Cash 3,000

47. Suffolk Corporation issued $100,000 of 20-year, 6 percent bonds at 98 on one of its semi-annual

interest dates. The straight-line method of amortization is to be used. After seven years, what is the

carrying value of the bonds?

a.

$98,350

b.

$98,700

c.

$99,300

d.

$99,650

48. Suffolk Corporation issued $100,000 of 20-year, 6 percent bonds at 98 on one of its semi-annual

interest dates. The straight-line method of amortization is to be used. What is the total interest cost of

the bonds?

a.

$120,000

b.

$122,000

c.

$118,000

d.

$117,500

49. Knollwood Corporation issued $278,000 of 30-year, 8 percent bonds at 106 on one of its semi-annual

interest dates. The straight-line method of amortization is to be used. The entry to record the bond

interest expense on the next interest payment date is:

a.

Bond Interest Expense 11,120

Cash 11,120

b.

Bond Interest Expense 11,398

Cash 11,398

c.

Bond Interest Expense 10,520

Cash 10,520

d.

Bond Interest Expense 10,842

Unamortized Bond Premium 278

Cash 11,120

50. Knollwood Corporation issued $300,000 of 30-year, 8 percent bonds at 106 on one of its semi-annual

interest dates. The straight-line method of amortization is to be used. What is the total interest cost of

the bonds?

a.

$719,500

b.

$702,000

c.

$720,000

d.

$738,000

51. Knollwood Corporation issued $281,000 of 30-year, 8 percent bonds at 106 on one of its semi-annual

interest dates. The straight-line method of amortization is to be used. After 11 years, what is the

carrying value of the bonds?

a.

$289,430

b.

$289,992

c.

$288,025

d.

$291,678

52. The effective interest method of amortization of bond premiums and discounts is superior to the

straight-line method because it results in a(n)

a.

more variable interest rate.

b.

uniform rate of interest.

c.

interest rate that increases or decreases slightly over time.

d.

interest rate that is close to the market interest rate.

53. A company issued $300,000 of 20-year, 8 percent bonds at 96. If interest is paid semi-annually, the

entry to record the amount of bond interest expense (assuming the straight-line method of

amortization) on any interest date is

a.

Bond Interest Expense 12,000

Cash 12,000

b.

Bond Interest Expense 24,300

Unamortized Bond Discount 300

Cash 24000

c.

Bond Interest Expense 23,700

Cash 23,700

d.

Bond Interest Expense 12,300

Unamortized Bond Discount 300

Cash 12000

54. A ten-year bond has a face value of $10,000, a face interest rate of 11 percent, an unamortized bond

premium of $400, and an effective interest rate of 10 percent. The bonds were issued on one of the

semi-annual interest payment dates. The entry to record the bond interest expense on the first

semi-annual interest payment date is: (assuming the effective interest method of amortization),

a.

Bond Interest Expense 520

Unamortized Bond Premium 30

Cash 550

b.

Bond Interest Expense 520

Cash 520

c.

Bond Interest Expense 550

Cash 550

d.

Unamortized Bond Premium 520

Cash 520

55. In 2007, Horwitz Corporation issued ten-year, 9 percent bonds when the market interest rate was 11

percent. Interest is payable annually. During 2010, the market rate of interest for similar bonds was 12

percent. Using the effective interest method of amortization, what interest rate will be used to calculate

interest expense for 2010?

a.

12 percent

b.

9 percent

c.

6 percent

d.

11 percent

56. Lassen Corporation issued ten-year term bonds on January 1, 2010, with a face value of $800,000. The

face interest rate is 6 percent and interest is payable semi-annually on June 30 and December 31. The

bonds were issued for $690,960 to yield an effective annual rate of 8 percent. The effective interest

method of amortization is to be used. The entry to record the bond interest expense on the first interest

payment date is: (Round answer to the nearest dollar.)

a.

Bond Interest Expense 24,000

Cash 24,000

b.

Bond Interest Expense 27,638

Unamortized Bond Discount 3,638

Cash 24,000

c.

Bond Interest Expense 27,638

Cash 27,638

d.

Bond Interest Expense 27,638

Unamortized Bond Discount 27,638

57. Lassen Corporation issued ten-year term bonds on January 1, 2010, with a face value of $800,000. The

face interest rate is 8 percent and interest is payable semi-annually on June 30 and December 31. The

bonds were issued for $690,960 to yield an effective annual rate of 10 percent. The effective interest

method of amortization is to be used. The entry on June 30, 2010, to record the payment of interest and

amortization of discount will be:

a.

Bond Interest Expense 32,000

Cash 32,000

b.

Bond Interest Expense 34,548

Unamortized Bond Discount 2,548

Cash 32,000

c.

Bond Interest Expense 34,548

Cash 34,548

d.

Bond Interest Expense 32,000

Unamortized Bond Discount 32,000

58. Lassen Corporation issued ten-year term bonds on January 1, 2010, with a face value of $800,000. The

face interest rate is 6 percent and interest is payable semiannually on June 30 and December 31. The

bonds were issued for $690,960 to yield an effective annual rate of 8 percent. The effective interest

method of amortization is to be used. How much bond interest expense (rounded to the nearest dollar)

should be reported on the income statement for the year ended December 31, 2010?

a.

$48,000

b.

$55,422

c.

$55,131

d.

$55,276

59. Lassen Corporation issued ten-year term bonds on January 1, 2010, with a face value of $800,000. The

face interest rate is 6 percent and interest is payable semi-annually on June 30 and December 31. The

bonds were issued for $690,960 to yield an effective annual rate of 8 percent. The effective interest

method of amortization is to be used. The entry to be recorded on December 31, 2010, for the payment

of interest (rounded to the nearest dollar) and the amortization of discount is:

a.

Bond Interest Expense 3,638

Unamortized Bond Discount 3,638

b.

Bond Interest Expense 27,784

Unamortized Bond Discount 3,784

Cash 24,000

c.

