Page 1

1.

A _____ is an organization that produces goods or services for sale.

A)

production function

B)

firm

C)

variable input

D)

fixed input

2.

In the short run:

A)

all inputs are fixed.

B)

all inputs are variable.

C)

some inputs are fixed and some inputs are variable.

D)

all costs are variable.

3.

The _____ is the increase in output that is produced when a firm hires an additional

worker.

A)

average product

B)

total product

C)

marginal product

D)

marginal cost

4.

Lauren has 11 people working in her tangerine grove. The marginal product of the

eleventh worker is 13 bushels of tangerines. If she hires a twelfth worker, the marginal

product of that worker will be:

A)

14 bushels.

B)

15 bushels.

C)

12 bushels.

D)

The answer cannot be determined with the information available.

5.

The total product curve:

A)

shows the relation between output and the quantity of a variable input for varying

levels of the fixed input.

B)

will become flatter as output increases if there are diminishing returns to the

variable input.

C)

will be downward-sloping if there are diminishing returns to the variable input.

D)

will become horizontal when the marginal product of the variable input is constant.

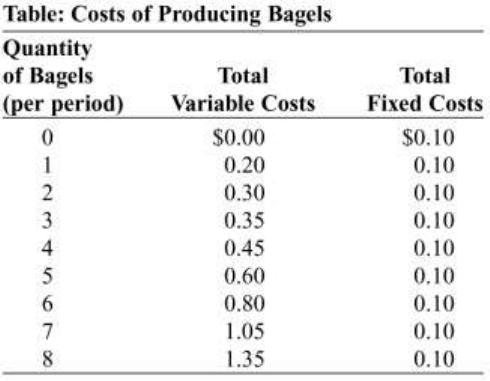

Page 2

Use the following to answer questions 6-7:

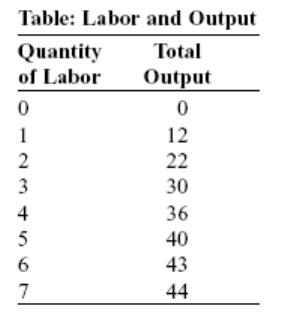

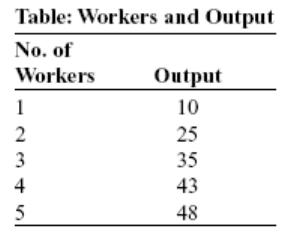

6.

(Table: Labor and Output) Look at the table Labor and Output. The marginal product of

the fifth worker is:

A)

8.

B)

4.

C)

3.

D)

40.

7.

(Table: Labor and Output) Look at the table Labor and Output. The marginal product of

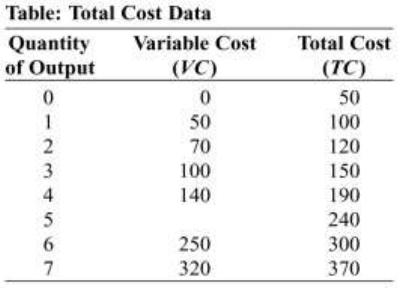

the fourth worker is:

A)

9.

B)

36.

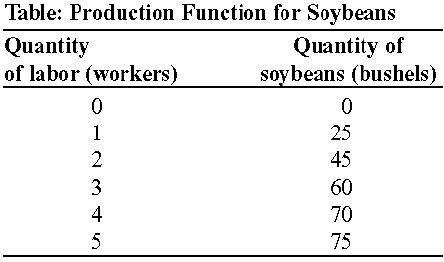

C)

10.

D)

6.

8.

The term diminishing returns refers to:

A)

a falling interest rate that can be expected as one’s investment in a single asset

increases.

B)

a reduction in profits caused by increasing output beyond the optimal point.

C)

a decrease in total output due to the firm hiring uneducated workers.

D)

a decrease in the extra output due to the use of an additional unit of a variable input

when all other inputs are held constant.

Page 3

9.

The idea of diminishing returns to an input in production suggests that if a local college

adds more custodians, the marginal product of labor for the custodial staff will:

A)

increase at an increasing rate.

B)

increase at a decreasing rate.

C)

decrease.

D)

not change.

10.

Diminishing returns to an input occur:

A)

when all inputs are fixed.

B)

when some inputs are fixed and some are variable.

C)

when all inputs are variable.

D)

only when there are no fixed inputs.

11.

If two firms are identical in all respects except that one has more of the fixed input

capital than another, the total product curve for the firm with more capital:

A)

must equal the total product curve for the firm with less capital.

B)

will lie above the total product curve for the firm with less capital.

C)

will lie below the total product curve for the firm with less capital.

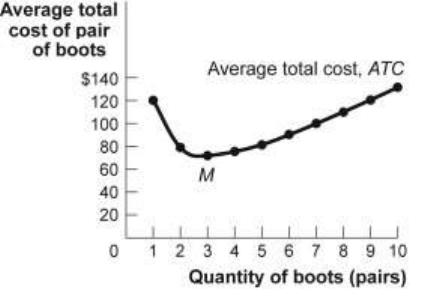

D)

will show no diminishing marginal returns.

12.

If two firms are identical in all respects except that one has more of the fixed input

capital than another, the marginal product curve for the firm with more capital:

A)

must equal the marginal product curve for the firm with less capital.

B)

will lie above the marginal product curve for the firm with less capital.

C)

will lie below the total marginal curve for the firm with less capital.

D)

will show no diminishing marginal returns.

Page 4

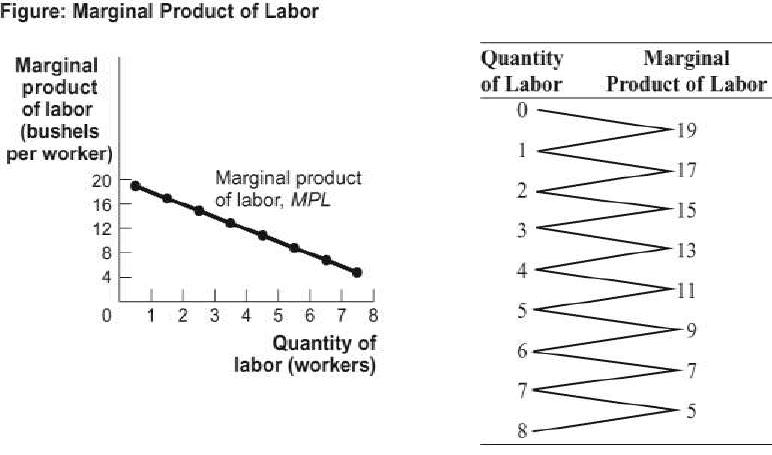

Use the following to answer questions 13-15:

13.

(Figure: Marginal Product of Labor) Look at the figure The Marginal Product of Labor.

The total product for three workers is _____ bushels.

A)

51

B)

45

C)

39

D)

15

14.

(Figure: Marginal Product of Labor) Look at the figure The Marginal Product of Labor.

The total product of labor for five workers is _____ bushels.

A)

11

B)

45

C)

55

D)

75

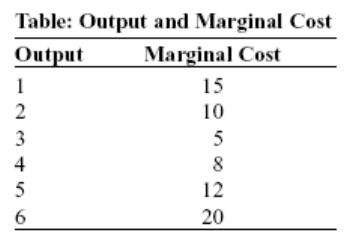

15.

(Figure: Marginal Product of Labor) Look at the figure The Marginal Product of Labor.

The total product of labor for eight workers is _____ bushels.

