132. A corporation has 50,000 shares of $25 par value stock outstanding that has a current market value of

$120. If the corporation issues a 5-for-1 stock split, the par value of the stock after the split will be:

133. A corporation has 60,000 shares of $25 par value stock outstanding that has a current market value of

$120. If the corporation issues a 5-for-1 stock split, the number of shares outstanding will be:

D. 30,000

134. Earnings per share

135. Samuels, Inc. reported net income for 2011 is $105,000. During 2011 the company had 5,000 shares of

$100 par, 5% preferred stock and 20,000 of $5 par common stock outstanding. Samuels’ earnings per share for

2011 is

136. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50

par common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

45,000

Year 3:

90,000

Determine the dividends per share for preferred and common stock for the first year.

137. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50

par common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

45,000

Year 3:

90,000

Determine the dividends per share for preferred and common stock for the second year.

138. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50

par common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

45,000

Year 3:

90,000

Determine the dividends per share for preferred and common stock for the third year.

139. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50

par common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

45,000

Year 3:

90,000

Determine the dividends in arrears for preferred stock for the second year.

140. Match the following stockholders equity concepts to the appropriate answer.

1. a company whose shares can be bought and sold on

2. formally creates a corporation

1

publicly held

assets to satisfy claims

5

3. creditors cannot pursue stockholder’s personal

and operate it

7

4. a legal entity, separate from the people who create

privately held

affairs

2

6. responsible for establishing corporate policies

3

5. rules and procedures for corporate conduct of its

articles of

stock exchange

6

8. earnings of a company distributed to stockholders

8

7. company whose shares are not bought or sold on a

141. Match the following stockholders equity concepts to the most appropriate answer.

issue to shareholders

2

1. the maximum number of shares a company can

additional paid in

8

2. account used when issue price exceeds par value of

stockholders

5

3. the number of sharing originally sold to

6

4. a class of stock that provides voting rights for

5. the number of shares currently held by stockholders

authorized shares

1

for shareholders

3

6. a class of stock that does not provide voting rights

exchange

4

8. a value established for the protection of creditors

7

7. a value that the stock is worth on the stock

4

142. Match the following stockholder’s equity concepts to the best answer.

1. the date that a share of stock must be owned to

stock dividends

2. distribution of a company’s earnings to

3. when dividends are actually distributed to

4. equity account reflecting shares “owed” to

additional paid in

7. Shares of common stock re-acquired by a

8. account used when shares are issued for an amount

143. Match the value to the appropriate account. For the year ended 2012 ABC had the following transactions:

– issued 10,000 shares of $2.00 par value common stock for $12.00 per share

– issued 3,000 shares of $50 par value 6% preferred stock for $70 per share

– purchased 1000 shares of previously issued common stock for $15.00 per share

-reported net income of $200,000

– declared and paid a total dividend of $40,000

Assume that retained earnings had a beginning balance of $75,000.

144. A company had stock outstanding as follows during each of its first three years of operations: 2,500 shares

of $10, $100 par, cumulative preferred stock and 50,000 shares of $10 par common stock. The amounts

distributed as dividends are presented below. Determine the total and per share dividends for each class of

stock for each year by completing the schedule.

Preferred

Common

Year

Dividends

Total

Per Share

Total

Per Share

1

$10,000

_________

_________

_________

_________

2

25,000

_________

_________

_________

_________

3

60,000

_________

_________

_________

_________

145. On April 1, 10,000 shares of $5 par common stock were issued at $22, and on April 7, 5,000 shares of $50

par preferred stock were issued at $104. Journalize the entries for April 1 and 7.

Common Stock

50,000

Paid-In Capital in Excess of Par-

Common Stock

170,000

7

Cash

520,000

Preferred Stock

250,000

Paid-In Capital in Excess of Par-

Preferred Stock

270,000

Preferred

Common

Year

Dividends

Total

Per Share

Total

Per Share

1

$10,000

$10,000

$ 4.00

None

None

2

25,000

25,000

10.00

None

None

3

60,000

40,000

16.00

$20,000

$ .40

146. On May 10, a company issued for cash 1,500 shares of no-par common stock (with a stated value of $2) at

$14, and on May 15, it issued for cash 2,000 shares of $15 par preferred stock at $58.