Bond Interest Expense 27,784

Cash 27,784

d.

Bond Interest Expense 24,000

Unamortized Bond Discount 24,000

60. Lassen Corporation issued ten-year term bonds on January 1, 2010, with a face value of $800,000. The

face interest rate is 6 percent and interest is payable semi-annually on June 30 and December 31. The

bonds were issued for $690,960 to yield an effective annual rate of 8 percent. The effective interest

method of amortization is to be used. The carrying value of the bonds payable on the December 31,

2010, balance sheet date should be (rounded to the nearest dollar)

a.

$696,412.

b.

$698,236.

c.

$698,382.

d.

$690,960.

61. Lenz Corporation issued ten-year, 8 percent bonds payable in 2009 at a premium. During 2009, the

company’s accountant failed to amortize any of the bond premium. The omission of the premium

amortization will

a.

cause net income for 2009 to be overstated.

b.

not affect net income reported for 2009.

c.

cause net income for 2009 to be understated.

d.

cause retained earnings at the end of 2009 to be overstated.

62. Penmark Corporation issued 15-year term bonds at a discount in 2010. Interest is payable

semi-annually. Which of the following statements is true, assuming that the effective interest method

of amortization is used for the bond discount?

a.

Interest expense decreases each six-month interest period.

b.

Interest expense as a percentage of the bond’s book value changes from period to period.

c.

Interest expense increases each six-month interest period.

d.

Interest expense remains constant in amount for each interest period.

63. When the effective interest method of amortization is used for a bond premium, the amount of interest

expense for an interest period is calculated by multiplying the

a.

carrying value of the bonds at the beginning of the period by the face interest rate.

b.

face value of the bonds at the beginning of the period by the effective interest rate.

c.

carrying value of the bonds at the beginning of the period by the effective interest rate.

d.

face value of the bonds at the beginning of the period by the face interest rate.

64. The amortization of a bond premium will result in reporting an amount of interest expense for an

interest period that

a.

exceeds the amount of cash to be paid for interest for the period.

b.

is less than the amount of cash to be paid for interest for the period.

c.

has no predictable relationship with the amount of cash to be paid for interest for the

period.

d.

equals the amount of cash to be paid for interest for the period.

65. When the straight-line method of amortization is used for a bond discount, the amount of interest

expense for an interest period is calculated by

a.

adding the amount of discount amortization for the period to the amount of cash paid for

interest during the period.

b.

deducting the amount of discount amortization for the period from the amount of cash paid

for interest during the period.

c.

multiplying the carrying value of the bonds by the effective interest rate.

d.

multiplying the face value of the bonds by the face interest rate.

66. If bonds payable were issued initially at a discount, the carrying value of the bonds at a balance sheet

date will be calculated by

a.

deducting the amount of discount amortized between the issuance date and the balance

sheet date from the face value.

b.

deducting the balance of unamortized bond discount from the face value.

c.

adding the balance of unamortized bond discount to the face value.

d.

adding the amount of discount amortized between the issuance date and the balance sheet

date to the face value.

67. When bonds have been issued at a premium, the periodic amortization of the premium will

a.

increase the carrying value of the bonds.

b.

have no effect on the carrying value of the bonds.

c.

decrease the carrying value of the bonds.

d.

cause the carrying value always to equal the face value of the bonds.

68. A company has $817,000 in bonds payable with an unamortized premium of $20,000. If one-fourth of

the bonds are converted to common stock, the entry that would record the conversion is:

a.

Bonds Payable 204,250

Common Stock 204,250

b.

Bonds Payable 224,250

Common Stock 224,250

c.

Common Stock 199,250

Bonds Payable 199,250

d.

Bonds Payable 204,250

Unamortized Bond Premium 5,000

Common Stock 209,250

69. A $300,000 bond issue with a carrying value of $311,000 is called at 103 and retired. The entry to

record the retirement of bonds would be:

a.

Bonds Payable 309,000

Cash 309,000

b.

Bonds Payable 311,000

Cash 311,000

c.

Cash 300,000

Bonds Payable 300,000

d.

Bonds Payable 300,000

Unamortized Bond Premium 11,000

Cash 309,000

Gain on Retirement of Bonds 2,000

70. A $50,000 bond issue with a carrying value of $47,000 is called at 102 and retired. The entry to record

the retirement of bonds would be:

a.

Bonds Payable 50,000

Loss on Retirement of Bonds 4,000

Unamortized Bond Discount 3,000

Cash 51,000

b.

Bonds Payable 47,000

Cash 47,000

c.

Bonds Payable 50,000

Gain on Retirement of Bonds 3,000

Cash 47,000

d.

Bonds Payable 50,000

Loss on Retirement of Bonds 1,000

Cash 51,000

71. When bonds are converted to common stock, which of the following could be part of the entry?

a.

Credit to Gain on Conversion of Bonds

b.

Credit to Unamortized Bond Premium

c.

Credit to Unamortized Bond Discount

d.

Debit to Common Stock

72. A company has $900,000 in bonds payable with an unamortized discount of $21,000. If two-thirds of

the bonds are converted to common stock, the carrying value of the bonds payable will decrease by

a.

$293,000.

b.

$586,000.

c.

$614,000.

d.

$628,000.

73. A $200,000 bond issue with a carrying value of $194,000 is called at 101 and retired. The entry to

record the retirement of bonds would be:

a.

Bonds Payable 200,000

Gain on Retirement of Bonds 6,000

Cash 194,000

b.

Bonds Payable 200,000

Cash 200,000

c.

Bonds Payable 200,000

Loss on Retirement of Bonds 8,000

Unamortized Bond Discount 6,000

Cash 202,000

d.

Bonds Payable 194,000

Loss on Retirement of Bonds 8,000

Cash 202,000

74. A $100,000 bond issue with a carrying value of $103,000 is called at 101 and retired. The entry to

record the retirement of bonds would be:

a.

Bonds Payable 101,000

Loss on Retirement of Bonds 2,000

Cash 103,000

b.

