Chapter 13: Financial Statement Analysis

90. Which of the following statements is true?

a. The return on assets ratio indicates whether the company can pay its current debt when it becomes due.

b. The causes for an increase or decrease in the return on assets ratio can be examined by calculating its two

components: return on sales and asset turnover.

c. If a company successfully applies leverage, its return on assets ratio will be greater than its return on

common stockholders’ equity ratio.

d. If a company’s return on assets ratio increases, the increase can be the result of decreased liquidity.

91. The return on assets ratio

a. considers the investment made by all creditors and stockholders.

b. is a measure of the liquidity of a company.

c. is based on average stockholders’ equity as compared to net income for the period.

d. reflects investments made only by the creditors of a company.

92. Dividends to preferred stockholders are deducted from net income when calculating the return on common

stockholders’ equity ratio because

a. dividends are not an expense on the income statement.

b. the ratio is an indicator of the return on “common” stockholders’ equity, not the return on preferred stock.

c. dividends are only available for distribution to common stockholders.

d. conservatism indicates that shareholders prefer a smaller numerator.

93. A company that uses leverage is attempting to earn an overall return that is higher than the cost of funds received

from

a. preferred and common stockholders.

b. common stockholders only.

c. preferred stockholders and borrowed funds.

d. borrowed funds only.

Chapter 13: Financial Statement Analysis

94. Presented below are selected data from the financial statements of Wizard Corp.

2016

2015

Net income

$150,000

$120,000

Cash dividends paid on preferred stock

15,000

15,000

Cash dividends paid on common stock

42,000

38,000

Weighted average number of preferred shares outstanding

20,000

20,000

Weighted average number of common shares outstanding

105,000

95,000

Earnings per share is reported on the 2016 income statement as

a. $1.08

b. $1.20

c. $1.29

d. $1.43

95. Presented below are selected data from the financial statements of Parade Corp.

2015

2016

Net income

$150,000

$123,000

Weighted average number of common shares outstanding

105,000

95,000

Market price per share of common stock at the end of the year

$12.00

$10.00

The price/earnings ratio for 2016 is

a. .80 to 1

b. 1.43 to 1

c. 8.39 to 1

d. 12.50 to 1

Chapter 13: Financial Statement Analysis

96. Presented below are selected data from the financial statements of Carnival Corp. for 2016 and 2015.

2016

2015

Net income

$110,000

$123,000

Cash dividends paid on common stock

$42,000

$38,000

Market price per share of common stock at the end of the year

$16.00

$13.00

Shares of common stock outstanding

140,000

140,000

The dividend yield ratio for 2016 is

a. 1.9%

b. 2.1%

c. 36.3%

d. 38.1%

97. Which of the following yields the return on assets ratio?

a. (return on common stockholders’ equity) x (asset turnover)

b. (return on sales) x (asset turnover)

c. (profit margin) x (return on sales)

d. (profit margin) x (asset turnover)

98. Which combination of ratios will best analyze Stetson’s income statement performance?

a. Earnings per share, gross profit, and profit margin ratio

b. Gross profit ratio, return on common stockholders’ equity ratio, debt-to-equity ratio

c. Debt-to-equity ratio, gross profit ratio, and profit margin ratio

d. Current ratio, gross profit ratio, and return on common stockholders’ equity ratio

99. Earnings per share is an indication of how much

a. the company paid as dividends for each share of stock held by stockholders.

b. the company earned for each share of outstanding common and preferred stock.

c. the company earned for each share of outstanding common stock.

d. cash the company has for each share of all outstanding stock.

Chapter 13: Financial Statement Analysis

100. Presented below are selected data from the financial statements of Provost Corp.

2016

2015

Net income

$110,000

$123,000

Cash dividends paid on common stock

$42,000

$38,000

Market price per share of common stock at the end of the year

$16.00

$13.00

Shares of common stock outstanding

140,000

140,000

The dividend payout ratio for 2016 is

a. 1.8%

b. 30.0%

c. 36.3%

d. 38.0%

101. Squid Lips, Inc. wants to measure the relationship between profitability and the investment made by stockholders.

Squid Lips should use the

a. return on stockholders’ equity ratio.

b. earnings per share.

c. profit margin.

d. statement of retained earnings.

