Chapter 11: Stockholders’ Equity

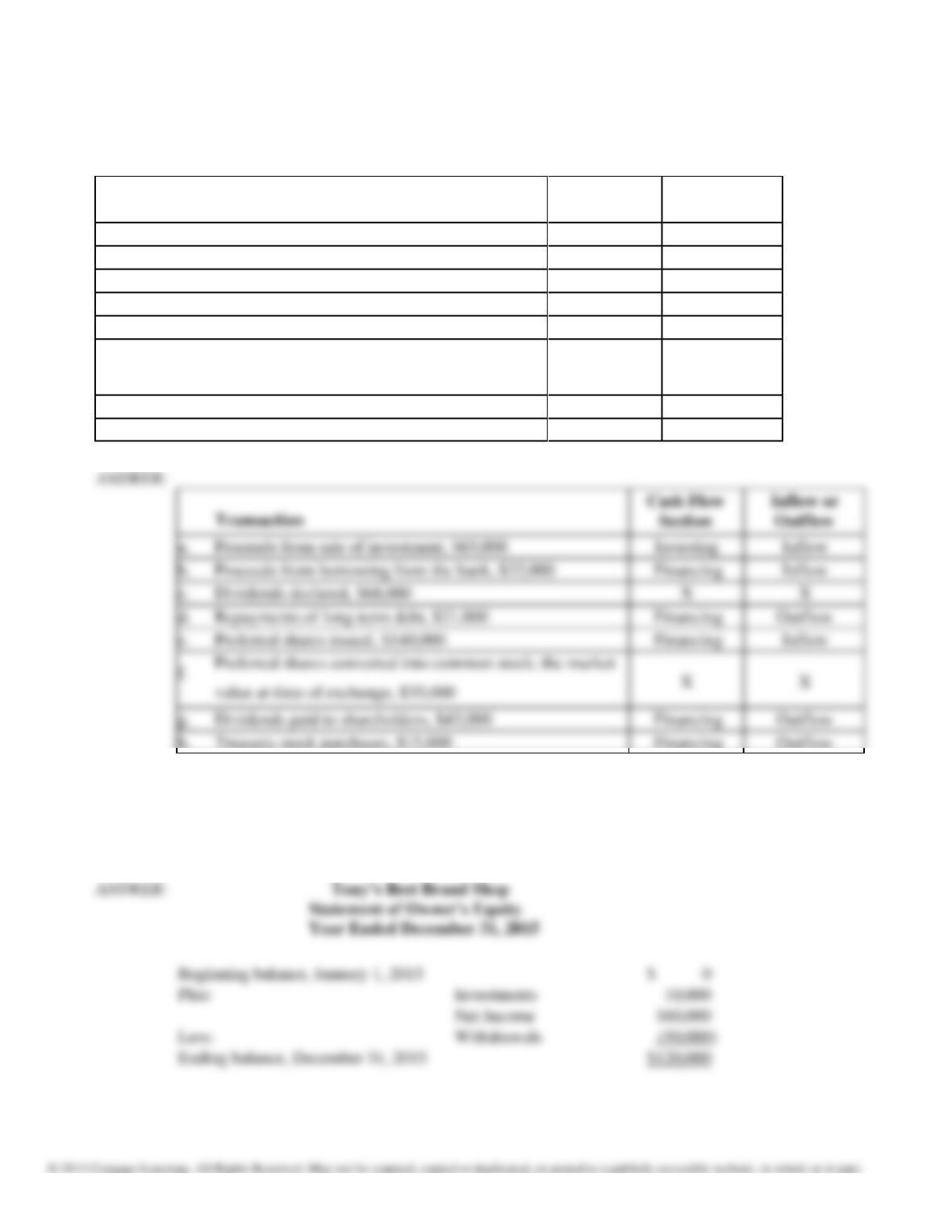

178. Information taken from the accounting records of Airways, Inc., for the year ended December 31, 2015, appears

in the table below. In the space provided, indicate in which section of the statement of cash flows (investing or

financing) each item would be reported, and whether the item is a cash inflow or outflow. If an item is neither an

investing activity or financing activity, place an X in the box.

Transaction

Cash Flow

Section

Inflow or

Outflow

a. Proceeds from sale of investment, $65,000

b. Proceeds from borrowing from the bank, $32,000

c. Dividends declared, $68,000

d. Repayments of long-term debt, $21,000

e. Preferred shares issued, $140,000

f. Preferred shares converted into common stock; the market

value at time of exchange, $35,000

g. Dividends paid to shareholders, $43,000

h. Treasury stock purchases, $15,000

Cash Flow

Section

Inflow or

Outflow

179. [APPENDIX] Tony Venato opened Tony’s Best Brand Shop as a sole proprietorship by investing $10,000 on

January 1, 2015. During the first year, the business earned revenues of $520,000 and incurred expenses of

$360,000. Tony withdrew $50,000 for personal use. Prepare Tony’s statement of owner’s equity for the year

ended December 31, 2015.

