CFIN4

Chapter 10 – Project Cash Flows and Risk

64. Which of the following cash flows are incremental cash flows that need to be considered when evaluating a capital

project?

a. Interest expenses on the financing of the project.

b. Sunk costs of engineering study to determine the feasibility of the project.

c. Opportunity cost of land being used for project that the firm already owns.

d. Both a and b are correct.

e. None of the above.

65. Depreciation must be considered when evaluating the incremental operating cash flows associated with a capital

budgeting project because

a. it represents a tax-deductible cash expense.

b. the firm has a cash outflow equal to the depreciation expense each year.

c. although it is a non–cash expense, depreciation has an impact on the taxes paid by the firm, which is a cash

flow.

d. depreciation is a sunk cost.

e. None of the above is correct.

66. Hill Top Lumber Company is considering building a sawmill in the state of Washington because the company

doesn‘t have such a facility to service its growing customer base that is located on the west coast. Hill Top’s

executives believe that future growth in west coast customers will make the sawmill project a good investment.

When evaluating the acceptability of the project, which of the following would not be considered a relevant cash

flow that should be included when determining its initial investment outlay?

a. Hill Top owns acreage that is large enough and would be an ideal location for the sawmill. The land, which

was purchased five years ago, has a current value of $3 million.

b. It is estimated that the cost of building the sawmill will be $175 million.

c. It will cost $3 million to clear the land on which Hill Top wants to build the sawmill.

d. It is estimated that $20 million of business from existing customers will move to the new sawmill.

e. All of these cash flows should be included in the computation of the sawmill‘s initial investment outlay.

67. A firm is evaluating a new machine to replace an existing, older machine. The old (existing) machine is being

depreciated at $20,000 per year, whereas the new machine‘s depreciation will be $18,000. The firm’s marginal tax

rate is 30 percent. Everything else equal, if the new machine is purchased, what effect will the change in

depreciation have on the firm‘s incremental operating cash flows?

a. There should be no effect on the firm’s cash flows, because depreciation is a noncash expense.

b. Operating cash flows will increase by $2,000.

c. Operating cash flows will increase by $1,400.

d. Operating cash flows will decrease by $600.

e. None of the above is correct.

68. When evaluating the cash flows associated with a capital budgeting project, shipping and installation costs

associated with the purchase of an asset, such as a lathe, are considered part of the

a. initial investment outlay because these expenses effectively are part of the asset’s purchase price.

b. incremental operating cash flows because shipping and installation costs represent expenses that have to be

written off over the life of the asset.

c. terminal cash flows, because these expenses aren’t paid until the end of the asset’s life.

d. sunk costs because these expenses do not affect any current or future cash flows associated with investing

in the asset.

e. None of the above is a correct answer.

69. Express Press evaluates many different capital budgeting projects each year. The risks of the projects often differ

significantly, from very little risk to risks that are substantially greater than the average risk associated with the

firm. If Express Press always uses its weighted average cost of capital, or average required rate of return, to

evaluate all of these capital budgeting projects, then the company might make an incorrect decision, or a mistake,

by

a. accepting projects that actually should be rejected.

b. accepting projects with internal rates of return that are too high.

c. rejecting projects that actually should be rejected.

d. rejecting projects with internal rates of return that are lower than the appropriate risk-adjusted required rate

of return.

e. accepting project that actually should be accepted.

70. Cyrus Cypress evaluates all capital budgeting projects with its normal, or average, required rate of return (k),

regardless of the risk associated with the projects. If Cyrus is currently examining projects that are significantly

riskier than the existing assets of the firm, the capital budgeting decisions that the firm makes could be

a. correct.

b. incorrect because acceptable projects might be rejected when they should be accepted.

c. incorrect because unacceptable projects might be accepted when they should be rejected.

d. Both a and b are correct answers.

e. Both a and c are correct answers.