Journalize the entries for May 10 and 15, assuming that the common stock is to be credited with the stated

value.

147. On February 1 of the current year, Motor, Inc. issued 700 shares of $2 par common stock to an attorney in

return for preparing and filing the Articles of Incorporation. The value of the services is $9,600. Journalize

this transaction.

148. On April 10, a company acquired land in exchange for 1,000 shares of $20 par common stock with a

current market price of $73. Journalize this transaction.

149. Sabas Company has 20,000 shares of $100 par, 1% non-cumulative preferred stock and 100,000 shares of

$50 par common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

15,000

Year 3:

90,000

Determine the dividends per share for preferred and common stock for each year.

150. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50

par common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

45,000

Year 3:

90,000

Determine the dividends per share for preferred and common stock for each year.

Amount distributed

$10,000

$45,000

$90,000

Preferred dividend (20,000 shares)

10,000

45,000

65,000

Common dividend (100,000 shares)

$25,000

Dividends per share:

Preferred stock

$0.50

$2.25

$3.25

Common stock

0

0

$0.25

Current year preferred dividend in arrears

$30,000

$25,000

Amount distributed

$10,000

$15,000

$90,000

Preferred dividend (20,000 shares)

10,000

15,000

20,000

Dividends per share:

Preferred stock

$0.50

$0.75

$1.00

Common stock

0

0

$0.70

151. Sabas Company has 40,000 shares of $100 par, 1% preferred stock and 100,000 shares of $50 par common

stock. The following amounts were distributed as dividends:

Year 1:

$ 50,000

Year 2:

90,000

Year 3:

130,000

Determine the dividends per share for preferred and common stock for each year.

152. A corporation, which had 18,000 shares of common stock outstanding, declared a 3-for-1 stock split.

(a)

What will be the number of shares outstanding after the split?

(b)

If the common stock had a market price of $240 per share before the stock split, what would be an approximate market price

per share after the split?

(c)

Journalize the entry to record the stock split.

(a)

54,000 shares

(b)

$80 per share

(c)

no entry

153. On May 1, 10,000 shares of $10 par common stock were issued at $30, and on May 7, 5,000 shares of $50

par preferred stock were issued at $111. Journalize the entries for May 1 and May 7.

May 1

Cash

300,000

Common Stock

100,000

Paid-In Capital in Excess of Par-

Common Stock

200,000

7

Cash

555,000

Preferred Stock

250,000

Paid-In Capital in Excess of Par-

Preferred Stock

305,000

Amount distributed

$50,000

$90,000

$130,000

Preferred dividend (40,000 shares)

40,000

40,000

40,000

Dividends per share:

Preferred stock

$1.00

$1.00

$1.00

Common stock

$0.10

$0.50

$0.90

154. The dates of importance in connection with a cash dividend of $50,000 on a corporation’s common stock

are January 15, February 15, and March 15. Journalize the entries required on each date.

155. Vincent Corporation has 100,000 share of $100 par common stock outstanding. On June 30, Vincent

Corporation declared a 5% stock dividend to be issued on July 30 to stockholders of record July 15. The

market price of the stock was $132 a share on June 30. Journalize the entries required on June 30, July 15 and

July 30.

156. On April 2nd a corporation purchased for cash 5,000 shares of its own $10 par common stock at $16 a

share. They sold 3,000 of the treasury shares at $19 a share on June 15th. The remaining 2,000 shares were

sold on November 10th for $12 a share.

(a)

Journalize the entries to record the purchase (treasury stock is recorded at cost).

(b)

Journalize the entries to record the sale of the stock.

157. On June 5, Belen Corporation reacquired 3,300 shares of its common stock at $45 per share. On July 15,

Belen sold 2,000 of the reacquired shares at $48 per share. On August 30, Belen sold the remaining shares at

$42 per share.

