26) Under what conditions should a competitive firm shut down in the short run?

27) Use a graph to show the demand, AVC, ATC, MC, and MR curves of a firm that should

temporarily shut down in the short run. Identify the shutdown point on the graph.

12.5 “If Everyone Can Do It, You Can’t Make Money at It”: The Entry and Exit of Firms in the

Long Run

1) Which of the following statements is correct?

A) Economic profit takes into account all costs involved in producing a product.

B) Accounting profit is not relevant in preparing the firm’s financial statement.

C) Economic profit always exceeds accounting profit.

D) Accounting profit is the same as economic profit.

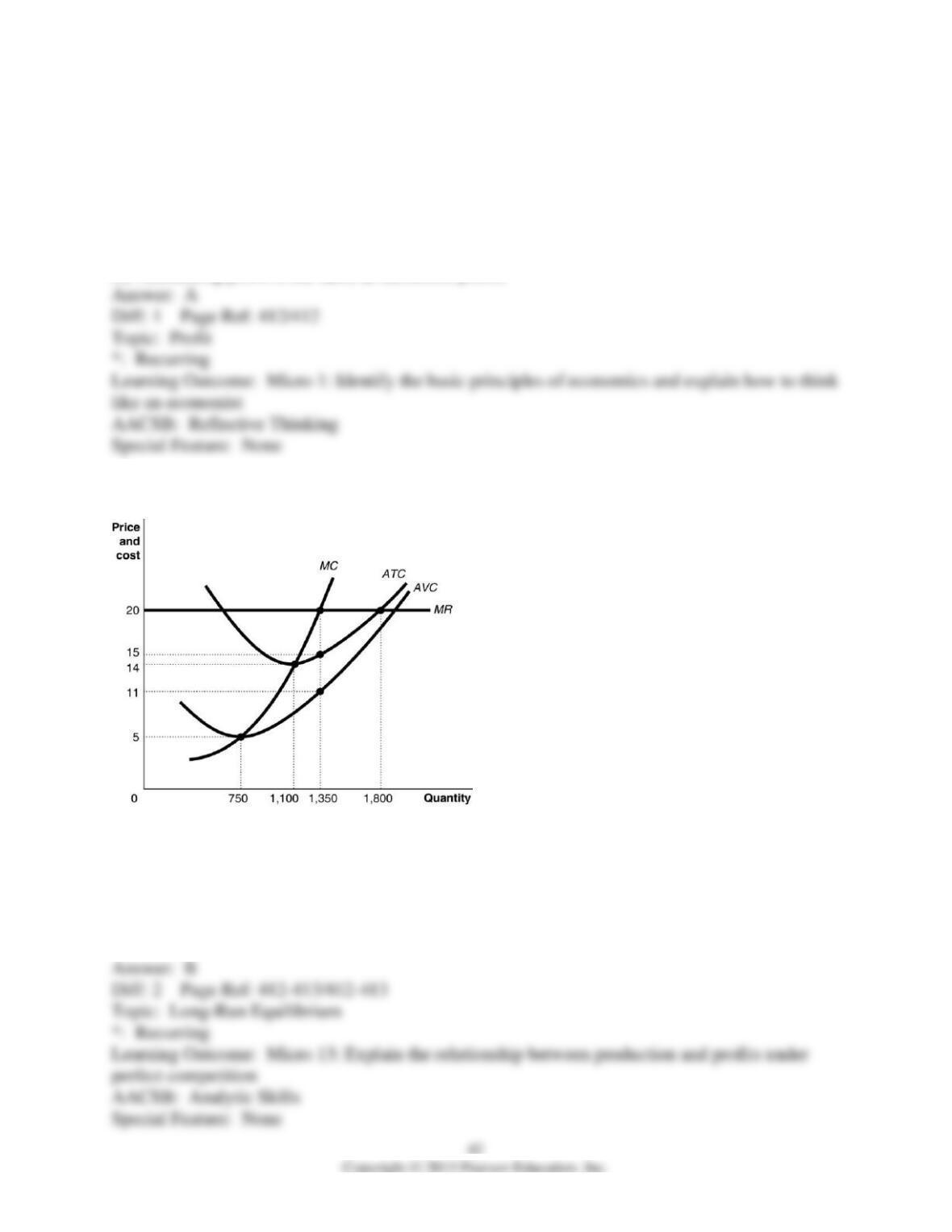

Figure 12-7

2) Refer to Figure 12-7. Suppose the prevailing price is $20 and the firm is currently producing

1,350 units. In the long-run equilibrium, the firm represented in the diagram

A) will continue to produce the same quantity.

