Table 13-3

Quantity

Price

(dollars)

Total Revenue

(dollars)

Total Variable

Cost

(dollars)

Total Cost

(dollars)

0

$21

$0

$0

$50

1

20

20

16

66

2

19

38

31

81

3

18

54

45

95

4

17

68

59

109

5

16

80

75

125

6

15

90

93

143

7

14

98

112

162

8

13

104

140

190

9

12

108

180

230

10

11

110

230

280

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

17) Refer to Table 13-3. What are the profit-maximizing/loss-minimizing output level and price?

A) Q=0 (firm should not produce)

B) Q=3; P=$18

C) Q=4; P=$17

D) Q=5; P=$16

18) Refer to Table 13-3. What is the amount of the firm’s loss at its optimal output level?

A) $0

B) $41

C) $45

D) $50

19) Refer to Table 13-3. What is its average variable cost of production at its optimal output

level?

A) $0 (because its optimal output =0)

B) $15

C) $14.75

D) $29

20) Refer to Table 13-3. What is the best course of action for the firm in the short run?

A) It should shut down.

B) It should stay in business because it covers some of its fixed cost.

C) It should increase its sales by lowering its price.

D) It should not cut its price but it should increase its sales by advertising.

21) Refer to Table 13-3. If this firm continues to produce, what is likely to happen to the

product’s price in the long run?

A) It will fall.

B) It will increase

C) It will remain constant.

D) It cannot be determined without information on its long run demand curve.

22) Assume price exceeds average variable cost over the relevant range of demand. If a

monopolistically competitive firm is producing at an output where marginal revenue is $23 and

marginal cost is $19, then to maximize profits the firm should

A) continue to produce the same quantity.

B) increase output.

C) decrease output.

D) shutdown.

