a.

They react slowly to actions taken by other firms

b.

They lower prices together

c.

They raise prices together

d.

They know with certainty what they other firms will do

e.

They take into consideration how other firms might react.

96. When oligopolists take into account their competitors’ behavior, this situation is called:

a.

mutual interdependence.

b.

monopolistic competition.

c.

independent.

d.

price discrimination.

e.

loss minimization.

97. Mutual interdependence applies to actions of:

a.

monopolistic competitors.

b.

oligopolists.

c.

perfect competitors.

d.

monopolists.

e.

firms operating in different industries.

98. Pricing and output determination under an oligopoly is more complicated than pricing and output

determinations in other industries. The primary reason for the complication is the:

a.

fewness of firms.

b.

brand loyalty of consumers.

c.

powerful effect of advertising.

d.

variability of concentration ratios.

e.

mutual interdependence of firms.

99. Suppose Ford, GM, and Dodge make the majority of pick-up trucks sold in the United States If they all

sell for approximately the same price, and Ford offers a $2,000 rebate on new truck sales, what can

Ford expect to see?

a.

an unprecedented increase in truck sales

b.

an immediate response by GM and Dodge

c.

a visit from the antitrust authorities of the government

d.

a revolution from Ford stockholders

e.

announcements by GM and Dodge that plans are underway to produce a much cheaper

pick-up truck in six years

100. A “kinked” demand curve reflects a tendency on the part of an oligopolist to:

a.

follow price increases but not price reductions.

b.

following price reductions but not price increases.

c.

be unconcerned with rivals’ behavior.

d.

None of these.

101. An oligopolist operating with a kinked demand curve would expect rivals to match its price:

a.

increases.

c.

both a and b.

b.

decreases.

d.

neither a nor b.

102. A kink in the demand curve facing an oligopolist is caused by:

a.

rapidly rising marginal revenues.

b.

excessive advertising.

c.

the belief that competitors will follow price increases but not match price decreases.

d.

the tendency of competitors to follow price reductions but not price increases.

103. As a result of a kinked demand curve, the price:

a.

fluctuates.

c.

settles at the kink.

b.

falls below the kink.

d.

rises above the kink.

104. Suppose an oligopoly has a dominant firm that sets the price for the entire industry. In this situation,

the oligopoly has:

a.

nonprice competition.

c.

price leadership.

b.

a kinked demand curve.

d.

a cartel.

105. The “kinked” oligopoly demand curve is a result of the assumption by an oligopolist that:

a.

price increases will be matched, but price reductions will not.

b.

price increases will not be matched, but price reductions will.

c.

both price increases and price reductions will be matched.

d.

neither price increases, nor price reductions will be matched.

106. The kinked demand theory attempts to explain why an oligopolistic firm:

a.

has relatively large advertising expenditures.

b.

fails to invest in research and development (R and D).

c.

infrequently changes its price.

d.

engages in excessive brand proliferation.

107. According to the kinked demand theory, when one firm raises its price, other firms will:

a.

also raise their prices.

b.

refuse to follow.

c.

increase their advertising expenditures.

d.

exit the industry.

108. A kink in the demand curve facing an oligopolist is caused by:

a.

the belief that competitors will follow price increases but not match price decreases.

b.

excessive advertising.

c.

rapidly rising marginal revenues.

d.

the assumption that competitors will follow price reductions but not price increases.

109. The assumption(s) made to construct a kinked-demand oligopoly model is (are) that:

a.

all firms in the industry will ignore the price changes made by any one firm.

b.

any price decrease will be ignored, but price increases will be followed.

c.

all firms will follow a price decrease but will ignore any price increase.

d.

all price changes made by any firm will be followed by all of the other firms.

e.

price can go up, but it cannot go down.

