61. Dividends in arrears cannot exist in conjunction with

a.

callable preferred stock.

b.

convertible preferred stock.

c.

noncumulative preferred stock.

d.

cumulative preferred stock.

62. Which of the following would not be an account in the general ledger of a corporation?

a.

Dividends Payable

b.

Retained Earnings

c.

Additional Paid-in Capital

d.

Dividends in Arrears

63. When callable preferred stock is called and surrendered, the shareholder is entitled to all of the

following except

a.

dividends in arrears.

b.

a prorated portion of the current period’s dividend.

c.

a call premium.

d.

the market value of the stock.

64. Preferred stock is least likely to have which of the following characteristics?

a.

Preference as to dividends

b.

The right of the holder to vote at stockholders’ meetings

c.

Preference as to assets upon liquidation of the corporation

d.

The right of the holder to convert to common stock

65. Which of the following stock terms is least like the others?

a.

Market value

b.

Stated value

c.

Par value

d.

Legal capital

66. Par value is the minimum cushion of capital established for the protection of

a.

investors (stockholders).

b.

management.

c.

creditors.

d.

all of these.

67. If a corporation has issued common stock at various prices that exceed par value, legal capital will be

made up of the

a.

par value of the shares issued.

b.

total stockholders’ equity plus total liabilities.

c.

total amount of contributed capital.

d.

total amount of contributed capital plus retained earnings.

68. The excess of the issuance price over the stated value of a no-par common stock should be credited to

the

a.

Common Stock account.

b.

Retained Earnings account.

c.

Additional Paid-in Capital.

d.

Treasury Stock.

69. The par value of the common stock represents the

a.

amount entered into the corporation’s Common Stock account when a share is issued.

b.

liquidation value of the stock.

c.

market value of a share of stock.

d.

amount the corporation received when the stock was issued.

70. In the rare instance when a par value stock is issued at a cash price below par, the excess of the par

value over the amount of cash received should be

a.

credited to a liability account.

b.

debited to the Retained Earnings account.

c.

debited to an account titled Discount on Capital Stock.

d.

credited to the Retained Earnings account.

71. When common stock is issued by a corporation for a cash price above par value, the excess of the cash

proceeds over the par value should be reported in the financial statements as a component of

a.

retained earnings on the balance sheet.

b.

total liabilities on the balance sheet.

c.

operating income on the income statement.

d.

total contributed capital on the balance sheet.

72. When stock is issued for noncash assets or services, the dollar amount to be recorded for this exchange

is determined by the

a.

treasurer of the corporation.

b.

par value of the stock.

c.

market value of the stock or the market value of the consideration received, whichever is

greater.

d.

market value of the stock or the market value of the consideration received when the

market value of the stock cannot be determined.

73. The Additional Paid-in Capital account normally arises in the accounting records when

a.

the number of shares issued exceeds par value.

b.

the stated value of capital stock is greater than the par value.

c.

the market value of the stock rises above par value.

d.

capital stock is issued at an amount greater than par value.

74. Use the following information to answer the question below.

When Calvert Corporation was formed on January 1, 2010, the corporate charter provided for 50,000

shares of $20 par value common stock. The following transactions were among those engaged in by

the corporation during its first month of operation:

1. The corporation issued 200 shares of stock to its lawyer in full payment of the $5,000 bill for

assisting the company in drawing up its articles of incorporation and filing the proper papers with the

state agency.

2. The company issued 8,000 shares of stock at a price of $25 per share.

3. The company issued 7,000 shares of stock in exchange for equipment that had a fair market value of

$160,000.

The entry to record transaction 1 would be:

a.

Start-up and Organization Costs 4,000

Common Stock 4,000

b.

Start-up and Organization Costs 5,000

Common Stock 4,000

Additional Paid-in Capital 1,000

c.

Start-up and Organization Costs 4,000

Additional Paid-in Capital 4,000

d.

Start-up and Organization Costs 5,000

Common Stock 5,000

75. Use the following information to answer the question below.

When Calvert Corporation was formed on January 1, 2010, the corporate charter provided for 50,000

shares of $20 par value common stock. The following transactions were among those engaged in by

the corporation during its first month of operation:

1. The corporation issued 200 shares of stock to its lawyer in full payment of the $5,000 bill for

assisting the company in drawing up its articles of incorporation and filing the proper papers with the

state agency.

