FOR INSTRUCTOR USE ONLY

CHAPTER 12

INVESTMENTS

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

True-False Statements

1.

1

K

8.

3

C

15.

4

C

22.

5

C

sg29.

1

K

2.

1

C

9.

3

C

16.

4

K

23.

6

K

sg30.

2

K

3.

2

K

10.

3

K

17.

5

C

24.

6

K

sg31.

3

K

4.

2

C

11.

3

C

18.

5

K

25.

6

C

sg32.

4

C

5.

2

C

12.

3

K

19.

5

K

a26.

7

K

sg33.

5

K

6.

2

C

13.

3

K

20.

5

C

a 27.

7

K

sg34.

6

C

7.

2

K

14.

4

K

21.

5

K

a 28.

7

K

Multiple Choice Questions

35.

1

K

58.

3

AP

81.

3

K

104.

5

K

127.

6

C

36.

1

K

59.

3

AP

82.

3

K

105.

5

K

a 128.

7

C

37.

1

K

60.

3

K

83.

3

K

106.

5

C

a 129.

7

C

38.

1

K

61.

3

AP

84.

3

K

107.

5

K

a 130.

7

AP

39.

1

K

62.

3

AP

85.

3

K

108.

5

K

a 131.

7

K

40.

2

K

63.

3

AP

86.

3

K

109.

5

K

a 132.

7

K

41.

2

C

64.

3

AP

87.

3

C

110.

5

AP

sg133.

1

C

42.

2

AP

65.

3

AP

88.

3

C

111.

5

AP

st134.

2

K

43.

2

AN

66.

3

K

89.

3

C

112.

5

C

st135.

2

K

44.

2

AP

67.

3

K

90.

3

AP

113.

5

K

st136.

3

K

45.

2

AP

68.

3

AP

91.

3

AP

114.

5

C

sg137.

3

K

46.

2

AN

69.

3

AP

92.

3

AN

115.

5

C

sg138.

3

K

47.

2

K

70.

3

K

93.

3

AN

116.

5

K

sg139.

3

AP

48.

2

C

71.

3

K

94.

3

AN

117.

5

AP

st140.

5

K

49.

2

K

72.

3

C

95.

3

AN

118.

5

K

sg141.

5

K

50.

2

AP

73.

3

C

96.

4

K

119.

5

AP

sg142.

6

K

51.

2

AP

74.

3

K

97.

4

C

120.

5

AP

st143.

6

K

52.

2

AP

75.

3

K

98.

4

K

121.

5

AP

144.

8

K

53.

2

K

76.

3

K

99.

4

K

122.

5

AP

145.

8

K

54.

2

K

77.

3

AP

100.

4

K

123.

6

C

146.

8

K

55.

2

AP

78.

3

K

101.

4

K

124.

6

K

147.

8

K

56.

2

AP

79.

3

C

102.

4

K

125.

6

C

148.

8

K

57.

3

AP

80.

3

C

103.

5

K

126.

6

K

Brief Exercises

149.

2

AP

151.

3

AP

153.

3

AP

155.

5

AP

157.

5

AP

150.

2

AP

152.

3

AP

154.

3

AP

156.

5

AP

158.

5

AP

sg This question also appears in the Study Guide.

st This question also appears in a self-test at the student companion website.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 2

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Exercises

159.

2

AP

164.

3

AP

169.

3

AP

174.

5

AP

179.

7

AP

160.

2

AN

165.

3,5

AN

170.

3

AP

175.

5

AN

180.

7

AP

161.

2

AP

166.

3,5

AN

171.

3

AP

176.

5

AP

181.

7

AP

162.

2,3

AP

167.

3

AP

172.

3

AP

177.

5

AN

163.

3

AP

168.

3

AP

173.

5,6

AN

178.

5,6

AP

Completion Statements

182.

2

K

185.

3

K

188.

5

K

191.

5

K

183.

2

K

186.

3

AP

189.

5

K

192.

5

K

184.

3

K

187.

4

K

190.

5

K

193.

6

K

Matching Statements

194.

2

K

Short-Answer Essay

195.

3,5

K

197.

5

K

199.

5

K

201.

3

K

196.

4

K

198.

5

K

200.

5

K

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

26.

TF

36.

MC

38.

MC

133.

MC

2.

TF

35.

MC

37.

MC

39.

MC

Learning Objective 2

3.

TF

30.

TF

44.

MC

49.

MC

54.

MC

149.

BE

162.

Ex

4.

TF

40.

MC

45.

MC

50.

MC

55.

MC

150.

BE

182.

C

5.

TF

41.

MC

46.

MC

51.

MC

56.

MC

159.

Ex

183.

C

6.

TF

42.

MC

47.

MC

52.

MC

134.

MC

160.

Ex

194.

Ma

7.

TF

43.

MC

48.

MC

53.

MC

135.

MC

161.

Ex

Learning Objective 3

8.

TF

58.

MC

69.

MC

80.

MC

91.

MC

155.

Ex

174.

C

9.

TF

59.

MC

70.

MC

81.

MC

92.

MC

156.

Ex

175.

C

10.

TF

60.

MC

71.

MC

82.

MC

128.

MC

157.

Ex

184.

SA

11.

TF

61.

MC

72.

MC

83.

MC

129.

MC

158.

Ex

190.

SA

12.

TF

62.

MC

73.

MC

84.

MC

130.

MC

159.

Ex

13.

TF

63.

MC

74.

MC

85.

MC

131.

MC

160.

Ex

28.

TF

64.

MC

75.

MC

86.

MC

143.

BE

161.

Ex

54.

MC

65.

MC

76.

MC

87.

MC

144.

BE

162.

Ex

55.

MC

66.

MC

77.

MC

88.

MC

145.

BE

163.

Ex

56.

MC

67.

MC

78.

MC

89.

MC

146.

BE

164.

Ex

57.

MC

68.

MC

79.

MC

90.

MC

154.

Ex

173.

C

Learning Objective 4

14.

TF

16.

TF

96.

MC

98.

MC

100.

MC

102.

MC

196.

SA

15.

TF

32.

TF

97.

MC

99.

MC

101.

MC

187.

C

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise

Investments

FOR INSTRUCTOR USE ONLY

12 – 3

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Learning Objective 5

17.

TF

104.

MC

112.

MC

120.

MC

158.

BE

178.

Ex

199.

SA

18.

TF

105.

MC

113.

MC

121.

MC

165.

Ex

188.

C

200.

SA

19.

TF

106.

MC

114.

MC

122.

MC

166.

Ex

189.

C

20.

TF

107.

MC

115.

MC

140.

MC

173.

Ex

190.

C

21.

TF

108.

MC

116.

MC

141.

MC

174.

Ex

191.

C

22.

TF

109.

MC

117.

MC

155.

BE

175.

Ex

192.

C

33.

TF

110.

MC

118.

MC

156.

BE

176.

Ex

197.

SA

103.

MC

111.

MC

119.

MC

157.

BE

177.

Ex

198.

SA

Learning Objective 6

23.

TF

34.

TF

125.

MC

142.

MC

173.

Ex

195.

SA

24.

TF

123.

MC

126.

MC

143.

MC

178.

Ex

199.

SA

25.

TF

124.

MC

127.

MC

172.

Ex

193.

C

Learning Objective 7

26.

TF

28.

TF

129.

MC

131.

MC

179.

Ex

181.

Ex

27.

TF

128.

MC

130.

MC

132.

MC

180.

Ex

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise

The chapter also contains one set of ten Matching questions and Seven Short-Answer Essay

questions. CHAPTER LEARNING OBJECTIVES

1. Discuss why corporations invest in debt and stock securities. Corporations invest for

three primary reasons: (a) They have excess cash; (b) They view investments as a

significant revenue source; or (c) They have strategic goals such as gaining control of a

competitor or moving into a new line of business.

2. Explain the accounting for debt investments. Companies record investments in debt

securities when they purchase bonds, receive or accrue interest, and sell the bonds. They

report gains or losses on the sale of bonds in the “Other revenues and gains” or “Other

expenses and losses” sections of the income statement.

3. Explain the accounting for stock investments. Companies record investments in

common stock when they purchase the stock, receive dividends, and sell the stock. When

ownership is less than 20%, the cost method is used. When ownership is between 20% and

50%, the equity method should be used. When ownership is more than 50%, companies

prepare consolidated financial statements.

4. Describe the use of consolidated financial statements. When a company owns more

than 50% of the common stock of another company, it usually prepares consolidated

financial statements. These statements indicate the magnitude and scope of operations of

the companies under common control.

5. Indicate how debt and stock investments are reported in financial statements.

Investments in debt and stock securities are classified as trading, available-for-sale, or held-

to-maturity securities for valuation and reporting purposes. Stock investments are classified

as either trading or available-for-sale securities. Stock investments have no maturity date

and therefore are never classified as held-to-maturity securities. Trading securities are

Test Bank for Financial Accounting, Ninth Edition

12 – 4

reported in current assets at fair value, with changes from cost reported in net income.

