Chapter 12: Accounting for Partnerships and Limited Liability Companies

119.

Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest

on

original capital. If they agree to share remaining profits and losses on a 3:2 ratio, what will Singer’s share of

the

income be if the income for the year is $50,000?

a. $24,000

b. $22,000

c. $16,000

d. $23,400

120.

Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest

on

original capital. If they agree to share remaining profits and losses on a 3:2 ratio, what will McMann‘s share of

the

income be if the income for the year is $30,000?

a. $20,000

b. $18,000

c. $18,600

d. $17,400

Chapter 12: Accounting for Partnerships and Limited Liability Companies

121.

Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest

on

original capital. If they agree to share remaining profits and losses on a 3:2 ratio, what will Singer’s share of

the

income (loss) be if the net loss for the year is $10,000?

a. $(12,600)

b. $(14,000)

c. $(6,000)

d. $(10,000)

122.

Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest

on

original capital. If they agree to share remaining profits and losses on a 3:2 ratio, what will Singer’s share of

the

income be if the income for the year is $15,000?

a. $9,000

b. $2,400

c. $1,000

d. $5,600

Chapter 12: Accounting for Partnerships and Limited Liability Companies

123.

Immediately prior to the admission of Allen, the Sanson-Jeremy Partnership assets had been adjusted to

current

market prices, and the capital balances of Sanson and Jeremy were $80,000 and $120,000 respectively.

If the

parties agree that the business is worth $240,000, what is the amount of bonus that should be recognized

in the

accounts at the admission of Allen?

a. $60,000

b. $80,000

c. $40,000

d. $100,000

124.

The Craig-Doran Partnership owns inventory that was purchased for $85,000, has a current replacement cost of

$54,500, and is priced to sell for $98,000. At what amount should the inventory be recorded in the accounts of

the

new partnership if Alexis is to be admitted?

a. $98,000

b. $54,500

c. $85,000

d. $79,167

125.

Paul and Roger are partners who share income in the ratio of 3:2. Their capital balances are $90,000 and

$130,000,

respectively. Income Summary has a credit balance of $50,000 after the second closing entry. What is

Roger’s

capital balance after closing Income Summary to the capital accounts?

a. $155,000

b. $150,000

c. $110,000

d. $115,000

Chapter 12: Accounting for Partnerships and Limited Liability Companies

126.

Paul and Roger are partners who share income in the ratio of 3:2. Their capital balances are $90,000 and

$130,000,

respectively. Income Summary has a credit balance of $50,000 after the second closing entry. What is

Paul’s

capital balance after closing Income Summary to the capital accounts?

a. $108,000

b. $120,000

c. $115,000

d. $180,000

127.

Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time

and

Campbell one-half time to the business. Determine the division of $150,000 of net income when there is no

reference to division in partnership agreement.

a. $75,000 and $75,000 b. $37,500 and $112,500

c. $100,000 and $50,000 d. $112,500 and $37,500

128.

Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time

and

Campbell one-half time to the business. Determine the division of $150,000 of net income in ratio of time

devoted

to business.

a. $75,000 and $75,000 b. $37,500 and $112,500

c. $100,000 and $50,000 d. $112,500 and $37,500

Chapter 12: Accounting for Partnerships and Limited Liability Companies

129.

Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time

and

Campbell one-half time to the business. Determine the division of $150,000 of net income in ratio of capital

balances.

a. $75,000 and $75,000 b. $37,500 and $112,500

c. $100,000 and $50,000 d. $50,000 and $100,000

130.

Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest

on

original capital. If they agree to share remaining profits and losses on a 3:2 ratio, what will McMann’s share of

the

income be if the income for the year is $15,000?

a. $6,000

b. $9,400

c. $12,600

d. $14,000

131.

Alpha and Beta are partners who share income in the ratio of 1:2 and have capital balances of $40,000 and

$70,000

at the time they decide to terminate the partnership. After all noncash assets are sold and all liabilities are

paid,

there is a cash balance of $50,000. What amount of loss on realization should be allocated to Alpha?

a. $60,000

b. $20,000

c. $30,000

d. $50,000

Chapter 12: Accounting for Partnerships and Limited Liability Companies

132.

