Page 1

1.

If a California avocado stand operates in a perfectly competitive market, that stand

owner will be a price:

A)

maker.

B)

taker.

C)

discriminator.

D)

maximizer.

2.

If all firms in an industry are price takers:

A)

each firm can sell at the price it wants to charge, provided it is not too different

from the prices other firms are charging.

B)

each firm takes the market price as given for its output level, recognizing that the

price will change if it alters its output significantly.

C)

an individual firm cannot alter the market price even if it doubles its output.

D)

the market sets the price, and each firm can take it or leave it by setting a different

price.

3.

The assumptions of perfect competition imply that:

A)

individuals in the market accept the market price as given.

B)

individuals can influence the market price.

C)

the price will be fair.

D)

the price will be high.

4.

Price takers are individuals in a market who:

A)

select a price from a wide range of alternatives.

B)

select the lowest price available in a competitive market.

C)

select the average of prices available in a competitive market.

D)

have no ability to affect the price of a good in a market.

5.

Individuals in a market who must take the market price as given are:

A)

quantity minimizers.

B)

quantity takers.

C)

price takers.

D)

price searchers.

6.

Perfect competition is characterized by:

A)

rivalry in advertising.

B)

fierce quality competition.

C)

the inability of any one firm to influence price.

D)

widely recognized brands.

Page 2

7.

When a firm cannot affect the market price of the good that it sells, it is said to be a:

A)

price taker.

B)

natural monopoly.

C)

dominant firm.

D)

cartel.

8.

The assumptions of perfect competition imply that:

A)

individuals in the market determine the market price.

B)

firms in the market accept the market price as given.

C)

there will be no new competition due to natural monopolies.

D)

the price will be decreasing yearly.

9.

In the model of perfect competition:

A)

the consumer is at the mercy of powerful firms that can set prices wherever they

prefer.

B)

individual firms can influence the price, but only slightly.

C)

no individual or firm has enough power to affect price.

D)

the price is determined by how many years are left in the product’s patent.

10.

A perfectly competitive firm is a:

A)

price taker.

B)

price searcher.

C)

cost maximizer.

D)

quantity taker.

11.

If a Florida strawberry wholesaler operates in a perfectly competitive market, that

wholesaler will have a _____ share of the market, and consumers will consider her

strawberries and her competitors’ strawberries to be _____. Therefore, _____

advertising will take place in this market.

A)

large; standardized; no

B)

small; standardized; little or no

C)

small; differentiated; no

D)

large; differentiated; extensive

12.

One characteristic of a perfectly competitive market is that there are _____ sellers of the

good or service.

A)

one or two

B)

a few

C)

usually fewer than 10

D)

many

Page 3

13.

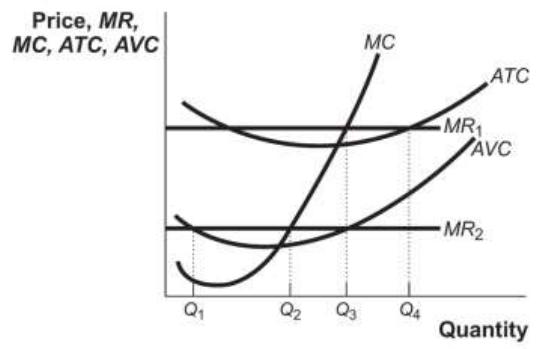

Which of the following is NOT a characteristic of a perfectly competitive industry?

A)

Firms seek to maximize profits.

B)

Profits may be positive in the short run.

C)

There are many firms.

D)

Products are differentiated.

14.

In a perfectly competitive industry, each firm:

A)

is a price maker.

B)

produces about half of the total industry output.

C)

produces a differentiated product.

D)

produces a standardized product.

15.

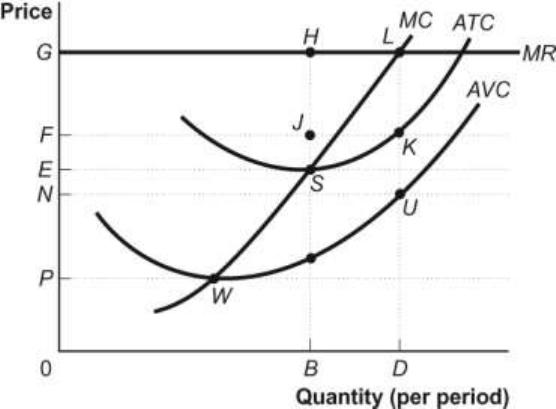

For the Colorado beef industry to be classified as perfectly competitive, ranchers in

Colorado must have _____ on prices and beef must be a _____ product.

A)

no noticeable effect; standardized

B)

a huge effect; standardized

C)

a huge effect; differentiated

D)

no noticeable effect; differentiated

16.

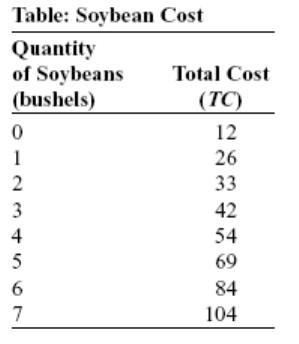

Which of the following is a necessary condition for perfect competition?

A)

A small number of firms control a large share of the total market.

B)

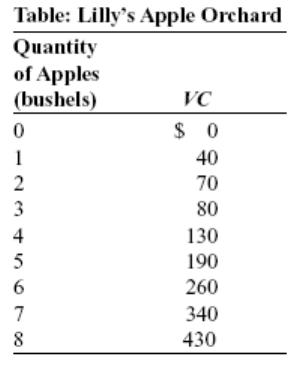

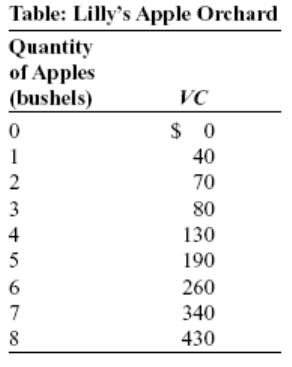

Movement into and out of the market is limited.

C)

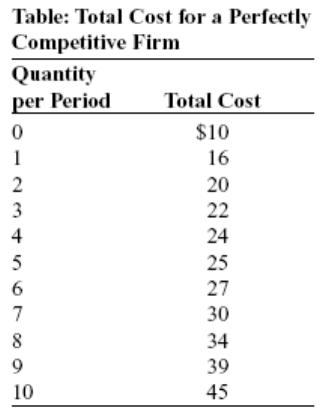

Firms produce a standardized product.

D)

Extensive advertising is used to promote the firm’s product.

17.

Which of the following statements is NOT characteristic of perfect competition?

A)

All firms produce the same standardized product.

B)

There are many producers, and each has only a small market share.

C)

There are many producers; one firm has a 25% market share, and all of the

remaining firms have a market share of less than 2% each.

D)

There are no obstacles to entry into or exit from the industry.

18.

The perfectly competitive model assumes all of the following EXCEPT:

A)

a great number of buyers.

B)

easy entry to and exit from the market.

C)

a standardized product.

D)

that firms attempt to maximize their total revenue.

Page 4

19.

The market for breakfast cereal contains hundreds of similar products, such as Froot

Loops, cornflakes, and Rice Krispies, that are considered to be different products by

different buyers. This situation violates the perfect competition assumption of:

A)

many buyers and sellers.

B)

a standardized product.

C)

ease of entry.

D)

ease of exit.

20.

An assumption of the model of perfect competition is:

A)

discrimination.

B)

difficult entry and exit.

C)

many buyers and sellers.

D)

limited information.

21.

The competitive model assumes all of the following EXCEPT:

A)

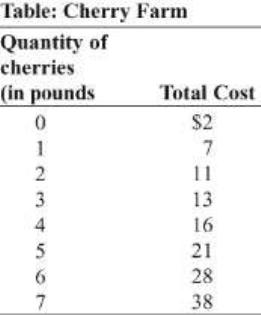

a large number of buyers.

B)

easy entry to and exit from the market.

C)

standardized product.

