102. When different units that perform the same types of activities within the same organization are compared

to the unit with the best performance, this practice is called

103. A technique for improving performance of activities and processes that predicts activity costs as activity

output changes is called

104. Mattison Company has developed cost formulas for the drivers of the following production activities:

Driver

Activity

Fixed

Variable

Labor hours

Materials

$ -0-

$20

Labor hours

Labor

-0-

10

Machine hours

Maintenance

10,000

8

Machine hours

Machining

50,000

2

Number of setups

Inspections

30,000

200

Number of setups

Setups

-0-

300

Number of purchase orders

Purchasing

75,000

3

The budgeted inspection cost for 20 setups is

105. Mattison Company has developed cost formulas for the drivers of the following production activities:

Driver

Activity

Fixed

Variable

Labor hours

Materials

$ -0-

$20

Labor hours

Labor

-0-

10

Machine hours

Maintenance

10,000

8

Machine hours

Machining

50,000

2

Number of setups

Inspections

30,000

200

Number of setups

Setups

-0-

300

Number of purchase orders

Purchasing

75,000

3

The activity levels are projected to be as follows:

Labor hours

1,000

Machine hours

5,000

Setups

100

Purchase orders

50

What is budgeted for this projected activity level?

106. Mattison Company has developed cost formulas for the drivers of the following production activities:

Driver

Activity

Fixed

Variable

Labor hours

Materials

$ -0-

$20

Labor hours

Labor

-0-

10

Machine hours

Maintenance

10,000

8

Machine hours

Machining

50,000

2

Number of setups

Inspections

30,000

200

Number of setups

Setups

-0-

300

Number of purchase orders

Purchasing

75,000

3

If the actual activity was 20 setups and the actual fixed cost for inspections was $28,000 and the variable cost for inspections was $5,000, the total

variance for inspections is

107. Mattison Company has developed cost formulas for the drivers of the following production activities:

Driver

Activity

Fixed

Variable

Labor hours

Materials

$ -0-

$20

Labor hours

Labor

-0-

10

Machine hours

Maintenance

10,000

8

Machine hours

Machining

50,000

2

Number of setups

Inspections

30,000

200

Number of setups

Setups

-0-

300

Number of purchase orders

Purchasing

75,000

3

If the actual activity was 20 setups and the actual fixed cost for inspections was $28,000 and the variable cost for inspections was $5,000, the total

variance for inspections is due to

108. The capacity variance is composed of the unused capacity variance and

109. Livingston Company has developed capacity standards. Information is as follows:

Standard cost of the activity capacity acquired

$250,000

Standard cost of the activity capacity used

200,000

Standard cost of the actual activity used

220,000

The volume variance is

D. $30,000 unfavorable.

110. Livingston Company has developed capacity standards. Information about a non-value-added activity is as

follows:

Standard cost of the activity capacity acquired

$60,000

Standard cost of the activity capacity used

-0-

Standard cost of the actual activity used

50,000

The volume variance is

111. Livingston Company has developed capacity standards. Information is as follows:

Standard cost of the activity capacity acquired

$250,000

Standard cost of the activity capacity used

200,000

Standard cost of the actual activity used

220,000

The unused capacity variance is

112. The unused capacity variance is

113. A technique for improving performance of activities and processes that compares the number of times an

activity can be performed to the number actually performed is called

114. Salvador Company has developed capacity standards. Information is as follows for a value-added activity:

Activity capacity acquired

60

Activity capacity used

50

Actual activity usage

30

Standard fixed activity rate

$2,000

The volume variance is

115. Salvador Company has developed capacity standards. Information is as follows for a value-added activity:

Activity capacity acquired

60

Activity capacity used

50

Actual activity usage

30

Standard fixed activity rate

$2,000

The unused capacity variance is

116. Under what conditions would the activity capacity used be zero?

117. Activity-based management can be viewed as an information system with broad objectives. Which of the

following is NOT on of the broad objectives of ABM?