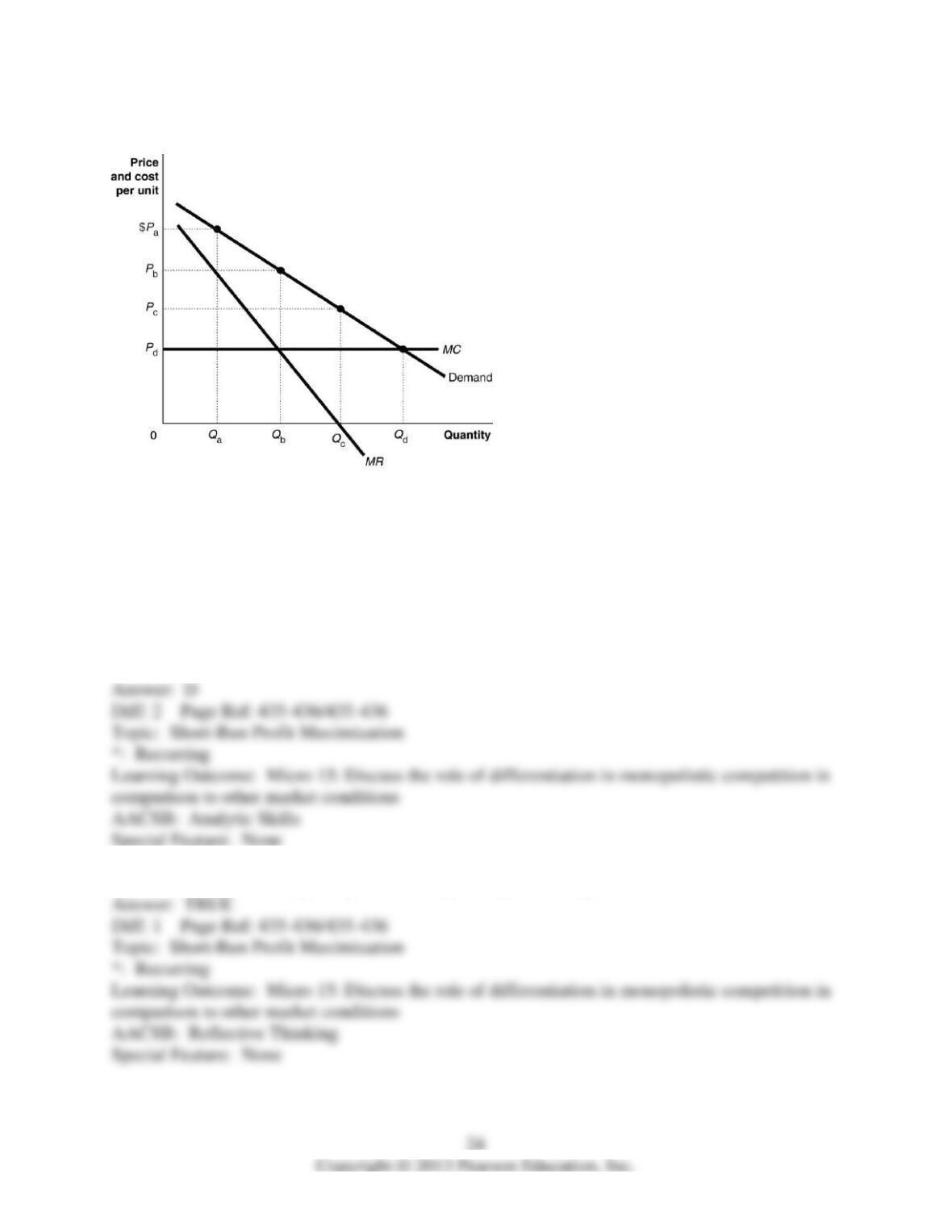

Figure 13-4

23) Refer to Figure 13-4. The candy store represented in the diagram is currently selling Qa

units of candy at a price of Pa. Is this candy store maximizing its profit and if it is not, what

would you recommend to the firm?

A) Yes, it is maximizing its profit by charging the highest price possible.

B) No, it is not; since its marginal cost is constant, it should produce and sell as much candy as it

can. It should sell Qd units at a price of Pd.

C) No, it is not; it should lower its price to Pc and sell Qc units.

D) No, it is not; it should lower its price to Pb and sell Qb units.

24) For a monopolistically competitive firm, price equals average revenue.

25) For a profit-maximizing monopolistically competitive firm, for the last unit sold, the

marginal cost of production is less than the marginal benefit received by a customer from the

purchase of that unit.

26) Consumers in a monopolistically competitive market do not receive any consumer surplus

because the price paid for the product exceeds the marginal cost of production.

27) Assume that price exceeds average variable cost over the relevant range of demand. If a

monopolistically competitive firm is producing at an output where marginal revenue is $111.11

and marginal cost is $118, then to maximize profits the firm should increase its output.

28) Arturo runs a Taco Bell franchise. He is selling 250 Gordita Supremes per week at a price of

$2.75. If he lowers the price to $2.70, he will sell 251 Gordita Supremes. What is the marginal

revenue of the 251st Gordita Supreme? If selling the extra Gordita Supreme adds $0.20 to

Arturo’s costs, what will be the effect on his profit from selling 251 Gordita Supremes instead of

250?