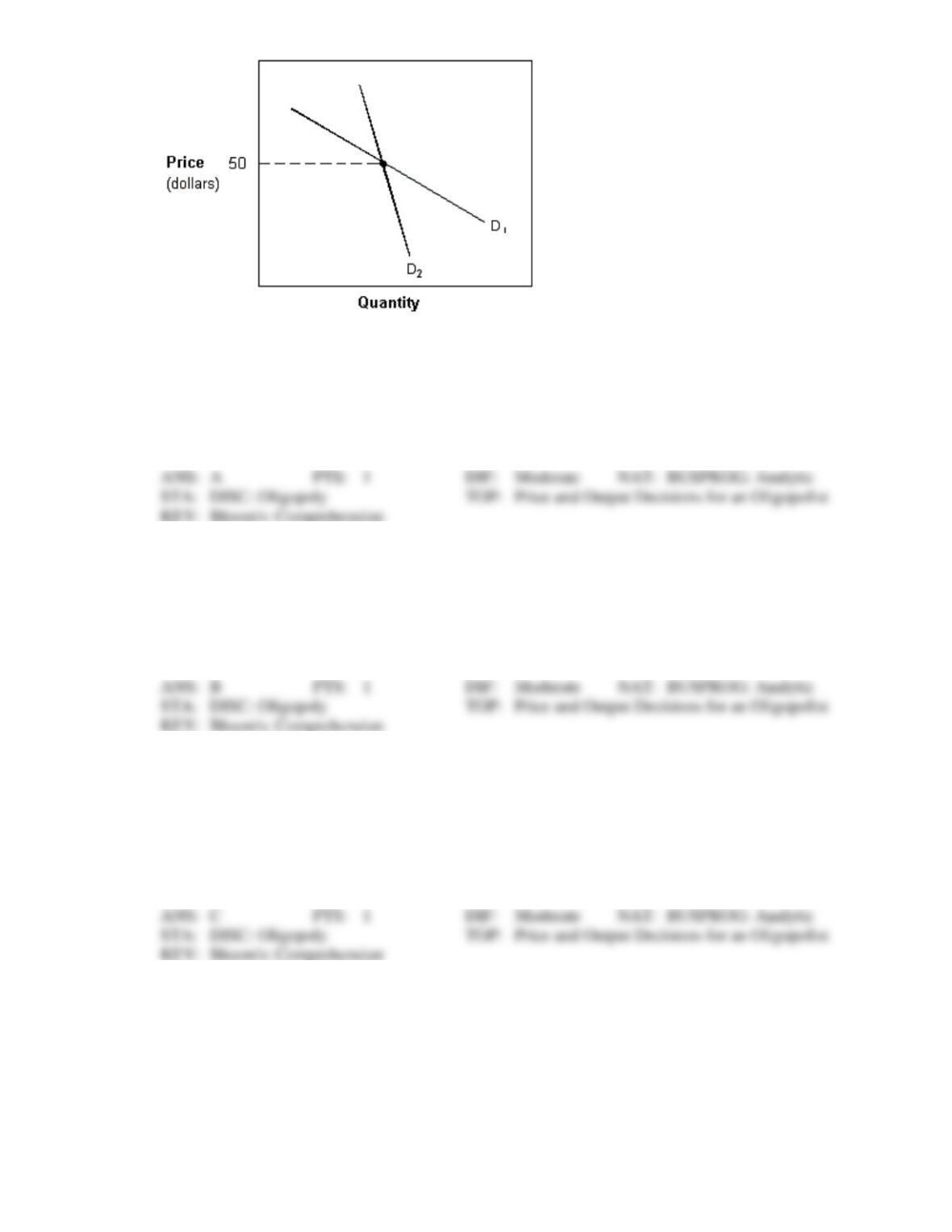

Exhibit 10-4 Kinked demand curves

110. In Exhibit 10-4, in a kinked-demand oligopoly model, D1 represents the:

a.

demand curve applicable to any price increase above $50.

b.

demand curve applicable to any price decrease below $50.

c.

demand curve facing firms when a cartel is formed.

d.

market demand curve.

e.

demand curve facing the price leader.

111. In Exhibit 10-4, in a kinked-demand oligopoly model, D2 represents the:

a.

demand curve applicable to any price increase above $50.

b.

demand curve applicable to any price decrease below $50.

c.

demand curve facing firms when a cartel is formed.

d.

market demand curve.

e.

demand curve facing the price leader.

112. In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is

$50. If one firm in the oligopoly now attempts to raise price, all firms will:

a.

follow along demand curve D1.

b.

follow along demand curve D2.

c.

ignore this price increase and cause the price-raising firm to move along D1.

d.

ignore this price increase and cause the price-raising firm to move along D2.

e.

lower their prices.

113. In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is

$50. If one firm in the oligopoly now attempts to lower price, all firms will:

a.

follow along demand curve D1.

b.

follow along demand curve D2.

c.

ignore this price decrease and cause the price-raising firm to move along D1.

d.

ignore this price decrease and cause the price-raising firm to move along D2.

e.

raise their prices.

114. The conclusion arrived at from a kinked-demand oligopoly model is that:

a.

oligopoly firms cannot maximize their profits.

b.

oligopoly firms should keep prices at their current level.

c.

all oligopoly firms should raise prices.

d.

all oligopoly firms should lower prices.

e.

oligopoly market structure will lead to lower prices than more competitive industries.

