Chapter 12: Accounting for Partnerships and Limited Liability Companies

179.

Watson purchased onehalf of Dalton’s interest in the Patton and Dalton partnership for $45,000. Prior to the

investment, land was revalued to a market value of $135,000 from a book value of $93,000. Patton and

Dalton

share net income equally. Dalton had a capital balance of $35,000 prior to these transactions.

Required:

a.

Provide the journal entry for the revaluation of land.

b.

Provide the journal entry to admit Watson.

180.

Wonder purchased one-half of Darwins’ interest in the Todd and Darwin’s partnership for $50,000. Prior to

the

investment, land was revalued to a market value of $175,000 from a book value of $100,000. Todd and

Darwin

share net income equally. Darwin had a capital balance of $40,000 prior to these transactions.

Required:

a.

Provide the journal entry for the revaluation of land.

b.

Provide the journal entry to admit Wonder.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

181.

S. Stephens and J. Perez are partners in Space Designs. Stephens and Perez share income equally. D. Fredricks will

be

admitted to the partnership. Prior to the admission, equipment was revalued downward by $8,000. The capital

balances of

each partner are $100,000 and $139,000, respectively, prior to the revaluation.

Required:

(1)

Provide the journal entry for the asset revaluation.

(2)

Provide the journal entry for Fredricks’ admission under the following independent situations:

a.

Fredricks purchased a 20% interest for $50,000.

b.

Fredricks purchased a 30% interest for $125,000.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

182.

Prior to liquidating their partnership, Samuel and Brian had capital accounts of $60,000 and $240,000,

respectively.

The partnership assets were sold for $120,000. The partnership had no liabilities. Samuel and Brian

share income

and losses equally.

Required:

a.

Determine the amount of Samuel’s deficiency.

b. Determine the amount distributed to Brian, assuming Samuel is unable to satisfy the deficiency.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

183.

Prior to liquidating their partnership, Craig and Jenny had capital accounts of $70,000 and $110,000, respectively.

The partnership assets were sold for $285,000. The partnership had $25,000 of liabilities. Craig and

Jenny share

income and losses equally. Determine the amount received by Jenny as a final distribution from

liquidation of the

partnership.

184.

Prior to liquidating their partnership, Porter and Robert had capital account balances of $160,000 and $100,000,

respectively. Prior to liquidation, the partnership had no cash assets other than what was realized from the sale

of

the partnership assets. These partnership assets were sold for $250,000. The partnership had $10,000 of

liabilities.

Porter and Robert share income and losses equally.

Required:

Determine the amount received by Porter as a final distribution from liquidation of the partnership.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

185.

Immediately prior to the process of liquidation, partners Micco, Niccum, and Orwell have capital balances of

$70,000, $20,000, and $30,000, respectively. There is a cash balance of $10,000, noncash assets total $160,000,

and

liabilities total $50,000. The partners share net income and losses in the ratio of 2:2:1.

Journalize the entries to record the liquidation outlined below, using Assets as the account title for the noncash

assets and Liabilities as the account title for all creditors’ claims.

(a)

Sold the noncash assets for $80,000 in cash.

(b)

Divided the loss on realization.

(c)

Paid the liabilities.

(d)

Received cash from the partner with the deficiency.

(e)

Distributed the cash to the partners.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

186.

Hamir, Darci, and Pete are partners sharing income 3:2:1, respectively. After the firm’s loss from liquidation

is

distributed, the capital account balances were: Hamir, $45,000 Dr.; Darci, $90,000 Cr., and Pete, $64,000

Cr. If

Hamir is personally bankrupt and unable to pay any of the $45,000, what will be the amount of cash

received by

Darci and Pete upon liquidation? Show your work.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