Chapter 11: Stockholders’ Equity

180. [APPENDIX] Chad Jones established Jones’ Cleaning Services, a sole proprietorship, by investing $1,000 on

January 1, 2015. During the first year of operations, the business generated net income of $42,000. The owner

withdrew cash for personal use. The ending balance of the capital account was $20,000. Prepare Jones’ statement

of owner’s equity for the year ended December 31, 2015.

181. [APPENDIX] Derek and Kent are partners. At the beginning of the current year, Derek’s capital account is

$30,000, while Kent’s is $50,000. The partners decided to allocate income with 10% interest on capital balances at

the beginning of the period and divide the balance equally. Net income for the current year, 2015, is $80,000. Each

partner withdrew $15,000 for personal use during the year. Determine the amount of income that each partner will

be allocated.

182. [APPENDIX] Fowler Company opened business as a sole proprietorship on January 1, 2015. The owner

contributed $525,000 cash on that date. During the year, the company had a net income of $20,000. The

company purchased equipment of $120,000 during the year. The owner also withdrew $75,000 to pay for

personal expenses during 2015.

REQUIRED:

Determine the company’s owner’s equity at December 31, 2015.

Chapter 11: Stockholders’ Equity

Ending balance

183. [APPENDIX] Body Sports is a surf shop owned by Chris, Nicole, and Dan in partnership. On January 1,

2015, their capital balances were as follows:

Chris, Capital

$30,000

Nicole, Capital

60,000

Dan, Capital

40,000

During 2015, Chris withdrew $10,000; Nicole, $20,000; and Dan, $15,000. Income for the partnership for 2015

was $75,000.

REQUIRED:

If the partners agreed to allocate income equally, what was the ending balance in each of their capital accounts on

December 31, 2015?

184. Stella Gregson received a windfall from one of her investments. She would like to invest $100,000 of the

money in Shoreline Industries, which is offering common stock, preferred stock, and bonds on the open

market. The common stock has paid $8 per share in dividends for the past three years, and the company expects

to be able to perform as well in the current year. The current market price of the common stock is $100 per

share. The preferred stock has an 8% dividend rate, cumulative and nonparticipating. The bonds are selling at

par with an 8% stated rate.

Required:

1. What are the advantages and disadvantages of each type of investment?

2. Recommend one type of investment over the others to Stella and justify your reason.

185. Contrast the two parts of stockholders’ equity.

186. Explain what amount is recorded in the Additional Paid-in Capital account when stock is issued.

Chapter 11: Stockholders’ Equity

187. Many firms operate at a dividend payout ratio of less than 50%. Why don’t firms pay a larger percentage of

income as dividends?

188. Why is stockholders’ equity viewed as a residual amount?

189. Explain the difference between IFRS and U.S. GAAP presentation for bonds that can be converted by

investors into stock.

190. Explain the difference between authorized, issued, and outstanding shares.

191. What is the difference between par value and market value? Which is the better indicator of the true worth of

the stock?

192. What is meant by the balance in the retained earnings account?

193. What is substance over form and how does this concept relate to the presentation of preferred stock?

Chapter 11: Stockholders’ Equity

194. Explain the two ways that a dividend rate on preferred stock may be stated by giving examples.

195. Gemini Company has the following accounts in the Stockholders’ Equity category of the balance sheet:

Common Stock, $10 no par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Preferred Stock, $100 par, 8%, cumulative, participating, 1,000 shares authorized, issued, and outstanding

Required:

1. Explain how the issuance of stock affects the financial statements when the stock has no par value.

2. Why would preferred stockholders want to have a cumulative feature in preferred stock?

3. When a participating feature is present in preferred stock, how does it affect the amount of dividends

that preferred stockholders can expect to receive?

196. Name two different examples of items that can be received (in addition to cash) in exchange for issuing

stock. Describe how the value of each item affects additional paid-in capital.

197. Chad Darrow, CFO of your company is considering constructing a deal with Extreme Industries, whereby stock

is issued in exchange for an asset (custom extrusion equipment valued at $400,000 by an outside appraiser). The

stock to be exchanged is a new class of preferred stock that has not yet been traded in the open market. He has

asked that you draft a memo to Marc Lyon, CEO about the valuation of the asset to be used in the exchange. In

your memo address the reporting amount for the asset and how fair market value could be determined.

