Chapter 13 – Short-Run Decision Making: Relevant Costing

1. The first step in making a short-run decision is to identify alternatives as possible solutions to the problem.

a.

True

b.

False

False

The first step in making a short-run decision is to define the problem.

2. In making a short-run decision, all alternatives need to be considered.

a.

True

b.

False

False

3. In short-run decision making, the alternative with the lowest overall cost is always chosen.

a.

True

b.

False

False

4. Irrelevant costs are costs that are the same for more than one alternative.

a.

True

b.

False

True

5. The benefit sacrificed when one alternative is chosen over another is called sunk cost.

a.

True

b.

False

False

The benefit sacrificed when one alternative is chosen over another is called opportunity cost.

6. Short-run decision making only involves short-run decisions that have nothing to do with the firm’s overall strategy.

a.

True

b.

False

False

7. A sunk cost is always relevant.

a.

True

b.

False

False

A sunk cost is never relevant.

8. Future costs that differ across alternatives are relevant costs.

a.

True

b.

False

9. Fixed costs are never relevant.

Chapter 13 – Short-Run Decision Making: Relevant Costing

a.

True

b.

False

False

10. Resources that are acquired in advance of usage are flexible resources.

a.

True

b.

False

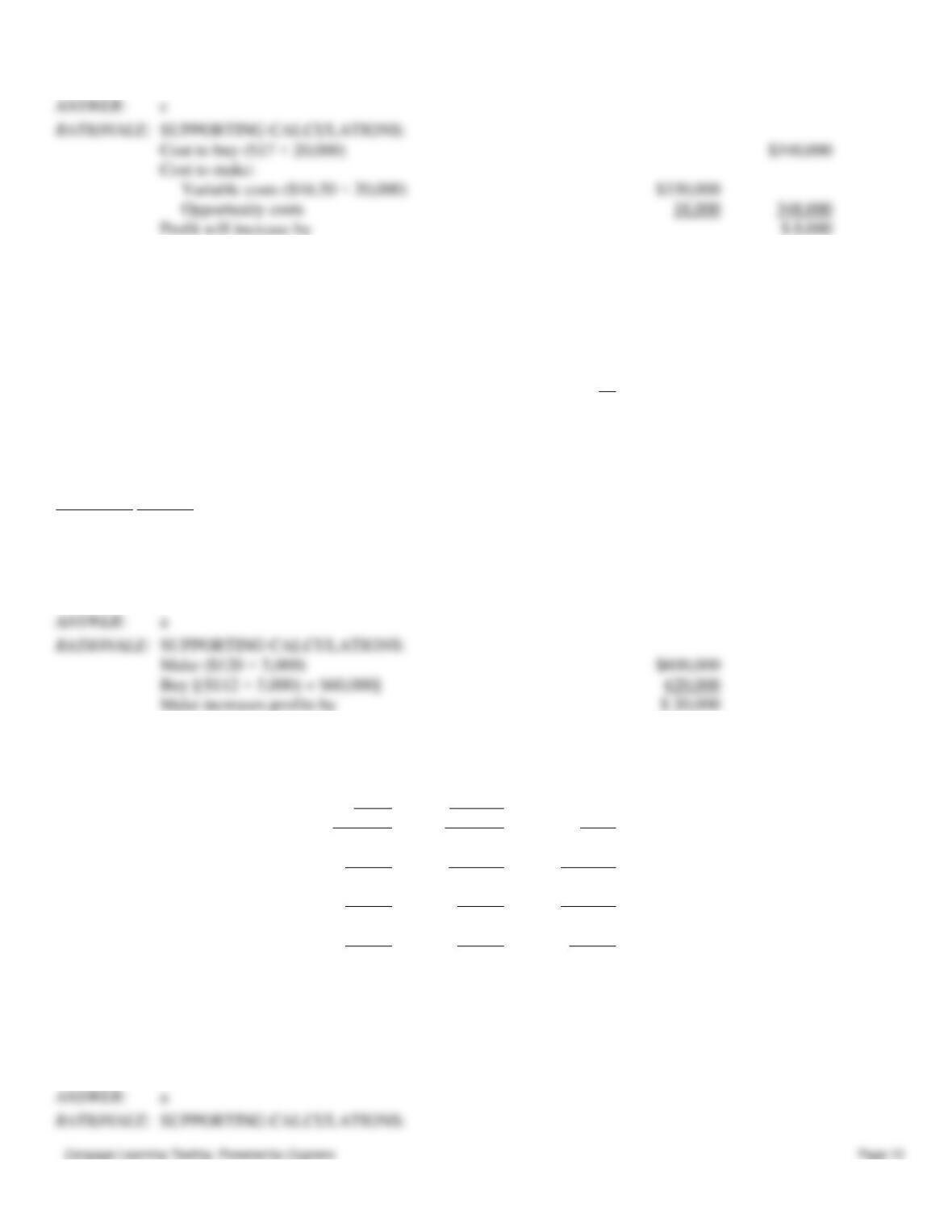

False

11. Flexible resources may have unused capacity.

a.

True

b.

False

False

12. A choice between internal and external production is a keep-or-drop decision.

a.

True

b.

False

False

A choice between internal and external production is a make-or-buy decision.

13. Typically in a special-order decision, a customer wants to pay more than the usual price.

a.

True

b.