115. The kinked demand curve:

a.

applies when competitors match price decreases but not price increases.

b.

could apply to market demand in any market structure.

c.

applies when competitors match price increases but not price decreases.

d.

applies to the price leadership model.

e.

applies when competitors act independently.

116. A kinked demand curve is perceived by the firm as being:

a.

more elastic to the right of the kink

b.

more inelastic to the right of the kink

c.

more inelastic to the left of the kink

d.

present when there is a monopoly

e.

bowed-in or bowed-out

117. For a kinked demand curve, the marginal revenue curve is:

a.

positively sloped.

b.

a horizontal line.

c.

a vertical line.

d.

discontinuous.

e.

above the demand curve.

118. Assume that an oligopolist has a kinked demand curve. Suppose that the marginal cost curve passes

through the gap in the marginal revenue curve. This means price and output will be shown by a point:

a.

above the curve.

b.

below the curve.

c.

at the kink

d.

on the upper part of the curve.

e.

on the lower part of the curve.

119. An increase in marginal cost that remains within the gap of the marginal revenue curve of a kinked

demand oligopolist will:

a.

keep price and output the same.

b.

raise price and decrease output.

c.

lower price and increase output.

d.

raise price and raise output.

e.

lower price and lower output.

120. In a price leadership oligopoly model,

a.

a cartel of leading firms determines price and industry output.

b.

the industry in consortium with the government determines price and output.

c.

one firm is the price leader and all other firms follow.

d.

the firms abandon a profit-maximizing goal.

e.

firms do not operate where MR = MC.

121. Suppose that R. J. Reynolds raises the price of cigarettes by 10 percent. Although they have no

requirement or agreement to do so, the other cigarette firms decide to raise their prices accordingly.

This situation is best described as:

a.

price leadership.

c.

monopolistic competition.

b.

a cartel.

d.

a market with kinked demand.

122. An organization of sellers designed to coordinate their supply decisions to maximize joint profits is

called a:

a.

consumer cooperative.

c.

regulatory agency.

b.

marketing association.

d.

cartel.

123. The two tendencies of a firm in a cartel are the incentive to:

a.

cheat to maximize joint profits and the incentive to raise prices.

b.

cheat and avoid collusion and the incentive to raise price to maximize the firm’s share of

profits.

c.

increase output in order to minimize per-unit cost and the incentive to reduce price in

order to maximize joint profit.

d.

cooperate to maximize joint profits and to cheat on the agreement in order to increase the

firm’s share of the profit.

124. Which of the following best describes a cartel?

a.

As a monopolist, a group of monopolistically competitive firms that jointly reduce output

and raise the price.

b.

As a monopolist, a group of cooperating oligopolists that jointly reduce output and raise

the price.

c.

A monopolist that reduces output and raises price.

d.

A group of identical non-cooperative oligopolists that are able to reproduce a monopoly

equilibrium through price rivalry.

125. Which of the following explains how a cartel with 100 percent control might raise price to monopoly-

like levels?

a.

By setting a group output level equal to a profit-maximizing monopolist, and then

assigning binding quota shares to cartel members.

b.

By setting an official price that members can secretly undercut.

c.

By forbidding price competition, but allowing non-cooperative rivalry in output levels.

d.

None of the above.

126. Cartel agreements are difficult to maintain because individual members:

a.

can gain by raising their price above the price that is best for the cartel.

b.

are often unable to police the price and output policies of other members.

c.

can gain by secretly raising their price above the price that is best for the cartel.

d.

can enforce price arrangements vigorously in court.

127. Which of the following market structures describes an industry in which a group of firms formally

agree to control prices and output of a product?

a.

Perfect competition.

b.

Monopoly.

c.

Oligopoly.

d.

Cartel.

e.

Monopolistic competition.

128. If OPEC is an effective cartel,

a.

price changes are dictated by changes in demand.

b.

output changes are dictated by changes in demand.

c.

members agree on output quotas.

d.

all of these.

129. In order to make oil profits as large as possible, OPEC meets to set oil production quotas for its

members. OPEC is best classified as a:

a.

monopoly.

c.

kinked demand industry.

b.

cartel.

d.

price-leadership industry.

130. Which of the following is evidence of an ineffective cartel?

a.

Output changes are dictated by changes in demand.

b.

Price changes are dictated by changes in demand.

c.

Members do not agree on output quotas.

d.

All of these.

131. A cartel:

a.

is a group of firms formally agreeing to control the price and the output of a product.

b.

has as its primary goal to reap monopoly profits by replacing competition with

cooperation.

c.

is illegal in the United States, but not in other nations.

d.

all of these.

