12.3 Illustrating Profit or Loss on the Cost Curve Graph

1) Letters are used to represent the terms used to answer this question: price (P), quantity of

output (Q), total cost (TC) and average total cost (ATC). Which of the following equations is

equal to a firm’s profit?

A) P – ATC

B) (P × Q) – TC

C) (P × Q) – (P × ATC)

D) P – TC

2) Letters are used to represent the terms used to answer this question: price (P), quantity of

output (Q), total cost (TC) and average total cost (ATC). Which of the following equations is

equal to a firm’s average profit?

A) P – ATC

B) (P – ATC) × Q

C) (P × Q) – TC

D) P – TC

3) If price = marginal cost at the output produced by a perfectly competitive firm and the firm is

earning an economic profit, then

A) marginal revenue is less than price.

B) average total cost is at a minimum.

C) total revenue equals total cost.

D) price exceeds average total cost.

4) What is always true at the quantity where a firm’s average total cost equals average revenue?

A) The firm’s revenue is maximized.

B) The firm’s profit is maximized.

C) The firm breaks even.

D) Marginal cost equals marginal revenue.

5) Profit is the difference between

A) marginal revenue and marginal cost.

B) total revenue and variable cost.

C) total revenue and total explicit cost.

D) total revenue and total cost.

Table 12-2

Quantity

Total Cost

Average

Total Cost

Marginal

Cost

0

$10.00

—–

—–

1

15.00

$15.00

$5.00

2

17.50

8.75

2.50

3

22.50

7.50

5.00

4

30.00

7.50

7.50

5

40.00

8.00

10.00

6

52.50

8.75

12.50

7

67.50

9.64

15.00

8

85.00

10.63

17.50

9

105.00

11.67

20.00

Arnie sells basketballs in a perfectly competitive market. Table 12-2 summarizes Arnie’s output

per day (Q), total cost (TC), average total cost (ATC) and marginal cost (MC).

6) Refer to Table 12-2. What price (P) will Arnie charge and how much profit will he earn if the

market price of basketballs is $12.50?

A) Price and profit cannot be determined from the information given.

B) P = $12.50; profit = $52.50

C) P = $12.50; profit = $22.50

D) P = $20; profit = $75.00.

7) Refer to Table 12-2. What will Arnie’s output be and how much profit will he earn if the

market price of basketballs is $5.00?

A) Q = 1; profit = -$10.

B) Q = 3; profit = -$7.50

C) Q = 0; profit = -$10.00

D) Price and profit cannot be determined from the information given.

8) A firm will break even when

A) P = ATC.

B) P > ATC.

C) P < AVC.

D) P = AVC.

9) A firm will make a profit when

A) P > AVC.

B) P > ATC.

C) P = ATC.

D) P = MC.

10) In the early 2000s, some entrepreneurs took advantage of a reduction in the price of

computed tomography (CT) scanning equipment by offering apparently healthy people

preventive body scans to provide early detection of diseases. This effort failed to earn the

entrepreneurs a profit. Which of the following is one reason for this failure?

A) Few people wanted to devote the time needed for an unnecessary medical procedure.

B) The Food and Drug Administration (FDA) published a warning to consumers that the

procedure could cause negative side effects.

C) Since the CT scan was a voluntary procedure it was not covered under most medical

insurance plans.

D) The American Medical Association (AMA) refused to endorse the procedure.

11) In the early 2000s, some entrepreneurs took advantage of a reduction in the price of

computed tomography (CT) scanning equipment by offering apparently healthy people

preventive body scans to provide early detection of diseases. Which of the following is one

reason for the failure of this effort to be profitable?

A) Negative publicity from “false positives” that occurred from the CT tests reduced the demand

for this service.

B) The federal government halted the CT body scans until further tests proved the procedure was

safe and effective.

C) The U.S. Congress passed a law that restricted the ability of the entrepreneurs to offer the

body scans. As a result, the industry was not able to reach minimum efficient scale.

D) A lack of publicity resulted in few consumers being aware that the procedure was available.

