Chapter 12: The Statement of Cash Flows

85. Pilot Company reported the following information for 2015 and 2016.

Prepaid insurance, December 31, 2015 $ 2,400

Prepaid insurance, December 31, 2016 1,500

Insurance expense—2016 14,200

How much cash was paid for insurance during 2016?

a. $13,300

b. $14,200

c. $15,100

d. $15,700

86. Suma Corp. reported the following information for 2015 and 2016.

Salaries payable, December 31, 2015 $ 3,700

Salaries payable, December 31, 2016 1,800

Salaries expense—2016 57,000

How much cash was paid for salaries during 2016?

a. $55,100

b. $55,200

c. $57,000

d. $58,900

87. Tulsa Corp. reported the following information for 2015 and 2016.

Interest payable, December 31, 2015 $ 5,700

Interest payable, December 31, 2016 6,200

Interest expense—2016 12,250

How much cash was paid for interest during 2016?

a. $11,750

b. $12,250

c. $12,500

d. $12,750

88. Dallas Corp. reported the following information for 2015 and 2016.

Interest receivable, December 31, 2015 $1,100

Interest receivable, December 31, 2016 1,400

Interest income—2016 3,200

How much cash was received for interest during 2016?

a. $2,900

b. $3,200

c. $3,500

d. $3,800

89. Use the information below for Alpha Inc. for 2015 and 2016 to answer the following question.

Equipment, December 31, 2015

$65,000

Equipment, December 31, 2016

72,000

Accumulated depreciation, December 31, 2015

39,000

Accumulated depreciation, December 31, 2016

30,000

During 2016, Alpha Inc. sold equipment with a cost of $30,000 and accumulated depreciation of $25,000. A

gain of $3,000 was recognized on the sale of the equipment This was the only equipment sale during the year.

What amount would be reported as the cash proceeds from the sale of equipment?

a. $2,000

b. $3,000

c. $5,000

d. $8,000

Chapter 12: The Statement of Cash Flows

90. Use the information below for Shorter Inc. for 2015 and 2016 to answer the following question.

Equipment, December 31, 2015

$65,000

Equipment, December 31, 2016

72,000

Accumulated depreciation, December 31, 2015

39,000

Accumulated depreciation, December 31, 2016

30,000

During 2016, Shorter Inc. sold equipment with a cost of $30,000 and accumulated depreciation of $25,000. A

gain of $3,000 was recognized on the sale of the equipment This was the only equipment sale during the year.

Assume that all purchases of equipment were paid with cash. How much cash was paid by Shorter for the

purchase of equipment during 2016?

a. $ 7,000

b. $30,000

c. $37,000

d. $72,000

91. Use the information below for Flora Inc. for 2015 and 2016 to answer the following question.

Equipment, December 31, 2015

$65,000

Equipment, December 31, 2016

72,000

Accumulated depreciation, December 31, 2015

39,000

Accumulated depreciation, December 31, 2016

30,000

During 2016, Flora Inc. sold equipment with a cost of $30,000 and accumulated depreciation of $25,000. A gain

of $3,000 was recognized on the sale of the equipment This was the only equipment sale during the year.

What was depreciation expense for 2016?

a. $ 9,000

b. $16,000

c. $21,000

d. $30,000

92. Which of the following statements is false regarding how the cash flow effects of the changes in the

equipment and accumulated depreciation accounts would be reported on a statement of cash flows if the

indirect method is used to prepare the operating activities section?

a. Cash proceeds from the sale of the equipment would be reported as a cash inflow in the investing

activities section.

b. The cash paid to purchase equipment would be reported as a cash outflow in the investing activities section

c. Depreciation expense would be added to net income in the operating activities section.

d. A loss on the sale of the equipment would be subtracted from net income in the operating activities section

Chapter 12: The Statement of Cash Flows

93. Use the information below for Focal Point Corp. for 2015 and 2016 to answer the following question.

Retained earnings, December 31, 2015

$300,000

Retained earnings, December 31, 2016

345,000

Dividends payable, December 31, 2015

19,000

Dividends payable, December 31, 2016

29,000

Net income—2016

150,000

Assume that there were no retained earnings transactions other than those dealing with dividends and net

income. How much dividends did Focal Point declare during 2016?

a. $ 95,000

b. $105,000

c. $140,000

d. $150,000

94. Use the information below for Barton Shipping Corp. for 2015 and 2016 to answer the following question.

Retained earnings, December 31, 2015

$300,000

Retained earnings, December 31, 2016

345,000

Dividends payable, December 31, 2015

19,000

Dividends payable, December 31, 2016

29,000

Net income—2016

150,000

How much cash did Barton Shipping pay for dividends during 2016?

