Managerial Decision Modeling w/ Spreadsheets, 3e (Balakrishnan/Render/Stair)

Chapter 11 Forecasting Models

11.1 Chapter Questions

1) Consider the following data that was fitted using a Linear Trend.

Period

Actual value

(or) Y

Period number

(or) X

Period 1

10

1

Period 2

11

2

Period 3

9

3

Period 4

12

4

Period 5

13

5

Period 6

12

6

Period 7

15

7

The intercept of the trend line is 8.714, and the slope is 0.75. What is the forecast for period 8?

A) 13.714

B) 14.714

C) 15.714

D) 16.714

E) 15.75

2) Which of the following is considered to be a category of forecasting models?

A) Qualitative

B) Time-series

C) Causal models

D) both A and B

E) A, B, and C

3) Which of the following is NOT a qualitative method of forecasting?

A) Delphi Method

B) Trend Analysis

C) Jury of Executive Opinion

D) Sales Force Composition

E) Consumer Market Survey

4) Which of the following is NOT considered to be a Time-Series method of forecasting?

A) Simple Linear Regression

B) Moving Average

C) Exponential Smoothing

D) Seasonality Analysis

E) Multiplicative/Additive Decomposition

5) An iterative group process that allows experts, who may be located in different places, to make

forecasts is referred to as ________.

A) a jury of executive opinion

B) a sales force composite

C) ca onsumer market survey

D) the Delphi method

E) trend analysis

6) Consider the following data that was fitted using a linear trend.

Period

Actual value

(or) Y

Period number

(or) X

Period 1

10

1

Period 2

11

2

Period 3

9

3

Period 4

12

4

Period 5

13

5

Period 6

12

6

Period 7

15

7

The intercept of the trend line is 8.714, and the slope is 0.75. What is the forecast error for period 7?

A) 1.036

B) 8

C) 2.37

D) 5.714

E) 4.75

7) Consider the following data and Excel output for a simple linear regression model. How much of the

total variation in the dependent variable (Y) is explained by the independent variable (X)?

Period

Y

X

Period 1

10

1

Period 2

11

2

Period 3

9

3

Period 4

12

4

Period 5

13

5

Period 6

12

6

Period 7

15

7

Intercept

2.267

Slope

0.843

SE

1.810

Correlation

0.890

r-squared

0.791

A) 2.267

B) 0.843

C) 1.810

D) 0.890

E) 0.791

8) Consider the following data and its associated Excel output for a simple linear regression model.

How would you describe the linear relationship between Y and X?

Period

Y

X

Period 1

10

1

Period 2

11

2

Period 3

9

3

Period 4

12

4

Period 5

13

5

Period 6

12

6

Period 7

15

7

Intercept

2.267

Slope

0.843

SE

1.810

Correlation

0.890

r-squared

0.791

A) no relationship

B) positive relationship

C) negative relationship

D) inverse relationship

E) not enough information is provided

9) The value of the coefficient of determination R2 ranges between

A) 0 and -1

B) -1 and +1

C) 0 and +1

D) – infinity and + infinity

E) +1 and + infinity

10) The value of the correlation coefficient “r” ranges between

A) – infinity and + infinity

B) +1 and + infinity

C) 0 and -1

D) -1 and +1

E) 0 and +1

11) “Blips” in the data that follow no discernible pattern are referred to as

A) trend

B) random variations

C) seasonality

D) cycles

E) stationary variations

12) Consider the following forecast errors. What is the Mean Absolute Deviation (MAD)?

Period

Error

1

-2

2

1

3

3

4

0

5

-1

6

2

7

4

A) 1

B) 1.86

C) 7

D) 13

E) 5

13) Consider the following time series data. Suppose that you use exponential smoothing with an alpha

of 0.7 to fit a forecasting model. The forecast for period 7 is

Period

Forecast

Actual value

Period 1

10

10

Period 2

10

11

Period 3

10.7

9

Period 4

9.51

12

Period 5

11.253

13

Period 6

12.476

11

A) 10.443

B) 12

C) 9.443

D) 12.443

E) 11.443

14) The least squares method for linear regression:

A) minimizes the sum of the errors

B) minimizes the sum of the squared errors

C) maximizes forecasting accuracy

D) minimizes the value of the coefficient of determination R2

E) minimizes the regression equation coefficients

15) Suppose that you intend to use Solver to compute the optimal weights for a weighted moving

average. Changing variable cells would refer to:

A) the MAD cell

B) the MSE cell

C) the MAPE cell

D) the weights cells

E) the forecast cells

16) A time series which has a significant upward or downward trend is referred to as:

