Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

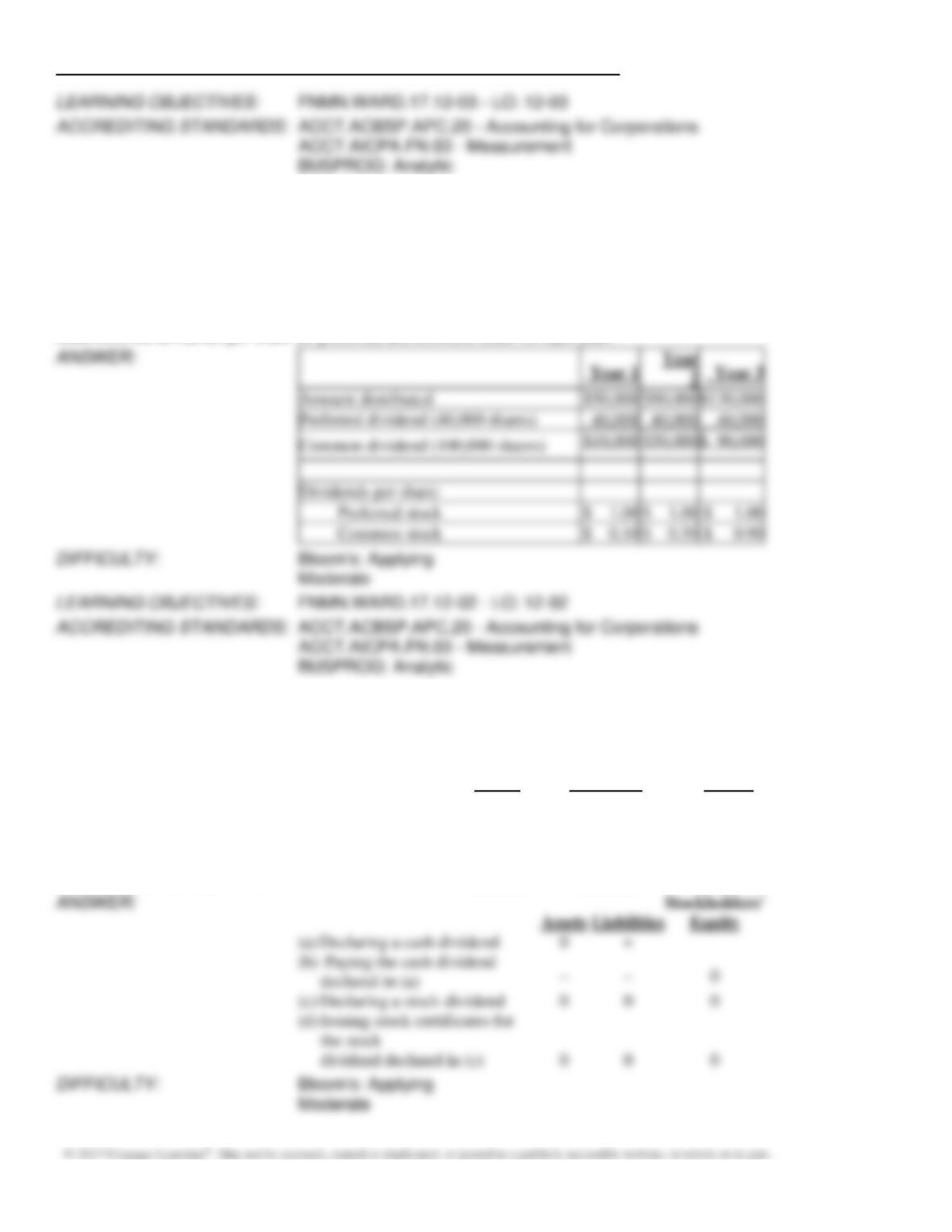

188. Sabas Company has 40,000 shares of $100 par, 1% preferred stock and 100,000 shares of $50 par common stock

issued and outstanding. The following amounts were distributed as dividends:

Year 1:

$ 50,000

Year 2:

90,000

Year 3:

130,000

Determine the dividends per share for preferred and common stock for each year.

Amount distributed

$130,000

Preferred dividend (40,000 shares)

40,000

Dividends per share:

189. Indicate whether the following actions would (+) increase, (–) decrease, or (0) not affect a company’s total assets,

liabilities, and stockholders’ equity.