118. Which of the following is NOT an objective of activity-based management?

119. Which of the following is NOT a reason for ABM implementation failure?

120. Which of the following is NOT an objective of responsibility accounting?

121. Which of the following is NOT a common step in an ABM implementation model?

122. Which of the following is NOT an essential element of responsibility accounting?

123. The responsibility accounting system developed for operations in a continuous improvement environment

would be

124. Which of the following is descriptive of activity-based responsibility accounting?

125. Which of the following is descriptive of financial-based responsibility accounting?

126. Which of the following is NOT a necessary essential element of activity-based responsibility accounting?

127. The process which refers to the performance of a process in a new way to achieve major improvements is

called:

128. Process improvement can be defined as

129. The process which refers to incremental or continual increases in the efficiency of an existing product is

called:

130. The process which refers to the adoption of new processes to meet strategic objectives is called:

132. The term(s )which refer(s) to a global incentive that encourages employees to contribute to the overall

financial well-being is(are) called

133. The term(s) which refer(s) to an incentive that specifically relates to sharing the gains from improvements

in projects is(are) called

134. The following is(are) awards made when performance is maintained or exceeds a specific measure:

135. Describe how activity-based management and activity-based costing systems differ.

136. What is process value analysis?

137. What is Kaizen costing? How does activity analysis help reduce costs?

138. Given the following data:

Activity

Driver

SQ2014

AQ2014

SP2014

SQ2015

AQ2015

SP2015

Purchasing

Purchase Orders

2,000

3,000

$85

2,000

2,500

$85

Receiving

Receiving Orders

3,750

4,300

$60

3,750

4,000

$60

Moving

# of moves

0

300

$110

0

200

$110

Setups

# of setups

0

75

$210

0

50

$210

Required:

1.

Determine the value-added and non-value added costs for each category for 2014 and 2015.

2.

Prepare a trend report that compares 2014 and 2015.

20104

2014

2015

2015

Value Added

Non-value added

Value Added

Non-value added

Purchasing

$170,000

$85,000

$170,000

$42,500

Receiving

$225,000

$33,000

$225,000

$15,000

Moving

$33,000

$22,000

Setups

$15,750

$10,500

Trend analysis

2014

2015

Non-value added

Non-value added

Change

Purchasing

$85,000

$42,500

$42,500

F

Receiving

$33,000

$15,000

$18,000

F

Moving

$33,000

$22,000

$11,000

F

Setups

$15,750

$10,500

$5,250

F

139. Lionel, Inc., has developed ideal standards for four activities: labor, materials, inspection, and receiving.

Information is as follows:

Activity

Activity Driver

SQ

AQ

SP

Labor

Hours

500

550

$ 32

Materials

Pounds

2,000

2,500

48

Inspection

Inspection hours

0

375

22

Receiving

Orders

60

75

800

The actual prices paid per unit of each activity driver were equal to the standard prices.

Required:

Complete the following cost report.

Activity

Value-Added

Non-value-Added

Actual

Labor

$_____________

$_____________

$____________

Materials

_____________

_____________

____________

Inspection

_____________

_____________

____________

Receiving

_____________

_____________

____________

Totals

$_____________

$_____________

$____________

(SQ ´ SP)

(AQ – SQ) ´ SP

Activity

Value-Added

Non-value-Added

Actual

Labor

$16,000

$ 1,600

$ 17,600

Materials

96,000

24,000

120,000

Inspection

-0-

8,250

8,250

Receiving

48,000

12,000

60,000

Totals

$160,000

$45,850

$205,850

140. Goodyear,, Inc., has developed ideal standards for four activities: labor, materials, inspection, and

receiving.

Information is as follows:

Activity

Activity Driver

SQ

AQ

SP

Labor

Hours

30,000

38,000

$11

Materials

Pounds

110,000

160,000

10

Inspection

Inspection hours

0

50,000

7

Receiving

Orders

600

700

450

The actual prices paid per unit of each activity driver were equal to the standard prices.

Required:

Complete the following cost report.

Activity

Value-Added

Non-value-Added

Actual

Labor

$_____________

$_____________

$____________

Materials

_____________

_____________

____________

Inspection

_____________

_____________

____________

Receiving

_____________

_____________

____________

Totals

$_____________

$_____________

$____________

(SQ ´ SP)

(AQ – SQ) ´ SP

Activity

Value-Added

Non-value-Added

Actual

Labor

$ 330,000

$ 88,000

$ 418,000

Materials

1,100,000

500,000

1,600,000

Inspection

-0-

350,000

350,000

Receiving

270,000

45,000

315,000

Totals

$1,700,000

$983,000

$2,683,000

141. The Opportunist Company recorded the following activities.Determine the amount of value-added and

non-value-added costs.

a.

Opportunist keeps 7 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs are $50,000 per

day.

b.

A time-and-motion study revealed that it should take 10 minutes to produce a product that now takes 50 minutes to produce. Labor is $18

per hour.

c.

