Chapter 13 – Short-Run Decision Making: Relevant Costing

139. Veblen Company manufactures a variety of athletic shoes: basketball, running, and tennis. Sales of the tennis shoes

have fallen off. Veblen is considering several options: 1) drop the tennis shoe line; 2) replace the tennis shoe line with golf

shoes; 3) retool the tennis shoe line to make “Airtennies.” Price and cost data are as follows:

Basketball

Running

Tennis

Golf

Airtennies

Price

$90

$65

$40

$60

$70

Variable cost/unit

$45

$40

$35

$43

$50

Fixed costs

$200,000

$210,000

$50,000

$50,000

$90,000

Number of units

10,000

15,000

2,500

25,000

6,000

If the tennis shoe line is dropped, the $50,000 fixed cost is totally avoidable.

A.

Calculate the impact on operating income, using relevant amounts only, for keeping the

tennis shoe line.

B.

Calculate the impact on operating income, using relevant amounts only, for option 1.

C.

Calculate the impact on operating income, using relevant amounts only, for option 2.

D.

Calculate the impact on operating income, using relevant amounts only, for option 3.

E.

Which option is best?

Sales

COGS & Net FC

Net Change

Clearly, the status quo (keeping the tennis shoe line) is the worst option and option 2

Option 2

Sales Increase = 25,000 × $60

$1,500,000 − 100,000 = $1,400,000

25,000 × $43

$1,075,000 +$50,000 − 137,500 = $987,500

Net Increase = $1,400,000 − $987,500 = $412,500

Option 3

Sales Increase = 6,000 × $70

$420,000 − 100,000 = $320,000

Option 3 COGS and Fixed Cost Increase

= 6,000 × $50

$300,000 +90,000 − 137,500 = $252,500

Net Increase = $320,000 − $252,500 = $67,500

Chapter 13 – Short-Run Decision Making: Relevant Costing

140. Tyler Company has been approached by a new customer with an offer to purchase 6,000 units of its product KR200

at a price of $11 each. The existing sales would not be affected by this special order. Tyler normally produces 40,000

units but plans to produce and sell 30,000 in the coming year. The normal sales price is $18 per unit. Unit cost information

is as follows:

Direct materials

$4.00

Direct labor

$2.75

Variable overhead

$1.50

Fixed overhead

$3.25

Total

$11.50

If Tyler accepts the order, no fixed manufacturing activities will be affected because there is sufficient excess capacity.

Required:

A. By how much will profit increase or decrease if the order is accepted?

B. Should Tyler accept the special order?

Direct materials

$4.00

Direct labor

$2.75

Variable overhead

$1.50

$8.25

$2.75 × 6,000 = $16,500 increase

B. Yes the order should be accepted.

141. Junior Company currently buys 30,000 units of a part used to manufacture its product at $40 per unit. Recently the

supplier informed Junior Company that a 20% increase will take effect next year. Junior has some additional space and

could produce the units for the following per-unit costs (based on 30,000 units):

Direct materials

$16

Direct labor

12

Variable overhead

12

Fixed overhead

10

Total

$50

If the units are purchased from the supplier, $200,000 of fixed costs will continue to be incurred. In addition, the plant can

be rented out for $20,000 per year if the parts are purchased externally.

Required: Should Junior Company buy the part externally or make it internally?

Purchase price (30,000 × $40 × 1.20)

Fixed costs

Rent received

Net cost to purchase

Cost to produce (30,000 × $50)

