Chapter 11—Strategic Cost Management Key

1. Strategic cost management is the identification of strategies to develop a competitive advantage.

2. Strategic decision making is important to achieve good inventory control.

3. The objective of strategic cost management is to reduce costs while strengthening strategic positions.

4. There are two general cost management strategies: cost leadership and focusing.

5. Value-chain analysis is identifying and exploiting internal and external linkages to achieve strong strategic

positions.

6. Exploiting internal linkages involves the assessment of management reliability.

7. Exploiting supplier linkages is the exploitation of a firm’s internal activities.

8. Exploiting customer linkages is not important since customers do not affect profitability.

9. Strategic cost management emphasizes the importance of an external focus and the need to recognize and

exploit internal and external linkages.

10. Life-cycle cost management involves two types of life-cycle viewpoints: the marketing viewpoint and the

production viewpoint.

11. Target costing provides a method for reducing costs by exploiting customer and supplier linkages.

12. Life-cycle costs are all costs associated with a product during the production viewpoint.

13. JIT manufacturing eliminates waste by producing products only when, and in the quantities needed.

14. In JIT purchasing, materials are usually at warehouse long before they are needed.

15. A major difference between traditional and JIT environments is the degree of responsibility given to

workers in the organization.

16. Acceptable quality level (AQL) allows defects to occur within predetermined parameters.

17. In a JIT environment, many overhead costs are directly traceable to products.

18. The structure for a JIT environment is a vastly complicated process costing system.

19. Accounting is simplified in the JIT system by the use of backflush costing.

20. In a job-order setting using JIT, repetitive business is separated from unique orders.

21. Choosing alternative strategies that provide long-term growth involves __________ decision making.

22. The creation of customer value for same or lower cost than competitors is called __________ advantage.

23. the difference between what the customer receives and gives up is the __________ .

24. __________ analysis relies on identifying and exploiting internal and external linkages.

25. The assignments to suppliers and customers that provide the best cost information needed are

called __________ assignments.

26. The length of time a product serves the needs of customers is called the __________ life.

27. The stage during which a product loses market acceptance is called the __________ stage.

28. The manufacturing system focused on reducing inventory levels and waste is called __________

manufacturing.

29. In traditional and JIT environments using direct tracing, the manufacturing costs assigned to products are

the direct materials costs and the __________ costs.

30. Accounting for the cost accounting cycle in a JIT environment is simplified by using __________ costing.

31. The strategy which involves choosing among alternative strategies with the goal of selecting a strategy or

strategies that provides a company with reasonable assurance of long-term growth and survival is called:

32. The strategy to create better customer value for the same or lower cost than competitors or creating

equivalent value for lower cost than offered by competitors is called:

33. A competitive advantage has been established when

34. The difference between what a customer receives and what the customer gives up is called:

35. The total product, the complete range of benefits that a customer receives from a purchased product

include(s):

36. The use of cost data to develop and identify superior strategies that will produce a sustainable competitive

advantage is called:

37. When a computer company maintains the internal storage space for a lower price, it is following a

38. When a computer company increases the internal storage space for the same price, it is following a

39. When a computer company targets customers in the South, it is following a

40. When a computer company selects a mix of strategies in order to create sustainable competitive advantage,

it is following a

41. The relationships among activities that are performed with a firm’s portion of the value chain is(are) called:

42. The industrial value-chain analysis

43. The factor(s) that describe the relationships of a firm’s value chain activities that are performed with its

suppliers and customers is(are) called:

44. When a computer manufacturing company addresses supplier production problems, it is focusing on

45. The structural and executional factors that determine the long-term cost structure of an organization are

called:

