Microeconomics, 4e (Hubbard/O’Brien)

Chapter 12 Firms in Perfectly Competitive Markets

12.1 Perfectly Competitive Markets

1) Assume the market for organic produce sold at farmers’ markets is perfectly competitive. All

else equal, as more farmers choose to produce and sell organic produce at farmers’ markets, what

is likely to happen to the equilibrium price of the produce and profits of the organic farmers in

the long run?

A) The equilibrium price is likely to increase and profits are likely to remain unchanged.

B) The equilibrium price is likely to remain unchanged and profits are likely to increase.

C) The equilibrium price is likely to decrease and profits are likely to decrease.

D) The equilibrium price is likely to increase and profits are likely to increase.

2) Assume the market for organically-grown produce is perfectly competitive. All else equal, as

farmers find it less profitable to produce and sell organic produce in this market,

A) the demand curve will shift to the left and the equilibrium price will decrease.

B) the supply curve will shift to the left and the equilibrium price will increase.

C) the supply curve will shift to the right, the demand curve will shift to the left, and the

equilibrium price will decrease.

D) the supply curve will shift to the left, the demand curve will shift to the left, and the

equilibrium price will increase.

3) Which of the following is not a characteristic of a perfectly competitive market structure?

A) There are a very large number of firms that are small compared to the market.

B) All firms sell identical products.

C) There are no restrictions to entry by new firms.

D) There are restrictions on exit of firms.

4) Which of the following is not a characteristic of a monopolistically competitive market

structure?

A) There is a large number of independently acting small sellers.

B) All sellers sell products that are differentiated.

C) There are low barriers to entry of new firms.

D) Each firm must react to actions of other firms.

5) Which of the following is a characteristic of an oligopolistic market structure?

A) There are few dominant sellers.

B) Each firm sells a unique product.

C) It is easy for new firms to enter the industry.

D) Each firm need not react to the actions of rivals.

6) Which of the following is a characteristic of a monopoly?

A) It is easy for new firms to enter the market.

B) There is only one seller in the market.

C) The product is not unique.

D) The firm has no control over price.

7) Perfect competition is characterized by all of the following except

A) heavy advertising by individual sellers.

B) homogeneous products.

C) sellers are price takers.

D) a horizontal demand curve for individual sellers.

8) A very large number of small sellers who sell identical products imply

A) a multitude of vastly different selling prices.

B) a downward sloping demand for each seller’s product.

C) the inability of one seller to influence price.

D) chaos in the market.

9) Which of the following is the best example of a perfectly competitive industry?

A) wheat production

B) steel production

C) electricity production

D) airplane production

10) The price of a seller’s product in perfect competition is determined by

A) the individual seller.

B) a few of the sellers.

C) market demand and market supply.

D) the individual demander.

11) Both individual buyers and sellers in perfect competition

A) can influence the market price by their own individual actions.

B) can influence the market price by joining with a few of their competitors.

C) have to take the market price as a given.

D) have the market price dictated to them by government.

12) Both buyers and sellers are price takers in a perfectly competitive market because

A) the price is determined by government intervention and dictated to buyers and sellers.

B) each buyer and seller knows it is illegal to conspire to affect price.

C) both buyers and sellers in a perfectly competitive market are concerned for the welfare of

others.

D) each buyer and seller is too small relative to others to independently affect the market price.

13) Suppose the equilibrium price in a perfectly competitive industry is $15 and a firm in the

industry charges $21. Which of the following will happen?

A) The firm’s profits will increase.

B) The firm’s revenue will increase.

C) The firm will not sell any output.

D) The firm will sell more output than its competitors.

14) The demand curve for each seller’s product in perfect competition is horizontal at the market

price because

A) each seller is too small to affect market price.

B) the price is set by the government.

C) all the sellers get together and set the price.

D) all the demanders get together and set the price.

15) An individual seller in perfect competition will not sell at a price lower than the market price

because

A) demand for the product will exceed supply.

B) the seller would start a price war.

C) the seller can sell any quantity she wants at the prevailing market price.

D) demand is perfectly inelastic.

