Chapter 11 – Flexible Budgets and Overhead Analysis

Direct labor:

Actual hours worked

12,000 hrs.

Standard hours allowed for actual production

10,000 hrs.

Average actual labor cost per hour

$18.00

The overhead rate is based on a normal volume of 12,000 direct labor hours. Standard cost data at 12,000 direct labor

hours were as follows:

Variable overhead

$48,000

Fixed overhead

24,000

Total overhead

$72,000

What is the fixed overhead spending variance for Griffen?

a.

$2,000 U

b.

$8,000 U

c.

$4,000 U

d.

$20,000 U

$26,000 − $24,000 = $2,000 U

114. Crawford Company’s standard fixed overhead cost is $6.00 per direct labor hour based on budgeted fixed costs of

$600,000. The standard allows 1 direct labor hours per unit. During 2011, Crawford produced 110,000 units of product,

incurred $630,000 of fixed overhead costs, and recorded 212,000 actual hours of direct labor.

What is the activity level on which Crawford based its fixed overhead rate?

a.

110,000 direct labor hours

b.

105,000 direct labor hours

c.

100,000 direct labor hours

d.

50,000 direct labor hours

115. If actual fixed overhead was $54,000 and there was a $1,300 unfavorable spending variance and a $1,000

unfavorable volume variance, budgeted fixed overhead must have been

a.

$56,300.

b.

$50,300.

c.

$53,000.

d.

$52,700.

116. Fixed overhead was budgeted at $200,000, and 25,000 direct labor hours were budgeted. If the fixed overhead

volume variance was $8,000 favorable and the fixed overhead spending variance was $6,000 unfavorable, fixed overhead

applied must be

a.

$208,000.

b.

$206,000.

c.

$202,000.

Chapter 11 – Flexible Budgets and Overhead Analysis

d.

$194,000.

117. Gina Production Company uses a standard costing system. The following information pertains to 2011:

Actual overhead costs ($16,500 is fixed)

$ 40,125

Actual direct labor costs (11,250 hours)

$131,625

Standard direct labor for 5,500 units:

Standard hours allowed

11,000 hours

Labor rate

$12.00

The overhead rate is based on an activity level of 10,000 hours. Standard cost data for 5,000 units is as follows:

Variable overhead

$22,500

Fixed overhead

13,500

Total overhead

$36,000

What is the fixed overhead volume variance for Gina Production Company?

a.

$1,350 F

b.

$3,600 F

c.

$4,125 U

d.

$1,350 U

118. An activity-budgetary system has the following benefit(s):

a.

it supports continuous improvement.

b.

it supports process management.

c.

it emphasizes cost reduction through elimination of wasteful activities.

d.

it helps improve the efficiency of necessary activities.

e.

all of these.

e

119. Which of the following is not one of the steps in building an activity-based budget?

a.

identifying activities

b.

classifying activities as value-added or nonvalue-added

c.

estimating the demand for each activity’s output

d.

estimating the cost of producing the output demanded by each activity

e.

None of these.

120. The major differences between activity-based budgeting and traditional budgeting are found in

a.

the materials and labor categories.

b.

the sales and production budgets.

c.

the cash budget.

d.

the overhead and selling and administrative categories.

Chapter 11 – Flexible Budgets and Overhead Analysis

e.

None of these.

121. In budgeting at the activity level, the cost behavior of each activity is defined with respect to

a.

direct labor hours.

b.

machine hours.

c.

the activity output measure.

d.

the activity’s resource driver.

e.

None of these.

122. In an activity framework controlling costs translates into

a.

managing activities.

b.

reducing direct labor hours.

c.

selling more goods.

d.

careful identification of resource drivers.

e.

All of these.

123. Activity flexible budgeting

a.

improves performance reporting.

b.

allows the prediction of activity costs as activity output changes.

c.

enhances the ability to manage activities.

d.

improves the ability to plan and monitor activity improvements.

e.

does all of these.