Journalize the transactions of June 5, July 15, and August 30.

June 5

Treasury Stock (3,300 ´ $45)

148,500

Cash

148,500

Treasury Stock (2,000 ´ $45)

90,000

August 30

Cash (1,300 ´ $42)

54,600

Treasury Stock (5,000 x $16)

80,000

Cash (3,000 x $19)

57,000

Paid-In Capital from Sale of Treasury Stock(3,000 x [$16 – $19])

9,000

November 10th

Treasury Stock (2,000 x $16)

32,000

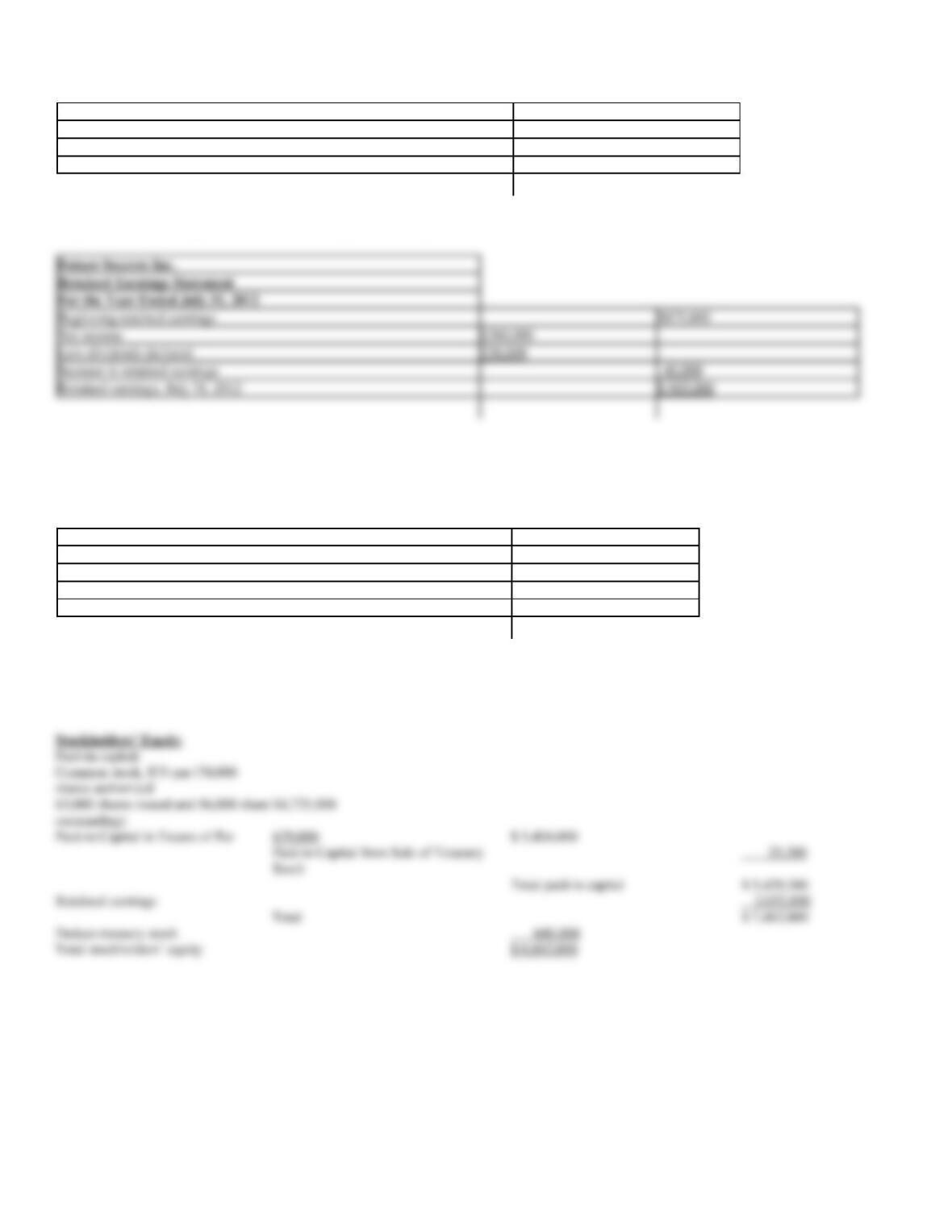

158. Using the following accounts and balances, prepare the Stockholders’ Equity section of the balance

sheet. Fifty thousand shares of common stock are authorized, and 5,000 shares have been reacquired.