Stockholders’

Assets

Liabilities

Equity

(a)

Declaring a cash dividend

_______

_______

_______

(b)

Paying the cash dividend declared in (a)

_______

_______

_______

(c)

Declaring a stock dividend

_______

_______

_______

(d)

Issuing stock certificates for the stock

dividend declared in (c)

_______

_______

_______

(a)

Declaring a cash dividend

(c)

Declaring a stock dividend

dividend declared in (c)

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

190. The following account balances appear on the balance sheet of Osgood Industries:

Common Stock (300,000 shares authorized, $100 par): $10,000,000

Paid-In Capital in Excess of Par—Common Stock: $2,000,000

Retained Earnings: $45,000,000

The board of directors declared a 2% stock dividend when the market price of the stock was $135 a share.

Required:

(1)

Journalize the entries to record

(a)

the declaration of the dividend, capitalizing an amount equal to market value

(b)

the issuance of the stock certificates

(2)

Determine the following amounts before the stock dividend was declared:

(a)

Total paid-in capital

(b)

Total retained earnings

(c)

Total stockholders’ equity

(3)

Determine the following amounts after the stock dividend was declared and closing

entries were recorded at the end of the year:

(a)

Total paid-in capital

(b)

Total retained earnings

(c)

Total stockholders’ equity

(1)

(a)

Stock Dividends

270,000

*Stock Dividends Distributable

(2,000 × $100)

Paid-In Capital in Excess of Par—

*[($10,000,000/$100) × $135]× 2%

(b)

Stock Dividends Distributable

200,000

Common Stock

(2)

(a)

$12,000,000 ($10,000,000 + $2,000,000)

(b)

$45,000,000

(c)

$57,000,000 ($12,000,000 + $45,000,000)

(3)

(a)

$12,270,000 ($12,000,000 + $270,000)

(b)

$44,730,000 ($45,000,000 – $270,000)

(c)

$57,000,000 ($12,270,000 + $44,730,000)

