Chapter 11—Risk-Adjusted Expected Rates of Return and the Dividends Valuation

Approach

MULTIPLE CHOICE

1. Which of the following is not a problem with using a dividend-based valuation formula

a.

dividends are arbitrarily established

b.

dividends represent a transfer of wealth to shareholders

c.

some firms do not pay a regular periodic dividend

d.

it is a challenge to forecast the final liquidating dividend

2. Assuming that riskless rate is 4.6% and the market premium is 7.3% calculate Zonk’s cost of equity

capital:

a.

10.4%

b.

7.69%

c.

11.89%

d.

8.28%

3. Determine the weight on debt capital that should be used to calculate Zonk’s weighted-average cost of

capital:

a.

21.7%

b.

21.00%

c.

50%

d.

58.2%

11-2

4. Determine the weight on equity capital that should be used to calculate Zonk’s weighted-average cost

of capital:

a.

79.00%

b.

78.3%

c.

41.8%

d.

50%

5. Using the above information, calculate Zonk’s weighted-average cost of capital:

a.

11.5%

b.

7.97%

c.

7.48%

d.

10.90%

6. Assume that Zonk is a potential leveraged buyout candidate. Assume that the buyer intends to put in

place a capital structure that has 70 percent debt with a pretax borrowing cost of 14 percent and 30

percent common equity. Compute the revised equity beta for Zonk based on the new capital structure.

a.

4.35

b.

4.77

c.

4.34

d.

3.91

7. Assume that Zonk is a potential leveraged buyout candidate. Assume that the buyer intends to put in

place a capital structure that has 70 percent debt with a pre tax borrowing cost of 14 percent and 30

percent common equity. Compute the weighted average cost of capital for Zonk based on the new

capital structure.

a.

8.85%

b.

12.56%

c.

13.01%

d.

9.94%

8. Equity-based valuation models are based on all metrics except

11-3

a.

dividends

b.

cash flow

c.

working capital

d.

earnings

9. One rationale for using expected dividends in valuation is

a.

Dividends are a necessary payment in order for a firm to have value.

b.

Dividends are paid in cash, and cash serves as a measurable common denominator for

comparing the future benefits of alternative investment opportunities.

c.

Dividends are the most reliable measure of value because most companies payout

dividends to shareholders.

d.

Dividend payout ratios are set based on profitability.

10. When deriving the equity value of a firm, an analyst forecasts the real dividends expected to be paid in

the future. In this case, which discount rate should be used?

a.

The nominal rate of return

b.

The real rate of return

c.

The risk free rate of return

d.

The risk adjusted rate of return

11. Equity valuation models based on dividends, cash flows, and earnings have been the

topic of many theoretical and empirical research studies in recent years. All of the following are true

regarding these studies except:

a.

share prices in the capital markets generally correlate closely with share value

b.

share prices do not always equal share values

c.

temporary deviations of price from value occur

d.

unexpected changes in earnings, dividends, and cash flows do not correlate closely

with changes in stock prices

12. The historical discount rate of the firm may be a good indicator of the appropriate discount

rate to apply to the firm in the future, when all of the following conditions hold true except:

a.

The current risk of the firm is the same as the expected future risk of the firm.

b.

Expected future interest rates are likely to equal current interest rates.

c.

The existing capital structure of the firm is the same as the expected future capital

structure of the firm.

d.

The current mix of debt and equity financing is equal.

13. Firm-specific factors that increase the firm’s nondiversifiable risk include all of the following

except:

a.

exposure to interest rate changes

b.

exposure to inflation

c.

exposure to management competence

d.

exposure to cyclicality

14. Investors typically accept a lower risk-adjusted rate of return on debt capital than on equity capital

because

a.

debt is typically less risky because fixed claims bear less residual risk than equity claims.

b.

equity bears less residual risk than debt.

c.

equity capital costs are tax deductible.

d.

the yield to maturity on equity is inversely related to its market value

15. All of the following are steps in the analysis and valuation framework used to understand the

fundamentals of a business and determine estimates of its value except:

a.