a. $ 95,000

b. $105,000

c. $115,000

d. $140,000

Chapter 12: The Statement of Cash Flows

95. Use the information below for Fargo Corp. for 2015 and 2016 to answer the following question.

Bonds payable, December 31, 2015

$500,000

Bonds payable, December 31, 2016

800,000

Loss on bond retirement—2016

15,000

Interest expense on bonds—2016

45,000

At the end of 2016, Fargo issued bonds at par value for $800,000 cash. The proceeds from these bonds were

used to retire the $500,000 bond issue outstanding at the end of 2015 (before their maturity date). All interest

expense was paid in cash during 2016.

How much did Fargo pay to retire the $500,000 bond issue during 2016?

a. $485,000

b. $500,000

c. $515,000

d. $560,000

96. Carpet World Inc. reported the following information for 2015 and 2016.

2015

2016

Accounts receivable

$51,000

$57,000

Inventories

42,000

39,000

Accounts payable

43,000

48,000

Net income

60,000

Depreciation expense

8,000

If Carpet World uses the indirect method to prepare the operating activities section of the statement of cash

flows, what amount will be reported as net cash inflow from operating activities for 2016?

a. $64,000

b. $66,000

c. $68,000

d. $70,000

Chapter 12: The Statement of Cash Flows

97. Washington Corp. reported the following information for 2015 and 2016.

2015

2016

Accounts receivable

$101,000

$93,000

Prepaid expenses

5,000

6,000

Accounts payable

71,000

76,000

Salaries payable

5,000

4,000

Net income

80,000

Depreciation expense

9,000

Gain on sale of equipment

5,000

If Washington uses the indirect method to prepare the operating activities section of the statement of cash flows,

what amount will be reported as net cash inflow from operating activities for 2016?

a. $ 73,000

b. $ 83,000

c. $ 95,000

d. $105,000

98. Two methods are available to prepare the operating activities section of a statement of cash flows. Which of

the following statements regarding these two methods is false?

a. If a company uses the indirect method, it must separately disclose the cash payments made for interest

and income taxes.

b. If a company uses the direct method, it must present a separate schedule which reconciles net income to

net cash from operating activities.

c. Advocates of the direct method believe that the indirect method reveals too much by telling readers

gross amounts of cash receipts and cash payments from operations.

d. The FASB prefers the direct method, while most companies use the indirect method in practice.

99. Which of the following is an addition to net income when the indirect method is used?

a. an increase in inventory

b. a loss on sale of equipment

c. a decrease in accounts payable

d. an increase in accounts receivable

Chapter 12: The Statement of Cash Flows

100. Vencenzia Company reported the following information in its annual report for 2016.

Cash flows from operating activities

$300,000

Capital Expenditures

225,000

Average amount of debt maturing over the next 5 years

200,000

What is the cash flow adequacy ratio for 2016 for Vencenzia Company?

a. 0.38

b. 1.50

c. 1.88

d. 7.50

101. Which of the following measures can be used to evaluate a company’s ability to meet future debt obligations

after paying income taxes and interest and making capital expenditures?

a. Earnings per share

b. Net income

c. Cash flow adequacy ratio

d. Net increase or decrease in cash and cash equivalents

102. Where would you tell someone to find the information needed to compute the cash flow adequacy ratio?

a. the balance sheet only

b. the statement of cash flows and the notes to the statements

c. the statement of cash flows only

d. the income statement only

103. The statement of cash flows summarizes the operating, investing, and financing activities of a business for a

period of time.

a. True

b. False

104. The accrual-based income statement is considered to be a good indicator of current cash inflows and outflows.

a. True

b. False

Chapter 12: The Statement of Cash Flows

105. Depreciation is a noncash expense that is added back to net income in determining cash provided from

operating activities under the indirect method.

a. True

b. False

106. In terms of the statement of cash flows, cash includes actual cash items plus certain cash equivalents such

as commercial paper, money market funds, and Treasury bills.

a. True

b. False

107. To be classified as a cash equivalent, an item must be readily convertible to a known amount of cash and have

an original maturity to the investor of three months or more.

a. True

b. False

108. Under certain conditions, an investment in common stock can be considered a cash equivalent.

a. True

b. False

109. Cash equivalents are reported in the Operating Activities section of the statement of cash flows.

a. True

b. False

110. The repurchase of a company’s own stock should be reported on the statement of cash flows as an investing

activity.

