Chapter 11 – Flexible Budgets and Overhead Analysis

146. Littleton Company uses a standard costing system. The following monthly cost functions apply to its manufacturing

overhead items:

Overhead Item

Cost Function

Indirect materials

$0.80 per DLH

Indirect labor

$1.00 per DLH

Utilities

$0.40 per DLH

Insurance

$8,000

Depreciation

$32,000

Information for the month of October is as follows:

Actual overhead costs incurred:

Indirect materials

$20,800

Indirect labor

24,000

Utilities

9,600

Insurance

8,800

Depreciation

32,000

Total

$95,200

Actual direct labor hours worked

24,000

Standard direct labor hours allowed for production achieved

27,000

Littleton uses expected capacity to calculate standard overhead rates. The monthly expected capacity is 25,000 hours.

A.

Calculate the following standard overhead rates based upon expected capacity:

Variable overhead rate

Fixed overhead rate

Total overhead rate

B.

Calculate the following variances:

Variable overhead spending variance

Variable overhead efficiency variance

Fixed overhead spending variance

Fixed overhead volume variance

A.

Variable overhead rate = $0.80 + $1.00 + $0.40 = $2.20 per DLH

Fixed overhead rate = ($8,000 + $32,000) / 25,000 = $1.60 per DLH

Total overhead rate = $2.20 + $1.60 = $3.80 per DLH

B.

Variable overhead spending variance:

(AVOH − SVOR) × AH

= ($20,800 + $24,000 + $9,600) −

(24,000 hours × $2.20)

= $54,400 − $52,800

= $1,600 U

Variable overhead efficiency variance:

(AH − SH) × SVOR

= (24,000 − 27,000) × $2.20

= $6,600 F

Fixed overhead spending variance:

AFOH − BFOH

= ($40,800 − $40,000)

= $800 U

Chapter 11 – Flexible Budgets and Overhead Analysis

147. The following standard overhead costs were developed for one of the products of Mildey Company:

Variable overhead:

5 hours × $4.00 per hour

20.00

Fixed overhead:

5 hours × $15.00 per hour

75.00

Total standard overhead cost per unit

$95.00

The following information is available regarding the company’s operations for the period:

Units produced

20,000

Direct labor

115,000 hours

Overhead incurred:

Variable

$437,500

Fixed

$1,320,000

Budgeted fixed overhead for the period is $1,350,000, and the standard fixed overhead rate is based on expected capacity

of 90,000 direct labor hours.

Required:

A.

Calculate the variable overhead spending variance and indicate whether it is favorable or

unfavorable.

B.

Calculate the variable overhead efficiency variance and indicate whether it is favorable or

unfavorable.

C.

Calculate the fixed overhead spending variance and indicate whether it is favorable or

unfavorable.

D.

Calculate the fixed overhead volume variance and indicate whether it is favorable or

unfavorable.

A.

$437,500 − (115,000 × $4.00)

B.

[115,000 − (20,000 units × 5 hours )] × $4.00

C.

$1,320,000 − $1,350,000

D.

$1,350,000 − (20,000 units × 5 hours × $15.00)

148. At the beginning of the year, Folsom Company had the following standard cost sheet for one of its food products:

Direct materials (10 lb @ 3.20)

$32.00

Direct labor (4 hr @ $9.00)

36.00

Fixed overhead (4 hr @ $4.00)

16.00

Variable overhead (4 hr @ $0.75)

3.00

Standard cost per unit

$87.00

Folsom computes its overhead rates using practical capacity, which is 72,000 units. The actual results for the year are:

Units produced

70,000

Direct labor hours

290,000

Actual wage per hour

$9.05

Fixed overhead

$1,160,000

Variable overhead

$218,000

A.

Compute the fixed overhead spending and volume variances.

B.

Compute the variable overhead spending and efficiency variances.

Fixed overhead volume variance:

(BFOH − SH) × SFOR

= $40,000 − (27,000 hours × $1.60)

= $3,200 F

Chapter 11 – Flexible Budgets and Overhead Analysis

A.

Actual FOH

Budgeted FOH

Applied FOH

$8,000 U

$32,000 U

B.

VOH Spending variance

= AVOH − (SVOR × AH)

= $218,000 − ($0.75 × 290,000)

= $500 U

VOH efficiency variance

= (AH − SH) × SVOR

= (290,000 − 280,000) × $0.75

= $7,500 U

149. Bushman Company is planning to produce 3,200,000 carburetors for the coming year. Each carburetor requires 0.375

standard hours of labor for completion. The company uses direct labor hours to assign overhead to products. The total

fixed overhead budgeted for the coming year is $1,980,000. Total budgeted overhead is $4,050,000. Predetermined

overhead rates are calculated using expected production, measured in direct labor hours. Actual results for the year follow:

Actual production (units)

3,540,000

Actual direct labor hours

1,190,000

Actual fixed overhead

$1,920,000

Actual variable overhead

$2,150,000

Required:

A.