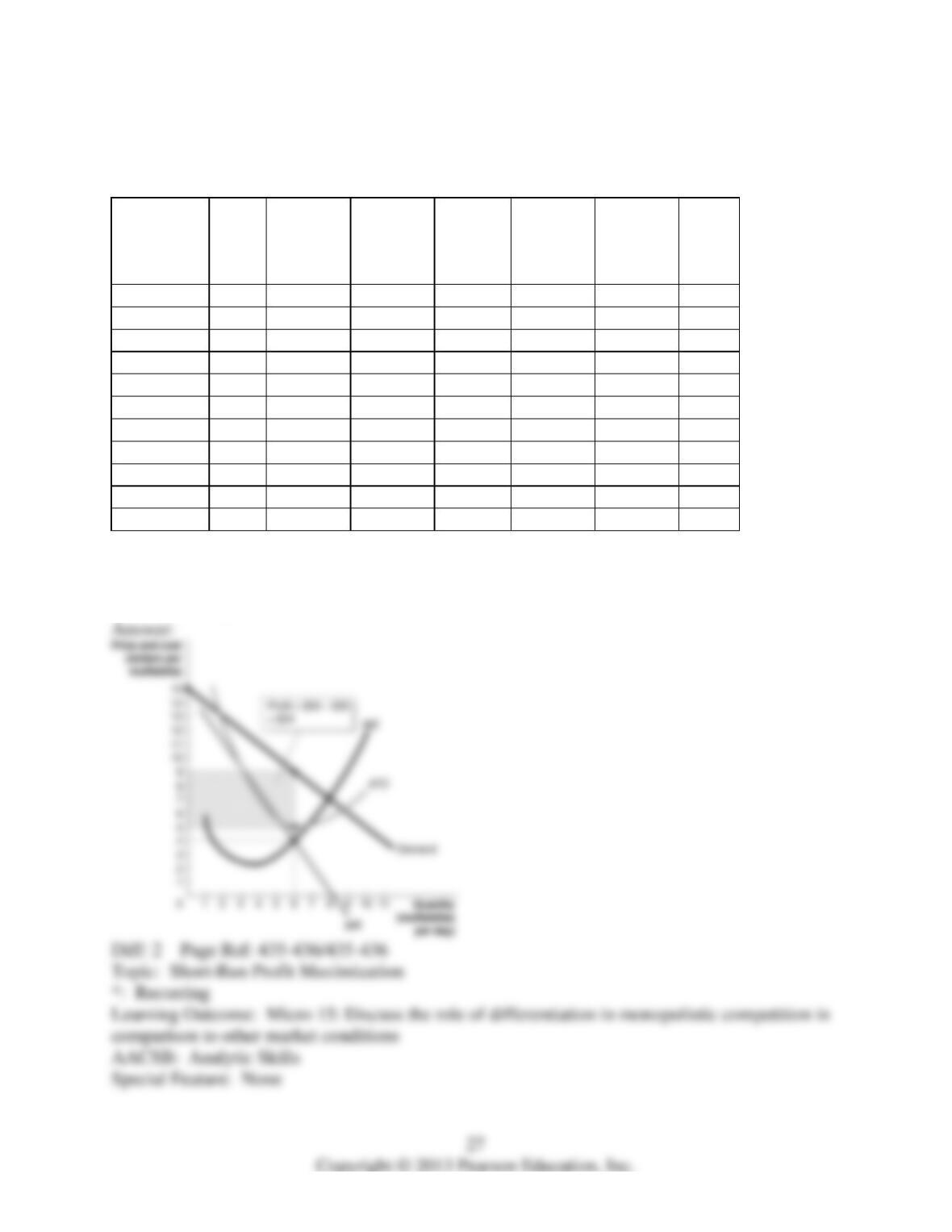

29) Central Grocery in New Orleans is famous for its muffaletta, a large round sandwich filled

with deli meats and topped with a tangy olive salad. Suppose the following table represents cost

and revenue data for Central Grocery.

Muffalettas

Sold per

Day

Price

(P)

Total

Revenue

(TR)

Marginal

Revenue

(MR)

Total

Cost

(TC)

Marginal

Cost (MC)

Average

Total

Cost

(ATC)

Profit

0

$15

$0

—

$12

—

—

-$12

1

14

14

$14

18

$6

$18.00

-4

2

13

26

12

20

2

10.00

6

3

12

36

10

21

1

7.00

15

4

11

44

8

23

2

5.75

21

5

10

50

6

26

3

5.20

24

6

9

54

4

30

4

5.00

24

7

8

56

2

35

5

5.00

21

8

7

56

0

42

7

5.25

14

9

6

54

-2

52

10

5.70

2

10

5

50

-4

78

16

7.80

-28

Illustrate this data by graphing the demand, MR, MC, and ATC curves. Identify the profit-

maximizing price and quantity, and show the area representing the total profit received by

Central Grocery.