124. Activity flexible budgeting provides a more accurate prediction of costs than a traditional flexible budgeting

approach because

a.

costs often vary with more than one driver.

b.

nonunit level drivers are often not highly correlated with direct labor hours.

c.

direct labor hours are often not measured correctly.

d.

costs often vary with more than one driver and nonunit level drivers are often not highly correlated with direct

labor hours.

e.

costs often vary with more than one driver and direct labor hours are not correct.

125. A performance report using activity flexible budgeting compares

a.

budgeted costs for actual activity usage levels with the actual activity costs.

b.

actual activity costs with budgeted overhead costs.

c.

actual overhead costs with the budgeted activity costs for actual activity usage levels.

d.

the static activity budget costs with the budgeted activity costs for the actual activity usage levels.

e.

None of these.

Chapter 11 – Flexible Budgets and Overhead Analysis

126. For activity flexible budgeting, a cost formula is developed for each

a.

overhead item as a function of direct labor hours.

b.

activity as a function of activity drivers.

c.

activity as a function of resource drivers.

d.

overhead item as a function of resource drivers.

e.

each activity as a function of direct labor hours.

127. In an activity flexible budget, the variable cost component typically corresponds to

a.

those resources that vary with direct labor hours.

b.

resources acquired as needed.

c.

resources acquired in advance of usage.

d.

resources that do not change as the activity output changes.

e.

None of these.

128. In an activity flexible budget, the fixed cost component typically corresponds to

a.

resources that vary with direct labor hours.

b.

resources that vary as the activity output changes.

c.

resources acquired in advance of usage.

d.

resources acquired as needed.

e.

None of these.

129. Building an activity-based budget requires

a.

the activities within an organization to be identified.

b.

the demand for each activity‘s output to be estimated.

c.

the cost of resources required to produce this activity output to be assessed.

d.

All of these.

e.

None of these.

130. If an organization has implemented an ABC or ABM system, they will already have accomplished which of the

following?

a.

Identified the activities within an organization.

b.

Estimated the demand for each activity’s output.

c.

Assessed the cost of resources required to produce this activity output.

d.

All of these.

e.

None of these.

Chapter 11 – Flexible Budgets and Overhead Analysis

131. The major differences between functional and activity-based budgeting are found within which of the following

categories?

a.

overhead

b.

selling

c.

administration

d.

All of these.

e.

None of these.

132. Activity-based budgeting

a.

builds a budget for each function.

b.

identifies only the overhead activity.

c.

classifies costs as variable or fixed with respect to the activity output measure.

d.

All of these.

e.

None of these.

Figure 11–5.

Merric Company uses an activity-based costing system. Four activities have been identified. The setup activity uses the

number of setups as its cost driver. The following budget information is available for this activity:

Fixed costs per month

$240,000

Variable cost per setup

5,400

The company expects to perform 25 setups in May.

133. Refer to Figure 11–5. If the company expects 25 setups in the month of May, what would be the total budgeted costs

of the setup activity?

a.

$240,000

b.

$375,000

c.

$135,000

d.

$397,500

e.

None of these.

Fixed costs

$240,000

Variable costs ($5,400 × 25)

Total

$375,000

134. Refer to Figure 11–5. Actual costs incurred were $246,000 fixed and $144,000 variable. If the actual number of

setups in May was 30, what is the activity-based flexible budget variance?

a.

$15,000 U

b.

$15,000 F

c.

$12,000 F

Chapter 11 – Flexible Budgets and Overhead Analysis

d.

$12,000 U

Fixed costs

Variable costs

Total

Figure 11–6.

Kyle Company uses forklifts to move materials from the storage area to the production floor. There are five forklifts. They

are fully used 20 hours per day (making 8 moves per hour). The company works 320 days per year, running two 7-hour

shifts per day. Fork-lift operators work 1,800 hours per year and are paid an annual salary of $56,000.

Based on a recent study each forklift uses 0.45 gallons of fuel per move. The cost of fuel is $3.80 per gallon.