Bonds Payable 100,000

Unamortized Bond Premium 3,000

Cash 101,000

Gain on Retirement of Bonds 2,000

c.

Bonds Payable 100,000

Loss on Retirement of Bonds 3,000

Cash 103,000

d.

Bonds Payable 103,000

Cash 103,000

75. A bond issue of $50,000 with a carrying value of $49,000 is converted into $10 par value common

stock at the rate of fifty shares for each $1,000 bond. The entry to record the conversion of bonds

would be:

a.

Bonds Payable 50,000

Loss on Retirement of Bonds 1,000

Unamortized Bond Discount 1,000

Common Stock 50,000

b.

Bonds Payable 50,000

Common Stock 25,000

Additional Paid-In Capital 25,000

c.

Bonds Payable 50,000

Common Stock 25,000

Additional Paid-In Capital 24,000

Unamortized Bond Discount 1,000

d.

Bonds Payable 49,000

Unamortized Bond Discount 1,000

Common Stock 25,000

Additional Paid-In Capital 25,000

76. Hooper Corporation has bonds outstanding with a face value of $100,000 and a carrying value of

$103,000 on December 31, 2010. If the company calls in and retires these bonds on December 31,

2010, for $105,000, the entry to record the retirement would be:

a.

Bonds Payable 103,000

Cash 103,000

b.

Bonds Payable 105,000

Cash 105,000

c.

Bonds Payable 100,000

Loss on Retirement of Bonds 3,000

Cash 103,000

d.

Bonds Payable 100,000

Loss on Retirement of Bonds 2,000

Unamortized Bond Premium 3,000

Cash 105,000

77. Bonds that contain a provision that allows the issuing corporation to buy back the bonds prior to the

maturity date are called

a.

secured bonds.

b.

callable bonds.

c.

convertible bonds.

d.

debenture bonds.

78. When bonds payable are converted into stock, the carrying value of the bonds should be

a.

credited to Retained Earnings.

b.

credited to contributed capital accounts.

c.

debited to Retained Earnings.

d.

debited to Loss on Conversion of Bonds.

79. Bonds that contain a provision that allows the holders to exchange the bonds for other securities of the

issuing corporation are called

a.

debenture bonds.

b.

secured bonds.

c.

callable bonds.

d.

convertible bonds.

80. When bonds are sold at face value between interest dates, the result is a debit to the Cash account that

a.

equals face value.

b.

depends on the circumstances.

c.

is less than face value.

d.

exceeds face value.

81. Peng Corporation has been authorized to issue bonds with interest payment dates of March 1 and

September 1. If the bonds are sold at face amount on April 1, the amount of cash to be received by the

issuer is equal to the face amount of the bonds

a.

minus the interest accrued from March 1 to April 1.

b.

plus the interest accrued from April 1 to September 1.

c.

minus the interest accrued from April 1 to September 1.

d.

plus the interest accrued from March 1 to April 1.

82. If $110,000 of 12 percent bonds are issued (at face value) one month after the last semi-annual interest

date, the entry made to record the issue is:

a.

Cash 111,100

Bonds Payable 110,000

Bond Interest Expense 1,100

b.

Cash 111,100

Bonds Payable 111,100

c.

Cash 105,600

Bond Interest Expense 5,500

Bonds Payable 111,100

d.

Cash 115,500

Bonds Payable 110,000

Bond Interest Expense 5,500

83. A corporation issues bonds that pay interest each February 1 and August 1. The corporation’s

December 31 adjusting entry might include a

a.

debit to Unamortized Bond Premium.

b.

debit to Cash.

c.

debit to Bond Interest Payable.

d.

credit to Bond Interest Income.

84. On March 1, 2010, Darby Corporation sold 82 of its 9 percent, $1,000 bonds for a price of 96 plus

accrued interest. The accrued interest amounted to $1,000. If a balance sheet were to be prepared at the

end of the day, March 1, 2010, the carrying value reported for the bonds payable would be

a.

$82,000.

b.

$78,720.

c.

$79,540.

d.

$77,900.

85. The amount of cash received on issuance of a 9 percent, $10,000 bond dated February 1 and issued

June 1 at 102 1/2 is

a.

$10,300.

b.

$11,100.

c.

$10,200.

d.

$10,550.

