21) A perfectly competitive wheat farmer in a constant-cost industry produces 1,000 bushels of

wheat at a total cost of $50,000. The prevailing market price is $48. What will happen to the

market price of wheat in the long run?

A) The price remains constant at $48.

B) The price falls below $48.

C) The price rises above $48.

D) There is insufficient information to answer the question.

22) In August 2008, Ethan Nicholas developed the iShoot application for the apple iPhone 3G,

and within five months had earned $800,000 from this program. By May 2009, Nicholas had

dropped the price from $4.99 to $1.99 in an attempt to maintain sales. This example indicates

that in a competitive market,

A) earning an economic profit in the long run is extremely easy.

B) earning an economic profit in the long run is extremely difficult.

C) it is impossible to earn an economic profit in either the short run or the long run.

D) economic profits are only earned in the long run.

23) Apple introduced its iPhone 3G in July 2008 and within a month sales had topped 3 million

units. By April 2009, more than 25,000 apps for the iPhone 3G were available in the iTunes

store, an indication that in a competitive market

A) the ease at which a new firm can enter a competitive market is low.

B) the ease at which a new firm can enter a competitive market is high.

C) entry into the market is blocked.

D) entry into the market is restricted in the short run, but becomes easier in the long run.

24) Assume that the tuna fishing industry is perfectly competitive. Which of the following best

characterizes the industry if, as demand for tuna increases, fishing boats have to go farther into

the ocean to harvest tuna?

A) a constant-cost industry

B) an increasing-cost industry

C) a decreasing-cost industry

D) a fixed-cost industry

25) If in the long run a firm makes zero profit, it should exit the industry.

26) A perfectly competitive firm in a constant-cost industry produces 1,000 units of a good at a

total cost of $50,000. If the prevailing market price is $48, the number of firms and the

industry’s output will decrease in the long run.

27) Suppose there are economies of scale in the production of a specialized memory chip that is

used in manufacturing microwaves. This suggests that the microwave industry is a decreasing-

cost industry.

28) In an increasing-cost industry the long-run supply curve is upward sloping.

29) What is meant by the term “long-run competitive equilibrium?

30) What is a long-run supply curve? What does a long-run supply curve look like on a perfectly

competitive market graph?