102. Because of its relationship to dividends and market price, which ratio is important to investors?

a. current ratio

b. debt-to-equity ratio

c. price/earnings ratio

d. asset turnover ratio

103. The concept of leverage is

a. it is appropriate to borrow if the return on the assets is greater than the cost of the financing.

b. it is appropriate to borrow as long as the lender approves the loan.

c. it is unfavorable to borrow funds rather than raise the capital from stockholders.

d. that a high debt-to–equity ratio is favorable.

Chapter 13: Financial Statement Analysis

104. Which of the following is not a characteristic of extraordinary items reported on the income statement?

a. appear near the end of the income statement

b. reported separately from continuing operations

c. shown net of tax effects

d. is shown as a combined amount with discontinued operations

105. Which of the following is true concerning discontinued operations?

a. Only the gain or loss is reported on the income statement.

b. It must be both unusual in nature and infrequent in occurrence.

c. Analysts would not normally include this item in making their decisions.

d. Net income or loss from prior years must also be disclosed in the year of disposition.

106. Which of the following items need not be reported separately at the bottom of the income statement?

a. Profitability ratios

b. Discontinued operations

c. Extraordinary gains and losses

d. Cumulative effect of a change in accounting principle

107. A gain or loss that qualifies for extraordinary treatment on the income statement must have which of the following

qualities?

I. Unusual in Nature

II. Discontinued Segment

III. Infrequent in Occurrence

IV. Nonoperating in Nature

V. Never Occurred

a. I and V

b. III and IV

c. I and III

d. I, II, and III

108. If two companies in the same industry use different methods to value inventory, this makes comparisons more

difficult but not impossible.

a. True

b. False

Chapter 13: Financial Statement Analysis

109. Comparing one company with another in the same industry should cause no problems since companies in the same

industry are required to use the same GAAP.

a. True

b. False

110. The FASB requires a separate note in the financial statements to show the effects of inflation so that investors are

able to compare statements more accurately.

a. True

b. False

111. The analysis of common-size statements is called horizontal analysis.

a. True

b. False

112. An example of horizontal analysis is the increase in cost of goods sold by 29% from 2015 to 2016.

a. True

b. False

113. Vertical analysis is a comparison of financial statement items for a single company over a period of time.

a. True

b. False

114. An increase in a company’s revenue and expense accounts will automatically cause an increase in net income for

the period.

a. True

b. False

115. Common-size financial statements exclude the dollar amount as a relevant variable in the analysis, which makes

comparison of one period with the next more meaningful.

a. True

b. False

Chapter 13: Financial Statement Analysis

116. The base, or benchmark, on which all items on the income statement are compared is net sales.

a. True

b. False

117. The profit margin ratio reflects the amount of income for each dollar of sales.

a. True

b. False

118. All line items in common-size comparative income statements are stated as a percentage of net income.

a. True

b. False

119. Inventories and prepaid assets are excluded from the numerator used to compute the quick ratio.

a. True

b. False

120. Three measures of liquidity are: working capital, the acid-test ratio, and the debt-to–equity ratio.

a. True

b. False

121. Inventory is more liquid than accounts receivable because receivables must be collected and some customers may

not be willing to pay, while inventory need only be sold in a retail store.

a. True

b. False

122. The most liquid of all assets is cash.

a. True

b. False

123. The amount of working capital is more meaningful to users than the current ratio because it provides information

on the composition of the current accounts.

a. True

b. False

Chapter 13: Financial Statement Analysis

124. The acid-test ratio is a stricter test of a company’s ability to pay its current debts as they are due than the current

ratio is.

a. True

b. False

125. Ratios that focus on cash are more useful than those that focus on income in the evaluation of the liquidity of

a company.

a. True

b. False

126. Apple Company had terms of net 60 days for customers. The number of days’ sales in accounts receivable for

Apple was 42 days. Apple is efficient in the collection of its receivables.

a. True

b. False

127. Spring Market has an inventory turnover ratio of 15 times. Fall Market has a turnover of 14 times. Fall is

more effective in managing inventory.