Warranty work costs the firm $500,000 per year. Warranty costs for the industry average $100,000 per year.

a.

Value-added costs = $0

Value-added costs = ($18 ´ 10/60) = $3.00

Non-value-added costs = [(50 – 10)/60] ´ $18 = $12.00

c.

Value-added costs = $0

Non-value-added costs = $500,000

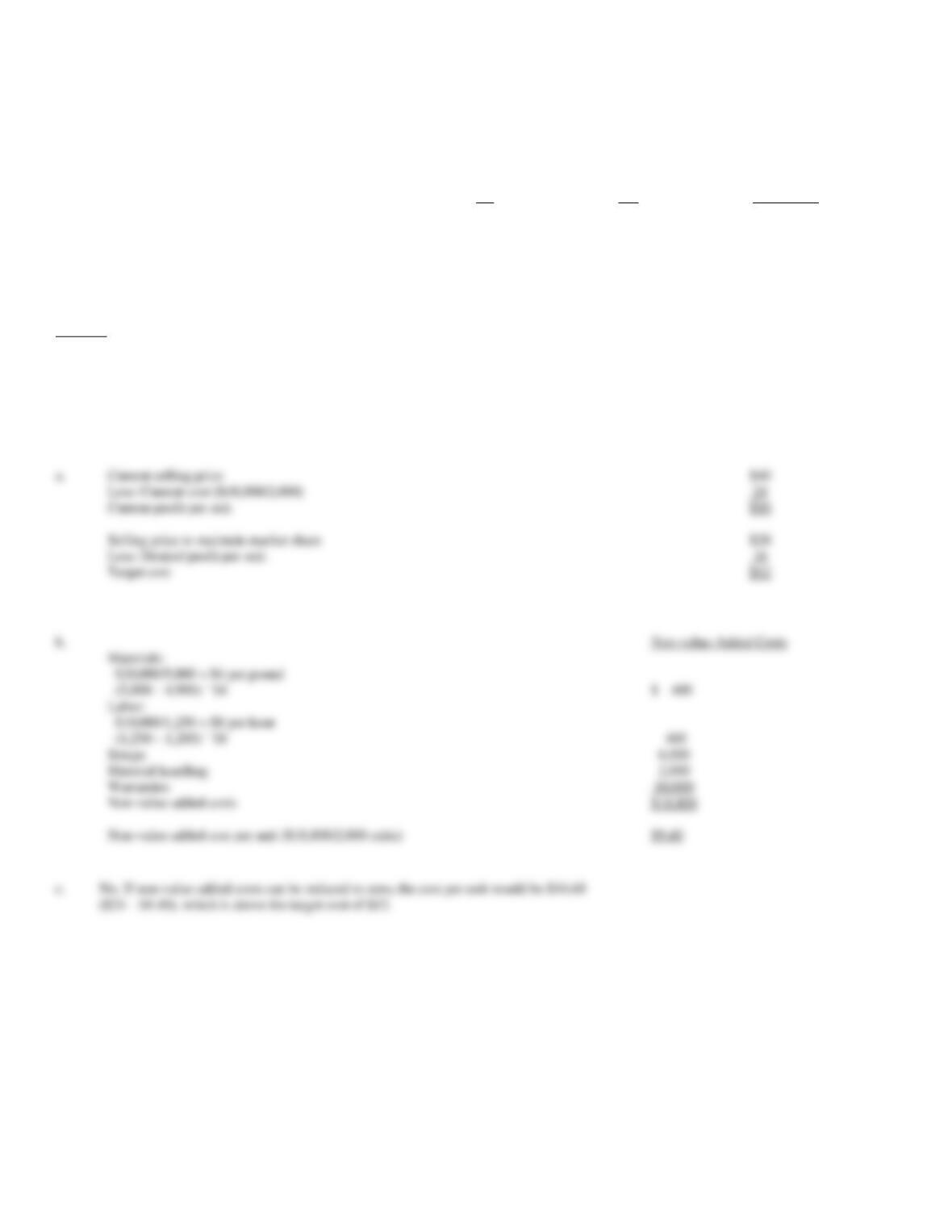

142. Suburbia, Inc., sells one of its products for $150 each. Sales volume averages 800 units per year. Recently,

its main competitor reduced the price of its product to $130. Suburbia expects sales to drop dramatically unless

it matches the competitor’s price. In addition, the current profit per unit must be maintained. Information about

the product (for production of 800) is as follows:

SQ

AQ

Actual Cost

Materials (pounds)

14,400

15,000

$30,000

Labor (hours)

2,000

2,400

18,000

Setups (hours)

0

1,400

8,000

Material handling (moves)

0

600

4,000

Warranties (number repaired)

0

400

20,000

Required:

a.