2. The company issued 8,000 shares of stock at a price of $25 per share.

3. The company issued 7,000 shares of stock in exchange for equipment that had a fair market value of

$160,000.

The entry to record transaction 2 would be:

a.

Cash 200,000

Common Stock 200,000

b.

Cash 200,000

Common Stock 160,000

Additional Paid-in Capital 40,000

c.

Cash 160,000

Additional Paid-in Capital 40,000

Common Stock 200,000

d.

Cash 160,000

Common Stock 160,000

76. Use the following information to answer the question below.

When Calvert Corporation was formed on January 1, 2010, the corporate charter provided for 50,000

shares of $20 par value common stock. The following transactions were among those engaged in by

the corporation during its first month of operation:

1. The corporation issued 200 shares of stock to its lawyer in full payment of the $5,000 bill for

assisting the company in drawing up its articles of incorporation and filing the proper papers with the

state agency.

2. The company issued 8,000 shares of stock at a price of $25 per share.

3. The company issued 7,000 shares of stock in exchange for equipment that had a fair market value of

$160,000.

The entry to record transaction 3 would be:

a.

Equipment 140,000

Common Stock 140,000

b.

Common Stock 140,000

Equipment 140,000

c.

Equipment 160,000

Common Stock 160,000

d.

Equipment 160,000

Common Stock 140,000

Additional Paid-in Capital 20,000

77. Use the following information to answer the question below.

When Calvert Corporation was formed on January 1, 2010, the corporate charter provided for 50,000

shares of $20 par value common stock. The following transactions were among those engaged in by

the corporation during its first month of operation:

1. The corporation issued 200 shares of stock to its lawyer in full payment of the $5,000 bill for

assisting the company in drawing up its articles of incorporation and filing the proper papers with the

state agency.

2. The company issued 8,000 shares of stock at a price of $25 per share.

3. The company issued 8,000 shares of stock in exchange for equipment that had a fair market value of

$160,000.

The entry to record transaction 3 would be:

a.

Equipment 160,000

Common Stock 160,000

b.

Common Stock 160,000

Equipment 160,000

c.

Additional Paid-in Capital 35,000

Equipment 125,000

Common Stock 160,000

d.

Cash 160,000

Equipment 160,000

78. A company purchases 300 shares of its $100 par value common stock at $110 per share. It then

reissues 50 shares at $114 per share. The entry upon reissue of the stock would be:

a.

Cash 5,700

Treasury Stock-Common 5,500

Paid-in Capital, Treasury Stock 200

b.

Cash 5,700

Treasury Stock-Common 5,500

Gain on Sale of Treasury Stock 200

c.

Cash 5,700

Treasury Stock-Common 5,000

Retained Earnings 700

d.

Cash 5,700

Treasury Stock-Common 5,700

79. A company purchases 600 shares of its $100 par value common stock at $110 per share. It then

reissues 100 shares at $114 per share. The entry upon reissue of the stock would be:

a.

Cash 11,400

Treasury Stock-Common 11,000

Paid-in Capital, Treasury Stock 400

b.

Cash 11,400

Treasury Stock-Common 11,400

c.

Cash 11,400

Treasury Stock-Common 11,000

Gain on Sale of Treasury Stock 400

d.

Cash 11,400

Treasury Stock-Common 10,000

Retained Earnings 1,400

80. The sale of treasury stock cannot result in

a.

an increase in Retained Earnings.

b.

the crediting of Paid-in Capital, Treasury Stock.

c.

the debiting of Paid-in Capital, Treasury Stock.

d.

an increase in total stockholders’ equity.

81. A company purchases 400 shares of its $50 par value common stock at $55 per share. It then reissues

60 shares at $58 per share. The entry upon reissue of the stock would be:

a.

Cash 3,480

Treasury Stock-Common 3,300

Paid-in Capital, Treasury Stock 180

b.

Cash 3,480

Treasury Stock-Common 3,480

c.