a. True

b. False

128. The number of days’ sales in inventory is the same as a company’s accounting cycle.

a. True

b. False

129. Solvency is the company’s ability to pay its current debts when they become due.

a. True

b. False

130. One measure of a company’s overall long-term financial health is the debt-to-equity ratio.

a. True

b. False

Chapter 13: Financial Statement Analysis

131. A company with a capital structure that shifts more toward debt financing will appear to be in a stronger position

to pay interest and any principal amount that may be maturing by using its cash flows generated by operating

activities.

a. True

b. False

132. Solvency is concerned with the ability of a company to pay next year’s debts as they come due.

a. True

b. False

133. The denominator of a return ratio will be some measure of the company’s income for the period.

a. True

b. False

134. The income number used in the rate of return on assets is income after interest expense is added back.

a. True

b. False

135. Because net income is on an after-tax basis, interest in the return on assets ratio must be placed on a before-tax

basis.

a. True

b. False

136. The return on sales ratio is a variation of the profit margin ratio.

a. True

b. False

137. The concept of leverage refers to the practice of using borrowed funds and amounts received from preferred

stockholders in an attempt to earn an overall return that is higher than the cost of these funds.

a. True

b. False

Chapter 13: Financial Statement Analysis

138. If a company must pay more for the amounts provided by creditors and preferred stockholders than it can earn

overall, as indicated by the return on assets, there will be favorable leverage.

a. True

b. False

139. A high P/E ratio always indicates that a stock is overpriced by the market.

a. True

b. False

140. Analysts trying to make investment decisions may very well ignore discontinued operations, and extraordinary

items.

a. True

b. False

141. Because discontinued segments of a business will not be part of the company’s future operations, discontinued

operations are disclosed separately on the income statement.

a. True

b. False

142. Discontinued operations and extraordinary items are two components of the income statement that are reported

after income from operations or are reported separately because of their unique nature.

a. True

b. False

143. , or an increase in the level of prices, is another important consideration in analyzing financial

statements.

144. _____________ ratio is capable of telling the user everything there is to know about a particular company.

145. Trend analysis is another name for analysis.

146. The ratio of net income to net sales is the relationship presented by the ratio.

Chapter 13: Financial Statement Analysis

147. In a vertical analysis, the base, or benchmark, on which all other items in the income statement are compared is:

___________________.

148. ___________________ statements recast all items on the statement as a percentage of a

selected item on the statement.

149. The three types of analysis that involve ratios are , , and

____________________.

150. The ratio indicates the company’s ability to meet the current year’s interest

payments out of the current year’s earnings.

151. In the numerator of the debt service coverage ratio, is a good substitute for cash flow from

operations before interest and tax payments, especially where changes in these accounts are insignificant.

152. The two groups of users that are especially interested in profitability are and

____________________.

153. is a line item on the income statement to reflect the net income or

loss of a discontinued business segment as well as any gain or loss incurred from its disposal.

154. is a line item on the income statement to reflect any gain or

loss from an event that is both unusual in nature and infrequent in occurrence.

155. What are two difficulties that are encountered when two companies are compared?

Chapter 13: Financial Statement Analysis

156. What are two reasons for why a company’s accounts receivable turnover may decrease?

2. Credit sales could decline because of economic conditions.

157. What are three specific ratios that are especially useful for creditors and lenders?

Given below are several ratios. Select the accounts or amounts that would be used in order to calculate the ratio.

You will have more than one response to each ratio. Some accounts or amounts may not be used at all. (Select all

that apply.)

158. Times interest earned ratio

a. Total liabilities

b. Total stockholders’ equity

c. Net income

d. Interest expense

e. Income tax expense

f. Cash flow from operations before interest and tax payments

g. Cash paid for acquisitions

h. Cash flow from operations

159. Cash flow from operations to capital expenditures ratio

a. Interest expense

b. Income tax expense

c. Cash flow from operations before interest and tax payments

d. Cash paid for acquisitions

e. Cash flow from operations

f. Total dividends paid

g. Interest payments

h. Principal payments on debt

Chapter 13: Financial Statement Analysis

160. Debt-to-equity ratio

a. Total liabilities

b. Total stockholders’ equity

c. Net income

d. Interest expense

e. Cash flow from operations before interest and tax payments

f. Cash paid for acquisitions

g. Cash flow from operations

h. Total dividends paid

161. Debt service coverage ratio

a. Interest expense

b. Income tax expense

c. Cash flow from operations before interest and tax payments

d. Cash paid for acquisitions

e. Cash flow from operations

f. Total dividends paid

g. Interest payments

h. Principal payments on debt

Given below are several ratios. Select the accounts or amounts that would be used in order to calculate the ratio.