Analyze the firm’s strategy in terms of the competition.

b.

Assess the quality of the firm’s accounting and financial reporting.

c.

Derive forecasts of future earnings from the firm’s projected financial statements.

d.

Obtain the national ranking of the firm’s external auditors.

16. Under the cash-flow-based valuation approach, free cash flows can be used instead of dividends as the

expected future payoffs to the investor in the numerator of the general valuation model because:

a.

this approach focuses on earnings as a measure of the capital that a firm creates.

b.

over the life of the firm, the free cash flows into the firm and cash flows paid out of the

firm in dividends to shareholders will be equivalent.

c.

over the life of the firm, the free cash flows out of the firm for investments and cash flows

paid into the firm in dividends from these investments will be equivalent.

d.

this approach focuses on wealth distribution to shareholders.

17. Returns on systematic risk-free securities (like U.S. Treasury securities) should exhibit what type of

correlation with returns on a diversified marketwide portfolio of stocks?

a.

nearly perfect correlation.

b.

perfect correlation.

c.

no correlation.

d.

Unable to tell without specifics about the portfolio.

18. If a firm has a market beta of 0.9, is subject to an income tax rate of 35 percent, has a risk-free rate of 6

percent, a market risk premium of 7 percent, and has a market value of debt to market value of equity

ratio of 60 percent, what does the market expect the firm to generate in terms of equity returns using

CAPM?

a.

6%

b.

7%

c.

12.3%

d.

13%

19. With respect to dividends and priority in liquidation, what has priority over common stock?

a.

treasury stock

b.

debt capital

c.

preferred stock

d.

nonconvertible common equity

COMPLETION

1. In theory, the value of a share of common equity is the present value of

____________________________________________________________.

2. To determine the appropriate weights to use in the weighted average cost of capital, an analyst will

need to determine the ______________________________ of the debt, preferred stock and common

equity capital.

3. One criticism in using the CAPM to calculate the cost of equity capital is that

______________________________ and the

__________________________________________________ are quite sensitive to the time period

and methodology used in their computation.

4. If dividend projections include the effect of inflation, then the discount rate used should be a

____________________ rate.

5. A company with a new

Capital structure will increase the __________ and at the same time the __________ risk.

6. A company with a market beta of 1 has systemic risk ____________________ to the average amount

of systemic risk of all equity securities in the market.

11-6

7. Because the market equity beta reflects the level of operating leverage, financial leverage, variability

of sales, and other characteristics of a firm, there are situations where an analyst might have to adjust

the beta because of changes in the capital structure. A situation that might require an analyst to

estimate a new levered beta is a ___________________________________.

8. Normally, valuation methods are designed to produce reliable estimates of the value of a firm’s

______________________________.

9. Dividends measure the cash that ____________________ ultimately receive from investing in an

equity share.

SHORT ANSWER

1. Suppose a firm has a market beta of 1.24 and the risk free interest rate is 6.25. In addition, the excess

return over the risk-free rate is 6.3%. Calculate the firm’s cost of equity capital using the CAPM

model.

Bridgetron

An analyst wants to value the sum of the debt and equity capital of the firm and is provided with the

following information:

Total Assets

$25,675

Interest-Bearing Debt

$18,525

Average Pre-tax borrowing cost

9.25%

Common Equity:

Book Value

$ 8,950

Market Value

$34,956

Income Tax Rate

35%

Market Equity Beta

1.05

Risk-free Rate

3.8%

Market Premium

5.7%

2. An analyst wants to value the common shareholders’ equity of Bridgetron, compute the relevant cost

of capital that should be used.

3. Provide the rationale for using expected dividends in a valuation model.

4. In what case will using dividends expected to be paid to shareholders yield the same valuation for the

firm as using free cash flows expected to be generated by the firm?

5. Implementing a dividend valuation model to determine the value of the common shareholders’ equity

requires an analyst to measure three elements. What are the three elements that the analyst needs to

measure?