Teri, Doug, and Brian are partners with capital balances of $20,000, $30,000, and $50,000, respectively. They

share

income and losses in the ratio of 3:2:1. Income Summary with a debit balance of $30,000 is closed to the

capital

accounts. Doug withdraws from the partnership. How much cash does he get upon withdrawal?

a. $30,000

b. $20,000

c. $40,000

d. $24,000

133.

A partnership liquidation occurs when

a.

a new partner is admitted

b.

a partner dies

c.

the ownership interest of one partner is sold to a new partner

d.

the assets are sold, liabilities paid, and business operations terminated

134.

The balance sheet of Morgan and Rockwell was as follows immediately prior to the partnership’s liquidation: cash,

$20,000; other assets, $160,000; liabilities, $40,000; Morgan, capital, $60,000; Rockwell, capital, $80,000. The other

assets were sold for $139,000. Morgan and Rockwell share profits and losses in a 2:1 ratio. As a final cash

distribution from the liquidation, Morgan will receive cash totaling

a. $46,000

b. $51,000

c. $60,000

d. $49,500

Chapter 12: Accounting for Partnerships and Limited Liability Companies

135.

Harriet, Mickey, and Zack decide to liquidate their partnership. All assets are sold and the liabilities are paid.

Following these transactions, the capital balances and profit and loss percentages are as follows: Harriet, $27,000 and

30%; Mickey, $(12,000) and 40%; Zack, $43,000 and 30%. Mickey is unable to contribute any assets

to reduce the

deficit. How much cash will Harriet receive as a result of the partnership liquidation?

a. $27,000

b. $21,000

c. $23,400

d. $15,000

136.

The remaining cash of a partnership (after creditors have been paid) upon liquidation is divided among

partners

according to their

a.

capital balances

b.

contribution of assets

c.

drawing balances

d.

income sharing ratio

137.

A gain or loss on realization is divided among partners according to their

a.

income sharing ratio

b.

capital balances

c.

drawing balances

d.

contribution of assets

Chapter 12: Accounting for Partnerships and Limited Liability Companies

138.

Adriana and Belen are partners who share income in the ratio of 3:2 and have capital balances of $50,000 and

$90,000 at the time they decide to terminate the partnership. After all noncash assets are sold and all liabilities are

paid, there is a cash balance of $90,000. How much cash should be distributed to Adriana?

a. $50,000

b. $20,000

c. $30,000

d. $45,000

139.

Everett, Miguel, and Ramona are partners, sharing income 1:2:3. After selling all of the assets for cash, dividing

losses on realization, and paying liabilities, the balances in the capital accounts are as follows: Everett, $50,000

Cr.;

Miguel, $40,000 Dr.; and Ramona, $30,000 Cr. How much cash is available for distribution to the partners?

a. $120,000

b. $30,000

c. $40,000

d. $90,000

140.

Everett, Miguel, and Ramona are partners, sharing income 1:2:3. After selling all of the assets for cash, dividing

losses on realization, and paying liabilities, the balances in the capital accounts are as follows: Everett, $50,000

Cr.;

Miguel, $40,000 Dr.; and Ramona, $30,000 Cr. How much cash should be distributed to Everett assuming

that

Miguel pays the deficiency?

a. $50,000

b. $20,000

c. $30,000

d. $40,000

Chapter 12: Accounting for Partnerships and Limited Liability Companies

141.

Antonio and Barbara are partners who share income in the ratio of 1:2 and have capital balances of $40,000 and

$70,000 at the time they decide to terminate the partnership. After all noncash assets are sold and all liabilities are

paid, there is a cash balance of $80,000. What amount of loss on realization should be allocated to Barbara?

a. $80,000

b. $10,000

c. $20,000

d. $30,000

142.

Soledad and Winston are partners who share income in the ratio of 1:3 and have capital balances of $100,000 and

$140,000 at the time they decide to terminate the partnership. After all noncash assets are sold and all liabilities

are

paid, there is a cash balance of $130,000. What amount of loss on realization should be allocated to Soledad?

a. $60,000

b. $27,500

c. $92,500

d. $32,500

143.