SHORT ANSWER

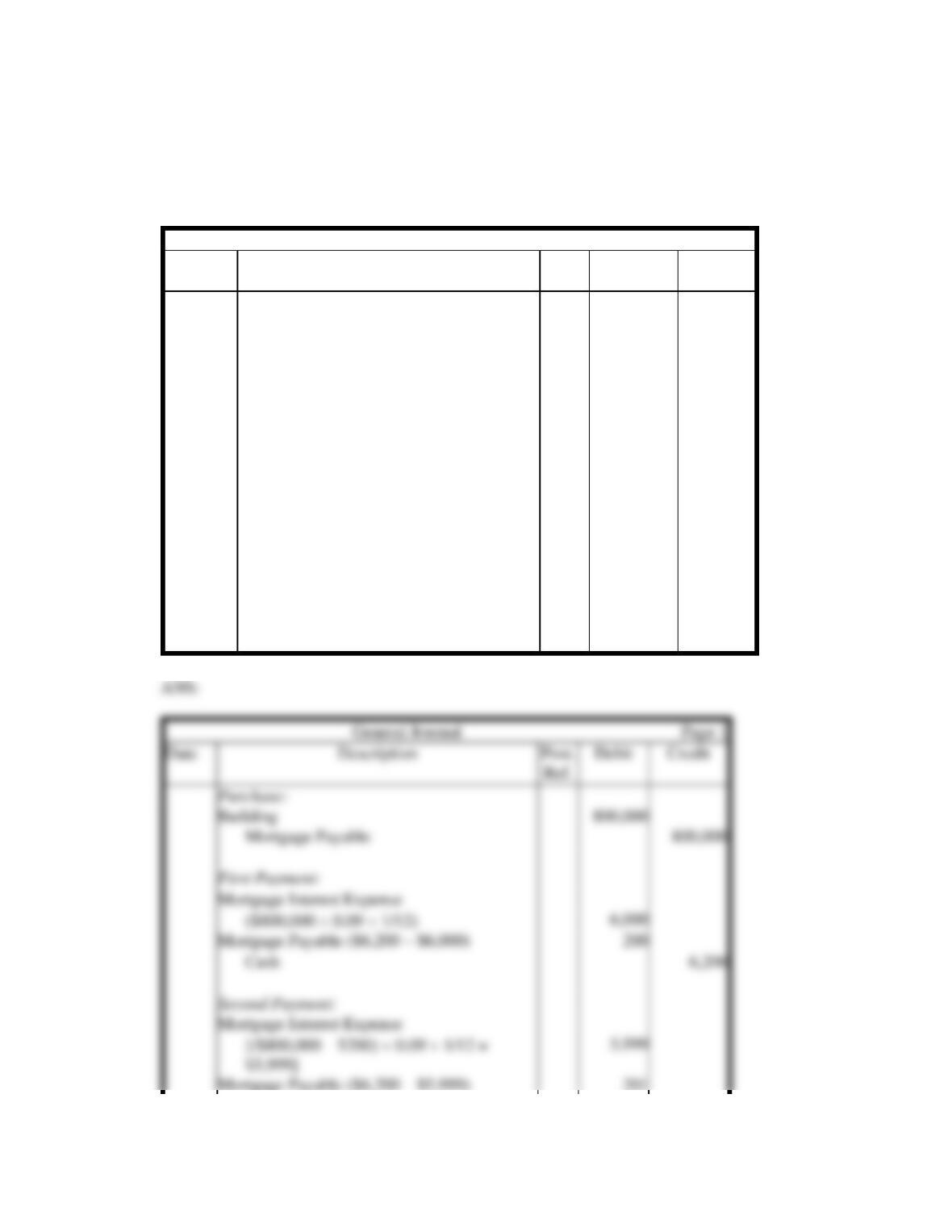

1. Alby Corporation purchased a warehouse by signing a long-term $800,000 mortgage with monthly

payments of $6,200. The mortgage carries an interest rate of 9 percent. Prepare entries in journal form

without explanations to record the purchase and the first two monthly payments. Round answers to the

nearest dollar.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

($800,000 0.09 1/12)

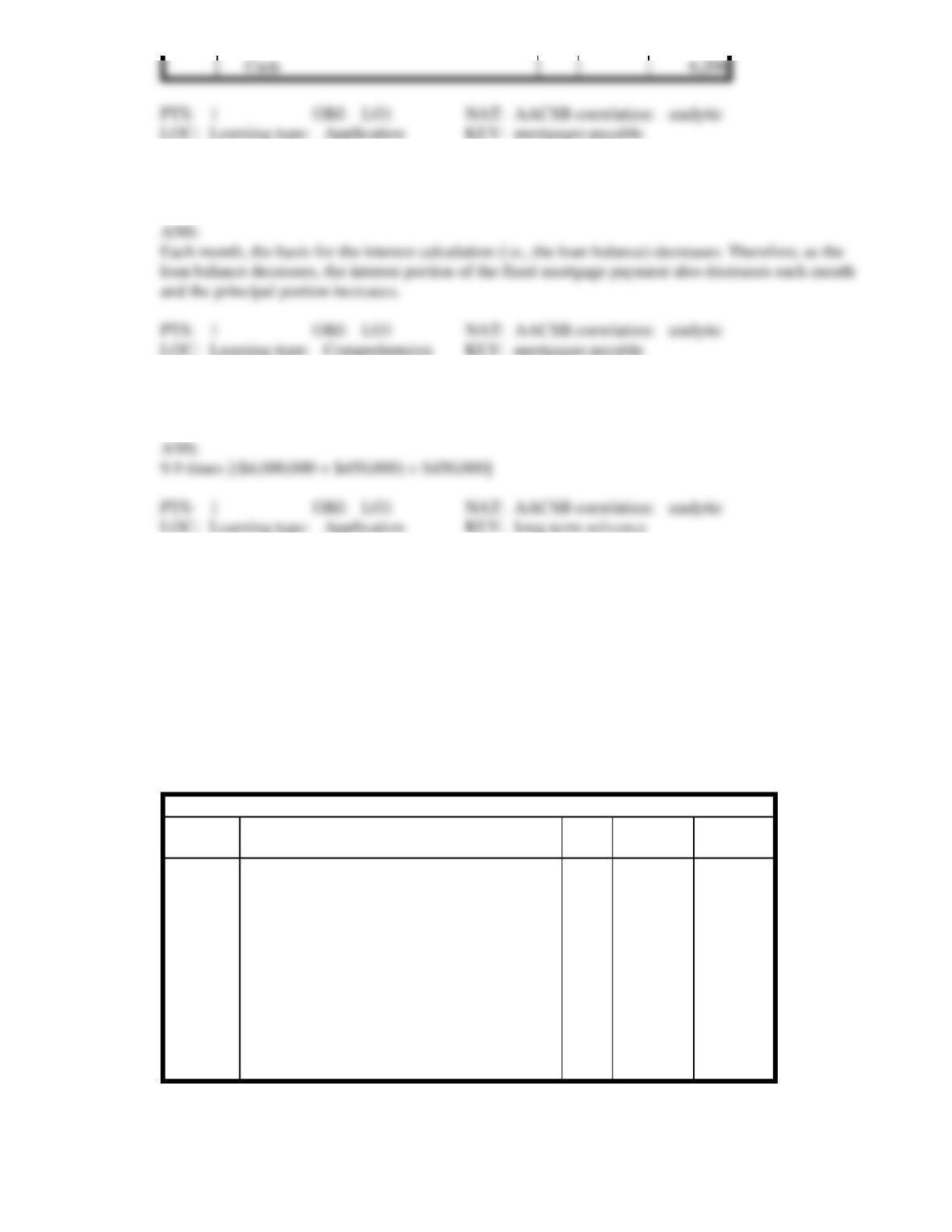

2. When fixed mortgage payments are made, in what way does the interest portion change each month,

and why?