132. Suppose an oil cartel has an agreement to restrict members’ production in order to maintain a price of

$30 per barrel. A single cartel member may want to cheat and exceed its quota so that it can:

a.

reduce its costs.

c.

make demand more inelastic.

b.

charge higher prices.

d.

earn a bigger profit.

133. A cartel is:

a.

a joint venture of two companies.

b.

a joining of firms for the purpose of fixing prices and controlling output.

c.

a breaking up of a company into two or more parts.

d.

the joining of industry with government to solve a specified problem.

e.

the joining of two firms with unrelated products.

134. The purpose of a cartel is to:

a.

promote product innovation.

b.

increase market competition.

c.

act like a monopoly.

d.

diversify operations.

e.

decrease market concentration.

135. Cartel members have an incentive to cheat on the cartel because:

a.

the cartel does not maximize profits.

b.

the cartel price is the competitive price.

c.

each member’s output quota is too high.

d.

each member’s MR is not equal to the cartel’s MC.

e.

the industry profit would be higher under competitive conditions.

136. A group of firms that collude to limit competition is called a(n):

a.

conglomerate.

b.

oligopoly.

c.

cartel.

d.

kinked demand.

e.

market concentration.

137. A cartel maximizes industry profit by:

a.

eliminating quotas.

b.

producing at the kink in its demand curve.

c.

producing where MR = MC.

d.

giving secret price concessions.

e.

producing more output than a monopoly would.

138. Cartel pricing refers to the output and price choice of a cartel. This choice most closely resembles that

of a:

a.

b or d

b.

godfather oligopoly.

c.

duopoly.

d.

monopoly.

e.

more competitive industry.

139. Game theory is an especially useful model for analysis in the following types of markets:

a.

perfect competition.

c.

oligopoly.

b.

monopolistic competition.

d.

monopoly.

140. Game theory is a model for describing oligopoly price decisions among firms that are:

a.

interdependent.

c.

regulated

b.

independent.

d.

merging

141. A(n) ____ can be used to demonstrate why a competitive oligopoly tends to result in a low-price

strategy that does not maximize mutual profits.

a.

interdependence index

c.

herfindahl index

b.

gini coefficient

d.

payoff matrix

142. Which of the following is a game theory strategy for oligopolists to avoid a low-price outcome?

a.

Tit-for-tat

c.

Last in-first out

b.

Win-win

d.

Second best

143. Which of the following is a game theory strategy for oligopolists to avoid a low-price outcome?

a.

Tit-for-tat

c.

Cartel

b.

Price leadership

d.

