Chapter 12: Accounting for Partnerships and Limited Liability Companies

164.

The capital accounts of Hope and Indiana have balances of $115,000 and $95,000, respectively. Clint and

Casey

are to be admitted to the partnership. Clint buys onefifth of Hope’s interest for $30,000 and onefourth

of

Indiana’s interest for $20,000. Casey contributes $45,000 cash to the partnership, for which he is to receive

ownership equity of $45,000.

Required:

(1)

Journalize the entries to record the admission of (a) Clint and (b) Casey.

(2)

What are the capital balances of each partner after the admission of the new partners?

Chapter 12: Accounting for Partnerships and Limited Liability Companies

165.

Holly and Luke formed a partnership, investing $240,000 and $80,000, respectively. Determine their participation in

the year’s net income of $200,000 under each of the following independent assumptions:

(a)

No agreement concerning division of net income

(b)

Divided in the ratio of original capital investment

(c)

Interest at the rate of 15% allowed on original investments and the remainder divided

in

the ratio of 2:3

(d)

Salary allowances of $50,000 and $70,000, respectively, and the balance divided equally

(e)

Allowance of interest at the rate of 15% on original investments, salary allowances of

$50,000 and $70,000, respectively, and the remainder divided equally

Chapter 12: Accounting for Partnerships and Limited Liability Companies

166.

Holly and Luke formed a partnership, investing $240,000 and $80,000, respectively. Determine their participation in

the year’s net income of $380,000 under each of the following independent assumptions:

(a)

No agreement concerning division of net income

(b)

Divided in the ratio of original capital investment

(c)

Interest at the rate of 15% allowed on original investments and the remainder divided

in

the ratio of 2:3

(d)

Salary allowances of $50,000 and $70,000, respectively, and the balance divided equally

(e)

Allowance of interest at the rate of 15% on original investments, salary allowances of

$50,000 and $70,000, respectively, and the remainder divided equally

Chapter 12: Accounting for Partnerships and Limited Liability Companies

167.

Gleason invested $90,000 in the James and Kirk partnership for ownership equity of $90,000. Prior to the

investment, land was revalued to a market value of $425,000 from a book value of $200,000. James and Kirk

share

net income in a 1:2 ratio.

a.

Provide the journal entry for the revaluation of land.

b.

Provide the journal entry to admit Gleason.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

168.

Gentry, sole proprietor of a hardware business, decides to form a partnership with Noel. Gentry’s accounts are as

follows:

Book Value

Market Value

Cash

$ 25,000

$ 25,000

Accounts Receivable (net)

52,000

45,000

Inventory

112,000

125,000

Land

40,000

100,000

Building (net)

300,000

340,000

Accounts Payable

25,000

25,000

Mortgage Payable

145,000

145,000

Noel agrees to contribute $80,000 for a 20% interest. Journalize the entries to record (a) Gentry’s investment and

(b) Noel’s investment.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

169.

Benson contributed land, inventory, and $22,000 cash to a partnership. The land had a book value of $65,000 and

a

market value of $111,000. The inventory had a book value of $60,000 and a market value of $58,000. The

partnership also assumed a $52,000 note payable owned by Benson that was used originally to purchase the land.

Required:

Provide the journal entry for Benson’s contribution to the partnership.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

170.

Brad Simmons, sole proprietor of a hardware business, decides to form a partnership with Rich Winter. Brad’s

accounts are as follows:

Book Value

Market Value

Cash

$ 30,000

$ 30,000

Accounts Receivable (net)

55,000

45,000

Inventory

112,000

135,000

Land

40,000

100,000

Building (net)

500,000

540,000

Accounts Payable

25,000

25,000

Mortgage Payable

125,000

125,000

Rich agrees to contribute $170,000 for a 20% interest. Journalize the entries to record (a) Brad’s investment and (b)