D)

patents and copyrights that serve as barriers to entry into the industry.

22.

_____ almost always take the market price as given—that is, are considered _____—but

this is often not true of _____.

A)

Consumers; quantity minimizers; producers

B)

Producers; quantity takers; consumers

C)

Consumers and producers; price takers; firms that produce a differentiated product

D)

Producers; price searchers; consumers

23.

An assumption of the model of perfect competition is:

A)

identical goods.

B)

difficult entry and exit.

C)

few buyers and sellers.

D)

cooperation and interdependence between sellers.

24.

People in the eastern part of Beirut are prevented by border guards from traveling to the

western part of Beirut to shop for or sell food. This situation violates the perfect

competition assumption of:

A)

price-setting behavior.

B)

a small number of buyers and sellers.

C)

differentiated goods.

D)

ease of entry and exit.

Page 5

25.

When perfect competition prevails, which of the following characteristics of firms are

we likely to observe?

A)

They erect and maintain barriers to new firms.

B)

There are not many of them.

C)

They all try to highlight the substantial product differentiation between producers.

D)

They are all price takers.

26.

In perfect competition:

A)

a firm’s total revenue is found by multiplying the market price by the firm’s

quantity of output.

B)

the firm’s total revenue curve is a downward-sloping line.

C)

at any price, the more sold, the higher a firm’s marginal revenue.

D)

the firm’s total revenue curve is nonlinear.

27.

A firm’s total output times the price at which it sells that output is _____ revenue.

A)

net

B)

total

C)

average

D)

marginal

28.

Total revenue is a firm’s:

A)

change in revenue resulting from a unit change in output.

B)

ratio of revenue to quantity.

C)

difference between revenue and cost.

D)

total output times the price of that output.

29.

If a perfectly competitive firm increases production from 10 units to 11 units and the

market price is $20 per unit, total revenue for 11 units is:

A)

$10.

B)

$20.

C)

$200.

D)

$220.

30.

If a perfectly competitive firm decreases production from 11 units to 10 units and the

market price is $20 per unit, total revenue for 10 units is:

A)

$10.

B)

$20.

C)

$200.

D)

$210.

Page 6

31.

The difference between total revenue and total cost is:

A)

economic profit or loss.

B)

nominal revenue.

C)

average revenue.

D)

marginal revenue.

32.

In a perfectly competitive industry, the market demand curve is usually:

A)

perfectly inelastic.

B)

perfectly elastic.

C)

downward-sloping.

D)

relatively elastic.

33.

The demand curve for a perfectly competitive firm is:

A)

perfectly inelastic.

B)

perfectly elastic.

C)

downward-sloping.

D)

relatively but not perfectly elastic.

34.

Marginal revenue:

A)

is the slope of the average revenue curve.

B)

equals the market price in perfect competition.

C)

is the change in quantity divided by the change in total revenue.

D)

is the price divided by the change in quantity.

35.

The marginal revenue received by a firm in a perfectly competitive market:

A)

is greater than the market price.

B)

is less than the market price.

C)

is equal to its average revenue.

D)

increases with the quantity of output sold.

36.

If a perfectly competitive gardening shop sells 30 evergreen bushes at $10 per bush, its

marginal revenue is:

A)

$10.

B)

more than $10.

C)

less than $10.

D)

$300.

Page 7

37.

Marginal revenue is a firm’s:

A)

ratio of profit to quantity.

B)

ratio of average revenue to quantity.

C)

price per unit times the number of units sold.

D)

increase in total revenue when it sells an additional unit of output.

38.

Perfectly competitive firms will:

A)

maximize total revenue by using the marginal decision rule.

B)

increase output up to the point that the marginal benefit of an additional unit of

output is greater than the marginal cost.

C)

increase output up to the point that the marginal benefit of an additional unit of

output is equal to the marginal cost.

D)

always attempt to minimize average variable cost.

39.

For a perfectly competitive firm, marginal revenue:

A)

is less than price.

B)

is greater than price.

C)

decreases as the firm increases output.

D)

is equal to price.

40.

A perfectly competitive firm will maximize profits when the:

A)

marginal revenue equals marginal cost.

B)

marginal revenue is lower than average variable cost.

C)

price is lower than marginal cost.

D)

price is higher than marginal cost.

41.

The equilibrium price of a guidebook is $35 in the perfectly competitive guidebook

industry. Our firm produces 10,000 guidebooks for an average total cost of $38,

marginal cost of $30, and average variable cost of $30. Our firm should:

A)

raise the price of guidebooks, because the firm is losing money.

B)

keep output the same, because the firm is producing at minimum average variable

cost.

C)

produce more guidebooks, because the next guidebook produced increases profit

by $5.

D)

shut down, because the firm is losing money.

Page 8

42.

Zoe’s Bakery operates in a perfectly competitive industry and has standard cost curves.

The variable costs at Zoe’s Bakery increase, so all of the cost curves (except fixed cost)

shift upward. The demand for Zoe’s pastries does not change, nor does the firm shut

down. To maximize profits after the variable cost increase, Zoe’s Bakery will _____ its

price and _____ its level of production.

A)

raise; increase

B)

decrease; increase

C)

raise; decrease

D)

do nothing to; decrease

43.

The slope of the total revenue curve is:

A)

marginal cost.

B)

net revenue.

C)

equal to marginal revenue and is constant under perfect competition.

D)

equal to marginal revenue and varies under perfect competition.

44.

The slope of the total cost curve is:

A)

marginal cost.

B)

marginal revenue.

C)

constant under perfect competition.

D)

always negative.

45.

For a firm producing at any level of output LOWER THAN the most profitable one, an

increase in output adds:

A)

more to total cost than to total revenue.

B)

more to total revenue than to total cost.

C)

the same amount to total revenue as to total cost.

D)

to total revenue but not to total cost.

46.

For a firm producing at any level of output GREATER THAN the most profitable one, a

reduction in output decreases total revenue _____ total cost.

A)

less than

B)

more than

C)

by the same amount as

D)

but not

Page 9

47.

A perfectly competitive firm maximizes profit in the short run by producing the quantity

at which:

A)

TR = TC.

B)

MR = MC.

C)

Q × (P – ATC) = 0.

D)

P < AVC.

48.

The price received by a firm in a perfectly competitive market:

A)

is equal to the market price.

B)

is less than the market price.

C)

is greater than the market price.

D)

decreases with the quantity of output sold by the firm.

49.

The marginal revenue received by a firm in a perfectly competitive market:

A)

is unrelated to the market price.

B)

is less than the market price.

C)

is greater than the market price.

D)

is the change in total revenue divided by the change in output.

50.

For a firm in a perfectly competitive market _____ revenue equals _____.

A)

marginal; total revenue

B)

marginal; market price

C)

net; price

D)

net; marginal revenue

51.

If a perfectly competitive firm sells 10 units of output at $30 per unit, its marginal

revenue is:

A)

$10.

B)

$30.

C)

more than $30.

D)

$300.

52.

Price in a perfectly competitive industry:

A)

is determined by each firm, depending on its costs of production.

B)

is always equal to marginal revenue for the firm.

C)

must be greater than average total cost or the firm will shut down in the short run.

D)

is indeterminate in the short run.

Page 10

53.

Marginal revenue is a firm’s:

A)

ratio of the change in total revenue to the change in output.

B)

ratio of average revenue to total revenue.

C)

profit per unit times the number of units sold.

D)

increase in profit when it sells an additional unit of output.

54.

If a firm in perfect competition sells 10 units of output at $5 per unit, its marginal

revenue is:

A)

$5.

B)

more than $5 but less than $50.

C)

$50.

D)

$250.

55.

If a perfectly competitive firm sells 300 units of output at $1 per unit, its marginal

revenue is:

A)

less than $1.

B)

$1.

C)

more than $1 but less than $300.

D)

$300.

56.

In perfect competition:

A)

price and average variable cost are the same.

B)

price and marginal revenue are the same.

C)

price and total revenue are the same.

D)

total revenue and total variable cost are the same.

57.