135. Refer to Figure 11–6. Prepare a salary budget for the activity, moving materials. Assume that the labor market does

not permit the hiring of part-time forklift operators.

a.

$980,000

b.

$1,008,000

c.

$905,000

d.

$1,135,000

e.

$760,000

operators

Budgeted salaries = 18 × $56,000 = $1,008,000

136. Refer to Figure 11–6. Calculate the fuel budget for the year for moving materials.

a.

$436,090

b.

$228,300

c.

$496,050

d.

$312,100

e.

$437,760

Moves = 5 × 20 × 8 × 320 = 256,000

Fuel cost = 0.45 × 256,000 × $3.80 = $437,760

137. Refer to Figure 11–6. Prepare a flexible budget formula for the moving materials activity.

a.

$880,000 + ($1.71 × moves)

b.

$1,450,000 + ($3.80 × moves)

c.

$905,000 + ($0.45 × moves)

d.

$1,008,000 + ($1.71 × moves)

e.

$850,000 + ($2.00 × moves)

Fixed costs = 18 × $56,000 = $1,008,000

Variable cost = 0.45 × $3.80 = $1.71 per move

Chapter 11 – Flexible Budgets and Overhead Analysis

138. Refer to Figure 11–6. Suppose that the actual moves made are 80% of the forklifts’ capacity. What is the after-the-fact

budgeted fuel cost?

a.

$448,000

b.

$299,600

c.

$492,000

d.

$353,600

e.

$350,208

Moves = 5 × 20 × 8 × 320 = 256,000

After-the-fact budgeted fuel cost = 0.80 × 256,000 × 0.45 × $3.80 = $350,208

Figure 11–7.

Larry Miller, controller for Kipling Company, has been instructed to develop a flexible budget for overhead costs. The

company produces two types of frozen desserts: Icey and Tasty. The two desserts use common raw materials in different

proportions. The company expects to produce 200,000 gallons of each product during the coming year. Icey requires 0.25

direct labor hour per gallon and Tasty requires 0.30. Larry has developed the following fixed and variable costs for each

of the four overhead items:

Overhead Item

Fixed Cost

Variable Rate per DLH

Maintenance

$52,000

$1.20

Power

1.50

Indirect labor

79,500

4.80

Rent

54,000

139. Refer to Figure 11–7.

Required:

A.

Prepare an overhead budget for the expected activity level for the coming year.

B.

