130. The balance in Premium on Bonds Payable

131. Debtors are interested in the times-interest-earned ratio because they want to

132. Any unamortized premium should be reported on the balance sheet of the issuing corporation as

133. Numbers of times interest charges earned is computed as

134. Balance sheet and income statement data indicate the following:

Bonds payable, 8% (issued 1990, due 2015)

$1,200,000

Preferred 8% stock, $100 par

(no change during the year)

200,000

Common stock, $50 par

(no change during the year)

1,000,000

Income before income tax for year

320,000

Income tax for year

80,000

Common dividends paid

60,000

Preferred dividends paid

16,000

Based on the data presented above, what is the number of times bond interest charges were earned (round to two decimal places)?

135. Balance sheet and income statement data indicate the following:

Bonds payable, 6% (issued 2000, due 2020)

$1,200,000

Preferred 8% stock, $100 par

(no change during the year)

200,000

Common stock, $50 par

(no change during the year)

1,000,000

Income before income tax for year

340,000

Income tax for year

80,000

Common dividends paid

60,000

Preferred dividends paid

16,000

Based on the data presented above, what is the number of times bond interest charges were earned (round to two decimal places)?

136. When the effective-interest method is used, the amortization of the bond premium

137. The Merchant Company issued 10-year bonds on January 1, 2011. The 15% bonds have a face value of

$100,000 and pay interest every January 1 and July 1. The bonds were sold for $117,205 based on the market

interest rate of 12%. Merchant uses the effective-interest method to amortize bond discounts and

premiums. On July 1, 2011, Merchant should record interest expense (round to the nearest dollar) of

138. The Designer Company issued 10-year bonds on January 1, 2011. The 6% bonds have a face value of

$800,000 and pay interest every January 1 and July 1. The bonds were sold for $690,960 based on the market

interest rate of 8%. Designer uses the effective-interest method to amortize bond discounts and premiums. On

July 1, 2011, Designer should record interest expense (round to the nearest dollar) of

139. If a company borrows money from a bank as an installment note, the interest portion of each annual

payment will:

140. On the first day of the fiscal year, Hawthorne Company obtained a $ 88,000, seven-year, 5% installment

note from Sea Side Bank. The note requires annual payments of $15,208, with the first payment occurring on

the last day of the fiscal year. The first payment consists of interest of $4,400 and principal repayment of

$10,808. The journal entry Hawthorne would record to make the first annual payment due on the note would

include:

141. On January 1, 2014, Gemstone Company obtained a $165,000, 10-year, 7% installment note from

Guarantee Bank. The note requires annual payments of $23,492, with the first payment occurring on the last

day of the fiscal year. The first payment consists of interest of $11,550 and principal repayment of $11,942. The

journal entry to record the payment of the first annual amount due on the note would include:

142. On January 1, 2014, Gemstone Company obtained a $165,000, 10-year, 7% installment note from

Guarantee Bank. The note requires annual payments of $23,492, with the first payment occurring on the last

day of the fiscal year. The first payment consists of interest of $11,550 and principal repayment of $11,942. The

journal entry to record the issuance of the installment note for cash on January 1, 2014 would include:

143. On January 1, 2011, Zero Company obtained a $52,000, four-year, 6.5% installment note from Regional

Bank. The note requires annual payments consisting of principal and interest of $15,179, beginning on

December 31, 2011. The December 31, 2011 carrying amount in the amortization table for this installment note

will be equal to:

144. On January 1, 2011, Zero Company obtained a $52,000, four-year, 6.5% installment note from Regional

Bank. The note requires annual payments of $15,179, beginning on December 31, 2011. The December 31,

2012 carrying amount in the amortization table for this installment note will be equal to:

145. On January 1, 2011, Zero Company obtained a $52,000, four-year, 6.5% installment note from Regional

Bank. The note requires annual payments of $15,179, beginning on December 31, 2011. The December 31,

2013 carrying amount in the amortization table for this installment note will be equal to:

146. An installment note payable for a principal amount of $94,000 at 6% interest requires Lawson Company to

repay the principal and interest in equal annual payments of $22,315 beginning December 31, 2014, for each of

the next five years. After the final payment, the carrying amount on the note will be