B) will reduce its output to 1,100 units.

C) will reduce its output to 750 units.

D) will cease to exist.

3) Refer to Figure 12-7. Suppose the prevailing price is $20 and the firm is currently producing

1,350 units. In the long-run equilibrium,

A) there will be fewer firms in the industry and total industry output decreases.

B) there will be more firms in the industry and total industry output increases.

C) there will be fewer firms in the industry but total industry output increases.

D) there will be more firms in the industry and total industry output remains constant.

4) Refer to Figure 12-7. If this is a constant-cost industry, what is the market price in the long-

run equilibrium?

A) $5

B) $14

C) $15

D) $20

5) If a typical firm in a perfectly competitive industry is earning profits, then

A) all firms will continue to earn profits.

B) new firms will enter in the long run causing market supply to decrease, market price to rise

and profits to increase.

C) new firms will enter in the long run causing market supply to increase, market price to fall

and profits to decrease.

D) the number of firms in the industry will remain constant in the long run.

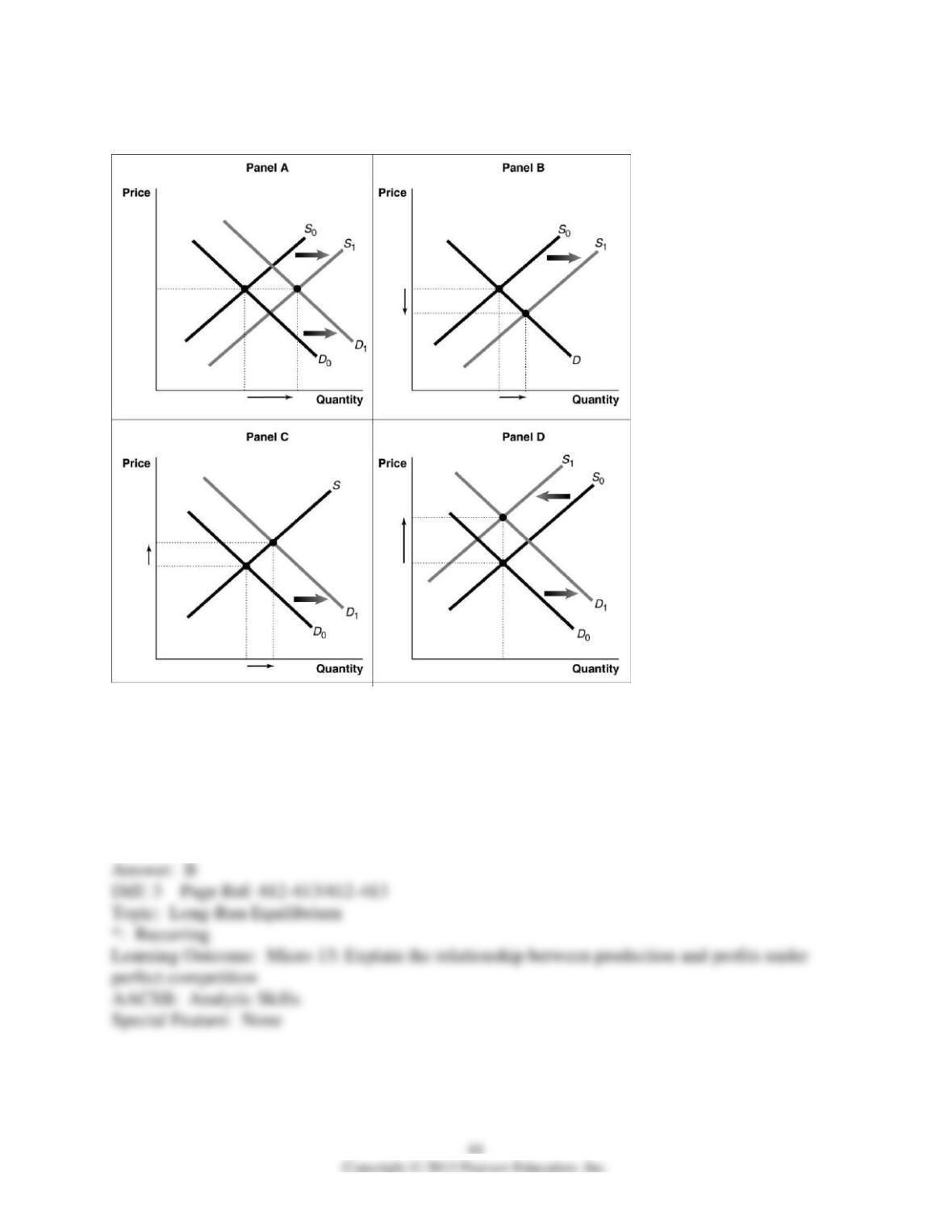

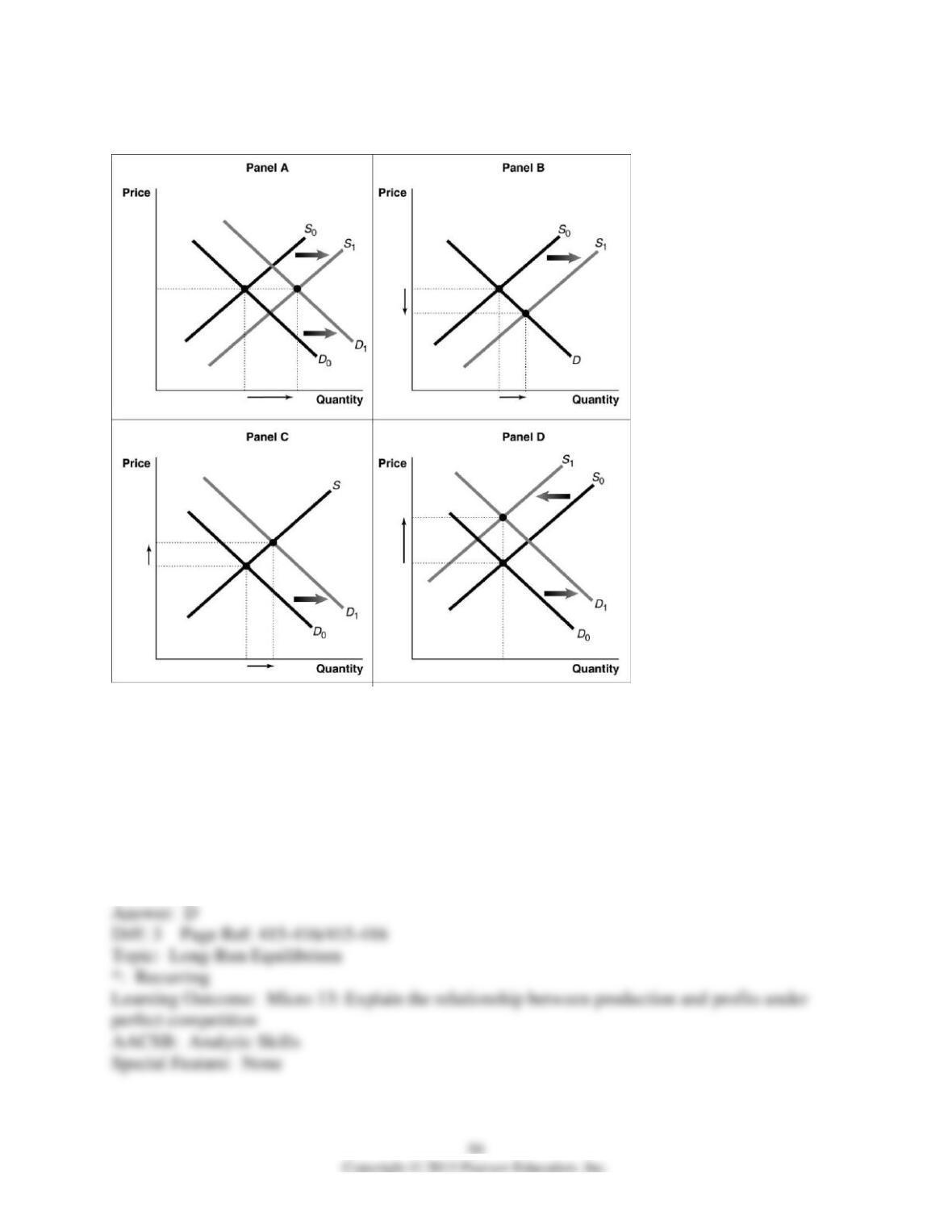

Figure 12-8

6) Refer to Figure 12-8. Consider a typical firm in a perfectly competitive industry that makes

short-run profits. Which of the diagrams in the figure shows the effect on the industry as it

transitions to a long-run equilibrium?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

7) If, in a perfectly competitive industry, the market price facing a firm is above its average total

cost at the output where marginal revenue equals marginal cost, then

A) firms are breaking even.

