136 Solnik/McLeavey • Global Investments, Sixth Edition

27. A differential swap, or switch LIBOR swap, involves the LIBOR rates in two different currencies but

with both legs denominated in the same currency. A Japanese insurance company engages in a

differential swap whereby it receives the six-month Japanese yen LIBOR and pays the six-month

U.S. dollar LIBOR plus 50 bp but with both legs denominated in yen. No principal is exchanged at

the end. The current LIBOR for the yen and the dollar are 6% and 4%, respectively, and the principal

is 100 million yen. Hence, the first swap payment will be based on a differential of 1.5% in yen [6% = (4% −

0.5%)]. The current yield pick-up is 150 bp. There is no currency risk on this swap.

Provide some intuitive explanation for the pricing of such a swap, knowing that at the time, the dollar

yield curve was very steep (long-term rates are much higher than short-term rates) and the yen yield

curve was almost flat.

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 137

28. You are an investment banker working in Switzerland where yields are very low (1% for all maturities).

You are planning to offer a five-year Swiss franc/British pound bond with the following characteristics:

• Issuer: Brit Ltd., a top-quality British company.

• Issue amount: SFr 100 million.

• Coupon in SFr: 5% (or SFr 5 million).

• Reimbursed value: £40 million.

This bond qualifies as a Swiss franc bond for the portfolio of a Swiss insurance company.

The current spot exchange rate is 2.5 Swiss francs per British pound. The yield curve in British

pounds is flat at 7%. The pound/franc swap rates are 7% in pounds against 1% in francs for all

maturities.

a. Assume that Swiss insurance companies can account for their Swiss franc bond holdings

at historical costs. Give a reason why it would be attractive to invest in this bond.

b. Is the coupon rate set at fair pricing (i.e., consistent with current market conditions)?

c. The British company desires to borrow in pounds and does not wish to carry any currency risk on

its debt. The investment banker needs to design a coupon swap that would hedge the currency

risk on that dual-currency bond for Brit Ltd. The designed swap should have a zero value at time

of contracting. Give one possible design for the swap and calculate its associated swap rate.

d. What is the pound yield paid by the British company, once it has hedged its currency risk on the

dual-currency bond using the swap described above? What is the annual cost-saving in British

pounds compared to a straight pound bond?

Solution

138 Solnik/McLeavey • Global Investments, Sixth Edition

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 139

29. Assume that an AAA customer pays 8% on a five-year loan and can contract a five-year interest

rate swap (paying fixed) at 8% against LIBOR. Assume that a BBB customer pays (8 + m)% on a

five-year loan and can contract a five-year interest rate swap (paying fixed) at (8 + µ)% against

LIBOR. Should a customer pay the same credit-quality spread (m and µ) on a loan and on a swap?

Solution

30. The current market conditions for an AAA client are 8% on a one-year dollar loan, and 8% fixed U.S.

dollars for 9% fixed British pounds on a one-year dollar/pound currency swap. Let’s consider a BBB

client borrowing at (8 + m)% on a one-year dollar loan. The same client can enter a dollar/pound

currency swap, paying (8 + µ)% fixed dollars and receiving 9% fixed pounds. Assume that the

customer has a probability of p% to default within a year. In case of default, the bank knows that it

will recover nothing on either transaction. The probability of default p (e.g., 5%) is known and

independent of movements in interest and exchange rates. The spot exchange rate is S0 = 1 $/£.

Assuming that you can observe the prices of $/£ currency options, suggest some approach to

determine the fair values of m and µ. (Assume that the bank has a large number of clients whose

probabilities of default are independent; therefore, the bank can diversify away the uncertainty of

default on this specific client.)

140 Solnik/McLeavey • Global Investments, Sixth Edition

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 141

142 Solnik/McLeavey • Global Investments, Sixth Edition

31. A traditional interest rate swap has a notional capital of 100 and exchange LIBOR (the floating leg)

against 6% (fixed leg). At maturity of the swap there is no capital exchange as the same notional

capital of 100 is “exchanged” on both legs. Assume that the swap has a five-year maturity.

A company needs to create an immediate cash flow to offset an immediate loss and decides to use an

amortizing swap. Its off-balance sheet items are accounted at their book or historical values. The

floating leg is LIBOR, paid quarterly, with a notional capital of 100. The fixed leg also has a notional

capital of 100, however, there is only an initial cash flow of X on the fixed leg of the amortizing swap

and no other cash flow (zero coupons). Hence, there is no capital exchanged at maturity of the swap

(capital identical on both legs). The swap is priced (the value of X is set) so that the initial swap value

is zero.

The company enters the amortizing swap to pay floating and receive fixed. In other words, its cash

flows on the swap are as follows:

• Receive X at time 0.

• Pays LIBOR every quarter for five years.