Compute the applied fixed overhead.

B.

Compute the fixed overhead spending and volume variances.

C.

Compute the applied variable overhead.

D.

Compute the variable overhead spending and efficiency variances. Carry per hour

computations out to 3 decimals.

A.

Fixed overhead rate (SFOR) = $1,980,000 / (0.375 × 3,200,000) = $1.65 per DLH

Applied FOH = $1.65 × 1,327,500 = $2,190,375

B.

FOH spending variance

= AFOH − BFOH

= $1,920,000 − $1,980,000

= $60,000 F

FOH volume variance

= BFOH − (SFOR × SH)

= $1,980,000 − $2,190,375

= $210,375 F

C.

SVOR = ($4,050,000 − $1,980,000) / 1,200,000 = $1.725 per DLH

Applied VOH

= $1.725 × 1,327,500

= $2,289,938 (rounded)

D.

VOH spending variance

= AVOH − (SVOR × AH)

= $2,150,000 − ($1.725 × 1,190,000)

= $97,250 U

Chapter 11 – Flexible Budgets and Overhead Analysis

150. Gallant Company uses standard costing. Overhead is applied to products on the basis of standard direct labor hours

for actual production. Data for Gallant follows:

Standard direct labor hours allowed for actual output

110,000

Actual direct labor hours

115,000

Direct labor hours budgeted in the master budget

120,000

Budgeted total fixed overhead cost

$210,000

Actual fixed overhead cost

$208,000

A.

Calculate the fixed overhead rate.

B.

Calculate the total fixed overhead applied to production.

C.

Calculate the fixed overhead spending variance.

D.

Calculate the fixed overhead volume variance.

E.

Calculate the total fixed overhead variance.

A.

Fixed overhead rate = $210,000 / 120,000 = $1.75

B.

Fixed overhead applied to production = $1.75 × 110,000 = $192,500

C.

Fixed overhead spending variance = $208,000 − $210,000 = $2,000 F

D.

Fixed overhead volume variance = $210,000 − $192,500 = $17,500 U

E.

Total fixed overhead variance = $2,000 F + $17,500 U = $15,500 U

151. The following costs were developed for one of the products of Larry Corporation:

Variable overhead: 8 hours × $8.00 per hour

$64.00

Fixed overhead: 8 hours × $12 per hour

$96.00

The following information is available regarding the company’s operations for the period:

Units produced:

11,000

Direct labor:

84,000 hours costing $840,000

Overhead incurred:

Variable

$756,000

Fixed

$1,000,000

Budgeted fixed overhead for the period is $960,000, and the standard fixed overhead rate is based on expected capacity of

80,000 direct labor hours.

Required:

A.

Calculate the variable overhead spending variance.

B.

Calculate the variable overhead efficiency variance.

C.

Calculate the fixed overhead spending variance.

D.

Calculate the fixed overhead volume variance.

A.

$84,000 U

$756,000 − (84,000 × $8.00)

B.

$32,000 F

(84,000 × $8.00) − (11,000 × 8 × $8.00)

C.

$40,000 U

($1,000,000 − $960,000)

D.

$96,000 F

$960,000 − (11,000 × 8 × $12.00)

VOH efficiency variance

= (AH − SH) × SVOR

= (1,190,000 − 1,327,500) × $1.725

= $237,188 F (rounded)

Chapter 11 – Flexible Budgets and Overhead Analysis

152. Mills Company uses standard costing for direct materials and direct labor. Management would like to use standard

costing for variable and fixed overhead.

The following monthly cost functions were developed for overhead items:

Overhead Item

Cost Function

Indirect materials

$1.00 per DLH

Indirect labor

$1.25 per DLH

Utilities

$0.50 per DLH

Insurance

$10,000

Depreciation

$40,000

The cost functions are considered reliable within a relevant range of 20,000 to 40,000 direct labor hours. The company

expects to operate at 25,000 direct labor hours per month.

Information for the month of June is as follows:

Actual overhead costs incurred:

Indirect materials

$ 20,000

Indirect labor

30,000

Utilities

12,000

Insurance

11,000

Depreciation

40,000

Total

$113,000

Actual direct labor hours worked:

24,000

Standard direct labor hours allowed for production achieved:

27,000

Required:

A.