B) new firms are attracted to the industry.

C) existing firms will exit the industry.

D) market supply will remain constant.

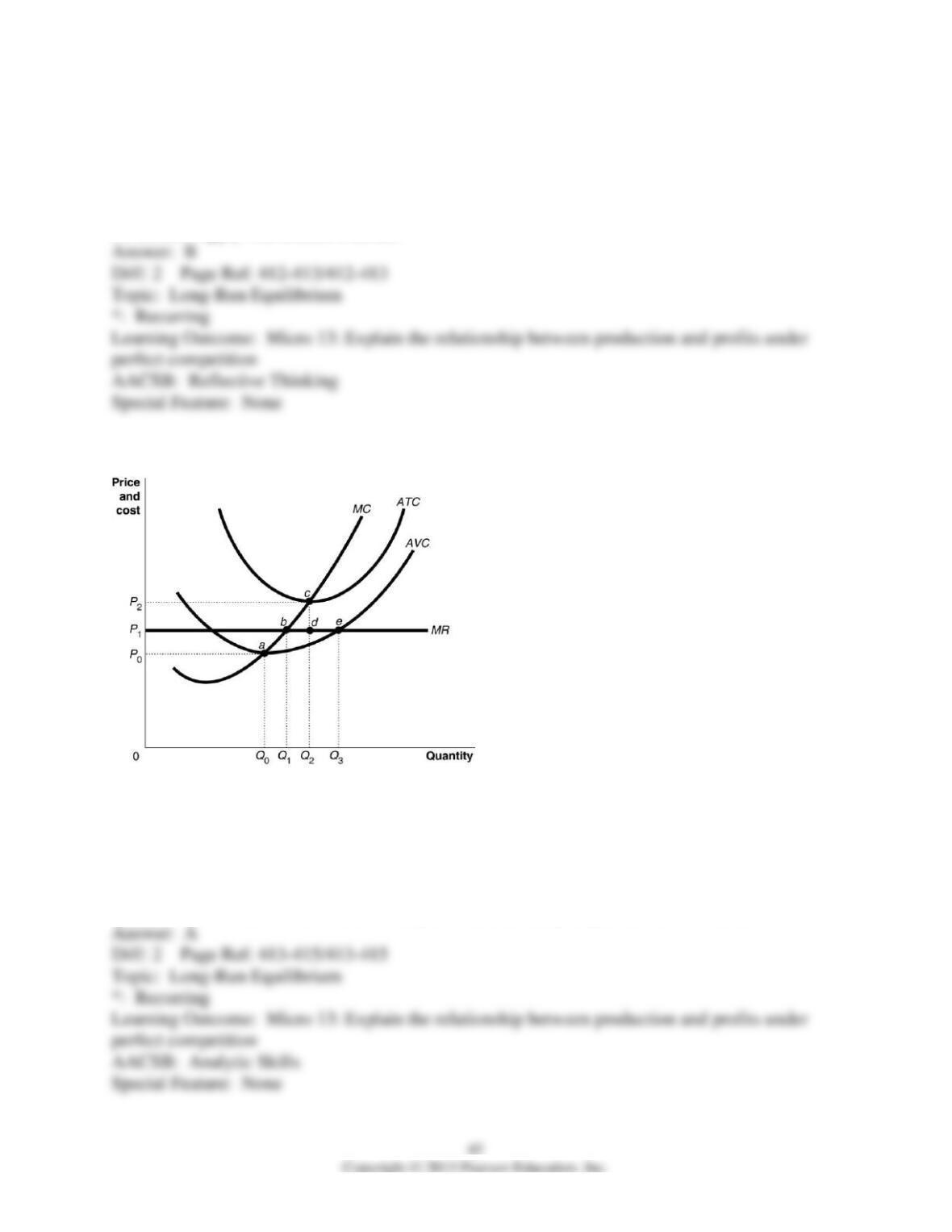

Figure 12-9

8) Refer to Figure 12-9. Suppose the prevailing price is P1 and the firm is currently producing

its loss-minimizing quantity. In the long-run equilibrium,

A) there will be fewer firms in the industry and total industry output decreases.

