Chapter 13—Valuation: Earnings-Based Approaches

MULTIPLE CHOICE

1. If an analyst expects a firm to generate net income each period exactly equal to required earnings, then

the value of the firm will be

a.

exactly equal to the book value of common shareholders’ equity.

b.

greater than the book value of common shareholders’ equity.

c.

less than the book value of common shareholders’ equity.

d.

exactly equal to working capital.

2. Residual income valuation focuses on

a.

dividend-paying capacity in free-cash flows.

b.

earnings as a periodic measure of shareholder wealth creation.

c.

free cash flows as a periodic measure of shareholder wealth creation.

d.

dividends as a periodic measure of shareholder wealth creation.

3. Over the life of a firm, the capital invested in the firm by the shareholders plus the income of the firm

will reflect

a.

the dividend paying ability of the firm.

b.

the free cash flows available to shareholders.

c.

the value of the firm to shareholders.

d.

the value of the firm for debtholders and shareholders.

4. Assume that a firm had shareholders’ equity on the balance sheet at a book value of $1,500 at the end

of 2010. During 2011 the firm earns net income of $1,900, pays dividends to shareholders of $200, and

issues new stock to raise $500 of capital. The book value of shareholders equity at the end of 2011 is:

a.

$2,750

b.

$250

c.

$1,450

d.

$3,700

5. Assume that a firm had shareholders’ equity on the balance sheet at a book value of $1,600 at the end

of 2010. During 2011 the firm earns net income of $1,300, pays dividends to shareholders of $600, and

uses $300 to repurchase common shares. The book value of shareholders equity at the end of 2011 is:

a.

$2,000

b.

$400

c.

$3,800

d.

$2,600

13-2

6. Residual income is

a.

adjusted net income the firm reports.

b.

the difference between the net income the analyst expects the firm to generate and the

required earnings of the firm.

c.

the difference between the net income the analyst expects the firm to generate and the

reported earnings of the firm.

d.

the book value of common equity capital at the beginning of the period multiplied by the

required rate of return on common equity capital.

7. Required earnings are the

a.

adjusted net income multiplied by the required rate of return on common equity capital.

b.

net income the analyst expects the firm to generate multiplied by the required rate of

return on common equity capital.

c.

the market value of common equity capital at the beginning of the period multiplied by the

required rate of return on common equity capital.

d.

the book value of common equity capital at the beginning of the period multiplied by the

required rate of return on common equity capital.

8. Residual income will begreater than zero when

a.

the firm’s reported net income exactly equals the required level of earnings necessary to

cover the cost of equity capital.

b.

the firm’s expected future income is greater than the required level of earnings necessary

to cover the cost of equity capital.

c.

the firm’s expected future income exactly equals the required level of earnings necessary

to cover the cost of equity capital.

d.

the firm’s expected future income is less than the required level of earnings necessary to

cover the cost of equity capital.

Jarrett Corp.

At the end of 2010 Jarrett Corp. developed the following forecasts of net income:

Forecasted

Year

Net Income

2011

$20,856

2012

$22,733

2013

$24,552

2014

$27,252

2015

$29,978

Management believes that after 2015 Jarrett will grow at a rate of 7% each year. Total common

shareholders’ was $112,768 on December 31, 2010. Jarrett has not established a dividend and does not

plan to paying dividends during 2011 to 2015. Its cost of equity capital is 12%.

9. Compute the value of Jarrett Corp. on January 1, 2011, using the residual income valuation model.

Use the half-year adjustment.

a.

$112,768

b.

$185,329

c.

$195,540

d.

$133,624

10. What would be Jarrett’s residual income in 2013?

a.

$24,552

b.

$18,763

c.

$5,789

d.

$5,200

13-4

11. What would be Jarrett’s common shareholders’ equity at the end of 2014?

a.

$180,909

b.

$208,161

c.

$95,540

d.

$112,768

12. Assume that a firm’s book value at the beginning of the year is $12,500 and that the firm reports net

income of $3,200 and pays dividends of $1,100. What will the firm’s book value at the end of the

year?

a.

$2,100

b.

$15,700

c.

$14,600

d.

