Chapter 11: Stockholders’ Equity

88. [APPPENDIX] When an individual wishes to form a sole proprietorship, he or she does so by

a. filing a petition with the IRS.

b. purchasing stock in the proprietorship.

c. filing corporate paperwork with the state.

d. contributing cash or other assets.

89. [APPENDIX] When the owner of a sole proprietorship withdraws assets from the business for personal use

a. it is treated like a noncash dividend.

b. it is illegal because the assets belong to the separate entity, the proprietorship.

c. it would be recorded as a loss by the proprietorship.

d. it is recorded as a reduction of owner’s equity.

90. [APPENDIX] Gordon Vending, a sole proprietorship, had the following balances and transactions during 2015:

beginning capital, $40,000; contribution of cash to the business by the owner, $15,000; revenue, $60,000;

expenses, $35,000; withdrawal by the owner, $5,000. What is the amount of the ending capital balance?

a. $40,000

b. $60,000

c. $75,000

d. $85,000

91. [APPENDIX] Which of the following statements regarding partnerships is true?

a. Partnerships have two owners.

b. The partnership ends when a new partner is added.

c. The partnership is responsible for its own taxes.

d. The partnership is a separate legal entity from its owners.

92. [APPENDIX] Which of the following statements regarding partnerships is true?

a. Partnerships must register with the federal government.

b. Partnerships pay taxes to the IRS.

c. Partners must register with the state government.

d. Partners must abide by the separate entity concept and keep their personal assets separate from the

partnership assets.

Chapter 11: Stockholders’ Equity

93. [APPENDIX] Debbie and Alex formed a new partnership. The partnership agreement specified that income

should be allocated in a 2-to-1 ratio, with Debbie receiving the larger portion. If revenue for the first year

was $90,000 and expenses were $60,000, how much would be allocated to each partner?

a. Debbie—$45,000; Alex—$45,000

b. Debbie—$20,000; Alex—$10,000

c. Debbie—$60,000; Alex—$30,000

d. Debbie—$40,000; Alex—$20,000

94. Under IFRS, an item such as a convertible bond must be separated into two parts, showing one part in the Liability

category and the other part in the Stockholders’ Equity category.

a. True

b. False

95. All issued stock is outstanding.

a. True

b. False

96. Stockholders’ equity is composed of three parts: contributed capital, earnings retained in the business, and

dividends paid.

a. True

b. False

97. The participating feature of stock allows stockholders to sell stock back to the company.

a. True

b. False

98. Preferred stock receives first preference on voting rights.

a. True

b. False

99. The cumulative feature of stock allows the firm to eliminate a class of stock by paying the stockholders a

specified amount.

a. True

b. False

Chapter 11: Stockholders’ Equity

100. When stock is issued for cash, only the par value of the stock should be reported in the stock account.

a. True

b. False

101. When stock is issued for a noncash asset, the par value of the stock is the best indicator of the value of the asset.

a. True

b. False

102. Treasury stock is stock that has been issued, but not currently outstanding.

a. True

b. False

103. When treasury stock is reissued and the cost is less than the reissue price, the difference increases additional paid–

in capital.

a. True

b. False

104. Treasury stock is reported as a reduction in stockholders’ equity.

a. True

b. False

105. The Treasury Stock account should be considered an asset account.

a. True

b. False

106. When treasury stock is resold for an amount less than its cost, the difference between the sales price and the cost

is deducted from the Additional Paid-In Capital—Treasury Stock account or the Retained Earnings account (if

the Additional Paid-In Capital—Treasury Stock account does not exist).

a. True

b. False

107. If 20,000 shares are authorized, 15,000 shares are issued, and 500 shares are held as treasury stock, a cash

dividend of $1 per share would amount to $15,000.

a. True

b. False

Chapter 11: Stockholders’ Equity

108. Cash dividends become a liability to a corporation on the date of record.

a. True

b. False

109. When the board of director’s declares a cash or stock dividend, this action decreases Retained Earnings.

a. True

b. False

110. Stock dividends involve the issuance of additional shares of stock.

a. True

b. False

111. Stock dividends reduce the par value of the stock.

a. True

b. False

112. A 15% stock dividend will increase the number of shares outstanding but the book value per share will decrease.

a. True

b. False

113. A stock split is similar to a stock dividend in that it results in additional shares of stock outstanding and

is nontaxable.