Common Stock, $50 parommon Stock, $50 par

$1,250,000

Paid-In Capital in Excess of Par

800,000

Paid in Capital from Sale of Treasury Stock

42,000

Retained Earnings

4,350,000

Treasury Stockeasury Stock

155,000

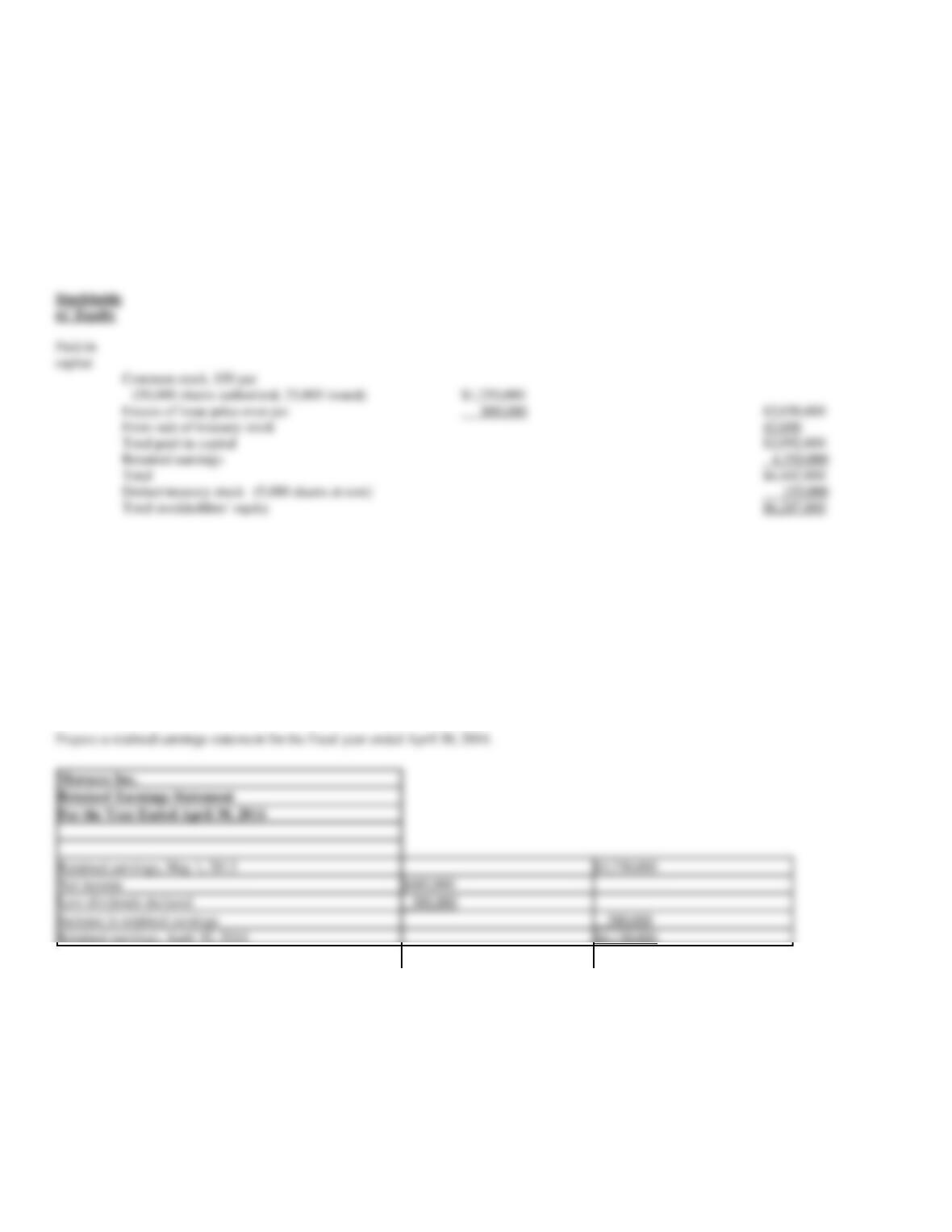

159. Morocco Inc. reported the following results for the year ending April 30, 2014:

Retained earnings, May 1, 2013

$3,750,000

Net income

680,000

Cash dividends declared

80,000

Stock dividends declared

220,000

Retained earnings, May 1, 2013

$3,750,000

Net income

$680,000

Less dividends declared

300,000

Increase in retained earnings

380,000

Retained earnings, April 30, 2014

$4,130,000

Excess of issue price over par

800,000

$2,050,000

From sale of treasury stock

42,000

Total paid-in capital

$2,092,000

Retained earnings

4,350,000

Total

$6,442,000

Deduct treasury stock (5,000 shares at cost)

155,000

Total stockholders’ equity

$6,287,000

160. Indicate whether the following actions would (+) increase, (-) decrease, or (0) not affect a company’s total

assets, liabilities, and stockholders’ equity.

Stockholders’

Assets

Liabilities

Equity

(1)

Declaring a cash dividend

_______

_______

_______

(2)

Paying the cash dividend declared in (1)

_______

_______

_______

(3)

Declaring a stock dividend

_______

_______

_______

(4)

Issuing stock certificates for the stock

dividend declared in (3)

_______

_______

_______

161. Macy Company has 10,000 shares of 2% cumulative preferred stock of $50 par and 25,000 shares of $75

par common stock. The following amounts were distributed as dividends:

Year 1

$30,000

Year 2

6,000

Year 3

80,000

Required:

Determine the dividends per share for preferred and common stock for each year.

