Chapter 12 – Performance Evaluation and Decentralization

600,000 boxes. If Centra and Mantra agree to transfer boxes, what is the ceiling of the bargaining range and which

division sets it?

a.

$1.48; Centra

b.

$1.35; Centra

c.

$1.80; Mantra

d.

$1.35; Mantra

e.

$1.80; Centra

111. Refer to Figure 12–3. Assume that Grey Inc. allows division managers to negotiate transfer price. Centra is producing

600,000 boxes. If Centra and Mantra agree to transfer boxes, what is the floor of the bargaining range and which division

sets it?

a.

$1.80; Centra

b.

$1.48; Centra

c.

$1.48; Mantra

d.

$1.35; Mantra

e.

$1.35; Centra

112. Refer to Figure 12–3. Assume that Grey Inc. allows division managers to negotiate transfer price. Centra is producing

700,000 boxes. If Centra and Mantra agree to transfer boxes, what is the floor of the bargaining range and which division

sets it?

a.

$1.80; Centra

b.

$1.35; Centra

c.

$1.48; Mantra

d.

$1.35; Mantra

e.

$1.80; Mantra

Figure 12–4.

Quinn Inc. has a number of divisions. One division, Style, makes zippers that are used in the manufacture of boots.

Another division, LeatherStuff, makes boots that use the zippers and needs 90,000 zippers per year. Style incurs the

following costs for one zipper:

Direct materials

$0.23

Direct labor

$0.20

Variable overhead

$0.95

Fixed overhead

$1.32

Total

$2.70

Quinn has capacity to make 950,000 zippers per year, but due to a soft market, only plans to produce and sell 620,000

zippers next year. LeatherStuff currently buys zippers from an outside supplier for $3.50 each (the same price that Style

receives).

Chapter 12 – Performance Evaluation and Decentralization

113. Refer to Figure 12–4. Assume that Quinn allows negotiated transfer pricing. What is the floor of the bargaining range

and which division sets it?

a.

$3.50; Style

b.

$2.70; LeatherStuff

c.

$2.70; Style

d.

$1.38; LeatherStuff

e.

$1.38; Style

114. Refer to Figure 12–4. Assume that Quinn allows negotiated transfer pricing. What is the ceiling of the bargaining

range and which division sets it?

a.

$3.50; Style

b.

$3.50; LeatherStuff

c.

$2.70; Style

d.

$2.70; LeatherStuff

e.

$1.38; Style

LeatherStuff, as the buying division, sets the ceiling at market price, $3.50.

115. Refer to Figure 12–4. Assume that Style and LeatherStuff have agreed on a transfer price of $3.25. What are the total

cost savings for LeatherStuff?

a.

$22,500

b.

$315,000

c.

$292,500

d.

$69,000

e.

$81,000

Previous cost to LeatherStuff = $3.50 × 90,000 = $315,000

Cost to LeatherStuff at $3.25 transfer price = $3.25 × 90,000 = $292,500

Savings to LeatherStuff = $315,000 – $292,500 = $22,500

116. Refer to Figure 12–4. Assume that Style and LeatherStuff have agreed on a transfer price of $3.25. What is the total

benefit for Style?

a.

$243,000

b.

$292,500

c.

$168,300

d.

$69,000

e.

$81,000

Revenue from components transferred = $3.25 × 90,000 = $292,500

Cost to Style = $1.38 × 90,000 = $124,200

117. Refer to Figure 12–4. Assume that Style and LeatherStuff have agreed on a transfer price of $3.25. What is the total

benefit for Quinn, Inc.?

Chapter 12 – Performance Evaluation and Decentralization

a.

$22,500

b.

$292,500

c.

$163,000

d.

$169,000

e.

$190,800

Total benefit = ($3.50 – $1.38) × 90,000 = $190,800

118. The strategic management system that translates an organization’s mission and strategy into operational objectives

and performance measures is

a.

activity-based management.

b.

responsibility accounting.

c.

strategic accounting.

d.