All of these

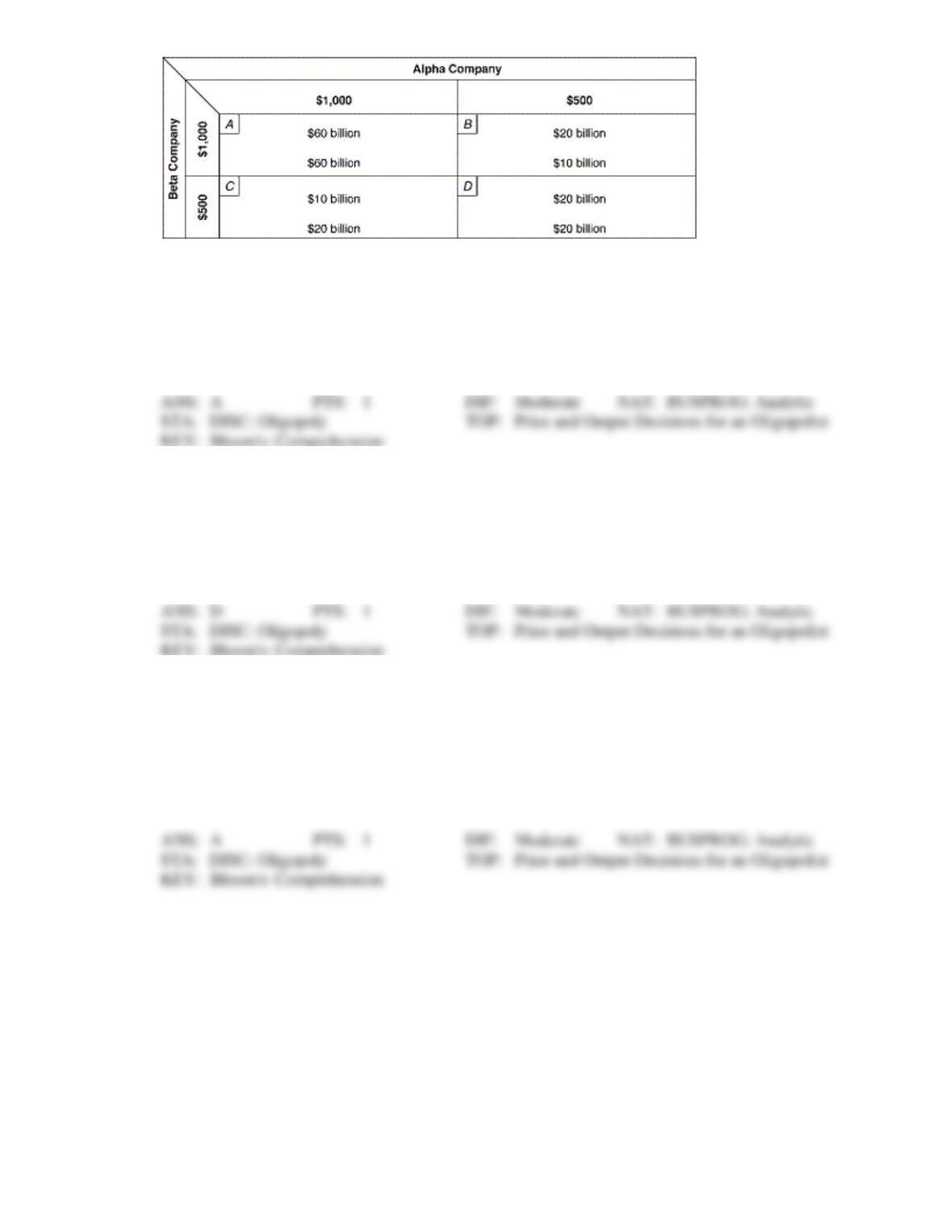

144. Assume costs are identical for the two firms in Exhibit 10-5. If both firms were allowed to form a

cartel and agree on their prices, equilibrium would be established by:

a.

Beta Co. charging $1,000 and Alpha Co. charging $1,000.

b.

Beta Co. charging $1,000 and Alpha Co. charging $500.

c.

Beta Co. charging $500 and Alpha Co. charging $500.

d.

Beta Co. charging $500 and Alpha Co. charging $1,000.

145. Suppose costs are identical for the two firms in Exhibit 10-5. If both firms assume the other will

compete and charge a lower price, equilibrium will be established by:

a.

Beta Co. charging $1,000 and Alpha Co. charging $1,000.

b.

Beta Co. charging $1,000 and Alpha Co. charging $500.

c.

Beta Co. charging $500 and Alpha Co. charging $500.

d.

Beta Co. charging $500 and Alpha Co. charging $1,000.

146. Suppose costs are identical for the two firms in Exhibit 10-5. Each firm assumes without formal

agreement that if it sets the high price its rival will not charge a lower price. Under these “tit-for-tat”

conditions, equilibrium will be established by:

a.

Beta Co. charging $1,000 and Alpha Co. charging $1,000.

b.

Beta Co. charging $1,000 and Alpha Co. charging $500.

c.

Beta Co. charging $500 and Alpha Co. charging $500.

d.

Beta Co. charging $500 and Alpha Co. charging $1,000.