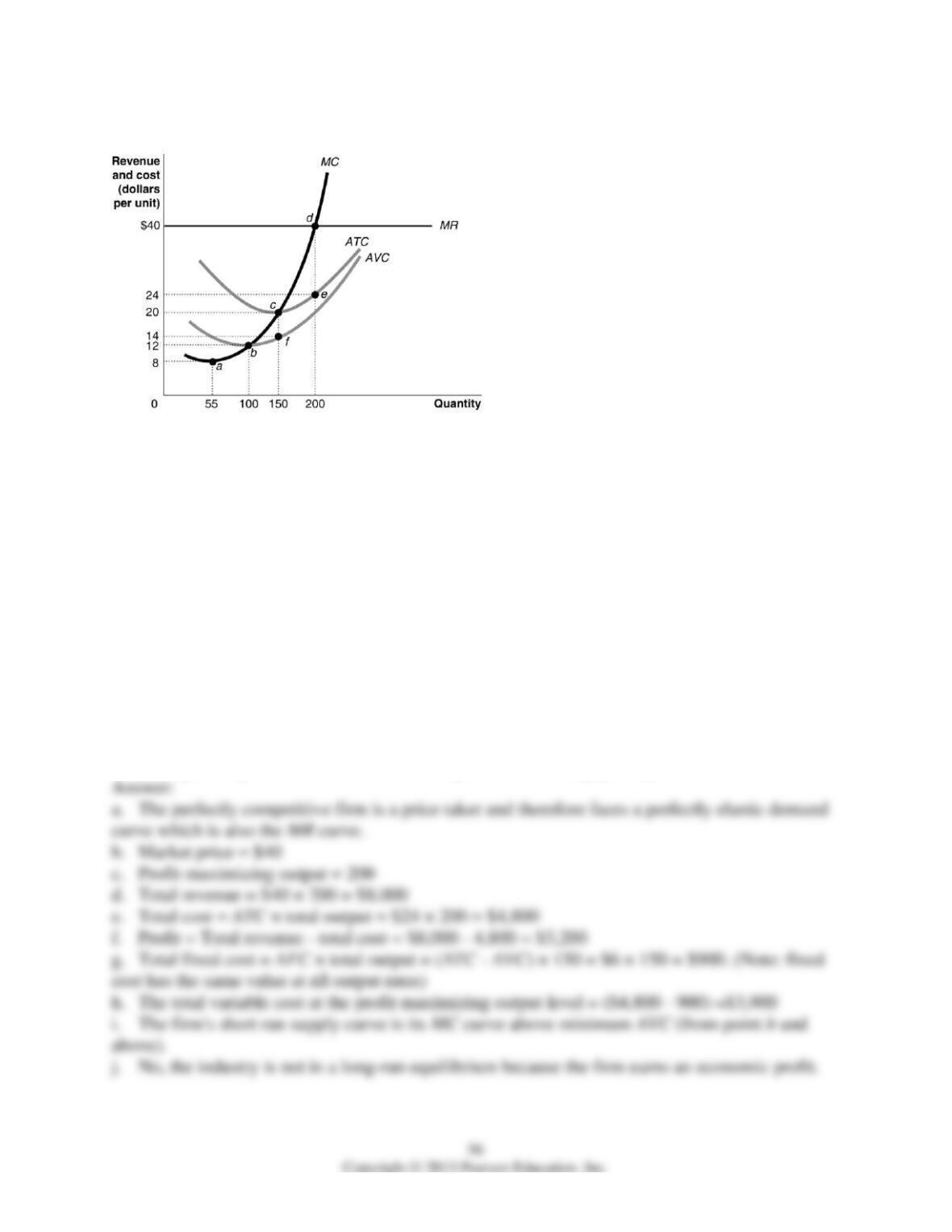

Figure 12-12

31) Use the figure above to answer the following questions.

a. How can you determine that the figure represents a graph of a perfectly competitive firm? Be

specific; indicate which curve gives you the information and how you use this information to

arrive at your conclusion.

b. What is the market price?

c. What is the profit-maximizing output?

d. What is total revenue at the profit-maximizing output?

e. What is the total cost at the profit-maximizing output?

f. What is the profit or loss at the profit-maximizing output?

g. What is the firm’s total fixed cost?

h. What is the total variable cost?

i. Identify the firm’s short-run supply curve.

j. Is the industry in a long-run equilibrium?

k. If it is not in long-run equilibrium, what will happen in this industry to restore long-run

equilibrium?

l. In long-run equilibrium, what is the firm’s profit maximizing quantity?

12.6 Perfect Competition and Efficiency

1) Which of the following describes a situation in which a good or service is produced at the

lowest possible cost?

A) productive efficiency

B) allocative efficiency

C) marginal efficiency

D) profit maximization

2) What is productive efficiency?

A) a situation in which resources are allocated to their highest profit use

B) a situation in which resources are allocated such that goods can be produced at their lowest

possible average cost

C) a situation in which resources are allocated such the last unit of output produced provides a

marginal benefit to consumers equal to the marginal cost of producing it

D) a situation in which firms produce as much as possible

3) The perfectly competitive market structure benefits consumers because

A) firms do not produce goods at the lowest possible price in the long run.

B) firms are forced by competitive pressure to be as efficient as possible.

C) firms add a much smaller markup over average cost than firms in any other type of market

structure.

D) firms produce high quality goods at low prices.

4) If the long-run average cost curve is U-shaped, the optimal scale of production from society’s

viewpoint is

A) the minimum efficient scale.

B) where maximum economic profit is earned by producers.

C) where firm profit is large enough to finance research and development.

D) one which guarantees economic profit.

5) Which of the following describes a situation in which every good or service is produced up to

the point where the last unit provides a marginal benefit to consumers equal to the marginal cost

of producing it?

A) productive efficiency

B) allocative efficiency

C) marginal efficiency

D) profit maximization

6) What is allocative efficiency?