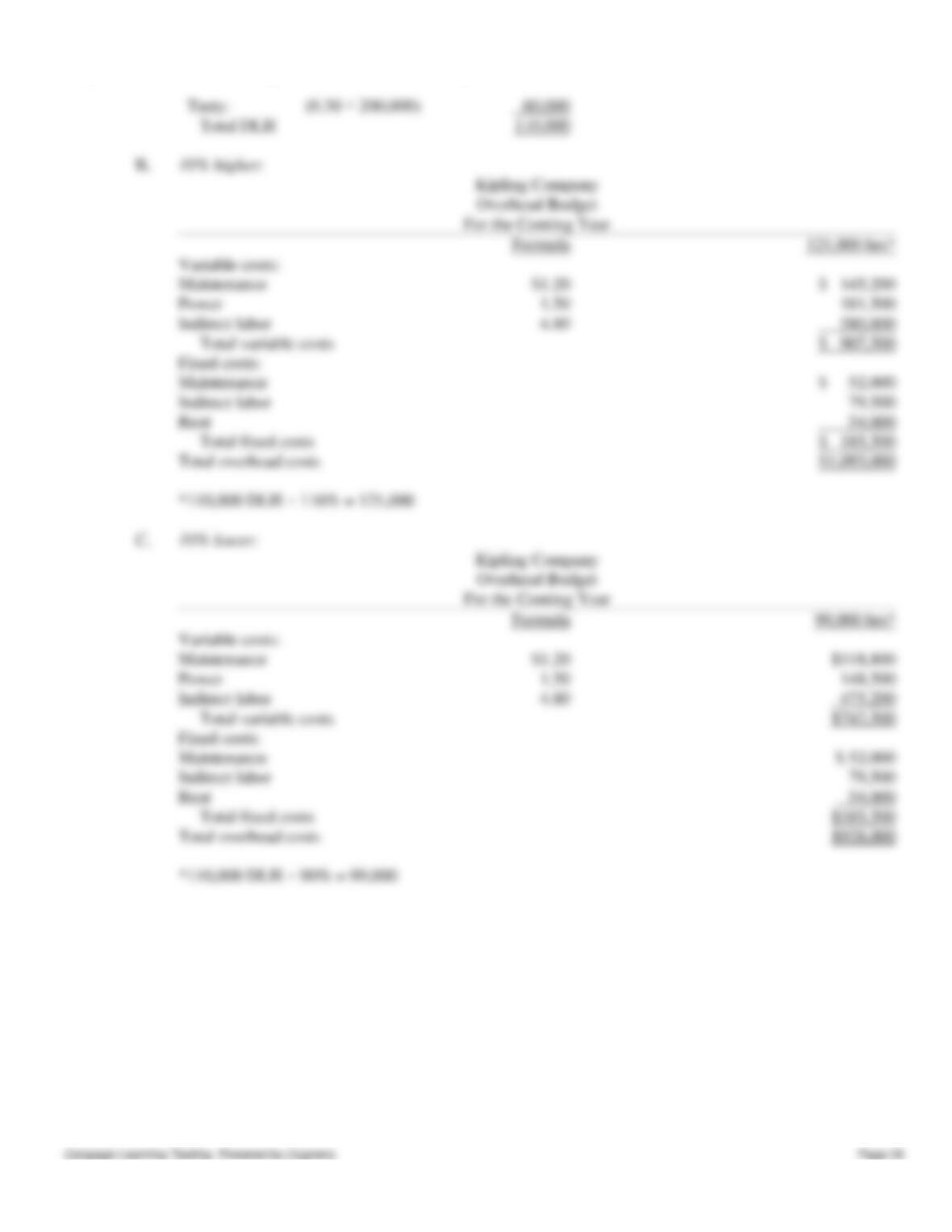

Prepare an overhead budget that reflects production that is 10% higher than expected (for

both products). Assume this quantity is within the relevant range.

C.

Prepare an overhead budget that reflects production that is 10% lower than expected (for

both products). Assume this quantity is within the relevant range.