71. Which of the following items should not be considered when computing the terminal cash flow for an expansion

project?

a. a change in net working capital associated with the purchase of the project

b. the selling price of the asset at the end of its life

c. increases in cash sales that occur because the project is purchased

d. taxes on the sale of the asset at the end of its life

e. none of the above

72. When determining the marginal cash flows associated with an expansion capital budgeting project, which of the

following would be included as an incremental operating cash flow?

a. depreciation

b. shipping and installation

c. increase in working capital

d. salvage value

e. decrease in sales

73. If a firm uses its weighted average cost of capital (WACC) to evaluate all capital budgeting projects, which of the

following could occur?

a. Projects with little or no risk might be rejected when they actually should be accepted.

b. Projects with significant risks might be accepted when the actually should be rejected.

c. Projects with average risk will always be rejected when they actually should be rejected.

d. All of the above could occur.

e. None of the above could occur.

74. An evaluation of four independent capital budgeting projects by the director of capital budgeting for Ziker Golf

Company yielded the following results:

Internal rate of

Project

of return, IRR

Risk level

L

19.0%

Average

E

15.0

High

M

12.0

Low

Q

11.0

Average

The firm’s weighted average cost of capital is 12 percent. Ziker Golf generally evaluates projects that are riskier

than average by adjusting its required rate of return by 4 percent, whereas projects with less-than-average risk are

evaluated by adjusting the required rate of return by 2 percent. Which project(s) should the firm purchase?

a. Project L

b. Projects L and E

c. Projects L and M

d. Projects L, E, and M

e. None of the above is a correct answer.

75. How do most firms deal with the risks of projects when making capital budgeting decisions?

a. Projects risks are not considered directly because the weighted average cost of capital (WACC) that is used

as the required rate of return for capital budgeting decisions is based on the riskiness of the firm. As a result,

all projects, no matter their risks, can be evaluated using WACC.

b. Evaluating risk is important only when the projects are similar to the firm’s existing assets.

c. Most firms adjust the discount rates used to evaluate new projects that have significantly different risks than

the risk associated with the firm‘s existing assets.

d. Firms generally increase the required rate of return used to evaluate projects that have significantly different

risks than the risk associated with the firm’s existing assets, regardless of whether the new projects’ risks are

higher or lower.

e. None of the above is a correct answer.

76. Dick Boe Enterprises, an all-equity firm, has a corporate beta coefficient of 1.5. The financial manager is

evaluating a project with an IRR of 21 percent, before any risk adjustment. The risk-free rate is 10 percent, and the

required rate of return on the market is 16 percent. The project being evaluated is riskier than Boe’s average project,

in terms of both beta risk and total risk. Which of the following statements is correct?

a. The project should be accepted because its IRR (before risk adjustment) is greater than its required return.

b. The project should be rejected because its IRR (before risk adjustment) is less than its required return.

c. The accept/reject decision depends on the risk-adjustment policy of the firm. If the firm’s policy were to

reduce a riskier-than-average project‘s IRR by 1 percentage point, then the project should be accepted.

d. Riskier-than-average projects should have their IRRs increased to reflect their added riskiness. Clearly, this

would make the project acceptable regardless of the amount of the adjustment.

e. Projects should be evaluated on the basis of their total risk alone. Thus, there is insufficient information in the

problem to make an accept/reject decision.

77. Carolina Insurance Company, an all-equity life insurance firm, is considering the purchase of a fire insurance

company. If the purchase is made, Carolina will be 50 percent larger than before. Currently, Carolina’s stock has a

beta of 1.2 and the return required is 15.2 percent. The fire insurance company is expected to generate a return of

20 percent with a beta of 2.5. If the risk-free rate is 8 percent and the market risk premium is 6 percent, should

Carolina make the investment?

a. No; the expected return is less than the required return.

b. No; the IRR is less than the appropriate required rate of return.

c. Yes; the IRR is greater than the appropriate required rate of return.

d. Yes; the expected return is greater than the required return.

e. Yes; the project’s risk/return combination lies above the SML.