A)

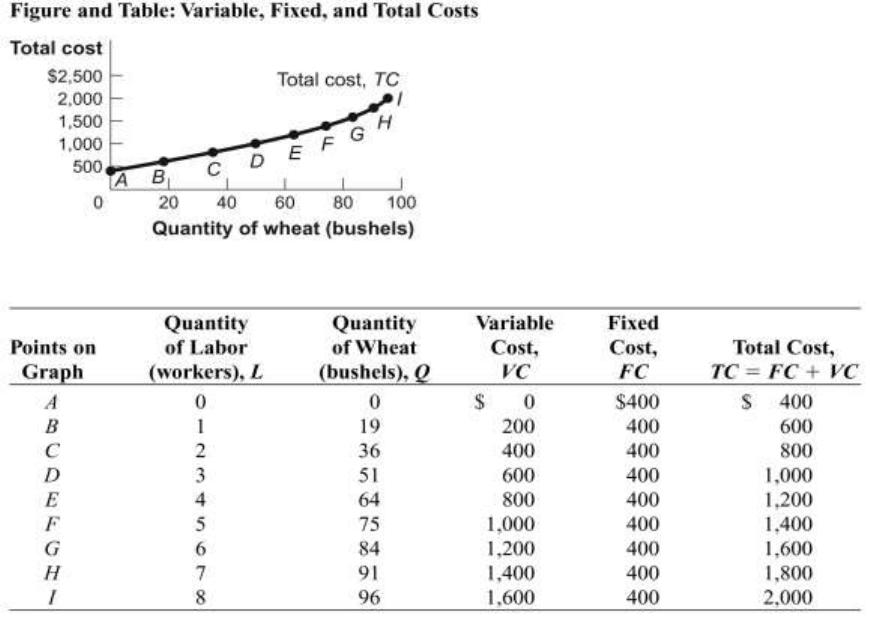

40

B)

35

C)

96

D)

75

Page 5

16.

In economics, the short run is defined as:

A)

less than 1 year.

B)

less than 6 months.

C)

the period in which some inputs are considered to be fixed in quantity.

D)

the period in which some inputs are fixed, but it cannot exceed 1 year.

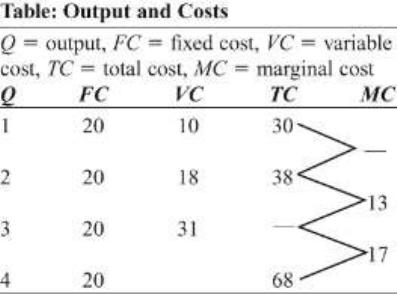

17.

In economics, the short run is:

A)

less than 1 week.

B)

less than 1 month.

C)

enough time to vary output but not plant capacity.

D)

enough time to change all inputs to production.

18.

An input whose quantity can be changed in the short run is a(n) _____ input.

A)

marginal

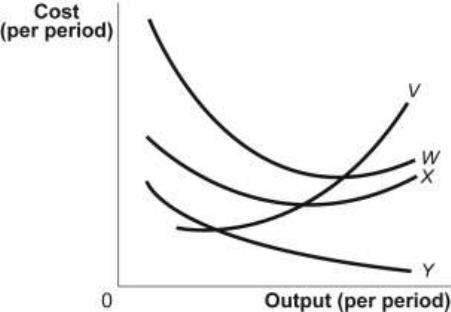

B)

fixed

C)

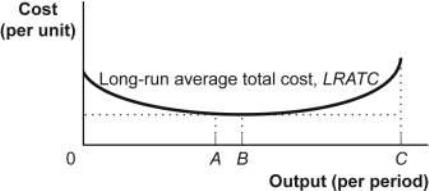

incremental

D)

variable

19.

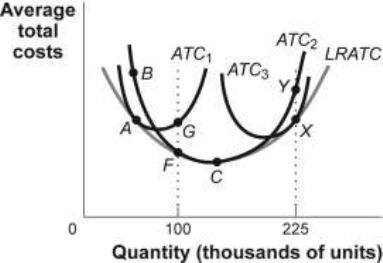

An input whose quantity CANNOT be changed in the short run is:

A)

marginal.

B)

fixed.

C)

incremental.

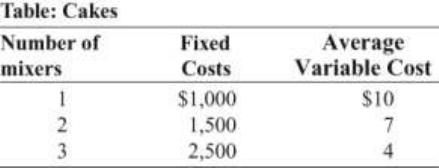

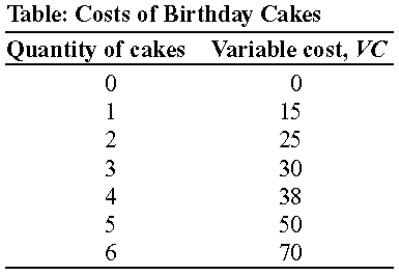

D)

variable.

20.

A fixed input is one:

A)

that exists in nature, and there is only so much of it.

B)

that can be used for one thing only.

C)

that can never produce more or less in any period.

D)

whose quantity cannot be changed in the short run.

21.

The long run is a planning period:

A)

over which a firm can consider all inputs as variable.

B)

of at least five years.

C)

of more than six months.

D)

of 6 months to 5 years.

Page 6

22.

In the long run:

A)

all inputs are fixed.

B)

inputs are neither variable nor fixed.

C)

at least one input is variable and one input is fixed.

D)

all inputs are variable.

23.

The _____ curve shows the quantities of output that can be obtained from different

quantities of a variable input, assuming other inputs are fixed.

A)

total input

B)

marginal input

C)

total product

D)

average total quantity

24.

A total product curve indicates the relationship between _____ when all other inputs are

fixed.

A)

a variable input and price

B)

a variable input and variable cost

C)

a variable input and output

D)

output and price

25.

The marginal product of labor is:

A)

the change in labor divided by the change in total product.

B)

the slope of the total product of labor curve.

C)

the change in average product divided by the change in the quantity of labor.

D)

the change in output that occurs when capital increases by one unit.

26.

A farm can produce 1,000 bushels of wheat per year with two workers and 1,300

bushels of wheat per year with three workers. The marginal product of the third worker

is _____ bushels.

A)

100

B)

300

C)

1,300

D)

2,300

Page 7

27.

When Caroline’s dress factory hires two workers, the total product is 50 dresses. When

she hires three workers, total product is 60, and when she hires four workers, total

product is 65. The slope of the marginal product curve when two to four workers are

hired is:

A)

upward.

B)

horizontal.

C)

vertical.

D)

downward.

28.

When Caroline’s dress factory hires two workers, the total product is 50 dresses. When

she hires three workers, total product is 60, and when she hires four workers, total

product is 75. The slope of the marginal product curve when two to four workers are

hired is:

A)

upward.

B)

downward.

C)

vertical.

D)

horizontal.

29.

When Caroline’s dress factory hires two workers, the total product is 50 dresses. When

she hires three workers, total product is 48, and when she hires four workers, total

product is 45. The marginal product of the third and fourth workers is:

A)

increasing and positive.

B)

increasing and negative.

C)

decreasing and positive.

D)

decreasing and negative.

Use the following to answer questions 30-32:

Page 8

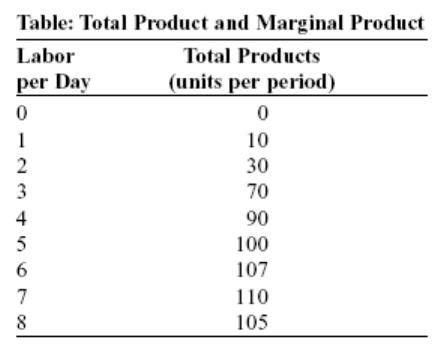

30.

(Table: Total Product and Marginal Product) Look at the table Total Product and

Marginal Product. The marginal product of the second worker is:

A)

10.

B)

15.

C)

20.

D)

30.

31.

(Table: Total Product and Marginal Product) Look at the table Total Product and

Marginal Product. The marginal product of the fourth worker is _____ units.

