148 Solnik/McLeavey • Global Investments, Sixth Edition

set at an annual 0.1%. The investment bank also proposes a five-year cap option at a strike of

13.75%. The cost of this cap is spread over the payment dates and set at an annual 0.05%. The

company can also enter into a five-year interest rate swap at 7% fixed against LIBOR.

a. Explain why it would be attractive to the French company to issue these FRNs compared to

current market conditions for plain-vanilla straight bonds and FRNs.

b. Find out the borrowing cost reduction that can be achieved by issuing bull notes compared to a

fixed-coupon rate of 7.25%.

c. Find out the borrowing cost reduction that can be achieved by issuing bear notes compared to an

FRN at LIBOR plus 0.25%.

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 149

40. The current yield curve on the international bond market in euro is flat at 4% for top-quality

borrowers. A French company of good standing can issue plain-vanilla straight and floating-rate

bonds at the following conditions:

• Bond A: Straight Bond. Five-year straight bond with a fixed coupon of 4%.

• Bond B: FRN. Five-year dollar FRN with a semiannual coupon set at LIBOR.

An investment banker proposes to the French company to issue bull and/or bear FRNs at the

following conditions:

• Bond C: Bull FRN. Five-year FRN with a semiannual coupon set at:

7.60% – LIBOR.

• Bond D: Bear FRN. Five-year FRN with a semiannual coupon set at:

2 LIBOR – 4.2%.

The floor on all coupons is zero. The investment bank also proposes a five-year floor option at a

strike of 2.1%. This floor will pay to the French company the difference between 2.1% and LIBOR, if

it is positive, or zero if LIBOR is above 2.1%. The cost of this floor is spread over the payment dates

and set at an annual 0.05%. The bank also proposes a five-year cap at a strike of 7.60%. The annual

premium on the cap is 0.1%. The company can also enter in a five-year interest-rate swap 4% fixed

against LIBOR.

a. Assume that the French company issues Bonds C and D in equal proportions. Is it more

advantageous than issuing Bonds A and B in equal proportion and why?

b. Find out the borrowing cost reduction that can be achieved by issuing the bull note compared to

issuing a fixed-coupon straight bond at 4%.

c. Find out the borrowing cost reduction that can be achieved by issuing the bull note compared to

issuing a plain-vanilla FRN at LIBOR.

d. Find out the borrowing cost reduction that can be achieved by issuing the bear note compared to

issuing a fixed-coupon straight bond at 4%.

e. Find out the borrowing cost reduction that can be achieved by issuing the bear note compared to

issuing a plain-vanilla FRN at LIBOR.

150 Solnik/McLeavey • Global Investments, Sixth Edition

41. The Kingdom of Papou issues a very-bull bond with a coupon equal to:

14.6 – 2 LIBOR.

Of course, the coupon cannot be negative.

The Kingdom could have issued a FRN at LIBOR + ¼ %, or a straight bond at 5.30%.

The current market conditions for swaps are 5% against LIBOR.

You could also trade in caps and floors with different exercise prices (these are levels of interest

rates). The premium are paid annually.

Exercise

Interest Rate

Annual Premium

Cap

Floor

7.3 %

0.2 %

2%

14.6 %

0.1 %

10 %

a. You are a buyer of this very-bull bond. Tell us what it is equivalent to, in terms of buying/selling:

FRN, straight bonds, caps or floors.

b. Assume that the Kingdom actually wanted to issue a straight bond (fixed coupon). The bank will

put in place a “de–mining” portfolio with swaps and options so that this very-bull bond plus the

“de–mining” portfolio is equivalent to a straight bond. What is exactly the “de–mining” portfolio?

(Be very precise and tell us if the Kingdom must pay fixed, receive LIBOR or vice versa, etc.)

c. What is the cost advantage for the Kingdom compared to issuing bonds at 5.30%?

d. Same question assuming that the Kingdom wanted to issue an FRN at LIBOR + ¼%?