A) stationary time series

B) non-stationary time series

C) random time series

D) cyclical time series

E) seasonal time series

17) The basic exponential smoothing formula is:

A) Ft = Ft+1 + α(At – Ft )

B) Ft+1 = Ft-1 + α(At – Ft )

C) Ft+1 = Ft-1 + α(At – Ft )

D) Ft+1 = Ft + α(At – Ft)

E) Ft = Ft+1 + α(At – Ft )

18) In using a moving average forecasting technique, as the number of averaging period, k, increases:

A) the forecast will respond more quickly to recent changes in the data

B) the forecast will be more accurate especially if the data exhibits a trend

C) the moving average will increase in value

D) the moving average approximates the weighted moving average

E) the moving average will smooth out variations

19) Time series models usually incorporate variables or factors that are perceived to influence the

variable being forecasted.

20) Cycles, one of the components of time series, is a pattern that repeats itself during the exact same

time period.

21) A moving average forecast tends to be more responsive to recent changes in the data series when

more data points are included in the average.

22) A smoothing constant of .1 will cause an exponential smoothing forecast to react less quickly to a

sudden change than a value of .3 will.

23) A time series that is unseasonalized may exhibit a trend, a random component, and a seasonal

pattern.

24) In an exponential smoothing forecast, the value of the smoothing constant alpha can range between –

1 and +1.

25) A multiple regression model may include one or more dependent variables.

26) In general, the higher the value of the coefficient of determination R2, the better the fit of the

regression model.

27) If a time series exhibits a strong, linear upward trend, the value of the correlation coefficient, r, is

expected to be positive and close to -1.

28) Removing the seasonal component from a data series (i.e., unseasonalization) can be accomplished

by multiplying each data point by its appropriate seasonal index.

29) The time series component random variation usually shows a discernible pattern and is easy to

forecast.

30) Moving averages are useful in forecasting stationary time series as they tend to smooth out random

variations.

31) In an exponential smoothing forecast, the weight associated with older data increases exponentially

over time.

32) A farmer develops a simple regression model to determine if there is a relationship between the

amount of crop that he will harvest and the amount of rainfall. In this example, the variable “rainfall”

would be the dependent variable.

33) The smaller the value of the standard error of the regression estimate, the better the fit of the

regression model.

11.2 Excel Problems

Use this information to answer the following questions.

The following time series represent the total population of the United States, in thousands, over the last

12 years.

Year

Population (in 000s)

1991

253,493

1992

256,894

1993

260,255

1994

263,436

1995

266,557

1996

269,667

1997

272,912

1998

276,115

1999

279,295

2000

282,434

2001

285,545

2002

288,600

1) Refer to the table above.