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

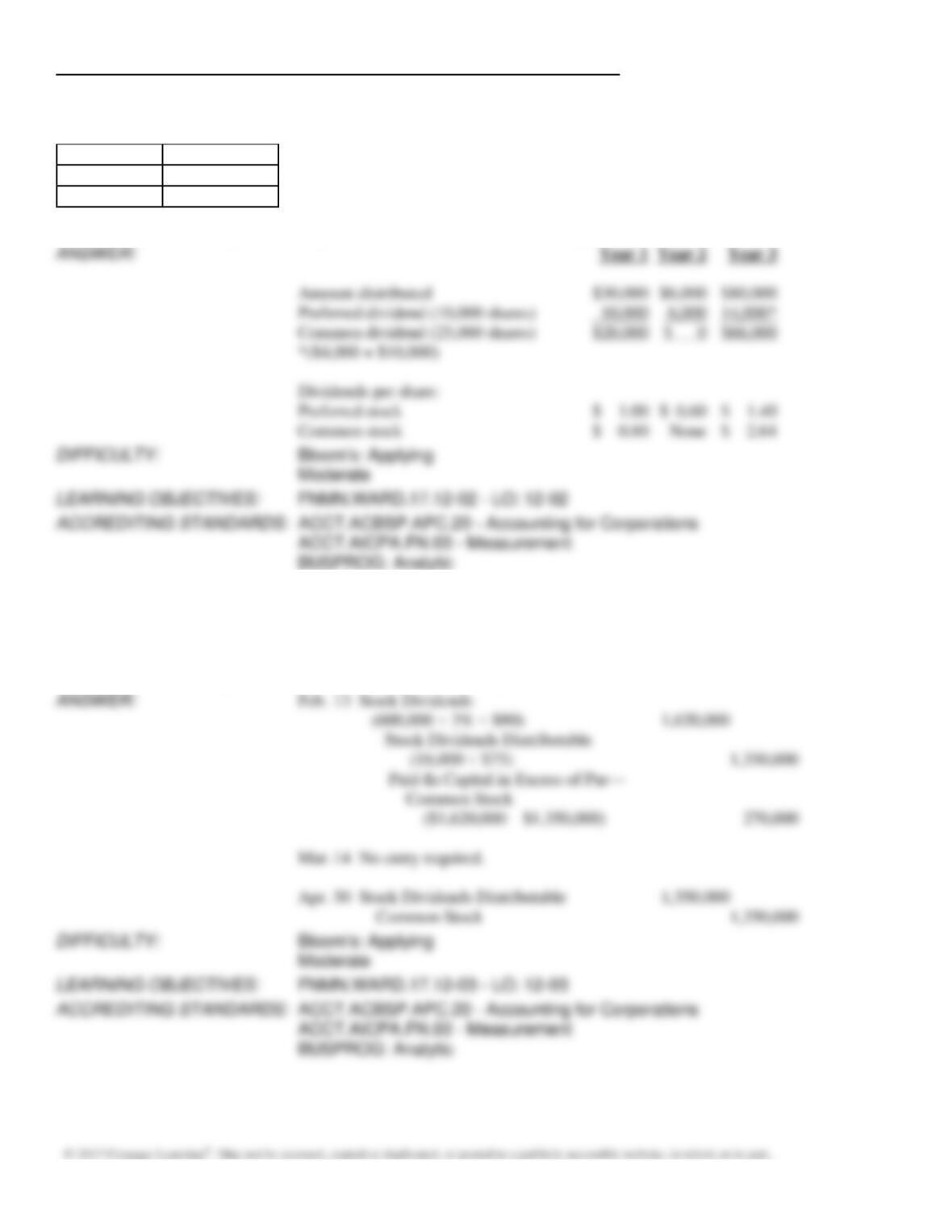

191. Macy Company has 10,000 shares of 2% cumulative preferred stock of $50 par and 25,000 shares of $75 par

common stock. The following amounts were distributed as dividends:

Year 1:

$30,000

Year 2:

6,000

Year 3:

80,000

Determine the dividends per share for preferred and common stock for each year.

192. Solar Company has 600,000 shares of $75 par common stock outstanding. On February 13, Solar declared a 3%

stock dividend to be issued on April 30 to stockholders of record on March 14. The market price of the stock was $90 per

share on February 13.

Journalize the entries required on February 13, March 14, and April 30.

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

193. The following transactions took place for the XYZ Corporation:

November 12 – Declared a total cash dividend of $45,000 for stockholders of record November 20 payable on December

1. Record the journal entries required by these events.

Briefly describe the significance of November 20.

194. Sabas Company has 20,000 shares of $100 par, 1% noncumulative preferred stock and 100,000 shares of $50 par

common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

15,000

Year 3:

90,000

Determine the dividends per share for preferred and common stock for each year.

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

195. On January 1, Year 1, a company had the following transactions:

– Issued 10,000 shares of $2.00 par common stock for $12.00 per share.

– Issued 3,000 shares of $50 par, 6% cumulative preferred stock for $70 per share.

– Purchased 1,000 shares of previously issued common stock for $15.00 per share.

– No other shares of stock were issued or outstanding.

The company had the following dividend information available:

Year 1 – No dividend paid

Year 2 – Paid a $2,000 total dividend

Year 3 – Paid a $20,000 total dividend

Year 4 – Paid a $25,000 total dividend

Using the following format, fill in the correct values for each year:

Year 1

Year 2

Year 3

Year 4

Common stock dividend

Preferred stock dividend

Dividends in arrears

Dividends in arrears

$ 5,000

LEARNING OBJECTIVES:

196. Journalize the following selected transactions completed during the current fiscal year:

Mar. 4

The board of directors of New Town, Inc. declared a stock split that reduced the par of

common shares from $100 to $20. This action increased the number of outstanding

shares to 500,000.

26

Declared a dividend of $1.75 per share on the outstanding shares of common stock.

Apr. 5

Paid the dividend declared on March 26.

Nov. 1

Declared a 5% stock dividend on the common stock outstanding (the fair market value

of the stock to be issued is $25).

Dec. 1

Issued the certificates for the common stock dividend declared on November 1.

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

Mar. 4

Cash Dividends

Apr. 5

Cash Dividends Payable

Nov. 1

Stock Dividends

Stock Dividends Distributable

197. Prepare entries to record the following selected transactions completed during the current fiscal year:

Feb. 1

The board of directors declared a stock split which reduced the par of common shares

from $100 to $20. This action increased the number of outstanding shares to 500,000.

11

Purchased 25,000 shares of the company’s own stock at $44, recording the treasury

stock at cost.

May 1

Declared a dividend of $2.50 per share on the outstanding shares of common stock.

15

Paid the dividend declared on May 1.

Oct. 19

Declared a 2% stock dividend on the common stock outstanding (the fair market value

of the stock to be issued is $55).

