Chapter 10: Fixed Assets and Intangible Assets

126.

On December 31, Strike Company has decided to discard one of its batting cages. The equipment had an initial

cost of $310,000 and has accumulated depreciation of $260,000. Depreciation has been recorded up to the end of

the year. Which of the following will be included in the entry to record the disposal?

a.

Gain on Disposal of Asset Cr., $50,000

b.

Loss on Disposal of Asset Dr., $260,000

c.

Accumulated Depreciation Dr., $310,000

d.

Equipment Cr., $310,000

127.

On December 31, Strike Company sold one of its batting cages for $50,000. The equipment had an original

cost of $310,000 and has accumulated depreciation of $260,000. Depreciation has been recorded up to the end

of the

year. What is the amount of the gain or loss on this transaction?

a.

no gain or loss

b.

loss of $50,000

c.

gain of $50,000

d.

cannot be determined

128.

On December 31, Strike Company sold one of its batting cages for $20,000. The equipment had an initial cost

of $310,000 and had accumulated depreciation of $260,000. Depreciation has been recorded up to the end of

the

year. What is the amount of the gain or loss on this transaction?

a.

gain of $20,000

b.

loss of $30,000

c.

gain of $20,000

d.

loss of $30,000

Chapter 10: Fixed Assets and Intangible Assets

129.

On December 31, Strike Company sold one of its batting cages for $55,000. The equipment had an initial cost

of $310,000 and has accumulated depreciation of $260,000. Depreciation has been taken up to the end of the

year.

What is the amount of the gain or loss on this transaction?

a.

loss of $55,000

b.

loss of $5,000

c.

gain of $5,000

d.

gain of $55,000

130.

On December 31, Strike Company traded-in one of its batting cages for another one that has a cost of $500,000.

Strike receives a trade-in allowance of $11,000. The old equipment had an initial cost of $215,000 and has

accumulated depreciation of $185,000. Depreciation has been recorded up to the end of the year. The difference

will be paid in cash. What is the amount of the gain or loss on this transaction?

a.

loss of $11,000

b.

no loss or gain will be recorded

c.

loss of $19,000

d.

gain of $11,000

131.

Machinery was purchased on January 1 for $51,000. The machinery has an estimated life of 7 years and an

estimated salvage value of $9,000. Double-declining-balance depreciation for the second year would be

(round

calculations to the nearest dollar):

a. $6,000

b. $10,500

c. $10,929

d. $10,408

Chapter 10: Fixed Assets and Intangible Assets

132.

When a company replaces a component of property, plant, and equipment, which statement below does not account

for one of the steps in the process?

a.

The asset cost of the replaced component is credited.

b.

Book value of the replaced component is written off to depreciation expense.

c.

The identifiable direct costs associated with the new component are expensed in the current period.

d.

The identifiable direct costs associated with the new component are capitalized.

133.

What is the cost of the land, based upon the following data?

Land purchase price

$178,000

Broker’s commission

15,000

Payment for the demolition

and removal of existing building

5,000

Cash received from the sale of materials

salvaged from the demolished building

2,000

Chapter 10: Fixed Assets and Intangible Assets

134.

Falcon Company acquired an adjacent lot to construct a new warehouse, paying $40,000 and giving a short–

term

note for $410,000. Legal fees paid were $13,275, delinquent taxes assessed were $14,500, and fees paid

to remove

an old building from the land were $15,800. Materials salvaged from the demolition of the building

were sold for $6,800. A contractor was paid $890,000 to construct the new warehouse. Determine the cost of

the land to be

reported on the balance sheet and show your work.

Chapter 10: Fixed Assets and Intangible Assets

135.

Identify each of the following expenditures as chargeable to (a) Land, (b) Land Improvements, (c) Buildings,

(d)

Machinery and Equipment, or (e) other account.

(1)

Cost of paving parking area for employees and customers

(2)

Insurance during construction of building

(3)

Interest incurred on loan during construction of building

(4)

Fee paid for installation of equipment

(5)

Special foundation for new equipment acquired

(6)

Insurance on new equipment while in transit

(7)

Freight charges on new equipment

(8)

Cost of repairing vandalism damage to equipment during installation

(9)

Sales tax on new equipment

(10)

Cost incurred in repairing damage resulting from installation of new equipment

(11)

Cost of land fill for building site

(12)

Cost of lubricating oil purchased for periodic oil changes for equipment

(13)

Parking lot lighting

(14)

Installing a fence around the parking lot

(15)

Repainting the trim on a building

(16)

Special assessment paid to city for extension of water main to property

(17)

Cost of razing and removing the old building on property acquired for a building site

(18)

Delinquent real estate taxes assumed by purchaser on property acquired for a building site

(19)

Attorney’s fee for title search

(20)

Architect’s fee for building plans and supervision of construction

Chapter 10: Fixed Assets and Intangible Assets

136.