Rich’s investment.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

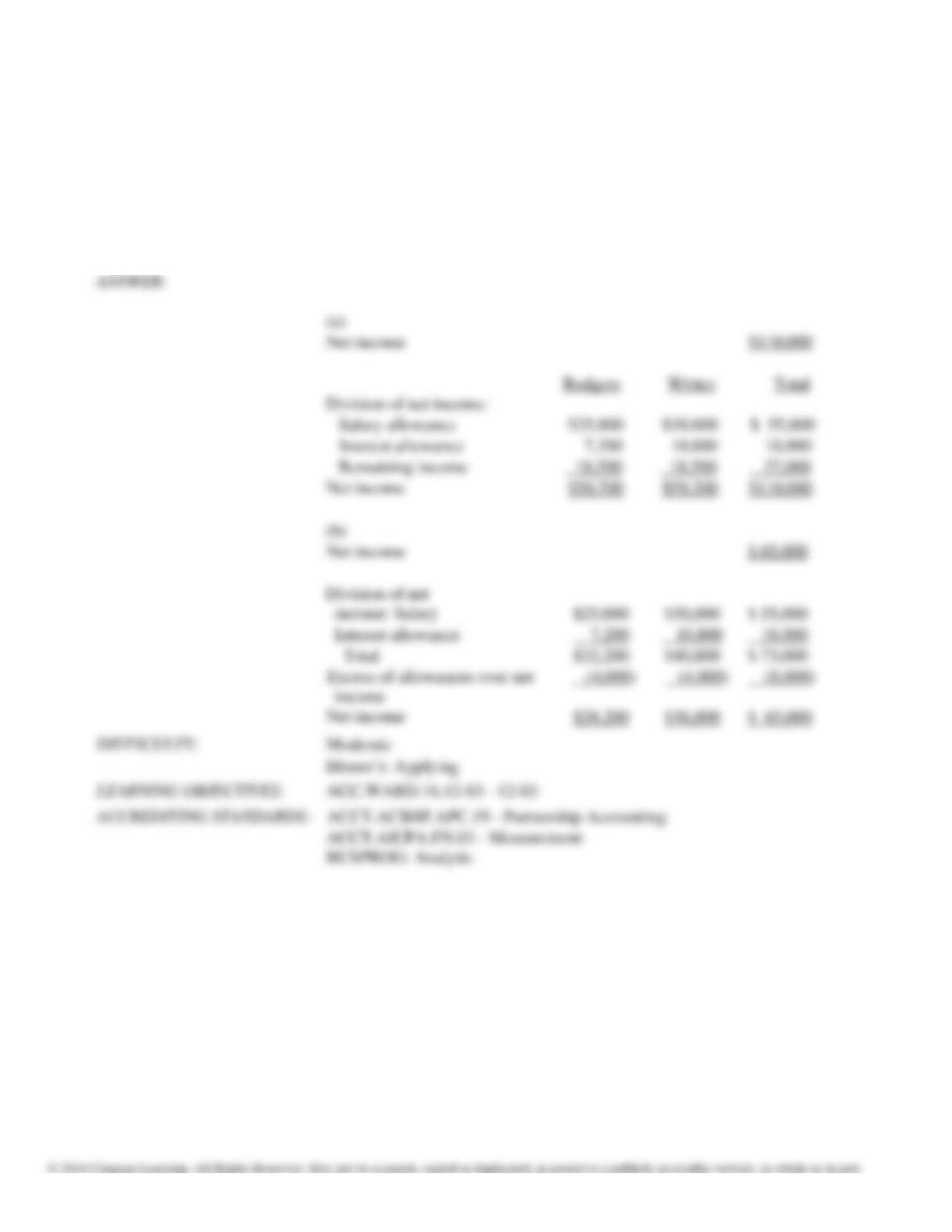

171.

Rodgers and Winter had capital balances of $60,000 and $90,000, respectively, at the beginning of the current

fiscal

year. The articles of partnership provide for salary allowances of $25,000 and $30,000, respectively, an

allowance

of interest at 12% on the capital balances at the beginning of the year; and with the remaining net

income divided

equally. Net income for the current year was $110,000.

(a)

Present the income division section of the income statement for the current year.