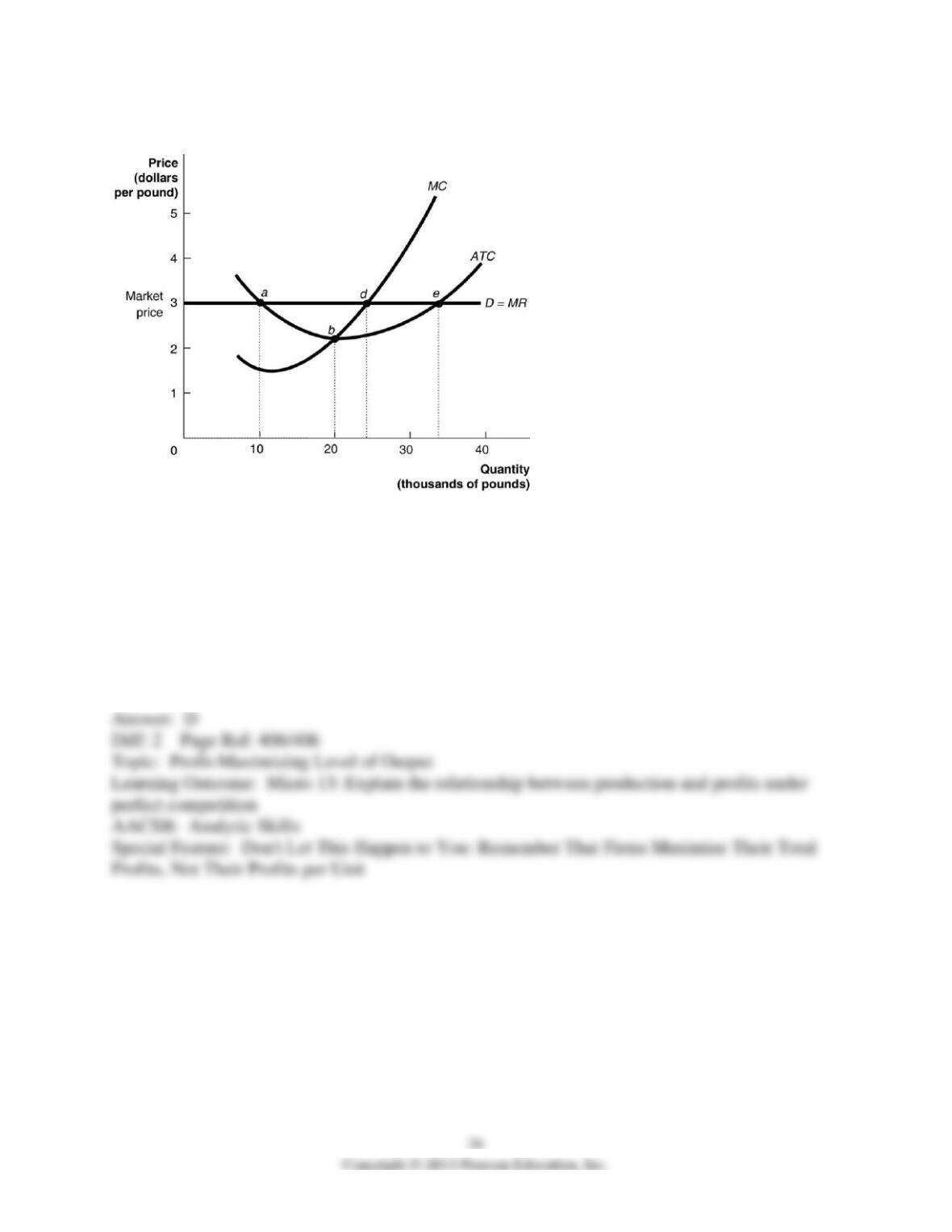

Figure 12-2

Figure 12-2 shows the demand, marginal cost (MC) and average total cost (ATC) curves for

Jason’s House of Apples.

12) Refer to Figure 12-2. To maximize his profit, Jason should produce the rate of output

indicated by point

A) a.

B) b.

C) e.

D) d.

13) Refer to Figure 12-2. Jason is currently producing 20 thousand pounds of apples. To

maximize his profit Jason should

A) keep production at 20 thousand pounds.

B) increase production to the output rate indicated by point d.