Available-for-sale securities are also reported at fair value, with the changes from cost

reported in stockholders’ equity. Available-for-sale securities are classified as short-term or

long-term depending on their expected future sale date.

6. Distinguish between short-term and long-term investments. Short-term investments are

securities that are (a) readily marketable and (b) intended to be converted to cash within the

next year or operating cycle, whichever is longer. Investments that do not meet both criteria

are classified as long-term investments.

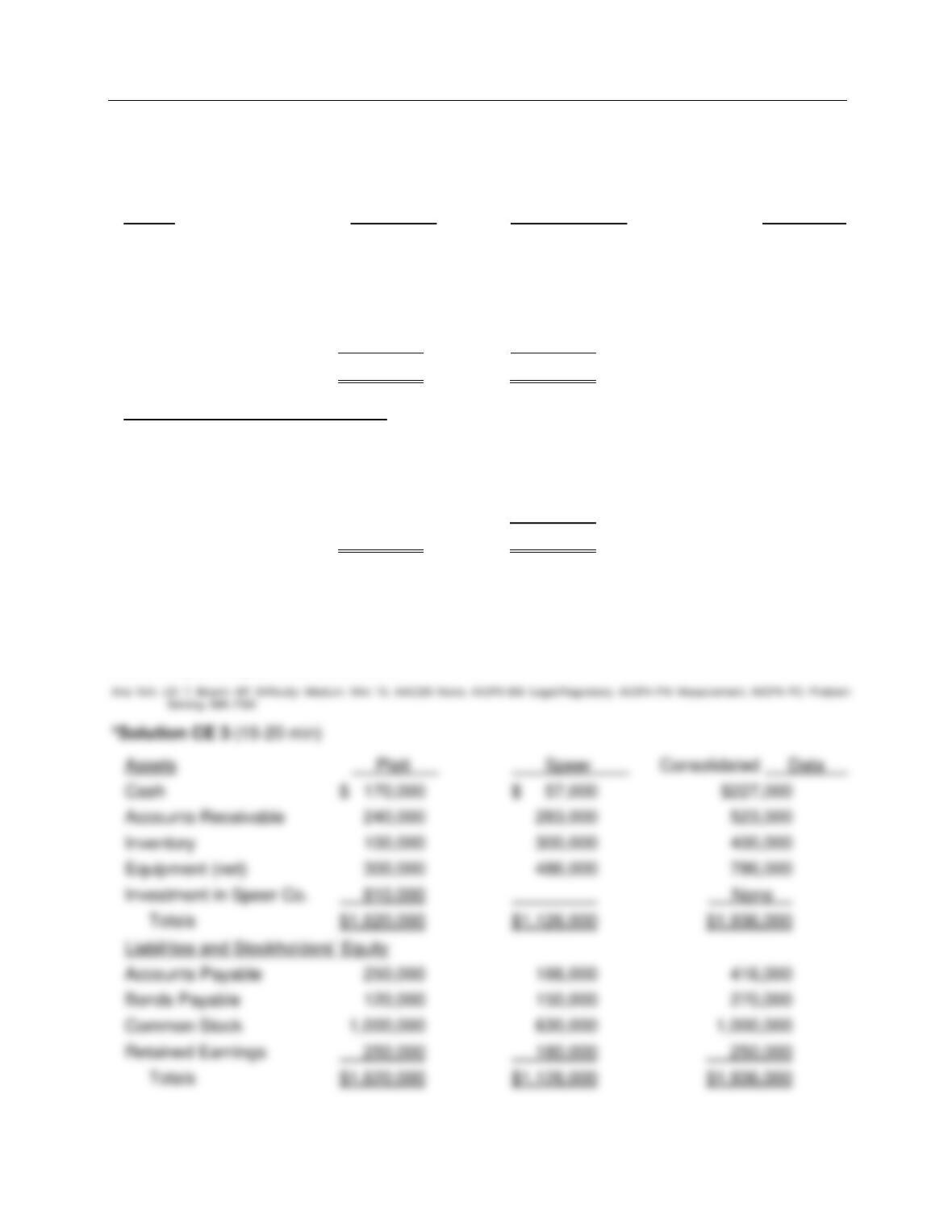

7. Describe the form and content of consolidated financial statements as well as how to

prepare them. Consolidated financial statements are similar in form and content to the

financial statements of an individual corporation. A consolidated balance sheet shows the

assets and liabilities controlled by the parent company. A consolidated income statement

shows the result of operations of affiliated companies as though they are one economic

unit. The worksheet for a consolidated balance sheet contains column for (a) the balance

sheet data for the separate entities, (b) intercompany eliminations, and (c) consolidated

data.

TRUE-FALSE STATEMENTS

1. Corporations purchase investments in debt or stock securities generally for one of two

reasons.

2. A reason some companies purchase investments is because they generate a significant

portion of their earnings from investment income.

3. The accounting for short-term debt investments and for long-term debt investments is

similar.

4. When debt investments are sold, the gain or loss is the difference between the net

proceeds from the sale and the fair value of the bonds.

5. Debt investments are investments in government and corporation bonds.

6. In accordance with the historical cost principle, brokerage fees should be added to the

cost of an investment.

7. In accordance with the historical cost principle, the cost of debt investments includes

brokerage fees and accrued interest.

Investments

12 – 5

8. In accounting for stock investments of less than 20%, the equity method is used.

9. Dividends received on stock investments of less than 20% should be credited to the Stock

Investments account.

10. If an investor owns between 20% and 50% of an investee’s common stock, it is presumed

that the investor has significant influence on the investee.

11. The Stock Investments account is debited at acquisition under both the equity method and

cost method of accounting for investments in common stock.

12. Under the equity method, the investment in common stock is initially recorded at cost, and

the Stock Investments account is adjusted annually.

13. Under the equity method, the receipt of dividends from the investee company results in an

increase in the Stock Investments account.

14. Consolidated financial statements are appropriate when an investor controls an investee

by ownership of more than 50% of the investee’s common stock.

15. Consolidated financial statements are prepared in place of the financial statements for the

parent and subsidiary companies.

16. Consolidated financial statements should be prepared only when a subsidiary company

has a controlling interest in the parent company.

17. The valuation of available-for-sale securities is similar to the procedures followed for

trading securities, except that changes in fair value are not recognized in current income.

18. An unrealized gain or loss on trading securities is reported as a separate component of

stockholders’ equity.

Test Bank for Financial Accounting, Ninth Edition

12 – 6

19. For available-for-sale securities, the unrealized gain or loss account is carried forward to

future periods.

20. A decline in the fair value of a trading security is recorded by debiting an unrealized loss

account and crediting the Fair Value Adjustment account.

21. If the fair value of an available-for-sale security exceeds its cost, the security should be

written up to fair value and a realized gain should be recognized.

22. The Fair Value Adjustment account can only have a credit balance or a zero balance.

23. To be classified as a short-term investment, the investment must be readily marketable

and intended to be converted into cash within the next year or operating cycle.

24. An investment is readily marketable if it is management’s intent to sell the investment.

25. Stocks traded on the New York Stock Exchange are considered readily marketable.

26. When a parent company acquires a wholly owned subsidiary for an amount in excess of

the book value of the net assets acquired, the excess is always allocated to goodwill.

27. A consolidated income statement will reflect only revenue and expense transactions

between the consolidated entity and parties outside the affiliated group.

28. The process of excluding intercompany transactions in preparing consolidated statements

is referred to as intercompany eliminations.

29. One of the reasons a corporation may purchase investments is that it has excess cash.

30. When recording bond interest, Interest Receivable is reported as a fixed asset in the

balance sheet.

Investments

12 – 7

31. Under the cost method, the investment is recorded at cost and revenue is recognized only

when cash dividends are received.

32. Consolidated financial statements present a condensed version of the financial

statements so investors will not experience information overload.

33. Available-for-sale securities are securities bought and held primarily for sale in the near

term to generate income on short-term price differences.

34. “Intent to convert” does not include an investment used as a resource that will be used

whenever the need for cash arises.

Answers to True-False Statements

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

MULTIPLE CHOICE QUESTIONS

35. Corporations invest excess cash for short periods of time in each of the following except

a. equity securities.

b. highly liquid securities.

c. low-risk securities.

d. government securities.

36. Corporations invest in other companies for all of the following reasons except to

a. house excess cash until needed.

b. generate earnings.

c. meet strategic goals.

d. increase trading of the other companies’ stock.

37. A typical investment to house excess cash until needed is

a. stocks of companies in a related industry.

b. debt securities.

c. low-risk, highly liquid securities.

d. stock securities.