$16,800

13. Assume that a firm’s book value at the beginning of the year is $17,800 and that the firm reports net

income of $6,200. If the firm’s book value at the end of the year is $20,000 what was the amount of

dividends paid during the year?

a.

$4,000

13-5

b.

$8,800

c.

$2,200

d.

Insufficient information to determine

14. If investors have invested $20,000 of common equity in a company and it is determined that the

required earnings of the company are $$1,250 each period, then investors must expect to earn what

return?

a.

the risk free rate

b.

9%

c.

6.25%

d.

the market premium

15. At the beginning of 2012 investors had invested $25,000 of common equity in Grant Corp.and expect

to earn a return of 11% per year. In addition, investors expect Grant Corp. to pay out 100% of income

in dividends each year. Forecasts of Grant’s net income are as follows:

2012 – $3,500

2013 – $3,200

2014 – $2,900

2015 and beyond – $2,750

Using this information what is Grant’s residual income valuation at the beginning of 2012?

a.

$25,000

b.

$26,350

c.

$26,151

d.

$26,041

16. At the beginning of 2012 investors had invested $125,000 of common equity in Jan Corp.and expect to

earn a return of 15% per year. In addition, investors expect Jan Corp. to pay out 100% of income in

dividends each year. Forecasts of Jan’s net income are as follows:

2012 – $41,000

2013 – $35,400

2014 – $33,200

2015 and beyond – $25,000

13-6

Using this information what is Jan’s residual income valuation at the beginning of 2012?

a.

$125,000

b.

$184,600

c.

$190,262

d.

$260,415

17. The appropriate discount rate for the residual income model is

a.

Weighted average cost of capital

b.

The risk free interest rate

c.

The risk free interest rate plus the market premium

d.

Cost of common equity capital

18. To measure a firm’s economic performance and position in a given period, it makes sense to

measure all of the following except:

a.

The daily free cash flow published by the Wall Street Journal.

b.

Expenses incurred for resources consumed in that period.

c.

A portion of the long-lived resources consumed during that period.

d.

The cost of commitments made during that period to pay retirement benefits to employees

in future periods.

19. Residual income is the

a.

difference between the net sales that the analyst expects the firm to generate and the

required earnings of the firm.

b.

difference between the net income that the analyst expects the firm to generate and the

required earnings of the firm.

c.

difference between the common stock that the analyst expects the firm to issue and the

required earnings of the firm.

d.

difference between the expenses that the analyst expects the firm to generate and the

required earnings of the firm.

20. Residual income in a long-run steady-state growth period is referred to as:

a.

dynamic residual income

b.

realistic residual income

c.

continuing residual income

d.

equilibrium residual income.

13-7

21. In some industries, competitive dynamics eventually drive long-run projections of the future returns

earned by the firm to an equilibrium level equal to the long-run expected cost of equity capital in the

firm. At that point, a firm can be expected to earn ____________ residual income in the future.

a.

increasing.

b.

zero.

c.

decreasing.

d.

There is not enough information to answer this question.

22. The residual income valuation model is a rigorous and straightforward valuation approach,

but the analyst should be aware of all of the following implementation issues that will hinder its ability

to measure firm value correctly except:

a.

common stock transactions.

b.

portions of net income attributable to equity claimants other than common shareholders.

c.

dirty surplus accounting items.

d.

positive book value of equity.

23. Dirty surplus items in U.S. GAAP typically arise from all of the following except:

a.

changes in investment security fair values

b.

foreign currency exchange rates

c.

interest rates

d.

realized gains

24. Clean surplus accounting for most common stock transactions holds for shares accounted for at market

value. An exception to this is:

a.

issuance of common equity shares for employee stock options exercises

b.

repurchase of common shares

c.

issuance of common shares to new shareholders in public exchanges

d.

none of these.

25. In theory, all three valuation models, when correctly implemented with internally consistent

assumptions, will produce the same estimates of value. However, in practice, which of the following

errors can result in different value estimates?

a.

incomplete or inconsistent earnings and cash flow forecasts.

b.

inconsistent estimates of weighted average costs of capital.

c.

incorrect continuing value computations.

d.

All of these errors result in different value estimates.

26. The two most popular discounted earnings models appear to be

a.