46. Structural and executional activities are types of

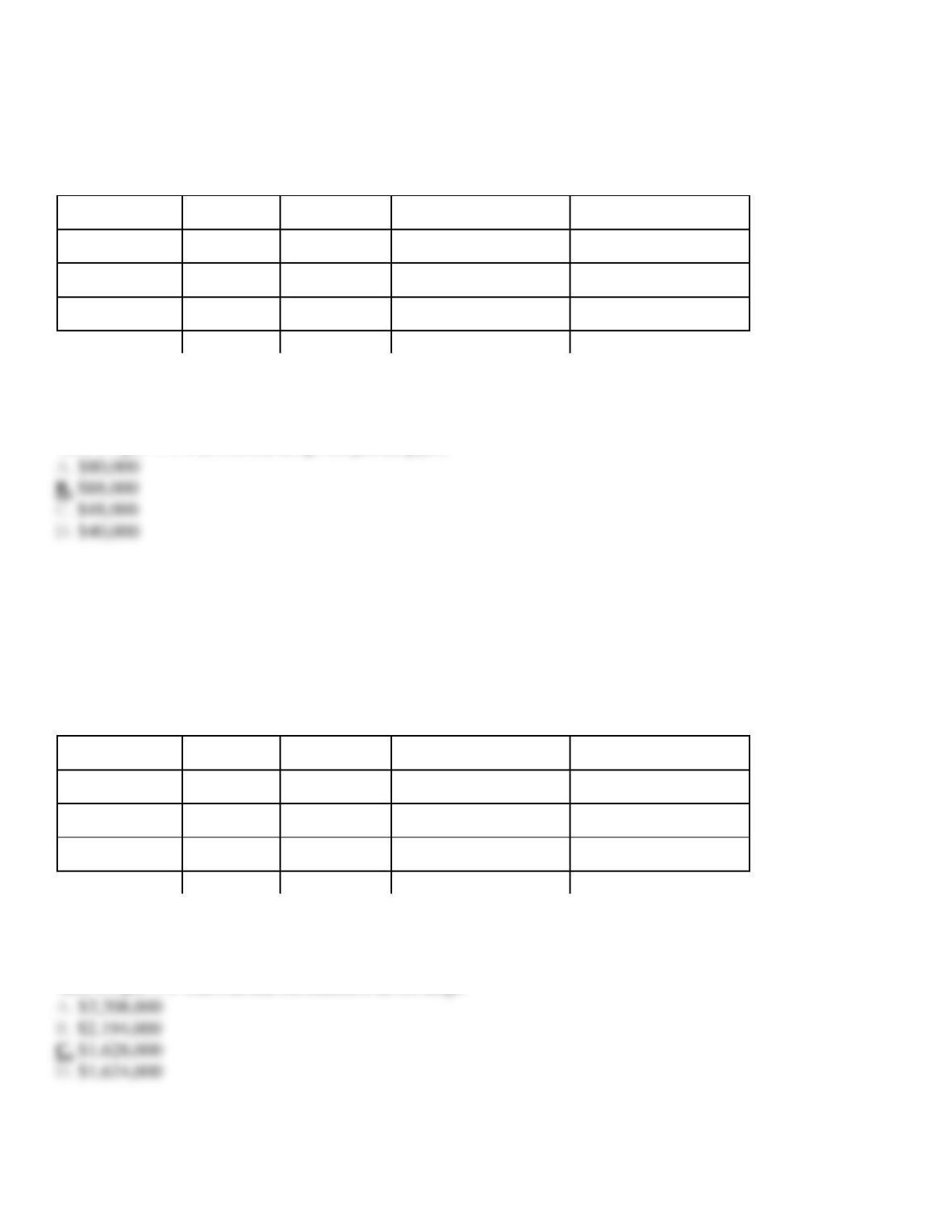

47. Building plants, management structuring, and grouping employees are examples of

48. The factors that drive the cost of day-to-day activities performed as a result of the structure and processes

selected by the organization are called:

49. Plant layout, quality management systems, and providing capacity are examples of

50. The operational activity of moving inventory is classified as a

51. The operational activity of setting up equipment is classified as a

52. The operational activity of assembling parts is an example of a

53. The operational activity of redesigning products is classified as a

54. The operational activity of inspecting is classified as a

55. Activities required to design, develop, produce, market, distribute, and service a product are known as

56. The first link of the internal value chain is

57. The last link of the internal value chain is

58. Analyzing how costs and other financial factors vary as different bundles of activities are considered to

strengthen a firm’s strategic position is the process of

59. The industry value chain includes

60. Identifying profitable and unprofitable customers is an example of exploiting

61. Figure 11-1

Ambrosia Corp. is a manufacturer of equipment used in manufacturing. It currently produces a product with 30

parts but through redesign has reduced the number of parts to 9. Then current activity capacity and demand for

the 30 unit configuration and expected activity demand for the 9 part configuration are provided below:

Activities

Activity

Driver

Activity Capacity

Current

Activity Demand

Expected

Activity Demand

Materials

usage

number of parts

300,000

300,000

90,000

Assembly

direct labor

hours

20,000

20,000

6,000

Purchasing parts

number of

orders

20,000

16,000

8,000

Materials usage has a rate of $6 per part and no fixed costs. Assembly has a rate of $20 per labor hour with no fixed component. Purchasing requires

clerks that can process 5,000 purchase orders. Each clerk earns $40,000 per year. There is also a $1 per order processing cost.