a. True

b. False

114. Stock dividends affect the par value per share of the stock.

a. True

b. False

115. A 2-for-1 stock split increases the par value per share.

a. True

b. False

116. An accounting transaction is not recorded when a corporation declares and executes a stock split.

a. True

b. False

117. None of the Stockholders’ Equity accounts are affected by the stock split.

a. True

b. False

118. All changes in all stockholders’ equity accounts must be shown in the Stockholders’ Equity section of the

balance sheet.

a. True

b. False

119. The statement of stockholders’ equity is useful in evaluating a company’s liquidity.

a. True

b. False

120. The all-inclusive income approach requires that all events and transactions that affect income should be reported

on the income statement to help prevent the manipulation of income.

a. True

b. False

121. The FASB has allowed certain items to be reported directly to stockholders’ equity in an effort to mitigate

the possibility of income fluctuating widely from period to period.

a. True

b. False

122. Comprehensive income is the increase in net assets resulting from all transactions occurring during an

accounting period except stockholders’ investments and dividends.

a. True

b. False

Chapter 11: Stockholders’ Equity

123. A company may prepare a statement of retained earnings instead of a statement of stockholders’ equity if the

only changes in the stockholders’ equity accounts that occurred during the year are earnings and dividends.

a. True

b. False

124. Book value is a measure of the market value of the stock.

a. True

b. False

125. Book value indicates the rights that stockholders have, based on recorded values, to the net assets in the event of

liquidation.

a. True

b. False

126. The issuance of stock is reported as a financing activity.

a. True

b. False

127. The payment of dividends is a financing activity.

a. True

b. False

128. [APPENDIX] A partnership can be owned by one or more entities or individuals.

a. True

b. False

129. [APPENDIX] A balance sheet of a sole proprietorship includes only the business assets and liabilities, not the

personal assets of the owner.

a. True

b. False

130. [APPENDIX] A sole proprietorship is a separate entity for legal purposes.

a. True

b. False

Chapter 11: Stockholders’ Equity

Select the best answer from the list below to complete statements 131-141 that follow.

authorized shares

treasury stock

book value per share

issued shares

stock dividend

par value per share

outstanding shares

additional paid-in-capital

market value per share

stock split

dividend payout ratio

retained earnings

131. The number of shares sold or distributed to stockholder are .

132. An arbitrary amount that is stated on the face of the stock certificate is .

133. The number of shares issued less the number of shares held as treasury stock are

______________________________.

134. The maximum number of shares a company may issue are .

135. Net income that has been earned by the corporation but not paid out as dividends are

______________________________.

136. The amount received for each share of stock in excess of par value is .

137. Stock issued by the firm, but then repurchased and not retired is ________________________.

138. The annual dividend amount divided by the annual net income is .

139. Distribution of additional shares of stock and reduction of the par value of the stock is

______________________________.

140. The selling price of the stock as indicated by the most recent stock transaction is

___________________________________.

141. Assuming no preferred stock exists, total stockholders’ equity divided by the number of shares of common stock

outstanding is equal to ________________________________________.

Chapter 11: Stockholders’ Equity

142. A drawing account is sometimes referred to as a ______________________.

143. The characteristic where each partner is personally liable for the debts of the partnership is known as

_____________________.

144. The document that specifies how much the owners will invest, what their salaries will be, and how profits will be

shared in a partnership is known as a .

145. A ________________ allows the firm to eliminate a class of stock by paying the stockholders a specified amount.

146. A allows preferred stockholders to share on a percentage basis in the distribution of

an abnormally large dividend.

Chapter 11: Stockholders’ Equity

147. Comfort Shoes had the following items included in its accounting records. In the space provided, indicate

whether each of the items listed is included in an account in the stockholders’ equity section of the balance

sheet.

Item

Included in a Stockholders’

Equity account? (yes or

no)

a. Preferred stock issued by Comfort Shoes.

b. Cash dividend unpaid that was declared last year.

c. Earnings accumulated but not distributed by Comfort Shoes.

d. Amount received in excess of cost when treasury stock is

reissued by Comfort Shoes.

e. Treasury stock purchased.

f. Dividends in arrears on Comfort Shoes preferred stock.

g. Amount received in excess of par value when common stock was

issued by Comfort Shoes.

h. Stock dividend declared but not yet distributed by Comfort Shoes.