Test Bank for Financial Accounting, Ninth Edition

12 – 8

38. A company may purchase a noncontrolling interest in another firm in a related industry

a. to house excess cash until needed.

b. to generate earnings.

c. for strategic reasons.

d. for speculative reasons.

39. Pension funds and mutual funds regularly invest in debt and stock securities to

a. generate earnings.

b. house excess cash until needed.

c. meet strategic goals.

d. control the company in which they invest.

40. At the time of acquisition of a debt investment,

a. no journal entry is required.

b. the historical cost principle applies.

c. the Stock Investments account is debited when bonds are purchased.

d. the Investment account is credited for its cost plus brokerage fees.

41. Which of the following is not a true statement regarding short-term debt investments?

a. The securities usually pay interest.

b. Investments are frequently government or corporate bonds.

c. This type of investment must be currently traded in the securities market.

d. Debt investments are recorded at the price paid less brokerage fees.

42. On January 1, 2014, Brenner Company purchased at face value, a $1,000, 6% bond that

pays interest on January 1 and July 1. Brenner Company has a calendar year end.

The entry for the receipt of interest on July 1, 2014, is

a. Cash ……………………………………………………………………….. 30

Interest Revenue ……………………………………………….. 30

b. Cash ……………………………………………………………………….. 60

Interest Revenue ……………………………………………….. 60

c. Interest Receivable ……………………………………………………. 30

Interest Revenue ……………………………………………….. 30

d. Interest Receivable ……………………………………………………. 60

Interest Revenue ……………………………………………….. 60

Investments

12 – 9

43. On January 1, 2014, Brenner Company purchased at face value, a $1,000, 8% bond that

pays interest on January 1 and July 1. Brenner Company has a calendar year end.

The adjusting entry on December 31, 2014, is

a. not required.

b. Cash ……………………………………………………………………….. 40

Interest Revenue ……………………………………………….. 40

c. Interest Receivable ……………………………………………………. 40

Interest Revenue ……………………………………………….. 40

d. Interest Receivable ……………………………………………………. 40

Debt Investments ………………………………………………. 40

44. On January 1, 2014, Brenner Company purchased at face value, a $1,000, 10% bond that

pays interest on January 1 and July 1. Brenner Company has a calendar year end.

The entry for the receipt of interest on January 1, 2015 is

a. Cash ……………………………………………………………………….. 110

Interest Revenue ……………………………………………….. 110

b. Cash ……………………………………………………………………….. 100

Interest Receivable ……………………………………………. 100

c. Cash ……………………………………………………………………….. 40

Interest Revenue ……………………………………………….. 40

d. Cash ……………………………………………………………………….. 50

Interest Receivable ……………………………………………. 50

45. On January 1, Skills Company purchased as a short-term investment a $1,000, 6% bond

for $1,000. The bond pays interest on January 1 and July 1. The bond is sold on October

1 for $1,200 plus accrued interest. Interest has not been accrued since the last interest

payment date. What is the entry to record the cash proceeds at the time the bond is sold?

a. Cash ……………………………………………………………………….. 1,200

Debt Investments ……………………………………………… 1,200

b. Cash ……………………………………………………………………….. 1,215

Debt Investments ………………………………………………. 1,000

Gain on Sale of Debt Investments ………………………… 200

Interest Revenue ……………………………………………….. 15

c. Cash ……………………………………………………………………….. 1,215

Debt Investments ………………………………………………. 1,200

Interest Revenue ……………………………………………….. 15

d. Cash ……………………………………………………………………….. 1,200

Debt Investments ………………………………………………. 1,000

Gain on Sale of Debt Investments ………………………… 200

Test Bank for Financial Accounting, Ninth Edition

12 – 10

46. Which of the following is not a true statement about the accounting for debt investments?

a. At acquisition, the historical cost principle applies.

b. The cost includes any brokerage fees.

c. Debt investments include investments in government and corporation bonds.

d. The cost includes any accrued interest.

47. The cost of debt investments includes each of the following except

a. brokerage fees.

b. commissions.

c. accrued interest.

d. the price paid.

48. If a short-term debt investment is sold, the Investment account is

a. credited for the book value of the bonds at the sale date.

b. credited for the cost of the bonds at the sale date.

c. credited for the fair value of the bonds at the sale date.

d. debited for the cost of the bonds at the sale date.

49. In accounting for debt investments, entries are made for each of the following except the

a. acquisition.

b. interest revenue.

c. sale.

d. entries are made for each answer choice.

50. Bay Company acquires 60, 8%, 5 year, $1,000 Community bonds on January 1, 2014 for

$60,000.

The journal entry to record this investment includes a debit to

a. Debt Investments for $64,800.

b. Debt Investments for $60,000.

c. Cash for $60,000.

d. Stock Investments for $60,000.

51. Bay Company acquires 60, 8%, 5 year, $1,000 Community bonds on January 1, 2014 for

$60,000.

Assume Community pays interest on January 1 and July 1, and the July 1 entry was done

correctly. The journal entry at December 31, 2014 would include a credit to

a. Interest Receivable for $2,400.

b. Interest Revenue for $4,800.

c. Accrued Expense for $4,800.

d. Interest Revenue for $2,400.

Investments

12 – 11

52. Bay Company acquires 60, 8%, 5 year, $1,000 Community bonds on January 1, 2014 for

$60,000.

If Bay sells all of its Community bonds for $64,500, what gain or loss is recognized?

a. Loss of $9,300

b. Loss of $4,500

c. Gain of $9,300

d. Gain of $4,500

53. Ban Co. purchased 50, 5% Waylan Company bonds for $50,000 cash plus brokerage fees

of $500. Interest is payable semiannually on July 1 and January 1. The entry to record the

July 1 semiannual interest payment would include a

a. debit to Interest Receivable for $1,250.

b. credit to Interest Revenue for $1,250.

c. credit to Interest Revenue for $1,262.50.

d. credit to Debt Investments for $1,262.50.

54. Ban Co. purchased 50, 5% Waylan Company bonds for $50,000 cash plus brokerage fees

of $500. Interest is payable semiannually on July 1 and January 1. The entry to record the

December 31 interest accrual would include a

a. debit to Interest Receivable for $1,250.

b. debit to Interest Revenue for $1,250.

c. credit to Interest Revenue for $1,262.50.

d. debit to Debt Investments for $1,262.50.

55. Tempest Co. purchased 60, 6% Urich Company bonds for $60,000 cash. Interest is

payable semiannually on July 1 and January 1. If 30 of the securities are sold on July 1 for

$32,000, the entry would include a credit to Gain on Sale of Debt Investments for

a. $1,600.

b. $1,750.

c. $1,800.

d. $2,000.

Test Bank for Financial Accounting, Ninth Edition

12 – 12

56. On January 1, Hamm Company purchased as an investment a $1,000, 6% bond for

$1,020. The bond pays interest on January 1 and July 1. What is the entry to record the

interest accrual on December 31?

a. Interest Receivable ……………………………………………………. 30

Interest Revenue ………………………………………………. 30

b. Debt Investments ……………………………………………………… 30

Interest Revenue ………………………………………………. 30

c. Interest Receivable ……………………………………………………. 60

Interest Revenue ………………………………………………. 60

d. Debt Investments ……………………………………………………… 60

Interest Revenue ………………………………………………. 60

57. Beak Corporation sells 200 shares of common stock being held as an investment. The

shares were acquired six months ago at a cost of $25 a share. Beak sold the shares for

$40 a share. The entry to record the sale is

a. Cash ……………………………………………………………………….. 5,000

Loss on Sale of Stock Investments ……………………………… 3,000

Stock Investments …………………………..………………… 8,000

b. Stock Investments …………………………………………………….. 8,000

Cash ……………………………………………………………….. 8,000

c. Cash ……………………………………………………………………….. 8,000

Gain on Sale of Stock Investments ………………………. 3,000

Stock Investments …………………………..………………… 5,000

d. Cash ……………………………………………………………………….. 8,000

Stock Investments …………………………..………………… 8,000

58. Yeloe Corporation sells 400 shares of common stock being held as an investment. The

shares were acquired six months ago at a cost of $60 a share. Yeloe sold the shares for

$40 a share. The entry to record the sale is

a. Cash ……………………………………………………………………….. 16,000

Loss on Sale of Stock Investments ……………………………… 8,000

Stock Investments …………………………..………………… 24,000

b. Cash ……………………………………………………………………….. 24,000

Gain on Sale of Stock Investments ………………………. 8,000

Stock Investments …………………………..………………… 16,000

c. Cash ……………………………………………………………………….. 16,000

Stock Investments …………………………..………………… 6,000

d. Stock Investments …………………………………………………….. 16,000

Loss on Sale of Stock Investments ……………………………… 8,000

Cash ………………………………………………………………… 24,000

Investments

12 – 13

59. Blaine Company had these transactions pertaining to stock investments:

Feb. 1 Purchased 2,000 shares of Horton Company (10%) for $51,000 cash.