The profit-maximizing level of output for a perfectly competitive firm in the short run

occurs where _____ equals _____.

A)

marginal cost; price

B)

marginal revenue; price

C)

total revenue; total cost

D)

average revenue; average total cost

58.

If a perfectly competitive firm is producing a quantity where MC > MR, then profit:

A)

is maximized.

B)

can be increased by increasing production.

C)

can be increased by decreasing production.

D)

can be increased by decreasing the price.

Page 11

59.

If a perfectly competitive firm is producing a quantity where MC < MR, then profit:

A)

is maximized.

B)

can be increased by increasing production.

C)

can be increased by decreasing production.

D)

can be increased by decreasing the price.

60.

If a perfectly competitive firm is producing a quantity where MC = MR, then profit:

A)

is maximized.

B)

can be increased by increasing production.

C)

can be increased by decreasing production.

D)

can be increased by decreasing the price.

61.

If a perfectly competitive firm is producing a quantity where P < MC, then profit:

A)

is maximized.

B)

can be increased by decreasing the price.

C)

can be increased by increasing production.

D)

can be increased by decreasing production.

62.

If a perfectly competitive firm is producing a quantity where P > MC, then the firm can

increase profit by:

A)

making no change in output or price because it is already maximizing profit.

B)

increasing the price.

C)

decreasing the price.

D)

increasing production.

63.

If a perfectly competitive firm is producing a quantity where P = MC, then profit:

A)

is maximized.

B)

can be increased by decreasing the quantity.

C)

can be increased by decreasing the price.

D)

can be increased by increasing production.

Page 12

Use the following to answer question 64:

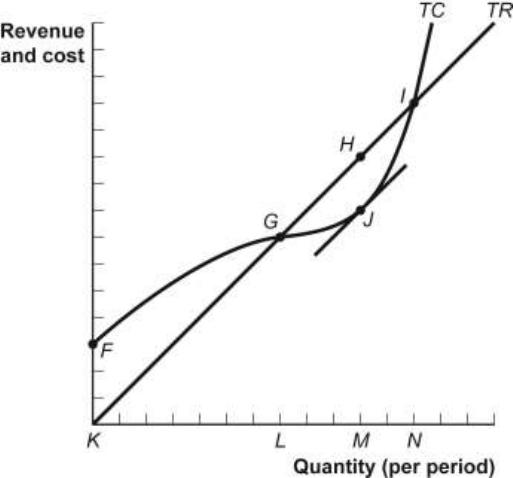

Figure: Total Revenue and Total Cost

64.

(Figure: Total Revenue and Total Cost) Look at the figure Total Revenue and Total

Cost. The most profitable level of output occurs at quantity:

A)

F.

B)

K.

C)

L.

D)

M.

65.

If the price is greater than average total cost at the profit-maximizing quantity of output

in the short run, a perfectly competitive firm will:

A)

produce at a loss.

B)

produce at a profit.

C)

shut down production.

D)

produce more than the profit-maximizing quantity.

66.

In the short run, a perfectly competitive firm produces output and earns an economic

profit if:

A)

P > ATC.

B)

P = ATC.

C)

P < MC.

D)

P < ATC.

Page 13

67.

In the short run, a perfectly competitive firm produces output and earns ZERO

economic profit if:

A)

P < ATC.

B)

P = ATC.

C)

P < MC.

D)

P > ATC.

68.

Which of the following is TRUE?

A)

Profit per unit is price minus MC.

B)

Total economic profit is per-unit profit times quantity.

C)

If price is less than ATC, the firm will break even in the short run.

D)

If price is less than marginal cost, the perfectly competitive firm should raise the

price and increase output.

69.

A perfectly competitive firm will earn a profit in the short run when it produces the

profit-maximizing quantity of output and the price is:

A)

greater than marginal cost.

B)

less than marginal cost.

C)

less than average variable cost.

D)

greater than average total cost.

70.

If the price is greater than average total cost at the profit-maximizing quantity of output

in the short run, a perfectly competitive firm will:

A)

continue to produce at a loss.

B)

produce at a profit.

C)

shut down production.

D)

reduce its fixed costs.

71.

For a perfectly competitive firm in the short run, if the firm produces the quantity at

which _____, the firm _____.

A)

P > ATC; is profitable

B)

P < ATC; breaks even

C)

P = ATC; incurs a loss

D)

P < ATC; is profitable

Page 14

72.

In the short run, a perfectly competitive firm produces output and breaks even if the firm

produces the quantity at which:

A)

P < ATC.

B)

P = ATC.

C)

P > ATC.

D)

P = (TR / Q + TC / Q) × Q.

73.

In the short run, if P = ATC, a perfectly competitive firm:

A)

produces output and earns zero economic profit.

B)

produces output and earns an economic profit.

C)

produces output and incurs an economic loss.

D)

does not produce output and incurs an economic loss.

74.

In the short run, if P > ATC, a perfectly competitive firm:

A)

produces output and earns zero economic profit.

B)

produces output and earns an economic profit.

C)

produces output and incurs an economic loss.

D)

does not produce output and earns economic profit.

75.

In perfectly competitive markets, if the price is _____, the firm will _____.

A)

greater than ATC; make an economic profit

B)

greater than the minimum ATC; break even

C)

less than ATC; make an economic profit

D)

less than ATC; break even

76.

A perfectly competitive firm will earn a profit and will continue producing the

profit-maximizing quantity of output in the short run if the price is:

A)

less than the average fixed cost.

B)

less than marginal cost.

C)

greater than average variable cost but less than average total cost.

D)

greater than average total cost.

77.

Consider a perfectly competitive firm in the short run. Assume the firm produces the

profit-maximizing output and earns economic profits. Which statement is FALSE?

A)

Price is equal to marginal cost.

B)

Price is equal to marginal revenue.

C)

Price is equal to average total cost.

D)

Marginal cost is greater than average total cost.

Page 15

78.

Suppose a perfectly competitive firm can increase its profits by increasing its output.

Then it must be true that the firm’s _____ exceeds its _____.

A)

marginal revenue; marginal cost

B)

price; average total cost but is less than marginal cost

C)

marginal cost; marginal revenue

D)

price; marginal revenue

79.

A competitive firm operating in the short run is producing at the output level at which

ATC is at a minimum. If ATC = $8 and MR = $9, to maximize profits (or minimize

losses), this firm should:

A)

increase output.

B)

reduce output.

C)

increase price.

D)

do nothing; the firm is already maximizing profits.

80.

Zoe’s Bakery operates in a perfectly competitive industry. When the market price of iced

cupcakes is $5, the profit-maximizing output level is 150 cupcakes. Her average total

cost is $4, and her average variable cost is $3. Zoe’s marginal cost is _____, and her

short-run profits are _____.

A)

$5; $150

B)

$5; $300

C)

$1; $150

D)

$1; $300

81.

A perfectly competitive firm is definitely earning an economic profit when:

A)

MR > MC.

B)

P > ATC.

C)

P > MC.

D)

P < ATC.

82.

Mikail’s perfectly competitive camera memory card–producing factory is making

positive economic profits. If the price of memory cards is $9, if Mikail’s output is 3,000

cards a month, and if his monthly average total cost is $7, what are his monthly profits?

A)

$6,000

B)

$27,000

C)

$21,000

D)

$2

Page 16

83.

Suppose Sarah’s pottery studio is charging the market price, which is just higher than

her minimum average total cost. This means that Sarah:

A)

is breaking even.

B)

should shut down immediately.

C)

is earning a small economic profit.

D)

is incurring a small economic loss.

84.

The break-even price for a perfectly competitive firm is equal to:

A)

the minimum value of average variable cost.

B)

the marginal revenue, provided that marginal revenue is equal to marginal cost.

C)

the average fixed cost at the given output level.

D)

the minimum value of average total cost.

85.

Consider a perfectly competitive firm in the short run. Assume that it is sustaining

economic losses but continues to produce at the profit-maximizing (loss-minimizing)

output. Which statement is FALSE?

A)

Marginal cost is less than average total cost.

B)

Marginal cost is equal to marginal revenue.