False

False

Typically in a special-order decision, a customer wants to pay less than the usual price.

14. In keep-or-drop decisions, both the segment’s contribution margin and its segment margin are useful in evaluating the

performance of the segment.

a.

True

b.

False

True

15. A segment margin is always greater than or equal to zero.

a.

True

b.

False

False

16. At split-off, the joint costs of production for joint products are not relevant to the sell-or-process-further decision.

a.

True

b.

False

True

17. In deciding the optimal mix of products that use a constrained resource, it is important to determine the contribution

margin per unit of scarce resource.

a.

True

b.

False

Chapter 13 – Short-Run Decision Making: Relevant Costing

True

18. Linear programming is a special technique that can be used to determine the optimal product mix when there are

multiple constraints.

a.

True

b.

False

True

19. A situation in which management tells divisions that they must reduce costs by 10% is called target costing.

a.

True

b.

False

False

20. Bellair Company produces a product that has manufacturing cost of $30 per unit. Bellair’s policy is to charge a price

equal to cost plus 30%. The 30% is pure profit to Bellair.

a.

True

b.

False

False

21. In determining the target price of a good, the company must first determine the target cost and the desired profit.

a.

True

b.

False

False

22. Demand is one side of the pricing equation; supply is the other side.

a.

True

b.

False

True

23. The markup includes desired profit and any costs not included in the base cost.

a.

True

b.

False

True

24. Many companies start with cost to determine price since revenue must cover cost for the firm to make a profit.

a.

True

b.

False

True

25. A major advantage of markup pricing is that standard markups are easy to apply.

a.

True

b.

False

True

Chapter 13 – Short-Run Decision Making: Relevant Costing

26. Target costing is a method of determining the cost of a product or service based on the price (target price) that

customers are willing to pay.

a.

True

b.

False

True

27. Target costing involves much more up-front work than cost-based pricing.

a.

True

b.

False

True

28. Target costing can be used most effectively in the design and development stage of the product life cycle.

a.

True

b.

False

True

29. ____________________ consists of choosing among alternatives with an immediate or limited end in view.

30. A _________________ can be used to structure the decision maker’s thinking and to organize the information to make

a good decision.

31. The difference between the summed costs of two alternatives in a decision is known as the __________________.

32. _____________________ are simply those factors that are hard to put a number on, including things like political

pressure and product safety.

33. Most short-run decisions require extensive consideration of ___________.

34. If a future cost is the same for more than one alternative, and it has no effect on the decision is known as a(n)

_____________ cost.

irrelevant

35. In order to be classified as a _________________, a cost must possess these two characteristics: 1) they are future

costs and 2) they differ across alternatives.

36. The benefit sacrificed or foregone when one alternative is chosen over another is known as the

____________________.

37. A cost that cannot be affected by any future action is called a(n) _______________.

Chapter 13 – Short-Run Decision Making: Relevant Costing

38. A manager will make a __________________ when determining if a specially priced order should be accepted or

rejected.

special-order decision

39. Segmented reports are helpful for managers to make _______________ decisions.

40. The decision on whether to produce a product internally or purchase it from a supplier is an example of a

_______________.

41. __________________ have common processes and costs of production up to a split-off point.

Joint products

42. ______________ is the point at which products become distinguishable after passing through a common process.

Split-off point

43. _______________________ focus on whether a product should be processed beyond the split-off point.

44. Limited resources or a limited demand for a product are examples of ______________.

45. In the presence of multiple constraints the solution is considerably more complex than for one constraint and requires

a technique known as ____________________.

linear programming.

46. ________________ refers to the relative amount of each product manufactured by a company.

Product mix

47. The percentage that is applied to the base cost is known as the _____________.

48. A method of determining the cost of a product or service based on the price that customers are willing to pay is called

________________.

target costing.

49. Pasha Company produced 50 defective units last month at a unit manufacturing cost of $30. The defective units were

discovered before leaving the plant. Pasha can sell them “as is” for $20 or can rework them at a cost of $15 and sell them

at the regular price of $50. Which of the following is not relevant to the sell-or-rework decision?

a.

$15 for rework

b.

$20 selling price of defective units

c.

$30 manufacturing cost

d.

$50 regular selling price

e.

All of these are relevant.

50. Which of the following is not a step in the decision-making model?

a.

define the problem

Chapter 13 – Short-Run Decision Making: Relevant Costing

b.

identify alternatives

c.

consider qualitative factors

d.

total relevant costs and benefits for each alternative

e.

determine costs and benefits for both feasible and unfeasible alternatives

51. The act of choosing among alternatives with an immediate or limited end in view is termed

a.

assessing feasible alternative.

b.

strategic decision making.

c.

constructing a decision model.

d.

short-run decision making.

e.

None of these.

52. Future costs that differ across alternatives are

a.

opportunity costs.

b.

sunk costs.

c.

relevant costs.

d.

variable costs.

e.

product costs.

53. Depreciation of equipment is an example of a(n)

a.

relevant cost.

b.

opportunity cost.

c.

sunk cost.

d.

variable cost.

e.

None of these.

54. Resources that can be purchased in the amount needed and at the time of use are

a.

lumpy resources.

b.

flexible resources.

c.

committed resources.

d.

product resources.

e.

implicit resources.