Refer to Figure 11-1. What is the savings in materials usage cost with the new design changes?

62. Figure 11-1

Ambrosia Corp. is a manufacturer of equipment used in manufacturing. It currently produces a product with 30

parts but through redesign has reduced the number of parts to 9. Then current activity capacity and demand for

the 30 unit configuration and expected activity demand for the 9 part configuration are provided below:

Activities

Activity

Driver

Activity Capacity

Current

Activity Demand

Expected

Activity Demand

Materials

usage

number of parts

300,000

300,000

90,000

Assembly

direct labor

hours

20,000

20,000

6,000

Purchasing parts

number of

orders

20,000

16,000

8,000

Materials usage has a rate of $6 per part and no fixed costs. Assembly has a rate of $20 per labor hour with no fixed component. Purchasing requires

clerks that can process 5,000 purchase orders. Each clerk earns $40,000 per year. There is also a $1 per order processing cost.

Refer to Figure 11-1. What is the cost savings from purchasing parts?

63. Figure 11-1

Ambrosia Corp. is a manufacturer of equipment used in manufacturing. It currently produces a product with 30

parts but through redesign has reduced the number of parts to 9. Then current activity capacity and demand for

the 30 unit configuration and expected activity demand for the 9 part configuration are provided below:

Activities

Activity

Driver

Activity Capacity

Current

Activity Demand

Expected

Activity Demand

Materials

usage

number of parts

300,000

300,000

90,000

Assembly

direct labor

hours

20,000

20,000

6,000

Purchasing parts

number of

orders

20,000

16,000

8,000

Materials usage has a rate of $6 per part and no fixed costs. Assembly has a rate of $20 per labor hour with no fixed component. Purchasing requires

clerks that can process 5,000 purchase orders. Each clerk earns $40,000 per year. There is also a $1 per order processing cost.

Refer to Figure 11-1. What is the total cost reduction of the new design?

64. Figure 11-1

Ambrosia Corp. is a manufacturer of equipment used in manufacturing. It currently produces a product with 30

parts but through redesign has reduced the number of parts to 9. Then current activity capacity and demand for

the 30 unit configuration and expected activity demand for the 9 part configuration are provided below:

Activities

Activity

Driver

Activity Capacity

Current

Activity Demand

Expected

Activity Demand

Materials

usage

number of parts

300,000

300,000

90,000

Assembly

direct labor

hours

20,000

20,000

6,000

Purchasing parts

number of

orders

20,000

16,000

8,000

Materials usage has a rate of $6 per part and no fixed costs. Assembly has a rate of $20 per labor hour with no fixed component. Purchasing requires

clerks that can process 5,000 purchase orders. Each clerk earns $40,000 per year. There is also a $1 per order processing cost.

Refer to Figure 11-1. If 10,000 units are being produced and the sales price is $500, what is the new sales price if the cost savings are passed on to

the consumer?

65. In activity-based costing, supplier costs

66. Figure 11-2

Blue Vibrance Company sells a product used in many manufacturing processes. The sales activity involves

three activity areas:

Activity Area

Cost Driver and Rate

Order taking

$100 per purchase order

Sales visits

$50 per visit

Delivery vehicles

$1 per delivery mile

The following customer information is given:

AX

BY

DZ

Units sold

100,000

80,000

60,000

List price

$50

$50

$50

Actual sales price

$45

$48

$50

Number of purchase orders

30

20

10

Number of sales visits

6

5

3

Number of delivery miles

100

80

60

Refer to Figure 11-2. Which customer is most profitable?

67. Figure 11-2

Blue Vibrance Company sells a product used in many manufacturing processes. The sales activity involves

three activity areas:

Activity Area

Cost Driver and Rate

Order taking

$100 per purchase order

Sales visits

$50 per visit

Delivery vehicles

$1 per delivery mile

The following customer information is given:

AX

BY

DZ

Units sold

100,000

80,000

60,000

List price

$50

$50

$50

Actual sales price

$45

$48

$50

Number of purchase orders

30

20

10

Number of sales visits

6

5

3

Number of delivery miles

100

80

60

Refer to Figure 11-2. Which customer has the least activity costs?