Free cash flow and dividend discount model.

b.

Sales/market capitalization and price-earnings.

c.

Discounted abnormal earnings and residual income.

d.

Price-cash flow and dividend discount.

27. Which of the following would likely be the most useful when valuing a dot.com company?

a.

Net asset value

b.

Dividend yield

c.

Discounted cash flow

d.

Price-earnings

28. Which of the following is probably the least likely reason for acquirers to pay too much in an

acquisition?

a.

Overbidding.

b.

Over optimistic appraisal of market potential.

c.

Over estimation of synergies.

d.

Overuse of conventional financial statements.

29. Early in a period in which sales were increasing at a modest rate and plan expansion and start-up costs

were occurring at a rapid rate, a successful business would likely experience

a.

Increased profits and no change in financing requirements.

b.

Decreased profits and increased financing requirements because of an increasing cash

shortage.

c.

Decreased profits and decreased financing requirements because of an increasing cash

surplus.

d.

Increased profits and increased financing requirements because of an increasing cash

shortage.

COMPLETION

1. The residual income_____________________________ valuation model uses

__________________ and the book value of common shareholders’ equity as the basis for valuation.

2. The value of a share of common equity should equal the present value of the

_____________________________________________ the shareholders will receive.

3. Residual income valuation focuses on ____________________ as a periodic measure of shareholder

wealth creation.

4. Accounting principles make accrual accounting earnings closer to the firm’s underlying economic

performance in a given period than are _________________________.

5. Economists sometimes argue that earnings are not a _________________________ attribute on which

to base valuation.

6. Over the life of the firm, the present value of ______________________________,

______________________________, and ____________________ will be the same.

7. The foundation for residual income valuation is the classical

_____________________________________________.

8. The residual income valuation approach assumes that accounting for net income and book value of

shareholders’ equity follows ________________________________________.

9. ______________________________ is the amount by which expected future earnings exceed the

required earnings.

10. If an analyst expects a firm to generate net income each period exactly equal to required earnings, then

the value of the firm will be equal to the ______________________________ of common

shareholders’ equity.

13-10

11. The required earnings of the firm equals the product of the required rate of return on common equity

capital times the __________________________________________________ at the beginning of the

period.

12. Clean surplus accounting means that net income includes all of the recognized elements of income for

the firm for _____________________________________________.

13. Clean surplus accounting means that ____________________ include all direct capital transactions

between the firm and the common equity shareholders.

14. Over sufficiently long periods, _________________________ equals free cash flows to common

equity.

15. Over the life of a firm, the capital invested in the firm by the shareholders plus the income of the firm

will reflect the ______________________________ to the shareholders.

16. ____________________ are the fundamental, value-relevant attribute of expected future returns.

17. Accounting earnings numbers provide a basis for valuation because earnings are the primary measure

of ______________________________ produced by the accrual accounting system.

18. Accounting for the residual income in a firm with 100% dividend payout can be expressed as follows:

RIt = CIt– ____________________ X BVt-1

19. When debating the issue of whether to use free cash flows or earnings in a valuation model,

economists sometimes argue that ____________________ can be subject to purposeful management

by a firm and thus make them less useful.

20. __________________ means that net income includes all of the recognized elements of income of the

firm for common equity shareholders and dividends include all direct capital transactions between the

firm and the common equity shareholders.

SHORT ANSWER

1. What is the rationale for using expected earnings as a basis for valuations?

2. What are the three arguments economists provide against using earnings as a value-relevant attribute

in valuation?

3. What is meant by the term clean surplus accounting?

4. What are the four components that make up dirty surplus accounting according to the FASB?

.

5. Investors have invested $30,000in common equity in a company. Given the risk inherent in the

company, the investors expect to earn a 13percent return. In addition, the investors expect the

company to return all income to investors in the form of dividends. The company earns $4,500 the first

year. For this company determine the following:

a.

The company’s required earnings

b.