A number of major structural repairs completed at the beginning of the current fiscal year at a cost of $1,000,000

are expected to extend the life of a building 10 years beyond the original estimate. The original cost of the

building

was $6,552,000, and it has been depreciated by the straight-line method for 25 years. Estimated residual

value is

negligible and has been ignored. The related accumulated depreciation account after the depreciation

adjustment at

the end of the preceding fiscal year is $4,550,000.

(a)

What has the amount of annual depreciation been in past years?

(b)

What was the original life estimate of the building?

(c)

To what account should the $1,000,000 be debited?

(d)

What is the book value of the building after the extraordinary repairs have been made?

(e)

What is the expected remaining life of the building after the extraordinary repairs have

been

made?

(f)

What is the amount of straight-line depreciation for the current year, assuming that the

repairs were completed at the very beginning of the current year? Round to the nearest

dollar.

Chapter 10: Fixed Assets and Intangible Assets

137.

Journalize each of the following transactions:

(a)

A wing costing $2,345,000 was added to the building. A new mortgage was issued for

the

cost.

(b)

Equipment was upgraded to increase its capacity to produce widgets. The upgrade cost of

$11,500 was paid in cash.

(c)

A major overhaul costing $8,000 on a machine increased the useful life by 4 years.

The

payment was made in cash.

138.

On April 15, Compton Co. paid $2,800 to upgrade a delivery truck and $125 for an oil change. Journalize

the

entries for the upgrade to delivery truck and oil change expenditures.

Chapter 10: Fixed Assets and Intangible Assets

139.

XYZ Co. incurred the following costs related to the office building used in operating its sports supply company:

a.

Replaced a broken window.

b.

Replaced the roof that had been on the building 23 years.

c.

Serviced all the air conditioners before summer started.

d.

Replaced the air conditioners in the customer service areas.

e.

Added a warehouse to the back of the building.

f.

Repainted the interior walls.

g.

Installed window shutters on all windows.

Classify each of the costs as a capital expenditure or revenue expenditure. For those costs identified as capital

expenditures, classify each as an additional or replacement component.

140.

Comment on the validity of the following statements. “As an asset loses its ability to provide services, cash

needs

to be set aside to replace it. Depreciation accomplishes this goal.”

Chapter 10: Fixed Assets and Intangible Assets

141.

Computer equipment was acquired at the beginning of the year at a cost of $65,000 that has an estimated

residual

value of $3,800 and an estimated useful life of 8 years. Determine the (a) depreciable cost, (b) straight–

line rate,

and (c) annual straight-line depreciation.

142.

The double-declining balance rate for calculating depreciation expense is determined by doubling the straight-

line

rate. Assuming that an asset has a useful life of 25 years, determine the rate to be used if using the double–

declining-balance method.

143.

Copy equipment was acquired at the beginning of the year at a cost of $72,000 that has an estimated residual value

of $9,000 and an estimated useful life of 5 years. It is estimated that the machine will output an estimated

1,000,000 copies. This year, 315,000 copies were made. Determine the (a) depreciable cost, (b) depreciation rate,

and (c) the units-of-output depreciation for the year.

Chapter 10: Fixed Assets and Intangible Assets

144.

A machine costing $57,000 with a 6-year life and $54,000 depreciable cost was purchased January 1. Compute

the

yearly depreciation expense using straight-line depreciation.

145.

A machine costing $185,000 with a 5-year life and $20,000 residual value was purchased January 2.

Compute

depreciation for each of the five years, using the double-declining-balance method.

146.

Computer equipment was acquired at the beginning of the year at a cost of $63,000 that has an estimated

residual

value of $3,000 and an estimated useful life of 5 years. Determine the (a) depreciable cost (b) double–

declining-balance rate, and (c) double-declining-balance depreciation for the first year.

Chapter 10: Fixed Assets and Intangible Assets

147.

Convert each of the following estimates of useful life to a straight-line depreciation rate, stated as a percentage.

(1)

2 years

(2)

8 years

(3)

10 years

(4)

20 years

(5)

25 years

(6)

40 years

(7)

50 years

Chapter 10: Fixed Assets and Intangible Assets

148.

Prior to adjustment at the end of the year, the balance in Trucks is $300,900 and the balance in Accumulated

Depreciation—Trucks is $88,200. Details of the subsidiary ledger are as follows:

Truck

No.

Cost

Estimated

Residual Value

Estimated

Useful Life

Accumulated

Depreciation at

Beginning of Year

Miles

Operated

During Year

1

$100,000

$13,000

300,000

—

30,000

2

72,900

9,900

300,000

$60,000

25,000

3

38,000

3,000

200,000

8,050

45,000

4

90,000

13,000

200,000

20,150

40,000

Required:

(1)

Based on the units-of-output method, determine the depreciation rates per mile and the

amount to be credited to the accumulated depreciation section of each of the

subsidiary

accounts for the miles operated during the current year.