Nov. 12

Issued the certificates for the common stock dividend declared on October 19.

Treasury Stock

May 1

Cash Dividends

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

198. Journalize the following selected transactions completed during the current fiscal year:

Jan. 3

The board of directors declared a stock split that reduced the par of common shares

from $100 to $20. This action increased the number of outstanding shares to 400,000.

22

Declared a dividend of $1.75 per share on the outstanding shares of common stock.

Feb. 8

Paid the dividend declared on January 22.

Sept. 1

Declared a 5% stock dividend on the common stock outstanding (the fair market value

of the stock to be issued is $30).

Oct. 1

Issued the certificates for the common stock dividend declared on September 1.

Cash Dividends

Cash Dividends Payable

Sept. 1

Stock Dividends

Paid-In Capital in Excess of

Par—Common Stock

Stock Dividends Distributable

Oct. 19

Stock Dividends

Nov. 12

Stock Dividends Distributable

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

199. Selected transactions completed by Breezeway Construction during the current fiscal year are as follows:

February 3

Split the common stock 2-for-1 and reduced the par from $40 to $20

per share. After the split, there were 250,000 common shares

outstanding.

April 10

Declared semiannual dividends of $1.50 on 18,000 shares of preferred

stock and $0.08 on the common stock to stockholders of record on

May 10, payable on June 9.

June 9

Paid the cash dividends.

October 10

Declared semiannual dividends of $1.50 on the preferred stock and

$0.04 on the common stock (before the stock dividend). In addition, a

2% common stock dividend was declared on the common stock

outstanding. The fair market value of the common stock is estimated

at $36.

December 9

Paid the cash dividends and issued the certificates for the common

stock dividend.

Journalize the transactions.

No entry required.

Cash Dividends

Cash Dividends Payable

Cash Dividends Payable

Stock Dividends

Cash Dividends Payable

Stock Dividends Distributable

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

200. A company has 10,000 shares of $10 par common stock outstanding. Prepare entries to record the following:

(a)

Purchased 1,500 shares of treasury stock at $16. The treasury stock is accounted for by the

cost method. There were no previous purchases of treasury shares.

(b)

Sold 1,000 shares of treasury stock at $19.

(c)

Purchased equipment for $80,000, paying $25,000 in cash and issuing 4,000 shares of

common stock for the remaining.

(d)

Sold 500 shares of treasury stock at $14.

Treasury Stock

Cash

Equipment

Stock

Cash

Paid-In Capital from Sale of Treasury Stock

201. On February 1, Marine Company reacquired 7,500 shares of its common stock at $30 per share. On March 15,

Marine sold 4,500 of the reacquired shares at $34 per share. On June 2, Marine sold the remaining shares at $28 per share.

Journalize the transaction of February 1, March 15, and June 2.

Feb.

Treasury Stock (7,500 × $30)

Cash

Mar.

Cash (4,500 × $34)

[4,500 × ($34-$30)]

June

Cash (3,000 × $28)

Treasury Stock (3,000 × $30)

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

202. On April 2 a corporation purchased for cash 5,000 shares of its own $10 par common stock at $16 a share. It sold

3,000 of the treasury shares at $19 a share on June 10. The remaining 2,000 shares were sold on November 10 for $12 a

share.

(a)

Journalize the entries to record the purchase (treasury stock is recorded at cost).

(b)

Journalize the entries to record the sale of the stock.

Treasury Stock(5,000 × $16)

Cash (3,000 × $19)

November 10

Cash (2,000 × $12)

203. On June 5, Belen Corporation reacquired 3,300 shares of its own common stock at $45 per share. On July 15, Belen

sold 2,000 of the reacquired shares at $48 per share. On August 30, Belen sold the remaining shares at $42 per share.

Journalize the transactions of June 5, July 15, and August 30.

June 5

Treasury Stock (3,300 × $45)

July 15

Cash (2,000 × $48)

Aug. 30

Cash (1,300 × $42)

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

204. On March 4 of the current year, Barefoot Bay, Inc. reacquired 5,000 shares of its common stock at $89 per share. On

August 7, Barefoot Bay sold 3,500 of the reacquired shares at $100 per share. The remaining 1,500 shares were sold at

$88 per share on November 29.

(a)

Journalize the transaction of March 4, August 7, and November 29.