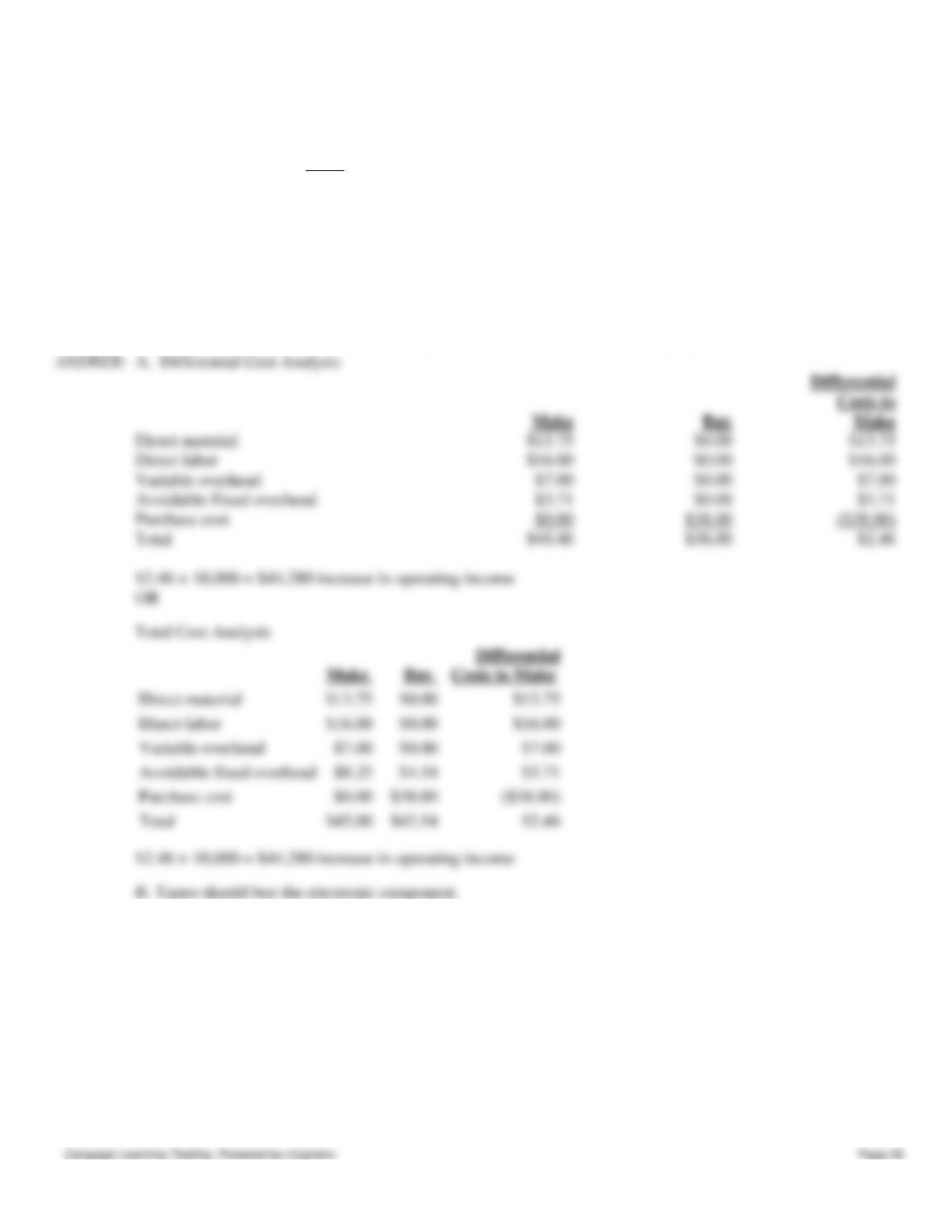

142. Tapeo Company has always made its electronic components that go into their GPS systems in-house. Streeter

Company has offered to supply these electronic components at a price of $38 each. Tapeo uses 18,000 units of these

components each year. The cost per unit of this component is as follows:

Chapter 13 – Short-Run Decision Making: Relevant Costing

Direct material

$13.75

Direct labor

$16.00

Variable overhead

$7.00

Fixed overhead

$8.25

Total

$45.00

Assume that 45% of Tapeo Company’s fixed overhead would be eliminated if the electronic component was no longer

produced in-house.

Required:

A. If Tapeo decided to purchase the electronic component from Streeter Company how much would its operating income

increase or decrease?

B. Should Tapeo continue to make the electronic component or buy it from Streeter Company?

Direct material

Direct labor

Variable overhead

Avoidable Fixed overhead

Purchase cost

$38.00

Total

$38.00

$2.46 × 18,000 = $44,280 increase in operating income

143. Island Princess Pineapples purchases pineapples from area farmers and processes them into rings, juice, and skins.

The cost of the pineapples is a joint cost, as is the initial processing in which the fruits are skinned, cored, and sliced into

rings. At the split-off point, Island Princess sells the skins (for fertilizer). Juice and rings are processed further (further

processing costs occurs for cooking and canning). Data for the three products follows:

Sales

Rings

$2,000

Juice

1,500

Fertilizer

400

Further processing costs:

Rings

500

Chapter 13 – Short-Run Decision Making: Relevant Costing

Juice

300

Joint costs

$1,600

A.

Prepare a segmented income statement for Island Princess, showing results for rings,

juice, fertilizer, and in total. Do not allocate joint costs individually.

B.

Now suppose that Island Princess is considering the option of processing the skins further

into pet food which would sell for $1,000. Additional costs would be $450. Should this

be done?

A.

Further processing costs

Product margin

Joint costs

Operating income

B.

costs do not come into play.