55. A company is considering a special order for 1,000 units to be priced at $8.90 (the normal price would be $11.50). The

order would require specialized materials costing $4.00 per unit. Direct labor and variable factory overhead would cost

$2.15 per unit. Fixed factory overhead is $1.20 per unit. However, the company has excess capacity and acceptance of the

order would not raise total fixed factory overhead. The warehouse, however, would have to add capacity costing $1,300.

Which of the following is relevant to the special order?

a.

$11.50 normal selling price

b.

$1.20 fixed factory overhead per unit

Chapter 13 – Short-Run Decision Making: Relevant Costing

c.

$7.35 spent on donuts and coffee

d.

$8.90 selling price per unit of special order

e.

None of these.

56. Walloon Company produced 150 defective units last month at a unit manufacturing cost of $30. The defective units

were discovered before leaving the plant. Walloon can sell them as is for $20 or can rework them at a cost of $15 and sell

them at the regular price of $50. The total relevant cost of reworking the defective units is

a.

$4,500.

b.

$6,750.

c.

$7,500.

d.

$3,000.

e.

$2,250.

Cost of reworking the defective units = 150 × $15 = $2,250

57. An important qualitative factor to consider regarding a special order is the

a.

variable costs associated with the special order.

b.

avoidable fixed costs associated with the special order.

c.

effect the sale of special-order units will have on the sale of regularly priced units.

d.

incremental revenue from the special order.

c

58. Qualitative factors that should be considered when evaluating a make-or–buy decision are

a.

the quality of the outside supplier’s product.

b.

whether the outside supplier can provide the needed quantities.

c.

whether the outside supplier can provide the product when it is needed.

d.

All of these.

59. Abbott Company is considering purchasing a new machine to replace a machine purchased one year ago that is not

achieving the expected results. The following information is available:

Expected maintenance costs of new machine

$12,000 per year

Purchase price of existing machine

$150,000

Expected cost savings of new machine

$20,000 per year

Expected maintenance costs of existing machine

$8,000 per year

Resale value of existing machine

$35,000

Which of these items is irrelevant?

a.

Expected maintenance costs of new machine

b.

Purchase cost of existing machine

c.

Expected maintenance costs of existing machine

d.

Expected resale value of existing machine

Figure 13–1.

Fuller Company makes frames. A customer wants to place a special order for 600 frames in green with the company logo

Chapter 13 – Short-Run Decision Making: Relevant Costing

painted on the frame, to be priced at $40 each. Normally, Fuller would charge $90 per frame for this type of order. Fuller

figures that wood and glass will cost $16 per frame, variable overhead (machining, electricity) is $4 per frame, direct

labor is $12 per frame, and one setup will be required at $1,000 per setup. The set–up charge costs are 100% labor.

Currently, the workers needed to set up for and make the frames are working at Fuller. Their wages will be paid whether

or not the special order is accepted. Fuller’s policy is to avoid layoffs to the extent possible.

60. Refer to Figure 13–1. Which costs of the special order relate to flexible resources?

a.

wood and glass

b.

wood, glass, and variable overhead

c.

depreciation on machinery

d.

wood, glass, and direct labor

e.

wood, glass, direct labor, and setup labor

61. Refer to Figure 13–1. Which of the following is a qualitative factor that Fuller would consider in making the decision

to accept or reject the special order?

a.

cost of yarn and backing

b.

cost of setup labor

c.

the no-layoff policy

d.

the use of machinery

e.

the machining and electricity

62. Refer to Figure 13–1. Which of the following is irrelevant to the special order decision?

a.

cost of wood and glass

b.

direct labor cost

c.

machining and electricity cost

d.

$40 price

e.

All of these are relevant.

63. Refer to Figure 13–1. If Fuller accepts the special order, by how much will operating income increase or decrease?

a.

$14,400 increase

b.

$12,000 decrease

c.

$12,000 increase

d.

$21,600 increase

e.

There will be no effect on operating income.

Sales ($40 × 600)

Less: wood and glass ($16 × 600)

Variable overhead ($4 × 600)

Increase in operating income

64. Which of the following costs is not relevant to a decision to sell a product at split-off or process the product further

and then sell the product?

a.

joint costs allocated to the product

b.

the selling price of the product at split-off

Chapter 13 – Short-Run Decision Making: Relevant Costing

c.

the additional processing costs after split-off

d.

the selling price of the product after further processing

a

65. A decision involving a choice between internal and external production is what kind of decision?

a.

relevant

b.

keep-or-drop

c.

sell-or-process-further

d.

special-order

e.

make-or–buy

e

66. A decision that focuses on whether a specially priced order should be accepted or rejected is what kind of decision?

a.

relevant

b.

make-or–buy

c.

sell-or-process-further

d.

special-order

e.

keep-or-drop

67. A decision in which a manager needs to determine whether a product line (or segment) should continue or be

eliminated is what kind of decision?

a.

relevant

b.

make-or–buy

c.

sell-or-process-further

d.

special-order

e.

keep-or-drop

e

68. Piersall Company makes a variety of paper products. One product is 20 lb copier paper, packaged 5,000 sheets to a

box. One box normally sells for $18. A large bank offered to purchase 3,000 boxes at $14 per box. Costs per box are as

follows:

Direct materials

$8

Direct labor

3

Variable overhead

1

Fixed overhead

5

No variable marketing costs would be incurred on the order. The company is operating significantly below the maximum

productive capacity. No fixed costs are avoidable.