A)

20

B)

22.5

C)

50

D)

90

32.

(Table: Total Product and Marginal Product) Look at the table Total Product and

Marginal Product. Negative marginal returns begin when the _____ worker is added.

A)

fifth

B)

sixth

C)

seventh

D)

eighth

Use the following to answer questions 33-39:

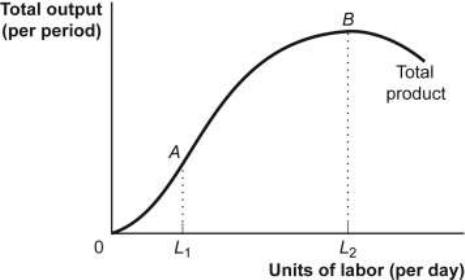

Figure: The Total Product

Page 9

33.

(Figure: The Total Product) Look at the figure The Total Product. Between points A and

B the marginal product of labor is:

A)

increasing.

B)

zero.

C)

falling.

D)

infinite.

34.

(Figure: The Total Product) Look at the figure The Total Product. Labor added from L1

and up to L2 is:

A)

subject to diminishing marginal returns.

B)

adding increasing amounts to total product.

C)

adding negative amounts to total product.

D)

adding negative amounts to total product and subject to diminishing marginal

returns.

35.

(Figure: The Total Product) Look at the figure The Total Product. As labor is hired

between L1 and L2, the total product is _____ and the marginal product is _____.

A)

rising; positive

B)

falling; zero

C)

rising; negative

D)

rising; zero

36.

(Figure: The Total Product) Look at the figure The Total Product. For hiring labor

between zero and L1:

A)

the marginal product of labor is increasing.

B)

the marginal product of labor is decreasing.

C)

the total product is increasing at a diminishing rate.

D)

the total product is decreasing.

37.

(Figure: The Total Product) Look at the figure The Total Product. After hiring L2 labor

and producing at point B on the total product curve, hiring more labor beyond L2 would

cause the:

A)

marginal product of labor to rise.

B)

marginal product of labor to be negative.

C)

total product to be negative.

D)

total product to be zero.

Page 10

38.

(Figure: The Total Product) Look at the figure The Total Product. When L2 labor is

hired, the total product is at a _____ and the marginal product of labor is _____.

A)

minimum; zero

B)

maximum; zero

C)

maximum; positive

D)

minimum; positive but falling

39.

(Figure: The Total Product) Look at the figure The Total Product. If the firm hires more

than L2 labor, the total product will _____ because the marginal product of labor is

_____.

A)

decrease; positive

B)

increase; positive

C)

decrease; negative

D)

increase; negative

40.

When an additional unit of a variable input adds less to total product than the previous

unit, the firm has:

A)

increasing returns.

B)

diminishing marginal returns.

C)

diminishing total returns.

D)

diminishing marginal returns and diminishing total returns.

41.

Diminishing marginal returns occur when:

A)

each additional unit of a variable factor adds more to total output than the previous

unit.

B)

each additional unit of a variable factor adds less to total output than the previous

unit.

C)

the marginal product of a variable factor is increasing at a decreasing rate.

D)

total product decreases.

42.

You own a deli. Which of the following is most likely a fixed input at your deli?

A)

the dining room

B)

the bread used to make sandwiches

C)

the tomato sauce used to make soups

D)

the employees

Page 11

43.

You own a deli. Which of the following is a decision most likely to be made in the

LONG run at your deli?

A)

You order more breadsticks.

B)

You order more soft drinks for next week.

C)

You renovate the second floor of your building to increase the size of the dining

room.

D)

You advertise for part-time workers.

Use the following to answer question 44:

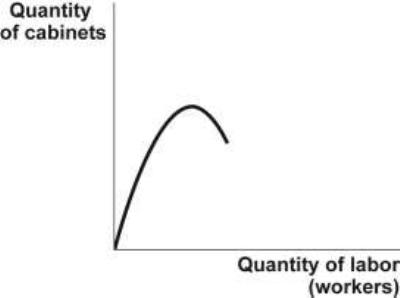

Figure: The Unknown Curve

44.

(Figure: The Unknown Curve) Look at the figure The Unknown Curve. You are a

cabinetmaker. You employ several workers to produce kitchen and bathroom cabinets.

Your summer intern has drawn a graph showing a relationship between the number of

cabinetmakers you employ and the number of cabinets produced. Unfortunately, your

intern has failed to identify this curve. It is likely to be the _____ curve:

A)

total cost

B)

total product

C)

marginal product

D)

total variable cost

Page 12

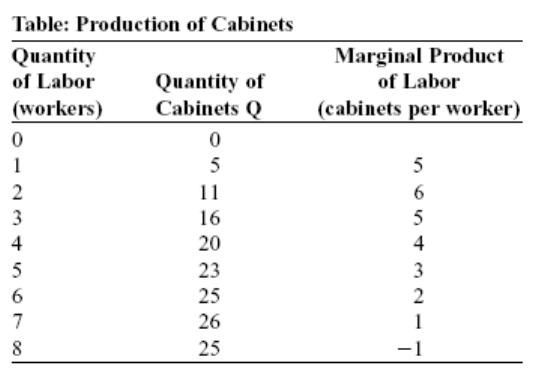

Use the following to answer questions 45-46:

45.

(Table: Production of Cabinets) Look at the table The Production of Cabinets. After the

_____ worker the firm begins to have diminishing returns to labor.

A)

first

B)

second

C)

third

D)

fourth

46.

(Table: Production of Cabinets) Look at the table The Production of Cabinets. If each

cabinetmaker could be hired at no cost, how many workers would your firm employ?

A)

two

B)

six

C)

seven

D)

eight

Page 13

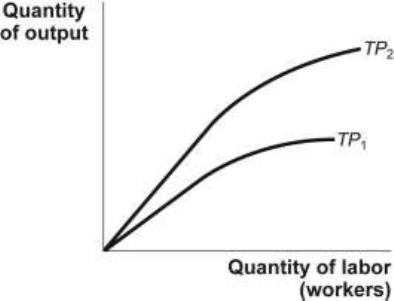

Use the following to answer questions 47-48:

Figure: Change in the Total Product

47.

(Figure: Change in the Total Product) Look at the figure Change in the Total Product.

Which of the following choices is a likely cause of the shift in production function from

TP1 to TP2?

A)

Workers in the firm are less productive on average.

B)

The firm employed more of a variable input in the short run.

C)

Available technology has decreased.

D)

The firm employed more of a fixed input in the long run.

48.

(Figure: Change in the Total Product) Look at the figure Change in the Total Product.

As indicated by the change in a production function from TP1 to TP2, the marginal

product of labor curve has:

A)

shifted upward.

B)

shifted downward.

C)

not moved.

D)

become inverted.

49.

A factor of production whose quantity can be changed during the SHORT run is a(n)

_____ factor of production.

A)

marginal

B)

fixed

C)

incremental

D)

variable

Page 14

50.

A factor of production whose quantity CANNOT be changed during the short run is a(n)

_____ factor of production.

A)

marginal

B)

fixed

C)

incremental

D)

variable

51.

Think about running a restaurant. Probably:

A)

cooks and hosts are variable resources.

B)

a building is a variable resource in the short run.

C)

cheese and other wholesale food items are fixed resources in the short run.

D)

valet parking staff is a fixed resource in the long run.

52.

As defined in the text, the long run is a planning period:

A)

in which a firm can adjust all resources.

B)

that is at least five years long.

C)

during which the firm must increase sales to stay in business.

D)

in which variable resources become fixed.

53.

A planning period during which all of a firm’s resources are variable is the _____ run.

A)

long

B)

fixed

C)

short

D)

nominal

54.