Chapter 11: Stockholders’ Equity

148. Big Surf Shop provided the following information from its 2015 financial statements:

Total Assets $655,000

Total Liabilities 225,000

In addition, the stockholders’ equity section of the balance sheet showed:

Preferred stock, 10%, $2 par value, 10,000 authorized, 8,000 issued and

outstanding, $5 liquidation value $16,000

Common stock, $4 par value, 20,000 shares authorized, 10,000 issued and outstanding 40,000

The common stock had a year-end market price of $24.

A) Calculate the book value per common share at year-end.

B) Indicate the usefulness of this ratio for Big Surf Shop.

149. The Lobster Shanty had the following account balances at December 31, 2015:

Retained earnings

$ 52,000

Treasury stock, 500 common shares at cost

(10,000)

Common stock, $1 par value, 10,000 shares authorized, 4,000 shares outstanding

4,000

Cash dividends payable—common

6,000

Additional paid-in capital—common

1,200

Additional paid-in capital-treasury stock

900

Common stock dividend distributable

6,200

Prepare the stockholders’ equity section of the balance sheet for The Lobster Shanty at December 31, 2015.

The Lobster Shanty

Stockholders’ Equity Section of the Balance Sheet

at December 31, 2015

Chapter 11: Stockholders’ Equity

150. The Stockholders’ Equity section of Stallion Tack Shack balance sheet on January 1, 2015, appeared as follows:

Common stock, $5 par, 30,000 shares issued and outstanding

$150,000

Additional paid-in capital—common

120,000

Retained earnings

300,000

Total stockholders’ equity

$570,000

On March 1, 2015, Stallion reacquired 3,000 shares of common stock at $8 per share. Answer the following

questions:

A) What amount would be reported on the March 31, 2015, balance sheet for treasury stock?

B) What is the number of outstanding shares at March 31, 2015?

C) How much is total stockholders’ equity to be reported on the March 31, 2015 balance sheet?

Chapter 11: Stockholders’ Equity

151. Reddy Parts reported the following information at December 31, 2015:

Preferred stock, 12%, $1 par, 50,000 shares authorized, issued, and

outstanding; cumulative; non-participating; callable at par value

$ 50,000

Common stock, $2 par, 30,000 shares authorized

40,000

Additional paid-in capital—common

50,000

Retained earnings

30,000

Total contributed capital and retained earnings

$170,000

Less: Treasury stock (500 common shares at cost)

(5,000)

Total stockholders’ equity

$165,000

Answer the following questions for Reddy Parts by placing the correct response in the space provided.

___________ A) How many shares of common stock are issued?

___________ B) How many shares of preferred stock are issued?

___________ C) How many common shares are outstanding?

___________ D) How many preferred shares are outstanding?

___________ E) How many of the common shares will receive dividends if and when they are paid?

___________ F) How many of the preferred shares will receive dividends if and when they are paid?

Chapter 11: Stockholders’ Equity

152. Overton Supply reported the following information at December 31, 2015:

Common stock, $1 par, 100,000 shares authorized

$ 80,000

Additional paid-in capital—common

60,000

Retained earnings

40,000

Total contributed capital and retained earnings

$180,000

Less: Treasury stock (2,000 common shares at cost)

(20,000)

Total stockholders’ equity

$160,000

Answer the following questions for Overton Supply.

1) Assuming that all shares were sold at the same price, how much did each share of common stock

originally sell for?

2) What is the total amount of contributed capital at December 31, 2015?

3) What is the amount of the book value per share at December 31, 2015?

4) Would the book value per share increase, decrease, or remain the same, if the company declared a 2-for-1

stock split on December 31, 2015? Explain.

Chapter 11: Stockholders’ Equity

153. The stockholders’ equity section of Augusta, Inc. is as follows:

Preferred stock, 7%, $10 par, 1,000 shares authorized, 300 shares issued

$ 3,000

Additional paid-in capital—preferred

9,000

Common stock, $1 par value, authorized 15,000 shares, issued 4,000 shares

4,000

Additional paid-in capital—common

20,000

Retained earnings

50,000

Total contributed capital and retained earnings

$86,000

Less: Treasury stock (1,000 common shares at cost )

(6,000)

Total stockholders’ equity

$80,000

The market price of the stock on December 31, 2015, was $8 per share. Answer the following independent

questions:

A) Calculate the average amount at which each share of common stock was initially sold.

B) What balance will be in the retained earnings account immediately after the declaration of a 2- for-1

stock split?