The company’s residual earnings

6. Investors have invested $25,000 in common equity in a company. Given the risk inherent in the

company the investors expect to earn a 15 percent return. In addition, the investors expect the

company to return all income to investors in the form of dividends. The company is forecasted to earn

$4,000 the first year, $5,000 the second year, $4,500 the third year and $3,750 each year after the third

year. For this company determine the company’s residual income valuation

7. Investors have invested $25,000 in common equity in a company. Given the risk inherent in the

company the investors expect to earn a 15 percent return. In addition, the investors expect that the

company will reinvest all income in projects that will earn 16%. The company is forecasted to earn

$6,000 the first year, $5,000 the second year, $5,500 the third year and $6,244 each year after the third

year. For this company determine the company’s residual income valuation (round all numbers to the

nearest dollar).

8. Where is comprehensive income reported and what is its relevancy to the computation of residual

income?

9. Why is the weighted average cost of capital not used as the discount rate when computing residual

income?

10. In many cases, using the residual income valuation model will result in a different value than either the

dividend discount model and the free cash flow valuation methods. What are some reasons that the

three valuation models would result in inconsistent valuations?

11. Explain required income. What does required income represent? How is required income conceptually

analogous to interest expense?

12. Explain residual income. What does residual income represent? What does residual income measure?

13. If the firm competes in a very competitive, mature industry, what effect will competitive conditions

have on residual income for the firm and others in the industry? Now suppose the firm holds a

competitive advantage in an industry, but the advantage is not likely to be sustainable for more than a

few years because of the potential for entry in the industry. As the firm’s competitive advantage

diminishes, what effect will that have on that firm’s residual income?

14. Why is it appropriate to use the required rate of return on equity capital (rather than the weighted

average cost of capital) as the discount rate in the residual income valuation approach?

PROBLEM

1. Todd Corp. manufactures train components. On January 1, 2011, management provided the following

forecast of income for the next five years:

Year

Forecasted

Net Income

2011

$53,576

2012

$65,853

2013

$77,985

2014

$88,646

2015

$97,672

Thomas’ common shareholders’ equity was $422,174 on January 1, 2011. The firm does not expect to

pay a dividend during the 2011-2015 period. Thomas’ cost of equity capital is 11 percent.

Required:

Compute the value of Todd Company on January 1, 2011, using the residual income valuation model

and the half year convention. T. Harp, the CEO of Todd, expects net income to grow at a rate of 6

percent annually after 2015.

