FOR INSTRUCTOR USE ONLY

CHAPTER 10

BUDGETARY CONTROL AND

RESPONSIBILITY ACCOUNTING

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

True-False Statements

1.

1

K

9.

2

C

17.

2

K

25.

3

K

33.

2

K

2.

1

C

10.

2

K

18.

2

K

26.

3

K

34.

3

C

3.

1

K

11.

2

K

19.

3

C

27.

4

K

35.

3

K

4.

1

K

12.

2

C

20.

3

C

28.

4

K

36.

4

K

5.

1

C

13.

2

C

21.

3

C

a29.

5

C

a37.

5

K

6.

1

C

14.

2

C

22.

3

C

a30.

5

C

7.

1

K

15.

2

K

23.

3

C

31.

1

K

8.

1

C

16.

2

K

24.

3

K

32.

1

K

Multiple Choice Questions

38.

1

K

64.

2

C

90.

3

AP

116.

3

C

142.

4

K

39.

1

C

65.

2

K

91.

3

C

117.

3

AP

143.

4

K

40.

1

K

66.

2

C

92.

3

C

118.

3

C

144.

4

AP

41.

1

C

67.

2

C

93.

3

C

119.

3

C

145.

4

C

42.

1

K

68.

2

K

94.

3

K

120.

3

AP

146.

4

AP

43.

1

K

69.

2

K

95.

3

C

121.

4

AP

147.

4

C

44.

1

K

70.

2

AP

96.

3

C

122.

4

AP

a148.

5

AP

45.

1

C

71.

2

C

97.

3

C

123.

4

AN

a149.

5

K

46.

1

C

72.

2

C

98.

3

C

124.

4

AP

a150.

5

C

47.

1

C

73.

2

C

99.

3

K

125.

4

AN

a151.

5

C

48.

1

C

74.

2

AP

100.

3

C

126.

4

AP

a152.

5

C

49.

1

C

75.

2

AP

101.

3

C

127.

4

AP

a153.

5

AP

50.

1

C

76.

2

AP

102.

3

C

128.

4

AP

a154.

5

AP

51.

1

C

77.

2

AP

103.

3

C

129.

4

AP

a155.

5

AP

52.

1

C

78.

2

AP

104.

3

K

130.

4

AP

156.

1

C

53.

1,2

C

79.

2

AP

105.

3

C

131.

4

AP

157.

1

K

54.

1

K

80.

2

AP

106.

3

C

132.

4

AP

st158.

1

K

55.

2

AP

81.

2

AP

107.

3

C

133.

4

AN

159.

2

AP

56.

2

AP

82.

2

AP

108.

3

C

134.

4

AP

st160.

2

K

57.

2

AP

83.

2

AP

109.

3

C

135.

4

AP

161.

2

K

58.

2

C

84.

2

AP

110.

3

K

136.

4

C

st162.

2

K

59.

2

C

85.

2

AP

111.

3

C

137.

4

C

163.

3

K

60.

2

K

86.

2

AP

112.

3

K

138.

4

K

st164.

3

K

61.

2

C

87.

2

AP

113.

3

C

139.

4

C

165.

4

K

62.

2

C

88.

2

AP

114.

3

C

140.

4

K

st166.

4

K

63.

2

C

89.

3

K

115.

3

AP

141.

4

AP

167.

4

AP

Brief Exercises

168 7

.

2

AP

171.

2

AP

174.

4

AP

177.

4

AN

169.

2

AP

172.

3

AP

175.

4

AP

a178.

5

AP

170.

2

AP

173.

.

3

AP

176.

4

AP

a179.

5

AP

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 2

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Exercises

180.

1

AP

185.

2

AP

190.

2

AP

195.

3

AN

200.

4

AP

181.

1,2

AP

186.

2

AP

191.

2,3

AP

196.

3

AN

201.

4

AN

182.

2

AP

187.

2

AP

192.

3

AP

197.

3,4

AP

202.

4

AN

183.

2

AP

188.

2

AP

193.

3

AN

198.

4

AP

203.

4

AN

184.

2

AP

189.

2

AP

194.

3

AP

199.

4

AP

204.

4

AN

Completion Statements

205.

1

K

208.

1

K

211.

3

K

214.

3

K

206.

1

K

209.

2

K

212.

3

K

215.

4

K

207.

1

K

210.

2

K

213.

3

K

216.

4

K

Matching

217.

1–4

K

Short-Answer Essay

218.

