firm in a competitive market will increase production when average revenue

exceeds marginal

cost.

a.

True

b.

False

6.

A profit-maximizing firm in a competitive market will decrease production when marginal cost

exceeds average

revenue.

a.

True

b.

False

7.

Because there are many buyers and sellers in a perfectly competitive market, no one seller can

influence the market

price.

a.

True

b.

False

8.

In competitive markets, firms that raise their prices are typically rewarded with larger profits.

a.

True

b.

False

9.

When an individual firm in a competitive market increases its production, it is likely that the market

price will fall.

a.

True

b.

False

10.

When an individual firm in a competitive market decreases its production, it is likely that the

market price will rise.

a.

True

b.

False

11.

In a competitive market, firms are unable to differentiate their product from that of other

producers.

a.

True

b.

False

12.

Firms in a competitive market are said to be price takers because there are many sellers in the

market, and the

goods offered by the firms are very similar if not identical.

a.

True

b.

False

13.

The two characteristics of a competitive market are 1) many buyers and sellers in the market and

2) the goods

offered by the various sellers are highly differentiated.

a.

True

b.

False

14.

Firms operating in perfectly competitive markets try to maximize profits.

a.

True

b.

False

15.

Because there are many sellers in a competitive market, individual firms are unable to maximize

profits.

a.

True

b.

False