Year

1

2011$53,576

2

2012$65,853

3

2013$77,985

4

2014$88,646

5

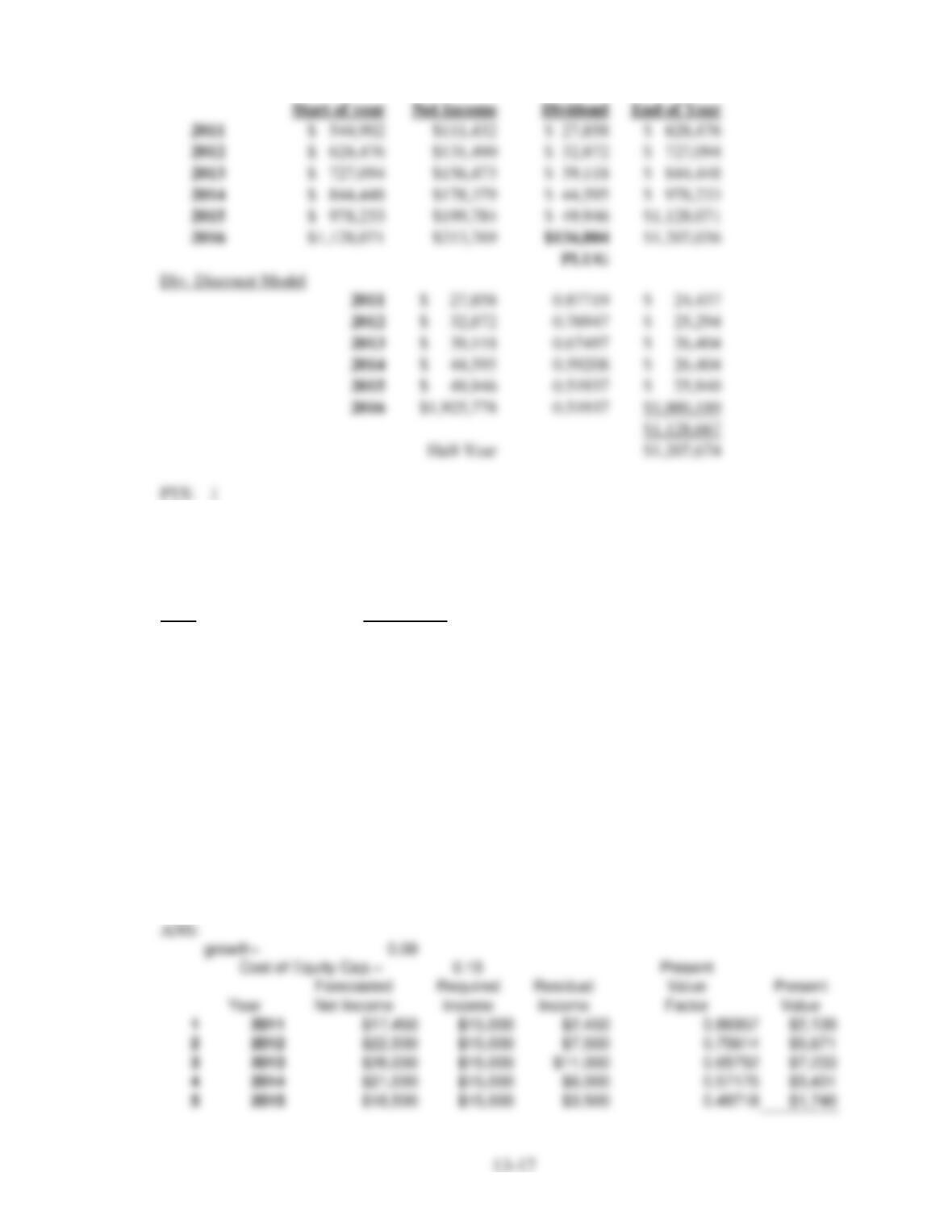

2. Booker, Inc. is a distributor of building supplies. Management for the company has developed the

following forecasts of net income:

Forecasted

Year

Net Income

2011

$111,432

2012

$131,490

2013

$156,473

2014

$178,379

2015

$199,784

Management expects net income to grow at a rate of 7 percent per year after 2015 and the company’s

cost of equity capital is 14%. Management has set a dividend payout ratio equal to 25% of net income

and plans to continue this policy. Booker’s common shareholders’ equity at January 1, 2011 is

$544,902.

Required:

a.

Using the residual income model, compute the value of Booker as of January 1, 2011.

b.

Using the dividend discount model, compute the value of Booker as of January 1, 2011.

In both cases use the half-year convention.