You will have more than one response to each ratio. Some accounts or amounts may not be used at all. (Select all

that apply.)

162. Profit margin ratio

a. Market price per share

b. Net sales

c. Gross profit

d. Average total assets

e. Interest expense, net of tax

f. Net income

g. Total liabilities

h. Total assets

Chapter 13: Financial Statement Analysis

163. Return on assets ratio

a. Market price per share

b. Net sales

c. Gross profit

d. Average total assets

e. Interest expense, net of tax

f. Net income

g. Total liabilities

h. Total assets

164. Asset turnover ratio

a. Market price per share

b. Net sales

c. Gross profit

d. Average total assets

e. Interest expense, net of tax

f. Net income

g. Total liabilities

h. Total assets

165. Return on sales ratio

a. Market price per share

b. Net sales

c. Gross profit

d. Average total assets

e. Interest expense, net of tax

f. Net income

g. Total liabilities

h. Total assets

Chapter 13: Financial Statement Analysis

166. Dividend yield ratio

a. Market price per share

b. Net sales

c. Average inventory outstanding

d. Interest expense, net of tax

e. Common dividends per share

f. Preferred dividends per share

g. Weighted average number of common shares outstanding

h. Total stockholders’ equity

167. Genenco, Inc., a supplier, is thinking of extending credit to a Fab Company but decides not to because the

Fab’s current ratio is only 0.60. Do you agree with the supplier’s decision? What other factors need to be

considered in drawing any conclusions about a company’s liquidity?