C) increase production to the output rate indicated by point e.

D) decrease production to the output rate indicated by point a.

14) Refer to Figure 12-2. Which of the following statements is true?

A) Jason should produce where MC equals $3 (point d) where he will minimize his losses.

B) Jason should produce where the distance between MC and his demand curve is greatest (point

b).

C) Jason cannot earn a profit from selling any number of apples.

D) Jason should produce where MC equals $3 (point d) where he will maximize his profit.

15) Refer to Figure 12-2. If Jason maximizes his profit he will produce the output rate indicated

by point ________ and his average profit will equal ________.

A) d; $3 minus ATC at point d

B) b; $3 minus ATC at point b

C) e; $3 minus ATC at point e

D) a; $3

16) A perfectly competitive firm will maximize its profit at the rate of output where the vertical

distance between its total revenue and total cost is the largest. This is the same rate of output

where

A) average total cost equals marginal revenue.

B) marginal revenue equals marginal profit.

C) marginal revenue equals marginal cost.

D) marginal revenue equals average revenue.

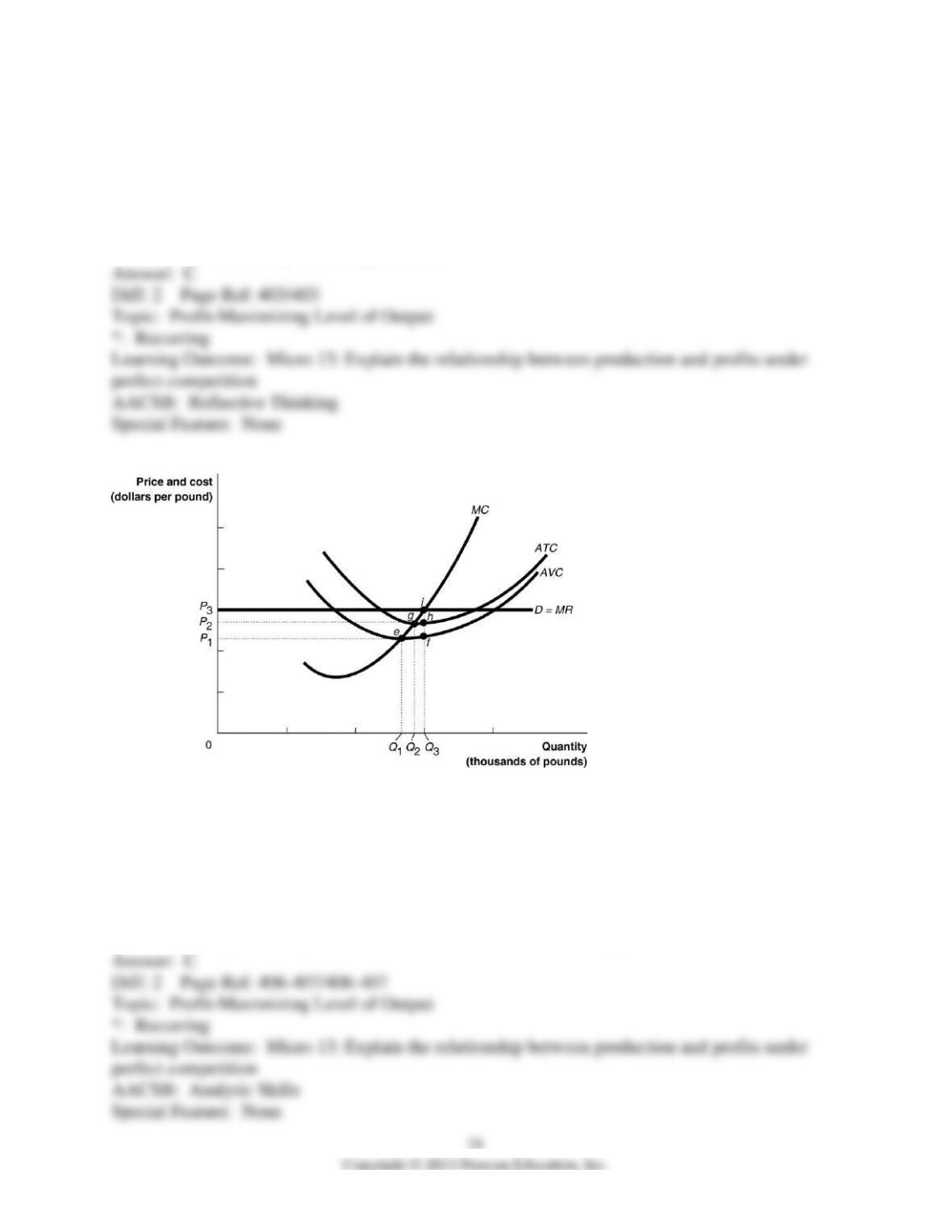

Figure 12-3

Figure 12-3 illustrates the cost curves of a perfectly competitive firm.

17) Refer to Figure 12-3. If the market price is P1

A) The firm will experience a loss and raise its price to P2. The firm will then break even.

B) The firm will break even by producing a quantity of Q2.

C) The firm will experience a loss since price is less than ATC.

D) The firm may make a profit if it can increase the demand for its product.

18) Refer to Figure 12-3. If the market price is P3 the firm

A) will break even.

B) will make a profit.

C) will earn enough revenue to cover its variable costs but not its fixed costs.

D) will produce a quantity of Q1.

19) Refer to Figure 12-3. If the market price is P2 the firm

A) will break even and produce a quantity of Q2.

B) will make a profit and produce a quantity of Q2.

C) will make a profit and produce a quantity of Q1.

D) will make a profit and produce a quantity of Q3.

