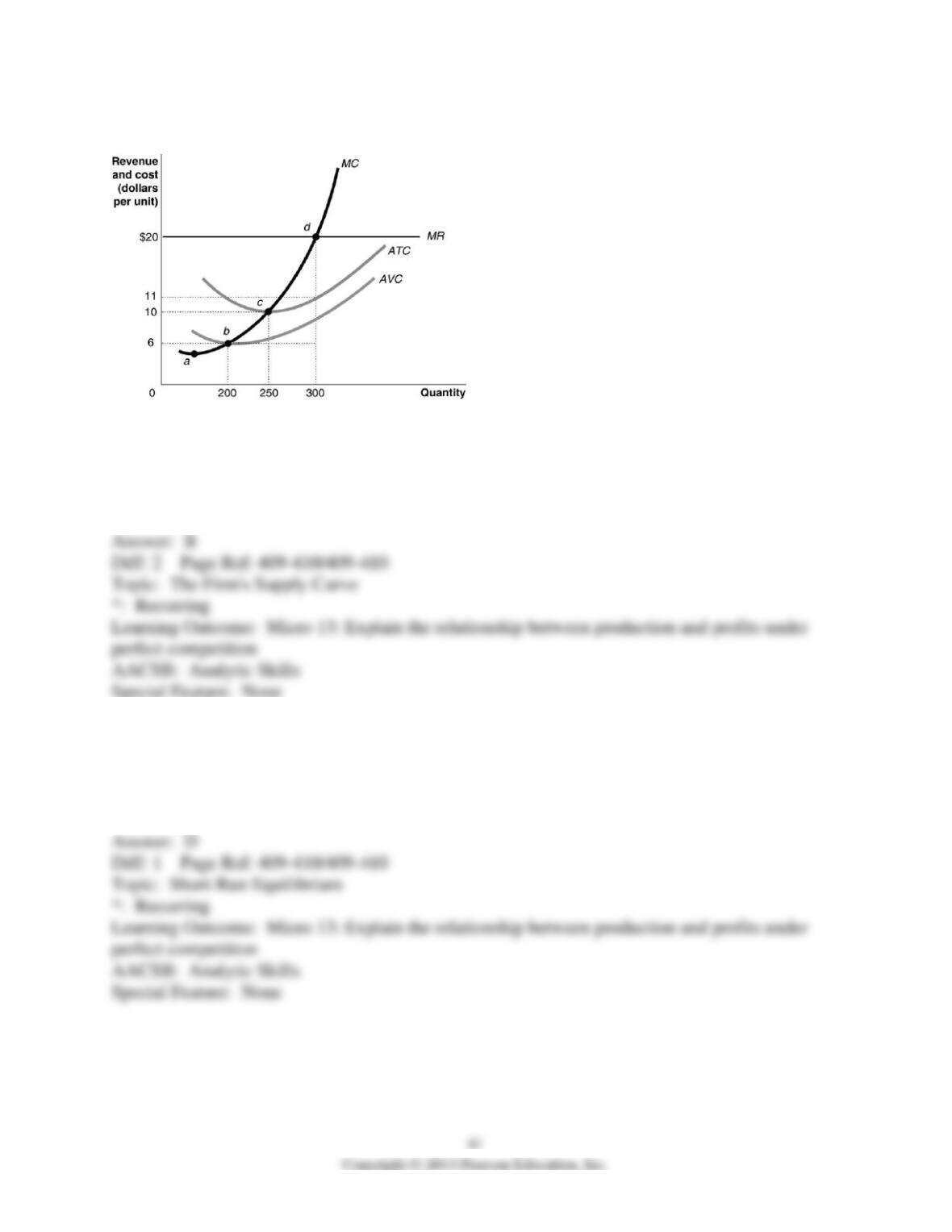

Figure 12-5

16) Refer to Figure 12-5. The firm’s short-run supply curve is its

A) marginal cost curve.

B) marginal cost curve from b and above.

C) marginal cost curve from c and above.

D) marginal cost curve from d and above.

17) Refer to Figure 12-5. Total revenue at the profit-maximizing level of output is

A) $1,200.

B) $2,500.

C) $4,800.

D) $6,000.

18) Refer to Figure 12-5. The total cost at the profit-maximizing output level equals

A) $4,800.

B) $3,300.

C) $2,500.

D) $1,800.

19) Refer to Figure 12-5. At the profit-maximizing output level, the firm earns

A) zero economic profit.

B) a profit of $600.

C) a profit of $1,200.

D) a profit of $2,700.

20) In the short run, a profit-maximizing firm will shut down if its total revenue is greater than

its variable costs.

21) In the short run, a firm might choose to produce rather than shut down even if its market

price is less than its average total cost of production.

22) If a firm’s total variable cost exceeds its total revenue, the firm should stop production by

shutting down temporarily.