C)

Price is equal to marginal cost.

D)

Marginal cost is less than average variable cost.

86.

Zoe’s Bakery determines that P < ATC and P > AVC. In the short run, Zoe should:

A)

continue to operate even though she is taking an economic loss.

B)

continue to operate, as she is making an economic profit.

C)

shut down immediately, as she is taking an economic loss.

D)

raise the price until she has maximized her profits.

87.

A perfectly competitive small organic farm produces 1,000 cauliflower heads in the

short run. Its ATC = $6 and AFC = $2. The market price is $3 per head and is equal to

MC. To maximize profits or minimize losses, this farm should:

A)

increase output.

B)

reduce output but continue to produce.

C)

shut down.

D)

do nothing; the firm is already maximizing profits.

Page 17

88.

If the price is consistently below average total cost, then in the short run a perfectly

competitive firm should:

A)

shut down.

B)

continue to produce to minimize losses.

C)

raise the price.

D)

There is not enough information given to answer this question.

89.

During the summer, Alex runs a mowing service, and lawn mowing is a perfectly

competitive industry. In the short run, Alex will shut down if:

A)

the total revenues can’t cover fixed costs.

B)

the total revenues can’t cover variable costs.

C)

the total revenues can’t cover total costs.

D)

the price exceeds the average total cost.

90.

Many furniture stores run “going out of business” sales but never go out of business. For

the shut-down decision to be the appropriate one, the price of furniture must be _____

than the _____ average variable cost.

A)

higher; maximum

B)

lower; minimum

C)

higher; minimum

D)

lower; maximum

91.

The short-run supply curve for a perfectly competitive firm is its:

A)

demand curve above its marginal revenue curve.

B)

marginal revenue curve to the right of its marginal cost curve.

C)

marginal cost curve above its average variable cost curve.

D)

average total cost curve below its marginal cost curve.

92.

The lowest point on a perfectly competitive firm’s short-run supply curve corresponds to

the minimum point on the _____ curve.

A)

ATC

B)

AVC

C)

AFC

D)

MC

Page 18

93.

If the price is consistently below the average variable cost, then in the short run a

perfectly competitive firm should:

A)

raise the price.

B)

sell more output.

C)

shut down.

D)

lower the price to sell more.

94.

A perfectly competitive firm will incur an economic loss but will continue to produce a

positive quantity of output in the short run if the price is:

A)

less than marginal cost.

B)

less than average variable cost.

C)

greater than average total cost.

D)

greater than average variable cost and less than average total cost.

95.

If the price is greater than the average variable cost and less than the average total cost

at the profit-maximizing quantity of output in the short run, a perfectly competitive firm

will:

A)

produce at an economic loss.

B)

produce at an economic profit.

C)

shut down production.

D)

produce more than the profit-maximizing quantity.

96.

The short-run shut-down price is:

A)

the price at which economic profit is zero.

B)

the minimum of the AVC curve.

C)

the intersection of the MC and ATC curves.

D)

the minimum of the AFC curve.

97.

For a perfectly competitive firm, the short-run supply curve is the:

A)

entire MC curve.

B)

rising part of the MC curve beginning at the shut-down point.

C)

rising part of the MC curve beginning where the firm starts earning economic

profit.

D)

MC curve below the shut-down point.

Page 19

98.

A perfectly competitive firm will continue producing in the short run as long as it can

cover its _____ cost.

A)

total

B)

average fixed

C)

variable

D)

fixed

99.

The short-run supply curve for a perfectly competitive firm is the ____ cost curve above

the _____ price.

A)

average total; break-even

B)

average variable; shut-down

C)

marginal; break-even

D)

marginal; shut-down

100.

Which of the following is TRUE?

A)

If price falls below average variable cost, the firm will shut down in the short run.

B)

Total revenue and marginal revenue are the same in perfect competition.

C)

Economic profit per unit is found by subtracting MC from price.

D)

Economic profit is always positive in the long run.

101.

In perfect competition, the profit-maximizing level of output occurs where the:

A)

MR = MC above minimum AVC.

B)

price < marginal cost above minimum AVC.

C)

MR > MC below minimum AVC.

D)

P = MR above MC.

102.

A perfectly competitive firm will incur an economic loss but will continue producing

output in the short run if the price is:

A)

less than marginal cost.

B)

greater than average fixed cost and less than average variable cost.

C)

greater than average total cost.

D)

greater than average variable cost but less than average total cost.

103.

If the price is greater than the average variable cost and less than the average total cost

at the profit-maximizing quantity of output in the short run, a perfectly competitive firm

will:

A)

continue to produce at an economic loss.

B)

earn an economic profit.

C)

encourage other firms to enter the industry.

D)

produce more than the profit-maximizing quantity.

Page 20

104.

In the short run, if AVC < P < ATC, a perfectly competitive firm:

A)

produces output and earns an economic profit.

B)

produces output and incurs an economic loss.

C)

does not produce output and earns an economic profit.

D)

does not produce output and earns zero economic profit.

105.

In the short run, a perfectly competitive firm produces output and incurs an economic

loss if:

A)

P > ATC.

B)

P < AVC.

C)

AVC > P > ATC.

D)

AVC < P < ATC.

106.

A perfectly competitive firm will not produce any output in the short run and will shut

down if the price is:

A)

greater than marginal cost.

B)

less than marginal cost.

C)

less than average variable cost.

D)

greater than average variable cost and less than average total cost.

107.

The shut-down point in the short run is:

A)

the point at which economic profit is zero.

B)

the minimum point of AVC.

C)

the intersection of the MC and ATC curves.

D)

the minimum point of AFC.

108.

If the price is less than the average variable cost at the quantity of output where MR =

MC, in the short run a perfectly competitive firm will:

A)

produce at a loss.

B)

produce at a profit.

C)

shut down production.

D)

produce more than the profit-maximizing quantity.

109.

Assume that in the short run a perfectly competitive firm does not produce output and

has economic losses. This occurs at the quantity where MR = MC and:

A)

P = ATC and FC = 0.

B)

P < AVC and FC > 0.

C)

AVC > P > ATC and FC = 0.

D)

AVC < P < ATC and FC > 0.

Page 21

110.

In the short run, if P < AVC at the quantity where MR = MC, a perfectly competitive

firm produces _____ and takes an economic _____.

A)

output; profit

B)

output; loss

C)

no output; profit

D)

no output; loss

111.

A firm’s shut-down point is the minimum value of:

A)

total cost.

B)

average variable cost.

C)

average total cost.

D)

marginal cost.

112.

A perfectly competitive firm’s short-run supply curve is its _____ cost curve above its

_____ cost curve.

A)

average variable; marginal

B)

marginal; average fixed

C)

marginal; average total

D)

marginal; average variable

113.

A perfectly competitive firm’s marginal cost curve above the average variable cost curve

is its _____ curve.

A)

input demand

B)

short-run supply

C)

marginal revenue

D)

total revenue

114.

A competitive firm operating in the short run is maximizing profits and just breaking

even. Its costs include a monthly state license fee of $100 that must be paid for as long

as the firm operates. If the license fee is raised to $150, what should the firm do to

maximize profits in the short run?

A)

increase price

B)

increase output

C)

reduce output

D)

not change output

Page 22

115.

Which of the following is TRUE?

A)

If the price falls below the average total cost, the firm will earn economic profits.

B)

Price and marginal revenue are the same in perfect competition.

C)

Economic profit per unit is found by subtracting AVC from the price.

D)

Economic profit is always positive in the short run.

116.

Wenqin is a farmer, and in the short run she produces 100 bushels of wheat. Her average

total cost per bushel is $1.75, total revenue is $450, and total fixed costs are $100.

Wenqin’s:

A)

average fixed cost is $1.50.

B)

profit per bushel is $2.75.

C)

average variable cost is $1.25.

D)

economic profit is $250.