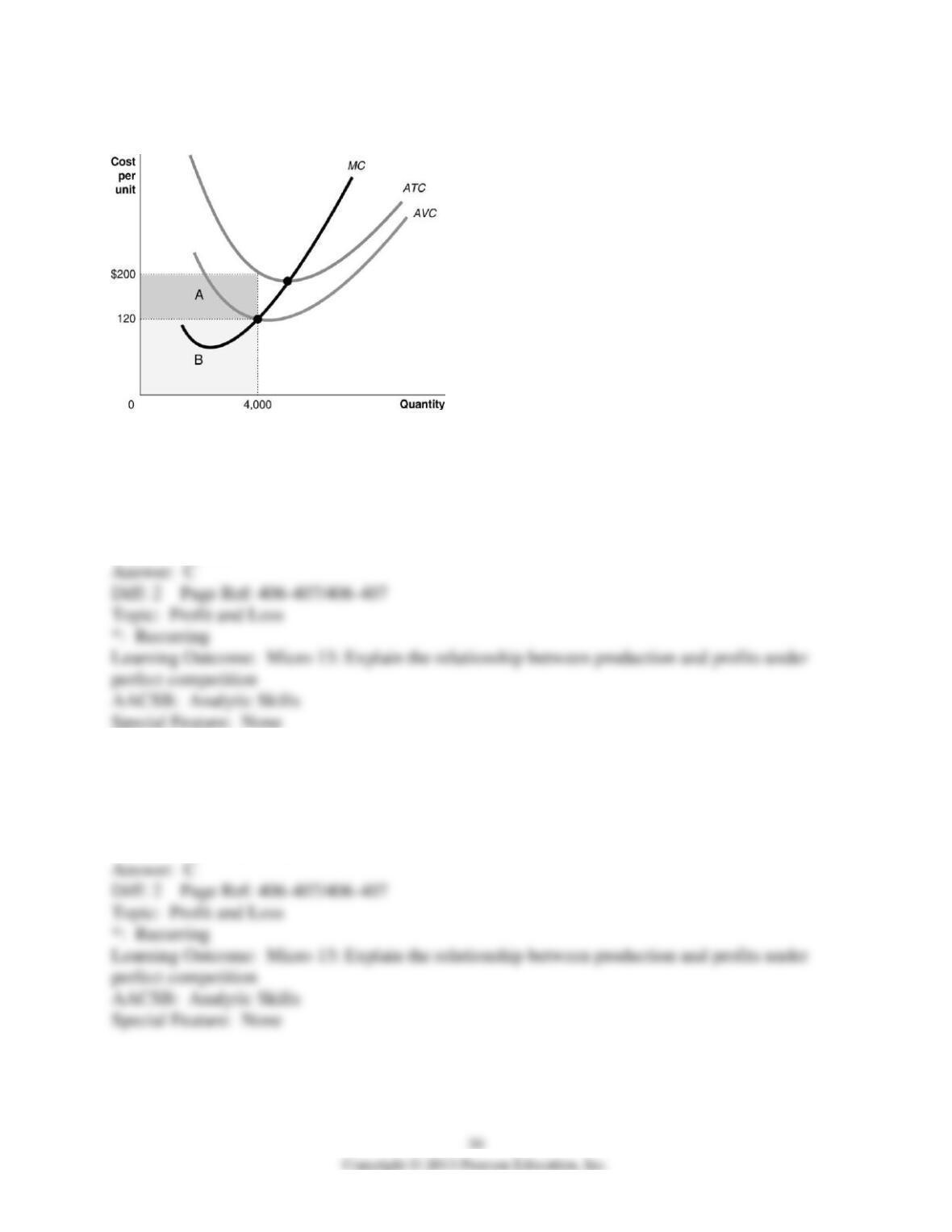

Figure 12-4

20) Refer to Figure 12-4. Suppose the firm produces 4,000 units. What does the shaded area

labeled A represent?

A) total variable cost

B) profit

C) total fixed cost

D) total revenue

21) Refer to Figure 12-4. Suppose the market price is $120. Which of the following is true?

A) The firm earns a profit equal to the area A.

B) The firm earns a profit equal to the area A + B.

C) The firm suffers a loss equal to the area A.

D) The firm will break even.

22) Refer to Figure 12-4. Suppose the firm produces 4,000 units. What does the shaded area

labeled B represent?

A) the firm’s economic loss

B) total variable cost

C) average variable cost

D) total fixed cost

Table 12-3

Quantity

Average

Fixed Cost

Average

Variable Cost

Marginal

Cost

20

$40

$18

$18

40

20

14

10

60

13.1

16

20

80

10

22

40

100

8

30

62

120

6.61

40

90

Table 12-3 shows the short-run cost data of a perfectly competitive firm. Assume that output can

only be increased in batches of 20 units.

23) Refer to Table 12-3. If the market price is $45 the firm will produce

A) 60 units.

B) 80 units.

C) 100 units

D) 120 units

24) Refer to Table 12-3. If the market price is $45, the firm

A) earn a profit of $3,600.

B) will suffer a loss of $200.

C) will break even.

D) will earn profit of $1,040.

25) If price is equal to average variable cost, a perfectly competitive firm breaks even.

26) For a given quantity, the total profit of a perfectly competitive firm is equal to the vertical

distance between the firm’s total revenue curve and its total cost curve.