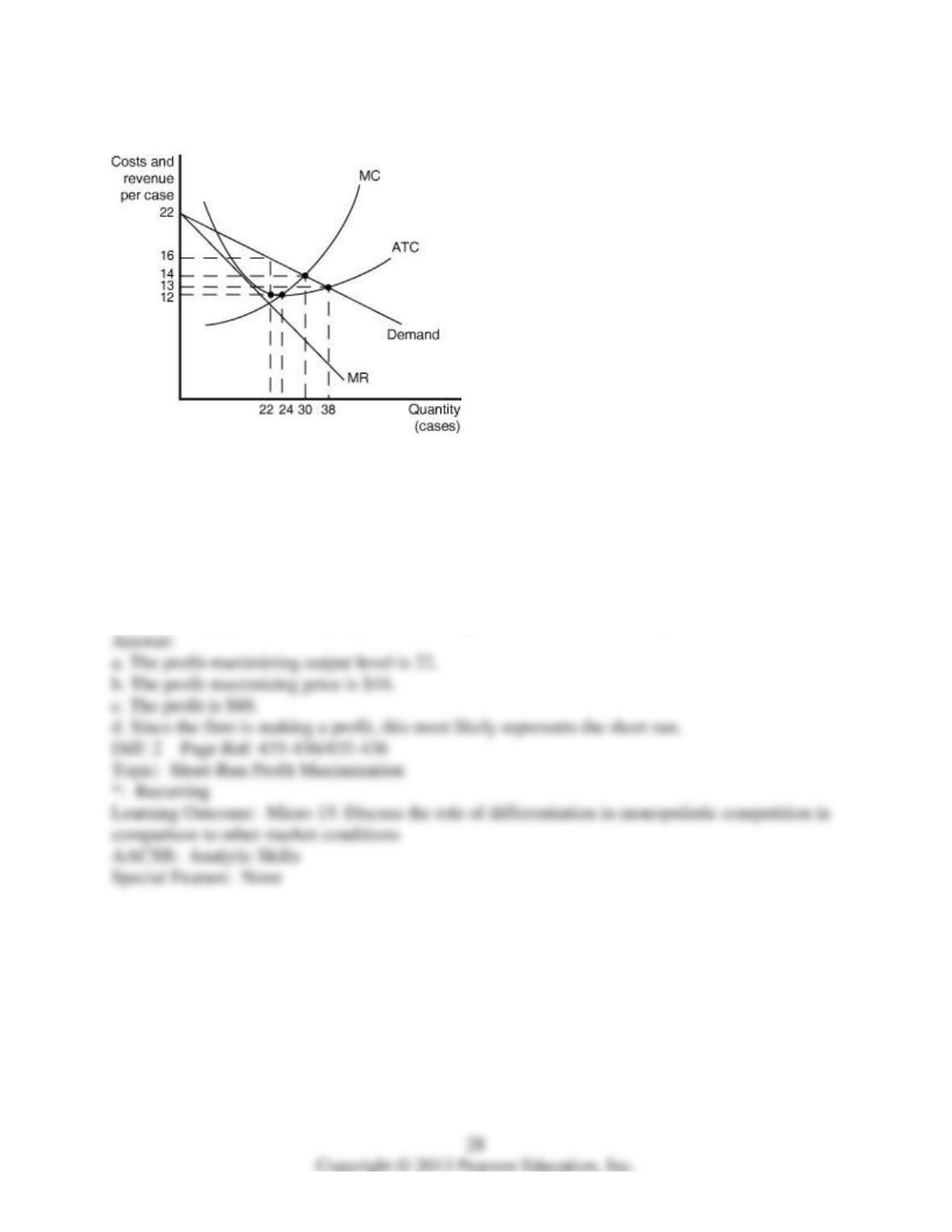

Figure 13-5

Figure 13-5 shows cost and demand curves for a monopolistically competitive producer of iced-

tea.