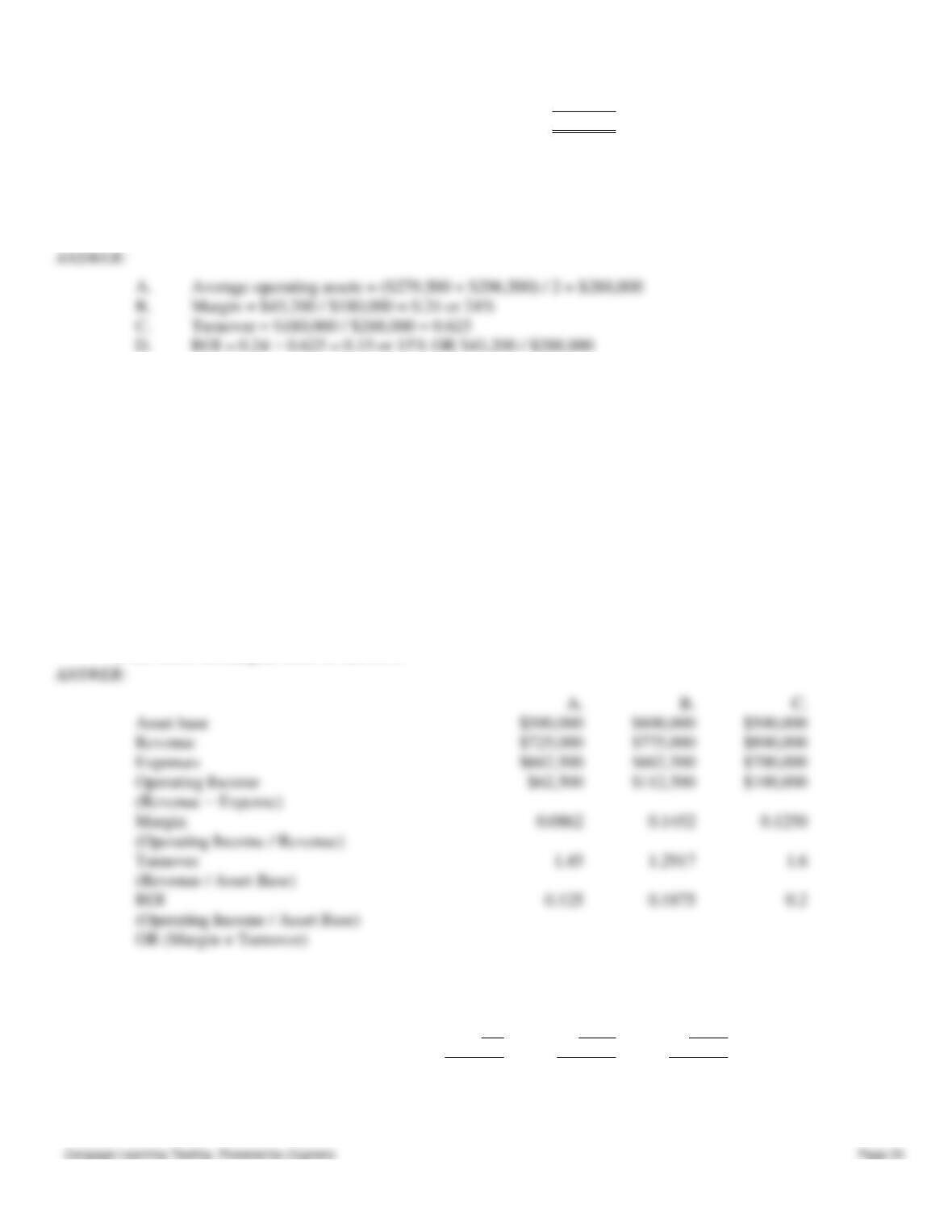

cost information management.

e.

Balanced Scorecard.

e

119. The Balanced Scorecard perspective that describes the internal processes needed to provide value for customers and

owners is the ____ perspective.

a.

customer

b.

internal business process

c.

learning and growth

d.

financial

e.