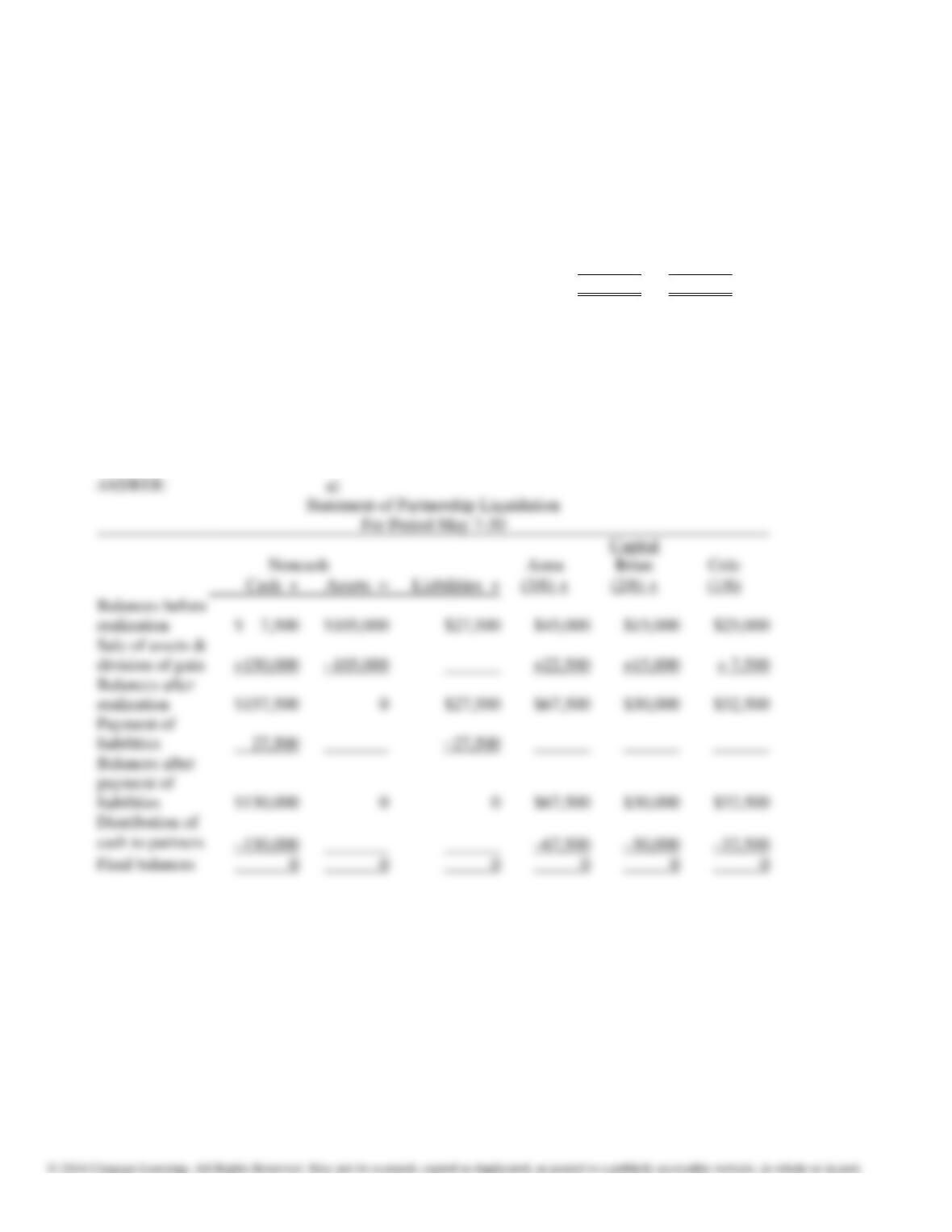

187.

After discontinuing the ordinary business operations and closing the accounts on May 7, the ledger of

the

partnership of Anna, Brian, and Cole indicated the following:

Cash

$ 7,500

Noncash Assets

105,000

Liabilities

$ 27,500

Anna, Capital

45,000

Brian, Capital

15,000

Cole, Capital

25,000

$112,500

$112,500

The partners share net income and losses in the ratio of 3:2:1. Between May 7-30, the noncash assets were sold

for $150,000, the liabilities were paid, and the remaining cash was distributed to the partners.