June 1 Received cash dividends of $2 per share on Horton stock.

Oct. 1 Sold 1,200 shares of Horton stock for $32,400.

The entry to record the purchase of the Horton stock would include a

a. debit to Stock Investments for $45,900.

b. credit to Cash for $45,900.

c. debit to Stock Investments for $51,000.

d. debit to Investment Expense for $5,100.

60. Blaine Company had these transactions pertaining to stock investments:

Feb. 1 Purchased 2,000 shares of Horton Company (10%) for $51,000 cash.

June 1 Received cash dividends of $3 per share on Horton stock.

Oct. 1 Sold 1,200 shares of Horton stock for $32,400.

The entry to record the receipt of the dividends on June 1 would include a

a. debit to Stock Investments for $6,000.

b. credit to Dividend Revenue for $6,000.

c. debit to Dividend Revenue for $6,000.

d. credit to Stock Investments for $6,000.

61. Blaine Company had these transactions pertaining to stock investments:

Feb. 1 Purchased 2,000 shares of Norton Company (10%) for $51,000.

June 1 Received cash dividends of $2 per share on Horton stock.

Oct. 1 Sold 1,200 shares of Horton stock for $32,400.

The entry to record the sale of the stock would include a

a. debit to Cash for $30,600.

b. credit to Gain on Sale of Stock Investments for $1,200.

c. debit to Stock Investments for $30,600.

d. credit to Gain on Sale of Stock Investments for $1,800.

62. Mize Company owns 30% interest in the stock of Lyte Corporation. During the year, Lyte

pays $20,000 in dividends to Mize, and reports $300,000 in net income. Mize Company’s

investment in Lyte will increase Mizes net income by

a. $6,000.

b. $90,000.

c. $96,000.

d. $10,000.

Test Bank for Financial Accounting, Ninth Edition

12 – 14

63. Penny Company owns 20% interest in the stock of Lynn Corporation. During the year,

Lynn pays $25,000 in dividends, and reports $200,000 in net income. Penny Company’s

investment in Lynn will increase by

a. $25,000.

b. $40,000.

c. $45,000.

d. $35,000.

64. On January 1, 2014, Grgante Corporation purchased 25% of the common stock

outstanding of Long Corporation for $270,000. During 2014, Long Corporation reported

net income of $80,000 and paid cash dividends of $40,000. The balance of the Stock

Investments—Long account on the books of Grgante Corporation at December 31, 2014

is

a. $270,000.

b. $310,000.

c. $350,000.

d. $280,000.

65. Gayton Corporation purchased 1,000 shares of Smart common stock ($50 par) at $80 per

share as a short-term investment. The shares were subsequently sold at $78 per share.

The cost of the securities purchased and gain or loss on the sale were

Cost Gain or Loss

a. $50,000 $2,000 gain

b. $50,000 $2,000 loss

c. $80,000 $2,000 gain

d. $80,000 $2,000 loss

66. In accounting for stock investments between 20% and 50%, the _______ method is used.

a. consolidated statements

b. controlling interest

c. cost

d. equity

67. When a company holds stock of several different corporations, the group of securities is

identified as a(n)

a. affiliated investment.

b. consolidated portfolio.

c. investment portfolio.

d. controlling interest.

Investments

12 – 15

68. Roxy Corporation makes a short-term investment in 180 shares of Sager Company’s

common stock. The stock is purchased for $53 a share. The entry for the purchase is

a. Debt Investments ………………………………………………………. 9,540

Cash ……………………………………………………………….. 9,540

b. Stock Investments …………………………………………………….. 9,540

Cash ……………………………………………………………….. 9,540

c. Stock Investments …………………………………………………….. 9,047

Cash ……………………………………………………………….. 9,047

d. Stock Investments …………………………………………………….. 9,000

Cash ……………………………………………………………….. 9,000

69. Alistair Corporation sells 500 shares of common stock being held as a short-term

investment. The shares were acquired six months ago at a cost of $55 a share. Alistair

sold the shares for $40 a share. The entry to record the sale is

a. Cash ……………………………………………………………………….. 20,000

Loss on Sale of Stock Investments ………………………………. 7,500

Stock Investments ……………………………………………… 27,500

b. Cash ……………………………………………………………………….. 27,500

Gain on Sale of Stock Investments ………………………. 7,500

Stock Investments ……………………………………………… 20,000

c. Cash ……………………………………………………………………….. 20,000

Stock Investments ……………………………………………… 20,000

d. Stock Investments …………………………………………………….. 20,000

Loss on Sale of Stock Investments ………………………………. 7,500

Cash ……………………………………………………………….. 27,000

70. For accounting purposes, the method used to account for long-term investments in

common stock is determined by

a. the amount paid for the stock by the investor.

b. the extent of an investor’s influence on the operating and financial affairs of the

investee.

c. whether the stock has paid dividends in past years.

d. whether the acquisition of the stock by the investor was “friendly” or “hostile.”

71. If an investor owns less than 20% of the common stock of another corporation as a long–

term investment,

a. the equity method of accounting for the investment should be employed.

b. no dividends can be expected.

c. it is presumed that the investor has relatively little influence on the investee.

d. it is presumed that the investor has significant influence on the investee.

Test Bank for Financial Accounting, Ninth Edition

12 – 16

72. If the cost method is used to account for a long-term investment in common stock,

dividends received should be

a. credited to the Stock Investments account.

b. credited to the Dividend Revenue account.

c. debited to the Stock Investments account.

d. recorded only when 20% or more of the stock is owned.

73. If 10% of the common stock of an investee company is purchased as a long-term

investment, the appropriate method of accounting for the investment is

a. the cost method.

b. the equity method.

c. the preparation of consolidated financial statements.

d. determined by agreement with whomever owns the remaining 90% of the stock.

74. The cost method of accounting for long-term investments in stock should be employed

when the

a. investor owns more than 50% of the investee’s stock.

b. investor has significant influence on the investee and the stock held by the investor

are marketable equity securities.

c. market value of the shares held is greater than their historical cost.

d. investor’s influence on the investee is insignificant.

75. When an investor owns between 20% and 50% of the common stock of a corporation, it is

generally presumed that the investor

a. has insignificant influence on the investee and that the cost method should be used to

account for the investment.

b. should apply the cost method in accounting for the investment.

c. will prepare consolidated financial statements.

d. has significant influence on the investee and that the equity method should be used to

account for the investment.

76. Under the equity method of accounting for long-term investments in common stock, when

a dividend is received from the investee company,

a. the Dividend Revenue account is credited.

b. the Stock Investments account is increased.

c. the Stock Investments account is decreased.

d. no entry is necessary.

Investments

12 – 17

77. On January 1, 2014, Lark Corporation purchased 35% of the common stock outstanding

of Dinc Corporation for $700,000. During 2014, Dinc Corporation reported net income of

$200,000 and paid cash dividends of $100,000. The balance of the Stock Investments—

Dinc account on the books of Lark Corporation at December 31, 2014 is

a. $700,000.

b. $735,000.

c. $770,000.

d. $665,000.

78. Under the equity method, the Stock Investments account is increased when the

a. investee company reports net income.

b. investee company pays a dividend.

c. investee company reports a loss.

d. stock investment is sold at a gain.

79. The account, Stock Investments, is

a. a subsidiary ledger account.

b. a long-term liability account.

c. a long-term investment account.

d. another name for Debt Investments.

80. Which of the following would not be considered a motive for making a stock investment in

another corporation?

a. Appreciation in the market value of the stock investment

b. Use of the investment for expanding its own operations

c. Use of the investment to diversify its own operations

d. An increase in the amount of interest revenue from the stock investment

81. Revenue is recognized when cash dividends are received under

a. the controlling interest method.

b. the cost method.

c. the equity method.

d. both the cost and equity methods.

82. Which of the following is the correct matching concerning an investor’s influence on the

operations and financial affairs of an investee?

% of Investor Ownership Presumed Influence

a. Less than 20% Short-term

b. Between 20%-50% Significant

c. More than 50% Long-term

d. Between 20%-50% Controlling

Test Bank for Financial Accounting, Ninth Edition

12 – 18

83. Which of the following is the correct matching concerning the appropriate accounting for

long-term stock investments?

% of Investor Ownership Accounting Guidelines

a. Less than 20% Cost method

b. Between 20%–50% Cost method

c. More than 50% Cost or equity method

d. Between 20%–50% Consolidated financial statements

84. If the cost method is used to account for a long-term investment in common stock,

a. it is presumed that the investor has significant influence on the investee.

b. the earning of net income by the investee is considered a proper basis for recognition

of income by the investor.

c. net income of the investee is not considered earned by the investor until dividends are

declared by the investee.

d. the Investment account may be, at times, greater than the acquisition cost.