Chapter 11: Stockholders’ Equity

198. What is treasury stock? How is it reported on the financial statements?

199. a. Explain what the dividend payout ratio is and which firms typically have a high ratio and which firms may

have the lowest.

b. Many firms operate at a dividend payout ratio of less than 50%. Why do many firms not pay a larger percentage

of income as dividends?

200. Contrast stock dividends and stock splits.

201. What is comprehensive income and what is contained in a statement of comprehensive income?

202. What is the difference between book value and market value of stock?

203. What section of the statement of cash flows is related to the Stockholders’ Equity section of the balance sheet?

Name four different transactions that are reported in that section that relate to the statement of cash flows.

204. [APPENDIX] Explain the differences between a partnership and sole proprietorship. Include in your

discussion whether either is considered a separate legal entity.

Chapter 11: Stockholders’ Equity

205. [APPENDIX] What are the advantages of organizing a company as a corporation instead of a partnership or

sole proprietorship?

206. [APPENDIX] Which accounts are used by a sole proprietorship that are not used by a corporation?

Match the terms to the definitions by selecting the letter of the term. Each term may be used more than once or

not at all.

a. cumulative feature

b. stock dividend

c. retired stock

d. retained earnings

e. callable feature

f. convertible feature

g. outstanding shares

h. treasury stock

i. participating feature

j. additional paid-in capital

207. The amount received for the issuance of stock in excess of par value.

208. The holders of this stock have the right to dividends in arrears before the current year dividend is distributed.

209. Allows preferred stock to be returned to the corporation in exchange for common stock.

210. Allows the holders of this stock to share in the distribution of dividends above the predetermined per share

amount.

Chapter 11: Stockholders’ Equity

211. Shares of stock that are repurchased and then discontinued by removing them from the accounting records.

Select the letter of the term each statement best describes.

a. authorized shares

b. issued shares

c. outstanding shares

d. par value

e. additional paid-in capital

f. retained earnings

g. cumulative feature

h. participating feature

i. callable stock

j. treasury stock

k. retirement of stock

l. dividend payout ratio

m. stock dividend

n. stock split

o. market value per share

p. convertible stock

q. book value per share

212. Allows preferred stock to be returned to the corporation in exchange for common stock.

213. Stock issued by the firm then repurchased but not retired.

214. Creation of additional shares of stock with a concurrent reduction of the par value of the stock.

215. The number of shares sold or distributed to stockholders.

216. An arbitrary amount stated on the face of the stock certificate that represents the legal capital of the firm.

217. Net income that has been earned by the corporation but not paid out as dividends.

218. Total stockholders’ equity divided by the number of shares of common stock outstanding.

219. The maximum number of shares a corporation may issue as indicated in the corporate charter.

Chapter 11: Stockholders’ Equity

220. The number of shares issued less the number of shares held as treasury stock.

221. The amount received for the issuance of stock in excess of the par value of the stock.

222. Stock that has a provision allowing the stockholders to share in the distribution of an abnormally large dividend

on a percentage basis.

223. Allows the issuing firm to eliminate a class of stock by paying the stockholders a fixed amount.

224. When the stock of a corporation is repurchased with no intention to reissue at a later date.

Select the statement on which each of the items provided below would be reported.

a. Statement of retained earnings

b. Statement of stockholders’ equity

c. Items that may require reporting on either statement

d. Items not reported on either of the statements

225. Issuance of common stock.

226. Net income for the period.

227. Dividends for the period.

228. Foreign currency translation adjustments.

From the following list, identify each item as operating (O), investing (I), financing (F), or not separately reported

on the statement of cash flows (N).

a. Operating—O

b. Investing—I

c. Financing—F

d. Not separately reported—N

229. Issuance of common stock for cash

230. Issuance of common stock for equipment

231. Conversion of preferred stock into common stock

Chapter 11: Stockholders’ Equity

232. Repurchase of common stock as treasury stock

233. Payment of cash dividend on preferred stock

234. Declaration of stock split

235. Distribution of stock dividend

236. Reissuance of common stock (held as treasury stock)

237. On May 1, 2015, Xiu Inc. had common stock of $345,000, additional paid-in capital of $1,298,000, and retained

earnings of $3,013,000. Xiu did not purchase or sell any common stock during the year. The company reported

net income of $556,000 and declared dividends in the amount of $78,000 during the year ended April 30, 2016.