3. Boris Corporation had income before income taxes of $4,000,000 and interest expense of $450,000.

Calculate Boris’s interest coverage ratio, rounded to one decimal place.

4. Dennis Corporation entered into a long-term lease for a piece of equipment. The lease term calls for an

annual payment of $2,000 for six years, which approximates the useful life of the equipment. Assume

a discount factor of 16 percent. (Note: Present value of a single sum factor at six years and 16% is

0.410; present value of an annuity factor at six years and 16% is 3.685.) Round answers to the nearest

dollar.

a. Prepare the entry without explanation to record the leased equipment.

b. Prepare the entry without explanation to record annual depreciation, assuming the straight-line

method and no residual value.

c. Prepare the entry without explanation to record the first annual payment of $2,000, after the

company has had the equipment for one year.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

5. On July 1, 20xx, Halo Corporation issued bonds with a face value of $500,000. The bonds carry a face

interest rate of 10 percent that is payable each July 1 and January 1.

a. Prepare the entry in journal form without explanation for the issuance assuming the bonds are issued

at 97.

b. Prepare the entry in journal form without explanation for the issuance assuming the bonds are issued

at 102.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

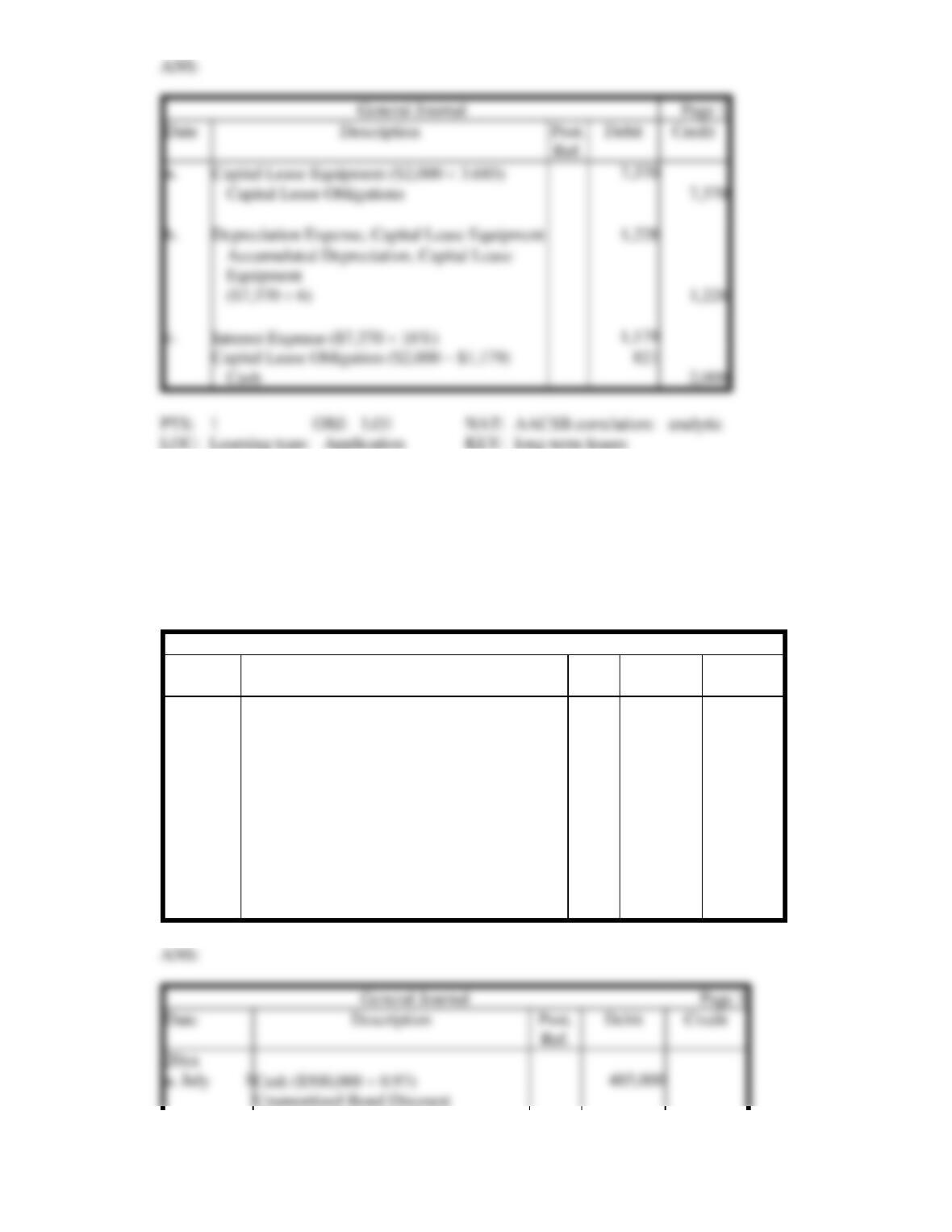

Cash ($500,000 0.97)

Capital Lease Equipment ($2,000 3.685)

6. On July 1, 20xx, Aloha Corporation issued bonds with a face value of $400,000. The bonds carry a

face interest rate of 8 percent that is payable each July 1 and January 1.

a. Prepare the entry in journal form without explanation for the issuance of the bonds assuming the

bonds are issued at 98.