30) Refer to Figure 13-5. to answer the following questions.

a. What is the profit-maximizing output level?

b. What is the profit-maximizing price?

c. At the profit-maximizing output level, how much profit will be realized?

d. Does this graph most likely represent the long run or the short run? Why?

13.3 What Happens to Profits in the Long Run?

1) A monopolistically competitive industry that earns economic profits in the short run will

A) continue to earn economic profits in the long run.

B) experience the entry of new rival firms into the industry in the long run.

C) experience the exit of existing firms out of the industry in the long run.

D) experience a rise in demand in the long run.

2) In the long run, if price is less than average cost,

A) there is an incentive for firms to exit the market.

B) there is profit incentive for firms to enter the market.

C) the market must be in long-run equilibrium.

D) there is no incentive for the number of firms in the market to change.

3) A monopolistically competitive firm that is earning profits will, in the long run, experience all

of the following except

A) new rivals entering the market.

B) a decrease in demand for its product.

C) demand for the firm’s product becomes more elastic.

D) a decrease in the number of rival products.

4) Assuming that the total market size remains constant, a monopolistically competitive firm

earning profits in the short run will find the demand for its product decreasing in the long run

because

A) new entrants into the market are more likely to have cutting edge products.

B) as the firm raises its price in the long run, it will lose some customers to new entrants in the

market.

C) some of its customers have switched to purchasing the products of new entrants in the market.

D) its costs of production rises.

5) You are planning to open a new Italian restaurant in your hometown where there are three

other Italian restaurants. You plan to distinguish your restaurant from your competitors by

offering northern Italian cuisine and using locally grown organic produce. What is likely to

happen in the restaurant market in your hometown after you open?

A) Your competitors are likely to change their menus to make their products more similar to

yours.

B) The demand curve facing each restaurant owner shifts to the right.

C) The demand curve facing each restaurant owner becomes more elastic.

D) While the demand curves facing your competitors becomes more elastic, your demand curve

will be inelastic.

6) You have just opened a new Italian restaurant in your hometown where there are three other

Italian restaurants. Your restaurant is doing a brisk business and you attribute your success to

your distinctive northern Italian cuisine using locally grown organic produce. What is likely to

happen to your business in the long run?

A) Your competitors are likely to change their menus to make their products more similar to

yours.

B) Your success will invite others to open competing restaurants and ultimately your profits will

be driven to zero.

C) If your success continues, you will be likely to establish a franchise and expand your market

size.

D) If you continue to maintain consistent quality, you will be able to earn profits indefinitely.

7) A monopolistically competitive firm earning profits in the short run will find the demand for

its product decreasing and becoming more elastic in the long run as new firms move into the

industry until

A) the original firm is driven into bankruptcy.

B) the firm’s demand curve is perfectly elastic.

C) the firm’s demand curve is tangent to its average total cost curve.

D) the firm exits the market.

8) In the long run, what happens to the demand curve facing a monopolistically competitive firm

that is earning short-run profits?

A) The demand curve will shift to the left and became more elastic.

B) The demand curve will shift to the left and became less elastic.

C) The demand curve will shift to the right and became more elastic.

D) The demand curve will shift to the right and became less elastic.

9) If a typical monopolistically competitive firm is making short-run losses, then

A) other more competitive firms will enter the market.

B) as some firms leave, the remaining firms will experience an increase in the demand for their

products.

C) as some firms leave, the demand for the products of the remaining firms will become more

elastic.

D) the industry will eventually cease to exist.