(b)

Assuming that the net income had been $65,000 instead of $110,000, present

the

income division section of the income statement for the current year.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

172.

Sharp and Townson had capital balances of $60,000 and $120,000, respectively, on January 1 of the current

year.

On May 8, Sharp invested an additional $10,000 in the partnership. During the year, Sharp and Townson

withdrew $25,000 and $45,000, respectively. After closing all expense and revenue accounts at the end of the

year,

Income Summary has a credit balance of $90,000, which Sharp and Townson have agreed to split on a 2:1

basis.

(a)

Journalize the entries to close the income summary account and the drawing accounts.

(b)

Prepare the statement of partnership equity for the current year.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

173.

Reardon and Reese had capital balances of $140,000 and $160,000, respectively, at the beginning of the

current

fiscal year. The partnership agreement provides for salary allowances of $25,000 and $35,000,

respectively, an

allowance of interest at 12% on the capital balances at the beginning of the year, and the

remaining net income

divided equally. Net income for the current year was $120,000.

(a)

Present the income division section of the income statement for the current year.

(b)

Assuming that the net income had been $76,000 instead of $120,000, present

the

income division section of the income statement for the current year.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

174.

Jackson and Campbell have capital balances of $100,000 and $300,000 respectively. Jackson devotes full time

and

Campbell one-half time to the business. Determine the division of $150,000 of net income under each of the

following assumptions:

(a)

No agreement as to division of net income

(b)

In ratio of capital balances

(c)

In ratio of time devoted to business

Chapter 12: Accounting for Partnerships and Limited Liability Companies

175.

Jackson and Campbell have capital balances of $100,000 and $300,000 respectively. Jackson devotes full time

and

Campbell one-half time to the business. Determine the division of $120,000 of net income under each of the

following assumptions:

(a)

No agreement as to division of net income

(b)

In ratio of capital balances

(c)

In ratio of time devoted to business

(d)

Interest of 10% on capital balances and the remainder divided equally

(e)

Interest of 10% on capital balances, salaries of $40,000 to Jackson and $20,000

to

Campbell, and the remainder divided equally

Chapter 12: Accounting for Partnerships and Limited Liability Companies

176.

Derek and Hailey, partners sharing net income in the ratio of 2:1, admit Ben to the partnership in accordance

with

the following agreement:

(1)

Merchandise inventory recorded in the partnership accounts at $62,500 is to be revalued

at

its current replacement price of $68,500.

(2)

Ben is to invest $48,000 in cash for a 30% interest in the partnership, which has total

net

assets (assets minus liabilities) of $130,000 after the inventory is revalued.

(3)

The income-sharing ratio of Derek, Hailey, and Ben is to be 2:1:1.

Required:

(a)

Journalize the entries to record the revaluation of merchandise inventory, and the

admission

of Ben to the partnership.

(b)

A few years later, the capital balances of Derek, Hailey, and Ben were $150,000, $90,000,

and $55,000, respectively. At this time, Kacy is admitted to the partnership by the

purchase

of onehalf of Derek’s interest for $80,000. Journalize the entry to record the

admission of

Kacy to the partnership.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

177.

Kala and Leah, partners in Best Designs, have capital balances of $40,000 and $60,000 respectively. Adam joins

the partnership by buying onehalf of Kala’s interest for $30,000. In addition, because of Adam’s outstanding

sales

skills, the partners agree to increase his interest to 40% if he invests another $10,000. The income-sharing

ratio of

Kala, Leah, and Adam is 4:3:1.

(a)

Journalize the entries to record the admission of Adam to the partnership.

(b)

Immediately after Adam’s admission to the partnership, Leah sells one-fourth of her interest to Denton for

$35,000. Journalize the entry to record this transaction.

178.

Amazon invested $128,000 in the Jungle and River partnership for ownership equity of $128,000. Prior to the

investment, equipment was revalued to a market value of $90,000 from a book value of $72,000. Jungle and

River

share net income in a 2:1 ratio.

Required:

a.

Provide the journal entry for the revaluation of equipment.

b.

Provide the journal entry to admit Amazon.