Use the following to answer questions 117-118:

Figure: Prices, Cost Curves, and Profits

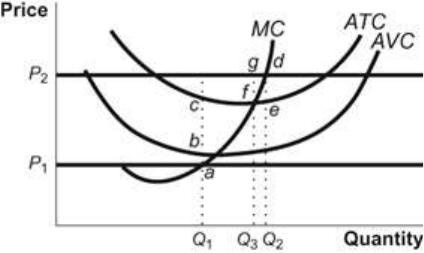

117.

(Figure: Prices, Cost Curves, and Profits) Look at the figure Prices, Cost Curves, and

Profits. If the price is P1 and the firm decides to produce at output Q1, then the firm

earns:

A)

a loss equal to (ba) × Q1.

B)

a loss equal to (ca) × Q1.

C)

a loss equal to (bc) × Q1.

D)

zero.

Page 23

118.

(Figure: Prices, Cost Curves, and Profits) Look at the figure Prices, Cost Curves, and

Profits. If the price is P2 and the firm is profit-maximizing, then the firm’s profit is:

A)

(fg) × Q3.

B)

(de) × Q2.

C)

(fg) × Q2.

D)

(de) × P2.

Use the following to answer questions 119-121:

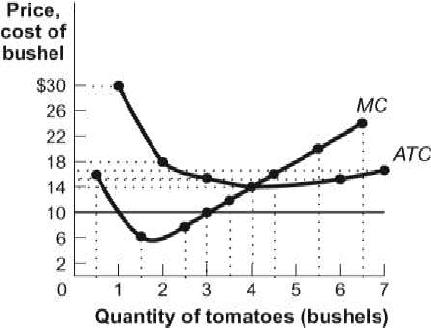

Figure: Cost Curves for Corn Producers

119.

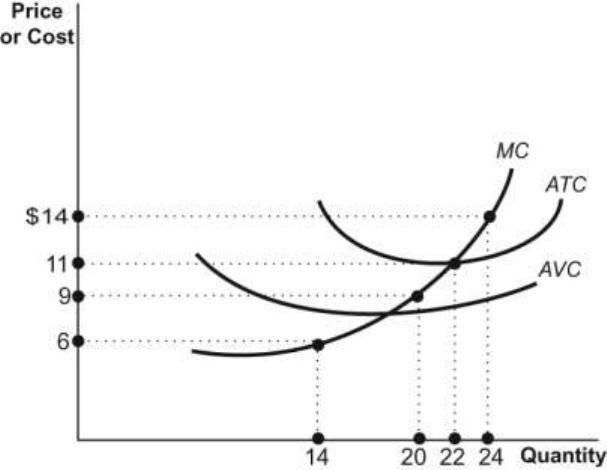

(Figure: Cost Curves for Corn Producers) Look at the figure Cost Curves for Corn

Producers. The market for corn is perfectly competitive. If the price of a bushel of corn

is $14, in the short run, the farmer will produce _____ of corn and earn an economic

_____ equal to _____.

A)

4 bushels; profit; $0

B)

4 bushels; profit; just less than $80 per bushel

C)

2 bushels; profit; $0

D)

2 bushels; loss; just more than $80 per bushel

120.

(Figure: Cost Curves for Corn Producers) Look at the figure Cost Curves for Corn

Producers. The market for corn is perfectly competitive. If the price of a bushel of corn

is $4, in the short run the farmer will produce _____ bushels of corn and earn an

economic _____ equal to _____.

A)

0; loss; average fixed costs

B)

0; loss; total fixed costs

C)

3; loss; $30 per bushel

D)

3; profit; $20 per bushel

Page 24

121.

(Figure: Cost Curves for Corn Producers) Look at the figure Cost Curves for Corn

Producers. The market for corn is perfectly competitive. If the price of a bushel of corn

is $10, then in the short run the farmer will produce _____ bushels of corn and take an

economic loss equal to _____.

A)

0; average fixed costs

B)

0; total variable costs

C)

3; total fixed costs

D)

3; $22 per bushel

Use the following to answer questions 122-123:

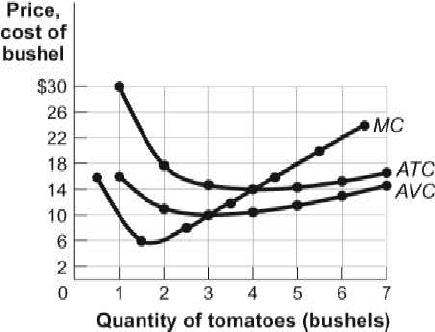

Figure: Costs and Profits for Tomato Producers

122.

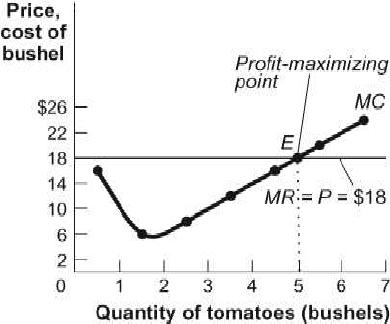

(Figure: Costs and Profits for Tomato Producers) Look at the figure Costs and Profits

for Tomato Producers. The market for tomatoes is perfectly competitive. The market

price of a bushel of tomatoes is $18. If the market price increases to $20, the farmer’s

marginal revenue _____ and the profit-maximizing output _____.

A)

increases; increases

B)

increases; decreases

C)

decreases; increases

D)

decreases; decreases

123.

(Figure: Costs and Profits for Tomato Producers) Look at the figure Costs and Profits

for Tomato Producers. The market for tomatoes is perfectly competitive. The market

price of a bushel of tomatoes is $18. If the market price falls to $16, the farmer’s

marginal revenue _____ and the profit-maximizing output _____.

A)

increases; decreases

B)

increases; increases

C)

decreases; increases

D)

decreases; decreases

Page 25

Use the following to answer question 124:

Figure: Total Cost for Tomato Producers

124.

(Figure: Total Cost for Tomato Producers) Look at the figure Total Cost for Tomato

Producers. The market for tomatoes is perfectly competitive. The market price of a

bushel of tomatoes is $14. The farmer’s total cost at the profit-maximizing number of

bushels is:

A)

$3.50.

B)

$14.00.

C)

$56.00.

D)

$72.00.

Use the following to answer question 125:

Figure: Revenues, Costs, and Profits for Tomato Producers

Page 26

125.

(Figure: Revenues, Costs, and Profits for Tomato Producers) Look at the figure

Revenues, Costs, and Profits for Tomato Producers. The market for tomatoes is

perfectly competitive. The market price of a bushel of tomatoes is $18. At the

profit-maximizing quantity of output in the figure, the farmer’s total revenue is _____,

total cost is _____, and profit is _____.

A)

$90; $14; $76

B)

$90; $70; $20

C)

$30; $42; –$12

D)

$48; $56; –$8

Use the following to answer question 126:

Figure: Revenues, Costs, and Profits for Tomato Producers II

126.

(Figure: Revenues, Costs, and Profits for Tomato Producers II) Look at the figure

Revenues, Costs, and Profits for Tomato Producers II. The market for tomatoes is

perfectly competitive. The market price of a bushel of tomatoes is $10. At the farmer’s

profit-maximizing output, total revenue is _____, total cost is _____, and profit is

_____.

A)

$90; $72; $18

B)

$56; $56; $0

C)

$30; $48; –$18

D)

$48; $56; –$8

Page 27

Use the following to answer questions 127-132:

Figure: Revenues, Costs, and Profits for Tomato Producers III

127.

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If market price of a bushel of tomatoes is $18, in the short run the

farmer’s profit-maximizing output is _____ bushels.

A)

2

B)

3

C)

4

D)

5

128.

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $14, in the short run

the farmer’s profit-maximizing output is _____ bushels.

A)

2

B)

3

C)

4

D)

5

Page 28

129.

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $8, in the short run

the farmer’s profit-maximizing output is _____ bushels.

A)

0

B)

1

C)

2

D)

3

130.

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $18, this farm will:

A)

minimize its losses by shutting down.

B)

minimize its losses by continuing to produce.

C)

break even.

D)

earn an economic profit.

131.

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $12, in the short run

this farm will:

A)

minimize its losses by shutting down.

B)

minimize its losses by continuing to produce.