CFIN4

Chapter 10 – Project Cash Flows and Risk

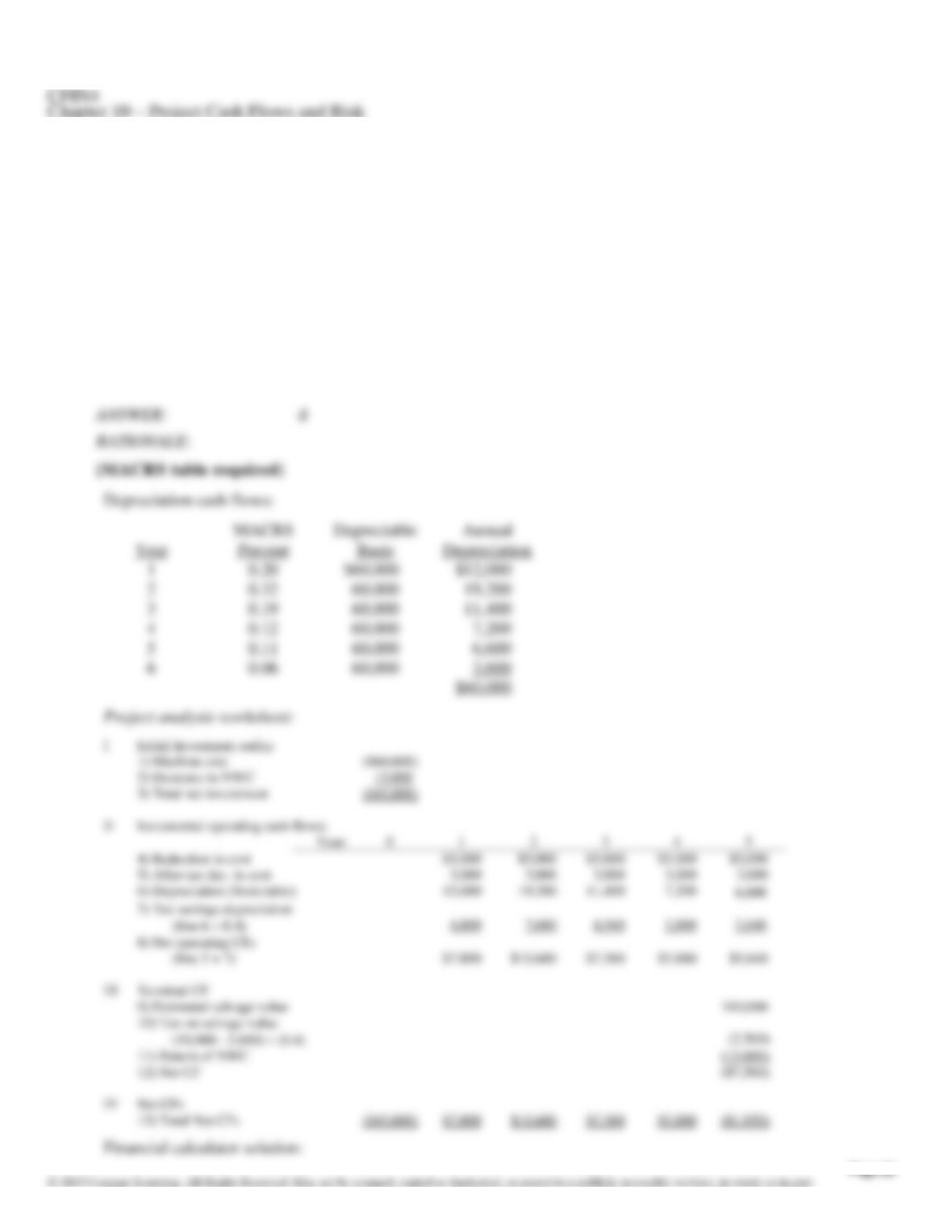

78. Given the following information, calculate the NPV of a proposed project: Cost = $4,000; estimated life = 3 years;

initial decrease in accounts receivable = $1000, which must be restored at the end of the project’s life; estimated

salvage value = $1,000; net income before taxes and depreciation = $2,000 per year; method of depreciation =