144. Rippey Corporation manufactures a single product with the following unit costs for 5,000 units:

Direct materials

$ 60

Direct labor

30

Factory overhead (40% variable)

90

Selling expenses (60% variable)

30

Administrative expenses (20% variable)

15

Total per unit

$225

Recently, a company approached Rippey Corporation about buying 1,000 units for $225. Currently, the models are sold to

dealers for $412.50. Rippey’s capacity is sufficient to produce the extra 1,000 units. No additional selling expenses would

be incurred on the special order.

Required:

A.

What is the profit earned by Rippey Corporation on the original 5,000 units?

B.

Should Rippey accept the special order if its goal is to maximize short-run profits? How

much will income be affected?

C.

Determine the minimum price Rippey would want to receive in order to increase profits

by $7,500 on the special order.

D.

When making a special-order decision, what qualitative aspects of the decision should

Rippey Corporation consider?

A.

Sales (5,000 × $412.50)

Less: costs (5,000 × $225)

Net income

Yes, profit will increase by:

Increase in sales (1,000 × $225)

Increase in direct labor (1,000 × $30)

Increase in var. overhead (1,000 × $90 × 0.40)

Chapter 13 – Short-Run Decision Making: Relevant Costing

145. Salley Company makes pagers. Currently, Salley purchases 10,000 plastic housings per year from an outside

company for $1 each. One of Salley’s engineers suggested that the company make its plastic housings in-house. Estimated

unit costs are as follows:

Direct materials

$0.30

Direct labor

0.20

Variable overhead

0.15

Fixed overhead*

0.40

* Fixed overhead is $2,400 per year in equipment costs specifically traceable to the plastic housing line and $1,600 per

year in general overhead costs to be allocated to this line

A.

If Salley makes the housing in-house, net income will be $__________________ Higher

or Lower?

B.

What is the highest price per unit that Salley would pay an outside company for the

housings?

C.

Now assume that all of the fixed overhead is allocated fixed overhead and will not be

affected by making the product in-house or purchasing it. If Salley makes the housing in–

house, net income will be $__________________ (Higher / Lower).

$0.89 = $0.30 + 0.20 + 0.15 + 0.24

traceable fixed overhead is irrelevant.

Figure 13-10.

Goutam Company prints a variety of publications and colored inserts for newspapers. Currently, Goutam produces its own

ink, including a special metallic color. India Inks has offered to supply Goutam with the 25,000 ounces of metallic ink that

it needs each year for $1.24 per ounce. Goutam is interested because this is a particularly difficult ink to make. The

purchasing department must make special efforts to locate suppliers, the metallic component requires special handling,

and, since the metallic ink uses machinery that is also used to make other colors of ink, the machinery must be cleaned

very well before every batch of metallic. The accounting department supplied the following unit costs:

Direct materials

$0.40

Direct labor

0.15

Variable overhead

0.06

Increase in var. adm. (1,000 × $15 × 0.20)

Increase in profits

$60 + $30 + ($90 × 0.40) + ($15 × 0.20) + ($7,500 / 1,000)

= $136.50 per unit

What is the impact on regular customers?

Chapter 13 – Short-Run Decision Making: Relevant Costing

Fixed overhead*

0.50

*Fixed overhead is applied on the basis of a plantwide rate based on direct labor hours.

146. Refer to Figure 13-10.

A.

Based on the cost figures, if Goutam purchases metallic ink from the outside supplier,

operating income will be $__________________ (Higher / Lower)?

B.

What is the highest price per ounce that Goutam would pay an outside supplier for the

ink?

147. Refer to Figure 13-10. Upon hearing of the analysis of the cost of making the metallic ink in-house versus buying it

from an outside supplier, Jim Webb, the production supervisor said “That’s nuts! This ink is a real pain to make and $1.24

per ounce sounds like a bargain to me!” Based on Jim’s feelings, Anna Ruiz (a new CMA in the accounting office) did an

ABC analysis of ink production. She came up with the same direct materials, direct labor and variable overhead, as well

as the following information on activities required by metallic ink production.

Setups

$ 60,000

600 setups per year

Purchasing

$270,000

9,000 purchase orders per year

The metallic ink requires 300 purchase orders per year and 80 setups.

A.

If Goutam purchases the ink from the outside supplier, operating income would be

$__________________ Higher Lower (circle one)

B.

What is the highest price per ounce that Goutam would pay an outside company for the

ink?

A.