a. True

b. False

111. For the statement of cash flows, companies are required to classify their cash activities into three

categories: operating, investing, and borrowing.

a. True

b. False

Chapter 12: The Statement of Cash Flows

112. Operating activities involve the acquiring and selling of goods and services for cash or on account.

a. True

b. False

113. Cash flows from purchases of merchandise are classified as investing activities.

a. True

b. False

114. Issuance of stock results in cash inflows that appear in the financing section of the statement of cash flows.

a. True

b. False

115. Cash flows from operating activities usually relate to an increase or decrease in either a current asset or a

current liability.

a. True

b. False

116. A building with a cost of $163,000 and accumulated depreciation of $32,000 was sold for a $11,000 gain.

When using the indirect method, the cash generated from this investing activity was $131,000.

a. True

b. False

117. Net income was $ 61,000 for the year. The accumulated depreciation balance increased by $14,000 over the

year. There were no sales of fixed assets or changes in noncash current assets or liabilities. Under the indirect

method, the cash flow from operations is $47,000.

a. True

b. False

118. Companies can use two different methods to report the amount of cash flow from their investing and

financing activities.

a. True

b. False

Chapter 12: The Statement of Cash Flows

119. The direct method of reporting cash flows from operating activities involves reconciling net income and cash

flow from operations.

a. True

b. False

120. Under the indirect method, the first line in the operating activities section of the statement of cash flows is the

net income or loss for the period.

a. True

b. False

121. The issuance of common stock in exchange for a building would appear both as a cash inflow in the

financing activities section of the cash flow statement and also as a cash outflow in the investing activities

section.

a. True

b. False

122. Significant noncash transactions are not reported on the statement of cash flows, but either in a separate

schedule or in a note to the financial statements.

a. True

b. False

123. The statement of cash flows emphasizes explanations for the change in net income.

a. True

b. False

124. The Financial Accounting Standards Board (FASB) has expressed a strong preference for the indirect method,

but allows companies to use the direct method in calculating the cash flow from operating activities.

a. True

b. False

125. The basic accounting equation can be restated in terms of cash by the following equation: Cash = current

liabilities + long-term liabilities + capital stock – retained earnings – noncash current assets + long-term assets.

a. True

b. False

Chapter 12: The Statement of Cash Flows

126. Determining the cash flows from operating activities generally requires analyzing each item on the

income statement as well as the current asset (except cash) and current liability accounts.

a. True

b. False

127. If the December 31, 2016, balance of accounts receivable is higher than the January 1, 2016, balance,

then the amount of cash collections will be less than the sales on account for the year.

a. True

b. False

128. If the December 31, 2016, balance of accounts payable is higher than the January 1, 2016, balance, then the

amount of cash payments will exceed the purchases on account for the year.

a. True

b. False

129. Because the cash received from the sale of long-term assets is reported in the investing activities section of

the statement of cash flows, any gain or loss is built into the cash received under the direct method.

a. True

b. False

130. A decrease in retained earnings indicates that a cash dividend has been paid.

a. True

b. False

131. Under the direct method, depreciation expense is treated as an outflow in the Investing Activities section of

the statement of cash flows.

a. True

b. False

132. Under the indirect method, instead of reporting cash receipts and payments, net income is reconciled with net

cash from operating activities.

a. True

b. False

Chapter 12: The Statement of Cash Flows

133. The cash flow adequacy ratio is defined as:

a. True

b. False

134. Many companies report cash flow per common share on the statement of cash flows.

a. True

b. False

135. All the information needed to compute the cash flow adequacy ratio is found on the balance sheet.

a. True

b. False

136. The cash flow adequacy ratio can only be calculated if a company uses the direct method to report cash flows

from operating activities.

a. True

b. False

137. Cash flow per share is computed by dividing cash on the balance sheet by the number of shares outstanding.

a. True

b. False

138. Some companies use a work sheet approach, which functions like the T account approach, as a tool to

aid in preparing the statement of cash flows.

a. True

b. False

139. The work sheet used to prepare a statement of cash flows (indirect method to determine cash flows from

operating activities) should have a total in the Changes column equal to total assets.

a. True

b. False

Chapter 12: The Statement of Cash Flows

140. A work sheet is an alternative to T accounts to help in the preparation of a statement of cash flows.

a. True

b. False

141. The financial statement that primarily reflects events related to the operating activities of a business, or the

selling of products or providing services is the .