16) Jason, a high-school student, mows lawns for families in his neighborhood. The going rate is

$12 for each lawn-mowing service. Jason would like to charge $20 because he believes he has

more experience mowing lawns than the many other teenagers who also offer the same service.

If the market for lawn mowing services is perfectly competitive, what would happen if Jason

raised his price?

A) He would lose some but not all his customers.

B) Initially, his customers might complain but over time they will come to accept the new rate.

C) If Jason raises his price he would lose all his customers.

D) If Jason raises his price, then all others supplying the same service will also raise their prices.

17) The demand curve for an individual seller’s product in perfect competition is

A) the same as market demand.

B) downward sloping.

C) vertical.

D) horizontal.

18) In perfect competition

A) the market demand curve and the individual’s demand are identical.

B) the market demand curve is perfectly inelastic while demand for an individual seller’s product

is perfectly elastic.

C) the market demand curve is perfectly elastic while demand for an individual seller’s product is

perfectly inelastic.

D) the market demand curve is downward sloping while demand for an individual seller’s

product is perfectly elastic.

19) A perfectly competitive firm’s horizontal demand curve implies that the firm does not have to

lower its price to sell more output.

20) The market demand curve for a perfectly competitive industry is the horizontal summation of

each individual firm’s demand curve.

21) Why are individual buyers and sellers in perfect competition called price takers?

22) Consider the market for wheat which is a perfectly competitive market. Is the market demand

curve the same as the demand curve facing an individual producer? If not, explain how and why

they are different? Illustrate your answer graphically.

12.2 How a Firm Maximizes Profit in a Perfectly Competitive Market

1) If the market price is $25, the average revenue of selling five units is

A) $5.

B) $12.50.

C) $25.

D) $125.

2) If the market price is $25 in a perfectly competitive market, the marginal revenue from selling

the fifth unit is

A) $5.

B) $12.50.

C) $25.

D) $125.

3) Which of the following is not true for a firm in perfect competition?

A) Profit equals total revenue minus total cost.

B) Price equals average revenue.

C) Average revenue is greater than marginal revenue.

D) Marginal revenue equals the change in total revenue from selling one more unit.

Table 12-1

Quantity

Total Cost

(dollars)

Variable Cost

(dollars)

0

$1,000

$0

100

1,360

360

200

1,560

560

300

1,960

960

400

2,760

1,760

500

4,000

3,000

600

5,800

4,800

Table 12-1 shows the short-run cost data of a perfectly competitive firm that produces plastic

camera cases. Assume that output can only be increased in batches of 100 units.

4) Refer to Table 12-1. What is the fixed cost of production?

A) $0

B) $500

C) $1,000

D) It cannot be determined.

5) Refer to Table 12-1. If the market price of each camera case is $8, what is the profit–

maximizing quantity?

A) 300 units

B) 400 units

C) 500 units

D) 600 units

6) Refer to Table 12-1. If the market price of each camera case is $8, what is the firm’s total

revenue?

A) $2,400

B) $3,200

C) $4000

D) $4,800

7) Refer to Table 12-1. If the market price of each camera case is $8 and the firm maximizes

profit, what is the amount of the firm’s profit or loss?

A) $0 (it breaks even)

B) loss of $1,000

C) profit of $440

D) loss of $440

8) Refer to Table 12-1. Suppose the fixed cost of production rises by $500 and the price per unit

is still $8. What happens to the firm’s profit-maximizing output level?

A) It must fall.

B) It must rise to offset the increased cost.

C) It will remain the same.

D) The firm will shut down.

9) Refer to Table 12-1. The firm will not produce in the short run if the output price falls below

A) $8.

B) $4.

C) $3.20.

D) $2.80.