6. Under the assumption of clean surplus accounting, how would you compute total dividends paid to

common equityholders in order to value the firm?

7. Why are dividends value-relevant to common equity shareholders?

8. Explain why analysts and investors use risk-adjusted expected rates of return as discount rates in

valuation. Why do risk-adjusted expected rates of return increase with risk?

9. The CAPM computes expected rates of return on common equity capital using the following model:

E[REj] = E[RF] + j x {E[RM] – E[RF]}

What are the roles of each of the three components of this model?

10. Identify the types of firm-specific factors that increase a firm’s nondiversifiable risk (systematic risk).

Identify the types of firm-specific factors that increase a firm’s diversifiable

risk (idiosyncratic risk or nonsystematic risk). Why do models of risk-adjusted expected

returns include no expected return premia for diversifiable risk?

11. Why do investors typically accept a lower risk-adjusted rate of return on debt capital than equity

capital? Suppose a stable, financially healthy, profitable, tax-paying firm that has been

financed with all equity and no debt decides to add a reasonable amount of debt to its capital

structure. What effect will that change in capital structure likely have on the firm’s

weighted average cost of capital?

12. Explain the theory behind the dividends valuation approach. Why are dividends value-relevant to

common equity shareholders?

13. The dividends valuation approach measures value-relevant dividends to encompass various

transactions between the firm and the common shareholders. What transactions should the analyst

include in value-relevant dividends for purposes of implementing the dividends valuation model?

Why?

11-10

14. Why is the dividends valuation approach applicable to firms that do not pay periodic (quarterly or

annual) dividends?

15. Conceptually, why should an analyst expect the dividends valuation approach to yield equivalent value

estimates to the valuation approach that is based on free cash flows available to be distributed to

common equity shareholders?

16. According to the text, dividends are value-relevant even though the firm’s dividend policy is

irrelevant. How can that be true? What is the key assumption in the theory of dividend policy

irrelevance?

PROBLEM

1. The following financial statement data pertains to Southwater, Inc., a manufacturer of women’s suits

(dollar amounts in millions):

Total Assets

$154,287

Interest-Bearing Debt

$33,984

11-11

Average Pre-tax borrowing cost

7.75%

Common Equity:

Book Value

$21,365

Market Value

$66,735

Income Tax Rate

39.6%

Market Equity Beta

0.77

Market Premium

7.45%

Risk-free interest rate

2.5%

Required:

a.

Calculate the company’s cost of equity capital.

b.

Calculate the weight on debt capital that should be used to determine Northridge’s

weighted-average cost of capital.

c.

Calculate the weight on equity capital that should be used to determine Northridge’s

weighted-average cost of capital.

d.

Calculate Northridge’s weighted-average cost of capital.

2. The following data pertain to Loren Corporation (dollar amounts in thousands):

Total Assets

$10,254

Interest-Bearing Debt

$1,257

Average Pre-tax borrowing cost

9.20%

Common Equity:

Book Value

$5,624

Market Value

$21,479

Income Tax Rate

32%

Market Equity Beta

1.56

Riskless interest rate

3.8%

Market risk premium

6.5%

a.

Cost of equity capital = =.025+.77(.0745)=.082365 or 8.237%

Market Value of Equity

c.

33.7%

Market Value of Equity

= .01643 + .05728=.01577+.05461=.07038

= .07371, or 7.371%=.07038 or 7.038%

Using this information, calculate the following:

a.

Loren Corporation’s cost of equity capital

b.

The weight on debt capital that should be used to calculate Loren’s weighted-average

cost of capital.

c.