Year 1

Year 2

Year 3

Amount distributed

$30,000

$6,000

$80,000

*($4,000 + $10,000)

Dividends per share:

Stockholders’

Assets

Liabilities

Equity

(1)

Declaring a cash dividend

0

+

–

(2)

Paying the cash dividend declared in (1)

–

–

0

(3)

Declaring a stock dividend

0

0

0

(4)

Issuing stock certificates for the stock

dividend declared in (3)

0

0

0

162. Future Sources, Inc. reported the following results for the year ending July 31, 2012:

Retained earnings, August 1, 2011

$875,000

Net income

260,000

Cash dividends declared

120,000

Stock dividends declared

100,000

Prepare a retained earnings statement for the fiscal year ended July 31, 2012.

163. Using the following information, prepare the Stockholders’ Equity section of the balance sheet. Seventy

thousand shares of common stock are authorized and 7,000 shares have been reacquired.

Common Stock, $75 par

$4,725,000

Paid-in Capital in Excess of Par

679,000

Paid-in Capital from Sale of Treasury Stock

25,200

Retained Earnings

2,032,800

Treasury Stock

600,000

Paid-in capital:

Paid-in Capital in Excess of Par

679,000

$ 5,404,000

Total paid-in capital

Retained earnings

Total

$ 7,462,000

Deduct treasury stock

600,000

Total stockholders’ equity

$ 6,862,000

Beginning retained earnings

$875,000

Net income

$260,000

Less dividends declared

220,000

Increase in retained earnings

40,000

Retained earnings, July 31, 2012

$ 915,000

164. The following account balances appear on the balance sheet of Osgood Industries:

Common Stock (300,000 shares authorized, $100 par): $10,000,000

Paid-in Capital in Excess of Par – Common Stock: $2,000,000;

Retained earnings: $45,000,000.