None of these.

120. The Balanced Scorecard perspective that describes the economic consequences of actions taken in the other three

perspectives is the ____ perspective.

a.

customer

b.

internal business process

c.

learning and growth

d.

financial

e.

None of these.

121. The Balanced Scorecard perspective that defines the customer and market segments in which the business unit will

compete is the ____ perspective.

a.

customer

b.

internal business process

c.

learning and growth

d.

financial

e.

None of these.

a

122. The Balanced Scorecard perspective that defines the capabilities than an organization needs to create long-term

growth and improvement is the ____ perspective.

Chapter 12 – Performance Evaluation and Decentralization

a.

learning and growth

b.

internal business process

c.

customer

d.

financial

e.

None of these.

a

123. A testable strategy is defined as a

a.

set of linked objectives aimed at an overall goal.

b.

means of providing managers with information about the effectiveness of strategy implementation and the

validity of the assumption underlying the strategy.

c.

means of specifying objectives, measures, targets, and initiatives for each perspective of the Balanced

Scorecard.

d.

strategic management system that defines a strategic-based responsibility accounting system.

e.

None of these.

a

124. The difference between realization and sacrifice defines

a.

target objectives.

b.

reliability.

c.

single-loop feedback.

d.

customer value.

e.

None of these.

125. The process value chain consists of

a.

value, operations, and objectives.

b.

innovation, satisfaction, and value.

c.

innovation, operations, and post-sales service.

d.

design, production, and selling.

e.

design, satisfaction, and post-sales service.

c

126. The number of units of output that can be produced in a given period of time is called

a.

cycle time.

b.

unit process time.

c.

responsiveness.

d.

cell conversion time.

e.

velocity.

e

127. MCE (manufacturing cycle efficiency) is calculated using the following formula:

a.

processing time / nonprocessing time.

b.

nonprocessing time / processing time.

c.

total time / processing time.

Chapter 12 – Performance Evaluation and Decentralization

d.

processing time / total time.

e.

total time / nonprocessing time.

128. Last night, Shirley worked on her accounting homework for one and one half hours. During that time, she completed

6 problems. What is the cycle time for one problem?

a.

4 minutes

b.

90 minutes

c.

15 minutes

d.

10 minutes

e.

6 minutes

Cycle time = (1.5 × 60 minutes) / 6 problems = 90 / 6 = 15 minutes per problem

129. Last night, Shirley worked on her accounting homework for one and one half hours. During that time, she completed

6 problems. What is the velocity in problems per hour?

a.

4 per hour

b.

0.67 per hour

c.

6 per hour

d.

10 per hour

e.

15 per hour

Velocity = 6 problems / 1.5 hours = 4 problems per hour

130. Porter Company makes children’s board games. One popular game requires the following amounts of time:

processing − 2 hours; waiting − 6 hours; moving − 4 hours. The Manufacturing Cycle Efficiency (MCE) for Porter

Company is

a.

16.67%.

b.

20.0%.

c.

100%.

d.

25%.

e.

33%.

131. A Utah hospital decided to streamline its surgical suite operation. In order to speed things up, the nurses in charge

studied how much time patients actually spent in various activities. They found that on average, a patient scheduled for an

operation spent about 1 hours waiting, and 1.5 hours in moving from lab to x-ray to the operating room. The average

operation takes 90 minutes. What is the MCE?

a.

100%

b.

60%

c.

50%

d.

37.5%

e.

20%

Chapter 12 – Performance Evaluation and Decentralization

MCE = Processing Time / (Processing time + Move time + Inspection Time + Waiting Time)

132. Pollux Company had the following income statement for last year:

Sales

$360,000

Less: Cost of goods sold

195,000

Gross margin

$165,000

Less: Selling & administrative expense

78,600

Operating income

$ 86,400

Beginning assets were $565,000 and ending assets were $597,000.

(Carry computations out to three decimal places.)

A.