B) there will be more firms in the industry and total industry output increases.

C) there will be fewer firms in the industry but total industry output increases.

D) there will be more firms in the industry and total industry output remains constant.

9) Refer to Figure 12-9. Suppose the prevailing price is P1 and the firm is currently producing

its loss-minimizing quantity. If the firm represented in the diagram continues to stay in business,

in the long-run equilibrium,

A) it will reduce its output to Q0 and face a price of P0.

B) it will continue to produce Q1 but faces the higher price of P2.

C) it will expand its output to Q2 and face a price of P2.

D) it will expand its output to Q3 and face a price of P1.

10) If a typical firm in a perfectly competitive industry is incurring losses, then

A) all firms will continue to lose money.

B) some firms will exit in the long run, causing market supply to decrease and market price to

rise increasing profits for the remaining firms.

C) some firms will exit in the long run, causing market supply to decrease and market price to

fall increasing losses for the remaining firms.

D) some firms will enter in the long run, causing market supply to increase and market price to

rise increasing profit for all firms.

11) A perfectly competitive market is in long-run equilibrium. At present there are 100 identical

firms each producing 5,000 units of output. The prevailing market price is $20. Assume that each

firm faces increasing marginal cost. Now suppose there is a sudden increase in demand for the

industry’s product which causes the price of the good to rise to $24. Which of the following

describes the effect of this increase in demand on a typical firm in the industry?

A) In the short run, the typical firm increases its output and makes an above normal profit.

B) In the short run, the typical firm’s output remains the same but because of the higher price, its

profit increases.

C) In the short run, the typical firm increases its output but its total cost also rises, resulting in no

change in profit.

D) In the short run, the typical firm increases its output but its total cost also rises. Hence, the

effect on the firm’s profit cannot be determined without more information.

12) In long-run perfectly competitive equilibrium, which of the following is false?

A) There is efficient, low-cost production at the minimum efficient scale.

B) Economic surplus is maximized.

C) Firms earn economic profit.

D) Economies of scale are exhausted.