85. If a company acquires a 40% common stock interest in another company,

a. the equity method is usually applicable.

b. all influence is classified as controlling.

c. the cost method is usually applicable.

d. the ability to exert significant influence over the activities of the investee does not

exist.

86. If a common stock investment is sold at a gain, the gain

a. is reported as operating revenue.

b. is reported under a special section, “Discontinued investments,” on the income

statement.

c. is reported in the Other revenues and gains section of the income statement.

d. contributes to gross profit on the income statement.

87. If the equity method is being used, cash dividends received

a. are credited to Dividend Revenue.

b. require no entry because investee net income has already been recorded at the

proper proportion on the investor’s books.

c. are credited to the Stock Investments account.

d. are credited to the Revenue from Stock Investments account.

88. If the equity method is being used, the Revenue from Stock Investments account is

a. just another name for a Dividend Revenue account.

b. credited when dividends are declared by the investee.

c. credited when net income is reported by the investee.

d. debited when dividends are declared by the investee.

Investments

FOR INSTRUCTOR USE ONLY

12 – 19

89. Under the equity method, the Stock Investments account is credited when the

a. investee reports net income.

b. investee reports a net loss.

c. investment is originally acquired.

d. investee reports net income and when the investment is originally acquired.

90. On August 1, Masters Company buys 2,000 shares of ABD common stock for $72,500

cash. On December 1, the stock investments are sold for $75,000 in cash. Which of the

following are the correct journal entries to record for the purchase and sale of the common

stock?

a. Aug. 1 Cash …………………………………………….. 72,500

Stock Investments …………………….. 72,500

Dec. 1 Cash …………………………………………….. 75,000

Stock Investments …………………….. 72,500

Gain on Sale of Stock Investments 2,500

b. Aug. 1 Stock Investments ………………………….. 72,500

Cash ……………………………………….. 72,500

Dec. 1 Cash …………………………………………….. 75,000

Stock Investments …………………….. 72,500

Gain on Sale of Stock Investments 2,500

c. Aug. 1 Stock Investments ………………………….. 72,500

Cash ……………………………………….. 72,500

Dec. 1 Stock Investments ………………………….. 75,000

Cash ……………………………………….. 72,500

Gain on Sale of Stock Investments 2,500

d. Aug. 1 Cash …………………………………………….. 72,500

Stock Investments …………………….. 72,500

Dec. 1 Stock Investments ………………………….. 75,000

Cash ……………………………………….. 72,500

Gain on Sale of Stock Investments 2,500

91. Cody Industries owns 35% of Macarthy Company. For the current year, Macarthy reports

net income of $250,000 and declares and pays a $60,000 cash dividend. Which of the

following correctly presents the journal entries to record Cody’s equity in Macarthy’s net

income and the receipt of dividends from Macarthy?

a. Dec. 31 Stock Investments ……………………………. 87,500

Revenue from Stock Investments …. 87,500

Dec. 31 Cash ……………………………………………… 21,000

Stock Investments ………………………. 21,000

b. Dec. 31 Stock Investments …………………………….. 87,500

Revenue from Stock Investments …. 87,500

Dec. 31 Cash ………………………………………………. 60,000

Stock Investments ……………………….. 60,000

c. Dec. 31 Stock Investments ………………………….. 66,500

Revenue from Stock Investments … 66,500

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 20

MC 91. (cont.)

d. Dec. 31 Revenue from Stock Investments ………. 87,500

Stock Investments ……………………… 87,500

Dec. 31 Stock Investments …………………………... 21,000

Cash ………………………………………… 21,000

92. On January 1, 2014, Gene Corp. paid $800,000 for 100,000 shares of Onofine Company’s

common stock, which represents 30% of Onofines outstanding common stock. Onofine

reported net income of $200,000 and paid cash dividends of $60,000 during 2014. Gene

should report the investment in Onofine Company on its December 31, 2014, balance

sheet at:

a. $800,000

b. $758,000

c. $818,000

d. $842,000

93. Viejo Inc. earns $600,000 and pays cash dividends of $150,000 during 2014. Cruz

Corporation owns 73,500 of the 210,000 outstanding shares of Viejo.

What amount should Cruz show in the investment account at December 31, 2014 if the

beginning of the year balance in the account was $40,000?

a. $197,500

b. $210,000

c. $157,500

d. $250,000

94. Cruz Inc. earns $450,000 and pays cash dividends of $150,000 during 2014. Cruz

Corporation owns 73,500 of the 210,000 outstanding shares of Viejo.

How much revenue from investment should Viejo report in 2014?

a. $52,500

b. $105,000

c. $157,500

d. $210,000

95. On January 1, 2014, Dumas Industries acquired a 18% interest in Arlongton Corporation

through the purchase of 12,000 shares of Arlongton Corporation common stock for

$250,000. During 2014, Arlongton Corp. paid $60,000 in dividends and reported a net loss

of $90,000. Dumas is able to exert significant influence on Arlongton. However, Dumas

mistakenly records these transactions using the cost method rather than the equity

method of accounting. Which of the following would show the correct presentation for

Dumas’s investment using the equity method?

Investments

12 – 21

MC 95. (cont.)

Investment Net

Account Earnings (loss)

a. $90,000 ($30,000)

b. $223,000 ($16,200)

c. $233,800 ($16,200)

d. $233,800 ($5,400)

96. Consolidated financial statements are prepared when a company owns _________ of the

common stock of another company.

a. less than 20%

b. between 20% and 50%

c. less than 50%

d. more than 50%

97. Consolidated financial statements present all of the following except the

a. individual assets and liabilities of the parent company

b. individual assets and liabilities of the subsidiary.

c. total revenues and expenses of the subsidiary.

d. All of these are presented in consolidated financial statements.

98. The company whose stock is owned by the parent company is called the

a. controlled company.

b. subsidiary company.

c. investee company.

d. sibling company.

99. A company that owns more than 50% of the common stock of another company is known

as the

a. charge company.

b. subsidiary company.

c. parent company.

d. management company.

100. If one company owns more than 50% of the common stock of another company,

a. the cost method should be used to account for the investment.

b. a partnership exists.

c. a parent-subsidiary relationship exists.

d. the company whose stock is owned must be liquidated.

Test Bank for Financial Accounting, Ninth Edition

12 – 22

101. If a parent company has two wholly owned subsidiaries, how many legal and economic

entities are there from the viewpoint of the shareholders of the parent company?

Legal Economic

a. 3 3

b. 1 2

c. 3 1

d. 2 1

102. When a company owns more than 50% of the common stock of another company,

a. affiliated financial statements are prepared.

b. consolidated financial statements are prepared.

c. controlling financial statements are prepared.

d. significant financial statements are prepared.

103. Changes from cost are reported as part of net income for

a. available-for-sale securities.

b. held-to-maturity securities.

c. debt securities.

d. trading securities.

104. Short-term investments are listed on the balance sheet immediately below

a. cash.

b. inventory.

c. accounts receivable.

d. prepaid expenses.

105. Short-term stock investments should be valued on the balance sheet at

a. the lower of cost or fair value.

b. the higher of cost or fair value.

c. cost.

d. fair value.

106. In recognizing a decline in the fair value of short-term stock investments, an unrealized

loss account is debited because

a. management intends to realize this loss in the near future.

b. the securities have not been sold.

c. the stock market is volatile.

d. management cannot determine the exact amount of the loss in value.

107. The Fair Value Adjustment account

a. is set up for each security in the company’s portfolio.

b. relates to the entire portfolio of securities held by the company.

c. is closed at the end of each accounting period.

d. appears on the income statement as Other Expenses and Losses.

Investments

12 – 23

108. The contra-account, Fair Value Adjustment, is also called a(n)

a. offset account.

b. adjustment account.

c. valuation account.

d. opposite account.

109. Reporting investments at fair value is

a. applicable to stock securities only.

b. applicable to debt securities only.

c. applicable to both debt and stock securities.

d. a conservative approach because only losses are recognized.

110. Brandy Corporation’s trading portfolio at the end of the year is as follows:

Security Cost Fair Value

Common Stock C $10,000 $12,000

Common Stock D 9,000 5,000

$19,000 $17,000

At the end of the year, Brandy Corporation should

a. set up a Fair Value Adjustment account for Stock D.

b. set up a Fair Value Adjustment account for the portfolio.

c. recognize an Unrealized Gain or Loss—Income for $4,000.

d. report a loss on the income statement for $4,000 under “Other expenses and losses.”