Cash 3,480

Paid-in Capital, Treasury Stock 3,480

d.

Cash 3,480

Treasury Stock-Common 3,000

Retained Earnings 480

82. On January 1, 2010, Belmont Corporation had 50,000 shares of $10 par value common stock issued

and outstanding. All 50,000 shares had been issued in a prior period at $15 per share. On February 1,

2010, Belmont purchased 2,000 shares of treasury stock for $18 per share and later sold the treasury

shares for $20 per share on March 2, 2010. The entry to record the purchase of the treasury shares on

February 1, 2010, would be:

a.

Cash 36,000

Treasury Stock-Common 36,000

b.

Cash 36,000

Treasury Stock-Common 30,000

Gain on Treasury Stock-Common 6,000

c.

Treasury Stock, Common 30,000

Loss on Treasury Stock-Common 6,000

Cash 36,000

d.

Treasury Stock, Common 36,000

Cash 36,000

83. On January 1, 2010, Belmont Corporation had 50,000 shares of $10 par value common stock issued

and outstanding. All 50,000 shares had been issued in a prior period at $15 per share. On February 1,

2010, Belmont purchased 2,000 shares of treasury stock for $18 per share and later sold the treasury

shares for $20 per share on March 2, 2010. The entry to record the sale of the treasury shares on March

2, 2010, would be:

a.

Cash 40,000

Treasury Stock-Common 40,000

b.

Cash 40,000

Treasury Stock-Common 36,000

Paid-in Capital, Treasury Stock 4,000

c.

Cash 40,000

Treasury Stock-Common 36,000

Retained Earnings 4,000

d.

Cash 40,000

Treasury Stock-Common 36,000

Gain on Treasury Stock 4,000

84. Use the following information to answer the question below.

The following transactions involving Lupine Corporation occurred during the year:

Apr.

1

Purchased 2,000 shares of its own preferred stock for $20, the current market

price. This is the first transaction involving its own stock engaged in by the

company.

May

3

Sold 400 of the shares purchased on April 1 for $25 per share.

June

5

Retired 600 of the shares purchased on April 1. The original issue price was $10.

The par value of the stock is $5.

The entry to record the April 1 transaction would be:

a.

Cash 40,000

Treasury Stock, Preferred 40,000

b.

Retained Earnings 40,000

Cash 40,000

c.

Paid-in Capital, Preferred 40,000

Treasury Stock, Preferred 40,000

d.

Treasury Stock, Preferred 40,000

Cash 40,000

85. Use the following information to answer the question below.

The following transactions involving Lupine Corporation occurred during the year:

Apr.

1

Purchased 2,000 shares of its own preferred stock for $20, the current market

price. This is the first transaction involving its own stock engaged in by the

company.

May

3

Sold 400 of the shares purchased on April 1 for $25 per share.

June

5

Retired 600 of the shares purchased on April 1. The original issue price was $10.

The par value of the stock is $5.

The entry to record the May 3 transaction would be:

a.

Treasury Stock, Preferred 10,000

Cash 10,000

b.

Cash 10,000

Treasury Stock, Preferred 8,000

Paid-in Capital, Treasury Stock 2,000

c.

Cash 4,000

Retained Earnings 6,000

Treasury Stock, Preferred 10,000

d.

Treasury Stock, Preferred 8,000

Cash 8,000

86. Use the following information to answer the question below.

The following transactions involving Lupine Corporation occurred during the year:

Apr.

1

Purchased 2,000 shares of its own preferred stock for $20, the current market

price. This is the first transaction involving its own stock engaged in by the

company.

May

3

Sold 400 of the shares purchased on April 1 for $25 per share.

June

5

Retired 600 of the shares purchased on April 1. The original issue price was $10.

The par value of the stock is $5.

The entry to record the June 5 transaction would be:

a.

Preferred Stock 3,000

Additional Paid in Capital, Preferred 3,000

Treasury Stock, Preferred 6,000

b.

Treasury Stock, Preferred 6,000

Cash 6,000

c.

Cash 3,000

Treasury Stock, Preferred 3,000

d.