Loren Corporation’s weighted-average cost of capital

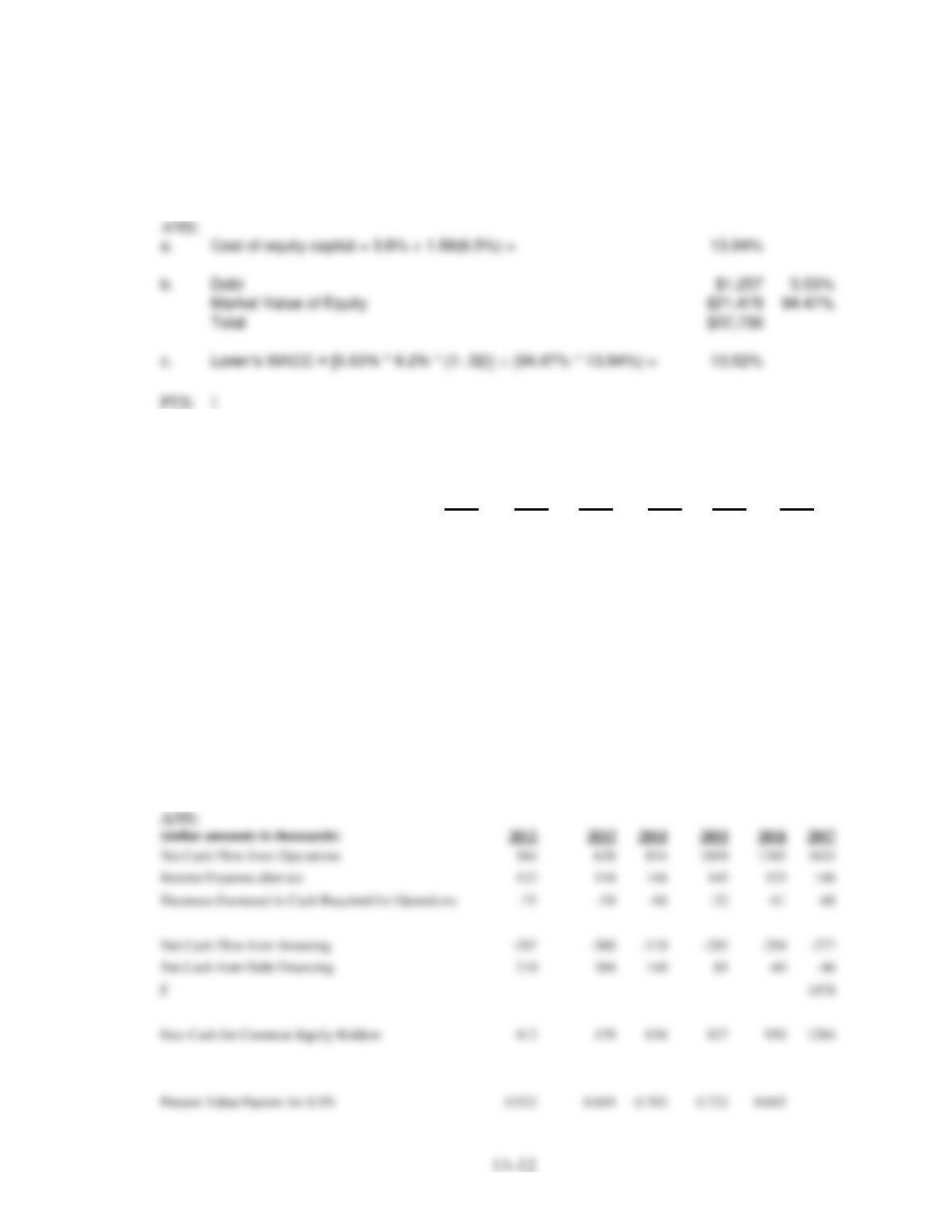

3. Shady Sunglasses operates retail sunglass kiosks in shopping malls. Below is information related to the

company:

(dollar amounts in thousands)

2012

2013

2014

2015

2016

2017

Net Cash Flow from Operations

564

628

854

1059

1345

1655

Interest Expense after tax

122

134

148

145

155

148

Decrease (Increase) in Cash

Required for Operations

-75

-54

-48

-32

-61

-48

Net Cash Flow from Investing

-287

-300

-310

-285

-294

-277

Net Cash from Debt Financing

210

204

140

85

-40

-46

Present Value Factors (Re = 8.5%)

0.922

0.849

0.783

0.722

0.665

Common Shares Outstanding

in thousands

1,512

Using the above information and assuming that steady-state growth in year 2017 and beyond will be

4% calculate Shady Sunglasses value per share.