(2)

Journalize the entry to record depreciation for the year.

Chapter 10: Fixed Assets and Intangible Assets

149.

An asset was purchased for $58,000 and originally estimated to have a useful life of 10 years with a residual value

of $3,000. After two years of straight-line depreciation, it was determined that the remaining useful life of the

asset

was only 2 years with a residual value of $2,000.

a)

Determine the amount of the annual depreciation for the first two years.

b)

Determine the book value at the end of Year 2.

c)

Determine the depreciation expense for each of the remaining years after revision.

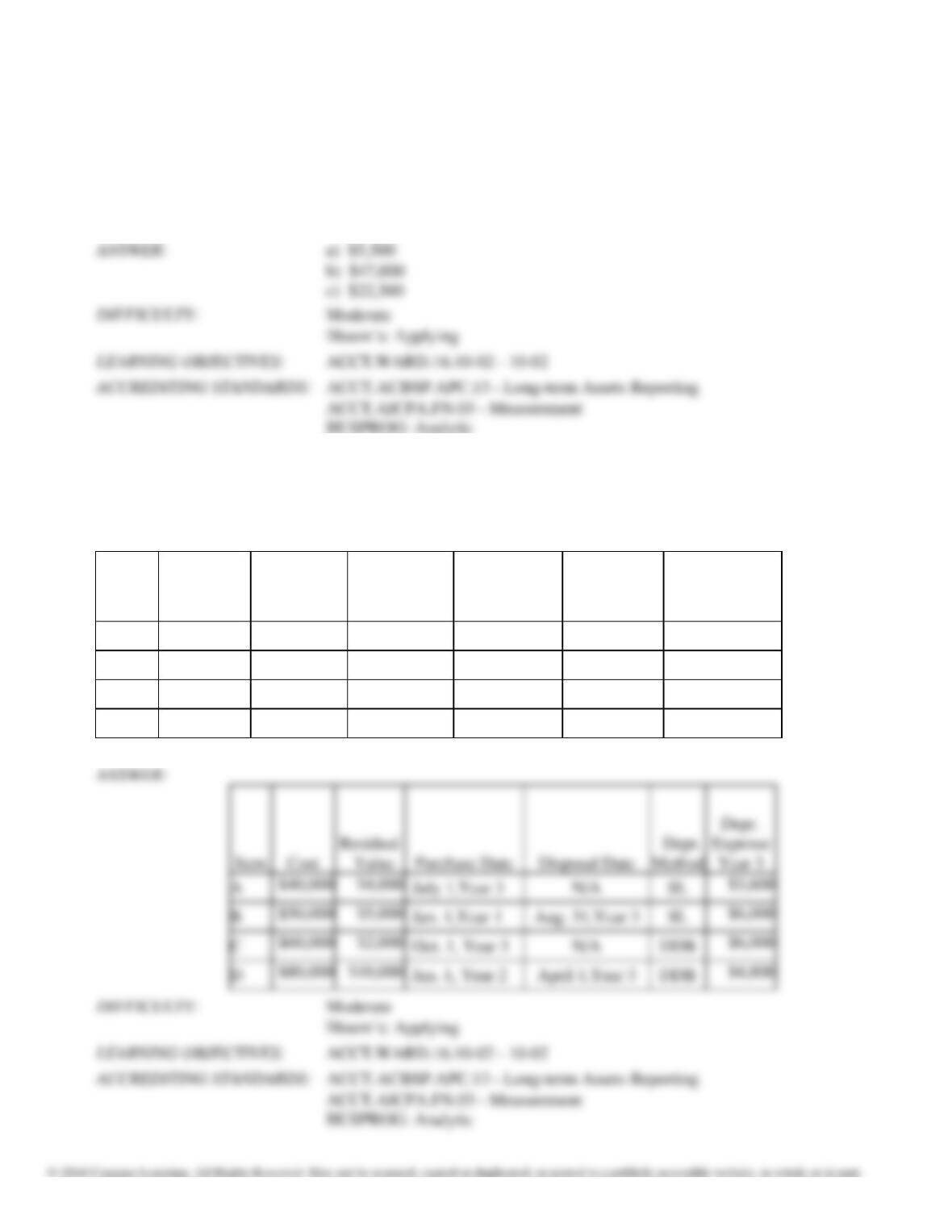

150.

For each of the following fixed assets, determine the depreciation expense for Year 3:

Disposal date is N/A if asset is still in use.

Method: SL = straight line; DDB = double declining balance

Assume the estimated life is 5 years for each asset.