Preferred Stock 3,000

Additional Paid in Capital, Preferred 3,000

Retained Earnings 6,000

Treasury Stock, Preferred 12,000

87. The purchase of treasury stock will result in

a.

no net changes in assets, liabilities, or stockholders’ equity.

b.

a decrease in assets and a decrease in stockholders’ equity.

c.

a decrease in one asset account and an increase in a different asset account.

d.

a decrease in assets and a decrease in liabilities.

88. If the entry to record the retirement of treasury stock contains a credit to a Paid-in Capital, Retirement

of Stock account, it is apparent that the

a.

cost of the treasury shares was less than par value.

b.

cost of the treasury shares was greater than the original issuance price of the shares.

c.

cost of the treasury shares was less than the original issuance price of the shares.

d.

original issuance price of the shares was less than par value.

89. Use the following information to answer the question below.

On January 1, 2010, Falcon Corporation had 40,000 shares of $10 par value common stock issued and

outstanding. All 40,000 shares had been issued in a prior period at $17 per share. On February 1, 2010,

Falcon purchased 6,100 shares of treasury stock for $19 per share and later sold the treasury shares for

$26 per share on March 2, 2010.

What amount of gain due to these treasury stock transactions should be reported on the income

statement for the year ended December 31, 2010?

a.

$0

b.

$42,700

c.

$6,100

d.

$4,270

90. Use the following information to answer the question below.

On January 1, 2009, Falcon Corporation had 40,000 shares of $10 par value common stock issued and

outstanding. All 40,000 shares had been issued in a prior period at $17 per share. On February 1, 2009,

Falcon purchased 1,000 shares of treasury stock for $19 per share and later sold the treasury shares for

$26 per share on March 2, 2009.

The entry to record the sale of the treasury shares on March 2, 2009 is:

a.

Cash 26,000

Common Stock 19,000

Retained Earnings 7,000

b.

Cash 24,000

Retained Earnings 2,000

Treasury Stock, Common 26,000

c.

Cash 26,000

Treasury Stock, Common 19,000

Gain on Treasury Stock, Common 7,000

d.

Cash 26,000

Treasury Stock, Common 19,000

Paid-in Capital, Treasury Stock 7,000

91. According to generally accepted accounting principles, treasury stock usually should be recorded at

a.

original issue cost.

b.

par or stated value.

c.

cost.

d.

net realizable value.

92. On the balance sheet, treasury stock owned by the company is classified properly as

a.

contra-stockholders’ equity.

b.

current assets.

c.

investments.

d.

a note to the financial statements.

SHORT ANSWER

1. Use the following information to obtain the ratios requested below. Where necessary, carry answers to

one decimal place.

Dividends per share: $.54

Market price per share: $30

Net income: $88,000

Average stockholders’ equity: $625,000

Earnings per share: $1.25

a. Dividends yield = _____________%

b. Return on equity = _____________%

c. Price/earnings (P/E) ratio = __________times

2. Identify (by code letter) each of the following characteristics as being an advantage of (A), a

disadvantage of (D), or not applicable to (N) the corporate form of business.

1. Separate legal entity

6. Mutual agency

2. Taxable entity resulting in double

7. Ease of transfer of ownership

taxation

3. Continuous existence

8. Ease of capital generation

4. Unlimited liability

9. Lack of mutual agency

5. Government regulation

10. Professional management

3. On June 1, 2008, Will Oldman, treasurer of A-One Corporation, received an option to purchase 2,000

shares of A-One $5 par value common stock for $20 per share any time during 2009 or 2010. Oldman

exercised his option on May 14, 2009. The market price of the stock was $20 per share on June 1,

2008, and $25 per share on May 14, 2009. Provide the entry in journal form to record the exercise of

the option on A-One’s books. Show computations. (Omit explanation.)

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

Common Stock

4. Under what circumstances should compensation expense be recorded for a stock option plan?

5. Berman Corporation was organized during 20xx. In organizing, the company incurred the following

costs:

1. Paid the state $900 for the corporate charter and related fees of incorporation.

2. Paid the attorney $2,500 for services rendered in connection with filing incorporation papers with

the state.