23) The short-run supply curve for a perfectly competitive firm is that part of the firm’s marginal

cost curve that lies above the minimum point of its average variable cost curve.

24) What is the difference between “shutting down temporarily” and “exiting the industry”?

44

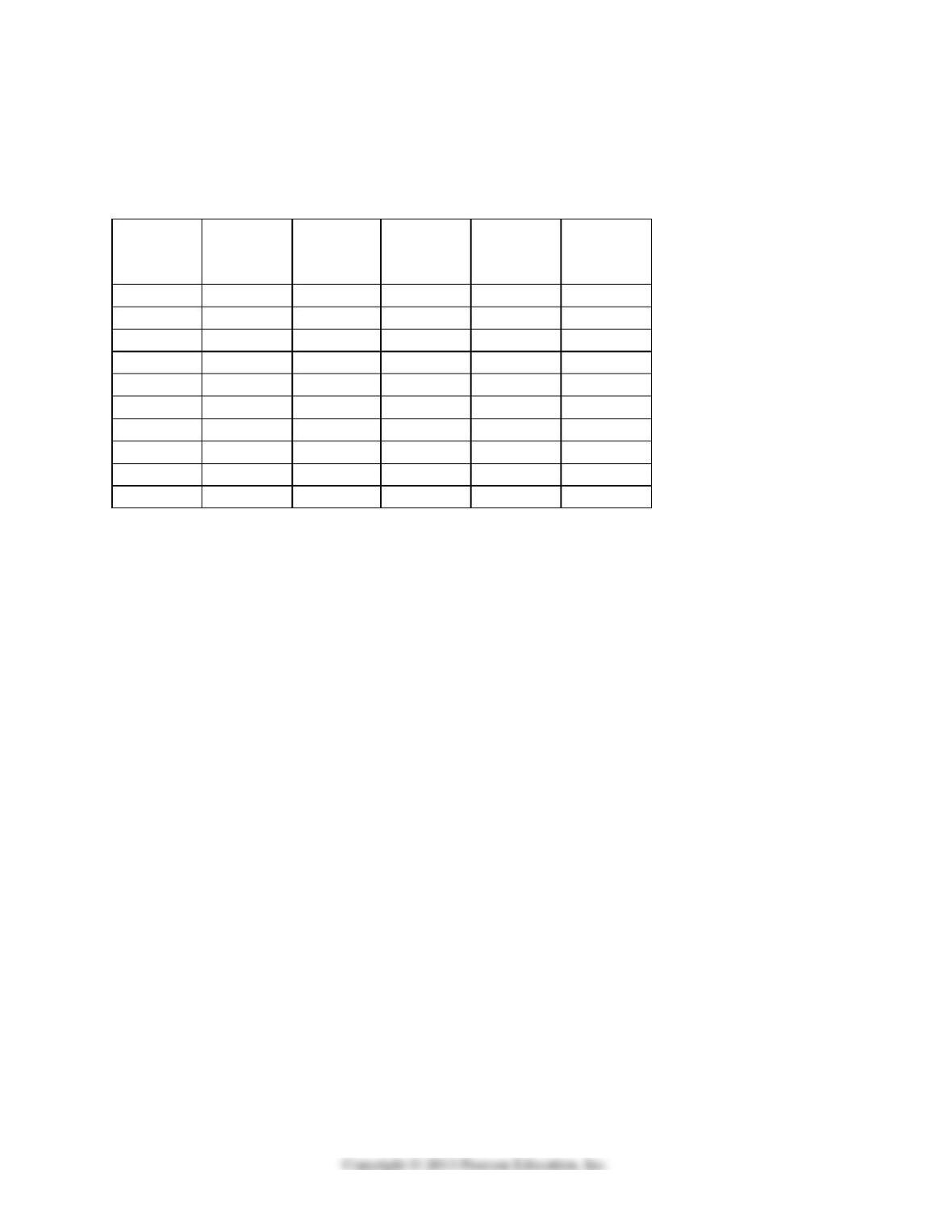

25) Werner & Sons is a manufacturer of three-ring binders operating in a perfectly competitive

industry. Table 12-4 shows the firm’s cost schedule.

Table 12-4

Quantity

(cases)

Variable

Cost

Total Cost

Marginal

Cost

Average

Variable

Cost

Average

Total Cost

0

$0

$76

1

30

106

2

50

3

134

4

140

5

160

6

114

7

150

8

190

9

316

Use the table to answer the following questions.

a. Complete Table 12-4 by filling in the blank cells.

b. Werner is selling in a perfectly competitive market at a price of $40. What is the profit

maximizing or loss-minimizing output?

c. Calculate the firm’s profit or loss.

d. Should the firm continue to produce in the short run? Explain.

e. If the firm’s fixed costs were $30 higher what would be the profit-maximizing output level in

the short run? Indicate whether the output level will increase, decrease or remain unchanged

compared to your answer in b.

f. Suppose fixed cost remains at $76. If the price of three-ring binders falls to $20 what is the

profit-maximizing or loss-minimizing output?

g. Calculate the profit or loss. Should the firm continue to produce in the short run? Explain

your answer.

h. Suppose the fixed cost remains at $76. What price corresponds to the shut-down point?

i. Suppose the fixed cost remains at $76. What price corresponds to the break-even point?