147. On the first day of the fiscal year, Lisbon Co. issued $1,000,000 of 10-year, 7% bonds for $1,050,000, with

interest payable semiannually. Orange Inc. purchased the bonds on the issue date for the issue price. If the

company uses the straight-line method for amortizing the premium, the journal entry to record the first

semiannual interest payment by Lisbon Co. would include a debit to:

148. On the first day of the fiscal year, Lisbon Co. issued $1,000,000 of 10-year, 7% bonds for $1,050,000, with

interest payable semiannually. Orange Inc. purchased the bonds on the issue date for the issue price. The

journal entry to record the amortization of the premium (by the straight line method) for the year by Lisbon Co.

includes a debit to:

149. On the first day of the fiscal year, Lisbon Co. issued $1,000,000 of 10-year, 7% bonds for $1,050,000, with

interest payable semiannually. Orange Inc. purchased the bonds on the issue date for the issue price. The

journal entry to record the amoritization of the bond premium (by straight-line method) for the year by Orange

Inc. includes a credit to:

150. Match the following terms to the most appropriate answer:

3. the allocation of a premium or discount over the life of a

151. Match the following terms to the most appropriate answer:

4. allows the bond hold to exchange bond for shares of

5. the entire principal of the bond is paid back on maturity

Convertible

152. Sorenson Co., is considering the following alternative plans for financing their company:

Plan I

Plan II

Issue 10% Bonds (at face)

–

$3,000,000

Issue $10 par Common Stock

$4,000,000

$1,000,000

Income tax is estimated at 40% of income.

Determine the earnings per share of common stock under the two alternative financing plans, assuming income before bond interest and income tax

is $1,000,000.

153. Using the following table, what is the present value of $25,000 to be received 5 years, if the market rate is

7% compounded annually?