2

2012

4

2014

Change in common shareholders’ equity

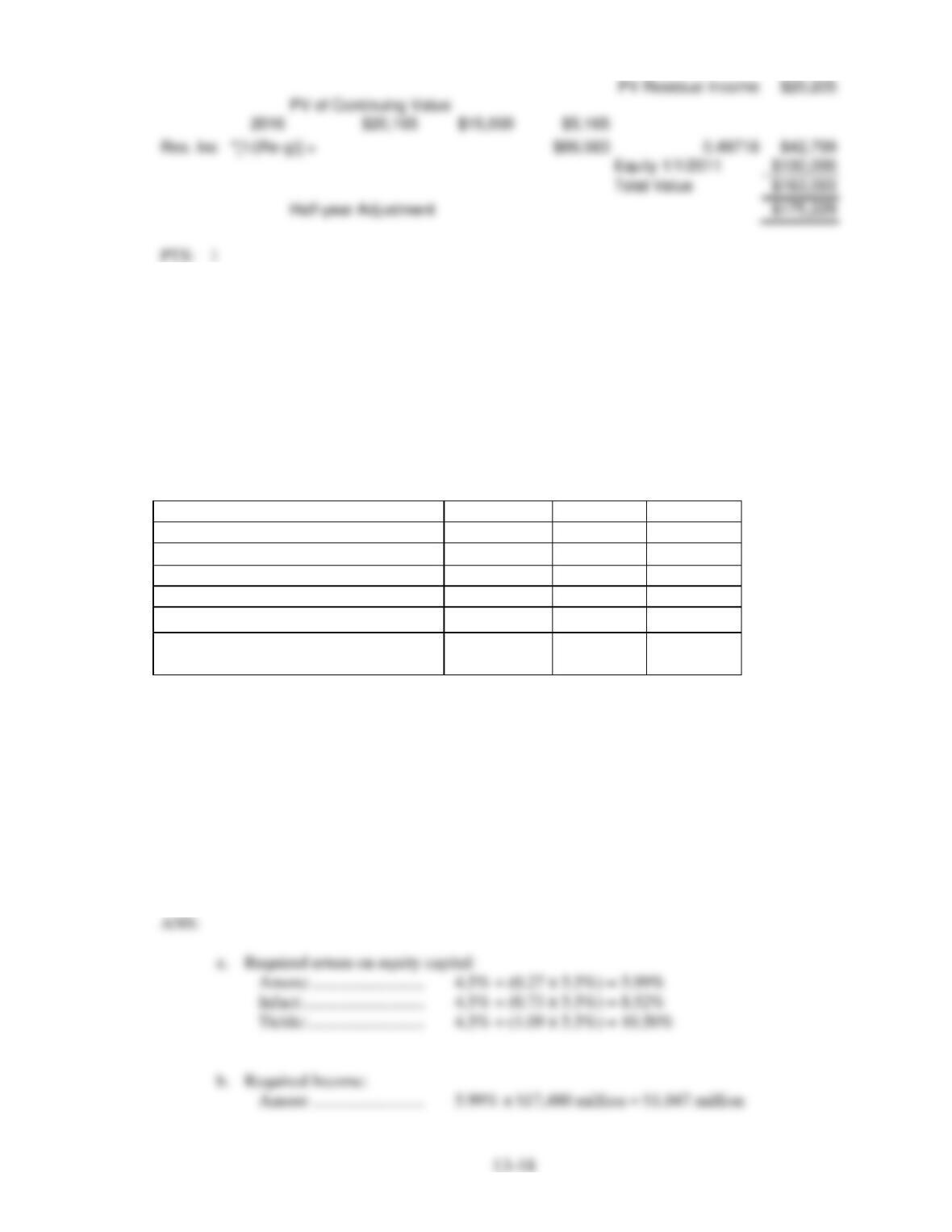

3. Porter, Inc. is a distributor of electrical supplies. Management for the company has developed the

following forecasts of net income:

Forecasted

Year

Net Income

2012

$17,450

2013

$22,500

2014

$26,000

2015

$21,000

2016

$18,500

Fred King, CFO of Porter, Inc., expects net income to grow at a rate of 9 percent per year after 2016

and the company’s cost of equity capital is 15%. Management plans to pay out all income in dividends

and plans to continue this policy into the future. Porter’s common shareholders’ equity at January 1,

2011 is $100,000.

Required:

Using the residual income model, compute the value of Porter, Inc. as of January 1, 2012. Use

the half-year adjustment.

4. The following data represent total assets, book value, and market value of common shareholders’

equity for Amore, Infact, and Tickle. Amore manufactures and sells cosmetics. Infact develops and

manufactures computer chips. Tickle operates a chain of general merchandise stores. In addition, these

data include existing market betas for the three firms and analysts’ consensus forecasts of net income

for Year +1

Assume that for each firm, analysts expect other comprehensive income items for

Year +1 to be zero; so Year +1 net income and comprehensive income will be identical.

Assume that the risk-free rate of return in the economy is 4.5 percent and the market risk

premium is 5.5 percent.

(dollar amounts in millions)

Amore

Infact

Tickle

Total Assets

$42,419

$109,524

$44,106

Common Equity:

Book Value

$17,480

$ 13,466

$13,712

Market Value

$83,050

$166,420

$34,600

Market Equity Beta

0.27

0.73

1.09

Analysts’ Consensus Forecasts of Net

Income for Year +1

$ 5,750

$ 12,956

$ 2,384

Required

a. Using the CAPM, compute the required rate of return on equity capital for each

firm.

b. Project required income for Year +1 for each firm.

c. Project residual income for Year +1 for each firm.

d. What do the different amounts of residual income imply about each firm? Do the

projected residual income amounts help explain the differences in market value of

equity across these three firms? Explain.