A) It refers to a situation in which resources are allocated to their highest profit use.

B) It refers to a situation in which resources are allocated such that goods can be produced at

their lowest possible average cost.

C) It refers to a situation in which resources are allocated such that the last unit of output

produced provides a marginal benefit to consumers equal to the marginal cost of producing it.

D) It refers to a situation in which resources are allocated fairly to all consumers in a society.

7) A perfectly competitive industry achieves allocative efficiency because

A) goods and services are produced at the lowest possible cost.

B) goods and services are produced up to the point where the last unit provides a marginal

benefit to consumers equal to the marginal cost of producing it.

C) it produces where market price equals marginal production cost.

D) firms carry production surpluses.

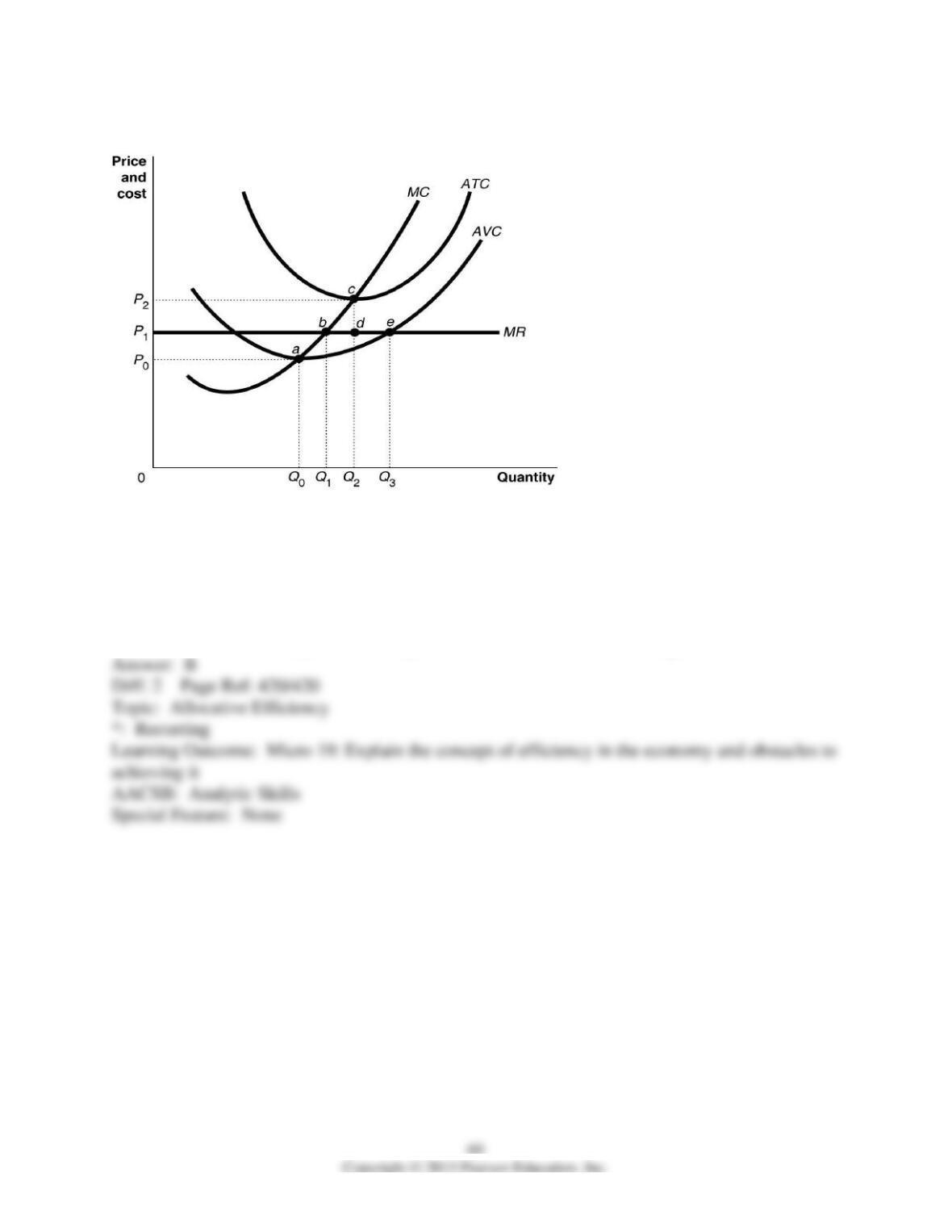

Figure 12-13

8) Refer to Figure 12-13. If the market price is P1, what is the allocatively efficient output

level?