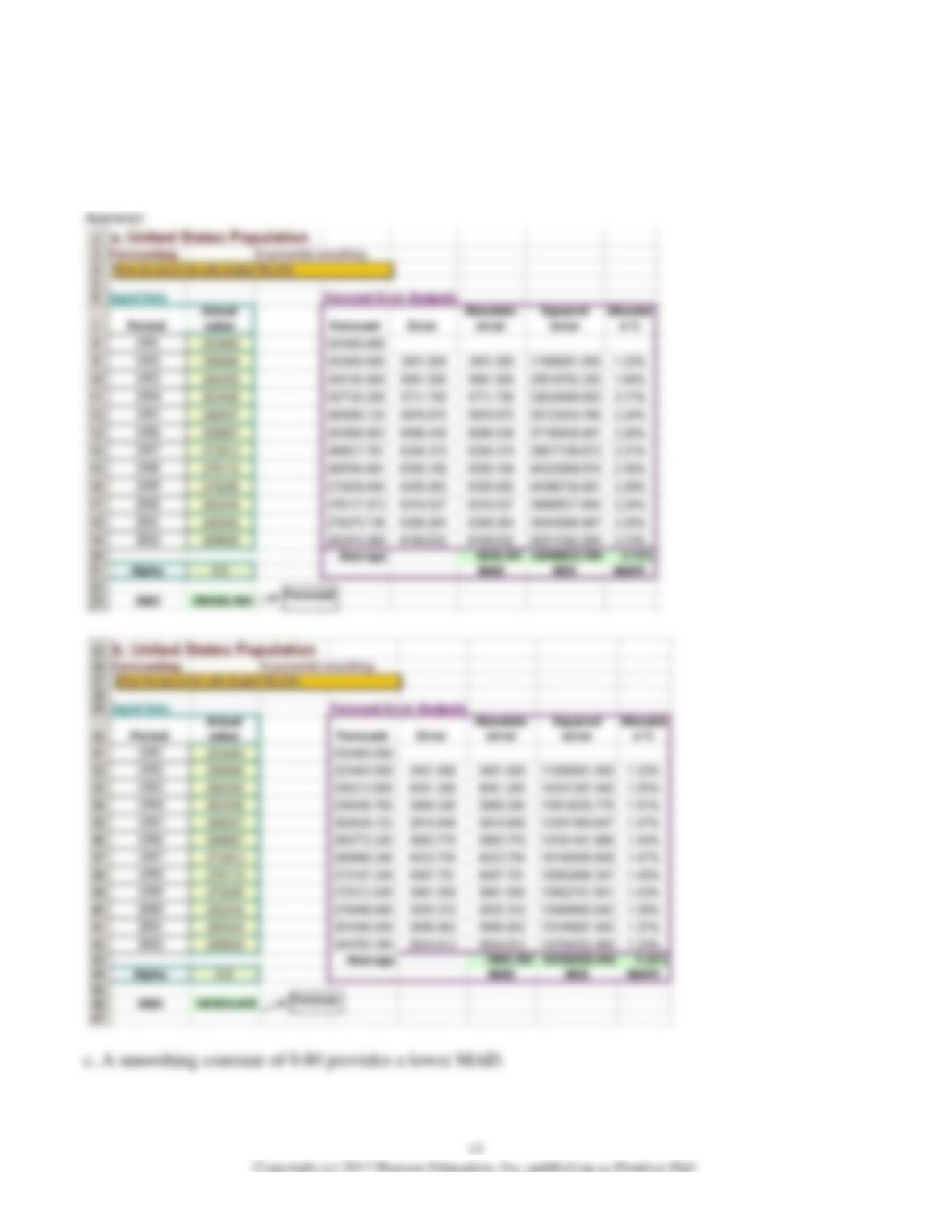

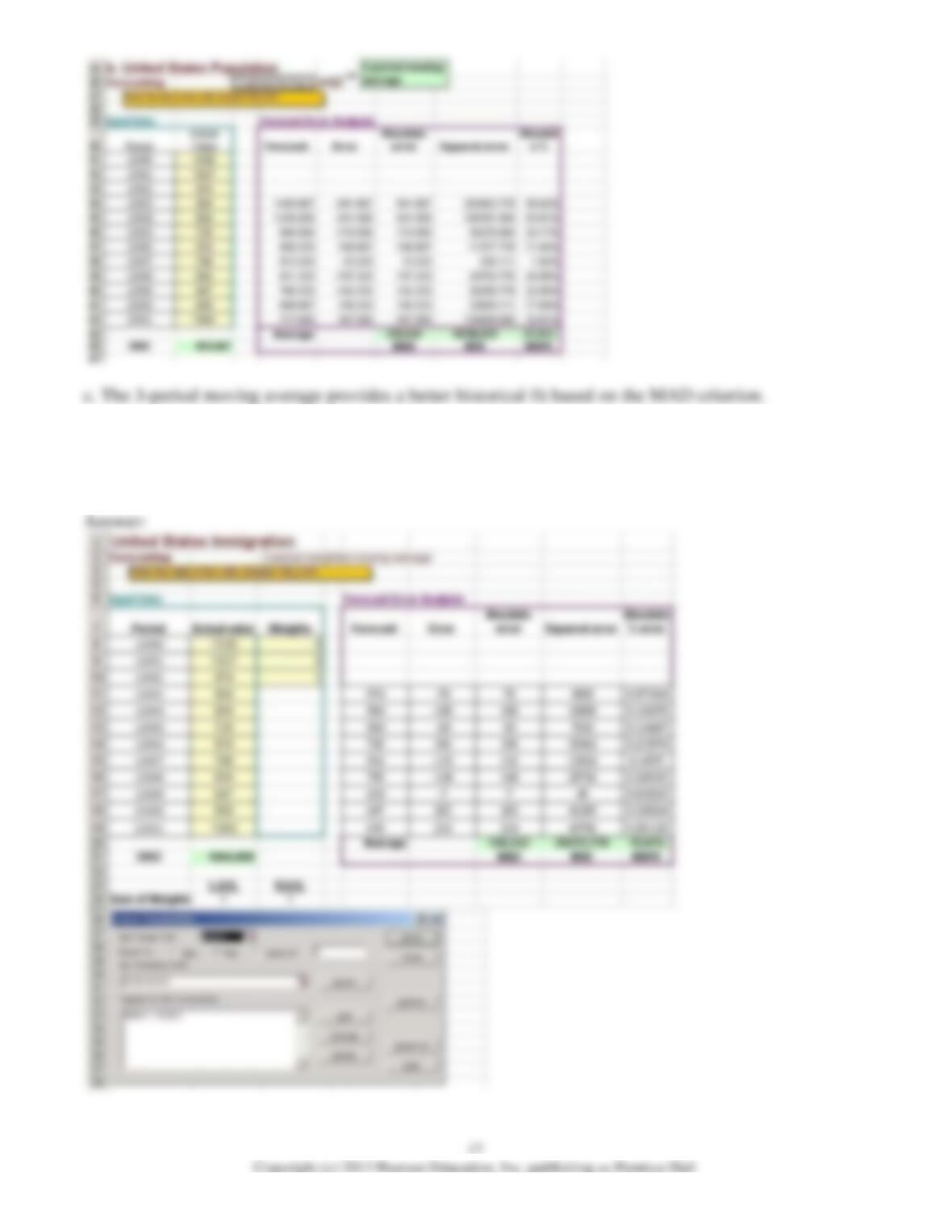

a. Use a 2-period moving average to forecast the population of the United States in 2003.

b. Use a 3-period moving average to forecast the population of the United States in 2003.

c. Which averaging period provides a better historical fit based on the MAD criterion?

2) Refer to the table above. Use a 3-period weighted moving average to forecast the population of the

United States in 2003. Use Solver to determine the optimal weights based on minimizing the MAD

criterion.

3) Refer to the table above.

a. Use exponential smoothing with a smoothing constant of 0.5 to forecast the population of the United

States in 2003.

b. Use exponential smoothing with a smoothing constant of 0.8 to forecast the population of the United

States in 2003.

c. Which of the two methods provides a more accurate forecast based on the MAD criterion?

4) Refer to the table above. Using Solver to find the optimal alpha that minimizes MAD, use exponential

smoothing to forecast the population of the United States in 2003.