MACRS; tax rate = 40 percent; required rate of return = 18 percent.

a. $1,137

b. −$151

c. $137

d. $804

e. $544

79. Mars Inc. is considering the purchase of a new machine which will reduce manufacturing costs by $5,000 annually.

Mars will use the MACRS accelerated method to depreciate the machine, and it expects to sell the machine at the

end of its 5-year operating life for $10,000. The firm expects to be able to reduce net working capital by $15,000

when the machine is installed, but required working capital will return to the original level when the machine is sold

after 5 years. Mars’ marginal tax rate is 40 percent, and it uses a 12 percent required rate of return to evaluate

projects of this nature. If the machine costs $60,000, what is the NPV of the project?

a. −$15,394

b. −$14,093

c. −$58,512

d. −$21,493

e. −$46,901

80. Stanton Inc. is considering the purchase of a new machine which will reduce manufacturing costs by $5,000

annually and increase earnings before depreciation and taxes by $6,000 annually. Stanton will use the MACRS

method to depreciate the machine, and it expects to sell the machine at the end of its 5-year operating life for

$10,000 before taxes. Stanton’s marginal tax rate is 40 percent, and it uses a 9 percent required rate of return to

evaluate projects of this type. If the machine’s cost is $40,000, what is the project’s NPV?

a. $1,014

b. $2,292

c. $7,550

d. $817

e. $5,040

CFIN4

Chapter 10 – Project Cash Flows and Risk

81. Whitney Crane Inc. has the following independent investment opportunities for the coming year:

Annual Cash

Project

Cost

Inflows

Life (years)

IRR

A

$10,000

$11,800

1

B

5,000

3,075

2

15

C

12,000

5,696

3

D

3,000

1,009

4

13

The IRRs for Project A and C, respectively, are:

a. 16% and 14%

b. 18% and 10%

c. 18% and 20%

d. 18% and 13%

e. 16% and 13%

82. Sun State Mining Inc., an all-equity firm, is considering the formation of a new division which will increase the

assets of the firm by 50 percent. Sun State currently has a required rate of return of 18 percent, U.S. Treasury

bonds yield 7 percent, and the market risk premium is 5 percent. If Sun State wants to reduce its required rate of

return to 16 percent, what is the maximum beta coefficient the new division could have?

a. 2.2

b. 1.0

c. 1.8

d. 1.6

e. 2.0

83. An all-equity firm is analyzing a potential project which will require an initial, after–tax cash outlay of $50,000 and

after-tax cash inflows of $6,000 per year for 10 years. In addition, this project will have an after–tax salvage value

of $10,000 at the end of Year 10. If the risk-free rate is 6 percent, the return on an average stock is 10 percent, and

the beta of this project is 1.50, then what is the project’s NPV?

a. $13,210

b. $4,905

c. $7,121

d. −$6,158

e. −$12,879

84. Real Time Systems Inc. is considering the development of one of two mutually exclusive new computer models.

Each will require a net investment of $5,000. The cash flow figures for each project are shown below:

Period

Project A

Project B

1

$2,000

$3,000

2

2,500

2,600

3

2,250

2,900

Model B, which will use a new type of laser disk drive, is considered a high-risk project, while Model A is of

average risk. Real Time adds 2 percentage points to arrive at a risk-adjusted discount rate when evaluating a high-

risk project. The rate used for average risk projects is 12 percent. Which of the following statements regarding the

NPVs for Models A and B is most correct?

a. NPVA = $380; NPVB = $1,815.

b. NPVA = $197; NPVB = $1,590.

c. NPVA = $380; NPVB = $1,590.

d. NPVA = $5,380; NPVB = $6,590.

e. None of the above statements is correct.