111. Brandy Corporation’s trading portfolio at the end of the year is as follows:

Security Cost Fair Value

Common Stock C $10,000 $12,000

Common Stock D 8,000 5,000

$18,000 $17,000

Brandy subsequently sells Stock D for $10,000. What entry is made to record the sale?

a. Cash …………………………..…………………………………………… 10,000

Stock Investments ……………………………………………… 10,000

b. Cash …………………………..…………………………………………… 10,000

Fair Value Adjustment Trading …………………………….. 2,000

Stock Investments ……………………………………………… 8,000

c. Cash ……………………………………………………………………….. 10,000

Stock Investments ……………………………………………… 8,000

Gain on Sale of Stock Investments ………………………. 2,000

d. Cash …………………………..…………………………………………… 10,000

Stock Investments ……………………………………………… 5,000

Gain on Sale of Stock Investments ………………………. 5,000

Test Bank for Financial Accounting, Ninth Edition

12 – 24

112. Which of the following would not be reported under “Other Revenues and Gains” on the

income statement?

a. Unrealized gain on available-for-sale securities

b. Dividend revenue

c. Interest revenue

d. Gain on sale of short-term debt investments

113. The balance in the Unrealized Gain or Loss—Equity account will

a. appear on the balance sheet as a contra asset.

b. appear on the income statement under Other Expenses and Losses.

c. appear as a deduction in the stockholders’ equity section.

d. not be shown on the financial statements until the securities are sold.

114. If the cost of an available-for-sale security exceeds its fair value by $40,000, the entry to

recognize the loss

a. is not required since the share prices will likely rebound in the long run.

b. will show a debit to an expense account.

c. will show a credit to a contra-asset account that appears in the stockholders’ equity

section of the balance sheet.

d. will show a debit to an unrealized loss account that is deducted in the stockholders’

equity section of the balance sheet.

115. The balance sheet presentation of an unrealized loss on an available-for-sale security is

similar to the statement presentation of

a. treasury stock.

b. discount on bonds payable.

c. allowance for doubtful accounts.

d. prepaid expenses.

116. At the end of its first year, the trading securities portfolio consisted of the following

common stocks.

Cost Fair Value

Atrium Corporation $ 46,500 $ 50,000

Barnes Inc. 60,000 58,000

Cantor Corporation 80,000 76,400

$186,500 $184,400

The unrealized loss to be recognized under the fair value method is

a. $2,000.

b. $5,600.

c. $2,100.

d. $3,600.

Investments

FOR INSTRUCTOR USE ONLY

12 – 25

117. At the end of its first year, the trading securities portfolio consisted of the following

common stocks.

Cost Fair Value

Atrium Corporation $ 46,500 $ 50,000

Barnes Inc. 60,000 58,000

Cantor Corporation 80,000 76,400

$186,500 $184,400

In the following year, the Barnes common stock is sold for cash proceeds of $57,000. The

gain or loss to be recognized on the sale is a

a. gain of $1,200.

b. loss of $3,000.

c. Loss of $1,000.

d. loss of $2,000.

118. At the end of the first year of operations, the total cost of the trading securities portfolio is

$245,000. Total fair value is $250,000. The financial statements should show

a. an addition to an asset of $5,000 and a realized gain of $5,000.

b. an addition to an asset of $5,000 and an unrealized gain of $5,000 in the stockholders’

equity section.

c. an addition to an asset of $5,000 in the current assets section and an unrealized gain

of $5,000 in “Other revenues and gains.”

d. an addition to an asset of $5,000 in the current assets section and a realized gain of

$5,000 in “Other revenues and gains.”

119. Comanic Corp. has common stock of $5,400,000, retained earnings of $2,000,000,

unrealized gains on trading securities of $100,000 and unrealized losses on available-for-

sale securities of $200,000. What is the total amount of its stockholders’ equity?

a. $7,200,000

b. $7,400,000

c. $7,300,000

d. $7,500,000

120. Cost and fair value data for the trading securities of McMahon Company at December 31,

2014, are $110,000 and $85,000, respectively. Which of the following correctly presents

the adjusting journal entry to record the securities at fair value?

a. Dec. 31 Unrealized Loss⎯Income ……………… 25,000

Trading Securities ……………………. 25,000

b. Dec. 31 Unrealized Gain⎯Income ………………. 25,000

Trading Securities …………………….. 25,000

c. Dec. 31 Unrealized Loss⎯Income ………………. 25,000

Fair Value Adjustment⎯Trading …. 25,000

Test Bank for Financial Accounting, Ninth Edition

12 – 26

MC 120. (cont.)

d. Dec. 31 Fair Value Adjustment -Trading 25,000

Unrealized Gain-Income ……………. 25,000

121. At December 31, 2014, the trading securities for Saddle, Inc. are as follows:

Security Cost Fair Value 12/31/14

A $90,000 $94,000

B 150,000 141,000

C 32,000 30,000

Saddle should report the following amount related to the securities in its 2014 income

statement:

a. $4,000 gain

b. $7,000 realized loss.

c. $7,000 unrealized loss.

d. $11,000 unrealized loss.

122. At December 31, 2014, Delta Inc. has these data on its security investments:

Security Cost Fair Value 12/31/14

Trading $ 140,000 $190,000

Available-for-sale 137,000 122,000

If the available-for-sale securities are held as long-term investments, which of the

following will be recorded to adjust the securities to fair value?

a. Securities ………………………………………………. 35,000

Unrealized Gain⎯Income …………………… 35,000

b. Unrealized Loss⎯Income …………………………. 15,000

Securities ……………………………………………….. 35,000

Unrealized Gain⎯Income …………………… 50,000

c. Fair Value Adjustment⎯Trading ………………… 50,000

Unrealized Gain⎯Income …………………… 50,000

Unrealized Gain or Loss⎯Equity ………………… 15,000

Fair Value Adjustment⎯Available-for-Sale 15,000

d. Unrealized Gain⎯Income …………………………. 50,000

Fair Value Adjustment⎯Trading ………….. 50,000

Fair Value Adjustment⎯Available-for-Sale ……. 15,000

Unrealized Gain or Loss⎯Equity ………….. 15,000

Investments

12 – 27

123. All of the following statements about short-term investments are true except:

a. Short-term investments are also called marketable securities

b. Trading securities are always classified as short-term investments.

c. Short-term investments are listed below accounts receivable in the current asset

section of the balance sheet.

d. Short-term assets must be readily marketable.

124. Available-for-sale securities are classified as

a. short-term investments only.

b. long-term investments only.

c. either short-term or long-term investments.

d. current assets only.

125. Which one of the following would not be classified as a short-term investment?

a. Marketable stock securities

b. Equity method investments

c. Marketable debt securities

d. Short-term paper

126. Short-term investments are securities that are readily marketable and intended to be

converted into cash within the next

a. year.

b. two years.

c. year or operating cycle, whichever is shorter.

d. year or operating cycle, whichever is longer.

127. Which of the following would not be classified as a short-term investment?

a. Short-term commercial paper

b. Idle cash in a bank checking account

c. Marketable stock securities

d. Marketable debt securities

128. If a parent company acquires wholly owned subsidiary at an amount greater than the book

value, the excess should be

a. allocated to expense on the date of acquisition.

b. allocated to identifiable assets to the extent of their fair values, with any remainder

allocated to goodwill.

c. allocated to goodwill, with any remainder allocated to the identifiable assets.

d. set up as a liability to the controlling interest.

Test Bank for Financial Accounting, Ninth Edition

12 – 28

129. The consolidated worksheet shows Excess of Cost Over Book Value of Subsidiary of

$210,000. Management of the parent company determines that the market values for

subsidiary company plant assets are $90,000 higher than book values. In the consolidated

balance sheet, goodwill will be reported at

a. $210,000.

b. $120,000.

c. $90,000.

d. $0.

130. Daniel Corporation acquired 100% of the common stock of Tysen Company for

$1,100,000. On the date of acquisition, Tysen Company’s stockholders’ equity consisted

of: Common Stock, $530,000; Retained Earnings, $410,000. The intercompany

elimination to be made on a worksheet to prepare a consolidated balance sheet is

a. Common Stock–Tysen ………………………………………….. 530,000

Retained Earnings–Tysen ……………………………………… 410,000

Investment in Tysen Stock ……………………………….. 940,000

b. Investment in Tysen Stock …………………………………….. 1,100,000

Cash …………………………………………………………….. 1,100,000

c. Common Stock–Daniel …………………………………………. 530,000

Retained Earnings–Daniel …………………………………….. 410,000

Goodwill …………………………..…………………………………. 160,000

Investment in Tysen Stock ……………………………….. 1,100,000

d. Common Stock–Tysen ………………………………………….. 530,000

Retained Earnings–Tysen ……………………………………… 410,000

Excess of Cost Over Book Value of Subsidiary …………. 160,000

Investment in Tysen Stock ……………………………….. 1,100,000

131. A consolidated income statement will show

a. revenue and expense transactions between the consolidated entity and parties

outside the affiliated group.

b. only the parent company’s net income.

c. only the income of partially owned subsidiaries.

d. only the income of wholly owned subsidiaries.