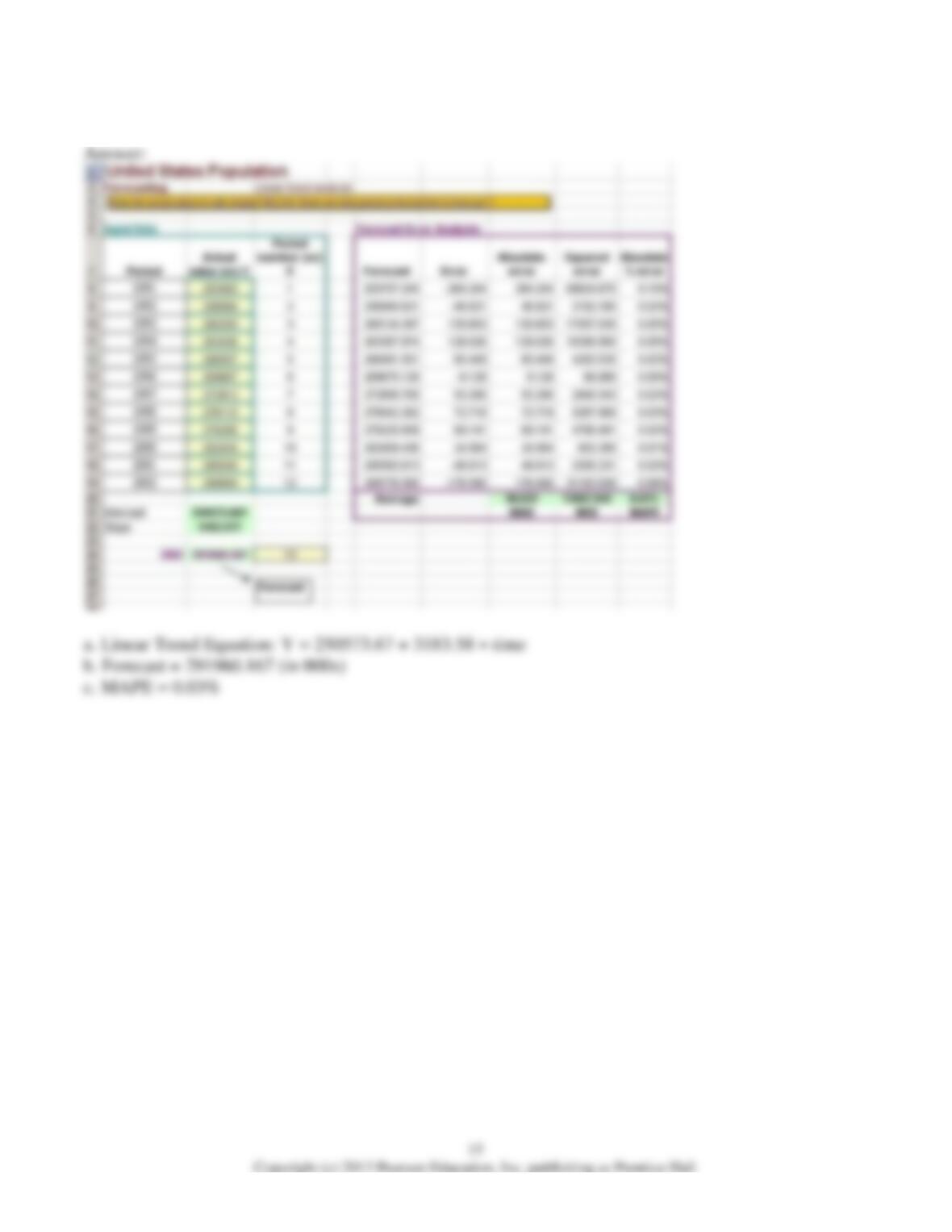

5) Refer to the table above. a. What is the linear trend equation that best fits the data?

b. What is the forecast of the population of the United States in 2003 using the linear trend equation?

c. What is the MAPE for this method?

Use this information to answer the following questions.

The following data, provided by the U.S. Bureau of Citizenship and Immigration Services, represent the

number of immigrants admitted to the United States, in thousands, from 1990-2001.

Year

No. of Immigrants

(in 000s)