Item

Cost

Residual

Value

Purchase Date

Disposal date

Depr.

Method

Depr.

Expense

Year 3

A

$40,000

$4,000

July 1,Year 3

N/A

SL

B

$50,000

$5,000

Jan. 1, Year 1

Aug. 31,Year 3

SL

C

$60,000

$2,000

Oc.t 1, Year 3

N/A

DDB

D

$80,000

$10,000

Jan. 1, Year 2

April 1, Year 3

DDB

Chapter 10: Fixed Assets and Intangible Assets

151.

Equipment purchased at the beginning of the fiscal year for $360,000 is expected to have a useful life of 5 years, or

14,000 operating hours, and a residual value of $10,000. Compute the depreciation for the first and second years of

use by each of the following methods:

(a)

straight-line

(b)

units-of-output (1,200 hours first year; 2,250 hours second year)

(c)

double-declining-balance

152.

Machinery is purchased on July 1 of the current fiscal year for $240,000. It is expected to have a useful life of 4

years, or 25,000 operating hours, and a residual value of $15,000. Compute the depreciation for the last six

months

of the current fiscal year ending December 31 by each of the following methods:

(a)

straight-line

(b)

double-declining-balance

(c)

units-of-output (used for 1,600 hours during the current year)

Chapter 10: Fixed Assets and Intangible Assets

153.

Determine the depreciation, for the year of acquisition and for the following year, of a fixed asset acquired on

October 1 for $500,000, with an estimated life of 5 years, and residual value of $50,000, using (a) the double

declining-balance method and (b) the straight-line method. Assume a fiscal year ending December 31.

154.

Equipment costing $80,000 with a useful life of 10 years and a residual value of $8,000 has been depreciated for

6

years by the straight-line method. Assume a fiscal year ending December 31.

(a)

What is the book value at the end of the sixth year of use?

(b)

If early in the seventh year it is estimated that the remaining useful life is 5 years

(instead of 4) and the residual value is $6,000, what is the amount of depreciation

for

the seventh year?

Chapter 10: Fixed Assets and Intangible Assets

155.

Golden Sales has bought $135,000 in fixed assets on January 1st associated with sales equipment. The residual

value of these assets is estimated at $10,000 at the end of their 4-year service life. Golden Sales managers want to

evaluate the options of depreciation.

(a)

Compute the annual straight-line depreciation and provide the sample depreciation journal entry to be

posted

at the end of each of the years.

(b)

Write the journal entries for each year of the service life for these assets using the double-declining

balance

method.

Chapter 10: Fixed Assets and Intangible Assets

156.

On July 1, Harding Construction purchases a bulldozer for $228,000. The equipment has a 8-year life with

a

residual value of $16,000. Harding uses straight-line depreciation.

(a) Calculate the depreciation expense and provide the journal entry for the first year ending December 31.

(b)

Calculate the third year’s depreciation expense and provide the journal entry for the third year ending

December 31.

(c)

Calculate the last year’s depreciation expense and provide the journal entry for the last year.

Chapter 10: Fixed Assets and Intangible Assets

157.

On July 1, Hartford Construction purchases a bulldozer for $228,000. The equipment has a 9-year life with a

residual value of $16,000. Hartford uses the units-of-output method depreciation, and the bulldozer is expected

to

yield 26,500 operating hours.

(a)

Calculate the depreciation expense per hour of operation.

(b)

The bulldozer is operated 1,250 hours in the first year, 2,755 hours in the second year, and 1,225 hours in

the

third year of operations. Journalize the depreciation expense for each year.

Chapter 10: Fixed Assets and Intangible Assets

158.

Eagle Country Club has acquired a lot to construct a clubhouse. Eagle had the following costs related to

the

construction:

Architects’ fees

$ 45,000

Construction labor

80,000

Engineers’ fees

15,000

Fences around building

9,000

Grading and leveling

10,000

Insurance costs incurred during construction

7,000

Interest on money borrowed for construction

5,000

Land

73,000

Building Materials

237,000

Sales taxes

6,000

Trees and shrubs

6,000

Determine the cost of the club house to be reported on the balance sheet.

Chapter 10: Fixed Assets and Intangible Assets

159.

Equipment was purchased on January 5, year 1, at a cost of $90,000. The equipment had an estimated useful

life

of 8 years and an estimated residual value of $8,000.

After using the equipment for 3 years, the useful life was revised to a total of 10 years and the residual value was

reduced to $2,004.

Determine the straight-line depreciation expense for the Year 4 and following years.

160.

A copy machine acquired on May 1 with a cost of $2,545 has an estimated useful life of 3 years. Assuming that

it

will have a residual value of $445, determine the depreciation for the first and second year by the straight-line

method. Round your answers to the nearest whole dollar.