132. When preparing a consolidated income statement,

a. only the revenues and expenses of the parent company are presented.

b. the income from partially owned subsidiaries is excluded.

c. all revenue and expense transactions between the parent and subsidiaries must be

eliminated.

d. intercompany transactions between affiliated companies do not have to be eliminated.

Investments

12 – 29

133. Which of the following reasons best explains why a company that experiences seasonal

fluctuations in sales may purchase investments in debt or stock securities?

a. The company may have excess cash.

b. The company may generate a significant portion of its earnings from investment

income.

c. The company may invest for the strategic reason of establishing a presence in a

related industry.

d. The company may invest for speculative reasons to increase the value in pension

funds.

134. When bonds are sold, the gain or loss on sale is the difference between the

a. sales price and the cost of the bonds.

b. net proceeds and the cost of the bonds.

c. sales price and the market value of the bonds.

d. net proceeds and the market value of the bonds.

135. Debt investments are recorded at the

a. face value of the bonds purchased.

b. face value of the bonds purchased plus interest.

c. price paid for the bonds plus interest.

d. price paid for the bonds plus brokerage fees.

136. Under the equity method, the investor records dividends received by crediting

a. Dividend Revenue.

b. Investment Income.

c. Revenue from Investment.

d. Stock Investments.

137. A company that acquires less than 20% ownership interest in another company should

account for the stock investment in that company using

a. the cost method.

b. the equity method.

c. the significant method.

d. consolidated financial statements.

138. The equity method of accounting for an investment in the common stock of another

company should be used by the investor when the investment

a. is composed of common stock and it is the investor’s intent to vote the common stock.

b. ensures a source of supply of raw materials for the investor.

c. enables the investor to exercise significant influence over the investee.

d. is obtained by an exchange of stock for stock.

Test Bank for Financial Accounting, Ninth Edition

12 – 30

139. On January 2, Angle Corporation acquired 40% of the outstanding common stock of

Bobbe Company for $550,000. For the year ended December 31, Bobbe reported net

income of $90,000 and paid cash dividends of $30,000 on its common stock. At

December 31, the carrying value of Angle’s investment in Bobbe under the equity method

is

a. $538,000.

b. $550,000.

c. $586,000.

d. $574,000.

140. An unrealized loss on available-for-sale securities is

a. reported under Other Expenses and Losses in the income statement.

b. closed-out at the end of the accounting period.

c. reported as a separate component of stockholders’ equity.

d. deducted from the cost of the investment.

141. Securities bought and held primarily for sale in the near term to generate income on short-

term price differences are

a. trading securities.

b. available-for-sale securities.

c. never-sell securities.

d. held-to-maturity securities.

142. Short-term investments are

a. (1) readily marketable and (2) intended to be converted into cash after the current year

or operating cycle, whichever is shorter.

b. (1) readily marketable and (2) intended to be converted into cash within the current

year or operating cycle, whichever is longer.

c. (1) readily marketable and (2) intended to be converted into cash after the current year

or operating cycle, whichever is longer.

d. (1) readily marketable and (2) intended to be converted into cash within the current

year or operating cycle, whichever is shorter.

143. Short-term investments are securities held by a company that are

a. readily marketable.

b. intended to be converted into cash within the next year.

c. readily marketable and intended to be converted into cash within the next year or

operating cycle, whichever is longer.

d. readily marketable and intended to be held until maturity.

Investments

12 – 31

144. Debt investments that are held to maturity are recorded at

a. amortized cost.

b. fair value.

c. original cost.

d. maturity value.

145. Under IFRS, equity investments are generally recorded and reported at

a. amortized cost.

b. fair value.

c. original cost.

d. maturity value.

146. Which of the following investment classifications are the same for GAAP and IFRS?

a. Available-for-sale

b. Held-to-maturity

c. Non-trading

d. Trading.

147. Which of the following are accounted for at amortized cost under IFRS?

a. Available-for-sale investments

b. Trading investments

c. Non-trading equity investments

d. Held-for-collection investments

148. Unrealized gains and losses related to available-for-sale/non-trading equity investments

are reported in other comprehensive income under

a. GAAP only.

b. IFRS only.

c. Both GAAP and IFRS.

d. Neither GAAP or IFRS.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 32

Answers to Multiple Choice Questions

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

BRIEF EXERCISES

BE 149

On January 14, Balcom Corporation purchased 20, 11%, $1,000 Eiger Company bonds for

$20,000. On November 30, the company sold 10 of the Eiger Company bonds for $11,600.

Prepare journal entries for the purchase and sale of the Eiger Company bonds.

BE 150

On January 2, Penny Company purchased 45, 10%, $1,000 Mikel Company bonds for $45,000

cash. Interest is payable semiannually on July 1 and January 1. On July 1, the company received

a semiannual interest payment on the Mikel Company bonds. Journalize the entries to record the

purchase of the bonds and the receipt of the interest payment.

Investments

FOR INSTRUCTOR USE ONLY

12 – 33

BE 151

On April 25, Davis Company buys 4,200 shares of Carter common stock for $94,500. On October

31, Davis sells 600 shares of Carter stock for $16,500,. Prepare journal entries for the purchase

and sale of the Carter common stock.

BE 152

On January 1, Sanchez Corporation purchased a 35% equity in Lawton Company for $380,000.

At December 31, Lawton declared and paid a $40,000 cash dividend and reported net income of

$98,000. Prepare the necessary journal entries for Sanchez Corporation.

BE 153

Jenner Company had the following transactions pertaining to its short-term stock investments.

Jan. 1 Purchased 600 shares of Pork Company stock for $8,420.

June 1 Received cash dividends of $0.60 per share on the Pork Company stock.

Sept. 15 Sold 300 shares of the Pork Company stock for $3,400 Cash.

Instructions

Journalize the transactions.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 34

BE 154

On January 1, 2014, Mink Company purchased 5,000 shares of Kusher Company stock for

$360,000. Mink’s investment represents 30 percent of the total outstanding shares of Kusher.

During 2014, Kusher paid total dividends of $100,000 and reported net income of $300,000. What

revenue does Mink report related to this investment and what is the amount to be reported as an

investment in Kusher stock at December 31?

BE 155

At January 1, 2014, the trading securities portfolio held by the Darren Corporation consisted of

the following investments:

1. 2,000 shares of Temper common stock purchased for $42 per share.

2. 1,500 shares of Logan common stock purchased for $50 per share.

At December 31, 2014, the fair values per share were Temper $38 and Logan $54.

Instructions

(a) Prepare a schedule showing the cost and fair value of the portfolio at December 31, 2014.

(b) Prepare the adjusting entry to report the portfolio at fair value at December 31, 2014.

Investments

FOR INSTRUCTOR USE ONLY

12 – 35

BE 156

At December 31, 2014, the trading securities for Eddy Company are as follows:

Security Cost Fair Value

A $16,000 $20,000

B 34,000 32,000

$50,000 $52,000

Prepare the adjusting entry at December 31, 2014, to report the securities at fair value.

BE 157

At January 1, 2014, Grand Corporation held one available-for-sale security: 1,500 shares of

Nettle common stock purchased for $40 per share. At December 31, 2014, the fair value per

share for Nettle was $42. Prepare the adjusting entry to report the portfolio at fair value at

December 31, 2014.

BE 158

Terra Cotta Company has the following data at December 31, 2014 for its securities:

Securities Cost Fair Value

Available-for-sale $34,000 $39,000

Trading 46,000 42,000

Instructions

Journalize the December 31 adjusting entries.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 36

EXERCISES

Ex. 159

Maxim Corporation had the following transactions pertaining to debt investments.

Jan. 1 Purchased 80, 8%, $1,000 Woodrow Company bonds for $80,000.

July 1 Sold 20 Woodrow Company bonds for $21,500.

Instructions

Prepare journal entries for the purchase and sale of the Woodrow Company bonds.

Ex. 160

Quagle Company had the following transactions pertaining to debt securities held as a short-term

investment.

Jan. 1 Purchased 40, 8%, $1,000 Steve Company bonds for $40,000 cash. Interest is payable

semiannually on July 1 and January 1.

July 1 Received semiannual interest on Steve Company bonds.

Oct. 1 Sold 24 Steve Company bonds for $26,000 plus accrued interest.

Instructions

(a) Journalize the transactions.

(b) Prepare the adjusting entry for the accrual of interest on December 31.

Investments

FOR INSTRUCTOR USE ONLY

12 – 37

Ex. 161

Pincher Company purchased 50 Issac Company 12%, 10-year, $1,000 bonds on January 1,

2014, for $50,000. The bonds pay interest semiannually. On January 1, 2015, after receipt of

interest, Pincher Company sold 30 of the bonds for $28,300.