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 151

42. Bank PAPOUF decides to issue two bonds and wonders what the fair interest rate on these bonds

should be:

A. A one-year currency option bond. The bond is issued in dollars with a face value of $100. The

bondholder can choose to have the coupon and principal paid in dollars or in SFr, at a specified

exchange rate of SFr/$ = 2, that is, receive either $100 or SFr 200 as principal repayment, and

receive either $C or SFr 2C as interest if C is the coupon set in dollars. The coupon rate is

c = C/100.

B. A two-year currency option bond. The bond is issued in dollars, with a face value of $100 and

pays an annual coupon C. The bondholder can choose to have the coupons and principal paid in

dollars or in SFr, at a specified exchange rate of SFr/$ = 2, that is, receive either $100 or SFr 200

as principal repayment, and receive either $C or SFr 2C as interest, if C is the coupon set in

dollars. The coupon rate is c = C/100.

Current market conditions are given below:

• Interest Rates 1-Year 2-Year

Zero-coupon rates

US$ 8% 8%

SFr 4% 4%

• Spot exchange rate: SFr/$ = 2

• Currency options:

SFr call, strike price 50 U.S. cents, expiration one year: 2 U.S. cents.

SFr call, strike price 50 U.S. cents, expiration two years: 5 U.S. cents.

a. Compute the coupon C on Bond A that would be consistent with market conditions at time of

issue.

b. Compute the coupon C‘ on Bond B that would be consistent with market conditions at time of

issue.

152 Solnik/McLeavey • Global Investments, Sixth Edition

Solution

43. Titi, a Japanese company, issued a six-year international bond in dollars convertible into shares of the

company. At time of issue, the long-term bond yield on straight dollar bonds was 10% for such an

issuer. Instead, Titi issued bonds at 8%. Each $1,000 par bond is convertible into 100 shares of Titi.

At time of issue, the stock price of Titi is 1,600 yen, and the exchange rate is 100 yen = 0.5 dollars

($/¥ = 0.005, ¥/$ = 200).

a. Why can the bond be issued with a yield of only 8%, below the market rate for straight dollar

bonds?

b. What would happen if:

• The stock price of Titi increases?

• The yen appreciates?

• The market interest rate of dollar bonds drops?

A year later, the new market conditions are as follows:

• The yield on straight dollar bonds of similar quality has risen from 10% to 11%.

• Titi stock price has moved up to ¥ 2,000.

• The exchange rate is $/¥ 0.006.

c. What would be a minimum price for the Titi convertible bond?

d. Could you try to assess the theoretical value of this convertible bond as a package of other

securities, such as straight bonds issued by Titi, options or warrants on the yen value of Titi

stock, and futures and options on the dollar/yen exchange rate?

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 153

44. Strumpf Ltd. decides to issue a convertible bond with a maturity of two years. Each bond is issued

with a nominal value of £ 100 and an annual coupon C; of course, C has to be determined. Each bond

can be redeemed for £ 100 or converted into one share of Strumpf at the option of the bondholder.

The current stock price of Strumpf is £90. The yield curve for an issuer like Strumpf is flat at 6%.

Barings is ready to issue long-term options on Strumpf shares. The premiums on calls with one-year

and two-year expirations are given below:

Strike

Price

European-Type

American-Type

1-Year

2-Year

1-Year

2-Year

90

11

16

12

17

100

6

8

6.5

9

a. American-type calls are more expensive than European-type calls. Is it reasonable?

b. Assume that the bond can only be converted at maturity, after payment of the second coupon.

What should be the fair coupon rate C, consistent with the above market conditions?

c. Assume that the bond is issued with the coupon rate determined above. The yield curve suddenly

moves from 6% to 6.1% and the option premiums stay the same. What should be the new market

price of the convertible bond?

d. Assume now that the bond can be converted on two dates (rather than one as above). These dates

are the first year (right after the first coupon payment) and the second year as above. It is not

possible to convert the two-year bond at any other date. Is it possible to construct an arbitrage

portfolio allowing to price the fair coupon C with the above data? Be precise in your explanation

and state what type of options you would need to price the bond.