142. The financial statement that summarizes the operating, investing, and financing activities of a business over a

period of time is the ___________________________________.

143. are items which are readily convertible into a known amount of cash and

have an original maturity to the investor of three months or less.

144. The term cash on the statement of cash flows includes .

145. An important activity for many companies is acquiring property.

146. The purchase of merchandise is an important activity for a retailer.

147. The decrease in accounts receivable over a period results in a(n) to net

income reported in the operating activities section of the statement of cash flows using the indirect method.

148. activities involve long-term liabilities and stockholders’ equity.

149. Under the , a company reports its major classes of gross cash receipts

and cash payments in the operating activities section of the statement of cash flows.

150. Under the , the net cash flow from operating activities is computed

by adjusting net income to remove the effect of all deferrals of past operating cash receipts and payments,

and all accruals of future operating cash receipts or payments.

Chapter 12: The Statement of Cash Flows

151. If the balance of accounts receivable decreases during the year, then cash collections will

____________________________ sales on account for the period.

152. If the balance of wages payable increases during the year, then the for

the period will be greater than the actual cash wages paid in the period.

153. If the balance of prepaid insurance was the same on January 1, 2016, and December 31, 2016, then the

insurance expense would the cash payments made for insurance during the year.

154. A decrease in retained earnings represents dividends that were during the period, not

necessarily those that were paid.

155. The objective of the indirect method is to reconcile net income to net cash flow from

_______________________________.

156. ___________________________ is a noncash expense related to plant assets.

157. Under the indirect method, a loss from the retirement of bonds is to net

income in the operating activities section of the statement of cash flows.

158. The amount of cash provided from operating activities is under both the direct

and indirect methods.

159. is a measure of a company’s ability to meet its future

debt obligations after paying income taxes and interest costs and making capital expenditures.

160. In place of _____________, a worksheet is a useful device to help in the preparation of a statement of

cash flows.

Chapter 12: The Statement of Cash Flows

161. The following events occurred at Cute Canines Company during its first year of business:

a. To establish the company, the two owners contributed a total of $60,000 in exchange for common stock.

b. Grooming service revenue for the first year amounted to $175,000, of which $50,000 was on account.

c. Customers owe $15,000 at the end of the year from the services provided on account.

d. At the beginning of the year, a storage building was rented. The company was required to sign a three-year

lease for $15,000 per year and make a $3,000 refundable security deposit. The first year’s lease payment

and the security deposit were paid at the beginning of the year.

e. At the beginning of the year, the company purchased a patent at a cost of $120,000 for a revolutionary

system for dog grooming. The patent is expected to be useful for ten years. The company paid 20% down

in cash and signed a four-year note at the bank for the remainder.

f. Operating expenses, including amortization of the patent and rent on the storage building, totaled $90,000

for the year. No expenses were accrued or unpaid at the end of the year.

g. The company declared and paid a $25,000 cash dividend at the end of the first year.

REQUIRED:

1. Prepare an income statement for the first year.

2. Prepare a statement of cash flows for the first year using the direct method in the Operating Activities

section.

3. Did the company generate more or less cash flow from operations than it earned in net income? Explain

why there is a difference.

4. Prepare a balance sheet as of the end of the first year.

Chapter 12: The Statement of Cash Flows

Chapter 12: The Statement of Cash Flows

162. Fairleigh Industries invested its excess cash in the following instruments during December 2015:

Certificate of deposit, due January 31, 2016

$ 45,000

Certificate of deposit, due June 30, 2016

95,000

Investment in City of Cleveland bonds, due May 1, 2017

15,000

Investment in Techno Data stock

66,000

Money market fund

125,000

90-day Treasury bills

95,000

Treasury note, due December 1, 2016

200,000

Determine the amount of cash equivalents that should be combined with cash on the company’s balance sheet at

December 31, 2015, and for purposes of preparing a statement of cash flows for the year ended December 31,

2015.