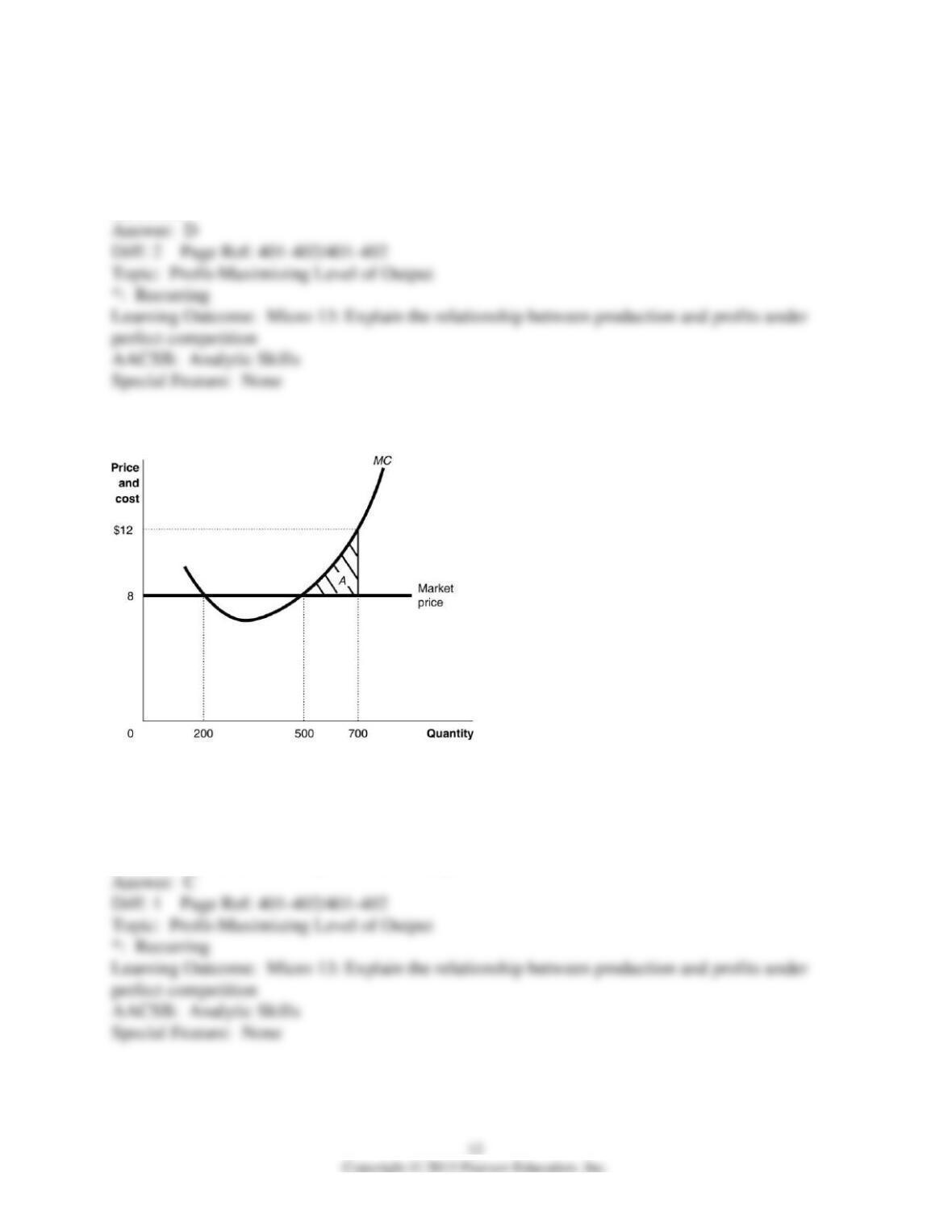

Figure 12-1

10) Refer to Figure 12-1. If the firm is producing 700 units,

A) it is making a profit.

B) it is making a loss.

C) it should cut back its output to maximize profit.

D) it should increase its output to maximize profit.

11) Refer to Figure 12-1. If the firm is producing 700 units, what is the amount of its profit or

loss?

A) loss of $280

B) loss equivalent to the area A

C) profit equivalent to the area A

D) There is insufficient information to answer the question.

12) Refer to Figure 12-1. If the firm is producing 200 units,

A) it breaks even.

B) it is making a loss.

C) it should cut back its output to maximize profit.

D) it should increase its output to maximize profit.