1

K

220.

3

K

222.

4

K

219.

2

K

221.

3

K

223.

4

K

st This question also appears in a self-test at the student companion website.

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

7.

TF

40.

MC

46.

MC

52.

MC

180.

Ex

217.

MA

2.

TF

8.

TF

41.

MC

47.

MC

53.

MC

181.

Ex

218.

S-A

3.

TF

31.

TF

42.

MC

48.

MC

54.

MC

205.

C

4.

TF

32.

TF

43.

MC

49.

MC

156.

MC

206.

C

5.

TF

38.

MC

44.

MC

50.

MC

157.

MC

207.

C

6.

TF

39.

MC

45.

MC

51.

MC

158.

MC

208.

C

Learning Objective 2

9.

TF

33.

TF

63.

MC

73.

MC

83.

MC

168.

BE

187.

Ex

10.

TF

53.

MC

64.

MC

74.

MC

84.

MC

169.

BE

188.

Ex

11.

TF

55.

MC

65.

MC

75.

MC

85.

MC

170.

BE

189.

Ex

12.

TF

56.

MC

66.

MC

76.

MC

86.

MC

171.

BE

190.

Ex

13.

TF

57.

MC

67.

MC

77.

MC

87.

MC

181.

Ex

191.

Ex

14.

TF

58.

MC

68.

MC

78.

MC

88.

MC

182.

Ex

209.

C

15.

TF

59.

MC

69.

MC

79.

MC

159.

MC

183.

Ex

210.

C

16.

TF

60.

MC

70.

MC

80.

MC

160.

MC

184.

Ex

217.

MA

17.

TF

61.

MC

71.

MC

81.

MC

161.

MC

185.

Ex

219.

S-A

18.

TF

62.

MC

72.

MC

82.

MC

162.

MC

186.

Ex

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 3

Learning Objective 3

19.

TF

35.

TF

97.

MC

106.

MC

115.

MC

173.

BE

212.

C

20.

TF

89.

MC

98.

MC

107.

MC

116.

MC

191.

Ex

213.

C

21.

TF

90.

MC

99.

MC

108.

MC

117.

MC

192.

Ex

214.

C

22.

TF

91.

MC

100.

MC

109.

MC

118.

MC

193.

Ex

217.

MA

23.

TF

92.

MC

101.

MC

110.

MC

119.

MC

194.

Ex

220.

S-A

24.

TF

93.

MC

102.

MC

111.

MC

120.

MC

195.

Ex

221.

S-A

25.

TF

94.

MC

103.

MC

112.

MC

163.

MC

196.

Ex

26.

TF

95.

MC

104.

MC

113.

MC

164.

MC

197.

Ex

34.

TF

96.

MC

105.

MC

114.

MC

172.

BE

211.

C

Learning Objective 4

27.

TF

126.

MC

134.

MC

142.

MC

167.

MC

200.

Ex

222.

K

28.

TF

127.

MC

135.

MC

143.

MC

174.

BE

201.

Ex

223.

K

36.

TF

128.

MC

136.

MC

144.

MC

175.

BE

202.

Ex

121.

MC

129.

MC

137.

MC

145.

MC

176.

BE

203.

Ex

122.

MC

130.

MC

138.

MC

146.

MC

177.

BE

204.

Ex

123.

MC

131.

MC

139.

MC

147.

MC

197.

Ex

215.

C

124.

MC

132.

MC

140.

MC

165.

MC

198.

Ex

216.

C

125.

MC

133.

MC

141.

MC

166.

MC

199.

Ex

217.

MA

Learning Objective 5a

29.

TF

37.

TF

149.

MC

151.

MC

153.

MC

155.

MC

179.

BE

30.

TF

148.

MC

150.

MC

152.

MC

154.

MC

178.

BE

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise S-A = Short-Answer

CHAPTER LEARNING OBJECTIVES

1. Describe budgetary control and static budget reports. Budgetary control consists of (a)

preparing periodic budget reports that compare actual results with planned objectives, (b)

2. Prepare flexible budget reports. To develop the flexible budget, it is necessary to: (a)

Identify the activity index and the relevant range of activity. (b) Identify the variable costs, and

3. Apply responsibility accounting to cost and profit centers. Responsibility accounting

involves accumulating and reporting revenues and costs on the basis of the individual

manager who has the authority to make the day-to-day decisions about the items. The

evaluation of a manager’s performance is based on the matters directly under the manager’s

control. In responsibility accounting, it is necessary to distinguish between controllable and

Test Bank for Managerial Accounting, Seventh Edition

10 – 4

noncontrollable fixed costs and to identify three types of responsibility centers: cost, profit,

and investment.