C) If a cash dividend of $1 per share was declared to both common and preferred stockholders, what

would be the balance in retained earnings immediately after the declaration?

D) What balance will be in the retained earnings account immediately after the declaration of a 20%

common stock dividend on December 31, 2015?

Chapter 11: Stockholders’ Equity

154. Given below are several transactions for Vision Inc. In the space provided, indicate the impact on each of the

stockholders’ equity accounts given, by placing the dollar amount and either a plus sign (+) or a minus sign (–) in

the box provided. For each account in which there is no effect, place an X in the box.

Transaction

Common

Stock

Additional

Paid-in

Stock

Retained

Earnings

1. Vision Inc. received authorization to issue

1,000 shares of $2 par value common

2. Vision Inc. issued 500 shares of

common stock for cash at $15 per share.

3. Vision Inc. issued 200 shares in

exchange for a truck worth $3,000.

4. Vision Inc. issued 100 shares of stock in

exchange for a patent. The patent had an

undeterminable market value. The stock was

selling for $14 per share.

1. Vision Inc. received authorization to issue

1,000 shares of $2 par value common

2. Vision Inc. issued 500 shares of

common stock for cash at $15 per share.

3. Vision Inc. issued 200 shares in

exchange for a truck worth $3,000.

Chapter 11: Stockholders’ Equity

155. Below are two transactions for Navaho Co.

1. On June 1, Navaho Co. issued 2,000 shares of $5 par common stock for $16 per share.

2. On June 15, Navaho Co. issued 1,200 shares of $5 par preferred stock to acquire a building. The stock is not

widely traded, and the current market value of the stock is not evident. The building has recently been appraised

by an independent firm as having a market value of $15,000.

REQUIRED: For each of these transactions, record the journal entry that Navaho Company would make.

Chapter 11: Stockholders’ Equity

156. The Stockholders’ Equity section of Sea Scape, Inc.’s balance sheet on January 1, 2015, appeared as follows:

Common stock, $2 par, 20,000 shares issued and outstanding

$ 40,000

Additional paid-in capital—common

120,000

Retained earnings

300,000

Total contributed capital and retained earnings

$460,000

Less: Cost of treasury stock (10,000 shares)

(80,000)