Should Piersall accept the order?

a.

Yes, income will increase by $6,000.

b.

Yes, income will increase by $9,000.

c.

No, income will decrease by $3,000.

d.

No, income will decrease by $6,000.

e.

It doesn’t matter; there will be no impact on income.

Chapter 13 – Short-Run Decision Making: Relevant Costing

69. Aerotoy Company makes toy airplanes. One plane is an excellent replica of a 737; it sells for $5. Vacation Airlines

wants to purchase 12,000 planes at $1.75 each to give to children flying unaccompanied. Costs per plane are as follows:

Direct materials

$1.00

Direct labor

0.50

Variable overhead

0.10

Fixed overhead

0.90

No variable marketing costs would be incurred. The company is operating significantly below the maximum productive

capacity. No fixed costs are avoidable. However, Vacation Airlines wants its own logo and colors on the planes. The cost

of the decals is $0.01 per plane and a special machine costing $1,500 would be required to affix the decals. After the order

is complete, the machine would be scrapped. Should the special order be accepted?

a.

Yes, income will increase by $300.

b.

No, income will decrease by $180.

c.

No, income will decrease by $1,500.

d.

Yes, income will increase by $180.

e.

It doesn’t matter; there will be no change in income.

Contribution margin [($1.75 − 1.61) ×12,000]

$1,680

Less: cost of special machine

1,500

Increased income

70. Foster Industries manufactures 20,000 components per year. The manufacturing cost of the components was

determined as follows:

Direct materials

$150,000

Direct labor

240,000

Inspecting products

60,000

Providing power

30,000

Providing supervision

40,000

Setting up equipment

60,000

Moving materials

20,000

Total

$600,000

If the component is not produced by Foster, inspection of products and provision of power costs will only be 10% of the

current production costs; moving materials costs and setting up equipment costs will only be 50% of the production costs;

and supervision costs will amount to only 40% of the production amount. An outside supplier has offered to sell the

component for $25.50.

What is the effect on income if Foster Industries purchases the component from the outside supplier?

a.

$25,000 increase

b.

$45,000 increase

c.

$90,000 decrease

d.

$90,000 increase

Make:

Direct materials

Direct labor

Chapter 13 – Short-Run Decision Making: Relevant Costing

71. Vest Industries manufactures 40,000 components per year. The manufacturing cost of the components was determined

as follows:

Direct materials

$ 75,000

Direct labor

120,000

Variable overhead

45,000

Fixed overhead

60,000

Total

$300,000

An outside supplier has offered to sell the component for $12.75. Fixed costs will remain the same if the component is

purchased from an outside supplier.

What is the effect on income if Vest Industries purchases the component from the outside supplier?

a.

$270,000 decrease

b.

$270,000 increase

c.

$30,000 decrease

d.

$30,000 increase

Make:

Direct materials

Direct labor

Variable overhead

Total

Buy:

Purchase price (40,000 × $12.75)

72. Vest Industries manufactures 40,000 components per year. The manufacturing cost of the components was determined

as follows:

Inspecting products (avoid 90%)

Providing power (avoid 90%)

Providing supervision (avoid 60%)

Setting up equipment (avoid 50%)

Moving materials (avoid 50%)

Total

Buy:

Purchase price (20,000 × $25.50)

Chapter 13 – Short-Run Decision Making: Relevant Costing

Direct materials

$ 75,000

Direct labor

120,000

Variable overhead

45,000

Fixed overhead

60,000

Total

$300,000

An outside supplier has offered to sell the component for $12.75. Fixed cost will remain the same if the component is

purchased from an outside supplier.

Vest Industries can rent its unused manufacturing facilities for $45,000 if it purchases the component from the outside

supplier.

What is the effect on income if Vest purchases the component from the outside supplier?

a.

$225,000 decrease

b.

$195,000 increase

c.

$165,000 decrease

d.

$135,000 increase

Make:

Direct materials

Direct labor

Variable overhead

Total

Buy:

Purchase price (40,000 × $12.75)

Rental income

45,000

Total

73. Miller Company produces speakers for home stereo units. The speakers are sold to retail stores for $30. Manufacturing

and other costs are as follows:

Variable costs per unit:

Fixed costs per month:

Direct materials

$ 9.00

Factory overhead

$120,000

Direct labor

4.50

Selling and admin.

60,000

Factory overhead

3.00

Total

$180,000

Distribution

1.50

Total

$18.00

The variable distribution costs are for transportation to the retail stores. The current production and sales volume is 20,000

per year. Capacity is 25,000 units per year.