(b)

What is the balance in Paid-in Capital from Sale of Treasury Stock on December

31 of the current year?

(c)

Why might Barefoot Bay Inc. have purchased the treasury stock?

(a)

Mar.

Treasury Stock

445,000

Aug.

Cash

311,500

Nov.

Cash

Paid-In Capital from Sale of

133,500

(b)

$37,000 credit

205. At December 31, Idaho Company had the following ending account balances:

Retained Earnings: $250,000

Preferred Stock ($100 par, 7% cumulative, 10,000 authorized, 5,000 issued and outstanding): $500,000

Treasury Stock: $40,000

Paid-In Capital in Excess of Par—Common Stock: $625,000

Paid-In Capital in Excess of Par—Preferred Stock: $50,000

Common Stock ($5 par value, 500,000 shares authorized, 105,000 issued): $525,000

Prepare the stockholders’ equity section of the balance sheet in good form with all of the required disclosures.

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

206. Using the following accounts and balances, prepare the stockholders’ equity section of the balance sheet. Fifty

thousand shares of common stock are authorized, and 5,000 shares have been reacquired.

Common Stock, $50 par

$1,250,000

Paid-In Capital in Excess of Par

800,000

Paid-In Capital from Sale of Treasury Stock

42,000

Retained Earnings

4,350,000

Treasury Stock

155,000

issued)

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

207. Big Bluestem Inc. reported the following results for the year ending April 30:

Retained earnings, May 1

$3,750,000

Net income

720,000

Cash dividends declared

80,000

Stock dividends declared

220,000

Prepare a retained earnings statement for the fiscal year ended April 30.

208. Using the following information, prepare the stockholders’ equity section of the balance sheet. Seventy thousand

shares of common stock are authorized and 7,000 shares have been reacquired.

Common Stock, $75 par

$4,725,000

Paid-In Capital in Excess of Par

679,000

Paid-In Capital from Sale of Treasury Stock

25,200

Retained Earnings

2,032,800

Treasury Stock

600,000

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

209. Firefly, Inc. reported the following results for the year ending July 31:

Retained earnings, August 1

$875,000

Net income

450,000

Cash dividends declared

140,000

Stock dividends declared

60,000

Prepare a retained earnings statement for the fiscal year ended July 31.

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

210. The Torre Company has the following stockholders’ equity account balances in stockholders equity on December 31.

Common Stock – $5 par, 60,000 shares issued

$300,000

Paid-In Capital in Excess of Par—Common Stock

600,000

Preferred Stock – $100 par, 5,000 shares issued

500,000

Paid-In Capital in Excess of Par—Preferred

100,000

Retained Earnings

200,000

Treasury Stock (cost – $12 per share)

60,000

Answer the following questions:

1. How many shares of treasury stock are owned?

2. What was the average market price per share at which common stock was issued?

3. What was the average market price per share at which preferred stock was issued?

4. What is the total value of the paid-in capital portion of stockholders’ equity?

5. What is the total value of stockholders’ equity?

6. How many shares of common stock are outstanding?

7. If net income for the year was $75,000 and a preferred stock dividend of $20,000 was paid,

what was the beginning value of retained earnings? How much is earnings per share for

the year?

Chapter 12 – Corporations: Organization, Stock Transactions, and Dividends

211. Marcos Company, which had 35,000 shares of common stock outstanding, declared a 4-for-1 stock split.

(a)

What will be the number of shares outstanding after the split?

(b)

If the common stock had a market price of $280 per share before the stock

split, what would be an approximate market price per share after the split?

212. A corporation, which had 18,000 shares of common stock outstanding, declared a 3-for-1 stock split.

(a)

What will be the number of shares outstanding after the split?

(b)

If the common stock had a market price of $240 per share before the stock split, what

would be an approximate market price per share after the split?

(c)

Journalize the entry to record the stock split.

outstanding × Ratio of stock split = 18,000 shares × 3 = 54,000

(c)

213. A company had the following stockholders’ equity information available at year-end.

– Issued 11,000 shares of $2.00 par value common stock for $12.00 per share.

– Issued 5,000 shares of $50 par value 6% preferred stock for $70 per share.

– Purchased 1,000 shares of previously issued common stock for $15.00 per share.

– Reported net income of $200,000.

– Declared and paid the preferred stock dividend.

Calculate the earnings per share for the current year.

($200,000 – $15,000)/10,000 common shares = $18.50 EPS