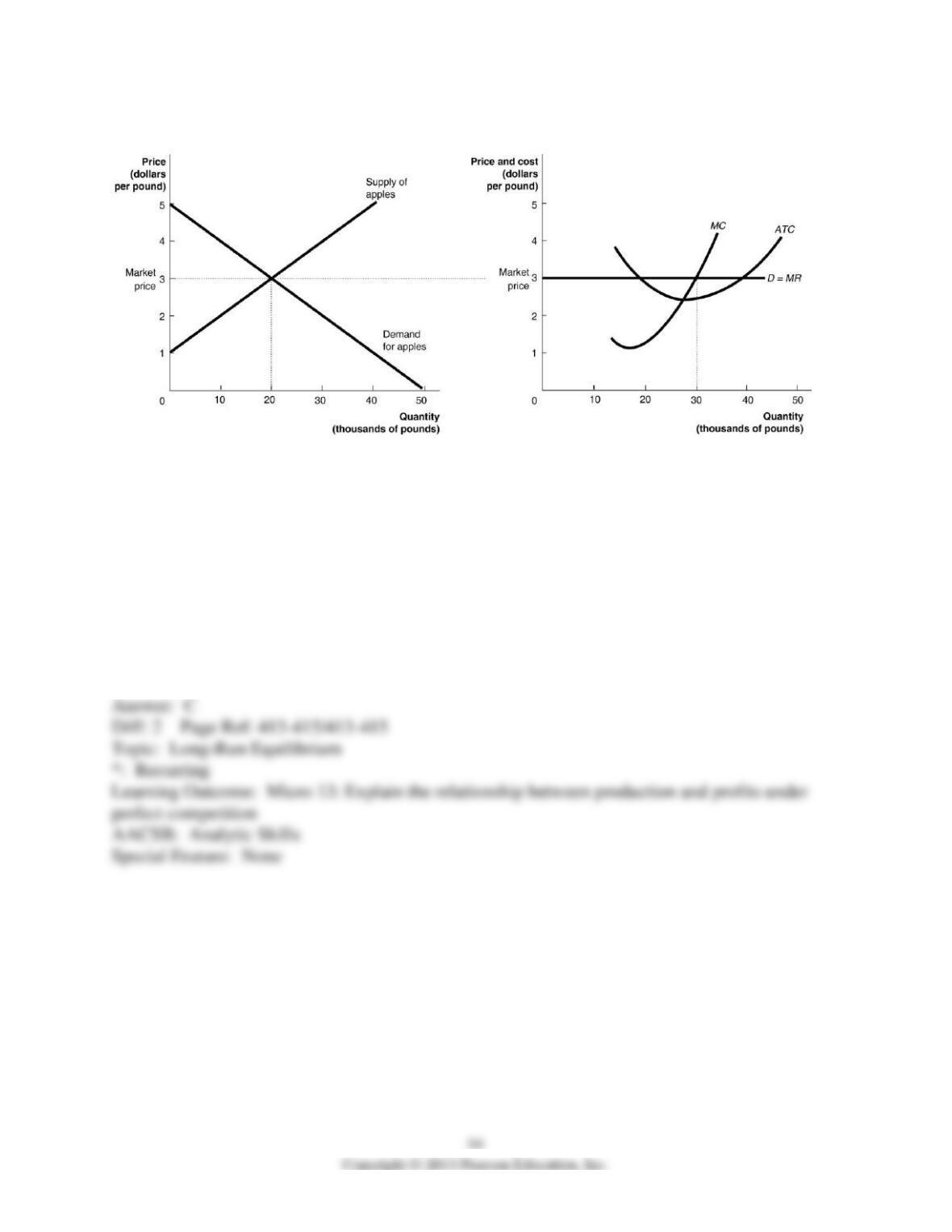

Figure 12-7

The graphs in Figure 12-7 represent the perfectly competitive market demand and supply curves

for the apple industry and demand and cost curves for a typical firm in the industry.