P

Continuing Value:

4. For each of the following companies, determine the total dividends paid to common equity holders in

order to value the firm:

Company

(amounts in thousands)

Adam

Baxter

Cooper

Dividends Paid to Common

Shareholders

$124

$2,134

$325

Common Stock Repurchases

$412

$140

$1,247

Common Stock Issued

$95

$1,985

$145

Dividends Paid to Common

Shareholders

Common Stock Repurchases

Common Stock Issued

11-14

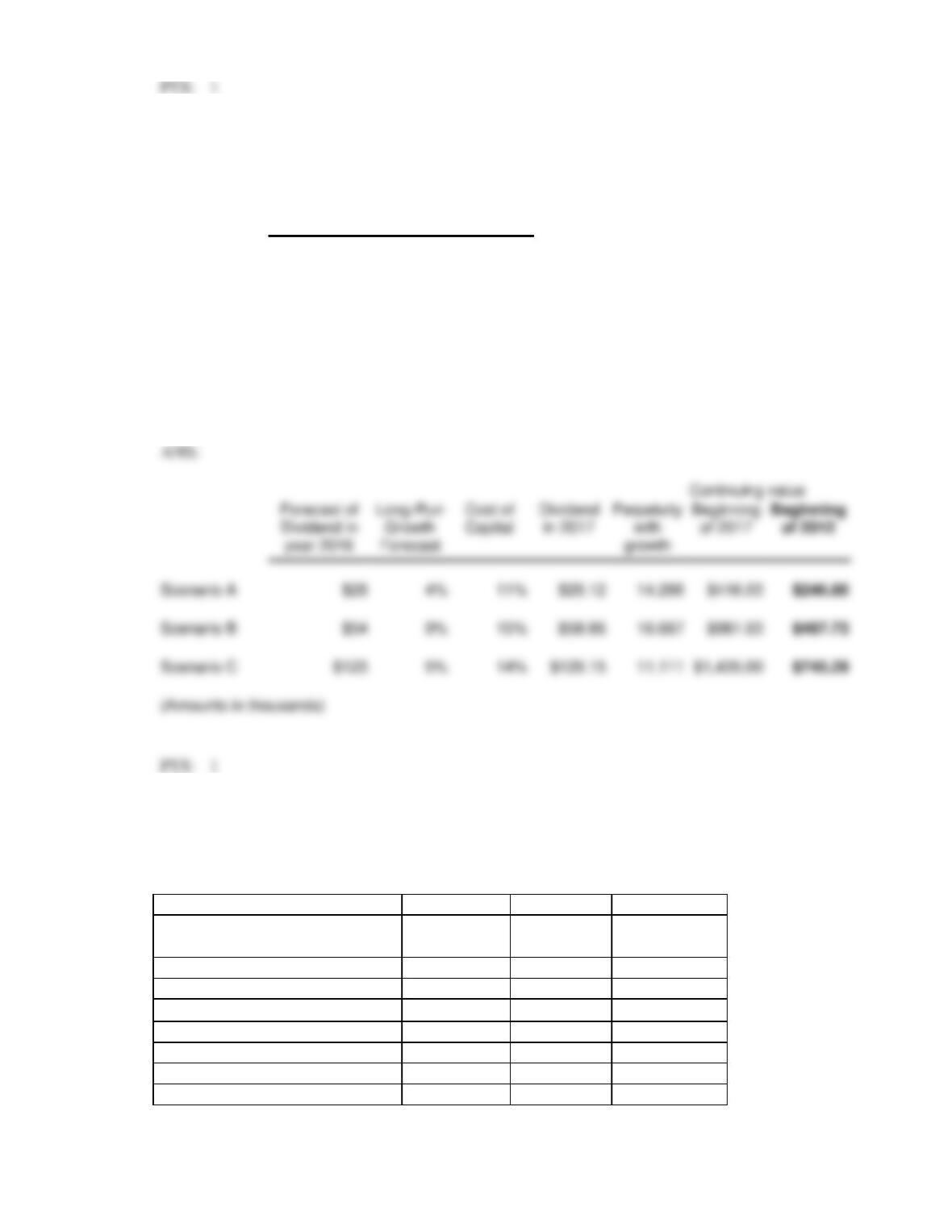

5. For each of the following scenarios determine the value as of the beginning of 2012 of the continuing

dividend:

Forecast of

Dividend in

year 2016

Long-Run

Growth

Forecast

Cost of

Capital

Scenario A

$28

4%

11%

Scenario B

$54

9%

15%

Scenario C

$123

5%

14%

(Amounts in thousands)

6. Watson manufactures and sells appliances. Intro develops and manufactures computer technology.

Trenton operates general merchandise retail stores. Selected data for these companies appear in the

following table (dollar amounts in millions). For each firm, assume that the market value of the debt

equals its book value.

($ amounts in millions)

Watson

Intro

Trenton

Total Assets

$13,532

$109,524

$44,106

Interest-Bearing Debt

$ 2,597

$ 33,925

$18,752

Average Pretax Borrowing Cost

6.1%

4.3%

4.9%

Common Equity:

Book Value

$ 3,006

$ 13,465

$13,712

Market Value

$ 2,959

$110,984

$22,521

Income Tax Rate

35.0%

35.0%

35.0%

Market Equity Beta

2.27

0.78

1.2

Required

a. Assume that the intermediate-term yields on U.S. Treasury securities

are roughly 3.5 percent. Assume that the market risk premium is 5.0 percent.

Compute the cost of equity capital for each of the three companies.

b. Compute the weighted average cost of capital for each of the three companies.

c. Compute the unlevered market (asset) beta for each of the three companies.

11-16

7. Carr Industries must raise $100 million on January 1, 2012 to finance its expansion into a new market.