b. Prepare the entry in journal form without explanation for the issuance of the bonds assuming the

bonds are issued at 101.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

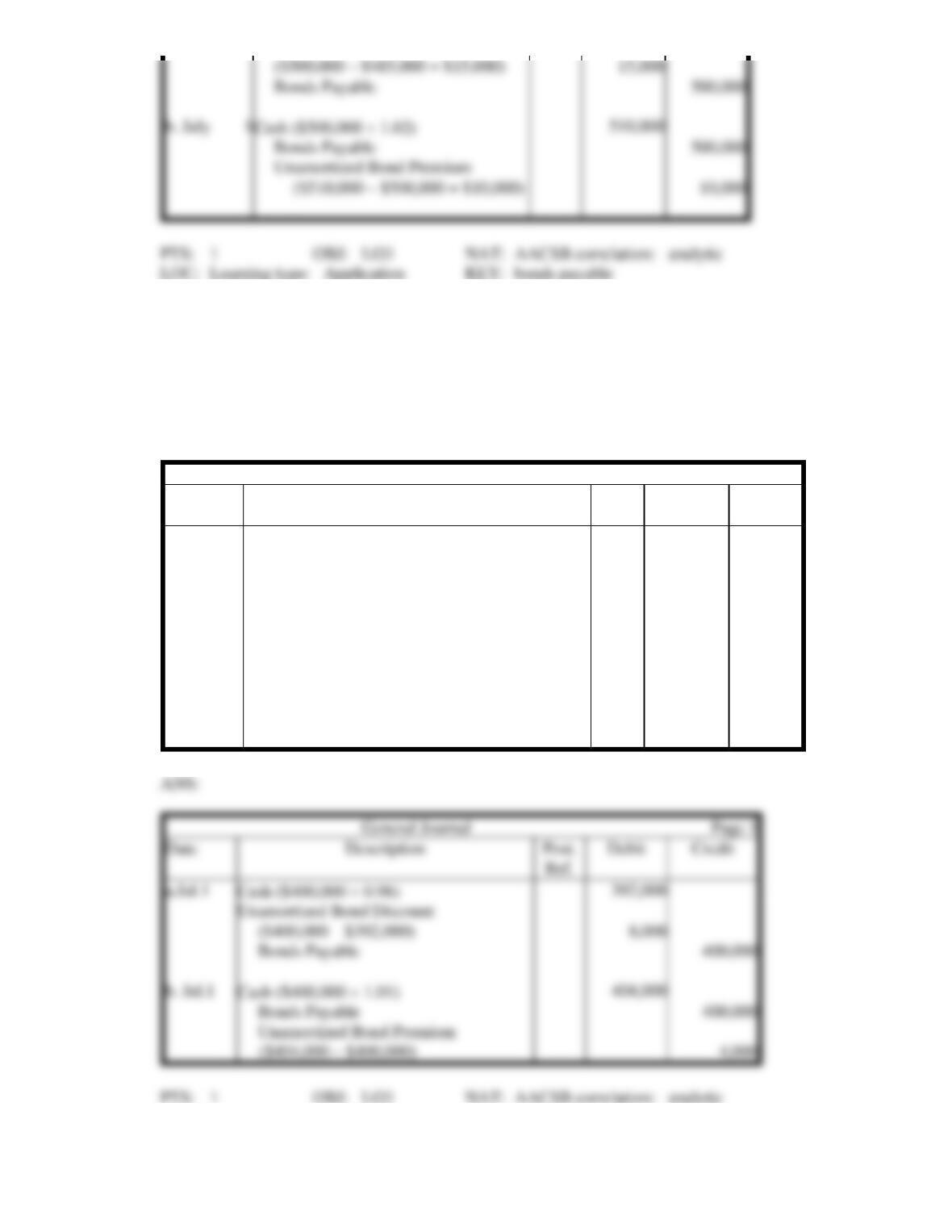

Cash ($400,000 0.98)

($400,000 – $392,000)

Cash ($400,000 1.01)

Unamortized Bond Premium

Cash ($500,000 1.02)

7. When a bond sells at a premium, what is probably true about the market interest rate versus the face

interest rate? Discuss.

8. When a bond sells at a discount, what is probably true about the market interest versus the face interest

rate? Discuss.

9. Flint Corporation issues $1,000,000 of 30-year, 8 percent bonds at 106. Interest is paid semi-annually,

and the effective interest method is used for amortization. Assume that the market interest rate for

similar investments is 7 percent and that the bonds are issued on an interest date.

a. What amount was received for the bonds?

b. How much interest is paid each interest period?

c. How much bond interest expense is recorded on the first interest date (after the issue date)?

d. What is the carrying value of the bonds after the first interest date (after the issue date)?

10. West Valley Corporation issues $800,000 of 20-year, 9 percent bonds at 95. Interest is paid

semi-annually, and the effective interest method is used for amortization. Assume that the market

interest rate for similar investments is 10 percent and that the bonds are issued on an interest date.

a. What amount was received for the bonds?

b. How much interest is paid each interest period?

c. How much bond interest expense is recorded on the first interest date (after the issue date)?

d. What is the carrying value of the bonds after the first interest date (after the issue date)?