27) If firms do not earn economic profits in a competitive equilibrium, why would the firms

choose to stay in business?

28) Suppose Veronica sells teapots in the perfectly competitive teapot market. Her output per

day and her costs are as follows:

Output per

Day

Total Cost

0

$20

1

32

2

37

3

48

4

61

5

75

6

92

7

113

8

136

Suppose the current equilibrium price in the teapot market is $10. To maximize profit, how many

teapots will Veronica produce, what price will she charge, and how much profit (or loss) will she

make? Draw a graph to illustrate your answer. Your graph should include Veronica’s demand,

ATC, AVC, MC, and MR curves, the price she is charging, the quantity she is producing, and the

area representing her profit (or loss).

29) To maximize profit, a firm will produce the level of output where MR = MC. If a firm

actually makes a profit depends on the relationship of price to average total cost. What are the

three possible relationships between price and average total cost that determine if a firm will

make a profit, experience a loss, or break even?

12.4 Deciding Whether to Produce or to Shut Down in the Short Run

1) In the short run, a firm that is operating at a loss has two options. These options are

A) to reduce output or reduce its variable costs.

B) to go out of business or declare bankruptcy.

C) to shut down temporarily or continue to produce.

D) to adopt new technology or change the size of its physical plant.

2) If a firm shuts down it

A) will suffer a loss equal to its fixed costs.

B) will produce nothing but must pay its variable costs.

C) will produce nothing but must pay its fixed and variable costs.