$1,250 higher

= [$1.24 − ($0.40 + 0.15 + 0.06 + 0.68)] × 25,000

($0.68 is the per ounce cost of setups and purchasing)

Setups = [($60,000 / 600) × 80] / 25,000 = 0.32

Purchasing = [($270,000 / 9,000) × 300] / 25,000 = 0.36

$1.29, since this is the avoidable cost of making the ink in-house, Goutam would not pay

148. Sherpa Company manufactures tents and sleeping bags. Tents are priced at $80, have variable cost of $55, and direct

fixed costs of $120,000. Sleeping bags are priced at $60, have variable cost of $35, and direct fixed costs of $66,000.

Common fixed costs equal $200,000. Last year, the division sold 5,000 tents and 10,000 sleeping bags.

A.

What was the segment margin for tents last year?

B.

What was the segment margin for sleeping bags last year?

C.

What was Sherpa’s operating income last year?

D.

If Sherpa stopped making tents, what would operating income be?

Sales ($80 × 5,000; $60 × 10,000)

10,000)

Chapter 13 – Short-Run Decision Making: Relevant Costing

149. Mickey Company manufactures three joint products: X, Y, and Z. The cost of the joint process is $30,000.

Information about the three products follows:

X

Y

Z

Anticipated production

5,600 lbs.

10,000 lbs.

2,500 lbs.

Selling price/lb. at split-off

$2.00

$1.00

$3.00

Additional processing costs/lb. after split-off

(all variable)

$1.50

$1.25

$.75

Selling price/lb. after further processing

$2.50

$3.75

$6.25

Allocated joint costs

$12,000

$10,500

$7,500

Required:

A.

Determine whether each product should be sold at split-off or processed further.

B.

Determine the firm’s income if the firm processed all three products beyond split-off.

A.

Sell at split-off

Process further

Process further

The joint costs are not relevant to the decision.

B.

$14,350 ($13,750 + $25,000 + $5,600 − $30,000)

150. The operations of Grant Corporation are divided into the Fix Division and the Split Division. Projections for the next

year are as follows:

Fix

Split

Division

Division

Total

Sales revenue

$60,000

$40,000

$100,000

Variable expenses

20,000

15,000

35,000

Contribution margin

$40,000

$25,000

$ 65,000

Contribution margin

$125,000

Less: Direct fixed overhead

Segment margin

Less: Common fixed overhead

Operating income

$ (11,000)

A.

Segment margin for tents = $5,000

B.

Segment margin for sleeping bags = $184,000

C.

Operating income = ($11,000)

D.

Operating income without tents = ($16,000)

Chapter 13 – Short-Run Decision Making: Relevant Costing

Direct fixed expenses

12,500

30,000

42,500

Segment margin

$27,500

$ (5,000)

$ 22,500

Allocated common costs

10,000

7,500

17,500

Total relevant benefit (loss)

$17,500

$(12,500)

$ 5,000

Required:

A.

Determine operating income for Grant Corporation as a whole if the Split Division is

dropped.

B.

Should the Split Division be eliminated?

A.

Sales

$60,000

Variable costs

Contribution margin

$40,000

Direct fixed costs

Segment margin

$27,500

Allocated common costs:

($10,000 + $7,500)

Operating income

$10,000

151. Classy Carry manufactures two types of handbags, the Clutch and the Tote, with unit contribution margins of $9 and

$15, respectively. Regardless of the type, each handbag must go through a stitching machine. The company owns 4

stitching machines and each provides 3,000 hours of machine time per year. Each Clutch handbag requires 12 minutes of

machine time and each Tote handbag requires 30 minutes of machine time. There are no other constraints.

Required:

A. What is the contribution margin per hour of machine time for each type of handbag?

B. What is the optimal mix of handbags?

C. What is the total contribution margin earned for the optimal mix?

Contribution margin per unit

Required machine time per unit*

Contribution margin per hour of machine time

C. 60,000 Clutch handbags × $9 CM = $540,000

152. Gordon Company produces two types of gears, Gear Q and Gear S, with unit contribution margins of $2 and $5,

Chapter 13 – Short-Run Decision Making: Relevant Costing

respectively. Each gear must spend time on a special machine. The firm owns ten machines that together provide 25,000

hours of machine time per year. Gear Q requires 0.10 hours of machine time; Gear S requires 0.4 hours of machine time.

A.

What is the contribution margin per hour of machine time for Gear Q? Gear S?

B.

If Gordon faces only the production constraint (25,000 hours of machine time), how

many units of Gear Q should be produced? Gear S? What is the total contribution margin

from this product mix?

C.

Now suppose that Gordon cannot sell more than 200,000 units of each type of gear. How

many units of Gear Q should be produced? Gear S? What is the total contribution margin

from this product mix?

A.