19) Refer to Figure 12-7. Which of the following statements is true?

A) The current market price is $3 but the firm will be able to increase the price in the future.

B) The current market price is $3 but the price will fall in the long-run as a result of a decrease in

demand.

C) The current market price is $3 but the price will fall in the long-run as new firms enter the

market.

D) The current market price is $3 but the price will increase in the future as the market demand

increases.

20) Refer to Figure 12-7. Which of the following statements is true?

A) The firm will produce 30 thousand pounds of apples in the short run and earn an economic

profit. New firms will enter the market and shift the market supply curve to the left.

B) The firm will produce 30 thousand pounds of apples in the short run and earn an economic

profit, but it would earn a greater profit if it produced at the lowest point on the ATC curve.

C) The firm will produce 30 thousand pounds of apples in the short run and earn an economic

profit. New firms will enter the industry; as a result, the firm will be forced to exit the industry in

the long run.

D) The firm will produce 30 thousands pounds of apples in the short run and earn an economic

profit. In the long run the firm will break even.

21) Refer to Figure 12-7. The graphs depicts a short run equilibrium. How will this differ from

the long-run equilibrium? (Assume this is a constant-cost industry.)

A) Fewer firms will be in the market in the long run than in the short run.

B) The price will be higher in the long run than in the short run.

C) The market supply curve will be further to the left in the long run than in the short run.

D) The firm’s profit will be lower in the long run than in the short run.

22) Assume that firms in a perfectly competitive market are earning economic profits. Which of

the following statements describes the change in market price and output as a result of the entry

of new firms into this market?

A) The market demand curve shifts to the right, causing price to rise and market output to

increase.

B) The market demand curve shifts to the left, causing price to fall and market output to

decrease.

C) The short-run market supply curve shifts to the right, causing price to fall and total market

output to increase.

D) The short-run market supply curve shifts to the left, causing price to rise and total market

output to decrease.

23) A firm could continue to operate for years without ever earning a profit as long as it is

producing an output where

A) MR < ATC.

B) ATC > AVC.

C) MR > AVC.

D) AFC < AVC.

24) A firm would decide to shut down if its production resulted in

A) MR < ATC.

B) ATC > AVC.

C) AFC > AVC.

D) MR < AVC.

25) After an increase in demand in a constant-cost industry, firms will find themselves with

higher average cost curves.

26) Competition has driven the economic profits in the video rental business to zero. Surya

Bacha, who owns a video rental business, would be better off leaving the industry for another

alternative.

27) In a decreasing-cost industry, the entry of new firms lowers average cost at each level of

output.

28) When firms exit a perfectly competitive industry, the market supply curve shifts to the left.

29) Assume that the personal computer industry is perfectly competitive. The fact that the price

of personal computers over the last decade has fallen despite increases in demand signifies that

the industry is a decreasing-cost industry.