In the long run:

A)

the firm has time to change the level of all inputs.

B)

inputs are neither variable nor fixed.

C)

at least one input is free.

D)

all inputs are more expensive.

55.

The long run is:

A)

long enough to vary the quantities of all factors of production.

B)

long enough to vary all factors of production except for the amount of capital

available.

C)

more than one month.

D)

at least one year.

Page 15

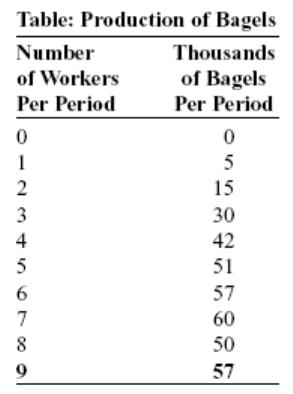

Use the following to answer questions 56-58:

56.

(Table: Production of Bagels) Look at the table Production of Bagels. The marginal

product of the third worker is _____ bagels.

A)

9,000

B)

10,000

C)

12,000

D)

15,000

57.

(Table: Production of Bagels) Look at the table Production of Bagels. The marginal

product of the fifth worker is _____ bagels.

A)

5,000

B)

9,000

C)

10,000

D)

12,000

58.

(Table: Production of Bagels) Look at the table Production of Bagels. Diminishing

marginal returns begin with the addition of the _____ worker.

A)

third

B)

fourth

C)

fifth

D)

sixth

Page 16

59.

Diminishing marginal returns means that:

A)

each additional unit of an input will decrease output.

B)

each additional unit of an input will increase output, but by smaller and smaller

amounts.

C)

each additional unit of an input will increase output by larger and larger amounts.

D)

the firm is maximizing profit.

60.

Assuming that all other factors of production are held constant, marginal product is the

change in _____ output resulting from a one-unit change in _____.

A)

total; a variable input

B)

total; a fixed input

C)

total; total product

D)

per unit; a fixed input

61.

The marginal product of labor is the change in _____ divided by the change in _____.

A)

labor; total product

B)

total output; the quantity of labor

C)

average output; the quantity of labor

D)

total costs; the quantity of labor

62.

A farm can produce 1,000 bushels of wheat per year with two workers or 1,300 bushels

of wheat per year with four workers. The marginal product of the fourth worker is

_____ bushels.

A)

100

B)

300

C)

1,300

D)

150

63.

The marginal product of labor is all of the following EXCEPT:

A)

the change in output resulting from a one-unit change in labor.

B)

the slope of the total product curve.

C)

positive at some levels of input and possibly negative at others.

D)

total product divided by total labor.

64.

Suppose that the first four workers generate corresponding total outputs of baby diapers

of 200, 350, 450, and 500, respectively. The marginal product of the second worker is:

A)

50.

B)

100.

C)

150.

D)

200.

Page 17

65.

Suppose that when a coal-mining firm hires one, two, three, four, and five workers, the

corresponding total outputs are 10, 15, 19, 22, and 24 tons, respectively. The marginal

product of the third worker is _____ tons.

A)

3

B)

4

C)

15

D)

19

66.

When a firm has diminishing marginal returns:

A)

its output is falling.

B)

marginal product is falling but is likely to be still positive.

C)

total product falls because marginal product is falling and positive.

D)

marginal product is always negative.

67.

The long run refers to the period for which:

A)

a fixed input exists.

B)

all inputs are variable.

C)

marginal costs are decreasing.

D)

diminishing returns raise marginal cost.

68.

The costs associated with variable inputs are _____, and the costs associated with _____

inputs are _____.

A)

variable; fixed; fixed

B)

fixed; fixed; variable

C)

variable; fixed; variable

D)

fixed; fixed; fixed

69.

Which of the following cost concepts is correctly defined?

A)

MC = TC / FC

B)

ATC = VC + FC

C)

ATC = AVC + AFC

D)

TC = AVC + AFC

70.

A cost that does not depend on the quantity of output produced is:

A)

marginal.

B)

fixed.

C)

variable.

D)

average.

Page 18

Use the following to answer questions 71-72:

71.

(Table: Total Cost Data) Look at the table Total Cost Data. What is the total fixed cost

for this bicycle firm?

A)

$40

B)

$50

C)

$100

D)

$70

72.

(Table: Total Cost Data) Look at the table Total Cost Data. What is the total variable

cost for this bicycle firm when the firm produces 5 bicycles?

A)

$50

B)

$240

C)

$60

D)

$190

73.

The total cost curve for a snowmobile dealership shows how _____ cost depends on the

quantity of _____.

A)

total; fixed inputs

B)

average; variable inputs

C)

total; output

D)

marginal; output

74.

A fixed cost:

A)

will exist only in the long run.

B)

depends on the level of output.

C)

can be positive, even if the firm doesn’t produce any output in the short run.

D)

decreases until the point of diminishing returns is reached.

Page 19

75.

The sum of fixed and variable costs is _____ cost.

A)

total

B)

marginal

C)

variable

D)

average

Use the following to answer questions 76-84:

76.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The fixed cost of producing 25 bushels of soybeans is:

A)

$50.

B)

$100.

C)

$150.

D)

$250.

77.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The variable cost of producing 25 bushels of soybeans is:

A)

$50.

B)

$100.

C)

$150.

D)

$250.

Page 20

78.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 25 bushels of soybeans is:

A)

$50.

B)

$100.

C)

$150.

D)

$250.

79.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The variable cost of producing 45 bushels of soybeans is:

A)

$100.

B)

$200.

C)

$350.

D)

$4,500.

80.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 45 bushels of soybeans is:

A)

$100.

B)

$200.

C)

$350.

D)

$4,500.

81.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The variable cost of producing 60 bushels of soybeans is:

A)

$5.

B)

$100.

C)

$150.

D)

$300.

Page 21

82.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 60 bushels of soybeans is:

A)

$150.

B)

$450.

C)

$750.

D)

$900.

83.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 70 bushels of soybeans is:

A)

$250.

B)

$400.

C)

$550.

D)

$1,024.

84.

(Table: Production Function for Soybeans) Look at the table Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 75 bushels of soybeans is:

A)

$650.

B)

$1,150.

C)

$1,225.

D)

$7,650.

85.

The total cost curve is:

A)

positively sloped.

B)

negatively sloped.

C)

vertical.

D)

horizontal.

86.

The fixed cost curve is:

A)

positively sloped.

B)

negatively sloped.

C)

vertical.

D)

horizontal.

Page 22

87.

Once diminishing returns have set in, as output increases, the total cost curve:

A)

gets steeper.

B)

gets flatter.

C)

becomes horizontal.

D)

increases at first, and then decreases.

88.

The total cost curve gets steeper as output increases because of:

A)

increasing returns to the variable input.

B)

decreasing returns to the variable input.

C)

increases in fixed cost.

D)

decreases in overhead costs.

89.

The change in total output resulting from a one-unit increase in the quantity of an input

used, holding the quantities of all other inputs constant, is:

A)

average cost.

B)

average product.

C)

marginal cost.

D)

marginal product.

90.

Austin’s total fixed cost at the bakery is $3,600 a month. Austin employs 20 workers and

pays each worker $8 an hour. The marginal product of the twentieth worker is 12 iced

cupcakes an hour. What is the marginal cost of the last cupcake produced by the last

worker Austin hired?

A)

$0.26

B)

$0.66

C)

$3.81

D)

$8.00

91.

For Heidi, the marginal cost of producing one additional photograph equals the change

in _____ divided by the change in the _____ of photographs.

A)

total cost; number

B)

marginal cost; number

C)

total cost; marginal product

D)

average cost; number

Page 23

92.