What are average operating assets?

B.

What is margin?

C.

What is turnover?

D.

What is ROI?

A.

Average operating assets = ($565,000 + $597,000) / 2 = $581,000

B.

Margin = $86,400 / $360,000 = 0.240 or 24%

C.

Turnover = $360,000 / $581,000 = 0.620

D.

ROI = $86,400 / $581,000 = 0.149 or 14.9% OR 0.240 × 0.620

133. Noble Company has two divisions, the Domestic Division and the International Division. Last year, the Domestic

Division earned $360,000 using average operating assets of $1,440,000. Sales for the Domestic Division were $3,600,000.

Last year, the International Division earned $560,000 using average operating assets of $2,800,000. Sales for the

International Division were $7,000,000.

A.

For the Domestic Division, margin is __________________ Turnover is

__________________ and ROI is __________________.

B.

For the International Division, margin is __________________ Turnover is

__________________ and ROI is __________________.

C.

If these are the only two divisions of Noble Company, what is ROI for Noble Company?

A.

Margin = $360,000 / $3,600,000 = 0.1 or 10%

Turnover = $3,600,000 / $1,440,000 = 2.5

ROI = 0.1 × 2.5 = 0.25 or 25% OR $360,000 × $1,440,000

B.

Margin = $560,000 / $7,000,000 = 0.08 or 8%

Turnover = $7,000,000 / $2,800,000 = 2.5

ROI = 0.08 × 2.5 = 0.20 or 20% OR $560,000 / $2,800,000

C.

ROI = ($360,000 + $560,000) / ($1,440,000 + $2,800,000) = 0.217 or 21.7%

134. Chase Company had the following income statement for last year:

Sales

$180,000

Less: Cost of goods sold

97,500

Gross margin

$ 82,500

Chapter 12 – Performance Evaluation and Decentralization

Less: Selling & Admin. Expense

39,300

Operating income

$ 43,200

Beginning assets were $279,500 and ending assets were $296,500.

A.

Average operating assets were $__________________.

B.

Margin was __________________.

C.

Turnover was __________________.

D.

Return on investment was __________________%.

A.

Average operating assets = ($279,500 + $296,500) / 2 = $288,000

B.

Margin = $43,200 / $180,000 = 0.24 or 24%

C.

Turnover = $180,000 / $288,000 = 0.625

D.

ROI = 0.24 × 0.625 = 0.15 or 15% OR $43,200 / $288,000

135. Given the following information for the Reardon Division:

Asset base

$500,000

Sales Revenues

$725,000

Expenses

$662,500

Required:

A.

What are the margin, turnover, and ROI for Reardon Division?

B.

Reardon has an option to make an additional investment that would add $100,000 to the

asset base. It would generate an additional $50,000 in sales revenue and no additional

expenses. What would be the effect on margin, turnover and ROI?

C.

Another option (independent of alternative B) for Reardon is to run an advertising

campaign that would require additional advertising expenses of $37,500, but the best

estimate is the campaign would generate an additional $75,000 of revenue. What would

be the effect on margin, turnover and ROI?

Asset base

$500,000

$600,000

$500,000

Revenue

$725,000

$775,000

$800,000

Expenses

$662,500

$662,500

$700,000

Operating Income

$62,500

$112,500

$100,000

(Revenue − Expense)

Margin

(Operating Income / Revenue)

Turnover

1.45

(Revenue / Asset Base)

ROI

0.125

136. Provide the missing data in the following situations:

Phi

Delta

Theta

Division

Division

Division

Sales

$ (A)

$250,000

$ (G)

Operating assets

$ (B)

$ (D)

$800,000

Net operating income

$400,000

$10,000

$144,000

Margin

0.08

(E)

0.12

Chapter 12 – Performance Evaluation and Decentralization

Turnover

(C)

(F)

1.5

Return on investment

16%

10%

(H)

A.

$400,000 / A = 0.08

A = $5,000,000

B.

$400,000 / B = 0.16

B = $2,500,000

C.