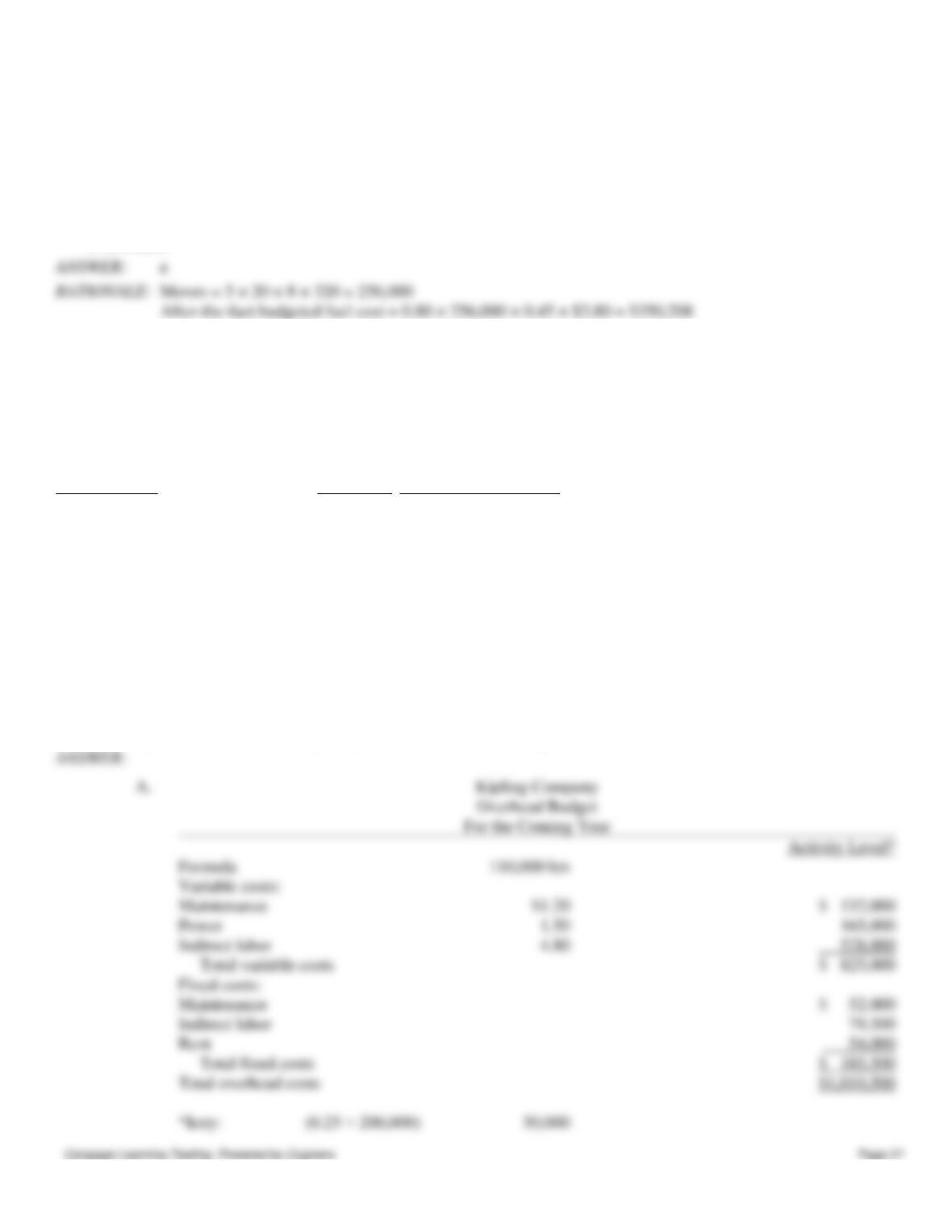

A.

Formula

Variable costs:

Maintenance

Power

Indirect labor

Total variable costs

Fixed costs:

Maintenance

Indirect labor

Rent

Total fixed costs

Total overhead costs

*Icey:

(0.25 × 200,000)

Chapter 11 – Flexible Budgets and Overhead Analysis

140. Refer to Figure 11–7. Assume that Kipling actually produced 240,000 gallons of Icey and 200,000 of Tasty. The

actual overhead costs incurred were:

Maintenance

$192,000

Power

181,700

Indirect labor

649,500

Rent

54,000

Required:

A.

Prepare a performance report for the period.

B.

Based on the report, would you judge any of the variances to be significant? Discuss

some possible reasons for the variances.

Tasty:

(0.30 × 200,000)

Total DLH

Variable costs:

Maintenance

Power

Indirect labor

Total variable costs

Fixed costs:

Maintenance

Indirect labor

Rent

Total fixed costs

Total overhead costs

*110,000 DLH × 110% = 121,000

Variable costs:

Maintenance

Power

Indirect labor

Total variable costs

Fixed costs:

Maintenance

Indirect labor

Rent

Total fixed costs

Total overhead costs

*110,000 DLH × 90% = 99,000

Chapter 11 – Flexible Budgets and Overhead Analysis

Production costs*:

Maintenance

Power

Indirect labor

Rent

Total costs

*Flexible budget amounts are based on 120,000 DLH:

(0.25 × 240,000) + (0.30 × 200,000) = 120,000 DLH

Power:

$1.50 × 120,000

increase. An investigation would be needed to know exactly why the variances occurred.