Soledad and Winston are partners who share income in the ratio of 1:3 and have capital balances of $100,000 and

$140,000 at the time they decide to terminate the partnership. After all noncash assets are sold and all liabilities

are

paid, there is a cash balance of $130,000. What amount of loss on realization should be allocated to Winston?

a. $110,000

b. $97,500

c. $42,500

d. $82,500

Chapter 12: Accounting for Partnerships and Limited Liability Companies

144.

Partners Ken and Macki each have a $40,000 capital balance and share income and losses in a ratio of 3:2. Cash

equals $20,000, noncash assets equal $120,000, and liabilities equal $60,000. If the noncash assets are sold for

$80,000, the Macki’s capital account will

a.

decrease by $16,000

b.

decrease by $24,000

c.

increase by $24,000

d.

decrease by $40,000

145.

Partners Ken and Macki each have a $40,000 capital balance and share income and losses in a ratio of 3:2. Cash

equals $20,000, noncash assets equal $120,000, and liabilities equal $60,000. If the noncash assets are sold for

$50,000, and each partner is personally insolvent, Partner Macki will eventually receive cash of

a.

$0

b. $10,000

c. $12,000

d. $20,000

146.

Partners Ken and Macki each have a $40,000 capital balance and share income and losses in a 3:2. Cash equals

$20,000, noncash assets equal $120,000, and liabilities equal $60,000. If the noncash assets are sold for

$60,000,

and both partners agree to make up any capital deficits with personal cash contributions, Partner

Macki will

eventually receive cash of

a.

$0

b. $4,000

c. $16,000

d. $24,000

Chapter 12: Accounting for Partnerships and Limited Liability Companies

147.

Based on this information, the statement of partners’ equity would show what amount in the capital account for Marti

on December 31?

a. $216,000

b. $164,000

c. $380,000

d. $52,000

148.

Based on this information, the statement of partners’ equity would show what amount in the capital account for

Harrison on December 31?

a. $216,000

b. $164,000

c. $380,000

d. $52,000

149.

Based on this information, the statement of partners’ equity would show what amount as total capital for the

partnership on December 31?

a. $216,000

b. $164,000

c. $308,000

d. $52,000

Chapter 12: Accounting for Partnerships and Limited Liability Companies

The capital accounts of Hawk and Martin have balances of $160,000 and $140,000, respectively, on January 1,

the

beginning of the current fiscal year. On April 10, Hawk invested an additional $10,000. During the year,

Hawk and

Martin withdrew $86,000 and $68,000, respectively, and net income for the year was $258,000. The

articles of

partnership make no reference to the division of net income.

150.

Based on this information, the statement of partners’ equity would show what amount in the capital account for

Martin on December 31?

a. $173,000

b. $211,000

c. $201,000

d. $232,000

151.

Based on this information, the statement of partners’ equity would show what amount in the capital account for

Hawk on December 31?

a. $211,600

b. $213,000

c. $201,000

d. $203,000

152.

Based on this information, the statement of partners’ equity would show what amount as total capital for the

partnership on December 31?

a. $384,600

b. $412,600

c. $404,000

d. $414,000

Chapter 12: Accounting for Partnerships and Limited Liability Companies

153.

What is a partnership? List three advantages and three disadvantages of the partnership form of business

organization.

154.

Jesse and Tim form a partnership by combining the assets of their separate businesses. Jesse contributes accounts

receivable with a face amount of $50,000 and equipment with a cost of $180,000 and accumulated depreciation of

$100,000. The partners agree that the equipment is to be valued at $58,000, that $3,500 of the accounts receivable

are completely worthless and are not to be accepted by the partnership, and that $2,000 is a reasonable allowance

for the uncollectibility of the remaining accounts receivable. Tim contributes cash of $21,000 and merchandise

inventory of $44,500. The partners agree that the merchandise inventory is to be valued at $48,000. Journalize

the

entries to record in the partnership accounts (a) Jesse’s investment and (b) Tim’s investment.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

155.