Chapter 12: The Statement of Cash Flows

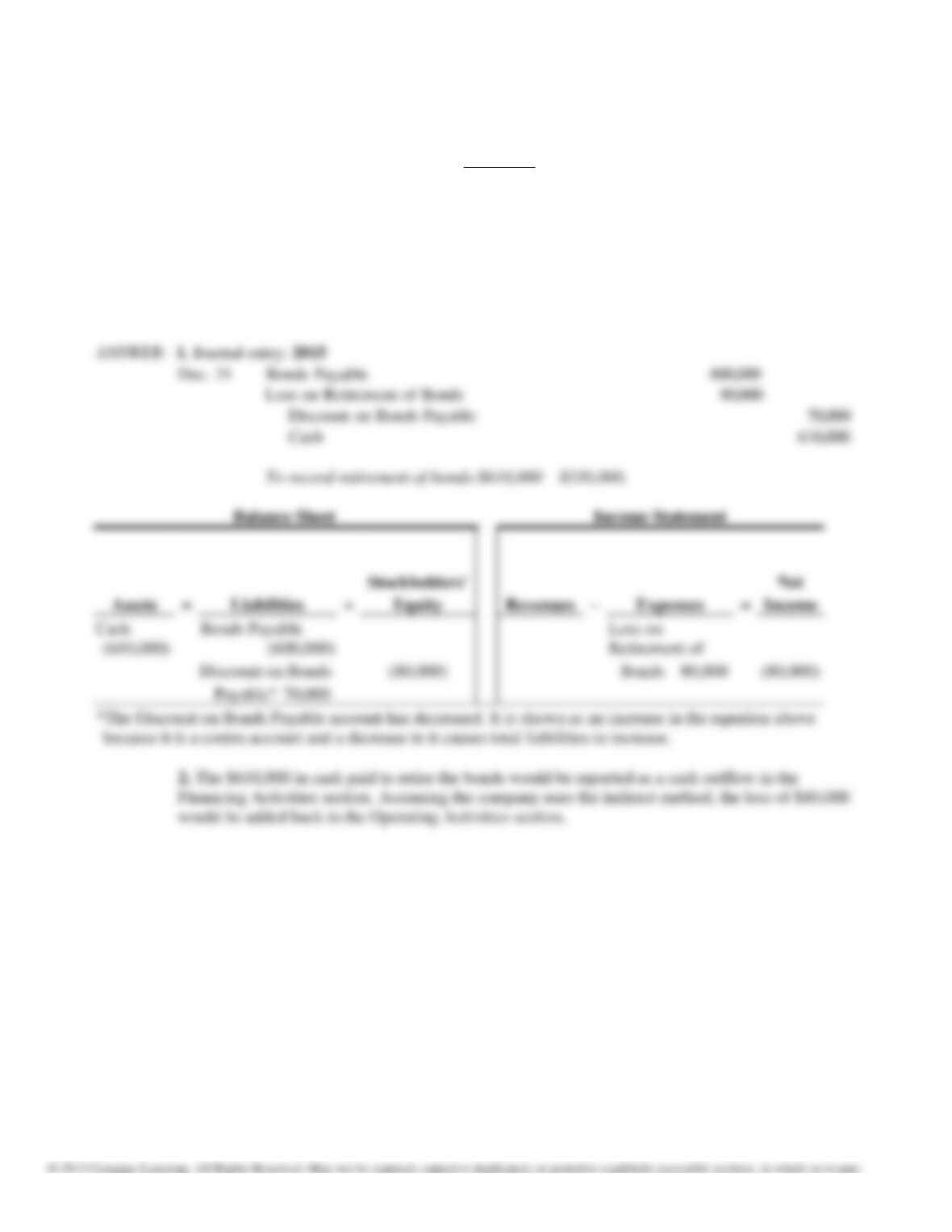

163. Dickinson Inc. has the following debt outstanding on December 31, 2015:

10% bonds payable, due 12/31/19

$600,000

Discount on bonds payable

(70,000)

Net bonds payable

$530,000

On this date, Dickinson retired the entire bond issue by paying cash of $610,000.

REQUIRED:

1. Prepare the journal entry to record the bond retirement.

2. Describe how the bond retirement would be reported on the statement of cash flows assuming that

Dickinson uses the indirect method.