Total stockholders’ equity

$380,000

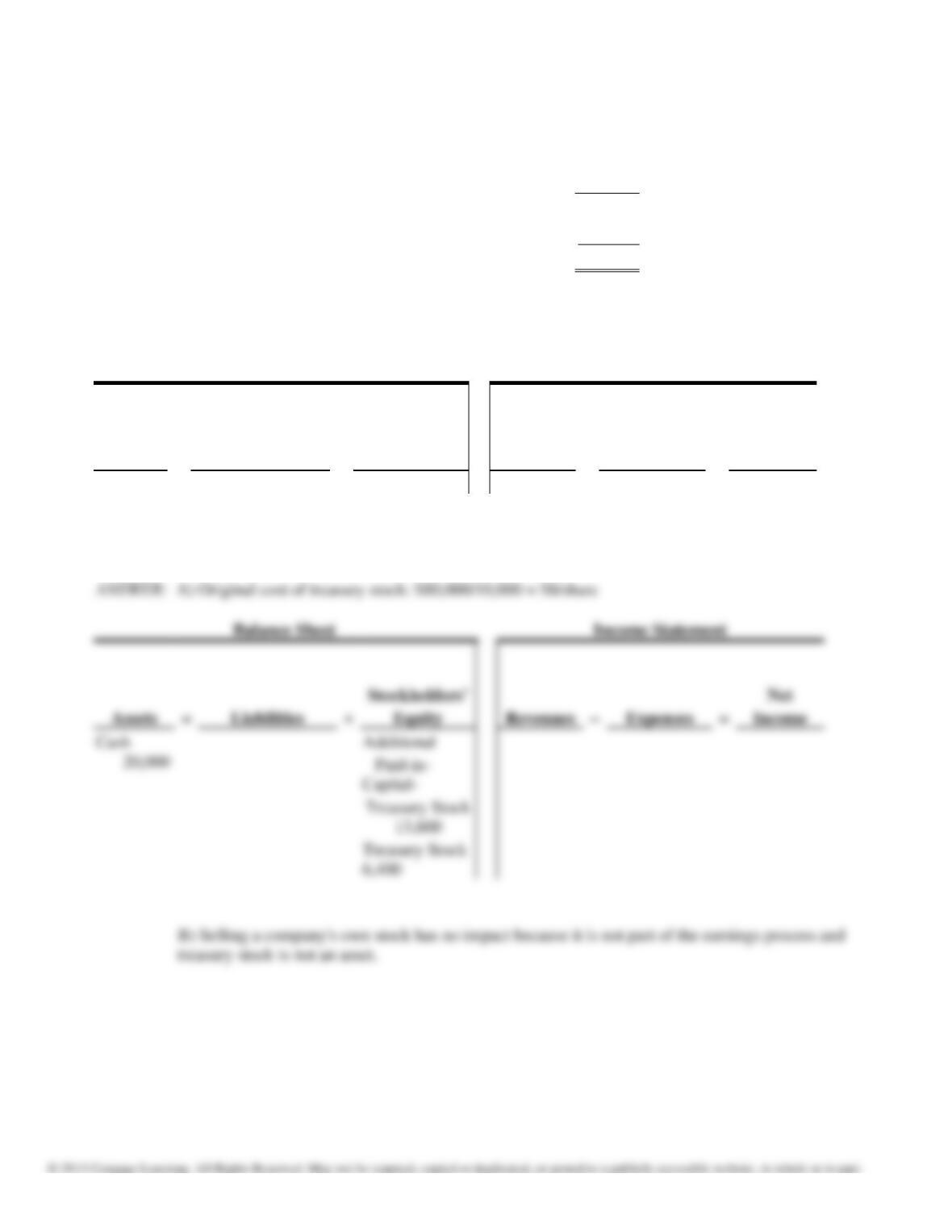

A) On March 1, 2015, Sea Scape resold 800 shares of treasury stock at $25 per share.

What is the effect of the March 1 transaction on the accounting equation?

Balance Sheet

Income Statement

Assets

=

Liabilities

+

Stockholders’

Equity

Revenues

–

Expenses

=

Net

Income

B) Why is the excess of the sales price of the 800 shares of treasury stock over the cost not reported on the

income statement?

Chapter 11: Stockholders’ Equity

157. Assume that the Stockholders’ Equity section of Cherokee Company’s balance sheet on December 31, 2015,

appears as follows:

Common stock, $10 par value, 1,500 shares issued and outstanding

$15,000

Additional paid-in capital—Common

17,000

Retained earnings

11,000

Total stockholders’ equity

$43,000

1. If on February 1, 2016, Cherokee buys 120 of its shares as treasury stock at $30 per share, what journal entry

will the company record?

2. How with the Stockholders’ Equity section of Cherokee’s balance sheet appear on February 1, 2016, after the

purchase of the treasury stock?

Chapter 11: Stockholders’ Equity

158. Lear Flower Shop presented the stockholders’ equity section of its balance sheet on January 1, 2015, as follows:

All common shares were originally sold for $6 each. The following transactions occurred during 2015:

—Reacquired 3,000 shares of common stock at $15 per share on February 16.

—Sold 2,000 shares of treasury stock at $20 per share on June 1.

Part 1. Show the effects of the transactions on the accounting equation.

Balance Sheet

Income Statement

Assets

=

Liabilities

+

Stockholders’

Equity

Revenues

–

Expenses

=

Net

Income

Part 2. How many shares of stock are outstanding at June 1, immediately after the sale of the 2,000

shares of treasury stock?

Balance Sheet

Income Statement

Assets

=

Liabilities

+

Stockholders’

Revenues

–

Expenses

=

Net

Balance Sheet

Income Statement

Assets

=

Liabilities

+

Stockholders’

Revenues

–

Expenses

=

Net

Common stock, $2 par, 10,000 shares issued and outstanding

$20,000

Additional paid-in capital—common

40,000

Retained earnings

10,000

Total stockholders’ equity

$70,000

Chapter 11: Stockholders’ Equity

159. The Stockholders’ Equity section of Gretchen’s Bistro’s balance sheet on January 1, 2015, appeared as follows:

Common stock, $2 par, 2,000 shares issued and outstanding

$ 4,000

Additional paid-in capital

1,600

Retained earnings

5,400

Total stockholders’ equity

$11,000

On March 1, 2015, Gretchen’s Bistro reacquired 800 shares of common stock at $12 per share. On April 6,

Gretchen’s Bistro resold 600 shares of treasury stock at $20 per share. How many shares of stock are outstanding

at March 31, and April 30, respectively?