REQUIRED:

Prepare a financial statement that explains the differences between the beginning and ending balances for the

accounts in the Stockholders’ Equity category of the balance sheet.

Chapter 11: Stockholders’ Equity

238. Assume that Cosmo Company’s Stockholders’ Equity category of the balance sheet appears as follows as of

December 31, 2015:

Common stock, $10 par, 60,000 shares issued and outstanding

$ 600,000

Additional paid-in capital—Common

480,000

Retained earnings

1,240,000

Total stockholders’ equity

$2,320,000

On May 1, 2016, Cosmo declared and issued a 15% stock dividend, when the stock was selling for $20 per share.

Then on November 1, it declared and issued a 2-for-1 stock split.

REQUIRED:

1. How many shares of stock are outstanding at year-end?

2. What is the par value per share of these shares?

3. Develop the Stockholders’ Equity category of Cosmo’s balance sheet as of December 31, 2016.

Chapter 11: Stockholders’ Equity

239. Falcon Company has 1,000 shares of $100 par value, 9% preferred stock and 10,000 shares of $10 par value

common stock outstanding. The preferred stock is cumulative and nonparticipating. Dividends were paid in

2012. Since 2012, Falcon has declared and paid dividends as follows:

2013

$ 0

2014

10,000

2015

20,000

2016

25,000

Required

1. Determine the amount of the dividends to be allocated to preferred and common stockholders for each year

2014 to 2016.

2. If the preferred stock had been noncumulative, how much would have been allocated to the preferred

and common stockholders each year?

Carlton Industries has identified the following items and would like you to answer a few questions about their

effect on Stockholders’ Equity. (Items are used only once.)

a. Preferred stock issued by Carlton

b. Amount received by Carlton in excess of par value when preferred stock was issued

c. Dividends in arrears on Carlton preferred stock

d. Cash dividend declared but unpaid on Carlton stock

e. Stock dividend declared but unissued by Carlton

f. Treasury stock

g. Amount received in excess of cost when treasury stock is reissued by MJ

h. Retained earnings

240. Which type of stock decreases stockholders’ equity?

Chapter 11: Stockholders’ Equity

241. Which item would not be recorded until declared?

242. Which item decreases Retained Earnings and also credits a payable (liability)?

243. Which item results in no change to stockholders’ equity?

244. Which item is recorded as Additional Paid-In Capital – Preferred Stock?

245. Which item increases Additional Paid-In Capital – Treasury Stock?

246. At December 31, 2016, Forgione Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 8,000 issued, 7,000 outstanding

Preferred Stock, $100 par, 7%, cumulative, 1,000 shares authorized, issued, and outstanding

The company did not pay any dividend during 2015 or 2014.

REQUIRED:

1. Compute the amount of dividend to be received by the common and preferred stockholders in 2016 if

the company declared a dividend of $50,000.

2. How many shares of treasury stock does Forgione have?

3. What are the dividends per share of common stock as a result of this distribution?

4. What are the dividends per share of Preferred stock as a result of this distribution?

Chapter 11: Stockholders’ Equity

247. At December 31, 2015, Marley Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

REQUIRED:

Indicate whether the following would increase, decrease, or have no effect on (a) assets, (b) retained earnings, and

(c) total stockholders’ equity.

1. A company declares and pays a cash dividend of $25,000.

2. A company declares and issues a 10% stock dividend.

248. At December 31, 2015, North Company and South Company have identical amounts of common stock and

retained earnings as follows:

Common Stock, $10 par, 50,000 shares authorized, 9,000 issued, 9,000

outstanding Retained Earnings, $500,000

At December 31, 2015, North Company declares and issues a 100% stock dividend, while South Company

declares and issues a 2-for-1 stock split.

REQUIRED:

Determine for each company the following amounts as of January 1, 2016:

Number of shares of common stock outstanding

Par value per share of the common stock

Total amount reported in Common Stock account

Retained earnings

Chapter 11: Stockholders’ Equity

249. At December 31, 2016, Corning Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Preferred Stock, $100 par, 8%, cumulative, 1,000 shares authorized, issued, and outstanding

The company did not pay any dividend during 2015 or 2014.

REQUIRED:

Compute the amount of dividend to be received by the common and preferred stockholders in 2016 if the company

declared a dividend of $24,000.

250. At December 31, 2016, Corning Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Preferred Stock, $100 par, 8%, cumulative, 1,000 shares authorized, issued, and outstanding

The company did not pay any dividend during 2015 or 2014.

REQUIRED:

Compute the amount of dividend to be received by the common and preferred stockholders in 2016 if the company

declared a dividend of $60,000.