68. Figure 11-2

Blue Vibrance Company sells a product used in many manufacturing processes. The sales activity involves

three activity areas:

Activity Area

Cost Driver and Rate

Order taking

$100 per purchase order

Sales visits

$50 per visit

Delivery vehicles

$1 per delivery mile

The following customer information is given:

AX

BY

DZ

Units sold

100,000

80,000

60,000

List price

$50

$50

$50

Actual sales price

$45

$48

$50

Number of purchase orders

30

20

10

Number of sales visits

6

5

3

Number of delivery miles

100

80

60

Refer to Figure 11-2. What is the profitability of customer BY?

69. Which of the following are true about total quality control?

70. Figure 11-3

Awesome Products Company manufactures a product sold to retailers. It is considering suppliers for its process.

The supplier quality involves four activity areas:

Activity Area

Cost Driver and Rate

Order cost

$120 per purchase order

Defective units

$200 per unit internal failure costs

Delivery trips

$5 per delivery mile

Carrying cost

$1 per order

The following supplier information is given:

X3

Y2

Z1

Materials units needed

100,000

100,000

100,000

Actual purchase price

$5

$4.99

$5.01

Number of purchase orders

20

30

18

Number of defects

6

12

0

Number of deliveries

20

30

18

Refer to Figure 11-3. Which supplier is least costly?

71. Figure 11-3

Awesome Products Company manufactures a product sold to retailers. It is considering suppliers for its process.

The supplier quality involves four activity areas:

Activity Area

Cost Driver and Rate

Order cost

$120 per purchase order

Defective units

$200 per unit internal failure costs

Delivery trips

$5 per delivery mile

Carrying cost

$1 per order

The following supplier information is given:

X3

Y2

Z1

Materials units needed

100,000

100,000

100,000

Actual purchase price

$5

$4.99

$5.01

Number of purchase orders

20

30

18

Number of defects

6

12

0

Number of deliveries

20

30

18

Refer to Figure 11-3. Which supplier has the most defective units?

72. Figure 11-3

Awesome Products Company manufactures a product sold to retailers. It is considering suppliers for its process.

The supplier quality involves four activity areas:

Activity Area

Cost Driver and Rate

Order cost

$120 per purchase order

Defective units

$200 per unit internal failure costs

Delivery trips

$5 per delivery mile

Carrying cost

$1 per order

The following supplier information is given:

X3

Y2

Z1

Materials units needed

100,000

100,000

100,000

Actual purchase price

$5

$4.99

$5.01

Number of purchase orders

20

30

18

Number of defects

6

12

0

Number of deliveries

20

30

18

Refer to Figure 11-3. What is the cost of supplier Z1?

73. The length of time that a product serves the needs of customers is called the:

74. The time a product exists—from conception to abandonment is called the:

75. The stage during which the product loses market acceptance is called the:

76. The period of time when sales increase at a decreasing rate is called the:

77. The stage characterized by preproduction and startup activities is called the:

78. The period of time when sales increase at an increasing rate is called the:

79. The viewpoint that describes the general sales pattern of a product as it passes through the introduction,

growth, maturity, and decline stages is called the:

80. The viewpoint which defines stages of the life cycle by changes in the type of activities performed is called

the:

81. Which stage in the marketing viewpoint is characterized by preproduction and startup activities?

82. Which of the following is NOT a stage of the marketing viewpoint of the product life cycle?

83. Which of the following is NOT a stage of the consumable life-cycle viewpoint?

84. Life-cycle cost management consists of

85. Which of the following is NOT a stage of the production life-cycle viewpoint?

86. Which of the life-cycle viewpoints is the revenue-oriented viewpoint?

87. Which of the following is NOT a stage of the production life-cycle viewpoint?

88. Which of the life-cycle viewpoints is the cost-oriented viewpoint?

89. Which viewpoint of the product life-cycle is customer-value oriented?

90. Which stage of the marketing life-cycle has slow sales growth with peak sales?

91. At which stage of the consumable life-cycle is price sensitivity low?

92. According to the authors, 90 percent or more of a product’s life-cycle costs are determined during

93. Information for life-cycle cost management is supported by a(n)