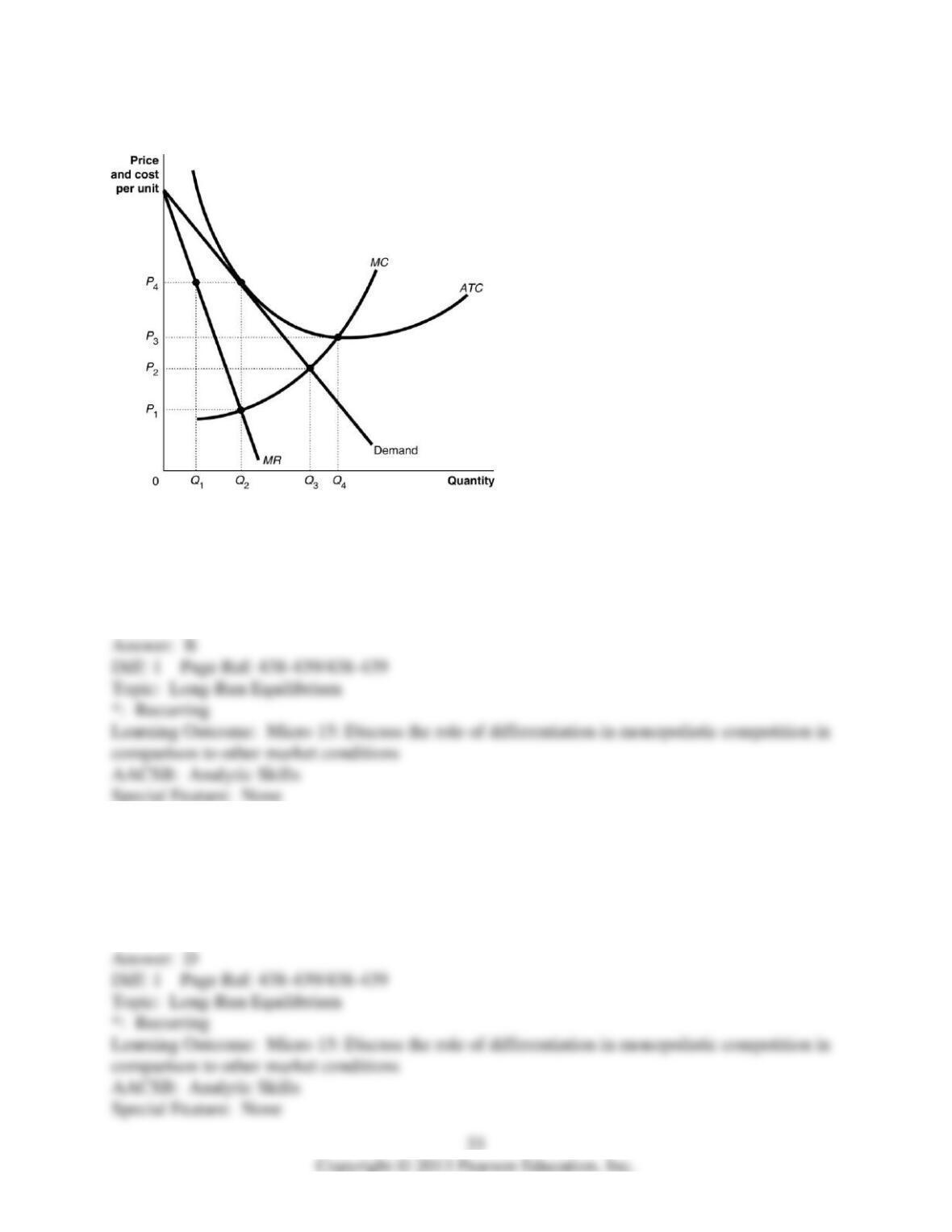

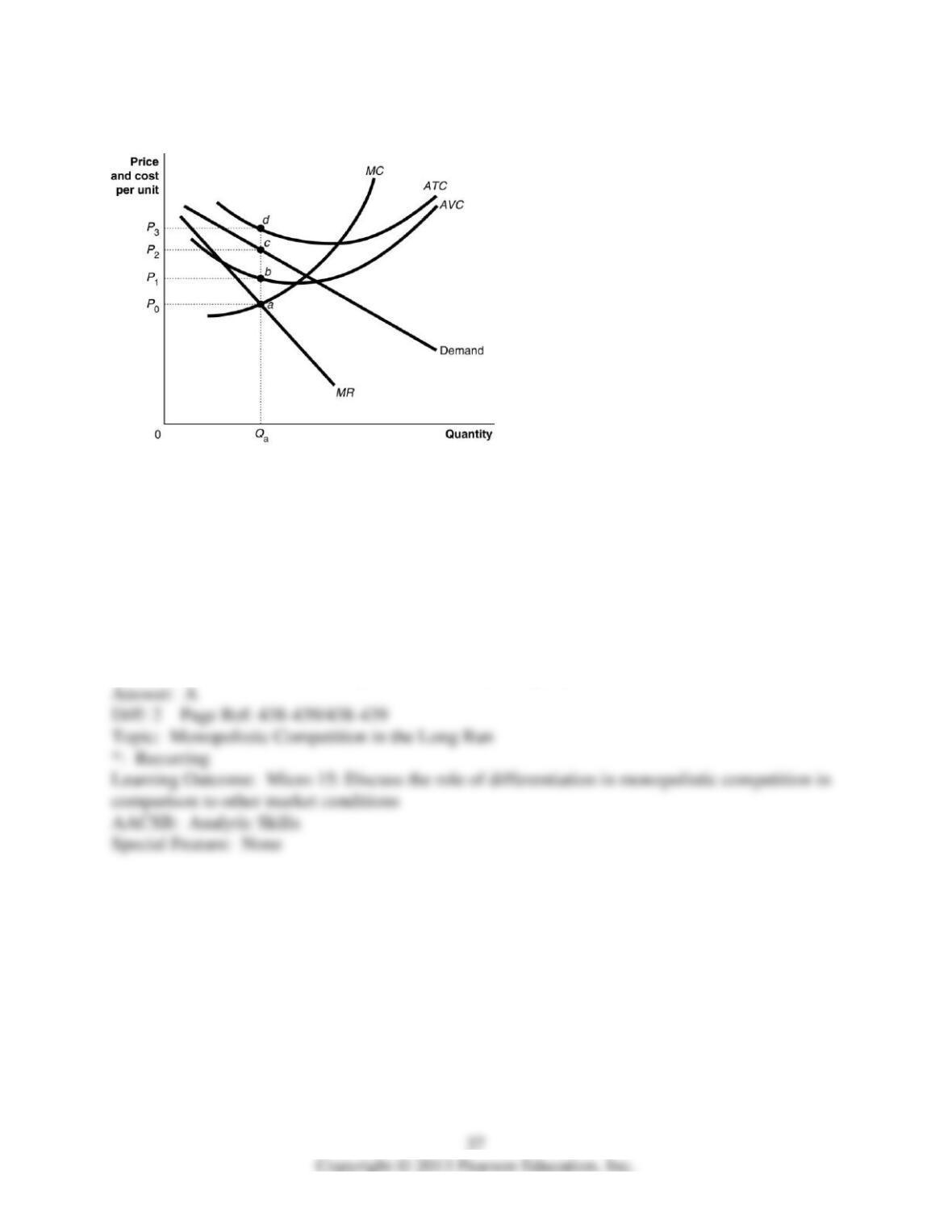

Figure 13-6

10) Refer to Figure 13-6. What is the monopolistic competitor’s profit maximizing output?

A) Q1 units

B) Q2 units

C) Q3 units

D) Q4 units

11) Refer to Figure 13-6. What is the monopolistic competitor’s profit maximizing price?