1990

1536

1991

1827

1992

974

1993

904

1994

804

1995

720

1996

916

1997

798

1998

654

1999

647

2000

850

2001

1064

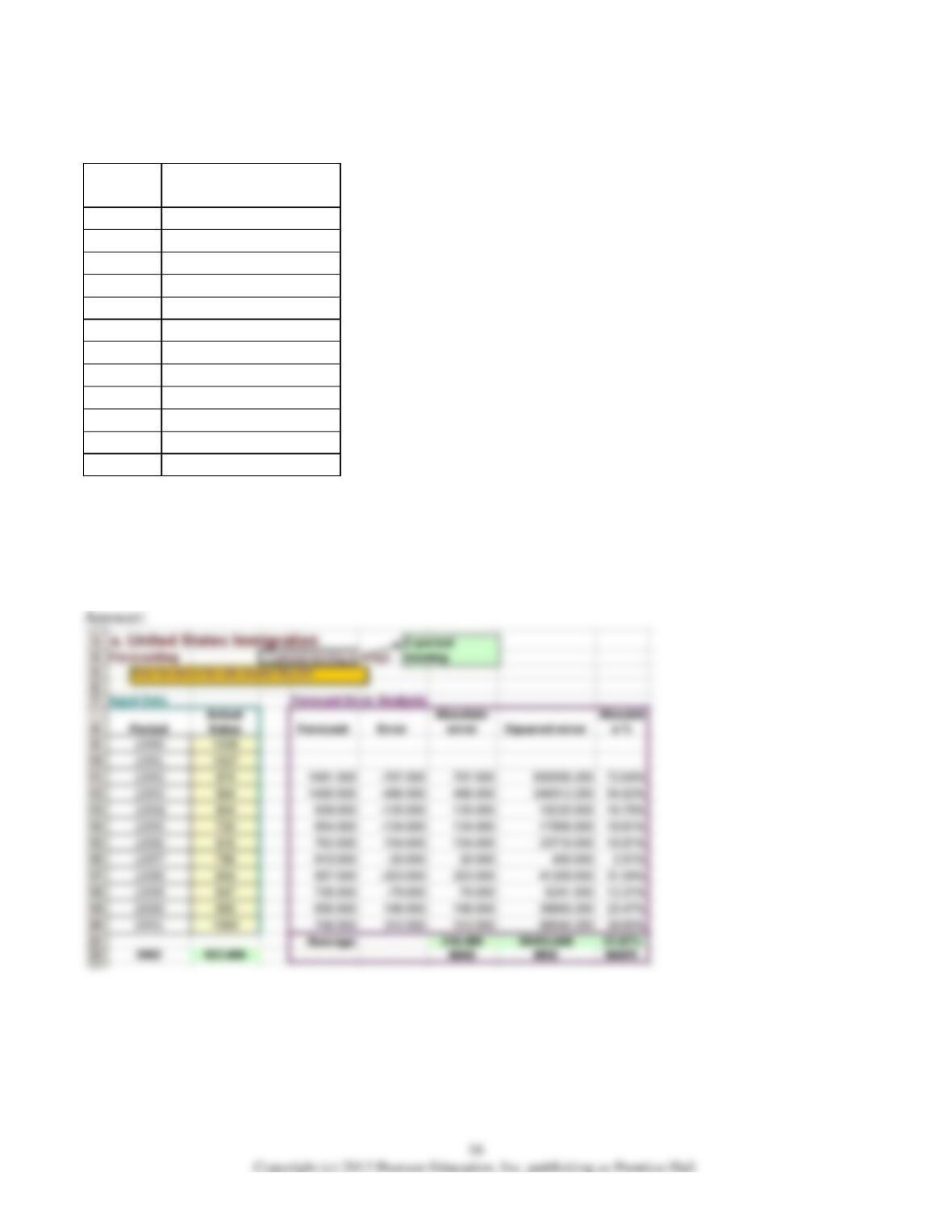

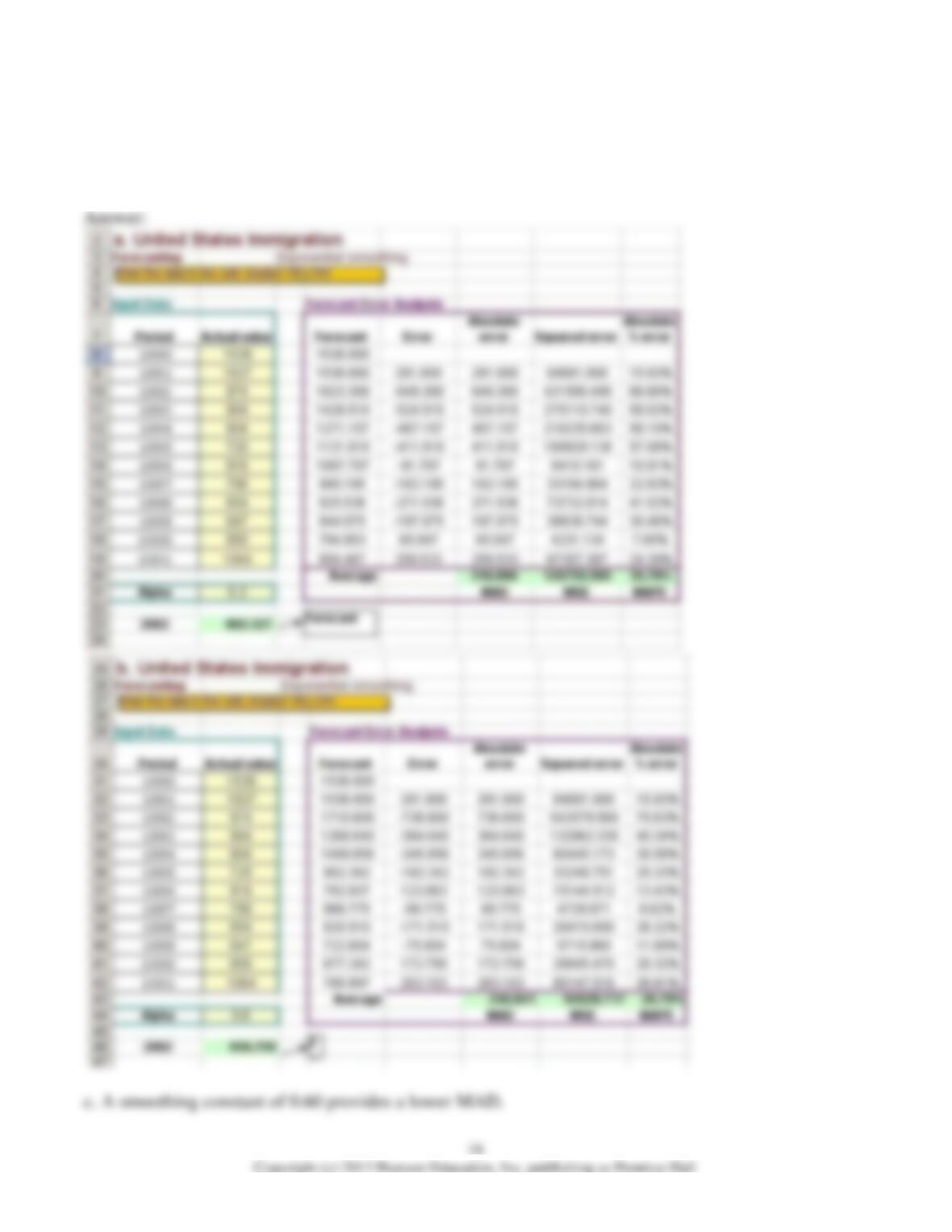

6) Refer to the table above.

a. Use a 2-period moving average to forecast the number of immigrants in 2002.

b. Use a 3-period moving average to forecast the number of immigrants in 2002.

c. Which averaging period provides a better historical fit based on the MAD criterion?