Instructions

Prepare the journal entries to record the transactions described above.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 38

Ex. 162

The following transactions were made by Allen Company. Assume all investments are short-term

and are readily marketable.

June 2 Purchased 400 shares of Snoop Corporation common stock for $45 per share.

July 1 Purchased 200 Barr Corporation bonds for $228,000.

30 Received a cash dividend of $1.50 per share from Snoop Corporation.

Sept. 15 Sold 120 shares of Snoop Corporation stock for $50 per share.

Dec. 31 Received semiannual interest check for $13,000 from Barr Corporation.

31 Received a cash dividend of $2 per share from Snoop Corporation.

Instructions

Journalize the transactions.

Investments

FOR INSTRUCTOR USE ONLY

12 – 39

Ex. 163

On April 1, Sign Company buys 4,000 shares of Polk common stock for $61,500. On October 1,

Sign sells 1,000 shares of Polk stock for $20,500..

Instructions

Prepare journal entries for the purchase and sale of the Polk common stock.

Ex. 164

Hungh Company had the following transactions pertaining to short-term investments in equity

securities.

Jan. 1 Purchased 1,500 shares of Antuni Company stock for $9,500 cash.

June 1 Received cash dividends of $.40 per share on Antuni Company stock.

Sept. 15 Sold 375 shares of Antuni Company stock for $2,300 less brokerage fees of $100.

Dec. 1 Received cash dividends of $.80 per share on Antuni Company stock.

Instructions

(a) Journalize the transactions.

(b) Indicate the income statement effects of the transactions.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 40

Ex. 165

Stewart Corporation’s balance sheet at December 31, 2013, showed the following:

Short-term investments, at fair value $46,500

Stewart Corporation’s trading portfolio of stock investments consisted of the following at

December 31, 2013:

Stock Number of Shares Cost

Conn Common Stock 200 $28,000

Ares Preferred Stock 400 6,000

Hall Common Stock 300 9,000

$43,000

During 2014, the following transactions took place:

Feb. 5 Sold 100 shares of Conn common stock for $18,000.

Mar. 30 Purchased 25 shares of Hall common stock for $1,000.

Sept. 9 Purchased 50 shares of Hall common stock for $3,000.

At year end on December 31, 2014, the fair values per share were:

Fair Value Per Share

Conn Common Stock $158.00

Ares Preferred Stock $14.00

Hall Common Stock $24.00

Instructions

(a) Prepare the journal entries to record the 2014 stock transactions.

(b) On December 31, 2014, prepare any adjusting entry that might be necessary relative to the

trading portfolio.

(c) Show how the stock investments will appear on Stewart Corporation’s balance sheet at

December 31, 2014.

Investments

FOR INSTRUCTOR USE ONLY

12 – 41

Ex. 166

On January 5, 2014, Grouse Company purchased the following stock securities as a long-term

investment:

300 shares Bonter Corporation common stock for $4,500.

500 shares Wane Corporation common stock for $10,000.

800 shares Strauss Corporation common stock for $22,800.

Assume that Grouse Company cannot exercise significant influence over the activities of the

investee companies and that the cost method is used to account for the investments.

On June 30, 2014, Grouse Company received the following cash dividends:

Bonter Corporation ……………………………….. $2.00 per share

Wane Corporation ………………………………… $1.25 per share

Strauss Corporation ………………………………. $1.50 per share

On November 15, 2014, Grouse Company sold 160 shares of Strauss Corporation common stock

for $7,200.

On December 31, 2014, the fair value of the securities held by Grouse Company is as follows:

Per Share

Bonter Corporation common stock $10

Wane Corporation common stock 16

Strauss Corporation common stock 28

Instructions

Prepare the appropriate journal entries that Grouse Company should make on the following

dates:

January 5, 2014

June 30, 2014

November 15, 2014

December 31, 2014

Test Bank for Financial Accounting, Ninth Edition

12 – 42

Ex. 167

Rosco Company purchased 35,000 shares of common stock of Paxton Corporation as a long-

term investment for $900,000. During the year, Paxton Corporation reported net income of

$300,000 and paid dividends of $100,000.

Instructions

(a) Assuming that the 35,000 shares represent a 10% interest in Paxton Corporation:

1. Prepare the journal entry to record the investment in Paxton stock.

2. Prepare any entries that Rosco Company should make in accounting for its investment

in Paxton stock during the year.

3. What is the balance of the Stock Investments account on Rosco Company’s books at

the end of the year?

(b) Repeat requirement (a) above except assume that the 35,000 shares represent a 20%

interest in Paxton Corporation.

Investments

FOR INSTRUCTOR USE ONLY

12 – 43

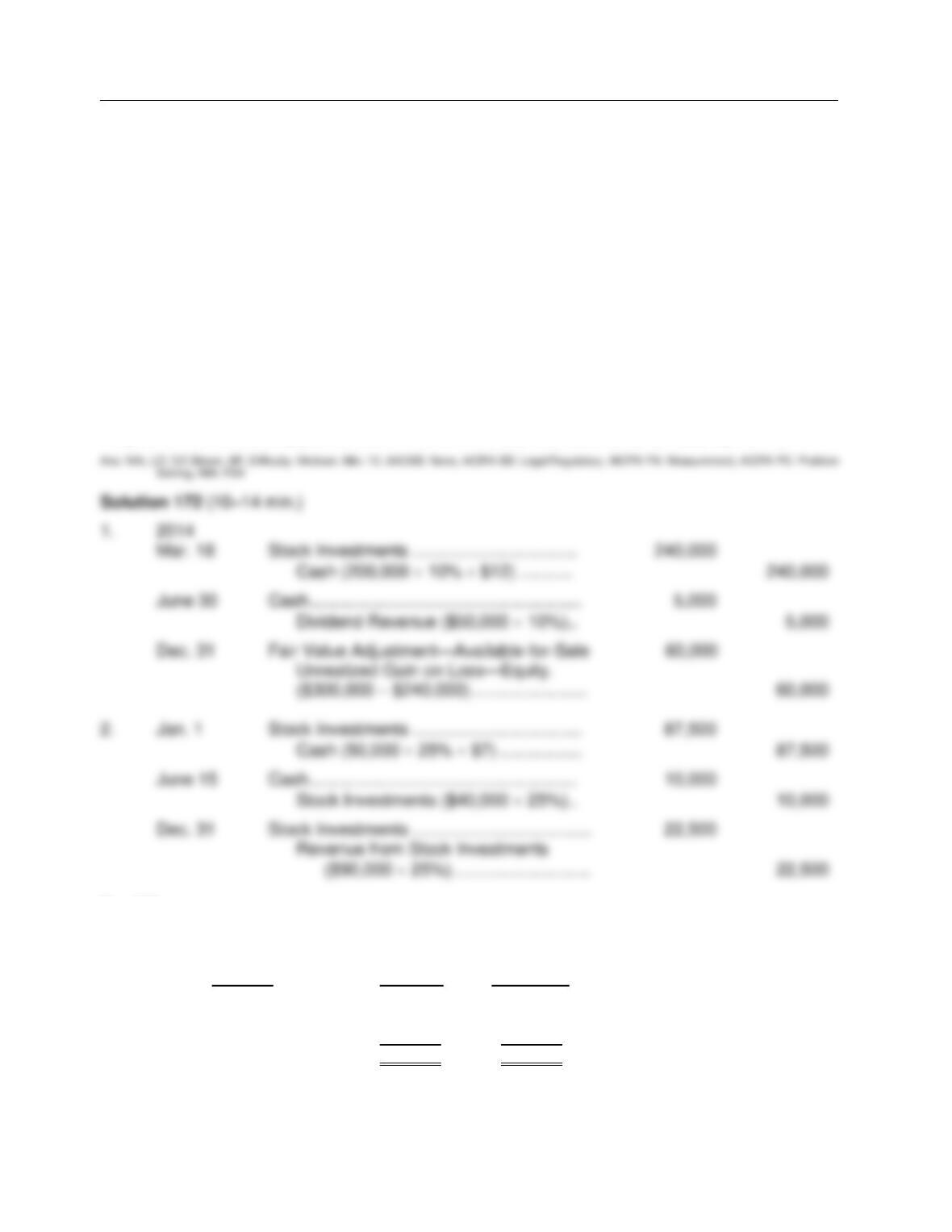

Solution 167 (16–21 min.)

Ex. 168

On January 1, Oetry Corporation purchased a 35% equity in Selig Company for $190,000. At

December 31, Selig declared and paid a $50,000 cash dividend and reported net income of

$80,000.

Instructions

Prepare the necessary journal entries for Oetry Corporation.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

12 – 44

Ex. 169

Information pertaining to long-term stock investments in 2014 by Bell Corporation follows:

Acquired 18% of the 250,000 shares of common stock of Kansas Company at a total cost of $8

per share on January 1, 2014. On July 1, Kansas Company declared and paid a cash dividend of