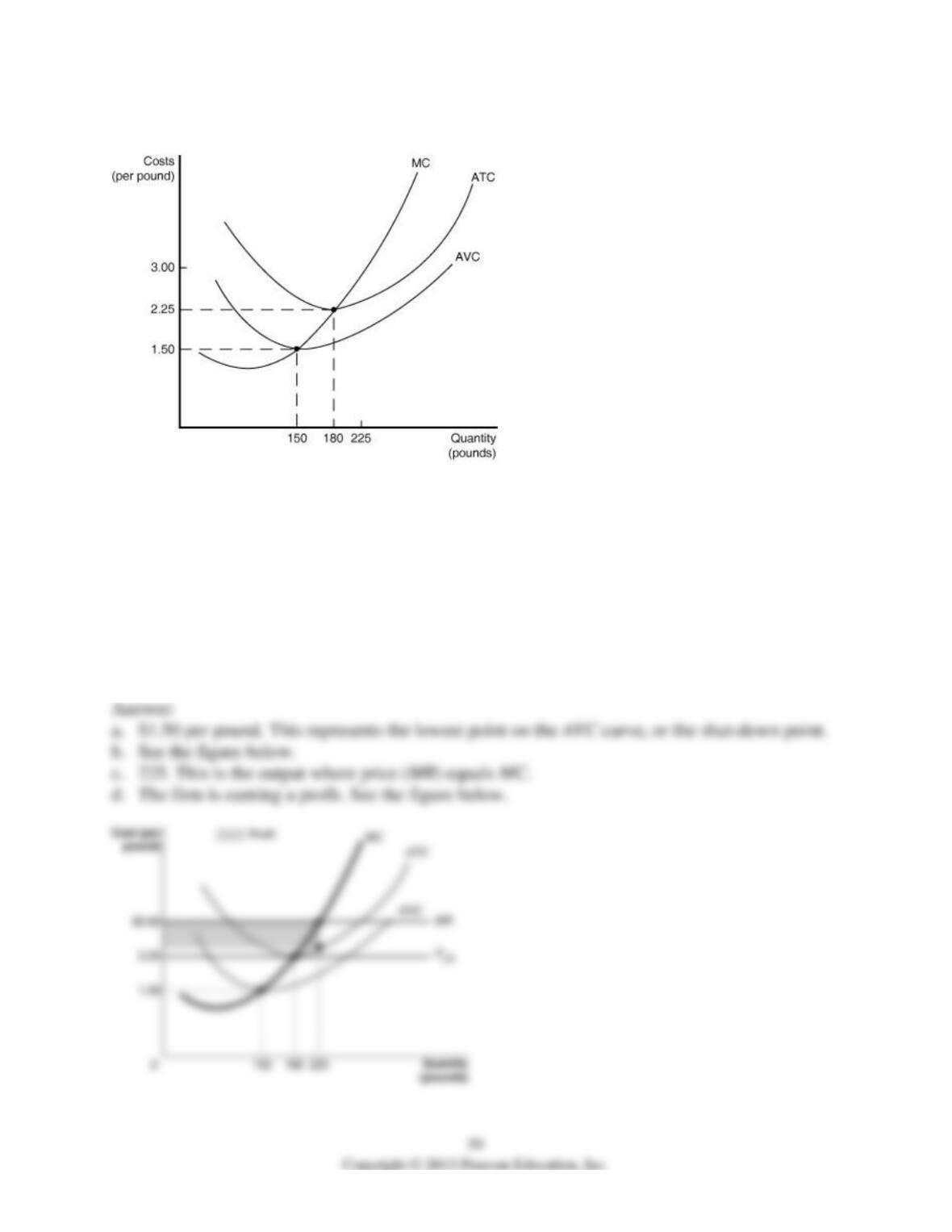

Figure 12-8

30) Refer to Figure 12-8. The figure above shows the cost curves of a perfectly competitive firm

in the coffee market. Use the graph in Figure 12-8 to answer the following questions. Assume the

market price is $3 per pound.

a. What is the lowest price at which the coffee grower will supply output in the short run?

b. In the diagram draw the firm’s demand curve (label this “MR” for marginal revenue).

c. What is the firm’s profit-maximizing output?

d. Is the firm earning a profit or a loss? Identify the area in the graph that represents the firm’s

profit or loss.

e. Explain how entry or exit will occur in the market to ensure that firms will break even in the

long run.

31) In the long run, perfectly competitive firms earn zero economic profit. Why do firms enter an

industry when they know that in the long-run they will not earn any profit?

32) Why would a company continue to operate for many years while never once turning a profit

rather than shut down immediately? Using revenue and cost analysis, explain when the company

would shut down.

12.6 Perfect Competition and Efficiency

1) Which of the following does not hold true for a perfectly competitive firm in long-run

equilibrium?

A) Its economic profit will be zero.

B) It will minimize average total cost.