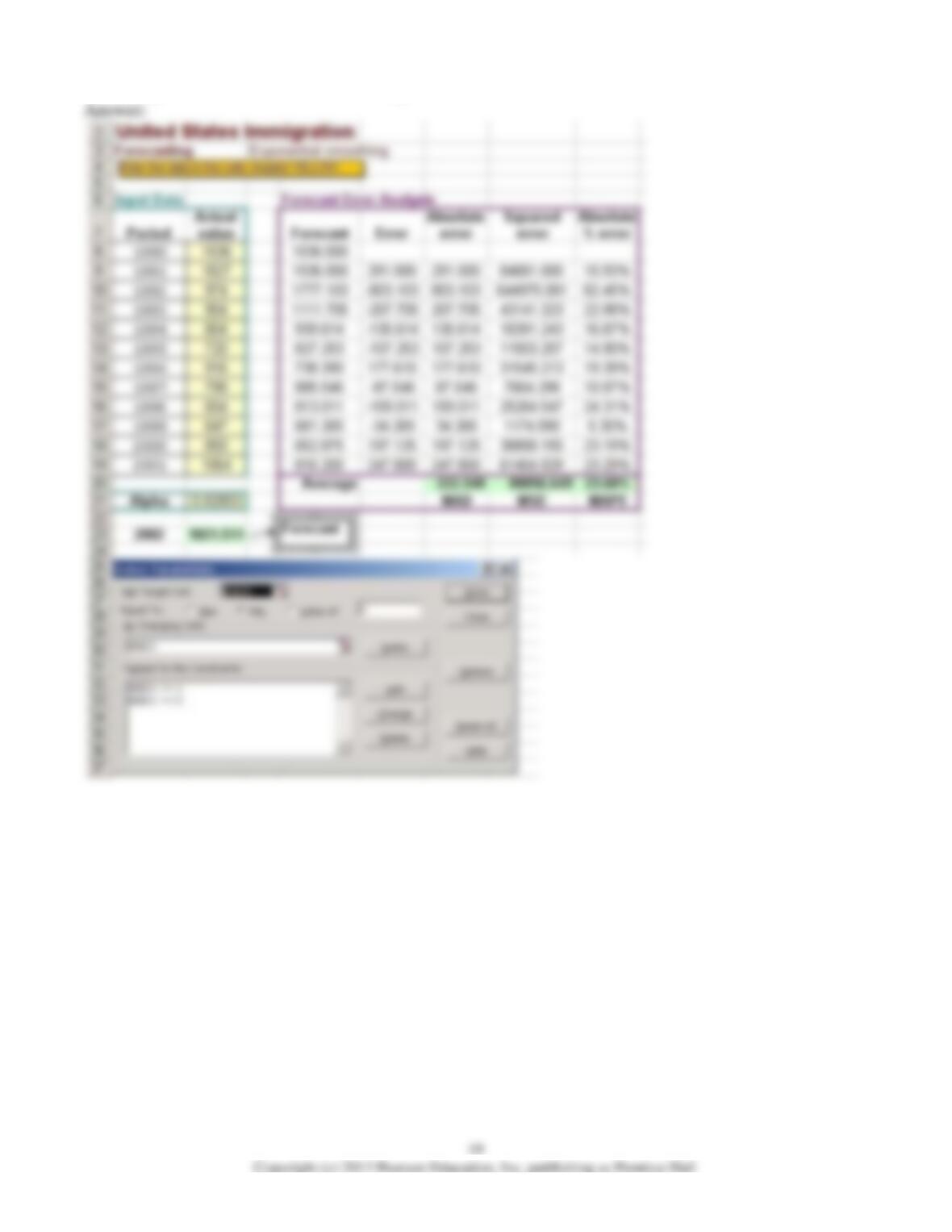

7) Refer to the table above. Use a 3-period weighted moving average to forecast the number of

immigrants in 2002. Use Solver to determine the optimal weights based on minimizing the MAD

criterion.