A Tennessee manufacturing firm has offered a one-year contract to supply speakers at a cost of $17.00 per unit. If Miller

Company accepts the offer, it will be able to rent unused space to an outside firm for $18,000 per year. All other

information remains the same as the original data. What is the effect on profits if Miller Company buys from the

Tennessee firm?

a.

decrease of $8,000

b.

increase of $9,000

c.

increase of $8,000

d.

decrease of $6,000

Chapter 13 – Short-Run Decision Making: Relevant Costing

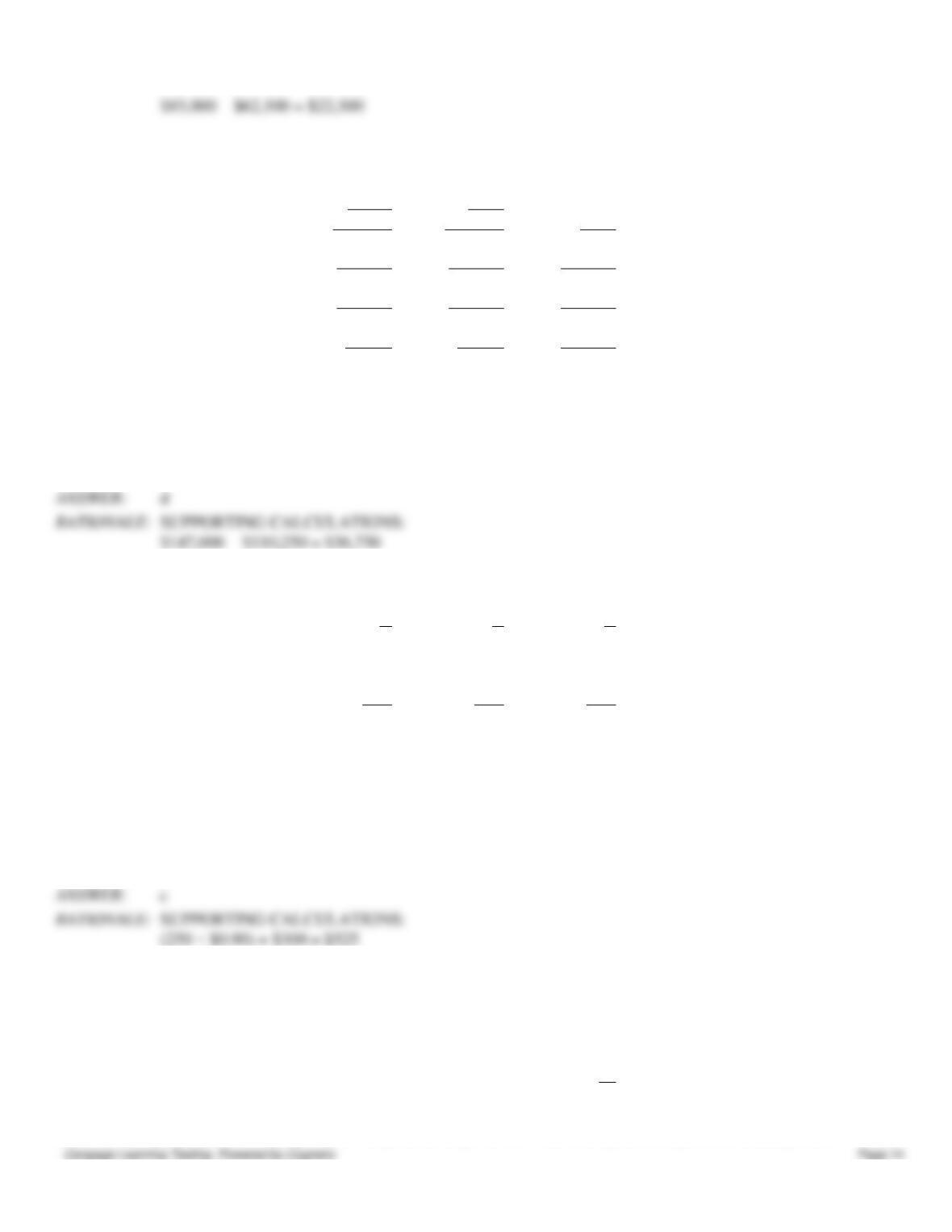

Cost to buy ($17 × 20,000)

$340,000

Cost to make:

Variable costs ($16.50 × 20,000)

$330,000

Profit will increase by

74. Houston Corporation manufactures a part for its production cycle. The costs per unit for 5,000 units of this part are as

follows:

Direct materials

$ 32

Direct labor

40

Variable overhead

16

Fixed overhead

32

Total

$120

Johnson Company has offered to sell Houston Corporation 5,000 units of the part for $112 per unit. If Houston

Corporation accepts Johnson Company’s offer, total fixed costs will be reduced to $60,000. What alternative is more

desirable and by what amount is it more desirable?

Alternative Amount

a.

Make $ 20,000

b.

Make $120,000

c.

Buy $ 40,000

d.

Buy $100,000

Make ($120 × 5,000)

$600,000

Buy [($112 × 5,000) + $60,000]

620,000

Make increases profits by

$ 20,000

75. The operations of Smits Corporation are divided into the Child Division and the Jackson Division. Projections for the

next year are as follows:

Child

Jackson

Division

Division

Total

Sales revenue

$250,000

$180,000

$430,000

Variable expenses

90,000

100,000

190,000

Contribution margin

$160,000

$ 80,000

$240,000

Direct fixed expenses

75,000

62,500

137,500

Segment margin

$ 85,000

$ 17,500

$102,500

Allocated common costs

35,000

27,500

62,500

Total relevant benefit (loss)

$ 50,000

$(10,000)

$ 40,000

Operating income for Smits Corporation as a whole if the Jackson Division were dropped would be

a.

$22,500.

b.

$40,000.

c.

$50,000.

d.

$60,000.