Periods

10%

1

.95238

.94340

.93458

.90909

2

.90703

.89000

.87344

.82645

3

.86384

.83962

.81630

.75132

4

.82270

.79209

.76290

.68301

5

.78353

.74726

.71299

.62092

6

.74622

.70496

.66634

.56447

7

.71068

.66506

.62275

.51316

9

.64461

.59190

.54393

.42410

.61391

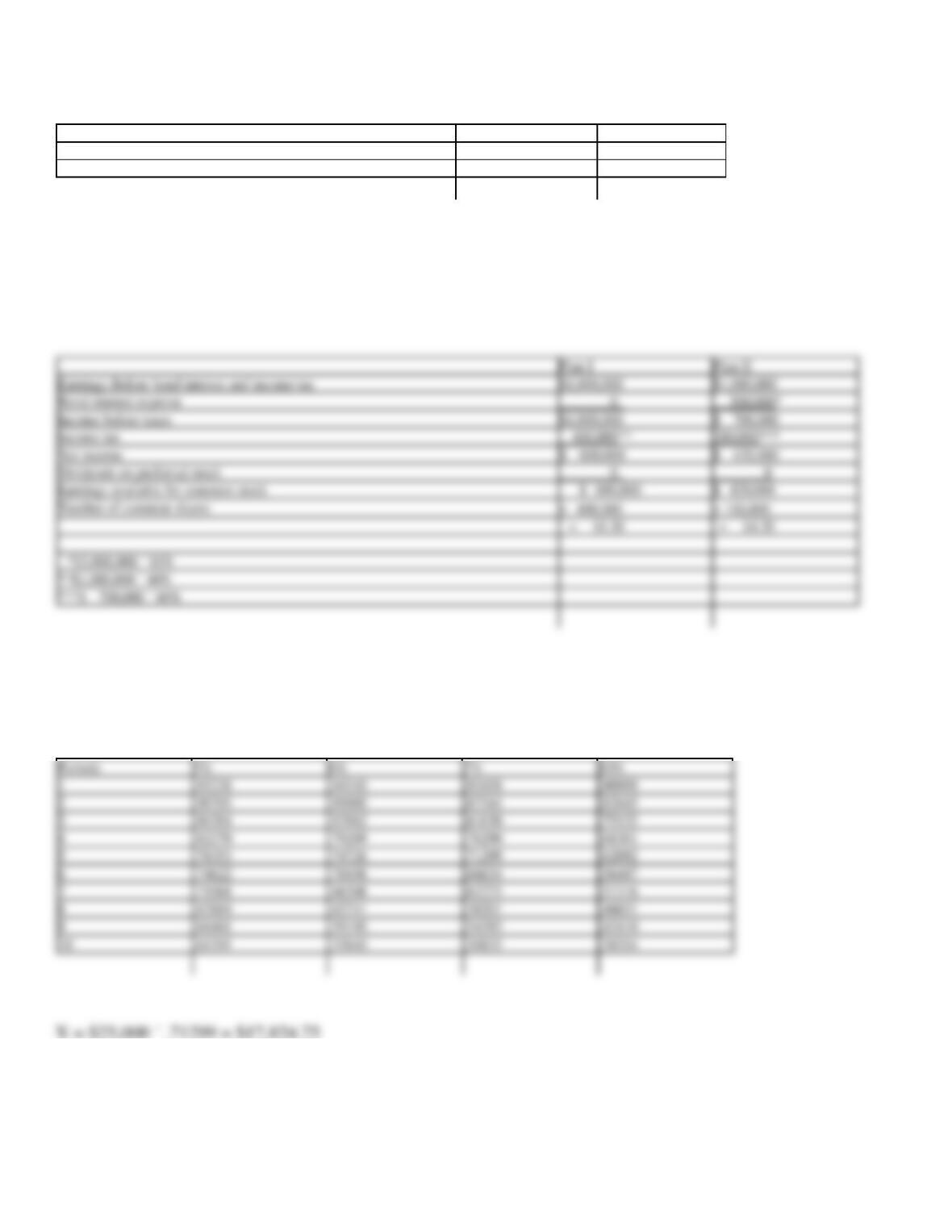

.55840

.50835

.38554

Plan I

Plan II

Earnings Before bond interest and income tax

$1,000,000

$1,000,000

Bond interest expense

300,000*

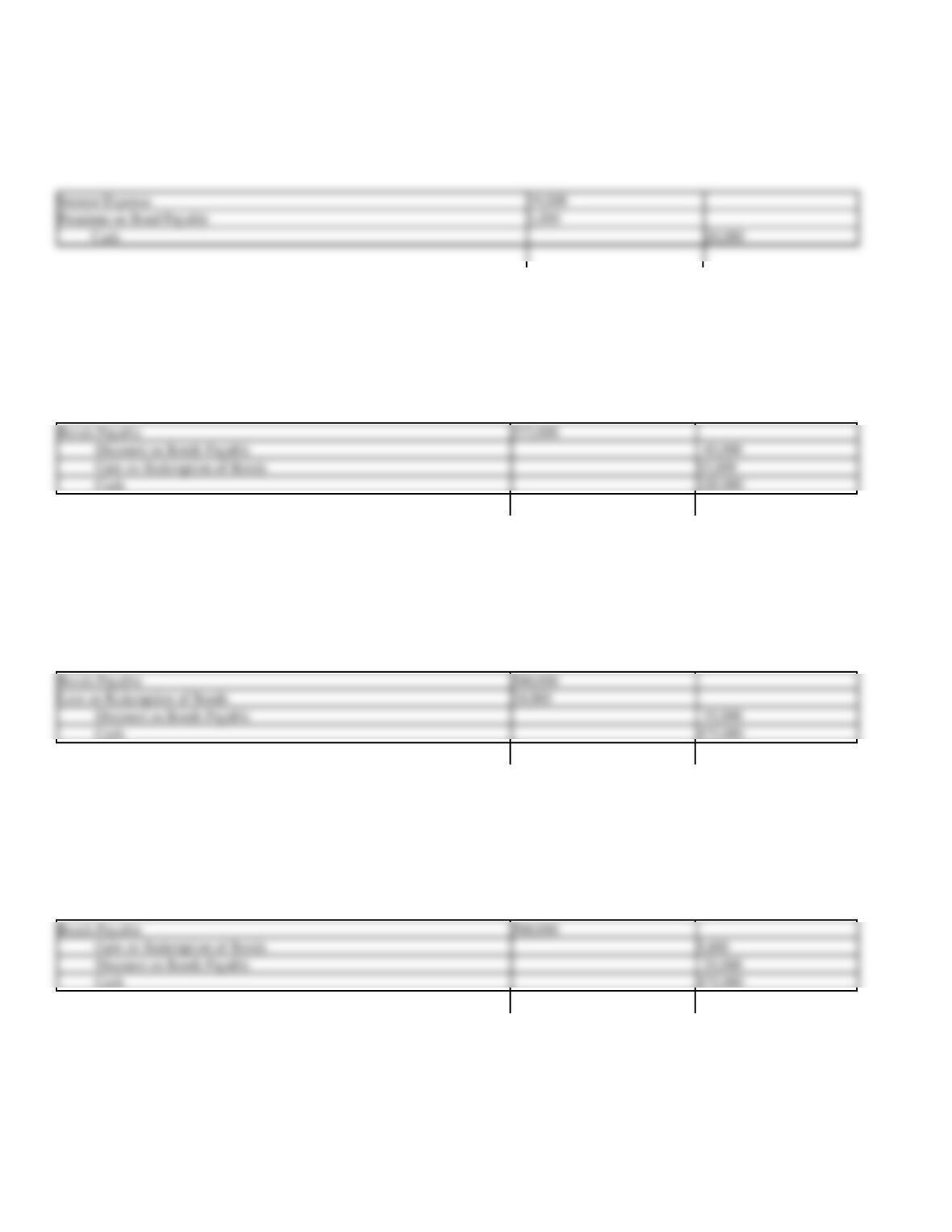

Income before taxes

$1,000,000

$ 700,000

Income tax

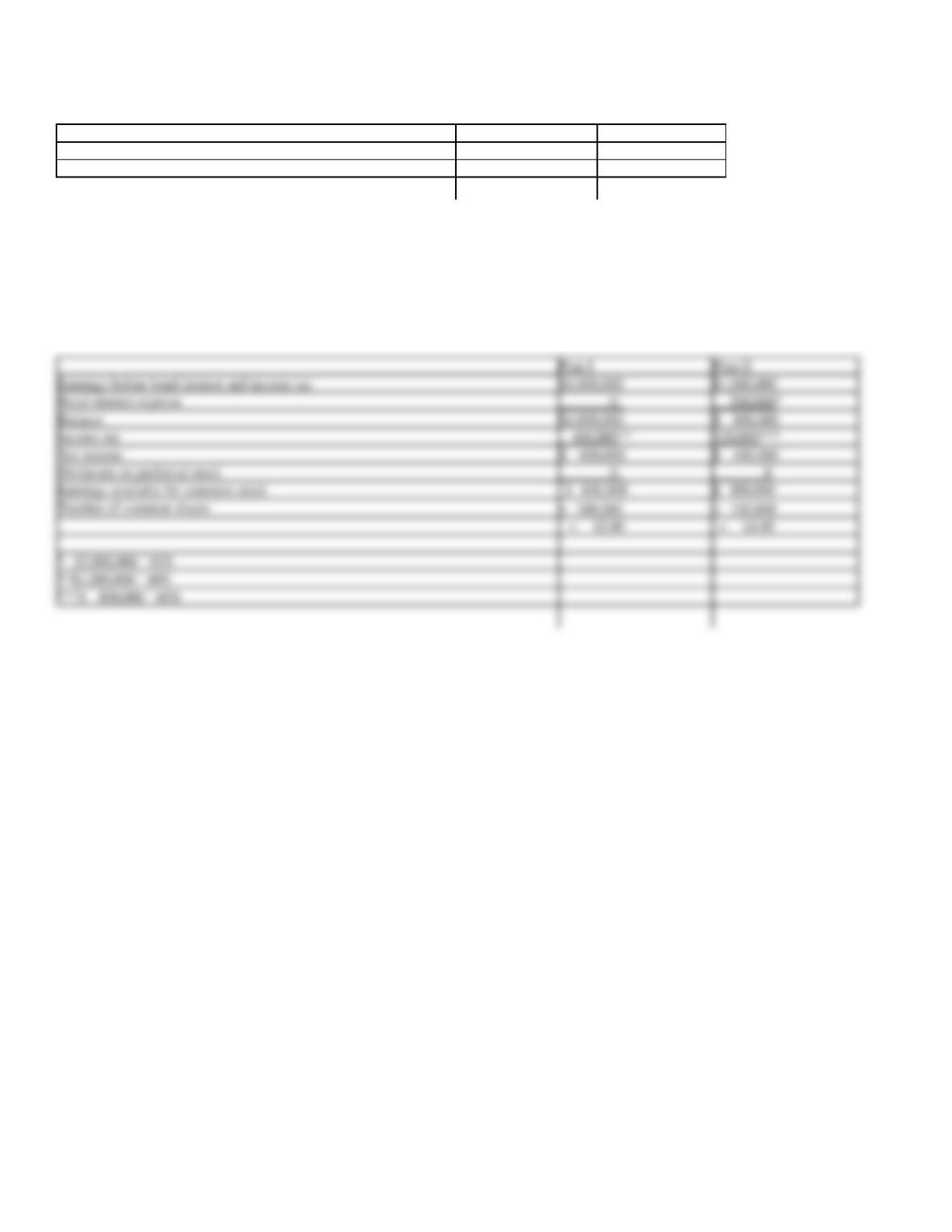

400,000**

Net income

$ 600,000

$ 420,000

Dividends on preferred stock

Earnings available for common stock

$ 600,000

$ 420,000

= $1.50

= $4.20

*$3,000,000 ´ 10%

**$1,000,000 ´ 40%

***$ 700,000 ´ 40%

154. Using the following table, what is the present value of $5,000 to be received 5 years, if the market rate is