C = $5,000,000 / $2,500,000 = 2.0

D.

$10,000 / D = 0.10

D = $100,000

E = $10,000 / $250,000 = 0.04 or 4%

F = $250,000 / $100,000 = 2.5 times

G.

$144,000 / G = 0.12

G = $1,200,000

H.

0.12 × 1.5 = .18 or 18%

Figure 12-7

Monfett Manufacturing earned operating income last year as shown in the following income statement:

Sales

$620,000

Cost of goods sold

316,000

Gross margin

$304,000

Selling and administrative expense

219,000

Operating income

$ 85,000

Less: Income taxes (at 40%)

34,000

Net income

$ 51,000

At the beginning of the year, the value of operating assets was $263,000. At the end of the year, the value of operating

assets was $336,000. Monfett Manufacturing requires a minimum rate of return of 15%. Total capital employed equal

$350,000 and actual cost of capital is 6%.

137. Refer to Figure 12–7. Calculate the following:

A. Average operating assets

B. Margin

C. Turnover

D. Return on investment

(Carry computations out to two decimal places.)

A.

Average operating assets = Beginning assets + ending assets / 2

($263,000 + $336,000) / 2 = $299,500

B.

Margin = Operating income / Sales

$85,000 / $620,000 = .14 or 14%

C.

Chapter 12 – Performance Evaluation and Decentralization

138. Refer to Figure 12–7. Calculate the following:

A. Residual income

B. EVA

A.

Residual income = operating income – (minimum rate of return × average operating assets)

$85,000 – (15% × $299,500) = $40,075

Average operating assets = (Beginning assets + ending assets) / 2

($263,000 + $336,000) / 2 = $299,500

EVA = after-tax operating income – (actual percentage cost of capital × total capital employed)

$51,000 – (6% × $350,000) = $30,000

139. Red Earth Company has two divisions, the Okla Division and the Homa Division. Last year, the Okla Division

earned $66,000 using average operating assets of $550,000. Last year, the Homa Division earned $260,000 using average

operating assets of $2,000,000. Minimum required rate of return for Red Earth is 9%.

A.

For the Okla Division, residual income is __________________.

B.

For the Homa Division, residual income is __________________.

Now assume that the minimum required rate of return for Red Earth is 12%.

C.

For the Okla Division, residual income is __________________.

D.

For the Homa Division, residual income is __________________.

140. The Southern Division of Jenkins Company had income of $48,300, average assets of $345,000 and sales of

$241,500. The minimum rate of return for Jenkins Company is 12%.

A.

What is margin for the Southern Division?

B.

What is turnover for the Southern Division?

C.

What is ROI for the Southern Division?

D.

What is residual income for the Southern Division?

A.

Margin = $48,300 / $241,500 = 0.2 or 20%

B.

Turnover = $241,500 / $345,000 = 0.7

Turnover = Sales / Average operating assets

$620,000 / $299,500 = 2.07

D.

ROI = Margin × Turnover

Chapter 12 – Performance Evaluation and Decentralization

141. Dixie Company has the following data for last year:

Division A

Division B

Sales

$400,000

$300,000

Contribution margin

$160,000

$125,000

Operating income

$80,000

$30,000

Average operating assets

$320,000

$200,000

Cost of capital

15%

15%

Dixie Company has a target ROI of 20%.

Required: Calculate the following amounts for each division:

A.

Margin ratio

B.

Turnover ratio

C.

ROI

D.

Residual income

E.

EVA

A.

Margin ratio = $80,000 / $400,000 = .20 or 20%

B.

Turnover ratio = $400,000 / $320,000 = 1.25

C.

ROI = 0.20 × 1.25 = 25%

D.

Residual income = $80,000 − (0.20 × $320,000) = $16,000

E.

EVA = $80,000 − (0.15 × $320,000) = $32,000

A.

Margin ratio = $30,000 / $300,000 = .10 or 10%

B.

Turnover ratio = $300,000 / $200,000 = 1.50

C.