Chapter 13: Financial Statement Analysis

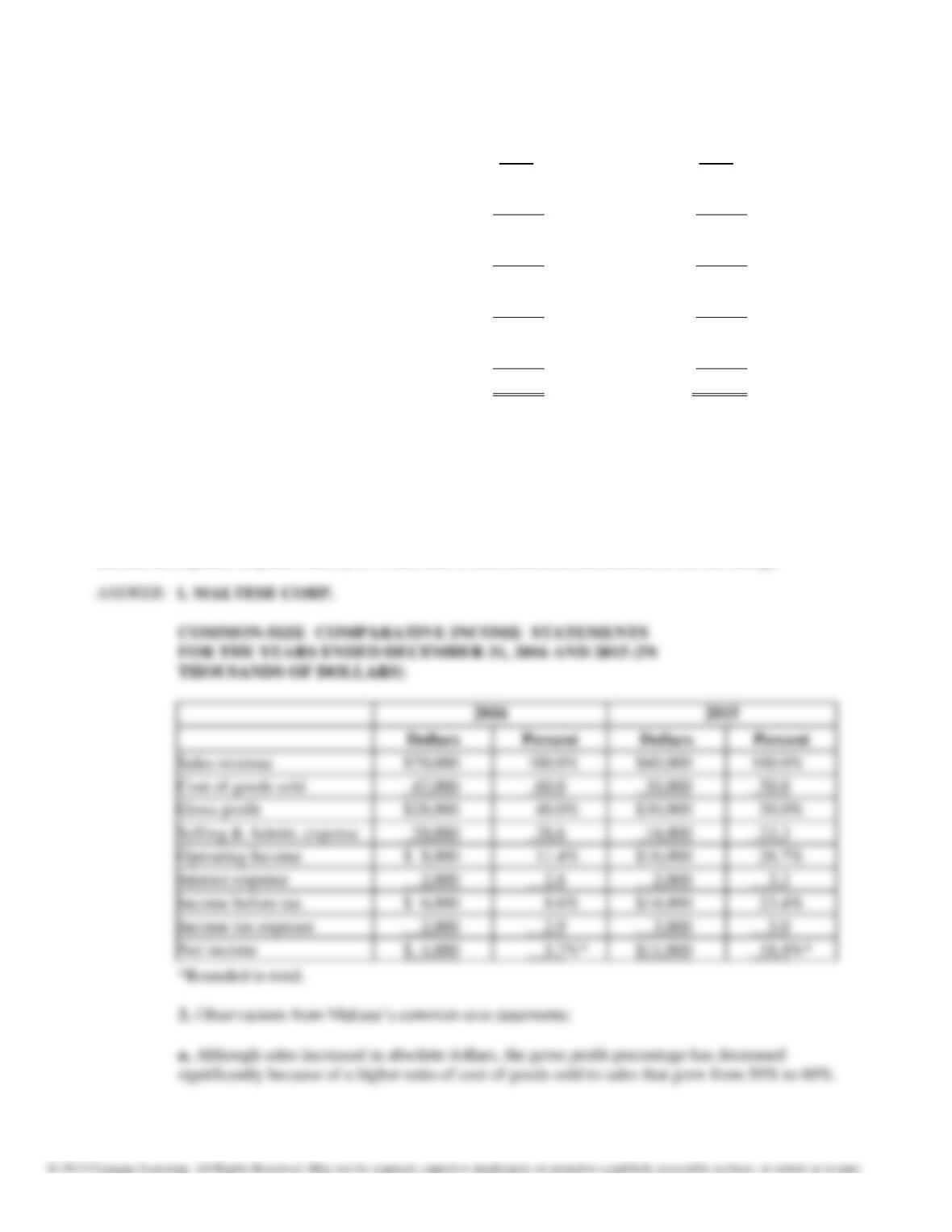

168. Income statements for Maltese Corp. for the past two years are as follows:

(amounts in thousands of dollars)

2016

2015

Sales revenue

$70,000

$60,000

Cost of goods sold

42,000

30,000

Gross profit

$28,000

$30,000

Selling and administrative expense

20,000

14,000

Operating income

$ 8,000

$16,000

Interest expense

2,000

2,000

Income before tax

$ 6,000

$14,000

Income tax expense

2,000

3,000

Net income

$ 4,000

$11,000

REQUIRED:

1. Prepare common-size comparative income statements for the two years for Maltese Corp.

2. What observations can you make about the common-size statements? List at least four observations.

3. Prepare comparative income statements for Maltese Corp., including columns for the dollars and for the

percentage increase or decrease in each item on the statement.

4. Assume that you are interested in identifying reasons for the changes in selling and administrative expenses and

income tax expense. Explain where you would look to find additional information about the change.

Chapter 13: Financial Statement Analysis

Chapter 13: Financial Statement Analysis

169. Use the current asset section of the balance sheets of the Breeze Company as of June 30, 2016 and 2015

presented below to answer the questions that follow.

2016

2015

Cash and cash equivalents

$ 75,000

$ 58,800

Trade accounts receivable, net

157,500

193,200

Inventory

208,200

253,400

Other current assets

18,400

15,500

Total current assets

$ 459,100

$ 520,900

Total assets

$2,650,000

$3,430,000

REQUIRED:

In the spaces provided below, complete a horizontal analysis of the current asset section of Breeze Company’s

balance sheet for 2016. Your answers for “% Change” should be rounded to one decimal place, e.g., 10.3%.

Provide a short evaluation of this analysis.

$ Change

% Change

Chapter 13: Financial Statement Analysis

170. Use the current asset section of the balance sheets of the Breeze Company as of June 30, 2016 and 2015 presented

below to answer the questions that follow.

2016

2015

Cash and cash equivalents

$ 75,000

$ 58,800

Trade accounts receivable, net

157,500

193,200

Inventory

208,200

253,400

Other current assets

18,400

15,500

Total current assets

$ 459,100

$ 520,900

Total assets

$2,650,000

$3,430,000

REQUIRED:

In the spaces provided below, complete a vertical analysis of the current asset section of Breeze Company’s

balance sheets for 2016 and 2015. Your answers should be rounded to one decimal place, e.g., 10.3%.