Chapter 12: The Statement of Cash Flows

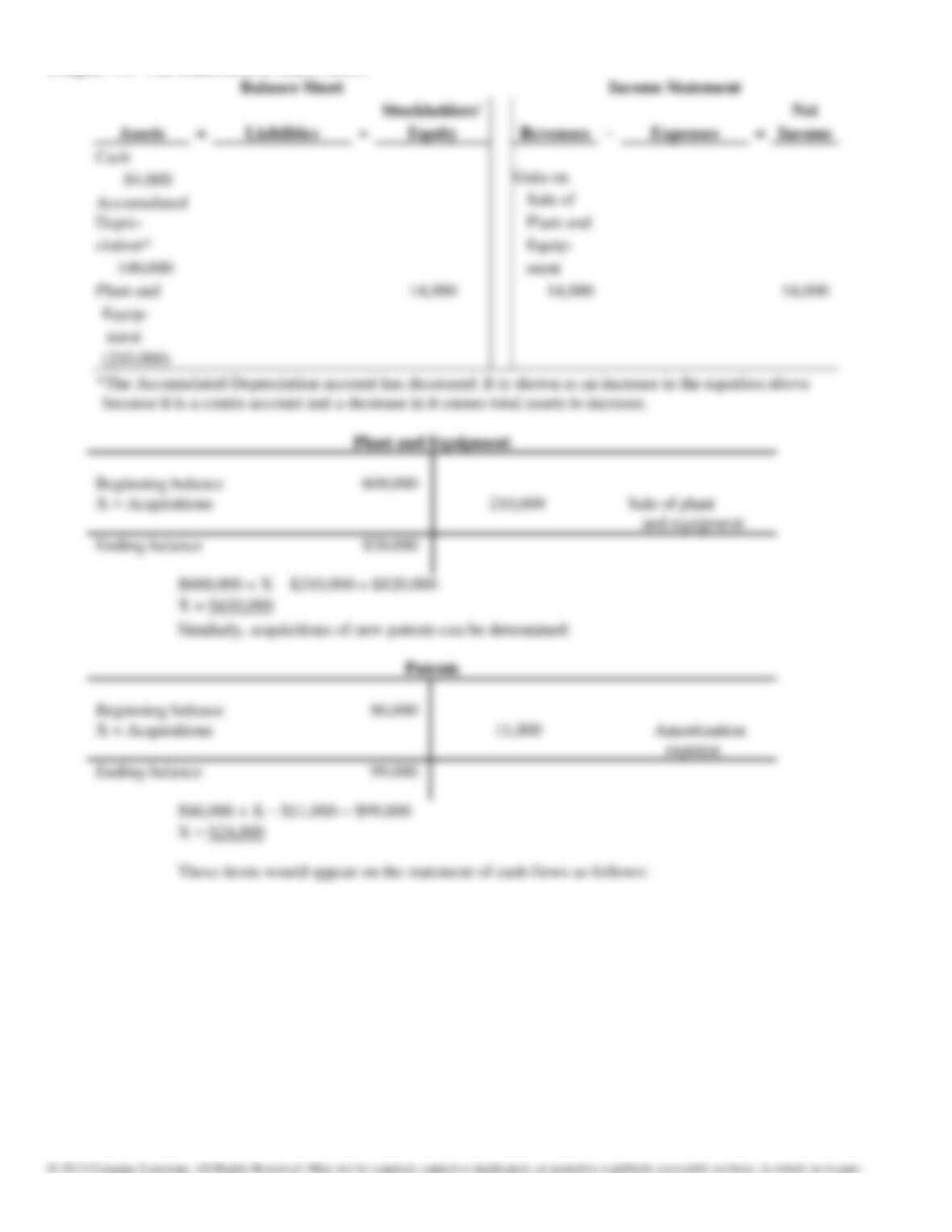

164. The following account balances are taken from the records of Morgantown Corp. for the past two years.

(Credit balances are shown in parentheses.)

Other information available for 2016 is as follows:

December 31,

2016

2015

Plant and equipment

$ 820,000

$ 600,000

Accumulated depreciation

(170,000)

(250,000)

Patents

99,000

86,000

Retained earnings

(825,000)

(675,000)

a. Net income for the year was $240,000.

b. Depreciation expense on plant and equipment was $60,000.

c. Plant and equipment with an original cost of $210,000 were sold for $84,000. (You will need to

determine the book value of the assets sold.)

d. Amortization expense on patents was $11,000.

e. Both new plant and equipment and patents were purchased for cash during the

year.

REQUIRED:

Indicate, with amounts, how all items related to these long-term assets would be reported in the 2016

statement of cash flows, including any adjustments in the Operating Activities section of the statement.

Assume that Morgantown uses the indirect method.

Chapter 12: The Statement of Cash Flows

Revenues

Beginning balance 600,000

X = Acquisitions

Ending balance 820,000

Beginning balance 86,000

X = Acquisitions

Ending balance 99,000

Cash Flows from Operating Activities

Net income

$240,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense

60,000

Amortization expense

11,000

Gain on sale of plant and equipment

(14,000)

Cash Flows from Investing Activities

Sale of plant and equipment

$84,000

Acquisition of plant and equipment

(430,000)

Acquisition of patents

(24,000)