When a cherry orchard in Oregon adds a worker, the total cost of production increases

by $24,000. Adding the worker increases total cherry output by 600 pounds. Therefore,

the marginal cost of the last pound of cherries produced is:

A)

$40.

B)

$19.

C)

$4,000.

D)

$24,000.

93.

Marginal cost can be calculated as:

A)

TC / Q, where TC is total cost and Q is output.

B)

VC / Q, where VC is variable cost and Q is output.

C)

the slope of the total cost curve.

D)

TC / Q, where TC is total cost and Q is output; VC / Q, where VC is variable

cost and Q is output; and as the slope of the total cost curve.

94.

If the marginal cost of producing the seventh sports jersey is $21, then the total cost of

seven sports jerseys is:

A)

$21.

B)

$60.

C)

$147.

D)

The answer cannot be determined from the information provided.

95.

If Marie Marionettes is operating under conditions of diminishing marginal product, the

marginal costs will be:

A)

equal to average total cost.

B)

decreasing.

C)

increasing.

D)

constant.

96.

Buford Bus Manufacturing installs a new assembly line. As a result, the output per

worker increases. The marginal cost of output at Buford:

A)

will increase (the MC curve will shift up).

B)

will decrease (the MC curve will shift down).

C)

will be unchanged.

D)

is at its maximum.

Page 24

97.

If the marginal cost of the first sports jersey is $21, the marginal cost of the second

sports jersey is $40, and the marginal cost of the third jersey is $17, what is the total

variable cost of producing three jerseys?

A)

$26

B)

$78

C)

$17

D)

$61

98.

The shape of the marginal cost curve is the mirror image of the shape of the _____

curve.

A)

total product

B)

average product

C)

marginal product

D)

average total cost

99.

Ashley Bakery expects its marginal cost curve will eventually slope upward, because as

with most production processes, baking has:

A)

constant opportunity costs.

B)

a maximum efficient scale.

C)

diminishing marginal returns.

D)

decreasing opportunity costs.

100.

The _____ curve shows the additional cost of producing each additional unit of output.

A)

average cost

B)

total cost

C)

marginal product

D)

marginal cost

101.

Marginal cost is the change in _____ cost resulting from a one-unit change in _____.

A)

total; a variable input

B)

total; output

C)

total; average cost

D)

average; output

102.

A firm’s marginal cost is:

A)

the ratio of the change in total cost to the change in the quantity of output.

B)

the change in total cost divided by the change in labor input.

C)

the slope of the average fixed cost curve.

D)

total cost divided by output.

Page 25

103.

Marginal cost _____ over the range of increasing marginal returns and _____ over the

range of diminishing marginal returns.

A)

increases; decreases

B)

decreases; increases

C)

is constant; decreases

D)

increases; is constant

104.

Which of the following statements is FALSE?

A)

When the marginal product of labor is upward-sloping, the marginal cost curve is

upward-sloping.

B)

The average fixed cost curve is downward-sloping and approaches the horizontal

axis.

C)

The marginal cost curve intersects the average variable cost curve at the minimum

of average variable cost.

D)

When the marginal cost curve is above the average cost curve, the average cost

curve is upward-sloping.

105.

The curve that shows the additional cost of each additional unit of output is called the

_____ curve.

A)

average cost

B)

total cost

C)

marginal product

D)

marginal cost

106.

Marginal cost is the change in:

A)

total product resulting from a one-unit change in a variable input.

B)

total cost resulting from a one-unit change in quantity of a variable input.

C)

total cost divided by the change in output.

D)

average cost resulting from a one-unit change in quantity of output.

107.

The change in total cost resulting from a one-unit change in quantity is _____ cost.

A)

average fixed

B)

average variable

C)

marginal

D)

average total

Page 26

108.

A firm’s marginal cost is:

A)

the ratio of the change in fixed cost to the change in the quantity of output.

B)

the slope of the total cost curve.

C)

the slope of the average variable cost curve.

D)

the ratio of the change in total output to the change in the quantity of labor.

109.

Marginal cost is the:

A)

increase in total cost when one more unit of output is produced.

B)

reduction in cost from economies of scale.

C)

ratio of average total cost to total cost.

D)

increase in output from the addition of one unit of labor.

110.

The larger the output, the more output over which fixed cost is distributed. Called the

_____ effect, this leads to a ______ average _____ cost.

A)

spreading; lower; fixed

B)

spreading; higher; fixed

C)

diminishing returns; lower; variable

D)

diminishing returns; higher; variable

111.

The larger the output, the more variable input required to produce additional units.

Called the _____ effect, this leads to a ______ average _____ cost.

A)

spreading; lower; fixed

B)

spreading; higher; fixed

C)

diminishing returns; lower; variable

D)

diminishing returns; higher; variable

112.

The average total cost curve has a U shape because the ______ effect is dominant at low

levels of output, and the _____ effect is dominant at high levels of output.

A)

diminishing returns; spreading

B)

spreading; diminishing returns

C)

comparative advantage; absolute advantage

D)

absolute advantage; comparative advantage

113.

The rent for Oscar’s sporting goods store is $2,500 per month. Oscar pays his staff $9

per hour, and his monthly electricity bill averages $700, depending on his total hours of

operation. Oscar’s fixed costs of production equal:

A)

$2,500 per month.

B)

$3,200 per month.

C)

$9 per hour multiplied by total hours of work plus $700.

D)

$9 per hour multiplied by total hours of work plus $3,200.

Page 27

114.

Krista’s dry-cleaning business incurs $900 per month in fixed costs. Last month her total

output was 3,000 pounds of clothes. This month her total output fell to 2,700 pounds.

This means her average fixed cost _____ by a little more than _____.

A)

fell; 3.33 cents

B)

increased; 3.33 cents

C)

fell; 2.50 cents

D)

increased; 2.50 cents

115.

Darren runs a barbershop with average fixed costs of $60 per day and a total output of

50 haircuts per day. Darren shuts down every year during the last week of July and the

first week of August. What is his annual fixed cost if he is open six days per week?

A)

$18,000

B)

$3,000

C)

$60

D)

The answer cannot be determined with the information available.

116.

The average total cost of producing cell phones in a factory is $20 at the current output

level of 100 units per week. If fixed cost is $1,200 per week:

A)

average fixed cost is $20.

B)

total cost is $3,200.

C)

variable cost is $2,000.

D)

average variable cost is $8.

117.

Average variable cost equals all of the following EXCEPT:

A)

variable cost divided by output.

B)

the quantity total cost minus fixed cost divided by output.

C)

average total cost minus average fixed cost.

D)

variable cost times output.

118.

You run a business producing picture frames. This month your total cost of production

is $10,000, your variable cost of production is $6,000, and you produce 3,000 picture

frames. It follows that average _____ cost is _____.

A)

variable; $2

B)

total; $3

C)

total; $1

D)

fixed; $1

Page 28

119.

For most restaurants, the average total cost curve _____ at _____ levels of output, then

_____ at _____ levels.

A)

falls; low; rises; high

B)

rises; low; falls; high

C)

rises; high; rises; low

D)

falls; high; falls; low

120.

In the short run, the average total cost curve slopes upward because of:

A)

economies of scale.

B)

diseconomies of scale.

C)

increasing returns.

D)

diminishing returns.

121.

The _____ cost curve is NOT affected by diminishing returns.

A)

average fixed

B)

average variable

C)

average total

D)

marginal

122.

The _____ cost curve continually declines as more output is produced in the short run.

A)

marginal

B)

average variable

C)

average fixed

D)

average total

Use the following to answer questions 123-125:

Figure: The Average Total Cost Curve

Page 29

123.

(Figure: The Average Total Cost Curve) Look at the figure The Average Total Cost

Curve. The total cost of producing three pairs of boots is approximately:

A)

$24.