154 Solnik/McLeavey • Global Investments, Sixth Edition

45. In 1990, the French bank, BNP, issued exchangeable bonds denominated in French francs (FF).

These are bonds issued for FF 100 on April 1, 1990, with an annual coupon of FF 5, plus an exchange

right. The bonds can be redeemed for FF 100 on April 1, 1996. The right can be exchanged on

April 1, 1991, with payment of an additional FF 100, for another bond identical to the old bond

(annual coupon of FF 5 and redeemed for FF 100 on April 1, 1996). If you exercise your right, you

will have paid an additional FF 100 on April 1, 1991, but you will then hold two BNP bonds with

maturity in 1996.

a. Under what scenario would you exercise the exchange right (exchange the right plus FF 100 for

an additional bond) on April 1, 1991? What is the attraction of such an exchangeable bond for

investors?

b. On April 1, 1990, the yield curve is flat at 6%. You can buy a call on a five-year bond with a

coupon of 5%. The call has a strike price of 100% and expires on April 1, 1991. Its premium is

2%. Construct a replication portfolio to determine at what price the exchangeable bond can be

issued by BNP.

Solution

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 155

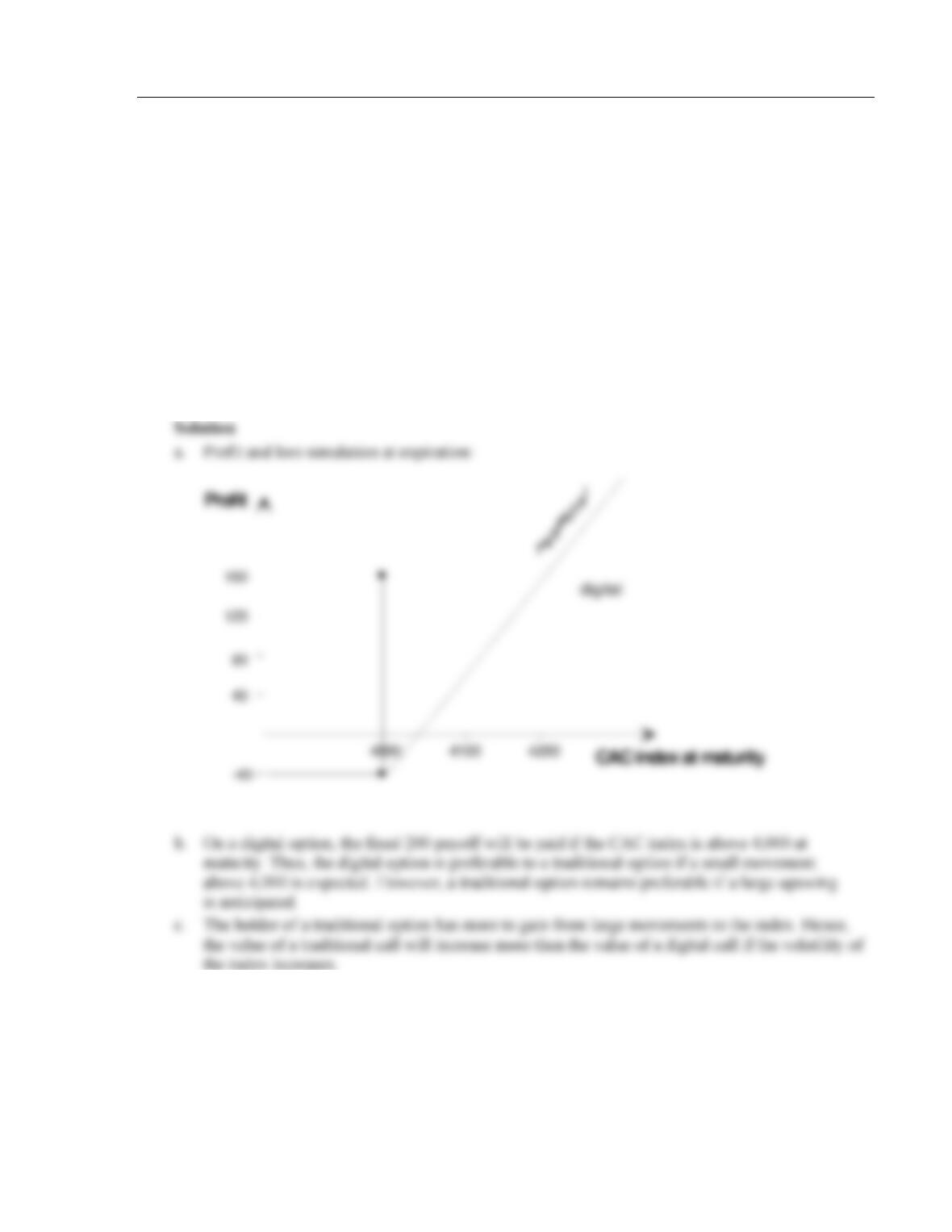

46. Digital options: Digital (or binary) options can only have two payoffs at maturity. If the strike

condition set in the option is met, the buyer will receive the full prespecified payoff. If not, the buyer

receives no payoff. This is different from a traditional option where there exists an infinite number of

payoffs. For example, we could have a digital option on the French CAC index, stating that the option

buyer will get €200 if the CAC index is above 4,000 at expiration and zero otherwise. On this digital

option, the buyer will get exactly 200 as soon as the CAC index is above the 4,000 level at expiration,

whether it be 4,001, 4,100, or 5,000.

a. Draw the profit and loss curve at expiration as a function of the CAC index for these two options:

• Traditional call on the CAC index: Exercise price: 4,000; premium: 40.

• Digital call on the CAC index: Exercise price: 4,000; payoff if exercised: 200; premium: 40.

b. What are the relative advantages of the two options?

c. Assume that the volatility of the French stock market increases suddenly. Should the premium on

the digital call increase more (or less) than the premium on the traditional call?

47. Guaranteed note.

You are a young banker offering a client to issue a guaranteed note. The yield curve is flat at 9% for

each maturity. Options on the stock index are offered by banks. A at-the-money call with a two-year

maturity trades at 12% of the index value, whereas a three-year call is worth 15% of the index.

You wonder about the characteristics of the bond. If you offer a high coupon, the indexation will be

low. Therefore, you decide to compute the indexation levels in accordance to the current market

conditions for maturities of two and three years and coupon levels of 0%, 2%, and 5%.

156 Solnik/McLeavey • Global Investments, Sixth Edition

Solution

48. You are a young investment banker considering the issuance of a guaranteed note with stock index

participation for a client. The current yield curve is flat at 8% for all maturities. Long-term at-the-

money options on the stock market index are traded by banks. Two-year at-the-money calls trade

at 17.84% of the index value; three-year at-the-money calls trade at 20% of the index value. You

are hesitant about the terms to set in the structured note. You know that if you guarantee a higher

coupon rate, the level of participation in the stock appreciation will be less. Your boss asks you to

compute the “fair” participation rate that would be feasible for various guaranteed coupon rates and

maturities. In other words, based on the current market conditions (as described above), estimate the

participation rates that are feasible with a maturity of two or three years, and a coupon rate of: 0%,

1%, 2%, 3%, 5%, and 7%.