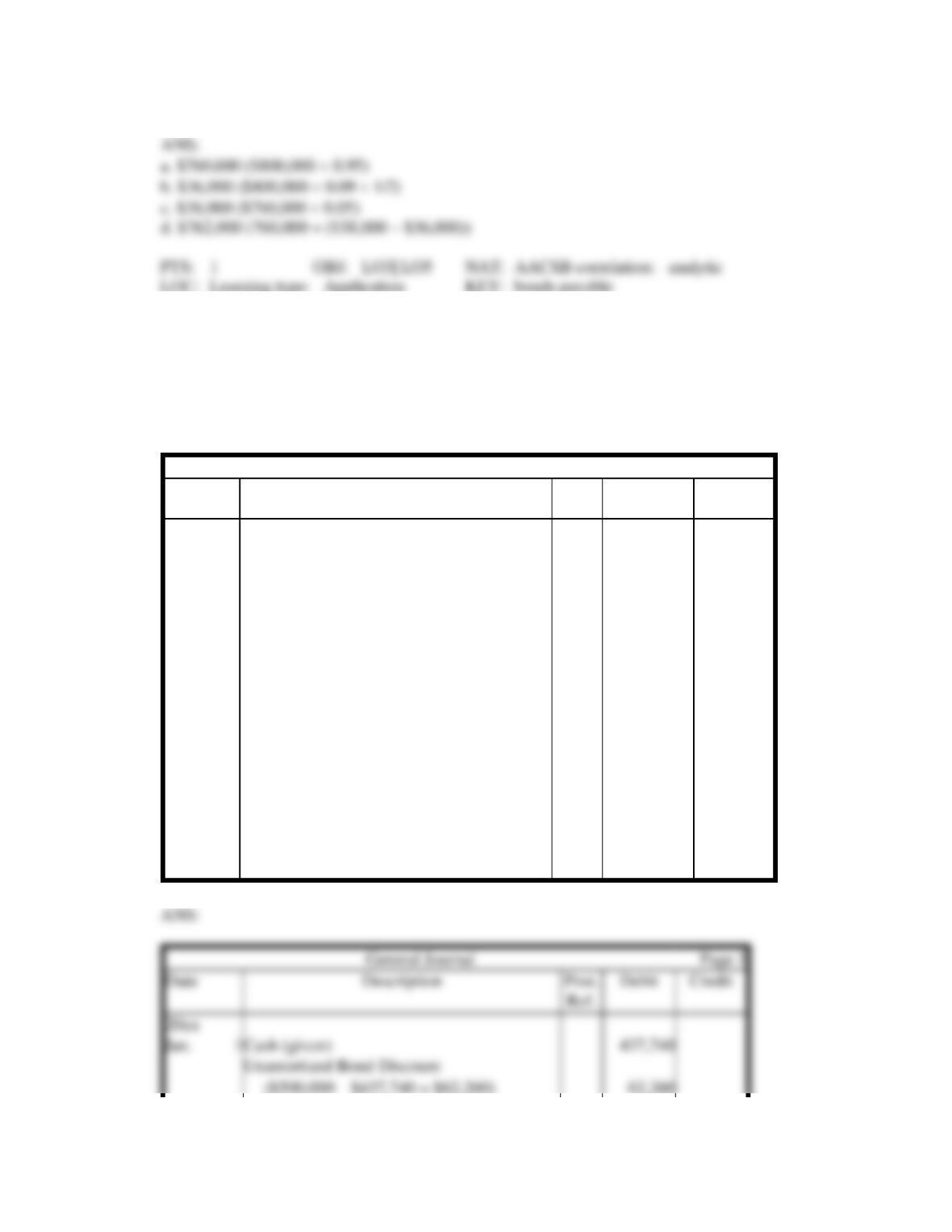

11. On January 1, 20xx, Lurline Corporation issued ten-year, 8 percent bonds with a face value of

$500,000. The semi-annual interest dates are June 30 and December 31. The bonds were issued for

$437,740 to yield an effective annual rate of 10 percent. The accounting year ends on December 31.

Prepare entries in journal form without explanations to record the bond issue on January 1, 20xx, and

the payments of interest and amortization of discount on June 30 and December 31, 20xx. Use the

effective interest method of amortization. Round answers to the nearest dollar.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