Contribution margin per unit

Hours of machine time

Contribution margin per hour of machine

Since Gear Q has the higher contribution margin per hour of the scarce resource, Gordon should produce

Gear Q units = 25,000 / 0.10 = 250,000

Gear S units = 0

Total contribution margin = ($2 × 250,000) = $500,000

Gear Q units = 200,000

Remaining machine time = 25,000 hours − (200,000 × 0.10) = 5,000 machine hours

Gear S units = 5,000 / 0.40 = 12,500

Total contribution margin = ($2 × 200,000) + ($5 × 12,500) = $462,500

153. David Company produces two types of gears, Gear A and Gear B, with unit contribution margins of $6 and $8,

respectively. Each gear must spend time on a special machine. The firm owns five machines that together provide 12,000

hours of machine time per year. Gear A requires 12 minutes of machine time; Gear B requires 24 minutes of machine

time.

A.

What is the contribution margin per hour of machine time for Gear A? Gear B?

B.

If David faces only the production constraint (12,000 hours of machine time), how many

units of Gear A should be produced? Gear B? What is the total contribution margin from

this product mix?

C.

Now suppose that David cannot sell more than 45,000 units of each type of gear. How

many units of Gear A should be produced? Gear B? What is the total contribution margin

from this product mix?

A.

Contribution margin per unit

Hours of machine time

Contribution margin per hour of machine

only Gear A, and no Gear B.

Chapter 13 – Short-Run Decision Making: Relevant Costing

Gear A units = 12,000 / 0.20 = 60,000

Gear B units = 0

Total contribution margin = ($6 × 60,000) = $360,000

C.

Gear A units = 45,000

Remaining machine time = 12,000 hours − (45,000 × 0.20) = 3,000 machine hours

Gear B units = 3,000 / 0.40 = 7,500

Total contribution margin = ($6 × 45,000) + ($8 × 7,500) = $330,000

154. Auden makes three types of vitamin supplements, all of which require the use of encapsulating machines that have

capacity of 10,000 hours. Information on the three types (per case) follows:

Basic

Vita-Stress

Antioxidant+

Selling price

$100

$125

$160

Variable cost

50

70

90

Machine hours required

0.4

0.50

0.8

A.

What is the contribution margin per case for each type?

B.

What is the contribution margin per hour of machine time for each type?

C.

Based on your analysis in requirement B, if the company can sell all that it can make of

all of the products, how many of each type should be sold to maximize total contribution

margin?

Price

Contribution margin per unit

Hours of machine time required

CM per hour of machine time

Basic has the highest contribution margin per machine hour. Therefore, the company would devote all

Basic = (1 hour / 0.40 cases per hour) × 10,000 hours

Vita-Stress = 0

Antioxidant+ = 0

155. The Exchange Company is in the process of developing a new product called LS500. The company requires a 35%

profit. The LS500 current design carries with it a total cost of $125.

Required:

A. What is the sales price of the LS500 using markup costing?

B. Assume that the Exchange Company’s marketing department has determined that consumers are willing to pay $140

for the LS500. What is the target cost for this product?

A. $125 × 1.35 = $168.75

Chapter 13 – Short-Run Decision Making: Relevant Costing

$140 – $49 = $91 target cost

156. “The accounting decision making model is not useful in real life because it only looks at the numbers.” Critique this

statement and give an example for which it does not hold true.

157. Why does a special order decision frequently ignore fixed overhead?

You decide

158. The managers of Computer World are trying to determine the best method of deciding the price of their new ultra

minicomputer. This computer will present the customers with several unique features that their other computers do not

offer. They have asked you to explain the advantages and disadvantages of the two costing methods they are considering;

markup costing and target costing.

Match each statement with the correct item below.

a.

the difference in total cost between the alternatives in a decision

b.

determine whether or not a segment should be kept or dropped

c.

limited resources and limited demand for each product

d.

a specific set of procedures that produces a decision

e.

the point at which products that have common processes and costs of production become distinguishable

f.

method of determining the cost of a product based on the price that customers are willing to pay

Chapter 13 – Short-Run Decision Making: Relevant Costing

g.

decisions involving a choice between internal and external production

h.

products that have common processes and costs of production up to a point

i.

past costs that cannot be affected by future decisions

j.

a percentage applied to the base cost to cover other costs plus profit

k.

determine whether a specially priced order should be accepted or rejected

l.

determine whether it is more profitable to process a joint product further

159. Decision model

160. Sunk costs

161. Differential cost

162. Joint products

163. Keep–or-drop decisions

164. Make-or–buy decisions

165. Sell-or-process-further decision

166. Special-order decisions

167. Split-off point

168. Constraints

169. Markup

170. Target costing