10% compounded annually?

155. Use the following tables to calculate the present value of a $25,000 7%, 5 year bond that pays $1,750

($25,000 ´ 7%) interest annually, if the market rate of interest is 7%

Present Value of $1 at Compound Interest

Periods

5%

6%

7%

10%

1

.95238

.94340

.93458

.90909

2

.90703

.89000

.87344

.82645

3

.86384

.83962

.81630

.75132

4

.82270

.79209

.76290

.68301

5

.78353

.74726

.71299

.62092

6

.74622

.70496

.66634

.56447

7

.71068

.66506

.62275

.51316

8

.67684

.62741

.58201

.46651

9

.64461

.59190

.54393

.42410

10

.61391

.55840

.50835

.38554

156. On the first day of the fiscal year, a company issues a $1,000,000, 7%, 5 year bond that pays semi-annual

interest of $35,000 ($1,000,000 ´ 7% ´ 1/2), receiving cash of $884,171. Journalize the entry to record the

issuance of the bonds.

Cash

884,171

Periods

10%

1

.95238

.94340

.93458

.90909

2

1.85941

1.83339

1.80802

1.73554

3

2.72325

2.67301

2.62432

2.48685

4

3.54595

3.46511

3.38721

3.16987

5

4.32948

4.21236

4.10020

3.79079

6

5.07569

4.91732

4.76654

4.35526

7

5.78637

5.58238

5.38929

4.86842

8

6.46321

6.20979

5.97130

5.33493

9

7.10782

6.80169

6.51523

5.75902

10

7.72174

7.36009

7.02358

6.14457

Total present value of bonds

$25,000*

157. On the first day of the fiscal year, a company issues a $500,000, 8%, 10 year bond that pays semi-annual

interest of $20,000 ($500,000 ´ 8% ´ 1/2), receiving cash of $437,740. Journalize the entry to record the

issuance of the bonds.

158. On the first day of the fiscal year, a company issues a $1,000,000, 7%, 5 year bond that pays semi-annual

interest of $35,000 ($1,000,000 ´ 7% ´ 1/2), receiving cash of $884,171. Journalize the first interest payment

and the amortization of the related bond discount using the straight-line method. Round answer to the nearest

dollar.