Calculate the following overhead rates based upon expected capacity:

1.

Variable overhead

2.

Fixed overhead rate

3.

Total overhead rate

B.

Calculate the following variances:

1.

Variable overhead spending variance

2.

Variable overhead efficiency variance

3.

Fixed overhead spending variance

4.

Fixed overhead volume variance

A.

1.

SVOR:

$2.75/DLH

($1.00 + $1.25 + $0.50)

2.

SFOR:

$2.00/DLH

($10,000 + $40,000) / 25,000

3.

Total mfg. oh. rate:

$4.75/DLH

($2.75 + $2.00)

B.

1.

Variable overhead spending variance

($20,000 + $30,000 + $12,000) − (24,000 × $2.75) = $4,000 F

Chapter 11 – Flexible Budgets and Overhead Analysis

Fixed overhead spending variance

($51,000* − $50,000) = $1,000 U

Fixed overhead volume variance

$50,000 − (27,000 × $2.00) = $4,000 F

Figure 11–8.

Booth Inc. uses three delivery trucks to transport finished parts from its plant to the plants of its customers. The delivery

trucks are obtained through a 5-year operating lease that costs $12,000 per year per truck. Booth employs 6 drivers who

receive an average salary of $36,000 per year, including benefits. Parts are placed in boxes and placed in the trucks. Each

truck holds 20 boxes. The average round-trip distance for a delivery is 40 miles. The boxes are retained by the customers.

Each box costs $2.00. Fuel for the trucks costs $1.80 per gallon. A gallon of gas is used every 20 miles. A driver can

travel 160 miles in an eight-hour shift. Each driver works 40 hours per week and 50 weeks per year.

153. Refer to Figure 11–8. Prepare an annual budget for the activity, assuming that all of the capacity of the activity is

used (use miles as the activity driver). Identify which resources you would treat as fixed costs and which would be viewed

as variable costs.

Resource

Salaries

$216,000

$216,000

Lease

36,000

36,000

Boxes*

240,000

Fuel**

21,600

Total

$252,000

$513,600

**$1.80 / 20

154. Refer to Figure 11–8. Assume that the company uses only 90% of the activity capacity. The actual costs incurred at

this level were:

Salaries

$252,000

Lease

36,000

Boxes

200,000

Fuel

20,400

A.

What is the budget for this level of activity?

B.

Prepare a performance report.