12.5 “If Everyone Can Do It, You Can’t Make Money at It”- The Entry and Exit of Firms in the

Long Run

1) In the long run, a firm in a perfectly competitive industry will supply output only if its total

revenue covers its

A) explicit plus its implicit costs.

B) fixed costs.

C) implicit costs.

D) explicit costs.

2) Which of the following statements is true?

A) A long-run competitive equilibrium can only be achieved in constant-cost industries.

B) When an industry achieves a long-run competitive equilibrium, industry output will not

change in the future.

C) A long-run competitive equilibrium outcome is not economically efficient.

D) When an industry reaches a long-run competitive equilibrium, the typical firm in the industry

breaks even.

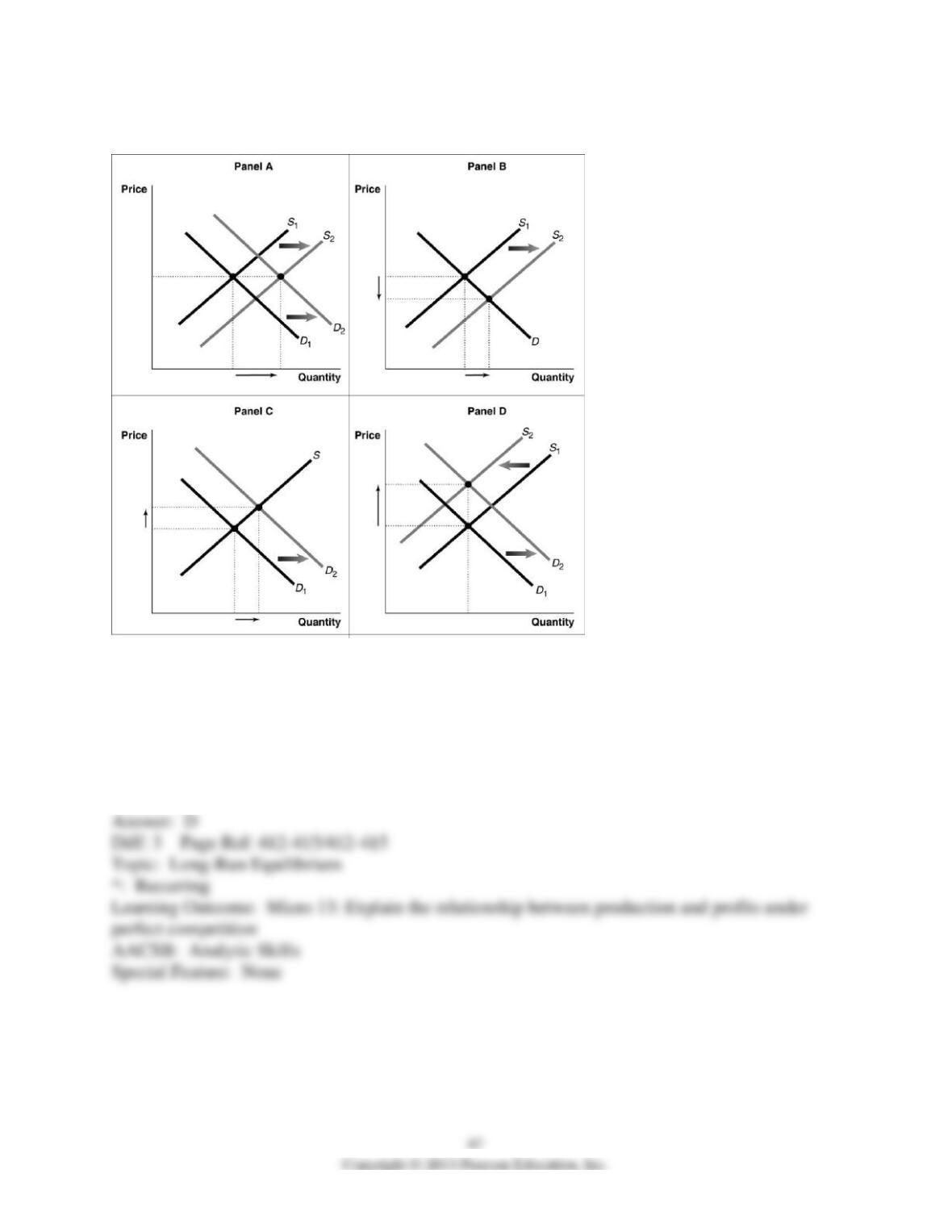

Figure 12-6

3) Refer to Figure 12-6. Which panel best represents the perfectly competitive organic produce

market in which some firms are experiencing short-run losses, and consumers are displaying an

increased preference for organic produce?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