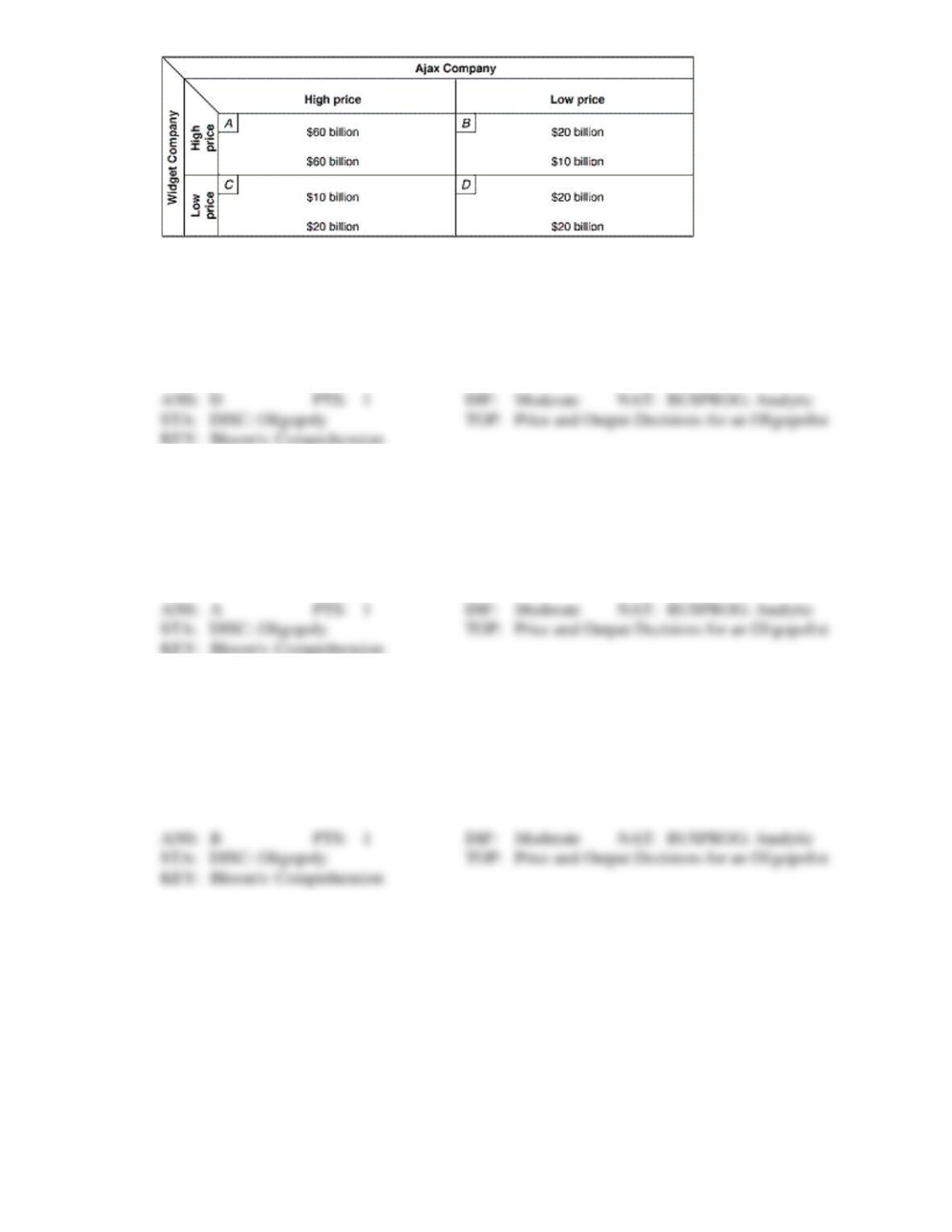

Exhibit 10-6 Two-Firm Payoff Matrix

147. Assume costs are identical for the two firms in Exhibit 10-6. If both firms were allowed to form a

cartel and agree on their prices, equilibrium would be established by:

a.

Widget Co. charging the low price and Ajax Co. charging the high price.

b.

Widget Co. charging the high price and Ajax Co. charging the low price.

c.

Widget Co. charging the low price and Ajax Co. charging the low price.

d.

Widget Co. charging the high price and Ajax Co. charging the high price.

148. Suppose costs are identical for the two firms in Exhibit 10-6. If both firms assume the other will

compete and charge a lower price, equilibrium will be established by:

a.

Widget Co. charging the low price and Ajax Co. charging the low price.

b.

Widget Co. charging the high price and Ajax Co. charging the low price.

c.

Widget Co. charging the low price and Ajax Co. charging the high price.

d.

Widget Co. charging the high price and Ajax Co. charging the high price.

149. Suppose costs are identical for the two firms in Exhibit 10-6. Each firm assumes without formal

agreement that if it sets the high price its rival will not charge a lower price. Under these “tit-for-tat”

conditions, equilibrium will be established by:

a.

Widget Co. charging the high price and Ajax Co. charging the low price.

b.

Widget Co. charging the high price and Ajax Co. charging the high price.

c.

Widget Co. charging the low price and Ajax Co. charging the low price.

d.

Widget Co. charging the low price and Ajax Co. charging the high price.