2016

2015

Chapter 13: Financial Statement Analysis

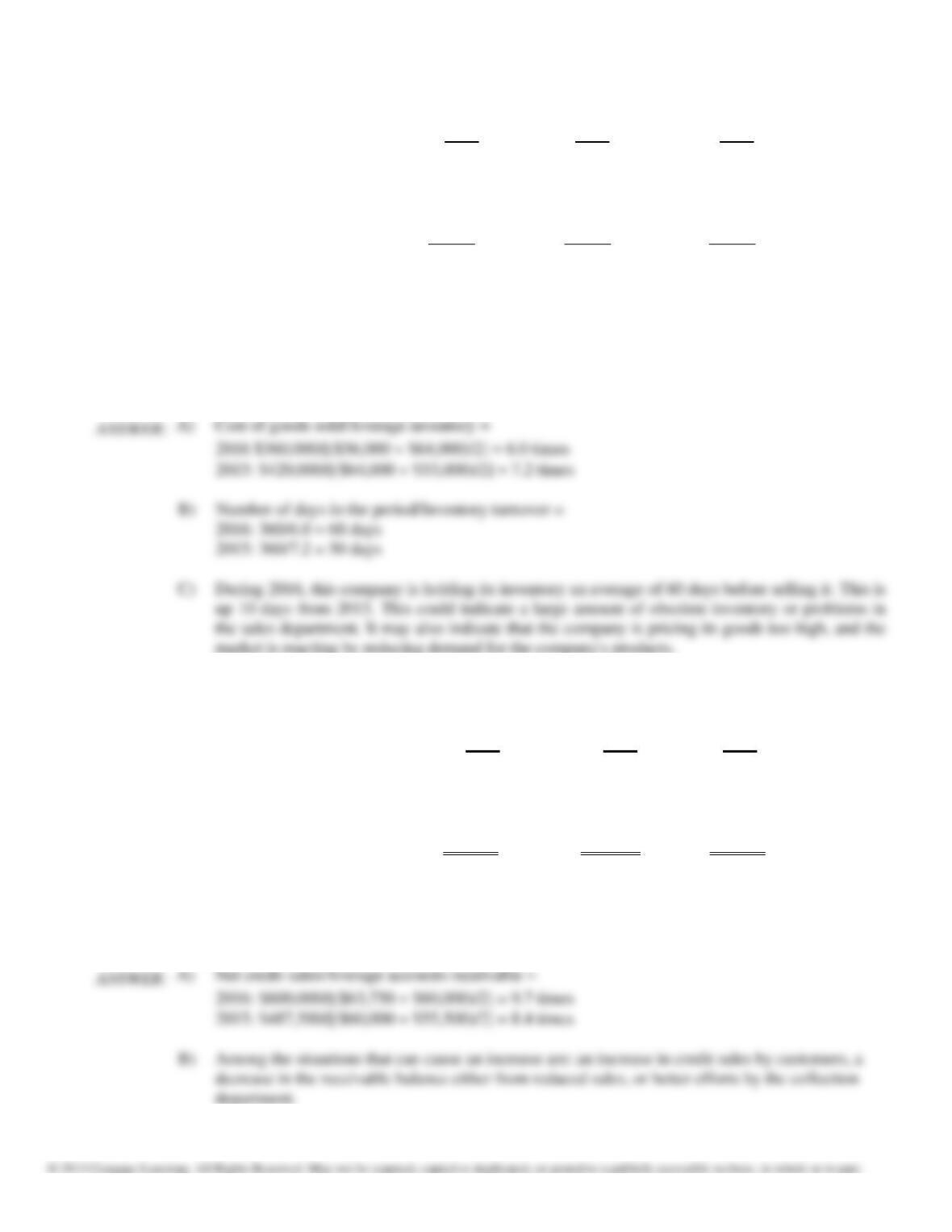

171. Presented below are selected data from the financial statements of Ripple Company for 2016, 2015, and 2014.

2016

2015

2014

Total assets

$1,205,000

$952,000

$945,000

Cost of goods sold

360,000

420,000

440,000

Inventory

56,000

64,000

53,000

Net income

65,000

25,000

16,000

A) Calculate Ripple’s inventory turnover ratio for 2016 and 2015.

B) How many days would it take to sell the entire inventory at December 31, 2016? At December 31, 2015?

Assume 360 days in a year.

C) What problems do you see in the company’s inventory management?

172. Presented below are selected data from the financial statements of Medtech Company for 2016, 2015, and 2014.

2016

2015

2014

Total assets

$487,500

$615,750

$600,000

Net credit sales

600,000

487,500

540,000

Accounts receivable

63,750

60,000

55,500

Net income

11,250

65,000

9,000

A) Calculate Medtech’s accounts receivable turnover ratio for 2016 and 2015.

B) What could have caused the change? Explain.