• No cash flow at maturity.

a. Why is the amortizing swap interesting for this company, which wants to window-dress an

immediate loss? How will it impact its future earnings?

b. The term structure is flat at 6%. What should be the “fair” value of X?

c. The company expects a loss of 10 million, what should be the notional capital of the amortizing

swap that should be contracted?

d. Assume now that the company must value all off-balance sheet items at their market value. What

would happen to the value of the swap immediately after the payment of X is received by the

company? Are amortizing swaps useful in deferring losses with this accounting convention?

Solution

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 143

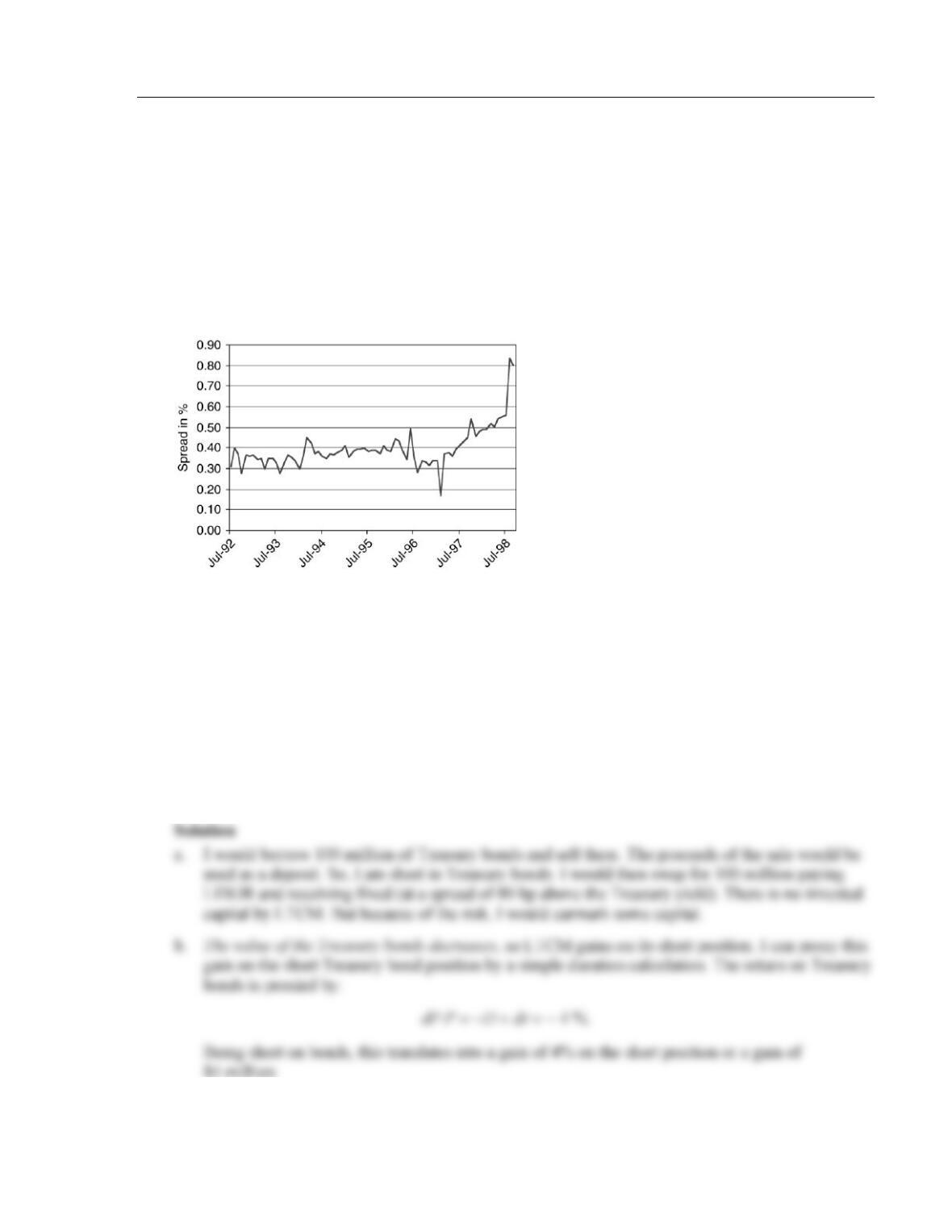

32. LTCM observed the following ten-year swap spreads on July 1, 1998. You remember that U.S. dollar

interest swaps (fixed rate against LIBOR three-month) are quoted as a spread over the Treasury yield

(so the fixed rate on the swap is equal to the interest rate on Treasury bonds for the same maturity

plus the quote spread). LTCM believes that the normal spread is 40 bp (basis points). The current

spread of 80 bp is expected to converge back to normal in three months.