ROI = 0.10 × 1.50 = 15% OR $30,000 / $200,000

D.

Residual income = $30,000 − (0.20 × $200,000) = $(10,000)

E.

EVA = $30,000 − (0.15 × $200,000) = $0

142. Paige Inc. has a division that makes paint and another division that constructs subdivision houses. The paint division

incurs the following costs for one gallon of paint:

Direct materials

$1.10

Direct labor

1.45

Variable overhead

0.90

Fixed overhead

1.15

Total

$4.60

The Paint Division can make 1,000,000 gallons per year, and is at capacity. The Construction Division currently buys its

C.

ROI = 0.20 × 0.7 = 0.14 or 14% OR $48,300 / $345,000

D.

Residual income = $48,300 − (0.12 × $345,000) = $6,900

Chapter 12 – Performance Evaluation and Decentralization

paint from an outside supplier for $5.20 per gallon (the same price that the Paint Division receives).

A.

The maximum transfer price per gallon of paint is $__________________; this price is

set by which of the two divisions?

B.

The minimum transfer price per gallon of paint is $__________________; this price is

set by which of the two divisions?

A.

$5.20; construction division

B.

$5.20; paint division

143. Paige Inc. has a division that makes paint and another division that constructs subdivisions. The paint division incurs

the following costs for one gallon of paint:

Direct materials

$1.10

Direct labor

1.45

Variable overhead

0.90

Fixed overhead

1.15

Total

$4.60

The Paint Division can make 1,000,000 gallons per year, and expects to produce 800,000 gallons next year. The

Construction Division currently buys 200,000 gallons of paint from an outside supplier for $5.30 per gallon (the same

price that the Paint Division receives).

A.

The maximum transfer price per gallon of paint is $__________________.

B.

The minimum transfer price per gallon of paint is $__________________.

C.

Assume that the transfer takes place at $5 per gallon; calculate the amount by which each

of the following will be better off with the transfer than without it.

Paint Division $__________________

Construction Division $__________________

Paige Inc.,as a whole $__________________

A.

$5.30 (market price)

B.

$3.45 (variable cost per gallon)

C.

Paint Division benefit = ($5.00 − $3.45) × 200,000 = $310,000

Construction Division benefit = ($5.30 − $5.00) × 200,000 = $60,000

Benefit to Paige Inc. = ($5.30 − $3.45) × 200,000 = $370,000

144. Paige Inc. has a division that makes paint and another division that constructs subdivisions. The paint division incurs

the following costs for one gallon of paint:

Direct materials

$1.10

Direct labor

1.45

Variable overhead

0.90

Fixed overhead

1.15

Total

$4.60

The Paint Division can make 1,000,000 gallons per year, and expects to produce 1,000,000 gallons next year. The

construction division currently buys 200,000 gallons of paint from an outside supplier for $5.20 per gallon (the same price

that the Paint Division receives).

A.

The maximum transfer price per gallon of paint is $__________________.

B.

The minimum transfer price per gallon of paint is $__________________.

C.

Does it matter whether or not the two divisions transfer?

Chapter 12 – Performance Evaluation and Decentralization

A.

$5.20 (market price)

B.

$5.20 (market price)

C.

No, it doesn’t matter since the appropriate transfer price is equal to the market price.

145. The Dear Division of Zimmer Company sells all of its output to the Finishing Division of the company. The only

product of the Dear Division is chair legs that are used by the Finishing Division. The retail price of the legs is $20 per

leg. Each chair completed by the Finishing Division requires four legs. Production quantity and cost data for last year are

as follows:

Chair legs

30,000

Direct materials

$135,000

Direct labor

90,000

Overhead (25% is variable)

90,000

Required: Compute the transfer price for a chair leg using:

A.

market price.

B.

variable product costs plus a fixed fee of 20%.

C.

full cost plus 20% markup.

D.

variable costs.

A.

B.

1.20 × [$135,000 + $90,000 + (0.25 × $90,000)] / 30,000 = $9.90

C.