159. On the first day of the fiscal year, a company issues a $800,000, 6%, 5 year bond that pays semi-annual

interest of $24,000 ($800,000 ´ 6% ´ 1/2), receiving cash of $690,960. Journalize the entry to record the first

interest payment and the amortization of the related bond discount using the straight-line method.

160. On the first day of the fiscal year, a company issues a $500,000, 8%, 10 year bond that pays semi-annual

interest of $20,000 ($500,000 ´ 8% ´ 1/2), receiving cash of $530,000. Journalize the entry to record the

issuance of the bonds.

161. On the first day of the fiscal year, a company issues a $500,000, 8%, 10 year bond that pays semi-annual

interest of $20,000 ($500,000 ´ 8% ´ 1/2), receiving cash of $520,000. Journalize the entry to record the first

interest payment and amortization of premium using the straight-line method.

162. A $375,000 bond issue on which there is an unamortized discount of $40,000 is redeemed for

$320,000. Journalize the redemption of the bonds.

163. A $500,000 bond issue on which there is an unamortized discount of $35,000 is redeemed for

$475,000. Journalize the redemption of the bonds.

164. A $500,000 bond issue on which there is an unamortized discount of $20,000 is redeemed for

$475,000. Journalize the redemption of the bonds.

165. On January 1, 2015, Yeargan Company obtained an $125,000, seven year 5% installment note from

Farmers Bank. The note requires annual payments of $21,602, with the first payment occurring on the last day

of the fiscal year. The first payment consists of $6,250 interest and principal repayment of $15,352.

Requirement:

(1)

Journalize the following entries:

a.

Issued the installment notes for cash on January 1, 2015.

b.

Paid the first annual payment on the note.

(2)

Determine the amount of interest expense on the note for the first

year.

(1)

a.

Cash

125,000

Notes Payable

125,000

Cash

21,602

166. Jenson Co., is considering the following alternative plans for financing their company:

Plan I

Plan II

Issue 10% Bonds (at face)

–

$2,000,000

Issue $10 Common Stock

$3,000,000

$1,000,000

Income tax is estimated at 40% of income.

Determine the earnings per share of common stock under the two alternative financing plans, assuming income before bond interest and income tax

is $1,000,000.

Plan I

Plan II

Earnings before bond interest and income tax

$1,000,000

$1,000,000

Bond interest expense

200,000*

Balance

$1,000,000

$ 800,000

Income tax

400,000**

Net income

$ 600,000

$ 480,000

Dividends on preferred stock

Earnings available for common stock

$ 600,000

$ 480,000

= $2.00

= $4.80

* $2,000,000 ´ 10%

**$1,000,000 ´ 40%

***$ 800,000 ´ 40%

167. Ulmer Company is considering the following alternative financing plans:

Plan 1

Plan 2

Issue 8% bonds at face value

$2,000,000

$1,000,000

Issue preferred stock, $15 par

—

1,500,000

Issue common stock, $10 par

2,000,000

1,500,000

Income tax is estimated at 35% of income. Dividends of $1 per share were declared and paid on the preferred stock.

Required: Determine the earnings per share of common stock, assuming income before bond interest and income tax is $600,000.

168. Given the following data, determine the times interest earned ratio.

Plan 1

Plan 2

Earnings before bond interest and income tax

$600,000

$600,000

Bond interest

Balance

$440,000

$520,000

Income tax

Net income

$286,000

$338,000

Dividends on preferred stock

0

100,000

Earnings available for common stock

$286,000

238,000

Number of common shares

¸200,000

¸150,000

Earnings per share on common stock

$ 1.43

$ 1.59

169. Given the following data, prepare the journal entry to record interest expense and any related amortization

on December 31st of the first year using the effective method. Assume interest is paid annually on January 1.

The bonds were issued on January 1 for $7,411,233.

170. Given the following data, prepare an amortization table (use the effective method)

1/1/10 – issue $800,000, 9%, 3 year bonds, interest paid annually on 12/31, to yield 8%

Use the following format (round to nearest dollar – may have a slight rounding difference);