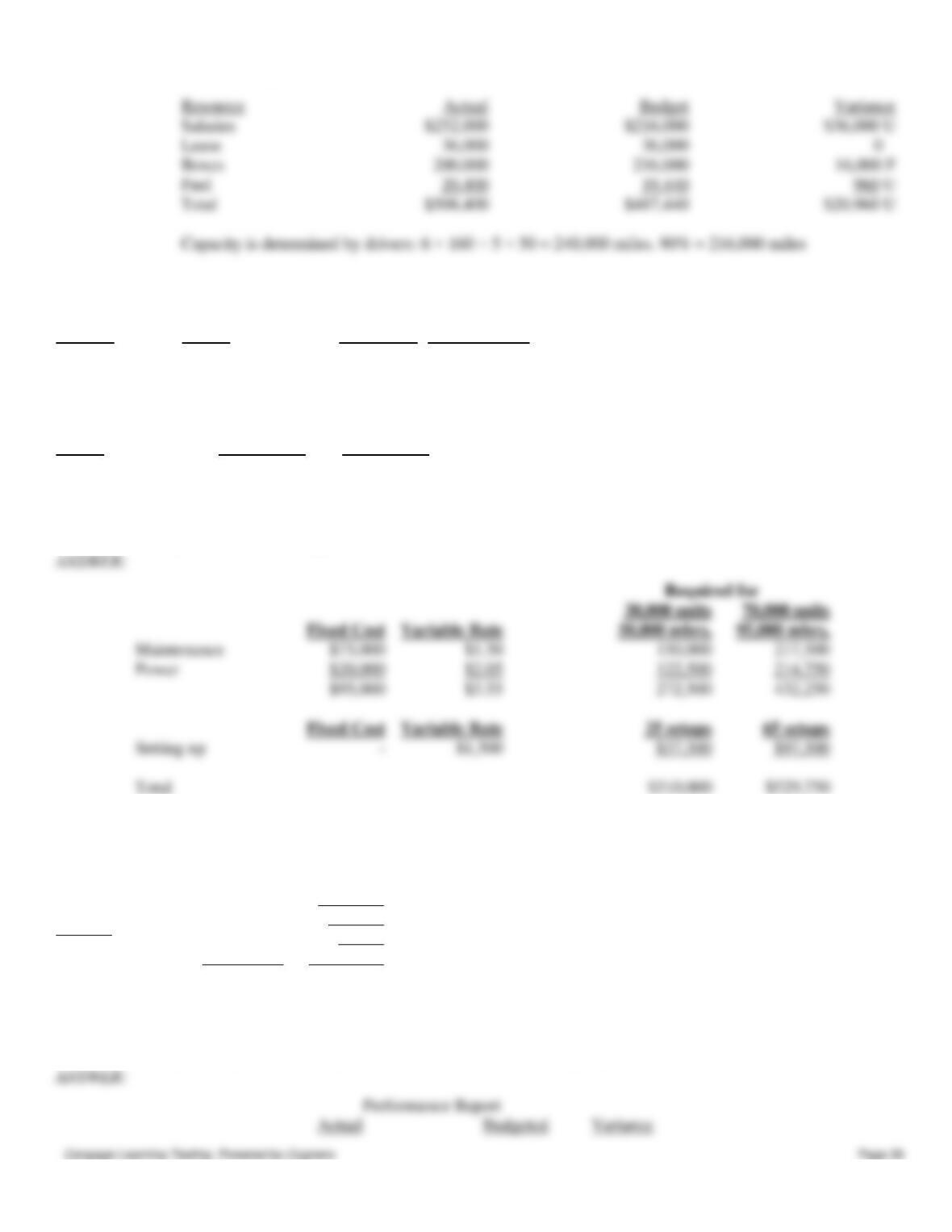

A.

Resource

Salaries

Lease

Boxes

Fuel

Total

B.

Chapter 11 – Flexible Budgets and Overhead Analysis

155. McCordy Company provided information on the following three overhead activities:

Activity

Driver

Fixed Cost

Variable Rate

Maintenance

Machine hours

$75,000

$1.50

Power

Machine hours

20,000

$2.05

Setting up

Setups

–

$1,500

McCordy has found that the following driver levels are associated with two different levels of production:

Driver

30,000 units

70,000 units

Machine hours

50,000

95,000

Setups

25

65

Required:

Prepare an activity-based flexible budget.

Maintenance

Power

Setting up

Total

156. Allen Company produced 44,000 units last year. The information on the actual costs and budgeted costs at actual

production of three activities is provided below.

Activity

Actual Cost

Budgeted

Cost for

Actual

Production

Machining

$215,000

$225,000

Maintenance

$178,000

$178,300

Purchasing

$122,000

$118,000

Required:

Prepare an activity-based performance report for the three activities for the past year.

Performance Report

Resource

Salaries

Lease

Boxes

Fuel

Total

Capacity is determined by drivers: 6 × 160 × 5 × 50 = 240,000 miles. 90% = 216,000 miles

Chapter 11 – Flexible Budgets and Overhead Analysis

157. Define static budget and flexible budget. What is each type used for?

You decide

158. Describe flexible budgeting, including the two types of flexible budgets.

159. Discuss the following statement: “As long as the total variable overhead variance is small, the managers can be

assured that actual activity is proceeding as planned. No further action is necessary.”

160. Discuss the following statement: “Since fixed overhead is, by definition, not related to changes in activity level, then

the fixed overhead spending variance is zero.”

Chapter 11 – Flexible Budgets and Overhead Analysis

161. What is the fixed overhead volume variance? Suppose that the fixed overhead volume variance is unfavorable; what

does that mean?

162. How does activity flexible budgeting differ from traditional-based flexible budgeting?

163. Discuss why activity flexible budgeting provides a more accurate prediction of costs than a traditional flexible

budget.

Match the following terms with the items below:

a.

(Actual hours − Standard hours)SVOR

b.

Prediction of what activity costs will be as activity output changes

c.

A measure of capacity utilization

d.

Actual variable overhead − (SVOR × Actual hours)

e.

Difference between the actual amount and the flexible budget amount

f.

A budget that specifies costs for a range of activity

g.

A budget for a particular level of activity

h.

Estimating activity output and then assessing the cost of resources to produce this output

i.

A report that compares actual with planned costs

j.

Difference between actual and budgeted fixed overhead

164. Performance report

165. Static budget

166. Flexible budget

in a fixed overhead spending variance.

Chapter 11 – Flexible Budgets and Overhead Analysis

167. Activity-based budgeting

168. Fixed overhead spending variance

169. Activity flexible budget

170. Fixed overhead volume variance

171. Variable overhead efficiency variance

172. Variable overhead spending variance

173. Flexible budget variance