C)

break even.

D)

earn an economic profit.

132.

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. The farm’s short-run supply curve is the _____ cost curve above a

price of _____.

A)

average total; $14

B)

average variable; $10

C)

marginal; $10

D)

marginal; $14

Page 29

Use the following to answer questions 133-138:

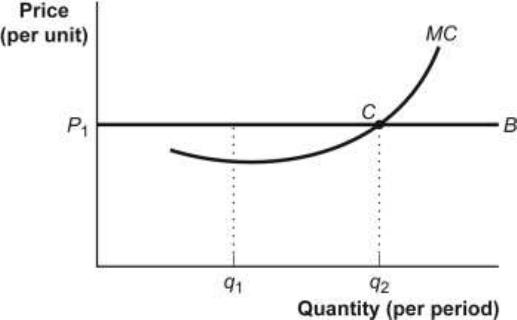

Figure: The Marginal Decision Rule

133.

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule. At q2,

or the _____, the _____ price is equal to marginal cost.

A)

minimum-cost output; shut-down

B)

profit-maximizing quantity; market

C)

maximum-cost output; break-even

D)

profit-minimizing quantity; break-even

134.

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule. If P1

is the market price and if this firm is maximizing profit, it should produce:

A)

where MR > MC.

B)

at quantity q2.

C)

at quantity q1, where MR > MC.

D)

a quantity greater than q1 but less than q2.

135.

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule. Given

the market price P1, B is the _____ curve.

A)

marginal revenue

B)

marginal cost

C)

marginal product

D)

average fixed cost

Page 30

136.

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule.

Economic profit:

A)

is earned between q1 and q2.

B)

is earned between the origin and q1.

C)

is earned as a maximum at q1.

D)

cannot be determined from the information provided.

137.

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule. As

long as the price is above the minimum variable cost, this firm should produce quantity

_____ where _____ equals _____ to maximize economic profit.

A)

q1; MR; MC

B)

q2; price; MC

C)

q2; MR; TR

D)

q1; TR; TC

138.

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule. To

the left of point C (e.g., at q1):

A)

economic profit is the vertical distance between curves B and MC.

B)

the firm is not maximizing profits.

C)

the firm is maximizing profits.

D)

the firm should produce less.

Use the following to answer questions 139-152:

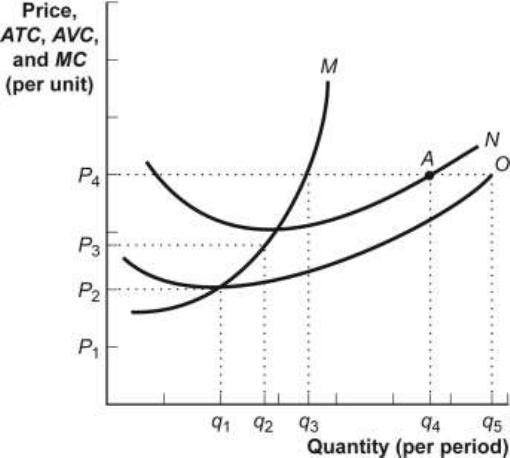

Figure: The Profit-Maximizing Firm in the Short Run

Page 31

139.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. M is the _____ curve.

A)

ATC

B)

MR

C)

MC

D)

AVC

140.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. N is the _____ curve.

A)

ATC

B)

MR

C)

MC

D)

AVC

141.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. If the market price is P3, the firm will

produce quantity _____ and _____ in the short run.

A)

q2; make a profit

B)

q1; break even

C)

q2; incur a loss

D)

q4; incur a loss

142.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. If the market price is P4, the firm will

produce quantity _____ and _____ in the short run.

A)

q1; break even

B)

q3; make a profit

C)

q4; break even

D)

q5; lose fixed costs

143.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm. O is the _____ curve.

A)

ATC

B)

MR

C)

MC

D)

AVC

Page 32

144.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. Curve M must cross curves N and O:

A)

at their maximum points.

B)

to the left of their minimum points.

C)

at their minimum points.

D)

to the right of their minimum points.

145.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. If the market price is less than P2, the firm

will _____ in the short run.

A)

produce q1 and break even

B)

produce q1 and incur a loss

C)

shut down

D)

produce q3 and make a profit

146.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. Which of the following statements is TRUE?

A)

AFC is represented by the vertical distance between curve M and curve N at any

level of output.

B)

AFC is represented by the vertical distance between curve N and curve O at any

level of output.

C)

This figure illustrates the long run because all costs are variable.

D)

Quantity q2 is to the left of the shut-down point.

147.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. The MC curve is represented by:

A)

none of the curves.

B)

curve O.

C)

curve M.

D)

curve N.

148.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. The ATC curve is represented by:

A)

curve N.

B)

curve M.

C)

curve O.

D)

none of the curves.

Page 33

149.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. Which of these curves is the AVC curve?

A)

curve M

B)

none of the curves

C)

curve N

D)

curve O

150.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. If the market price is P4, marginal revenue:

A)

and price are the same.

B)

is less than P4.

C)

is greater than P4.

D)

and price are unrelated.

151.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. If the market price is P4:

A)

firms will leave the industry and the price will fall in the long run.

B)

there will be economic profits and firms will enter the industry in the long run.

C)

the market supply curve will shift to the left and price will fall in the long run.

D)

the firm will produce q4.

152.

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. At q2, ATC is the vertical distance between q2

on the horizontal axis and:

A)

curve M.

B)

curve N.

C)

curve O.

D)

P4.

Page 34

Use the following to answer questions 153-163:

Figure: A Perfectly Competitive Firm in the Short Run

153.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm’s total cost of producing its most profitable

level of output is:

A)

BS.

B)

DK.

C)

0FKD.

D)

0ESB.

154.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm’s total revenue from the sale of its most

profitable level of output is:

A)

0GLD.

B)

0GHB.

C)

BH.

D)

DL.

155.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm’s total economic profit at its most

profitable level of output is:

A)

0GHB.

B)

EFJS.

C)

EGHS.

D)

FGLK.

Page 35

156.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The lowest price that will yield zero economic

profit is indicated by the letter:

A)

G.

B)

F.

C)

E.

D)

N.

157.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm will produce in the short run if the price is

at least as high as point:

A)

F.

B)

E.

C)

N.

D)

P.

158.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm will shut down in the short run if the price

falls below:

A)

G.

B)

F.

C)

E.

D)

P.

159.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. If the market price is G, the firm’s total cost of

producing its most profitable level of output is:

A)

BS.

B)

DK.

C)

0FKD.

D)

0ESB.

160.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. If market price is G, the firm’s total revenue from

the sale of its most profitable level of output is:

A)

0GLD.

B)

0GHB.

C)

BH.

D)

DL.

Page 36

161.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. If the market price is G, the firm’s total economic

profit at its most profitable level of output is:

A)

0GHB.

B)

EFJS.

C)

EGHS.

D)

FGLK.

162.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The minimum price that the firm must receive to

produce in the short run is:

A)

F.

B)

E.

C)

N.

D)

P.

163.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm’s short-run supply curve is the:

A)

entire MC curve.

B)

rising part of the MC curve beginning at point W.

C)

rising part of the MC curve beginning at the point at which the firm starts earning

economic profit.

D)

MC curve below point P.

Use the following to answer questions 164-167:

Page 37

164.

(Table: Soybean Cost) Look at the table Soybean Cost. If the market price of a bushel of

soybeans is $15, how many bushels will the farmer produce to maximize short-run

profit?

A)

2

B)

5

C)

3

D)

7

165.

(Table: Soybean Cost) Look at the table Soybean Cost. If the market price of a bushel of

soybeans is $15, what will be the farmer’s short-run maximum profit?

A)

$75

B)

$69

C)

$6

D)

$5

166.

(Table: Soybean Cost) Look at the table Soybean Cost. What is the break-even price for

this farmer?

A)

$13.00

B)

$13.50

C)

$14.00

D)

$14.50

167.

(Table: Soybean Cost) Look at the table Soybean Cost. What is the shut-down price for

this farmer?