C) It will charge a price equal to marginal cost.

D) Marginal cost will be minimized.

2) A perfectly competitive industry achieves allocative efficiency in the long run. What does

allocative efficiency mean?

A) Each firm produces up to the point where the price of the good equals the marginal cost of

producing the last unit.

B) Each firm produces up to the point where all scale economies are exhausted.

C) Production occurs at the lowest average total cost.

D) Firms use an input combination that minimizes cost and maximizes output.

3) New York Times writer Michael Lewis wrote that “The sad truth, for investors, seems to be

that most of the benefits….are passed through to consumers free of charge.” To which of the

following did Lewis refer?

A) apple farming in New York state

B) the Enron accounting scandal

C) the medical screening industry

D) new technologies developed in the 1990s

4) When plasma television sets were first introduced prices were high and few firms were in the

market. Later, economic profits attracted new firms and the price of plasma televisions fell. This

example illustrates

A) a decreasing-cost industry.

B) that consumers receive this new technology “free of charge” in the sense that they only have

to pay a price for plasma televisions equal to the lowest production cost.

C) an industry with a low minimum efficient scale.

D) how fickle consumer demands are.

5) Perfectly competitive firms produce up to the point where the price of the good equals the

marginal cost of producing the last unit. This condition is referred to as

A) productive efficiency.

B) constant returns to scale.

C) allocative efficiency.

D) perfectly competitive efficiency.

6) Which of the following describes a difference between allocative efficiency and productive

efficiency in a perfectly competitive market?

A) Allocative efficiency is achieved only in the long run. Productive efficiency is achieved only

in the short run.

B) Allocative efficiency is achieved only in the long run. Productive efficiency is achieved in the

short run and the long run.

C) Allocative efficiency is achieved only in the short run. Productive efficiency is achieved only

in the long run.

D) Allocative efficiency is achieved in the short run and the long run. Productive efficiency is

achieved only in the long run.

7) If a perfectly competitive firm achieves productive efficiency then

A) it will raise its price in order to earn an economic profit.

B) the price of the good it sells is equal to the benefit consumers receive from consuming the last

unit of the good sold.

C) it is producing at minimum efficient scale.

D) it is producing the good it sells at the lowest possible cost.

8) If productive efficiency characterizes a market,

A) the marginal cost of production is minimized.

B) firms produce the goods that consumers desire most.

C) the output is being produced at the lowest possible cost.

D) firms use the best technology available to produce the good.

9) A teenaged babysitter is similar to a firm in a perfectly competitive industry in that, for both,

A) fixed costs are lower than variable costs.

B) there are many other suppliers of similar goods or services.

C) the implicit costs of production exceed the explicit costs of production.

D) average costs of production do not change when their industry expands.

10) Being able to label products as organic becomes very important to a number of firms when

demand for these products is increasing. The increase in demand allows a firm to

A) decrease the quantity supplied and block entry into the market.

B) increase supply, which raises the market price.

C) charge a higher market price and earn a larger economic profit.

D) lower average total cost and marginal cost, thereby increasing economic profit.

11) ________ in demand for organic food products in the United Kingdom will decrease a firm’s

economic profit, and the ________ in cost to grow organic food products in the United Kingdom

will decrease a firm’s economic profit.

A) An increase; increase

B) An increase; decrease

C) A decrease; increase

D) A decrease; decrease

12) Allocative efficiency is achieved in an industry when firms supply those goods and services

that provide consumers with a marginal benefit equal to the marginal cost of producing those

goods and services.

13) A perfectly competitive firm in long-run equilibrium produces output at the lowest possible

average total cost.

14) What is meant by allocative efficiency? How does a perfectly competitive firm achieve

allocative efficiency?

15) In long-run competitive equilibrium, the perfectly competitive firm produces where price

equals minimum average total cost.

a. What is this efficiency criterion called?

b. How does it benefit consumers?