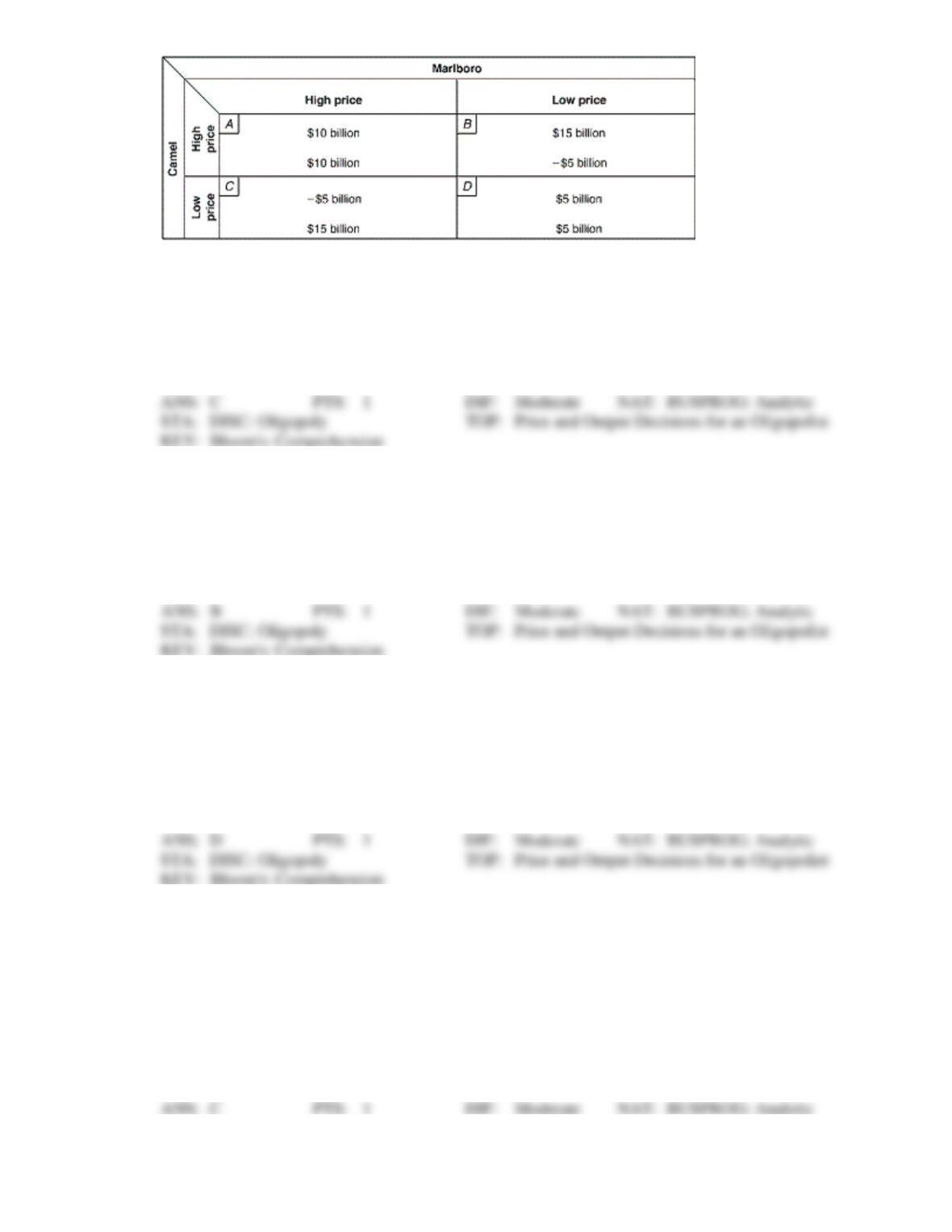

Exhibit 10-7 Two-Firm Payoff Matrix

150. Assume costs are identical for the two firms in Exhibit 10-7. If both firms were allowed to form a

cartel and agree on their prices, equilibrium would be established by:

a.

Camel charging the low price and Marlboro charging the high price.

b.

Camel charging the high price and Marlboro charging the low price.

c.

Camel charging the high price and Marlboro charging the high price.

d.

Camel charging the low price and Marlboro charging the low price.

151. Suppose costs are identical for the two firms in Exhibit 10-7. If both firms assume the other will

compete and charge a lower price, equilibrium will be established by:

a.

Camel charging the high price and Marlboro charging the high price.

b.

Camel charging the low price and Marlboro charging the low price.

c.

Camel charging the low price and Marlboro charging the high price.

d.

Camel charging the high price and Marlboro charging the low price.

152. Suppose costs are identical for the two firms in Exhibit 10-7. Each firm assumes without formal

agreement that if it sets the high price its rival will not charge a lower price. Under these “tit-for-tat”

conditions, equilibrium will be established by:

a.

Camel charging the high price and Marlboro charging the high price.

b.

Camel charging the high price and Marlboro charging the low price.

c.

Camel charging the low price and Marlboro charging the low price.

d.

Camel charging the low price and Marlboro charging the high price.

153. Which of the following is a distinction between perfectly competitive and monopolistic competition?

a.

Perfectly competitive firms must compete with rival sellers; monopolistically competitive

firms do not confront rival sellers.

b.