Solution

Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 157

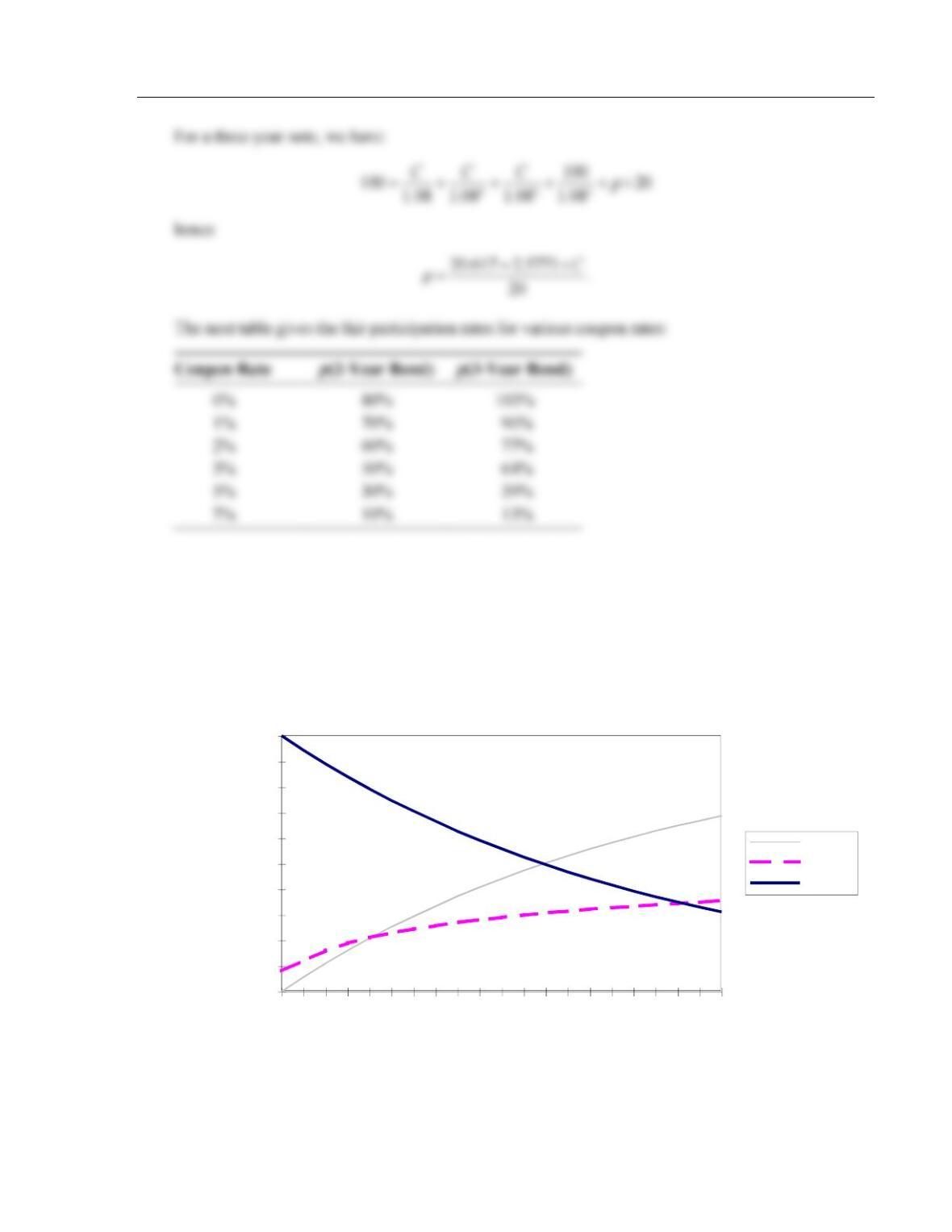

49. You’re a banker. A client wishes to buy a guaranteed note with a 100% indexation to the stock

index’s growth. In other words, he doesn’t want any coupon but requires 100% of the index growth.

You wonder about the maturity of such a note. You check the prices of various index calls traded on

the market for different maturities. Their strike is the current index level and their price is expressed

as a percentage of this level. (For instance if the CAC is worth 3,000, the strike is 3,000 and the one-

year maturity call trades at 11% of 3,000. You also check the price of a zero-coupon in percentage for

various maturities. The following graph shows, for each maturity, the price of the option, that of the

zero-coupon, and 100%-zero.

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

0

2

4

6

8

10

12

14

16

18

20

Maturity

100-Zero

Option

Zero

158 Solnik/McLeavey • Global Investments, Sixth Edition

a. What is the maturity of the guaranteed note (coupon = 0%, indexation = 100%)? Justify.

b. If as a banker, you want to make a profit, should you lengthen or shorten the maturity of that

note? Explain why.

c. Everything remaining constant (that is, same volatility and interest rate), should the maturity of

the guaranteed note be shorter or longer if the index pays a low dividend rather than a high one?

Why?