Barton and Fallows form a partnership by combining the assets of their separate businesses. Barton contributes

accounts receivable with a face amount of $50,000 and equipment with a cost of $190,000 and accumulated

depreciation of $100,000. The partners agree that the equipment is to be valued at $85,000, that $3,500 of the

accounts receivable are completely worthless and are not to be accepted by the partnership, and that $1,500 is a

reasonable allowance for the uncollectibility of the remaining accounts receivable. Fallows contributes cash of

$28,500 and merchandise inventory of $55,500. The partners agree that the merchandise inventory is to be

valued

at $60,000. Journalize the entries to record in the partnership accounts (a) Barton’s investment and (b)

Fallows’s

investment.

156.

Trevor Smith contributed equipment, inventory, and $54,000 cash to a partnership. The equipment had a book

value

of $30,000 and a market value of $36,000. The inventory had a book value of $60,000, but only had a

market value

of $20,000, due to obsolescence. The partnership also assumed a $17,000 note payable owed by

Smith that was

used originally to purchase the equipment.

Provide the journal entry for Smith’s contribution to the partnership.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

157.

Emmett and Sierra formed a partnership dividing income as follows:

1. Annual salary allowance to Emmett of $48,000

2. Interest of 8% on each partner’s capital balance on January 1

3. Any remaining net income divided equally

Emmett and Sierra had $25,000 and $140,000, respectively, in their January 1 capital balances.

Net income for the

year was $200,000.

How much net income should be distributed to Emmett?

158.

Emerson and Dakota formed a partnership dividing income as follows:

1. Annual salary allowance to Emerson of $58,000

2. Interest of 8% on each partner’s capital balance on January 1

3. Any remaining net income divided equally

Emerson and Dakota had $25,000 and $140,000 respectively in their January 1 capital balances.

Net income for

the year was $220,000.

How much net income should be distributed to Dakota?

Chapter 12: Accounting for Partnerships and Limited Liability Companies

159.

Gavin invested $45,000 in the Jason and Kelly partnership for ownership equity of $45,000. Prior to the

investment

land was revalued to a market value of $320,000 from a book value of $200,000. Jason and Kelly

share net income

in a 1:2 ratio.

a.

Provide the journal entry for the revaluation of land.

b.

Provide the journal entry to admit Gavin.

160.

Malcolm has a capital balance of $90,000 after adjusting to fair market value. Celeste contributes $45,000

to

receive a 25% interest in a new partnership with Malcolm.

Determine the amount and recipient of the partner bonus.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

161.

The capital accounts of Heidi and Moss have balances of $90,000 and $65,000, respectively on January 1, the

beginning of the current fiscal year. On April 10, Heidi invested an additional $8,000. During the year, Heidi

and

Moss withdrew $40,000 and $32,000, respectively, and net income for the year was $120,000. The articles

of

partnership make no reference to the division of net income.

Required:

(1)

Journalize the entries to:

(a)

Close the income summary account.

(b)

Close the drawing accounts.

(2)

Prepare a statement of partners’ equity for the partnership of Heidi and Moss.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

162.

After the tangible assets have been adjusted to current market prices, the capital accounts of Harper and Kahlil

have balances of $60,000 and $90,000, respectively. Fay is to be admitted to the partnership, contributing

$45,000

cash, for which she is to receive an ownership equity of $60,000. All partners share equally in income.

Required:

(1)

Journalize the entry to record the admission of Fay, who is to receive a bonus of $15,000.

(2)

What are the capital balances of each partner after the admission of the new partner?