3. Issued 500 shares of $5 par value common stock to an accountant in exchange for accounting

services valued at $3,000.

Prepare the entries in journal form necessary to record the above transactions without explanations.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

ANS:

6. Mertz Motors Corporation has 2,000,000 authorized shares of $10 par value common stock. As of

June 30, 20xx, there were 1,000,000 shares issued and outstanding. On June 30, 20xx, the board of

directors declared a $0.20 per share cash dividend to be paid on August 1, 2010, to shareholders of

record on July 15, 20xx. Prepare the necessary entries in journal form to be recorded on (a) the date of

declaration, (b) the date of record, and (c) the date of payment. (Omit explanations.)

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

7. Indicate on the blanks below the net effect (I = increase, D = decrease, NE = no effect) of each of the

following entries on working capital.

_____ 1. To record the declaration of a cash dividend

_____ 2. To record the payment of a previously declared and recorded cash dividend

_____ 3. To close the Dividends account at the end of the accounting period

8. Indicate on the blanks below the net effect (I = increase, D = decrease, NE = no effect) of each of the

following entries on total stockholders’ equity.

_____ 1. To record the declaration of a cash dividend

_____ 2. To record the payment of a previously declared and recorded cash dividend

_____ 3. To close the Dividends account at the end of the accounting period

ANS:

9. Why must a corporation have sufficient retained earnings before it may declare cash dividends?

10. The following information relates to the number of common shares of the Nelly Corporation:

40,000 Authorized shares

15,000 Unissued shares

2,500 Treasury shares

Calculate the number of outstanding shares from the information given. Show your calculations.

11. The following information relates to the number of common shares of the Telly Corporation:

80,000 Authorized shares

30,000 Unissued shares

5,000 Treasury shares

Calculate the number of outstanding shares from the information given. Show your calculations.