A) Q0

B) Q1

C) Q2

D) There is no allocatively efficient output level because the firm is making a loss.

9) Assume that the LCD and plasma television sets industry is perfectly competitive. Suppose a

producer develops a successful innovation that enables it to lower its cost of production. What

happens in the short run and in the long run?

A) Initially, the firm will be able to increase its profit significantly, but in the long run its profits

will still be greater than zero but lower than its short run profits because other firms would also

innovate.

B) The firm will probably incur losses temporarily because of the high cost of the innovation, but

in the long run it will start earning positive profits.

C) This firm will be able to earn above normal profits indefinitely if it obtains a patent for its

innovation.

D) The firm will be able to increase its profits temporarily, but in the long run its profits will be

eliminated as other firms copy the innovation.

10) In early 2007, Pioneer and JVC, two Japanese electronics firms, each announced that their

profits were going to be lower than expected because they both had to cut prices for LCD and

plasma television sets. Which of the following could explain why these firms did not simply

raise their prices and increase their profits?

A) The move to cut prices is probably just a temporary one to gain market share. In the long run

the firms will raise prices and be able to increase their profits.

B) Most likely, intense competition between these two major producers probably pushed prices

down. Thereafter, each feared that it would lose its customers to the other if it raised its prices.

C) In perfect competition, prices are determined by the market and firms will keep lowering

prices until there are no profits to be earned.

D) The firms are still making profits, just not as high as expected so there is room to lower prices

until one can force the other out of business.

11) Writing in the New York Times on the technology boom of the late 1990s, Michael Lewis

argues, “The sad truth, for investors, seems to be that most of the benefits of new technologies

are passed right through to consumers free of charge.” What does Lewis means by the benefits of

new technology being “passed right through to consumers free of charge”?

A) Firms in perfect competition are price takers. Since they cannot influence price, they cannot

dictate who benefits from new technologies, even if the benefits of new technology are being

“passed right through to consumers free of charge.”

B) In perfect competition, price equals marginal cost of production. In this sense, consumers

receive the new technology “free of charge.”

C) In the long run, price equals the lowest possible average cost of production. In this sense,

consumers receive the new technology “free of charge.”

D) In perfect competition, consumers place a value on the good equal to its marginal cost of

production and since they are willing to pay the marginal valuation of the good, they are

essentially receiving the new technology “free of charge.”

12) Without government subsidization, the conversion of farmland in the United Kingdom from

conventional to organic production will generally cause a farmer’s

A) marginal cost and average total cost to decrease.

B) marginal cost and average total cost to increase.

C) average total cost to increase and marginal cost to decrease.

D) marginal cost to increase and average total cost to remain unchanged.

13) A decrease in demand for organic products will ________ a firm’s economic profit, and the

increase in costs to produce organic produce will ________ a firm’s economic profit.

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

14) If a firm in a perfectly competitive industry introduces a lower-cost way of producing an

existing product, the firm will be able to earn economic profits in the long run.

15) Firms in perfect competition produce the productively efficient output level in the short run

and in the long run.

16) Firms in perfect competition produce the allocatively efficient output in the short run and in

the long run.

17) What is meant by productive efficiency? How does a perfectly competitive firm achieve

productive efficiency?

18) Using two graphs, illustrate how a positive technological change in the market for notebook

computers could eliminate short-run economic profit for a firm in that market. On the first graph,

use a supply and demand graph to illustrate the positive technological change. On the second

graph, use demand, ATC, MC and MR curves to illustrate the elimination of economic profit

resulting from the positive technological change. Explain what is taking place in each graph.