1.20 × ($135,000 + $90,000 + $90,000) / 30,000 = $12.60

D.

[$135,000 + $90,000 + (0.25 × $90,000)] / 30,000 = $8.25

Figure 12-8

Bostonian Inc. has a number of divisions, including Delta Division and ListenNow Division. The ListenNow Division

owns and operates a line of MP3 players. Each year the ListenNow Division purchases component AZ in order to

manufacture the MP3 players. Currently it purchases this component from an outside supplier for $6.50 per component.

The manager of the Delta Division has approached the manager of the ListenNow Division about selling component AZ

to the ListenNow Division. The full product cost of component AZ is $3.10. The Delta Division can sell all of the

components AZ it makes to outside companies for $6.50. The ListenNow Division needs 18,000 component AZs per year;

the Delta Division can make up to 60,000 components per year.

146. Refer to Figure 12–8.

Required:

A. Which division sets the maximum transfer price? Which division sets the minimum transfer price?

B. Suppose the company policy is that all transfer take place at full cost. What is the transfer price?

A.

The maximum transfer price is set by the buying division, in this case, the ListenNow Division. The minimum

B.

Full cost transfer price = $3.10

147. Refer to Figure 12–8. Assume that the company policy is that all transfer prices are negotiated by the divisions

involved.

Required:

Chapter 12 – Performance Evaluation and Decentralization

A. What is the maximum transfer price? Which division sets it?

B. What is the minimum transfer price? Which division sets it?

C. If the transfer takes place, what will be the transfer price?

148. Refer to Figure 12–8. Although the Delta Division has been operating at capacity (60,000 components per year), it

expects to produce and sell only 45,000 components for $6.50 each next year. The Delta Division incurs variable costs of

$1.50 per component. The company policy is that all transfer prices are negotiated by the divisions involved.

Required:

A. What is the maximum transfer price? Which division sets it?

B. What is the minimum transfer price? Which division sets it?

C. Suppose that the two divisions agree on a transfer price of $5.75. What is the change in operating income for the Delta

Division? For the ListenNow Division? For Bostonian Inc. as a whole?

Revenue ($5.75 × 18,000)

Less: Variable cost ($1.50 × 18,000)

Benefit

Outside supplier ($6.50 × 18,000)

Transfer price ($5.75 × 18,000)

Benefit

149. Each month, the vacuum cleaner manufacturing cell has 800 hours of time available. During that time, the cell could

have manufactured up to 2,400 vacuums; but only 1,600 vacuums were actually manufactured. Calculate the following:

A.

Theoretical cycle time in minutes.

B.

Theoretical velocity per hour.

C.

Actual cycle time in minutes.

D.

Actual velocity per hour.

A.

Theoretical cycle time = (800 × 60 minutes) / 2,400 = 20 minutes/vacuum

Chapter 12 – Performance Evaluation and Decentralization

B.

Theoretical velocity = 2,400 vacuums / 800 hours = 3 vacuums per hour

C.

Actual cycle time = 9800 × 60 minutes) / 1,600 = 30 minutes/vacuum

D.

Actual velocity =1600 vacuums / 800 hours = 2 vacuums per hour

150. The pager manufacturing cell has 1,200 hours of time available per quarter. The cell could make 7,200 pagers but

only made 6,000 during that time. Calculate the following:

A.

Theoretical cycle time in minutes.

B.

Theoretical velocity per hour.

C.

Actual cycle time in minutes.

D.

Actual velocity per hour.

E.

MCE is __________________ % (round your answer two digits).

A.

Theoretical cycle time = (1,200 × 60 minutes) / 7,200 = 10 minutes/pager

B.

Theoretical velocity per hour = 7,200 pages / 1,200 hours = 6 pagers per hour

C.

Actual cycle time = (1,200 × 60 minutes) / 6,000 = 12 minutes/pager

D.

Actual velocity = 6,000 pagers / 1,200 hours = 5 pagers per hour

E.