Monopolistically competitive firms can raise their price without losing sales; perfectly

competitive firms must lower their price in order to sell more of their product.

c.

Perfectly competitive firms confront a perfectly elastic demand curve; monopolistically

competitive firms face a downward-sloping demand curve.

d.

Perfectly competitive firms may make either economic profits or losses in the short run,

but monopolistically competitive firms always earn an economic profit.

154. Some economists argue that monopolistically competitive markets are inefficient because:

a.

the firms earn economic profits in the long run.

b.

the firms’ marginal costs and marginal revenues are not always equal.

c.

firms do not produce the output rate that would minimize their average total cost.

d.

barriers to entry are high.

155. Compared to the perfectly competitive outcome, monopolistically competitive markets will result in:

a.

a wider variety of products and higher prices.

b.

less product variety and higher prices.

c.

a wider variety of products and lower prices.

d.

less product variety and lower prices.

156. In long-run equilibrium, output is expanded to the minimum long-run average total cost by:

a.

perfectly competitive firms but not by monopolistically competitive firms.

b.

monopolistically competitive firms but not by perfectly competitive firms.

c.

both monopolistically competitive firms and perfectly competitive firms.

d.

neither perfectly competitive firms nor monopolistically competitive firms.

157. In the long run, a monopolistically competitive firm will set price:

a.

at the intersection of the marginal cost and demand curves.

b.

at the intersection of the average total cost and demand curves.

c.

higher than the competitive level, but lower than the monopoly price.

d.

higher than the marginal cost, but lower than average total cost.

158. How will the price and output of a monopolist compare with perfect competition?

a.

The output of the monopolist will be too large and the price too high.

b.

The output of the monopolist will be too large and the price too low.

c.

The output of the monopolist will be too small and the price too high.

d.

The output of the monopolist will be too small and the price too low.

159. Which of the following is true for perfect competition, monopolistic competition, and monopoly?

a.

The product of all firms is homogeneous.

b.

Firms will earn zero economic profits in the long run.

c.

Short-run profits are maximized when marginal cost equals marginal revenue.

d.

All of these.

160. Under which one of the following market structures are sellers most likely to consider the reaction of

rival sellers when they set the price of their product?

a.

Perfectly competition.

c.

Monopolistic competition.

b.

Monopoly.

d.

Oligopoly.

TRUE/FALSE

1. The monopolistic competition market structure is characterized by a few large firms which account for

a large percentage of industry sales.

2. A monopolistically competitive firm, like a perfectly competitive firm, is a price taker.

3. In a monopolistically competitive market like retail trade, firms can easily enter and exit the market.

4. In the short run, the monopolistic competitive firm will charge a price equal to marginal cost.

5. In a monopolistic competitive industry, short-run economic profit encourages entry of new firms until

there are no economic profits in the long-run.

6. In the long run, marginal cost must equal marginal revenue for a monopolistic competitive firm, but

not at the minimum point of the long-run average cost curve.

7. A monopolistic competitive firm in the long run sets price equal to the minimum point on the long-run

average cost curve.

8. Examples of nonprice competition include advertising and product differentiation.

9. An oligopoly market structure is characterized by firms closely watching their rivals’ pricing policies.

10. The theory of oligopolistic interdependence means that the outcome is uncertain because price and

output decisions depend on responses of rivals.

11. In an oligopoly, the outcome is uncertain because price and output decisions depend on the response of

rivals.

12. Easy entry and exit cause oligopoly profits to be zero in the long run.

13. Oligopolies have few sellers and difficult entry.

14. A kinked demand curve is based on the actions of an oligopolist to follow a price increase but not a

price reduction.

15. An oligopolist operating with a kinked demand curve would expect rivals to match both its price

increases and price decreases.

16. Oligopolies with kinked demand curves change their prices quickly and frequently.

17. A cartel is a formal agreement among firms to control price and output of a product.

18. Cartels are legal in the United States.

19. A cartel is an agreement among firms to divide output of a product among members.

20. A major cartel problem is that member firms cheat by attempting to steal customers from one another.

21. In order from the most to the least competitive market structure is the perfectly competitive,

monopolistically competitive, monopolist and then the oligopolistic market structure.

22. In the short run both the monopolistically competitive firm and the perfectly competitive firm will

charge a price equal to marginal cost.

ESSAY

1. What are the characteristics of monopolistic competition?

2. What are the characteristics of an oligopoly?

3. Compare and contrast the four market models in terms of the profit-maximizing output level for each,

the shut-down rule for each, the probability of long-run economic profits being earned, and their social

desirability.