8) Refer to the table above.

a. Use exponential smoothing with a smoothing constant of 0.3 to forecast the number of immigrants in

2002.

b. Use exponential smoothing with a smoothing constant of 0.6 to forecast number of immigrants in

2002.

c. Which of the two methods provides a more accurate forecast based on the MAD criterion?

9) Refer to the table above. Using Solver to find the optimal alpha that minimizes MAD, use exponential

smoothing to forecast the number of immigrants in 2002.

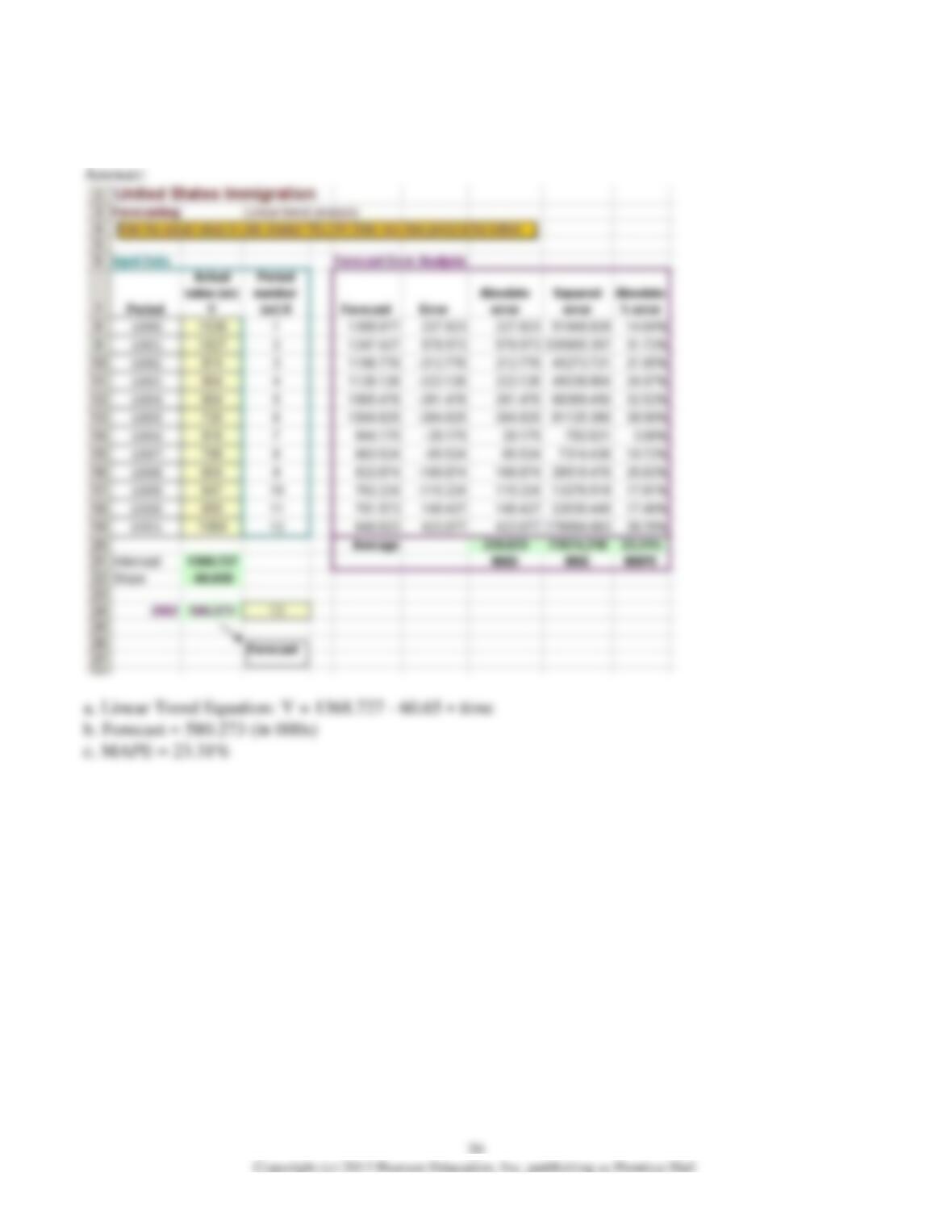

10) Refer to the table above.

a. What is the linear trend equation that best fits the data?

b. What is the forecast of the number of immigrants in 2002 using the linear trend equation?

c. What is the MAPE for this method?