85. The Unlimited, a national retailing chain, is considering an investment in one of two mutually exclusive projects. The

discount rate used for Project A is 12 percent. Further, Project A costs $15,000, and it would be depreciated using

MACRS. It is expected to have an after-tax salvage value of $5,000 at the end of 6 years and to produce after-tax

cash flows (including depreciation) of $4,000 for each of the 6 years. Project B costs $14,815 and would also be

depreciated using MACRS. B is expected to have a zero salvage value at the end of its 6-year life and to produce

after-tax cash flows (including depreciation) of $5,100 each year for 6 years. The Unlimited’s marginal tax rate is

40 percent. What risk-adjusted discount rate will equate the NPV of Project B to that of Project A?

a. 15%

b. 16%

c. 18%

d. 20%

e. 12%

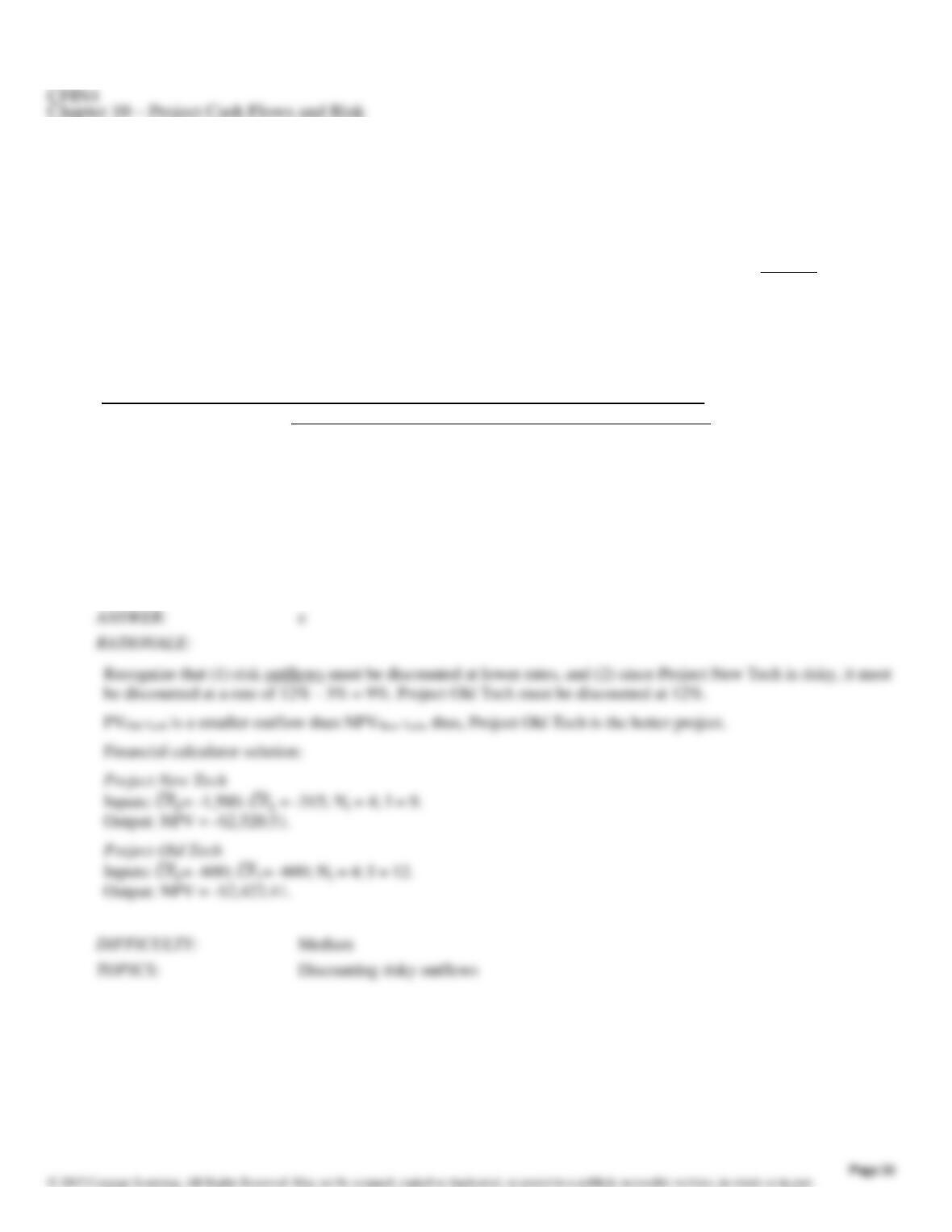

86. Alabama Pulp Company (APC) can control its environmental pollution using either “Project Old Tech” or “Project

New Tech.” Both will do the job, but the actual costs involved with Project New Tech, which uses unproved, new

state-of-the–art technology, could be much higher than the expected cost levels. The cash outflows associated with

Project Old Tech, which uses standard proven technology, are less risky they are about as uncertain as the cash

flows associated with an average project. APC’s required rate of return for average risk projects normally is set at

12 percent, and the company adds 3 percent for high risk projects but subtracts 3 percent for low risk projects. The

two projects in question meet the criteria for high and average risk, but the financial manager is concerned about

applying the normal rule to such cost-only projects. You must decide which project to recommend, and you should

recommend the one with the lower PV of costs. What is the PV of costs of the better project?

Cash Outflows

Years

0

1

2

3

4

Project New Tech

1,500

315

315

315

315

Project Old Tech

600

600

600

600

600

a.

2,521

b.

2,399

c.

2,457

d.

2,543

e.

2,422