B)

$72.

C)

$75.

D)

$216.

124.

(Figure: The Average Total Cost Curve) Look at the figure The Average Total Cost

Curve. The total cost of producing five pairs of boots is approximately:

A)

$408.

B)

$82.

C)

$108.

D)

$17.

125.

(Figure: The Average Total Cost Curve) Look at the figure The Average Total Cost

Curve. The total cost of producing 10 pairs of boots is approximately:

A)

$13.

B)

$54.

C)

$131.

D)

$1,308.

126.

Average total cost is:

A)

the change in cost divided by the change in output.

B)

total cost divided by output.

C)

the change in output divided by the change in costs.

D)

total cost times output.

127.

Total cost divided by the quantity of output produced is:

A)

average total cost.

B)

average fixed cost.

C)

average product.

D)

marginal cost.

128.

Average variable cost is:

A)

variable cost per unit multiplied by output.

B)

total variable cost divided by output.

C)

the difference between average total cost and total variable cost.

D)

the difference between total cost and total variable cost.

Page 30

129.

Average variable cost is the ratio of:

A)

total cost to marginal cost.

B)

total cost to the amount of variable input.

C)

variable cost to the quantity of output.

D)

marginal cost to the quantity of output.

130.

A business produces 10 pairs of eyeglasses. It incurs $30 in average variable cost and $5

in average fixed cost. The average total cost of producing 10 pairs of eyeglasses is:

A)

$30.

B)

$35.

C)

$50.

D)

$300.

131.

A business produces 10 pairs of eyeglasses. It incurs $35 in average total cost and $5 in

average fixed cost. The average variable cost of producing 10 pairs of eyeglasses is:

A)

$30.

B)

$35.

C)

$50.

D)

$300.

132.

A business produces 10 pairs of eyeglasses. It incurs $30 in average variable cost and $5

in average fixed cost. The total cost of producing 10 pairs of eyeglasses is:

A)

$35.

B)

$50.

C)

$300.

D)

$350.

133.

A business produces 10 pairs of eyeglasses. It incurs $30 in average variable cost and

$35 in average total cost. The total fixed cost of producing 10 pairs of eyeglasses is:

A)

$3.

B)

$35.

C)

$50.

D)

$300.

134.

Average total cost is:

A)

the change in variable cost divided by the change in quantity.

B)

total cost divided by quantity.

C)

the change in quantity divided by the change in labor costs.

D)

total cost times quantity.

Page 31

135.

Average variable cost is:

A)

variable cost per unit multiplied by quantity.

B)

total variable cost divided by quantity.

C)

the difference between average total cost and total cost.

D)

the difference between total cost and total fixed cost.

136.

Average total cost is the ratio of _____ cost to _____.

A)

total; marginal cost

B)

total; quantity of output

C)

total; amount of variable input

D)

marginal; amount of variable input

137.

Total cost divided by the quantity of output produced is:

A)

always increasing.

B)

always decreasing.

C)

average total cost.

D)

marginal cost.

138.

Average variable cost is the ratio of:

A)

total cost to the marginal cost.

B)

variable inputs to fixed inputs.

C)

variable cost to the quantity of output.

D)

fixed costs to variable cost.

139.

Variable cost divided by the quantity of output produced is _____ cost.

A)

marginal

B)

average total

C)

average fixed

D)

average variable

140.

Tankao makes earbuds for mobile devices. When Tankao produces 20 sets of earbuds,

its average variable cost is $5 per set and its average total cost is $8 per set. Tankao’s:

A)

marginal cost is less than $3 per set.

B)

marginal cost is $3 per set.

C)

average fixed cost is $3 per set.

D)

marginal cost is equal to its average fixed cost.

Page 32

141.

Tankao makes Bluetooth sets for mobile devices. When 50 Bluetooth sets are produced

in the short run, the average variable cost is $30. Tankao’s average _____ cost is _____.

A)

total; $30.

B)

total; greater than $30.

C)

total; less than $30.

D)

fixed; $30.

142.

Austin’s total fixed cost is $3,600 a month at his cupcake bakery. Austin employs 20

workers and pays each worker $600 a month. If labor is his only variable cost, what is

Austin’s total cost?

A)

$3,600

B)

$1,200

C)

$15,600

D)

$12,000

143.

When marginal cost is rising:

A)

average variable cost must be rising.

B)

average total cost must be rising.

C)

average variable cost and average total cost must be falling.

D)

both average variable cost and average total cost may be rising or falling.

144.

When Aishe’s Bar-B-Que produces 10 pork sandwiches, the total cost is $5. When 11

pork sandwiches are produced, the total cost rises to $6. From this we know that the

marginal cost of the eleventh pork sandwich:

A)

is equal to the average cost of 11 pork sandwiches.

B)

is greater than the average cost of 11 pork sandwiches.

C)

is less than the average cost of 11 pork sandwiches.

D)

can’t be calculated without more information.

145.

Suppose the marginal cost curve in the short run first decreases and then increases. If

marginal cost is decreasing, _____ must be _____ and _____ must be _____.

A)

marginal product; increasing; average fixed cost; decreasing

B)

average variable cost; decreasing; average fixed cost; increasing

C)

average total cost; increasing; marginal cost; decreasing

D)

marginal product; increasing; average variable cost; decreasing

Page 33

146.

Suppose the marginal cost curve in the short run first decreases and then increases. If

marginal cost is increasing, _____ must be _____.

A)

marginal product; increasing

B)

average variable cost; increasing

C)

average total cost; increasing

D)

marginal product; decreasing

147.

At the current level of output, Becca Furniture’s marginal cost curve is above the

average total cost curve. This means Becca Furniture’s average total cost curve:

A)

must be rising.

B)

must be flat.

C)

must be falling.

D)

may be rising, falling, or flat depending on other things.

148.

The marginal cost curve intersects the average variable cost curve at:

A)

its lowest point.

B)

its maximum.

C)

its end point.

D)

no point; the curves don’t intersect.

149.

When marginal cost is BELOW average variable cost, average variable cost must be:

A)

at its minimum.

B)

at its maximum.

C)

falling.

D)

rising.

150.

When marginal cost is ABOVE average variable cost, average variable cost must be:

A)

at its minimum.

B)

at its maximum.

C)

falling.

D)

rising.

151.

If marginal cost is GREATER THAN average total cost:

A)

average total cost is increasing.

B)

average total cost is decreasing.

C)

average total cost is unchanged.

D)

marginal cost is decreasing.

Page 34

152.

If marginal cost is equal to average total cost:

A)

average total cost is increasing.

B)

average total cost is at its maximum.

C)

average total cost is at its minimum.

D)

marginal cost is decreasing.

153.

If an increase in output results in a decrease in average total cost, the corresponding

marginal cost is:

A)

less than average total cost.

B)

greater than average total cost.

C)

equal to average total cost.

D)

negative.

154.

When a fine caterer produces 30 catered meals, its marginal cost and average variable

cost each equal $10. Therefore, assuming normally shaped cost curves, at 29 meals its

marginal cost is _____ $10 and its average variable cost is _____ $10.

A)

more than; less than

B)

less than; more than

C)

more than; more than

D)

equal to; equal to

155.

When marginal cost is below average variable cost, average variable cost must be:

A)

above average total cost.

B)

below average fixed cost.

C)

falling.

D)

rising.

156.

When marginal cost is above average variable cost, average variable cost must be:

A)

at its minimum.

B)

at its maximum.

C)

greater than average total cost.

D)

increasing.

157.

If marginal cost is greater than average total cost, then average total cost is:

A)

at its maximum.

B)

at its minimum.

C)

increasing.

D)

decreasing.

Page 35

158.