MCE = 10 / 12 = 0.8333 or 83.33%

Figure 12–6.

The First National Bank has a mortgage loan office with conversion cost of $73,950 per month. There are five employees

who each work 170 hours per month. Last month, 1,020 loan applications were processed, but the staff believes that

system improvements could lead to the processing of as many as 1,700 per month.

151. Refer to Figure 12–6. Calculate the following:

A.

Actual cycle time in minutes.

B.

Theoretical cycle time in minutes.

C.

Actual velocity per hour.

D.

Theoretical velocity per hour.

A.

Actual cycle time = (5 × 170 × 60) / 1,020 = 50 minutes/application

B.

Theoretical cycle time = (5 × 170 × 60) / 1,700 = 30 minutes/application

C.

Actual velocity = 60 / 50 = 1.2 applications per hour

D.

Theoretical velocity = 60 / 30 = 2 applications per hour

152. Refer to Figure 12–6. Calculate the following:

A.

Conversion cost in minutes.

B.

Theoretical conversion cost per unit.

C.

Actual conversion cost per unit.

D.

How much more is the department spending per application than it should be if perfect

efficiency could be attained?

A.

Conversion cost = $73,950 / (5 × 170 × 60) = $1.45 per minute

D.

The department is spending $29 ($72.50 − $43.50) more per application than it should be.

Chapter 12 – Performance Evaluation and Decentralization

153. Marshal Company has the following data for one of its manufacturing plants:

Maximum units produced in a quarter = 425,000 units

Actual units produced in a quarter = 354,500 units

Productive hours in one quarter = 35,450 hours

Required:

A. Computer the theoretical cycle time (in minutes).

B. Computer the actual cycle time (in minutes).

C. Compute the theoretical velocity in units per hour.

D. Compute the actual velocity in units per hour.

A.

B.

C.

60 minutes per hour / 5 minutes per unit = 12 units per hour

D.

60 minutes per hour / 6 minutes per unit = 10 units per hour

You decide

154. Explain the differences between centralized and decentralized decision making. Also list some of the reasons why a

company would choose to decentralize.

155. What are the advantages and disadvantages of return on investment (ROI)?

156. How is EVA (Economic Value Added) different from standard residual income calculations?

Chapter 12 – Performance Evaluation and Decentralization

157. The Glass Division of a company makes glass vases which have the following unit costs:

Direct materials

$0.20

Direct labor

0.35

Variable overhead

0.15

Fixed overhead

1.30

Selling commission

0.50

The Florist Division of the company sells cut flowers and uses the glass vases. The Florist Division uses 10,000 vases per

year and currently buys them from an outside supplier for $4 each. The Glass Division produces and sells 100,000 glass

vases per year and sells them on the outside market for $4 each. Vases sold outside incur the sales commission; this

commission would not be paid on internal transfers. The Glass Division and the Florist Division managers just met and

agreed on a transfer price of $3.75 per vase. Is this a good idea for each division? Explain.

158. Describe the four perspectives of the Balanced Scorecard.

Select the term from below to match with the correct statement.

a.

centralization

b.

revenue center

c.

profit center

d.

cost center

e.

investment center

f.

decentralization

159. A(n) ___________ is a responsibility center in which a manager is responsible only for costs.

160. A(n) ___________ is a responsibility center in which a manager is responsible only for sales, or revenues.

161. A(n) ___________ is a responsibility center in which a manager is responsible for revenues, costs, and investments.

e

162. The manager of a(n) ___________ is evaluated on the basis of income.

c

Chapter 12 – Performance Evaluation and Decentralization

163. The practice of delegating decision-making authority to lower levels is __________.

Select the appropriate definition for each of the items listed below.

a.

Turnover

b.

Margin

c.

ROI

d.

Residual income

164. The most common measure of performance for an investment center.

c

165. The ratio of operating income to sales.

166. The ratio of sales to average operating assets.

a

167. The dollar difference between operating income and minimum required return on a company’s operating assets.