4) Refer to Figure 12-6. Which panel best represents the perfectly competitive organic produce

market’s transition to the long run when some firms in the market are earning economic profits?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

5) Refer to Figure 12-6. Which panel best represents the perfectly competitive organic produce

market in which some firms are earning short-run economic profits, and the Surgeon General

announces that switching from non-organic produce to organic produce will add 5 years to the

average life span of consumers?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

6) Refer to Figure 12-6. Which panel best represents the perfectly competitive organic produce

market in which firms are breaking even, economically, organic produce is considered a normal

good, and the average income level of consumers is rising?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

7) In a perfectly competitive industry, in the long-run equilibrium

A) the typical firm is producing at the output where its long-run average total cost is not

minimized.

B) the typical firm is earning an accounting profit greater than its implicit costs.

C) the typical firm earns zero profit.

D) the typical firm is maximizing its revenue.

8) A constant cost, perfectly competitive market is in long-run equilibrium. At present, there are

1,000 firms each producing 400 units of output. The price of the good is $60. Now suppose there

is a sudden increase in demand for the industry’s product which causes the price of the good to

rise to $64. In the new long-run equilibrium, how will the average total cost of producing the

good compare to what it was before the price of the good rose?

A) The average total cost will be higher than it was before the price increase since the increase in

demand will drive up input prices.

B) The average total cost will be lower than it was before the price increase because of

economies of scale.

C) The average total cost will be higher than it was before the price increase because of

diseconomies of scale arising from the increased demand.

D) The average total cost will be the same as it was before the price increase.

9) A constant-cost industry is an industry in which

A) average costs fall as the industry expands output.

B) average costs rise as the industry expands output.

C) average costs remain constant as the industry expands output.

D) input prices rise at a constant rate as firms in the industry use more inputs.

10) The long-run supply curve for a perfectly competitive, constant-cost industry

A) is upward-sloping.

B) is horizontal.

C) is downward-sloping.

D) is found by adding up the marginal cost curves for all firms in the industry.

11) A perfectly competitive firm in a constant-cost industry produces 3,000 units of a good at a

total cost of $36,000. The prevailing market price is $15. What will happen to the number of

firms in the industry and to the industry’s output in the long run?

A) The number of firms and the industry’s output increase.

B) The number of firms and the industry’s output decrease.

C) The number of firms remains constant and the industry’s output increases.

D) The number of firms remains constant and the industry’s output decreases.

12) A perfectly competitive firm in a constant-cost industry produces 1,000 units of a good at a

total cost of $50,000. The prevailing market price is $48. Assuming that this firm continues to

produce in the long run, what happens to output level in the long run?

A) The firm’s output falls.

B) The firm’s output increases.

C) The firm produces the same output level.

D) There is insufficient information to answer the question.

13) If, as a perfectly competitive industry expands, it can supply larger quantities only at a higher

long-run equilibrium price, it is

A) a constant-cost industry.

B) an increasing-cost industry.

C) a decreasing-cost industry.

D) a fixed-cost industry.

14) If, as a perfectly competitive industry expands, it can supply larger quantities at the same

long-run market price, it is

A) a constant-cost industry.

B) an increasing-cost industry.

C) a decreasing-cost industry.

D) a fixed-cost industry.

15) Ethan Nicholas, who developed the iShoot application for the iPhone 3G, found that to

maintain sales in a profitable competitive market, the price of a product

A) will usually rise.

B) will usually fall.

C) will usually remain stable.

D) will eventually fall to zero.

16) What characteristic of a competitive market has made the “long run pretty short” in the

market for iPhone applications?

A) few firms in the market

B) identical products

C) ease of entry

D) blocked entry

17) If a firm in a perfectly competitive industry experiences persistent losses, in the long run it

should

A) shut down temporarily and wait for market conditions to change.

B) exit the industry.

C) raise its price to cover average total cost.

D) continue to operate if it can raise the demand for its product through advertising and quality

improvements.

18) Assume that a perfectly competitive market is in long-run equilibrium. Suppose as a result of

a health hazard associated with the industry’s product, demand decreases drastically. What is the

immediate result of this event?

A) The market price falls and the typical firm suffers an economic loss.

B) The market supply increases to offset the fall in demand.

C) The typical firm’s average total cost curve shifts downward.

D) The typical firm’s marginal cost curve shifts to the left.