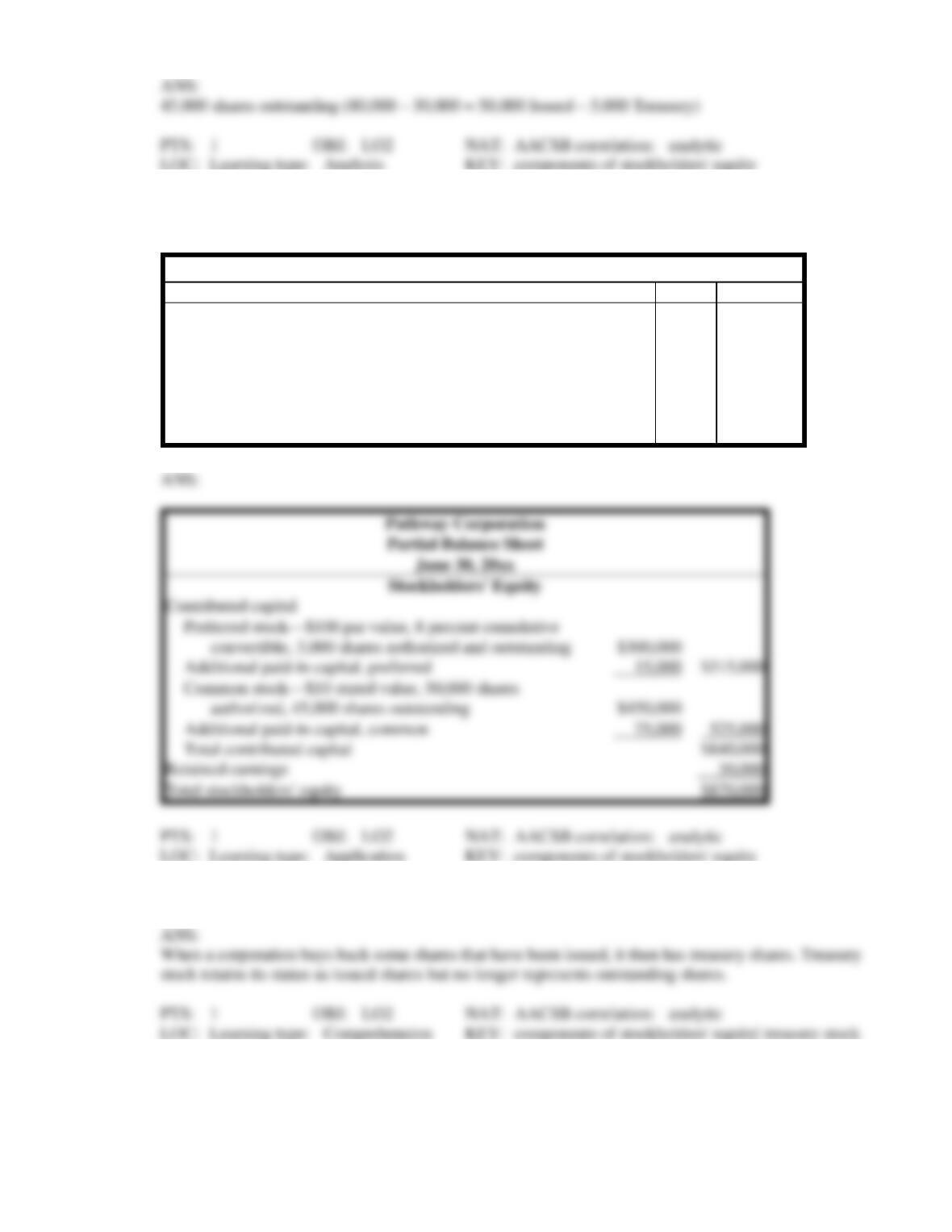

12. Prepare in proper form the stockholders’ equity section of the balance sheet from the following

selected accounts and balances taken from the adjusted trial balance of Pathway Corporation on June

30, 20xx.

Partial Adjusted Trial Balance

Account

Debit

Credit

Common Stock—$10 stated value, 50,000 shares authorized,

45,000 shares outstanding

450,000

Preferred Stock—$100 par value, 8 percent cumulative convertible,

3,000 shares authorized and outstanding

300,000

Additional Paid-in Capital, Preferred

15,000

Additional Paid-in Capital, Common

75,000

Retained Earnings

30,000

13. How is it possible for a corporation to have more shares issued than it has outstanding?

14. Define outstanding stock.

15. People’s Electric Company omitted all its preferred stock dividends indefinitely in an effort to improve

liquidity. All of the company’s cumulative preferred stock was affected. According to the Wall Street

Journal, “Some interpreted the drastic action as a requisite for the cash-strapped utility to secure a new

credit agreement. . . . If the credit agreement falls through, the omission of preferred-stock dividends

would suggest People’s Electric is perilously close to filing for bankruptcy.” What is cumulative

preferred stock? Why is the omission of dividends on those shares a drastic action? If new bank

financing is not obtained, why would the company have to consider declaring bankruptcy?

16. Duncan Corporation has 2,000 shares of $100 par value, 6 percent cumulative preferred stock and

20,000 shares of $10 par value common stock outstanding. In its first four years of operation, Duncan

Corporation paid cash dividends as follows: 2007, $15,000; 2008, $0; 2009, $20,000; 2010, $25,000.

Calculate the total cash dividends received by owners of preferred and common stock in each year.

17. Paloma Corporation had 5,000 shares of $100 par value, 9 percent cumulative preferred stock and

30,000 shares of $10 par value common stock outstanding during each of its first four years of

operation. The following amounts of cash dividends were paid during the years indicated: 2007, $0;

2008, $80,000; 2009, $220,000; 2010, $270,000. Determine the cash dividends per share paid to the

preferred and common stockholders during each of the four years.

18. Margil Industries has 40,000 shares of 9 percent cumulative preferred stock and 30,000 shares of

common stock outstanding. Par value for each is $50. The company has paid no dividends for the past

two years. This year, a $620,000 dividend is paid. How much of the $620,000 is paid to the common

shareholders?

19. Red River Corporation has 24,000 shares of 11 percent noncumulative preferred stock and 60,000

shares of common stock outstanding. Par value for each is $10. The company paid no dividends last

year. This year, a $100,000 dividend is paid. How much of the $100,000 is paid to the preferred

shareholders?

20. Why might someone prefer to invest in a company by purchasing preferred stock rather than common

stock?