141. Favor Company budgeted the following amounts:

Variable costs of production:

Direct materials

6 pounds @ $1.25 per pound

Direct labor

0.75 hours @ $16.00 per hour

Variable overhead

0.75 hours @ $2.65 per hour

Fixed overhead:

Materials handling

$9,000

Depreciation

$2,300

Required: Prepare a flexible budget for 1,500 units, 1,800 units and 2,100 units. Assume all are within the relevant range

and round to the nearest dollar.

Direct materials

Direct labor

Variable overhead

Fixed overhead:

Materials handling

Depreciation

142. Vallo Pharmacy operates a home delivery service with more than 2,000 housebound clients. Vallo has a fleet of

Chapter 11 – Flexible Budgets and Overhead Analysis

vehicles and has invested in a sophisticated computerized communications system to coordinate its deliveries. Vallo has

gathered the following data on last year’s operations:

Deliveries made:

21,000

Direct labor:

15,000 delivery hours at $8.00

Actual variable overhead:

$145,000

Vallo uses a standard costing system. During the year, the following variable overhead rate was used: $8.10 per delivery

hour. The labor standard requires 0.75 hours per delivery.

Compute the variable overhead spending variance and the variable overhead efficiency variance.

VOH spending variance

= AVOH − (SVOR × AH)

= $145,000 − ($8.10 × 15,000)

= $145,000 − $121,500

= $23,500 U

VOH efficiency variance

= (AH − SH) × SVOR

= (15,000 − 15,750) × $8.10

= $6,075 F

143. A company had the following information for the year:

Standard variable overhead rate (SVOR) per direct labor hour

$6.75

Standard hours (SH) allowed per unit

4

Actual production

17,400

Actual variable overhead costs

$478,000

Actual direct labor hours

69,800

Required:

A. Calculate the actual variable overhead rate (AVOR).

B. Calculate the applied variable overhead.

C. Calculate the total variable overhead variance.

Applied variable overhead = actual units × SH × SVOR

17,400 × 4 × $6.75 = $469,800

Actual variable overhead

Applied variable overhead

Total variable overhead variance

U

Chapter 11 – Flexible Budgets and Overhead Analysis

144. Gallant Company uses standard costing. Overhead is applied to products on the basis of standard direct labor hours

for actual production. Data for Gallant follows:

Standard direct labor hours allowed for actual output

110,000

Actual direct labor hours

115,000

Direct labor hours budgeted in the master budget

120,000

Budgeted total variable overhead cost

$360,000

Actual variable overhead cost

$328,000

A.

Calculate the variable overhead rate.

B.

Calculate the total variable overhead applied to production.

C.

Calculate the variable overhead spending variance.

D.

Calculate the variable overhead efficiency variance.

E.

Calculate the total variable overhead variance.

A.

Variable overhead rate = $360,000 / 120,000 = $3.00 per direct labor hour

B.

Variable overhead applied to production = $3.00 × 110,000 = $330,000

C.

Variable overhead spending variance = $328,000 − ($3.00 × 115,000) = $17,000 F

D.

Variable overhead efficiency variance

= ($3.00 × 115,000) − ($3.00 × 110,000)

= $15,000 U

OR

E.

Total variable overhead variance = $17,000 F + $15,000 U = $2,000 F

145. A company provided the following data:

Standard fixed overhead rate (SFOR)

$13.00 per direct labor hour

Actual fixed overhead costs

$385,800

Standard hours allowed per unit

2

Actual production

15,000 units

Required:

A. Calculate the standard hours allowed for actual production.

B. Calculate the applied fixed overhead

C. Calculate the total fixed overhead variance

A.

Standard hours for actual units = SH per unit × actual units produced

2 × 15,000 = 30,000

B.

Applied fixed overhead = Standard hours for actual units × SFOR

30,000 × $13.00 = $390,000

Actual fixed overhead

Applied fixed overhead

Total fixed overhead variance