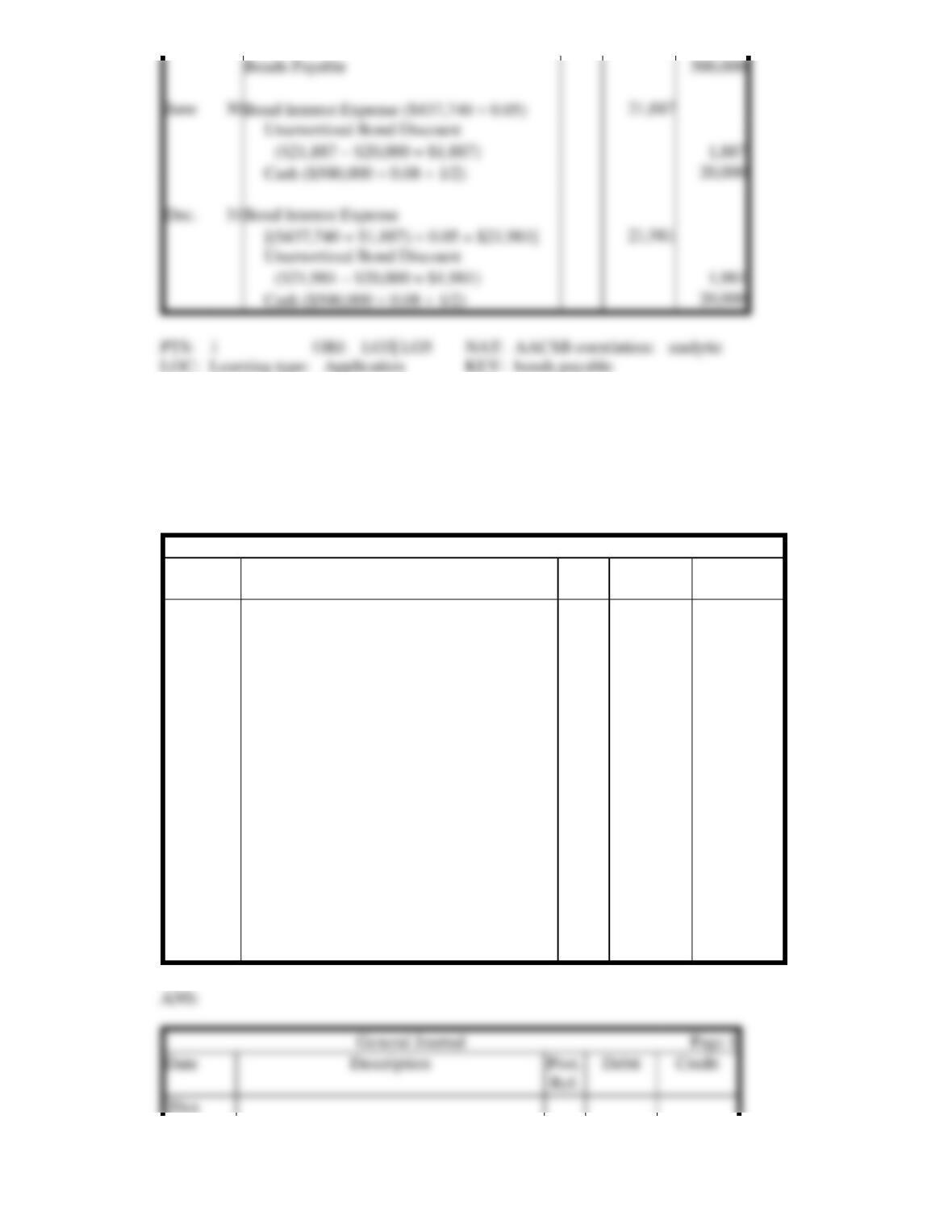

12. On January 2, 20xx, Horst Corporation issued ten-year, 8 percent bonds with a face value of

$1,000,000. The semi-annual interest dates are June 30 and December 31. The bonds were issued for

$875,480 to yield a market interest rate of 10 percent. The accounting year ends on December 31.

Prepare entries in journal form without explanations to record the bond issue on January 2, 20xx, and

the payments of interest and amortization of discount on June 30 and December 31, 20xx. Use the

straight-line method of amortization. Round answers to the nearest dollar.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

Bond Interest Expense ($437,740 0.05)

($21,887 – $20,000 = $1,887)

Bond Interest Expense

[($437,740 + $1,887) 0.05 = $21,981]

($21,981 – $20,000 = $1,981)

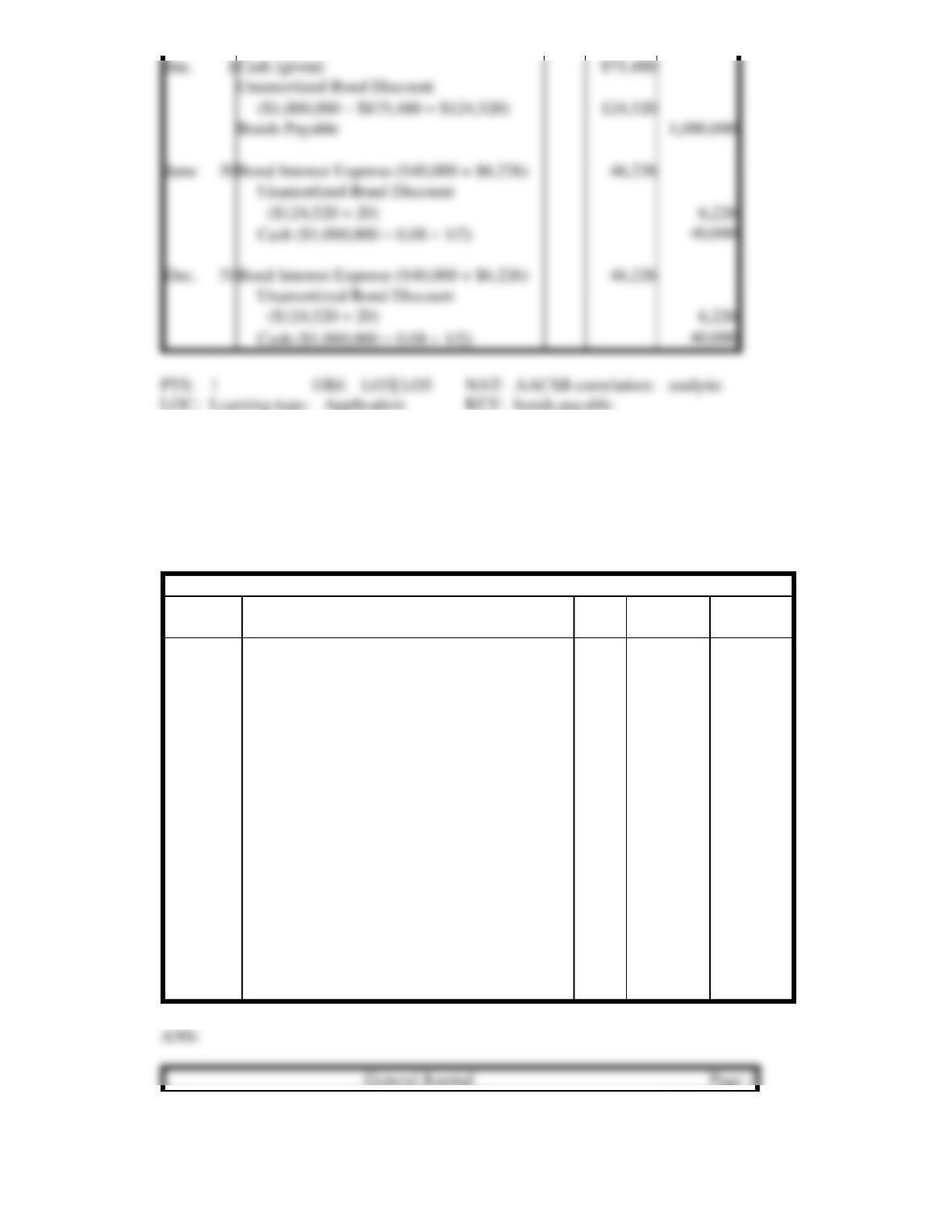

13. On November 1, 2009, Fields Corporation issued $800,000 worth of ten-year, 9 percent bonds. The

semi-annual interest dates are November 1 and May 1. Because the market interest rate of similar

investments was 8.5 percent, the bonds were issued at a price of 103. Ignoring year-end accruals,

prepare entries in journal form without explanations to record the bond issue on November 1, 2009,

and the payments of interest and amortization of premium on May 1 and November 1, 2010. Use the

effective interest method of amortization. Round answers to the nearest dollar.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

Cash ($1,000,000 0.08 1/2)