If marginal cost is less than average total cost, then _____ cost is _____.

A)

average total; increasing

B)

average total; decreasing

C)

marginal; necessarily increasing

D)

marginal; necessarily decreasing

159.

Suppose Cyd knows the average total cost of producing 9 scones is $5, while the

average total cost of producing 10 scones is $5.20. What is the marginal cost of the tenth

scone?

A)

$7.00

B)

$5.20

C)

$0.20

D)

$5.00

Use the following to answer question 160:

160.

(Table: Output and Marginal Cost) Look at the table Output and Marginal Cost. After

graduation you achieve your dream of opening an art shop that specializes in selling

mud statues. How many statues should you produce to minimize your average variable

costs?

A)

two

B)

three

C)

four

D)

five

161.

Kaile Cakes produces 10 cakes per day. The marginal cost of the tenth cake is $24, and

average total cost of 10 cakes is $6. The average total cost of 9 cakes is:

A)

$4.

B)

$5.

C)

$6.

D)

$8.

Page 36

162.

Cindy operates Birds-R-Us, a small store manufacturing and selling 100 bird feeders per

month. Cindy’s monthly total fixed costs are $500, and her monthly total variable costs

are $2,500. If for some reason Cindy’s fixed cost fell to $400, then her _____ costs

would _____.

A)

average fixed; increase

B)

average total; decrease

C)

marginal; decrease

D)

average variable; decrease

163.

In the short run, as output gets larger:

A)

fixed cost gets smaller.

B)

the average variable cost curve gets closer to the average total cost curve.

C)

marginal cost gets smaller.

D)

average total cost decreases after the point of diminishing returns.

Use the following to answer questions 164-168:

Page 37

164.

(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table

Variable, Fixed, and Total Costs. The marginal cost of increasing production from 19 to

36 bushels of wheat is:

A)

$23.53.

B)

$11.76.

C)

$22.22.

D)

$11.11.

165.

(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table

Variable, Fixed, and Total Costs. The marginal cost of increasing production from 51 to

64 bushels of wheat is:

A)

$16.00.

B)

$15.38.

C)

$12.50.

D)

$18.75.

166.

(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table

Variable, Fixed, and Total Costs. The marginal cost of increasing production from 84 to

91 bushels of wheat is:

A)

$13.00.

B)

$19.78.

C)

$22.22.

D)

$28.57.

167.

(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table

Variable, Fixed, and Total Costs. When 51 bushels of wheat is produced, the average

fixed cost is _____, average variable cost is _____, and average total cost is _____.

A)

$7.84; $11.76; $19.60

B)

$133.33; $200.00; $333.33

C)

$400.00; $600.00; $1,000.00

D)

$5.33; $13.33; $18.67

168.

(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table

Variable, Fixed, and Total Costs. When 96 bushels of wheat is produced, the average

fixed cost is _____, average variable cost is _____, and average total cost is _____.

A)

$7.84; $11.76; $19.60

B)

$133.33; $200.00; $333.33

C)

$4.17; $16.67; $20.83

D)

$5.33; $13.33; $18.67

Page 38

Use the following to answer questions 169-173:

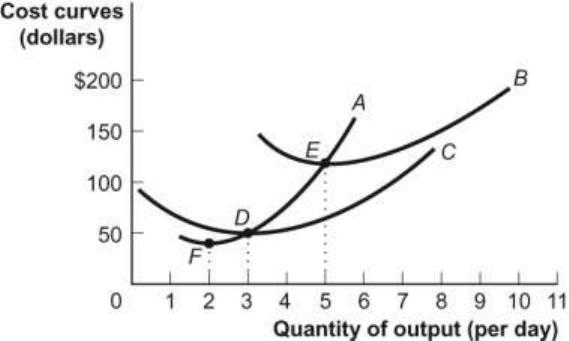

Figure: Short-Run Costs

169.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. A is the _____ cost

curve.

A)

average total

B)

average variable

C)

marginal

D)

total

170.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. B is the _____ cost

curve.

A)

average total

B)

average variable

C)

marginal

D)

total

171.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. C is the _____ cost

curve.

A)

average total

B)

total

C)

marginal

D)

average variable

Page 39

172.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. The vertical difference

between curve B and curve C at any quantity of output is _____ cost.

A)

marginal

B)

fixed

C)

average fixed

D)

average variable

173.

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. At 7 units of output,

average fixed cost is approximately _____, and average variable cost is approximately

_____.

A)

$100; $100

B)

$10; $135

C)

$40; $100

D)

$140; $140

Use the following to answer questions 174-181:

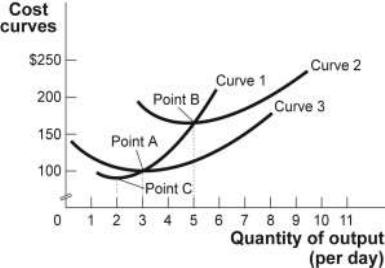

Figure: Short-Run Costs II

174.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. Curve 1 is the _____

cost curve.

A)

average total

B)

average variable

C)

marginal

D)

total

Page 40

175.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. Curve 2 is the _____

cost curve.

A)

average total

B)

average variable

C)

marginal

D)

total

176.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. Curve 3 is the _____

cost curve.

A)

average total

B)

total

C)

marginal

D)

average variable

177.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. Curve 1 crosses the

average variable cost curve at:

A)

3 units of output.

B)

approximately 5.3 units of output.

C)

the minimum value of curve 2.

D)

the level of output at which diminishing marginal returns begin.

178.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. Curve 1 crosses the

average total cost curve at:

A)

the minimum value of curve 2.

B)

approximately 4.3 units of output.

C)

approximately 2.8 units of output.

D)

point A.

179.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. At 6 units of output,

marginal cost is approximately:

A)

$100.

B)

$120.

C)

$250.

D)

$200.

Page 41

180.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. At 6 units of output,

average total cost is approximately:

A)

$100.

B)

$120.

C)

$170.

D)

$250.

181.

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. At 6 units of output,

average variable cost is approximately:

A)

$100.

B)

$120.

C)

$200.

D)

$250.

Use the following to answer questions 182-195:

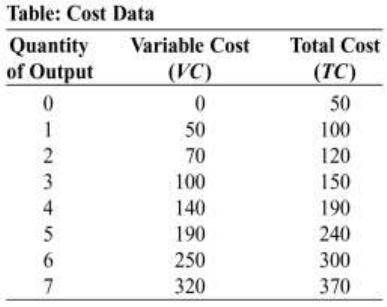

182.

(Table: Cost Data) Look at the table Cost Data. When the purse factory produces 5 units

of output (purses):

A)

marginal cost is above average total cost, and average total cost is rising.

B)

average total cost is above average variable cost, and average variable cost is

falling.

C)

marginal cost is below average variable cost, and average variable cost is falling.

D)

marginal cost is above average variable cost and below average total cost, and

average total cost is rising.

Page 42

183.

(Table: Cost Data) Look at the table Cost Data. The average variable cost of producing

2 purses is:

A)

$190.

B)

$70.

C)

$50.

D)

$35.

184.

(Table: Cost Data) Look at the table Cost Data. The average fixed cost of producing 2

purses is:

A)

$0.

B)

$50.

C)

$25.

D)

$2.

185.

(Table: Cost Data) Look at the table Cost Data. The average total cost of producing 2

purses is:

A)

$60.

B)

$120.

C)

$190.

D)

$220.

186.

(Table: Cost Data) Look at the table Cost Data. The marginal cost of producing the

second purse is:

A)

$60.

B)

$50.

C)

$35.

D)

$20.

187.

(Table: Cost Data) Look at the table Cost Data. The average variable cost of producing

4 purses is:

A)

$190.00.