13) A perfectly competitive firm produces 3,000 units of a good at a total cost of $36,000. The

price of each good is $10. Calculate the firm’s short-run profit or loss.

A) loss of $6,000

B) profit of $6,000

C) profit of $30,000

D) There is insufficient information to answer the question.

14) If, for the last unit of a good produced by a perfectly competitive firm, MR > MC, then in

producing it, the firm

A) added more to total costs than it added to total revenue.

B) added more to total revenue than it added to total cost.

C) is maximizing marginal profit.

D) has minimized its losses.

15) If, for a perfectly competitive firm, price exceeds the marginal cost of production, the firm

should

A) increase its output.

B) reduce its output.

C) keep output constant and enjoy the above normal profit.

D) lower the price.

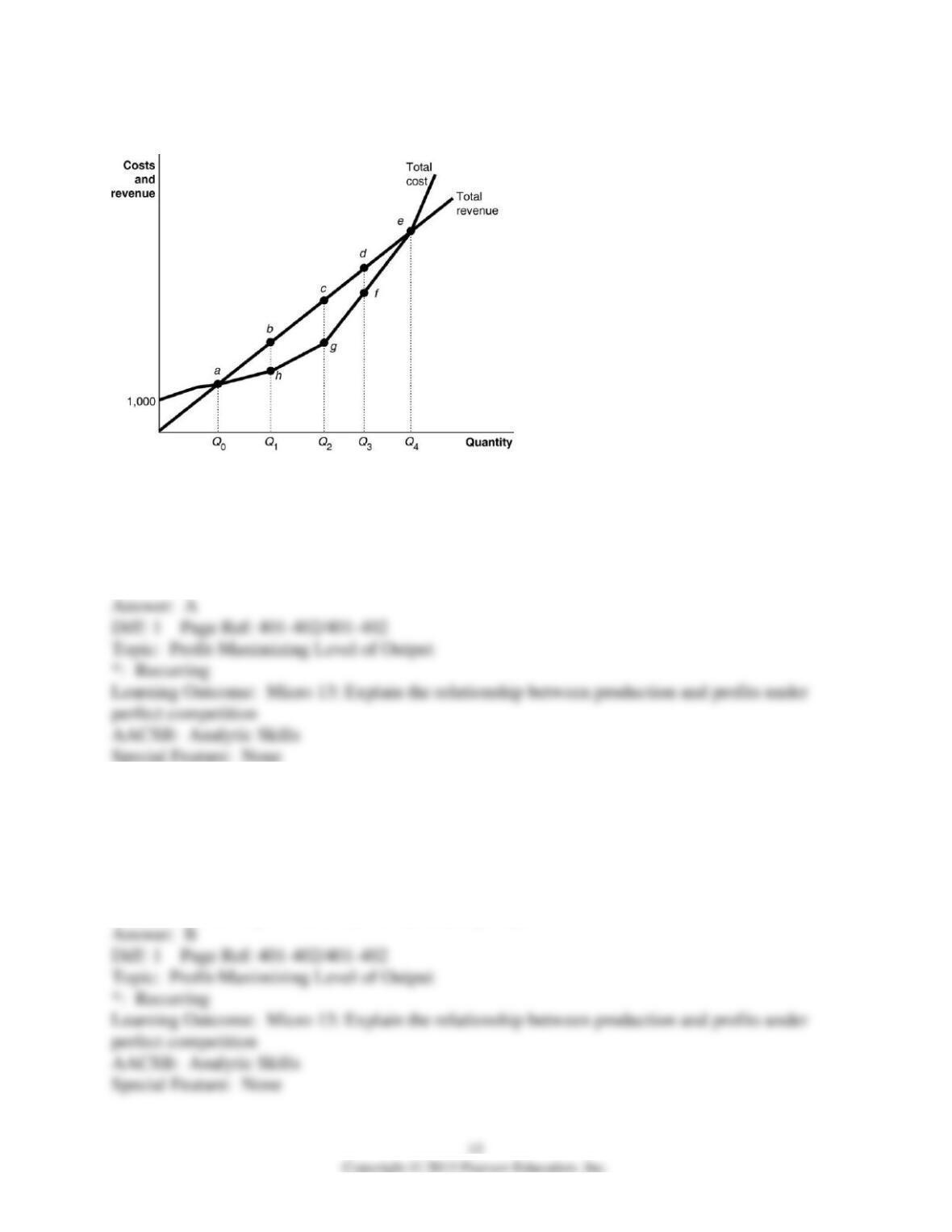

Figure 12-2

16) Refer to Figure 12-2. What is the amount of profit if the firm produces Q2 units?