Chapter 12: Accounting for Partnerships and Limited Liability Companies

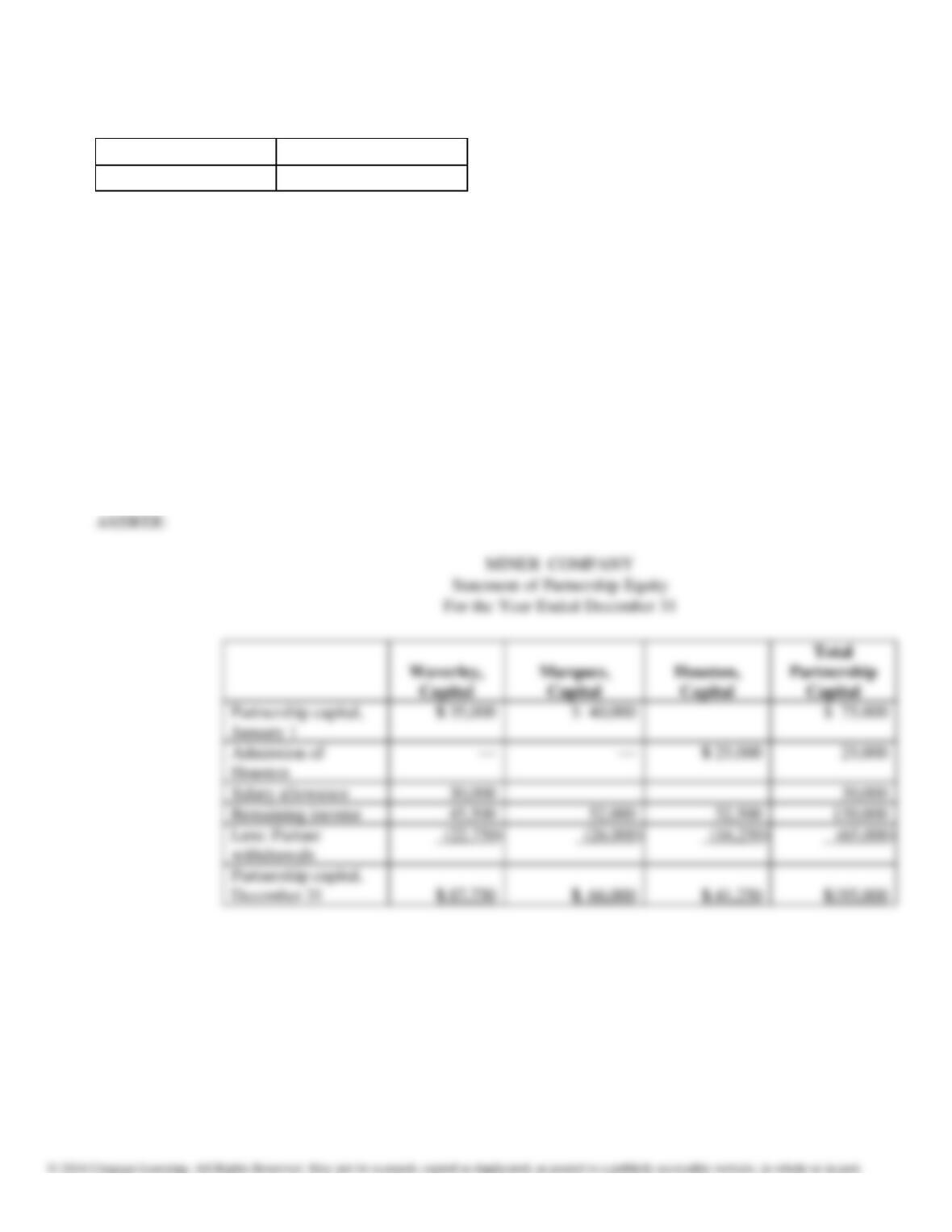

163.

The partnership of Miner Company began operations on January 1, with contributions as follows:

Waverley

$35,000

Marquez

40,000

The following additional partner transactions took place during the year:

(1)

In early January, Houston is admitted to the partnership by contributing $25,000 cash

for

a 25% interest.

(2)

Net income of $160,000 was earned. In addition, Waverley received a salary

allowance

of $30,000 for the year. The three partners agree to an income-sharing ratio

equal to

their capital balances after admitting Houston.

(3)

The partners’ withdrawals are equal to half of their respective distributions of income after salary (i.e., half

their respective portions of the $130,000).

Required:

Prepare a statement of partnership equity for the year ended December 31.

Chapter 12: Accounting for Partnerships and Limited Liability Companies