A) P1

B) P2

C) P3

D) P4

12) Refer to Figure 13-6. The firm represented in the diagram

A) makes zero economic profit.

B) makes zero accounting profit.

C) should exit the industry.

D) should expand its output to take advantage of economies of scale.

13) Refer to Figure 13-6. What is the productively efficient output for the firm represented in

the diagram?

A) Q1 units

B) Q2 units

C) Q3 units

D) Q4 units

14) Refer to Figure 13-6. What is the allocatively efficient output for the firm represented in the

diagram?

A) Q1 units

B) Q2 units

C) Q3 units

D) Q4 units

15) Refer to Figure 13-6. The diagram depicts a firm

A) in a constant cost industry.

B) in an increasing cost industry.

C) in long run equilibrium.

D) that is making short run losses.

16) Refer to Figure 13-6. What is the amount of excess capacity?

A) Q4 – Q3 units

B) Q4 – Q2 units

C) Q3 – Q2 units

D) Q3 – Q1 units

17) Why do most firms in monopolistic competition typically make zero profit in the long run?

A) because firms produce differentiated products

B) because the lack of entry barriers would compete away profits

C) because firms do not produce at their minimum efficient scale

D) because the total market is not large enough to accommodate so many firms

18) If a monopolistically competitive firm breaks even, the firm

A) is earning an accounting profit and will have to pay taxes on that profit.

B) is earning zero accounting and zero economic profit.

C) should advertise its product to stimulate demand.

D) should expand production.

Figure 13-7

Figure 13-7 shows short-run cost and demand curves for a monopolistically competitive firm in

the market for designer watches.

19) Refer to Figure 13-7. If the diagram represents a typical firm in the designer watch market,

what is likely to happen in the long run?

A) Some firms will exit the market causing the demand to increase for firms remaining in the

market.

B) The firms that are making losses will be purchased by their more successful rivals.

C) Inefficient firms will exit the market and new cost efficient firms will enter the market.

D) Firms will have to raise their prices to cover costs of production.

20) Firms such as Caribou Coffee and Diedrich Coffee operate hundreds of coffeehouses

nationwide while firms such as Dunn Brothers Coffee operate only in four states. How would

you characterize these stores?

A) Caribou Coffee and Diedrich Coffee are oligopolists while Dunn Brothers is a monopolistic

competitor.

B) Caribou Coffee and Diedrich Coffee are duopolists while Dunn Brothers is a monopolistic

competitor.

C) Caribou Coffee and Diedrich Coffee are duopolists while Dunn Brothers is an oligopolist

D) They are all monopolistic competitors.

21) According to a Wall Street Journal article, hhgregg has differentiated itself from its

competition, particularly from large chain stores such as Best Buy,

A) by charging lower prices.

B) by providing better customer service.

C) by selling inferior products.

D) by offering discounts for cash sales.

22) The financial situation at Starbucks in the late 2000s illustrates the fact that maintaining

long-run profits in a monopolistically competitive market is

A) impossible.

B) very difficult.

C) fairly easy.

D) almost always guaranteed.

23) In theory, in the long run, monopolistically competitive firms earns zero profits. However, in

reality there are some ways by which a firm can avoid losing profits. Which of the following is

one such way?

A) gradually increase the mark up on the goods produced

B) lower the price of its products to expand its market share

C) identify new markets and develop products precisely for those markets

D) find a market niche and keep it as narrow as possible so as to prevent other producers from

entering this market segment

24) If a monopolistically competitive firm breaks even, the firm is earning as much in this

industry as it could in any other comparable industry.

25) A monopolistically competitive industry that earns economic profits in the short run will be

able to expand its market share even if the market size remains constant.

26) A monopolistically competitive industry that earns economic profits in the short run will face

a more elastic demand curve in the long run.

27) What is the difference between zero accounting profit and zero economic profit?