SUPPORTING CALCULATIONS:

Chapter 13 – Short-Run Decision Making: Relevant Costing

$85,000 − $62,500 = $22,500

76. The operations of Knickers Corporation are divided into the Pacers Division and the Bulls Division. Projections for

the next year are as follows:

Pacers

Bulls

Division

Division

Total

Sales revenue

$420,000

$252,000

$672,000

Variable expenses

147,000

115,500

262,500

Contribution margin

$273,000

$136,500

$409,500

Direct fixed expenses

126,000

105,000

231,000

Segment margin

$147,000

$ 31,500

$178,500

Allocated common costs

63,000

47,250

110,250

Total relevant benefit (loss)

$ 84,000

$(15,750)

$ 68,250

Operating income for Knickers Corporation as a whole if the Bulls Division were dropped would be

a.

$99,750.

b.

$84,000.

c.

$68,250.

d.

$36,750.

77. The following information pertains to Dodge Company’s three products:

A

B

C

Unit sales per year

250

400

250

Selling price per unit

$9.00

$12.00

$ 9.00

Variable costs per unit

3.60

9.00

9.90

Unit contribution margin

$5.40

$ 3.00

$(0.90)

Contribution margin ratio

60%

25%

(10)%

Assume that product C is discontinued and the extra space is rented for $300 per month. All other information remains the

same as the original data. Annual profits will

a.

increase by $75.

b.

decrease by $75.

c.

increase by $525.

d.

remain the same.

78. The following information relates to a product produced by Creamer Company:

Direct materials

$24

Direct labor

15

Variable overhead

30

Fixed overhead

18

Unit cost

$87

Fixed selling costs are $500,000 per year, and variable selling costs are $12 per unit sold. Although production capacity is

600,000 units per year, the company expects to produce only 400,000 units next year. The product normally sells for $120

Chapter 13 – Short-Run Decision Making: Relevant Costing

each. A customer has offered to buy 60,000 units for $90 each.

The incremental cost per unit associated with the special order is

a.

$84.

b.

$81.

c.

$69.

d.

$64.

Direct materials

$24

Direct labor

15

Variable overhead

30

Variable selling

12

$81

79. Meco Company produces a product that has a regular selling price of $360 per unit. At a typical monthly production

volume of 2,000 units, the product’s average unit cost of goods sold amounts to $270. Included in this average is $120,000

of fixed manufacturing costs. All selling and administrative costs are fixed and amount to $30,000 per month.

Meco Company has just received a special order for 1,000 units at $240 per unit. The buyer will pay transportation, and

the regular selling price will not be affected if Meco accepts the order.

Assuming Meco Company has excess capacity, the effect on profits of accepting the order would be

a.

$60,000 increase.

b.

$60,000 decrease.

c.

$30,000 increase.

d.

$30,000 decrease.

80. The following information relates to a product produced by Creamer Company:

Direct materials

$24

Direct labor

15

Variable overhead

30

Fixed overhead

18

Unit cost

$87

Fixed selling costs are $500,000 per year, and variable selling costs are $12 per unit sold. Although production capacity is

600,000 units per year, the company expects to produce only 400,000 units next year. The product normally sells for $120

each. A customer has offered to buy 60,000 units for $90 each.

If the firm produces the special order, the effect on income would be a

a.

$360,000 increase.

b.

$360,000 decrease.

c.

$540,000 increase.

d.

$540,000 decrease.

SUPPORTING CALCULATIONS:

Chapter 13 – Short-Run Decision Making: Relevant Costing

81. Gundy Company manufactures a product with the following costs per unit at the expected production of 30,000 units:

Direct materials

$ 4

Direct labor

12

Variable overhead

6

Fixed overhead

8

The company has the capacity to produce 30,000 units. The product regularly sells for $40. A wholesaler has offered to

pay $32 per unit for 2,000 units.

If the firm chooses to accept the special order and reject some regular sales, the effect on operating income would be

a.

a $20,000 increase.

b.

a $16,000 decrease.

c.

a $4,000 increase.

d.

$-0-.

82. Walton Company manufactures a product with the following costs per unit at the expected production level of 84,000

units:

Direct materials

$12

Direct labor

36

Variable overhead

18

Fixed overhead

24

The company has the capacity to produce 90,000 units. The product regularly sells for $120. A wholesaler has offered to

pay $110 per unit for 7,500 units. If the special order is accepted, the effect on operating income would be a

a.

$75,000 decrease.

b.

$429,000 increase.

c.

$495,000 increase.

d.

$249,000 increase.

Incremental revenue (7,500 × $110)

Lost revenue from regular sales (1,500 × $120)

Incremental costs:

Direct materials (6,000 × $12)

Direct labor (6,000 × $36)

Variable overhead (6,000 × $18)

Incremental profit

83. Rose Manufacturing Company had the following unit costs:

Direct materials

$24

Direct labor

8

Incremental revenue (60,000 × $90)

Less: Incremental costs (60,000 × $81)

Incremental profit

Chapter 13 – Short-Run Decision Making: Relevant Costing

Variable overhead

10

Fixed overhead (allocated)

18

A one-time customer has offered to buy 2,000 units at a special price of $48 per unit. Assuming that sufficient unused

production capacity exists to produce the order and no regular customers will be affected by the order, how much

additional profit or loss will be generated by accepting the special order?

a.

$12,000 profit

b.

$96,000 profit

c.

$84,000 loss

d.