The board of directors declared a 2% stock dividend when the market price of the stock was $135 a

share. Osgood reported no income or loss for the current year.

Required:

(1)

Journalize the entries to record

a.

the declaration of the

dividend, capitalizing an

amount equal to market

value; and

b.

the issuance of the stock

certificates.

(2)

Determine the following amounts before the stock dividend was declared:

a.

Total paid-in capital;

b.

Total retained earnings;

and

c.

Total stockholders’ equity.

(3)

Determine the following amounts after the stock dividend was declared and closing

entries were recorded at the end of the year:

a.

Total paid-in capital;

b.

Total retained earnings;

and

c.

Total stockholders’ equity.

(1)

(a)

Stock Dividends

270,000*

Stock Dividends Distributable (2,000 ´ $100)

200,000

Common Stock

70,000

*[($10,000,000/$100) ´ $135] ´ 2%

(b)

Stock Dividends Distributable

200,000

Common Stock

200,000

(2)

(a)

$12,000,000 ($10,000,000 +

(b)

$45,000,000

(c)

$57,000,000 ($12,000,000 +

$45,000,000)

(3)

(a)

$12,270,000 ($12,000,000 +

(b)

$44,730,000 ($45,000,000 –

(c)

$57,000,000 ($12,270,000 +

165. On March 4, of the current year, Barefoot Bay, Inc. reacquired 5,000 shares of its common stock at $89

per share. On August 7, Barefoot Bay sold 3,500 of the reacquired shares at $100 per share. The remaining

1,500 shares were sold at $88 per share on November 29.

Required:

(1)

Journalize the transaction of March 4, August 7, and November 29.

(2)

What is the balance in Paid-in Capital from Sale of Treasury Stock on December 31, of the current year?

(3)

Why might Barefoot Bay Inc. have purchased the treasury stock?

166. Marcos Company, which had 35,000 shares of common stock outstanding, declared a 4-for-1 stock split.

Required:

(1)

What will be the number of shares outstanding after the split?

(2)

If the common stock had a market price of $280 per share before the stock split, what would be an approximate

market price per share after the split?

(1)

Mar.

4

Treasury Stock

445,000

Cash

445,000

Aug.

7

Cash

350,000

Treasury Stock (3,500 ´ $89)

311,500

Paid-In Capital from Sale of

38,500

Nov.

Cash

132,000

Paid-In Capital from Sale of

1,500

Treasury Stock (1,500 ´ $89)

133,500

167. Selected transactions completed by Breezeway Construction during the current fiscal year are as follows:

February 3

Split the common stock 2 for 1 and reduced the par from $40 to $20 per share. After the split there

were 250,000 common shares outstanding.

April 10

Declared semiannual dividends of $1.50 on 18,000 shares of preferred stock and $0.08 on the common

stock to stockholders of record on May 10, payable on June 9.

June 9

Paid the cash dividends.

October 10

Declared semiannual dividends of $1.50 on the preferred stock and $0.04 on the common stock (before

the stock dividend). In addition, a 2% common stock dividend was declared on the common stock

outstanding. The fair market value of the common stock is estimated at $36.

December 9

Paid the cash dividends and issued the certificates for the common stock dividend.

Required: Journalize the transactions.

Feb.

3

No entry required. The stockholders ledger would be revised to record the increased number of shares held by each

Apr.

Cash Dividends

47,000*

Cash Dividends Payable

*[(18,000 shares ´ $1.50) + (250,000 shares

´ $0.08)] = $27,000 + $20,000 = $47,000

Cash

Oct.

Cash Dividends

37,000*

*[(18,000 shares ´ $1.50) + (250,000 shares

´ $0.04)] = $27,000 + $10,000 = $37,000

Stock Dividends Distributable (5,000 ´ $20)

Paid-In Capital in Excess of Par—Common Stock

Dec.

9

Cash Dividends Payable

37,000

Cash

9

Stock Dividends Distributable

100,000

Common Stock