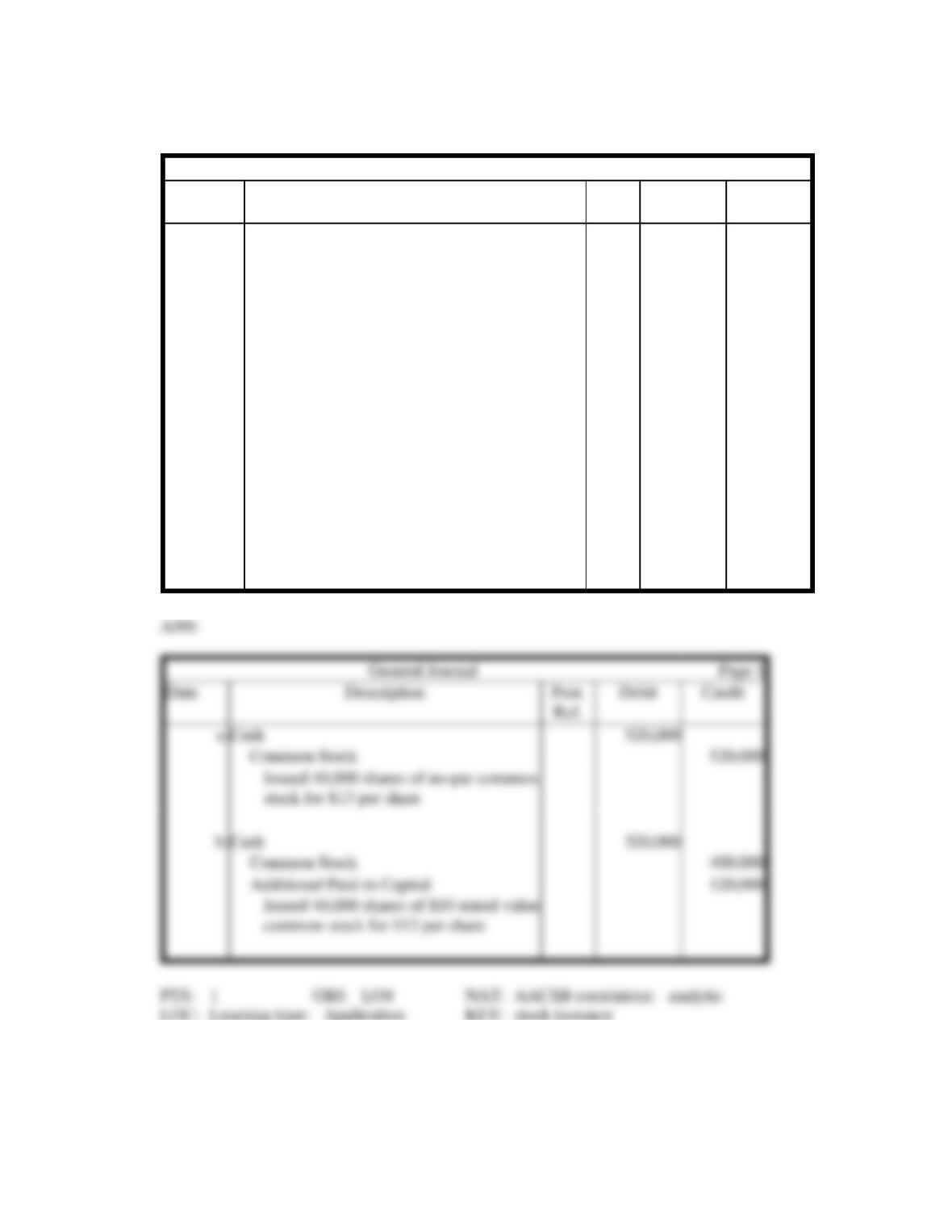

21. Simpson Corporation is authorized to issue 100,000 shares of no-par stock. The company recently sold

40,000 shares for $13 per share.

a. Prepare the entry in journal form to record the sale of the stock assuming there is no stated value.