B)

$140.00.

C)

$47.50.

D)

$35.00.

Page 43

188.

(Table: Cost Data) Look at the table Cost Data. The average fixed cost of producing 4

purses is:

A)

$12.50.

B)

$47.50.

C)

$50.00.

D)

$82.50.

189.

(Table: Cost Data) Look at the table Cost Data. The average total cost of producing 4

purses is:

A)

$12.50.

B)

$47.50.

C)

$50.00.

D)

$82.50.

190.

(Table: Cost Data) Look at the table Cost Data. The marginal cost of producing the

fourth purse is:

A)

$60.

B)

$50.

C)

$40.

D)

$20.

191.

(Table: Cost Data) Look at the table Cost Data. The average total cost of producing 6

purses is:

A)

$190.

B)

$70.

C)

$50.

D)

$35.

192.

(Table: Cost Data) Look at the table Cost Data. The average fixed cost of producing 5

purses is:

A)

$0.

B)

$50.

C)

$25.

D)

$10.

Page 44

193.

(Table: Cost Data) Look at the table Cost Data. The average variable cost of producing

5 purses is:

A)

$10.

B)

$38.

C)

$48.

D)

$190.

194.

(Table: Cost Data) Look at the table Cost Data. The average total cost of producing 5

purses is:

A)

$10.

B)

$38.

C)

$48.

D)

$240.

195.

(Table: Cost Data) Look at the table Cost Data. The marginal cost of producing the fifth

purse is:

A)

$60.

B)

$50.

C)

$35.

D)

$20.

Use the following to answer questions 196-198:

Figure: A Firm’s Cost Curves

Page 45

196.

(Figure: A Firm’s Cost Curves) Look at the figure A Firm’s Cost Curves. The curve

labeled V represents the firm’s _____ cost curve.

A)

total

B)

average total

C)

marginal

D)

average variable

197.

(Figure: A Firm’s Cost Curves) Look at the figure A Firm’s Cost Curves. The curve

labeled W represents the firm’s _____ cost curve.

A)

average fixed

B)

average total

C)

average variable

D)

total variable

198.

(Figure: A Firm’s Cost Curves) Look at the figure A Firm’s Cost Curves. The curve X

represents the firm’s _____ cost curve.

A)

marginal

B)

average total

C)

average fixed

D)

average variable

199.

The long-run average total cost curve is tangent to an infinite number of short-run _____

cost curves.

A)

total

B)

marginal

C)

average variable

D)

average total

200.

At the long-run quantity of output, where the long-run average total cost curve is at its

lowest point, it is tangent to the _____ of the corresponding short-run average total cost

curve.

A)

minimum

B)

maximum

C)

right of the minimum

D)

left of the minimum

Page 46

201.

At quantities less than the long-run minimum cost per unit of output, the long-run

average total cost curve is _____ of the corresponding short-run average total cost

curve.

A)

tangent to the minimum

B)

tangent to the maximum

C)

to the right of the minimum

D)

to the left of the minimum

202.

At quantities greater than the long-run minimum cost per unit of output, the long-run

average total cost curve is _____ of the corresponding short-run average total cost

curve.

A)

tangent to the minimum

B)

tangent to the maximum

C)

to the right of the minimum

D)

to the left of the minimum

Use the following to answer questions 203-204:

Figure: Long-Run and Short-Run Average Cost Curves

203.

(Figure: Long-Run and Short-Run Average Cost Curves) Look at the figure Long-Run

and Short-Run Average Cost Curves. If a firm faced the long-run average total cost

curve shown in the figure and it expected to produce 100,000 units of the good in the

long run, the firm should build the plant associated with:

A)

ATC1.

B)

ATC2.

C)

ATC3.

D)

ATC1 or ATC2.

Page 47

204.

(Figure: Long-Run and Short-Run Average Cost Curves) Look at the figure Long-Run

and Short-Run Average Cost Curves. If a firm is producing at point C on the ATC2 but

anticipates increasing output to 225,000 units in the long run, the firm will build a

_____ plant and have _____ of scale.

A)

smaller; economies

B)

smaller; diseconomies

C)

bigger; economies

D)

bigger; diseconomies

205.

In the long run, all costs are:

A)

fixed.

B)

constant.

C)

variable.

D)

marginal.

206.

In the long run:

A)

all factors are fixed.

B)

all factors are variable.

C)

production choices are more limited than in the short run.

D)

production is always greater than zero.

207.

When a firm adds physical capital, in the short run fixed costs will:

A)

increase.

B)

decrease.

C)

remain the same.

D)

decrease at first and then increase.

208.

When a firm adds capital, in the short run workers will be:

A)

less productive and let the machines do most of the work.

B)

more productive, since they have more equipment.

C)

at the same level of productivity.

D)

more productive at first and then less productive after a few weeks.

209.

When a firm adds capital, in the short run variable costs for any level of output will:

A)

increase.

B)

decrease.

C)

remain the same.

D)

increase at first and then decrease.

Page 48

Use the following to answer questions 210-236:

210.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer and bakes 100 cakes per day, what is her average fixed cost?

A)

$10,000

B)

$1,000

C)

$15

D)

$10

211.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer and bakes 100 cakes per day, what is her average total cost?

A)

$1,010

B)

$20

C)

$15

D)

$10

212.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer and bakes 200 cakes per day, what is her average fixed cost?

A)

$5

B)

$10

C)

$200

D)

$1,000

Page 49

213.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer and bakes 200 cakes per day, what is her average total cost?

A)

$5

B)

$15

C)

$200

D)

$1,000

214.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer and bakes 400 cakes per day, what is her average fixed cost?

A)

$0.025

B)

$2.50

C)

$1,000

D)

$400,000

215.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer and bakes 400 cakes per day, what is her average total cost?

A)

$2.50

B)

$10

C)

$12.50

D)

$1,010

216.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer, her average fixed cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

Page 50

217.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases one mixer, her average total cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

218.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 100 cakes per day, what is her average fixed cost?

A)

$10,000

B)

$1,000

C)

$15

D)

$10

219.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 100 cakes per day, what is her average total cost?

A)

$8

B)

$10

C)

$15

D)

$22

220.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 200 cakes per day, what is her average fixed cost?

A)

$300,000

B)

$1,508

C)

$187.50

D)

$7.50

Page 51

221.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 200 cakes per day, what is her average total cost?

A)

$8

B)

$14.50

C)

$1,492

D)

$1,508

222.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 400 cakes per day, what is her average fixed cost?

A)

$0.02

B)

$3.75

C)

$500

D)

$1,508

223.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 400 cakes per day, what is her average total cost?

A)

$0.02

B)

$10.75

C)

$500

D)

$1,507

224.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers, her average fixed cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

Page 52

225.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers, her average total cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

226.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers and bakes 100 cakes per day, what is her average fixed cost?

A)

$4

B)

$25

C)

$2,496

D)

$10,000

227.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers and bakes 100 cakes per day, what is her average total cost?

A)

$4

B)

$25

C)

$29

D)

$625

228.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers and bakes 200 cakes per day, what is her average fixed cost?

A)

$0.05

B)

$2.50

C)

$5.00

D)

$12.50

Page 53

229.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers and bakes 200 cakes per day, what is her average total cost?

A)

$50.00

B)

$12.50

C)

$16.50

D)

$800.00

230.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers and bakes 400 cakes per day, what is her average fixed cost?

A)

$0.05

B)

$2.50

C)

$5.00

D)

$6.25

231.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers and bakes 400 cakes per day, what is her average total cost?

A)

$10.25

B)

$12.50

C)

$16.50

D)

$2,504.00

232.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases three mixers, her average fixed cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

Page 54

233.

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in