(a)

Prepare a statement of partnership liquidation.

(b)

Assume the same facts as in (a), except that the noncash assets were sold for $45,000

and any partner with a capital deficiency pays the amount of the deficiency to the

partnership. Prepare a statement of partnership liquidation.

Assets =

realization

Final balances

Chapter 12: Accounting for Partnerships and Limited Liability Companies

Chapter 12: Accounting for Partnerships and Limited Liability Companies

188.

Top Dog, LLC provides repair services for oil rigs. The firm has 5 members in the LLC, which did not change

between the first year and the second year. During Year 2, the business expanded into three new regions of the

country. The following revenue and employee information is provided:

Year 1

Year 2

Revenues (in thousands)

$60,525

$58,500

Number of employees

120

160

Required:

a.

For Year 1 and Year 2, determine the revenue per employee (excluding members).

b.

Interpret the trend between the two years.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

189.

Easy Sailing, LLC provides repair services for commercially-owned boats and yachts. The firm has 5 members in

the LLC, which did not change between the first year and the second year. During Year 2, the business expanded

into three new regions of the country. The following revenue and employee information is provided:

Year 1

Year 2

Revenues (in thousands)

$50,625

$57,750

Number of employees

125

175

Required:

a.

For Year 1 and Year 2, determine the revenue per employee (excluding members).

b.

Interpret the trend between the two years.

Chapter 12: Accounting for Partnerships and Limited Liability Companies

Match each statement to the appropriate term (a-h):

a.

deficiency

b.

realization

c.

proprietorship

d.

partnership

e.

mutual agency

f.

liquidation

g.

income sharing ratio

h.

statement of partnership equity

DIFFICULTY: Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES: ACCT.WARD.16.12-01 – 12–01

ACCT.WARD.16.12-04 – 12–04

ACCT.WARD.16.12-05 – 12–05

ACCREDITING STANDARDS: ACCT.ACBSP.APC.19 – Partnership Accounting

ACCT.AICPA.BB.03 – Legal

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

190.

Where changes in partner capital accounts for a period of time are reported

191.

The share of loss on realization is greater than the balance in partner capital

192.

Each partner may act on behalf of the entire partnership so that the liabilities created by one partner become the

liabilities of all partners

193.

An association of two or more persons to own and manage a business for profit

194.

Business owned by a single individual

195.

A step during liquidation when partnership assets are sold

Chapter 12: Accounting for Partnerships and Limited Liability Companies

196.

Used to divide the excess of allowances over loss when net losses occur

197.

The winding-up process of a partnership

Match each statement to the appropriate term (a-h).

a.

partnership

b.

partnership agreement

c.

distribution of remaining cash to partners

d.

mutual agency

e.

equally

f.

death of a partner

g.

liquidation

h.

unlimited liability

DIFFICULTY: Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES: ACCT.WARD.16.12-01 – 12–01

ACCT.WARD.16.12-04 – 12–04

ACCREDITING STANDARDS: ACCT.ACBSP.APC.19 – Partnership Accounting

ACCT.AICPA.BB.03 – Legal

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

198.

When a partnership cannot pay its debts with business assets, the partners must use personal assets to meet the

debt

199.

Agreement that is the contract between partners

200.

A voluntary association of two or more persons who co-own a business for profit

201.

Every partner can bind the business to a contract within the scope of the partnership’s regular business operations

Chapter 12: Accounting for Partnerships and Limited Liability Companies

202.

The process of going out of business by selling the entity’s assets and paying its liabilities

203.

Without an agreement, the law will stipulate this method of sharing profits and losses

204.

The final step in the liquidation of a partnership

205.

Causes the closing of accounts and settling with a partner’s estate