The company will use the money to finance construction of four retail outlets and a distribution center.

The stores are expected to open later this year. The CFO has come up with three alternatives for

raising the money:

1) Issue $100 million of 8% nonconvertible debt due in 20 years.

2) Issue $100 million of 6% nonconvertible preferred stock (100,00 shares).

3) Issue $100 million of common stock (1 million shares).

The company’s internal forecasts indicate the following 2012 year-end amounts before any option is

chosen:

$ in millions

Total debt

$425

Total shareholders’ equity

250

Net income for the year

10

Carr has no preferred stock outstanding but currently has 10 million shares of common stock

outstanding. EPS has been declining for the past several years. Earnings in 2011 were $1 per share,

which was down from $1.10 during 2010, and management wants to avoid another decline during

2012. One of the company’s existing loan agreements requires a debt–to-equity ratio to be less than 2.

Carr pays taxes at a 40% rate.

Required:

1. Assess the impact of each financing alternative on 2012 EPS and the year-end debt to equity ratio.

2. Which financing alternative would you recommend and why?

ANS:

11-17

8. The following financial statement data pertains to Outside, Inc., a manufacturer of men’s outerware

(dollar amounts in millions):

Total Assets

$145,782

Interest-Bearing Debt

$30,659

Average Pre-tax borrowing cost

9.25%

Common Equity:

Book Value

$22,515

Market Value

$60,843

Income Tax Rate

42%

Market Equity Beta

0.88

Market Premium

8.5%

Risk-free interest rate

2.4%

Required:

a.

Calculate the company’s cost of equity capital.

b.

Calculate the weight on debt capital that should be used to determine Outside’s weighted–

average cost of capital.

c.

Calculate the weight on equity capital that should be used to determine Outside’s

weighted-average cost of capital.

d.

Calculate Outside’s weighted-average cost of capital.