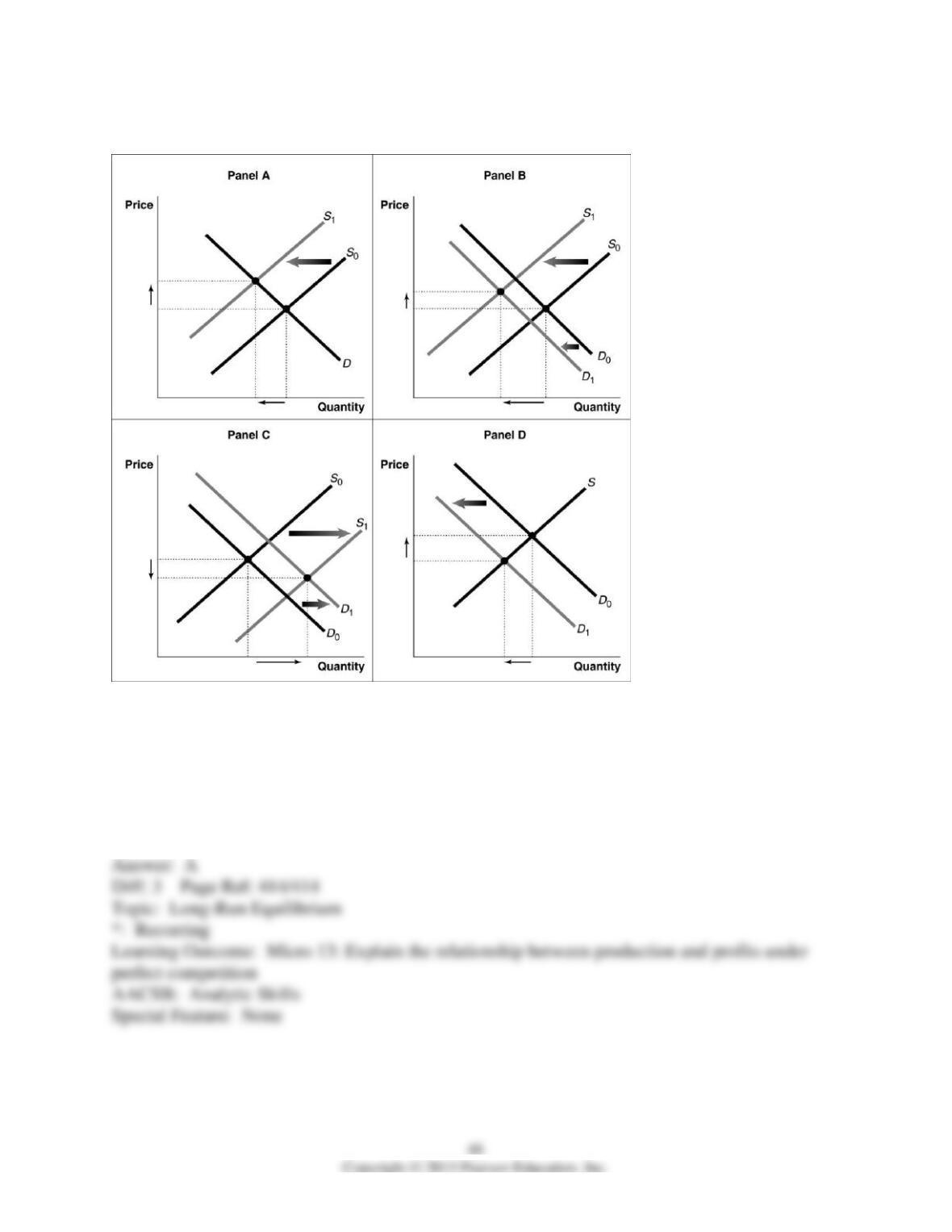

Figure 12-10

13) Refer to Figure 12-10. Consider a typical firm in a perfectly competitive industry which is

incurring short-run losses. Which of the diagrams in the figure shows the effect on the industry

as it transitions to a long-run equilibrium?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

14) If in a perfectly competitive industry, the market price facing a firm is below its average total

cost but above average variable cost at the output where marginal cost equals marginal revenue

A) the industry supply will not change.

B) new firms are attracted to the industry.

C) some existing firms will exit the industry.

D) firms are breaking even.

Figure 12-11

15) Refer to Figure 12-11. Assume that the medical screening industry is perfectly competitive

and that some firms are making short-run losses. Suppose the medical screening industry runs an

effective advertising campaign which convinces a large number of people that yearly CT scans

are critical for good health. Which of the diagrams in the figure best describes what happens in

the industry?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

16) Refer to Figure 12-11. Suppose a typical firm in a perfectly competitive market is earning

economic profits in the short run. Which of the diagrams in the figure depicts what happens to in

the industry as it transitions to along run equilibrium?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

17) Assume that the medical screening industry is perfectly competitive. Consider a typical firm

that is making short-run losses. Suppose the medical screening industry runs an effective

advertising campaign which convinces a large number of people that yearly CT scans are critical

for good health. How will this affect a typical firm that remains in the industry?

A) The firm’s supply curve shifts right and its marginal revenue curve shifts upwards as the

market price rises and ultimately the firm starts making profits.

B) The firm’s marginal revenue curve and average cost curve shift upwards in response to the

increase in market price and advertising expenditure. The firm increases output until it starts

breaking even.

C) The marginal revenue curve shifts upwards, the firm’s output increases along its marginal cost

curve, it expands production and eventually starts making profits.

D) The marginal revenue curve shifts upwards, the firm’s output increases along its marginal cost

curve, it expands production until it breaks even.

18) An industry’s long-run supply curve shows

A) the relationship in the long run between market price and quantity supplied.

B) how the government determines the price of the product.

C) how average productivity is changing.

D) greater than normal profit.

19) In the long run, a perfectly competitive market will

A) produce only the quantity of output that yields a long-run profit for the typical firm.

B) supply whatever amount consumers will buy at a price which earns the market an economic

profit.

C) supply whatever amount consumers demand at a price determined by the minimum point on

the typical firm’s average total cost curve.

D) generate a long-run equilibrium where the typical firm operates at a loss.

20) A perfectly competitive wheat farmer in a constant-cost industry produces 3,000 bushels of

wheat at a total cost of $36,000. The prevailing market price is $15. What will happen to the

market price of wheat in the long run?

A) The price remains constant at $15.

B) The price falls to $12.

C) The price rises above $15.

D) There is insufficient information to answer the question.