b. Prepare the entry in journal form if a $10 stated value is authorized by the company’s board of

directors.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

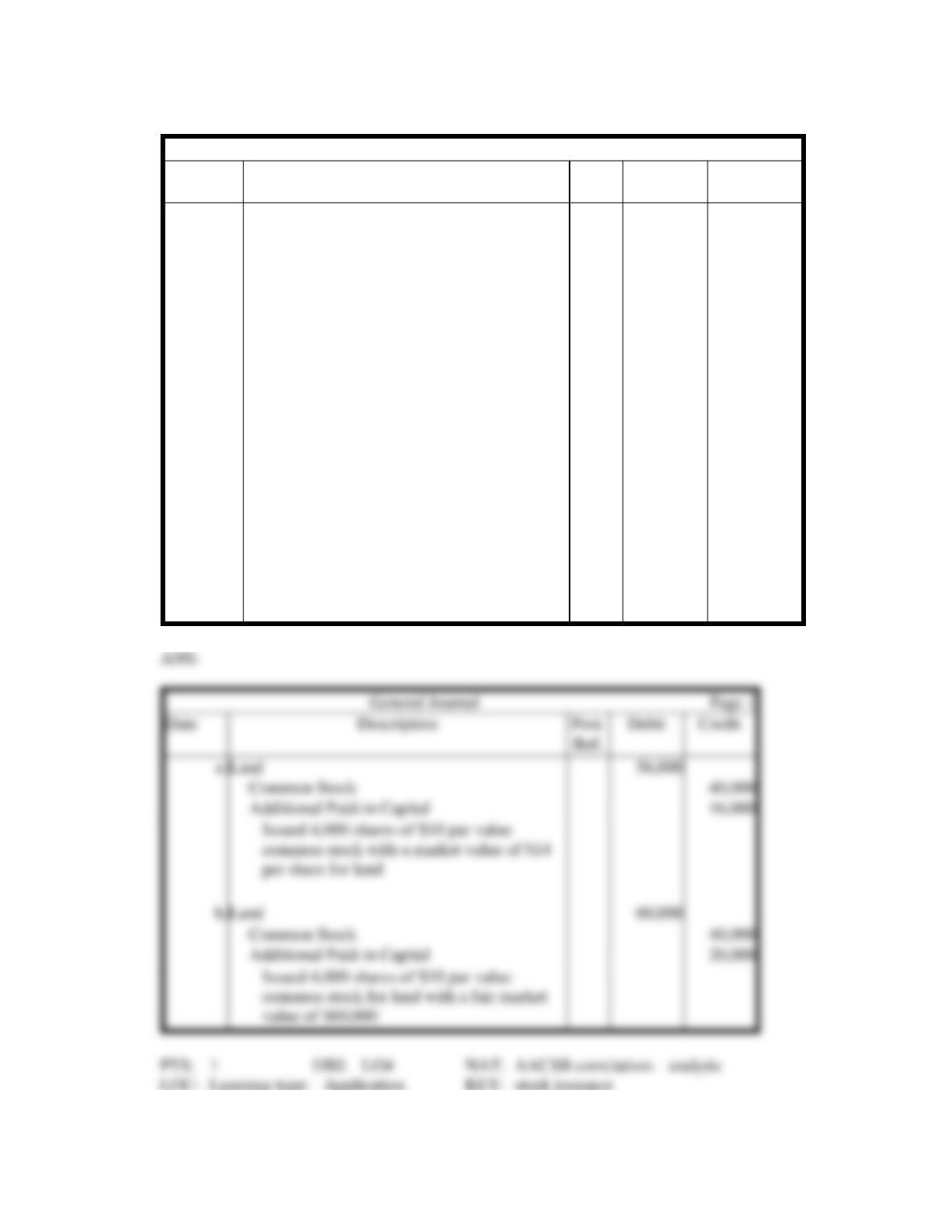

22. Siegfried Corporation issued 4,000 shares of its $10 par value common stock for some land. The land

had a fair market value of $60,000.

Prepare the entries in journal form necessary to record the stock issue for the land under each of the

following conditions:

a. The stock was selling for $14 per share on the day of the transaction.

b. Management attempted to place a market value on the common stock but could not do so.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

Land

Common Stock

Common Stock