$24,000 loss

84. Reggie Corporation manufactures a single product with the following unit costs for 1,000 units:

Direct materials

$2,400

Direct labor

960

Overhead (30% variable)

1,800

Selling expenses (50% variable)

900

Administrative expenses (10% variable)

840

Total per unit

$6,900

Recently, a company approached Reggie Corporation about buying 100 units for $5,100 each. Currently, the models are

sold to dealers for $7,800. Reggie Corporation’s capacity is sufficient to produce the extra 100 units. No additional selling

expenses would be incurred on the special order.

How much will income change if the special order is accepted?

a.

increase by $398,400

b.

decrease by $180,000

c.

increase by $111,600

d.

no change

85. Boone Products had the following unit costs:

Direct materials

$24

Direct labor

10

Variable overhead

8

Fixed factory (allocated)

18

A one-time customer has offered to buy 2,000 units at a special price of $48 per unit. Because of capacity constraints,

1,000 units will need to be produced during overtime. Overtime premium is $8 per unit. How much additional profit or

loss will be generated by accepting the special order?

a.

$30,000 loss

b.

$4,000 loss

c.

$24,000 loss

d.

$4,000 profit

SUPPORTING CALCULATIONS:

Chapter 13 – Short-Run Decision Making: Relevant Costing

86. Stars Manufacturing Company produces Products A1, B2, C3, and D4 through a joint process. The joint costs amount

to $200,000.

If Processed Further

Units

Sales Value

Additional

Sales

Product

Produced

at Split-Off

Costs

Value

A1

3,000

$10,000

$2,500

$15,000

B2

5,000

30,000

3,000

35,000

C3

4,000

20,000

4,000

25,000

D4

6,000

40,000

6,000

45,000

If Product B2 is processed further, profits will

a.

increase by $30,000.

b.

decrease by $3,000.

c.

increase by $32,000.

d.

increase by $2,000.

87. Manning Company uses a joint process to produce products W, X, Y, and Z. Each product may be sold at its split-off

point or processed further. Additional processing costs of specific products are entirely variable. Joint processing costs for

a single batch of joint products are $120,000. Other relevant data are as follows:

Additional

Product

Sales Value

at Split-Off

Processing

Costs

Sales Value of

Final Product

W

$ 40,000

$ 60,000

$ 80,000

X

$ 12,000

$ 4,000

$ 20,000

Y

$ 20,000

$ 32,000

$120,000

Z

$ 28,000

$ 20,000

$ 32,000

$100,000

$116,000

$252,000

Which products should Manning process further?

a.

All.

b.

All except Z.

c.

Y and X.

d.

None.