A)

$10

B)

$11

C)

$12

D)

$13

Page 38

Use the following to answer questions 168-169:

168.

(Table: Lilly’s Apple Orchard) Look at the table Lilly’s Apple Orchard. Lilly is the

price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the price

of a bushel of apples is $25, how many bushels will Lilly produce to maximize profit?

A)

0

B)

1

C)

2

D)

3

169.

(Table: Lilly’s Apple Orchard) Look at the table Lilly’s Apple Orchard. Lilly is the

price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the price

of a bushel of apples is $35, her economic profit will be:

A)

–$30

B)

–$5

C)

$0

D)

$5

Page 39

Use the following to answer questions 170-176:

170.

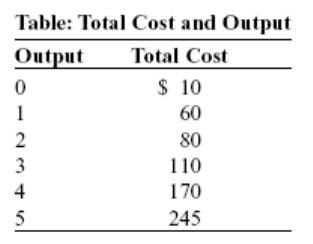

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. If the market price is $4.50, the profit-maximizing output is

_____ units.

A)

5

B)

7

C)

8

D)

9

171.

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. If the market price is $3.50, the profit-maximizing output is

_____ units.

A)

5

B)

7

C)

8

D)

9

172.

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. If the market price is $5.50, the profit-maximizing quantity

of output is _____ units.

A)

5

B)

7

C)

8

D)

9

Page 40

173.

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. If the market price is $4.50, profit at the profit-maximizing

quantity of output is:

A)

$2.00.

B)

$4.50.

C)

$5.00.

D)

$34.00.

174.

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. The firm will produce at a profit in the short run if the price

is at least:

A)

$2.07.

B)

$2.53.

C)

$3.47.

D)

$4.26.

175.

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. In the short run, the firm will produce, but at a loss, if the

price is:

A)

$2.00.

B)

$2.50.

C)

$3.50.

D)

$4.50.

176.

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. The firm will stop production and shut down if the price is:

A)

$2.50.

B)

$3.50.

C)

$4.50.

D)

$5.00.

Page 41

Use the following to answer questions 177-180:

Figure: The Perfectly Competitive Firm

177.

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

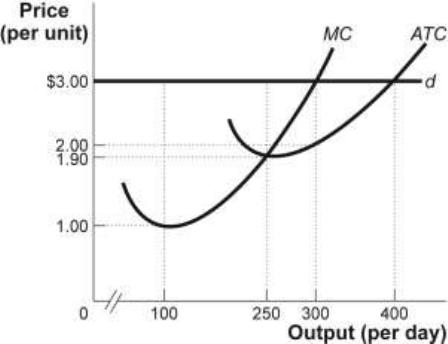

Firm. The figure shows a perfectly competitive firm that faces demand curve d and

maximizes profit. If the market price is $3, the firm will produce _____ units of output

per day.

A)

100

B)

250

C)

300

D)

400

178.

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d

maximizes profit. Given the market price, the firm’s total revenue per day is:

A)

$475.

B)

$600.

C)

$900.

D)

$1,200.

179.

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d and

maximizes profit. Given the market price, the firm’s total cost per day is:

A)

$475.

B)

$600.

C)

$900.

D)

$1,200.

Page 42

180.

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d and

maximizes profit. If the firm faces a market price of $3, its total profit per day is:

A)

$0.

B)

$250.

C)

$275.

D)

$300.

Use the following to answer questions 181-182:

Figure: Short-Run Costs

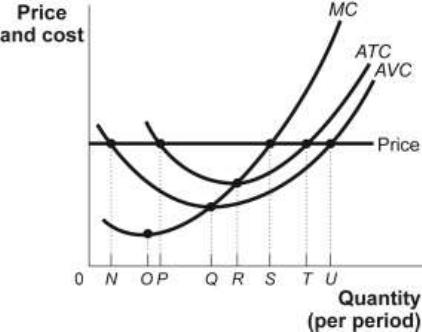

181.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. At the given price, the

most profitable level of output occurs at quantity:

A)

N.

B)

P.

C)

S.

D)

T.

182.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. This firm’s short-run

supply curve begins at quantity:

A)

Q.

B)

R.

C)

S.

D)

T.

Page 43

183.

The short-run industry supply curve:

A)

shows the total quantity supplied by all firms in an industry for each possible price

when the number of producers is fixed.

B)

is drawn on the assumption that the number of firms in the industry doesn’t

increase, but it allows for a decrease in the number of firms due to bankrupt firms

leaving the industry.

C)

is a meaningful concept only if all firms in the industry are identical.

D)

is of limited usefulness, since it is not relevant when markets are perfectly

competitive.

Use the following to answer question 184:

184.

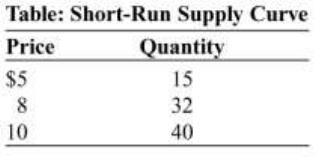

(Table: Short-Run Supply Curve) Look at the table Short-Run Supply Curve. The table

lists three supply points for a perfectly competitive firm operating in the short run. If the

industry is composed of 120 identical firms, a price of _____ and a quantity of _____

will be a point on the short-run industry supply curve.

A)

$5; 1,650

B)

$1,200; 40

C)

$960; 3,840

D)

$10; 4,800

185.

The supply curve found by taking the horizontal summation of the short-run supply

curves of all of the firms in a perfectly competitive industry is called the _____ curve.

A)

marginal cost

B)

short-run market supply

C)

interim market supply

D)

competitive

186.

In perfect competition, the assumption of easy entry and exit implies that in the _____

run all firms in the industry will earn _____ economic profits.

A)

long; zero

B)

short; positive

C)

short; zero

D)

long; positive

Page 44

187.

If firms are making positive economic profits in the short run, then in the long run:

A)

the short-run industry supply curve will shift leftward.

B)

firms will enter the industry.

C)

industry output will rise and the price will rise.

D)

firms will leave the industry.

188.

The market for beef is in long-run equilibrium at $3.25 per pound. The announcement

that mad cow disease has been discovered in the United States reduces the demand for

beef sharply, and the price falls to $2.00 per pound. If the long-run supply curve is

horizontal, when the long-run equilibrium is reestablished, the price will be:

A)

$3.25 per pound.

B)

$2.00 per pound.

C)

greater than $2.00 per pound but less than $3.25 per pound.

D)

More information is needed to answer this question.

189.

Suppose economic profits exist in perfect competition in the short run. Firms will enter

in the long run because of easy entry, the short-run market _____ curve will shift to the

right, and _____ will _____.

A)

supply; output; increase

B)

demand; supply; fall

C)

supply; demand; also shift to the right

D)

demand; price; increase

190.

Economic profits in a perfectly competitive industry encourage firms to _____ the

industry, and losses encourage firms to _____ the industry.

A)

exit; enter

B)

enter; enter

C)

enter; exit

D)

exit; exit

191.

Suppose that some firms in a perfectly competitive industry earn negative economic

profits. In the long run, the:

A)

short-run industry supply curve will not shift.

B)

short-run industry supply curve will shift to the left.

C)

number of firms in the industry will not change.

D)

number of firms in the industry will increase.

Page 45

192.

If firms are taking economic losses in the short run, firms will leave the industry,

industry output will _____, and economic losses will _____ in the long run.

A)

fall; fall

B)

rise; fall

C)

rise; rise

D)

fall; rise

193.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward-sloping. The price of sugar

rises, increasing the marginal and average total costs of producing candy canes by

$0.05. In the short run a typical producer of candy canes will be making:

A)

an economic profit.

B)

zero economic profit.

C)

negative economic profit.

D)

The answer is impossible to determine from the information given.

194.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward-sloping. The price of sugar

rises, increasing the marginal and average total cost of producing candy canes by $0.05;

there are no other changes in production costs. In the long run we will observe:

A)

firms leaving the industry.

B)

firms entering the industry.

C)

some firms entering and some firms leaving.

D)

neither entry to nor exit from the industry.