A) It is equal to the vertical distance c to g.

B) It is equal to the vertical distance c to Q2.

C) It is equal to the vertical distance g to Q2.

D) It is equal to the vertical distance c to g multiplied by Q2 units.

17) Refer to Figure 12-2. Suppose the firm is currently producing Q2 units. What happens if it

expands output to Q3 units?

A) Its profit increases by the size of the vertical distance df.

B) It makes less profit.

C) It incurs a loss.

D) It will be moving toward its profit maximizing output.

18) Refer to Figure 12-2. The firm breaks even at an output level of

A) Q1 units.

B) Q2 units.

C) Q3 units.

D) Q4 units.

19) Refer to Figure 12-2. What happens if the firm produces more than Q4 units?

A) Its profit increases.

B) It makes a loss.

C) Its total revenue is increasing faster than its total cost.

D) It could make a profit or a loss depending on what happens to demand.

20) Refer to Figure 12-2. Why is the total revenue curve a ray from the origin?

A) because revenue increases at an increasing rate

B) because revenue increases at a decreasing rate

C) because the firm can sell its product at a constant price

D) because the firm must lower its price to sell more

21) In a graph with output on the horizontal axis and total revenue on the vertical axis, what is

the shape of the total revenue curve for a perfectly competitive seller?

A) U-shaped

B) inverted U-shaped

C) a horizontal line

D) a ray from the origin

22) For a perfectly competitive firm, which of the following is not true at profit maximization?

A) Market price is greater than marginal cost.

B) Marginal revenue equals marginal cost.

C) Total revenue minus total cost is maximized.

D) Price equals marginal cost.

23) Assume that price is greater than average variable cost. If a perfectly competitive seller is

producing at an output where price is $11 and the marginal cost is $14.54, then to maximize

profits the firm should

A) continue producing at the current output.

B) produce a larger level of output.

C) produce a smaller level of output.

D) There is not enough information given to answer the question.

24) An increase in a firm’s fixed cost will not change the firm’s profit-maximizing output in the

short run.

25) A perfectly competitive firm’s marginal revenue curve is downward sloping.

26) Assume that price is greater than average variable cost. If a perfectly competitive firm is

producing at an output where price is $114 and the marginal cost is $102, then the firm is

probably producing more than its profit-maximizing quantity.

27) How are market price, average revenue, and marginal revenue related for a perfectly

competitive firm and why?

19

28) Assuming a market price of $4, fill in the columns in the following table. What is the profit-

maximizing level of production? What are the two ways to determine the profit-maximizing

level of production?

Quantity

Total

Revenue

(TR)

Total

Cost

(TC)

Profit

Marginal

Revenue

(MR)

Marginal

Cost (MC)

0

3

1

5

2

6

3

9

4

14

5

20

6

28

7

40

Answer:

Marginal

Revenue

0

0

3

-3

—

—

1

4

5

-1

4

2

2

8

6

2

4

1

12

9

3

4

3

4

16

14

2

4

5

5

20

20

0

4

6

6

24

28

-4

4

8

7

12.3 Illustrating Profit or Loss on the Cost Curve Graph

1) A firm’s total profit can be calculated as all of the following except

A) total revenue minus total cost.

B) average profit per unit times quantity sold.

C) (price minus average total cost) times quantity sold.

D) marginal profit times quantity sold.

2) If a perfectly competitive firm’s price is above its average total cost, the firm

A) is earning a profit.

B) should shut down.

C) is incurring a loss.

D) is breaking even.