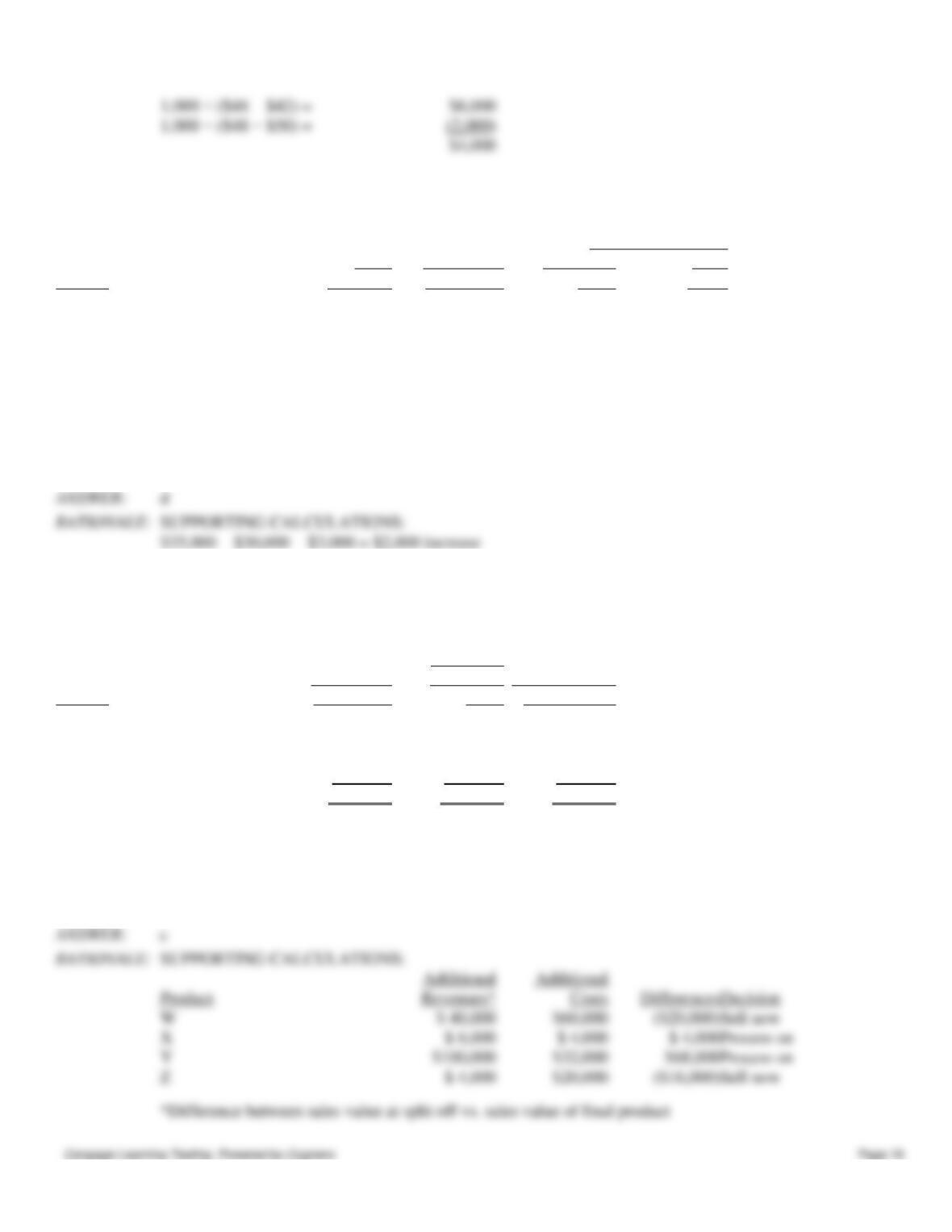

Additional

Additional

Product

Costs

Decision

$ 40,000

$60,000

Sell now

$ 8,000

$ 4,000

$ 4,000

Process on

$100,000

$32,000

$68,000

Process on

*Difference between sales value at split off vs. sales value of final product

1,000 × ($48 − $42) =

$6,000

1,000 × ($48 − $50) =

$4,000

Chapter 13 – Short-Run Decision Making: Relevant Costing

88. Information about three joint products follows:

A

B

C

Anticipated production

5,000 lbs.

1,000 lbs.

2,000 lbs.

Selling price/lb. at split-off

$10

$30

$16

Additional processing costs/lb. after split-off

(all variable)

$6

$12

$24

Selling price/lb. after further processing

$20

$40

$50

The cost of the joint process is $60,000. Which of the joint products should be sold at split-off?

a.

A.

b.

B.

c.

C.

d.

Both A and B.

Split-Off

Process Further

$10

$20 − $6 = $14

$30

$40 − $12 = $28

*Sell now

$16

$50 − $24 = $26

89. Information about three joint products follows:

X

Y

Z

Anticipated production

12,000 lbs.

8,000 lbs.

7,000 lbs.

Selling price/lb. at split-off

$16

$26

$48

Additional processing costs/lb. after split-off

(all variable)

$8

$20

$20

Selling price/lb. after further processing

$20

$40

$70

The cost of the joint process is $140,000. Which of the joint products should be processed further?

a.

X.

b.

Y.

c.

Z.

d.

Both X and Y.

Split-Off

Process Further

$16

$20 − $8 = $12

$26

$40 − $20 = $20

$48

$70 − $20 = $50

*Process on

Figure 13–2.

ColorPro uses part 87A in the production of color printers. Unit manufacturing costs for part 87A are:

Direct materials

$8

Direct labor

2

Variable overhead

1

Fixed overhead

4

ColorPro uses 100,000 units of 87A per year. Filbert Company has offered to sell ColorPro 100,000 units of 87A per year

for $12. Fixed overhead is unavoidable.

90. Refer to Figure 13–2. Should ColorPro make or buy the part?

Chapter 13 – Short-Run Decision Making: Relevant Costing

a.

Make the part because it will save $100,000 over buying it.

b.

Buy the part because it will save $100,000 over making it.

c.

Make the part because it will save $1,100,000 over buying it.

d.

Buy the part because it will save 1,100,000 over making it.

e.

Buy the part because it will save $300,000 over making it.

Direct materials

Direct labor

Variable overhead

Purchase price

Total relevant costs

91. Refer to Figure 13–2. Now suppose that ColorPro discovers that other costs will increase by $7,000 per year if the

component is purchased rather than made internally. Should ColorPro make or buy the part?

a.

Make the part because it will save $100,000 over buying it.

b.

Buy the part because it will save $100,000 over making it.

c.

Make the part because it will save $107,000 over buying it.

d.

Buy the part because it will save $107,000 over making it.

e.

Make the part because it will save $10,000 over buying it.

Direct materials

Direct labor

Variable overhead

Purchase price

Materials handling cost

Total costs

92. Refer to Figure 13–2. Which of the following is a qualitative factor that might affect ColorPro’s decision?

a.

Filbert has an outstanding reputation for quality.

b.

Ordering from Filbert would give ColorPro a chance to see how well Filbert could meet JIT standards for

ColorPro’s other products.

c.

Filbert is known for the reliability of its products.

d.

Making the part in-house would help ColorPro avoid layoffs of direct and indirect labor.

e.

All of these.

Figure 13–6.

Autry Company manufactures veterinary products. One joint process involves refining a chemical (dactylyte) into two

chemicals − dac and tyl. One batch of 5,000 gallons of dactylyte can be converted to 2,000 gallons of dac and 3,000

gallons of tyl at a total joint processing cost of $12,000. At the split-off point, dac can be sold for $3 per gallon and tyl can

be sold for $4 per gallon. Autry has just learned of a new process to convert dac into prodac. The new process costs

$4,000 and yields 1,700 gallons of prodac for every 2,000 gallons of dac. Prodac sells for $5 per gallon.

93. Refer to Figure 13–6. What is Autry’s profit from refining one batch of dactylyte if both dac and tyl are sold at the