4. Evaluate performance in investment centers. The primary basis for evaluating

performance in investment centers is return on investment (ROI). The formula for computing

ROI for investment centers is Controllable margin ÷ Average operating assets.

a5. Explain the difference between ROI and residual income. ROI is controllable margin

divided by average operating assets. Residual income is the income that remains after

TRUE-FALSE STATEMENTS

1. Budget reports comparing actual results with planned objectives should be prepared only

once a year.

2. If actual results are different from planned results, the difference must always be

investigated by management to achieve effective budgetary control.

3. Certain budget reports are prepared monthly, whereas others are prepared more

frequently depending on the activities being monitored.

4. The master budget is not used in the budgetary control process.

5. A master budget is most useful in evaluating a manager’s performance in controlling

costs.

6. A static budget is one that is geared to one level of activity.

7. A static budget is changed only when actual activity is different from the level of activity

expected.

Budgetary Planning and Responsibility Accounting

10 – 5

8. A static budget is most useful for evaluating a manager’s performance in controlling

variable costs.

9. A flexible budget can be prepared for each of the types of budgets included in the master

budget.

10. A flexible budget is a series of static budgets at different levels of activities.

11. Flexible budgeting relies on the assumption that unit variable costs will remain constant

within the relevant range of activity.

FSA

12. Total budgeted fixed costs appearing on a flexible budget will be the same amount as total

fixed costs on the master budget.

FSA

13. A flexible budget is prepared before the master budget.

FSA

14. The activity index used in preparing a flexible budget should not influence the variable

costs that are being budgeted.

FSA

15. A formula used in developing a flexible budget is: Total budgeted cost = fixed cost + (total

variable cost per unit × activity level).

16. Flexible budgets are widely used in production and service departments.

FSA

17. A flexible budget report will show both actual and budget cost based on the actual activity

level achieved.

18. Management by exception means that management will investigate areas where actual

results differ from planned results if the items are material and controllable.

19. Policies regarding when a difference between actual and planned results should be

investigated are generally more restrictive for noncontrollable items than for controllable

items.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 6

20. A distinction should be made between controllable and noncontrollable costs when

reporting information under responsibility accounting.

21. Cost centers, profit centers, and investment centers can all be classified as responsibility

centers.

22. More costs become controllable as one moves down to each lower level of managerial

responsibility.

23. In a responsibility accounting reporting system, as one moves up each level of

responsibility in an organization, the responsibility reports become more summarized and

show less detailed information.

24. A cost center incurs costs and generates revenues and cost center managers are

evaluated on the profitability of their centers.

25. The terms “direct fixed costs” and “indirect fixed costs” are synonymous with “traceable

costs” and “common costs,” respectively.

26. Controllable margin is subtracted from controllable fixed costs to get net income for a

profit center.

27. The denominator in the formula for calculating the return on investment includes operating

and nonoperating assets.

28. The formula for computing return on investment is controllable margin divided by average

operating assets.

a29. When evaluating residual income, the calculation tells management what percentage

return was generated by the particular division being evaluated.

a30. Residual income generates a dollar amount which represents the increase in value to the

company beyond the cost necessary to pay for the financing of assets.

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 7

31. Budget reports provide the feedback needed by management to see whether actual

operations are on course.

32. A static budget is an effective means to evaluate a manager’s ability to control costs,

regardless of the actual activity level.

33. The flexible budget report evaluates a manager’s performance in two areas: (1)

production and (2) costs.

34. The terms controllable costs and noncontrollable costs are synonymous with variable

costs and fixed costs, respectively.

35. Most direct fixed costs are not controllable by the profit center manager.

36. The manager of an investment center can improve ROI by reducing average operating

assets.

a37. Residual income and ROI are used as performance evaluation methods for profit center

performance

Answers to True-False Statements

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Test Bank for Managerial Accounting, Seventh Edition

10 – 8

MULTIPLE CHOICE QUESTIONS

38. What is budgetary control?

a. Another name for a flexible budget

b. The degree to which the CFO controls the budget

c. The use of budgets in controlling operations

d. The process of providing information on budget differences to lower level managers

39. A major element in budgetary control is

a. the preparation of long-term plans.

b. the comparison of actual results with planned objectives.

c. the valuation of inventories.

d. approval of the budget by the stockholders.