87. Arizona Rock, an all-equity firm, currently has a beta of 1.25, and rRF = 7 percent and rM = 14 percent. Suppose

the firm sells 10 percent of its assets (beta = 1.25) and purchases the same proportion of new assets with a beta of

1.1. What will be the firm’s new overall required rate of return, and what rate of return must the new assets

produce in order to leave the stock price unchanged?

a. 15.645%; 15.645%

b. 15.75%; 14.7% c.

15.645%; 14.7% d.

15.75%; 15.645% e.

14.75%; 15.75%

88. Klott Company encounters significant uncertainty with its sales volume and price in its primary product. The firm

uses scenario analysis in order to determine an expected NPV, which it then uses in its budget. The base case, best

case, and worst case scenarios and probabilities are provided in the table below. What is Klott’s expected NPV,

standard deviation of NPV, and coefficient of variation of NPV?

Probability of

Outcome

Unit Sales

Volume

Sales

Price

NPV

(In Thousands)

Worst case

0.30

6,000

$3,600

-$6,000

Base case

0.50

10,000

4,200

+13,000

Best case

0.20

13,000

4,400

+28,000

a.

Expected NPV = $35,000; NPV = 17,500; CVNPV = 2.0.

b.

Expected NPV = $35,000; NPV = 11,667; CVNPV = 0.33.

c.

Expected NPV = $10,300; NPV = 12,083; CVNPV = 1.17.

d.

Expected NPV = $13,900; NPV = 8,476; CVNPV = 0.61.

e.

Expected NPV = $10,300; NPV = 13,900; CVNPV = 1.35.

Worst case

0.3(-6,000) = -1,800

Base case

0.50

Best case

Worst case

Base case

Best case

146.01

89. Rucker Truck Line (RTL) is evaluating whether the fleet of trucks it owns should be replaced. If the trucks are

replaced, current operating revenues and expenses will not change, except for depreciation expenses. Annual

depreciation will increase from $150,000 to $175,000. Based on this information, how will the change in depreciation

expense affect the incremental operating cash flows RTL examines when making its capital budgeting decision

about replacing the trucks? RTL‘s marginal tax rate is 40 percent.

a. After-tax operating cash flows will increase by $15,000.