D) will earn enough revenue to cover its variable costs but not all of its fixed costs.

3) How are sunk costs and fixed costs related?

A) They are not related in any way.

B) Sunk costs cannot be recovered and fixed costs can be avoided by shutting down.

C) In the short run they are equal to each other.

D) In the long run they are equal to each other.

4) If a firm shuts down in the short run it will

A) break even.

B) declare bankruptcy.

C) suffer a loss equal to its variable costs.

D) suffer a loss equal to its fixed costs.

5) Ben’s Peanut Shoppe suffers a short-run loss. Ben will not choose to shut down if

A) his Shoppe’s total revenue exceeds his fixed cost.

B) his Shoppe’s total revenue exceeds his variable cost.

C) his Shoppe’s total revenue exceeds his implicit costs.

D) his Shoppe’s total revenue exceeds his capital costs.

6) Ted’s Pancake Kitchen suffers a short-run loss. When should Ted decide to shut down rather

than continue to produce?

A) if his Kitchen’s revenue is less than its variable costs

B) if his Kitchen’s revenue is less than its fixed costs

C) if his Kitchen’s revenue is less than its explicit costs

D) if his Kitchen’s revenue is less than its total costs

7) Marty’s Bird House suffers a short-run loss. Marty can reduce his loss below the amount of his

total fixed costs by continuing to produce if his revenue

A) exceeds his implicit costs.

B) exceeds his nonmonetary opportunity costs.

C) exceeds his variable costs.

D) exceeds his marginal costs.

8) In analyzing the decision to shut down in the short run we assume that the firm’s fixed costs

are

A) implicit costs.

B) capital costs.

C) nonmonetary opportunity costs.

D) sunk costs.

9) Molly Sharp is producing a documentary about the plight of the six-toed ferrets of Sri Lanka.

Molly has spent $125,000 of her own money on this project and the documentary is now

complete. Molly just found out that no studio is willing to release her documentary and she must

now shop it to cable television networks, where she knows she will not be able to recoup her

investment. Which of the following statements regarding Molly Sharp’s documentary is true?

A) She should not try to have her documentary aired on television because she cannot recoup her

$125,000 investment.

B) Since the $125,000 is a sunk cost, she should still try to have her documentary aired on

television even though she will not see a profit.

C) The $125,000 is a variable cost, so will not be incurred if she chooses not to have her

documentary aired.

D) The $125,000 investment is an economic cost, and she will still make an accounting profit

even if the television network willing to air her documentary pays her less than $125,000.

10) Which of the following is not an option for a perfectly competitive firm that suffers short-run

losses?

A) shutting down

B) reducing production

C) reducing the use of variable factors

D) raising price

11) The supply curve of a perfectly competitive firm in the short run is

A) the firm’s average variable cost curve.

B) the portion of the firm’s marginal cost curve below the minimum point of the average variable

cost curve.

C) the portion of the firm’s marginal cost curve above the minimum point of the average variable

cost curve.

D) the portion of the firm’s marginal cost curve above the minimum point of the average total

cost curve.

12) A perfectly competitive firm’s short-run supply curve is

A) upward sloping and is the portion of the marginal cost curve that lies above the average total

cost curve.

B) upward sloping and is the portion of the marginal cost curve that lies above the average

variable cost curve.

C) perfectly elastic at the market price.

D) horizontal at the minimum average total cost.

13) The minimum point on the average variable cost curve is called

A) the shutdown point.

B) the break-even point.

C) the loss minimizing point.

D) the point of diminishing returns.

14) If a perfectly competitive firm’s total revenue is less than its total variable cost, the firm

A) should raise its price above its average variable cost.

B) should continue to produce and increase its demand.

C) should stop production by shutting down temporarily.

D) should adopt new technology in order to lower its costs of production.

15) In the mid-1990s, cattle ranchers in the United States kept raising cattle even though prices

were at a ten-year low and below average total cost. What is the likely explanation for this?

A) Continuing to operate resulted in smaller losses than would have been incurred by shutting

down.

B) The ranchers were hoping to receive government subsidies.

C) The exit costs were too high.

D) Cattle is an important source of protein and its production is essential for the United States.