195.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward-sloping. The price of sugar

rises, increasing the marginal and average total cost of producing candy canes by $0.05;

there are no other changes in production costs. Once all of the adjustments to long-run

equilibrium have been made, the price of candy canes will equal:

A)

$0.05.

B)

$0.10.

C)

$0.15.

D)

The question is impossible to answer without knowing exactly how many firms

entered and/or left the industry.

Page 46

196.

Suppose that the market for haircuts in a community is perfectly competitive and that

the market is initially in long-run equilibrium. Subsequently, an increase in population

increases the demand for haircuts. In the short run, the market price will _____ and the

output of a typical firm will _____.

A)

rise; rise

B)

rise; fall

C)

fall; rise

D)

fall; fall

197.

Suppose that the market for haircuts in a community is perfectly competitive and that

the market is initially in long-run equilibrium. Subsequently, an increase in population

increases the demand for haircuts. In the short run, the typical firm is likely to:

A)

earn an economic profit.

B)

incur an economic loss.

C)

have no change in its economic profit.

D)

have neither an economic profit nor an economic loss.

198.

Suppose that the market for haircuts in a community is a perfectly competitive

constant-cost industry and that the market is initially in long-run equilibrium.

Subsequently, an increase in population increases the demand for haircuts. In the long

run, firms will _____ the market, driving the price of haircuts _____ and the profits of

individual firms _____.

A)

enter; up; back to zero

B)

enter; down; back to zero

C)

leave; up; up

D)

leave; up; back to zero

199.

Assuming a downward-sloping demand curve, a decrease in production costs for firms

in a perfectly competitive market initially in long-run equilibrium will cause a(n):

A)

permanent increase in the price.

B)

economic profit for firms in the short run.

C)

increase in demand.

D)

increase in firms’ marginal revenue.

200.

In perfect competition, a change in fixed cost will:

A)

cause a change in the price in the short run.

B)

cause a change in output in the short run.

C)

encourage entry or exit in the long run so that price will change enough to leave

firms earning zero profits.

D)

cause a change in variable cost.

Page 47

201.

In a perfectly competitive market:

A)

the price will change to reflect any change in production cost.

B)

the existence of profits leads firms to exit the industry, while losses lead firms to

enter the industry.

C)

in the long run, economic profits are positive.

D)

perfect competition generates prices greater than marginal costs.

202.

A curve that shows the quantity of a good or service supplied at various prices after all

long-run adjustments to a price change have been completed is a long-run _____ curve.

A)

marginal revenue

B)

marginal cost

C)

industry supply

D)

production

203.

Which of the following is TRUE?

A)

The long-run industry supply curve relates the price of a good or service to the

quantity produced after all adjustments to a price change have been made.

B)

Every point on a long-run industry supply curve shows a price and quantity

supplied at which firms in the industry are earning positive economic profit.

C)

For establishing the long-run industry supply curve, factor costs and the number of

firms are held constant.

D)

In perfectly competitive industries, the long-run supply curve is always horizontal.

204.

Lilly is the price-taking owner of an apple orchard. The price of apples is high enough

that Lilly is earning positive economic profits. In the long run, Lilly should expect

_____ apple prices due to the _____ firms.

A)

lower; entry of new

B)

higher; exit of existing

C)

lower; exit of existing

D)

higher; entry of new

205.

Which of the following is MOST likely to cause firms to exit a perfectly competitive

industry?

A)

Consumer tastes and preferences for this product get stronger.

B)

A technological advance allows all firms to produce more efficiently.

C)

The price of a key variable input falls.

D)

Consumer income falls.

Page 48

Use the following to answer question 206:

206.

(Table: Lilly’s Apple Orchard) Look at the table Lilly’s Apple Orchard. Lilly is the

price-taking owner of an apple orchard; the orchard’s variable costs are given in the

table. Her orchard has fixed costs of $30. If the price of a bushel of apples is $85, we

would expect total industry output to _____ and Lilly’s output to _____ in the long run.

A)

rise; rise

B)

fall; fall

C)

fall; rise

D)

rise; fall

Use the following to answer questions 207-208:

Figure: The Perfectly Competitive Firm

Page 49

207.

(Figure: The Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The firm faces demand curve d and maximizes profit. In a long-run equilibrium,

this firm will produce _____ units of output and sell its output for _____.

A)

100; $1.00

B)

250; $1.90

C)

300; $2.00

D)

400; $3.00

208.

(Figure: The Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d and

maximizes profit. The firm’s economic profit in the long run will be:

A)

$0.

B)

$250.

C)

$275.

D)

$300.

209.

If some firms in a perfectly competitive industry are earning positive economic profits,

then in the long run, the:

A)

industry is in equilibrium.

B)

short-run industry supply curve will shift to the right.

C)

number of firms in the industry will not change.

D)

number of firms in the industry will decrease.

210.

Suppose that some firms in a perfectly competitive industry are earning positive

economic profits. In the long run, the:

A)

industry is in equilibrium.

B)

industry supply curve will shift to the left.

C)

number of firms in the industry will not change.

D)

number of firms in the industry will increase.

211.

Suppose that the market for haircuts in a community is perfectly competitive and that

the market is initially in long-run equilibrium. Subsequently, a decrease in population

decreases the demand for haircuts. In the short run, we expect that the market price will

_____ and the output of a typical firm will _____.

A)

rise; rise

B)

rise; fall

C)

fall; rise

D)

fall; fall

Page 50

212.

In perfectly competitive long-run equilibrium:

A)

all firms make positive economic profits.

B)

all firms produce at the minimum point of their average total cost curves.

C)

the industry supply curve must be upward-sloping.

D)

all firms face the same price, but the value of marginal cost will vary directly with

firm size.

213.

When economic profits in an industry are zero:

A)

firms are really doing badly.

B)

firms are doing as well as they could do in other markets.

C)

firms should exit so they can make an economic profit in some other market.

D)

the industry is not in long-run equilibrium.

214.

When a perfectly competitive firm is in long-run equilibrium, the firm is producing at

_____ cost.

A)

maximum average total

B)

maximum average variable

C)

minimum marginal

D)

minimum long-run average total

215.

Provided that there are no external benefits or costs, resources are efficiently allocated

when:

A)

P = MR.

B)

P = AVC.

C)

P = MC.

D)

MC = AVC.

216.

In a long-run equilibrium, economic profits in a perfectly competitive industry are:

A)

positive.

B)

zero.

C)

negative.

D)

indeterminate.

217.

When a perfectly competitive industry is in long-run equilibrium, its firms:

A)

earn more than zero economic profits.

B)

combine their variable and fixed resources inefficiently.

C)

are not in short-run equilibrium.

D)

allocate all of their resources efficiently.

Page 51

218.

A perfectly competitive industry is in a state of long-run equilibrium. Which of the

following must be TRUE?

A)

P = MR = MC > ATC.

B)

P = MR = MC < AVC.

C)

P = MR = MC = ATC.

D)

P > MR = MC = AVC.

219.

A perfectly competitive industry is said to be efficient because the:

A)

marginal cost of production of the last unit of output is minimized.

B)

product is standardized across firms in the industry.

C)

average total cost of production of the industry’s output is minimized.

D)

market price of the good is equal to economic profit for all firms in the industry.

Use the following to answer questions 220-232:

220.

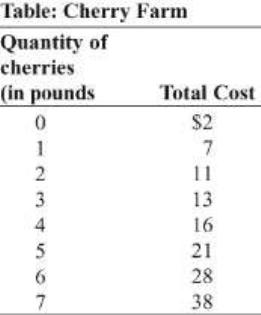

(Table: Cherry Farm) Look at the table Cherry Farm. If Hank and Helen have one of

100 farms in the perfectly competitive cherry industry and if the price is $5, in the short

run the industry will supply _____ pounds.

A)

100

B)

200

C)

400

D)

500

Page 52

221.

(Table: Cherry Farm) Look at the table Cherry Farm. If Hank and Helen have one of

100 farms in the perfectly competitive cherry industry and if the price is $4, in the short

run the industry will supply _____ pounds.

A)

200

B)

400

C)

600

D)

700

222.