Calculate the target cost for maintaining current market share and profitability.

b.

Calculate the non-value-added cost per unit.

c.

If non-value-added costs can be reduced to zero, can the target cost be achieved?

a.

Current selling price

$150

Less: Current cost ($80,000/800)

100

Current profit per unit

$ 50

Selling price to maintain market share

$130

Less: Desired profit per unit

50

Target cost

$ 80

Non-value-Added Costs

Materials:

$30,000/15,000 = $2 per pound

(15,000 – 14,400) ´ $2

$ 1,200

Labor:

$18,000/2,400 = $7.50 per hour

(2,400 – 2,000) ´ $7.50

3,000

Setups

8,000

Material handling

4,000

Warranties

20,000

Non-value-added costs

$36,200

Non-value-added cost per unit ($36,200/800 units)

$ 45.25

($100 – $45.25), which is well below the target cost of $80.

143. Metropolitan, Inc., sells one of its products for $40 each. Sales volume averages 2,000 units per year.

Recently, its main competitor reduced the price of its product to $28. Metropolitan expects sales to drop

dramatically unless it matches the competitor’s price. In addition, the current profit per unit must be maintained.

Information about the product (for production of 2,000) is as follows:

SQ

AQ

Actual Cost

Materials (pounds)

4,900

5,000

$20,000

Labor (hours)

1,200

1,250

10,000

Setups (hours)

0

200

6,000

Material handling (moves)

0

350

2,000

Warranties (number repaired)

0

250

10,000

Required:

a.

Calculate the target cost for maintaining current market share and profitability.

b.

Calculate the non-value-added cost per unit.

c.

If non-value-added costs can be reduced to zero, can the target cost be achieved?

a.

Current selling price

Less: Current cost ($48,000/2,000)

Current profit per unit

Selling price to maintain market share

Less: Desired profit per unit

Target cost

Non-value-Added Costs

Materials:

$20,000/5,000 = $4 per pound

(5,000 – 4,900) ´ $4

$ 400

Labor:

$10,000/1,250 = $8 per hour

(1,250 – 1,200) ´ $8

400

Setups

6,000

Material handling

2,000

Warranties

10,000

Non-value-added costs

$18,800

Non-value-added cost per unit ($18,800/2,000 units)

$9.40

144. Buoungiorno Manufacturing has developed the following standards for its activities:

ACTIVITY

ACTIVITY DRIVER

SQ

AQ

SP

Materials usage

Yards

48,000

50,000

$5

Purchasing

Purchase orders

1,000

1,200

$40

Inspection

Inspection hours

0

6,000

$10

Assume the materials usage and purchasing costs correspond to flexible resources that acquired as needed and that inspections use resources that are

acquired in blocks of 2,000 hours. The actual prices paid for inputs equal the standard prices.

Required:

1. Assume that continuous improvement efforts reduce the demand for inspection by 30 percent during the year, which drops the actual

activity usage by 30 percent. Calculate the volume and unused capacity variances for inspection activity, materials usage and purchasing. Explain the

meaning of these variances.

2. Prepare a cost report that shows the value- and non-value-added costs.

3. Buoungiorno wants to reduce all non-value added costs by 30 percent. What Kaizen standards would be used to evaluate the company’s

progress? What would be the savings in resource spending?

COSTS

Value-added costs

Non-value added costs

Total

Materials use

$240,000 (48,000 ´ $5)

$10,000 [(48,000 – 50,000) ´ $5]

$250,000

Purchasing

$40,000 (1,000 ´ $40)

$8,000 [(1,000 – 1,200) ´ $40]

$ 48,000

Inspecting

$0

$60,000

$ 60,000

TOTAL

$280,000

$78,000

$358,000

Kaizen quantity

Kaizen cost

Materials use

50,000

600 (2,000 ´ .3)

49,400

$247,000

Purchasing

1,200

60 (200 ´ .3)

1,140

$ 45,600

Inspection

6,000

1,800(6000 ´.3)

4,200

$ 60,000

145. Describe how the activity-based management model combines the process and costing views. What are the

steps involved in each? What are the objectives of the activity-based management system?

146. What is responsibility accounting? Compare and contrast financial-based responsibility accounting with

activity-based responsibility accounting.