If you borrow securities, you have to deposit as collateral an equivalent amount of cash that is

marked-to-market. For example, if you borrow a security that is worth 100, you have to deposit 100;

if the value of the security increases to 110, you have to deposit 10 more. Swaps are also marked-to-

market and free of default risk.

a. What arbitrage using Treasury bonds and swaps could you put in place if you believe that the

spread will revert back to its normal level? Be very precise and assume you do the above

arbitrage for $100 million. How much of LTCM capital is invested in the arbitrage?

b. Suppose that the spread is still at 80 bp on October 1, but that Treasury yields have moved

up by 40 bp on October 1 (reset date for the floating leg). What is your gain/loss in dollars?

[You only need to provide a rough estimate assuming that the sensitivity (duration) on the

Treasury bond and fixed leg of the swap is equal to 10.]

c. Other scenario: How much would you gain (from July 1) if Treasury yields do not move, but

the spread reverts back to 40 bp three months later on October 1 (reset date for the floating leg)?

[You only need to provide a rough estimate assuming that the sensitivity (duration) on the

Treasury bond and fixed leg of the swap is equal to 10.]

144 Solnik/McLeavey • Global Investments, Sixth Edition

33. If the average premium on gold call options declines, does this mean that they are becoming

undervalued and, therefore, should be bought? Using valuation models, give at least two possible

reasons for this decline.

Solution

34. The average premium on currency calls has decreased, whereas the premium on currency puts has

increased. What explanations can you provide?

35. You will receive $10 million at the end of June and will invest it for three months on the Eurodollar

market. The current three-month Eurodollar rate is 6%, and you are worried that the rate will drop by

the end of June. Here are some market quotes:

• Eurodollar LIBOR futures, June delivery: Price 94%.

• Call eurodollar, June expiration, strike price 94%: Premium 0.4%.

• Put Eurodollar, June expiration, strike price 94%: Premium 0.4%.

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 145

The contract sizes are $1 million.

a. Should you buy or sell futures to hedge your interest rate risk?

b. Should you buy (or sell) calls (or puts) to insure a minimum rate at the time you will invest your

money? What is this rate?

c. In June, the Eurodollar rate has moved to 4%. What is the result of your strategies using futures

and using options?

d. What if the rate is equal to 8% in June?

Solution

36. The French futures market, MATIF, trades Euribor contracts. The Euribor is the three-month

interbank interest rate on euros. The contract size is €1 million, and the margin is €3,000. On

January 10, March futures trade at 90.74%. Options on the Euribor futures contract are also listed.

The premiums (in %) on March options are as follows:

Strike Price

Call

Put

90.40

0.30

0.06

90.80

0.17

0.18

91.00

0.09

0.34

A few days later (January 14), the futures price moves to 89.50.

a. What is the gain or loss, in euros, for someone who sold a futures contract on January 10?

b. What is the return, as a percentage of the initial investment (margin)?

c. Are all option premiums quoted on January 10 reasonable?

d. You know that you will have to borrow €10 million in March and fear a rise in interest rates.

What are the maximum borrowing rates that you can insure using the various options?

e. To cap your borrowing rate, you decide to use options with a strike price of 90.80. How many

calls (or puts) should you buy (or sell)?

On January 14, the premium on the call March 90.80 moves to 0.02, and the premium on the put

March 90.80 moves to 1.33.

f. What is the € profit (or loss) on your option position?

g. What is the rate of return on your option position?

146 Solnik/McLeavey • Global Investments, Sixth Edition

Solution

37. You are currently borrowing €10 million at three-month Euribor + 75 basis points. The Euribor is

at 3%. You expect to borrow this amount for five years but are worried that Euribor will rise in the

future. You can buy a 4% cap on three-month Euribor over the next five years with an annual cost of

0.75% (paid quarterly). Describe the evolution of your borrowing costs under various interest rate

scenarios (i.e., above and below 4%).

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 147

Solution

38. You would like to protect your portfolio of British equity against a downward movement of the

British stock market.

a. What are the relative advantages of stock index futures and options?

b. Should you prefer in-the-money or out-of-the-money options?

Solution

39. The current dollar yield curve on the dollar international bond market is flat at 7% for top-quality

borrowers. A company of good standing can issue plain-vanilla straight and floating-rate dollar bonds

under the following conditions:

• Bond A: Straight bond. Five-year straight dollar bond with a coupon of 7.25%.

• Bond B: FRN. Five-year dollar FRN with a semiannual coupon set at LIBOR plus 0.25% and

a cap of 14%. The cap means that the coupon rate is limited to 14% even if the LIBOR passes

13.75%.

An investment banker proposes to a French company to issue bull and/or bear FRNs under the

following conditions:

• Bond C: Bull FRN. Five-year FRN with a semiannual coupon set at: 13.75% – LIBOR.

• Bond D: Bear FRN. Five-year FRN with a semiannual coupon set at: 2 LIBOR – 7% and a cap

of 20.5%.

Coupons on all bonds cannot be negative. The investment bank also proposes a five-year floor option

at 3.5%. This floor will pay to the French company the difference between 3.5% and LIBOR, if it is

positive, or zero if LIBOR is above 3.5%. The cost of this floor is spread over the payment dates and