40. Budget reports should be prepared

a. daily.

b. monthly.

c. weekly.

d. as frequently as needed.

41. On the basis of the budget reports,

a. management analyzes differences between actual and planned results.

b. management may take corrective action.

c. management may modify the future plans.

d. All of these answers are correct.

42. The purpose of the departmental overhead cost report is to

a. control indirect labor costs.

b. control selling expense.

c. determine the efficient use of materials.

d. control overhead costs.

43. The purpose of the sales budget report is to

a. control selling expenses.

b. determine whether income objectives are being met.

c. determine whether sales goals are being met.

d. control sales commissions.

44. The comparison of differences between actual and planned results

a. is done by the external auditors.

b. appears on the company’s external financial statements.

c. is usually done orally in departmental meetings.

d. appears on periodic budget reports.

Budgetary Planning and Responsibility Accounting

10 – 9

45. A static budget

a. should not be prepared in a company.

b. is useful in evaluating a manager’s performance by comparing actual variable costs

and planned variable costs.

c. shows planned results at the original budgeted activity level.

d. is changed only if the actual level of activity is different than originally budgeted.

46. A static budget report

a. shows costs at only 2 or 3 different levels of activity.

b. is appropriate in evaluating a manager’s effectiveness in controlling variable costs.

c. should be used when the actual level of activity is materially different from the master

budget activity level.

d. may be appropriate in evaluating a manager’s effectiveness in controlling costs when

the behavior of the costs in response to changes in activity is fixed.

47. A static budget is appropriate in evaluating a manager’s performance if

a. actual activity closely approximates the master budget activity.

b. actual activity is less than the master budget activity.

c. the company prepares reports on an annual basis.

d. the company is a not-for-profit organization.

48. When budgeted and actual results are not the same amount, there is a budget

a. error.

b. difference.

c. anomaly.

d. by-product.

49. Top management’s reaction to a difference between budgeted and actual sales often

depends on

a. whether the difference is favorable or unfavorable.

b. whether management anticipated the difference.

c. the materiality of the difference.

d. the personality of the top managers.

50. If costs are not responsive to changes in activity level, then these costs can be best

described as

a. mixed.

b. flexible.

c. variable.

d. fixed.

Test Bank for Managerial Accounting, Seventh Edition

10 – 10

51. Assume that actual sales results exceed the planned results for the second quarter. This

favorable difference is greater than the unfavorable difference reported for the first quarter

sales. Which of the following statements about the sales budget report on June 30 is true?

a. The year-to-date results will show a favorable difference.

b. The year-to-date results will show an unfavorable difference.

c. The difference for the first quarter can be ignored.

d. The sales report is not useful if it shows a favorable and unfavorable difference for the

two quarters.

52. A static budget is appropriate for

a. variable overhead costs.

b. direct materials costs.

c. fixed overhead costs.

d. None of these answers are correct.

53. What is the primary difference between a static budget and a flexible budget?

a. The static budget contains only fixed costs, while the flexible budget contains only

variable costs.

b. The static budget is prepared for a single level of activity, while a flexible budget is

adjusted for different activity levels.

c. The static budget is constructed using input from only upper level management, while

a flexible budget obtains input from all levels of management.

d. The static budget is prepared only for units produced, while a flexible budget reflects

the number of units sold.

54. Another name for the static budget is

a. master budget.

b. overhead budget.

c. permanent budget.

d. flexible budget.

55. The master budget of Windy Co. shows that the planned activity level for next year is

expected to be 50,000 machine hours. At this level of activity, the following manufacturing

overhead costs are expected:

Indirect labor $720,000

Machine supplies 180,000

Indirect materials 210,000

Depreciation on factory building 150,000

Total manufacturing overhead $1,260,000

A flexible budget for a level of activity of 60,000 machine hours would show total

manufacturing overhead costs of

a. $1,482,000.

b. $1,260,000.

c. $1,512,000.

d. $1,362,000.

Budgetary Planning and Responsibility Accounting

10 – 11

56. Boland Manufacturing prepared a 2016 budget for 120,000 units of product. Actual

production in 2016 was 130,000 units. To be most useful, what amounts should a

performance report for this company compare?

a. The actual results for 130,000 units with the original budget for 120,000 units.

b. The actual results for 130,000 units with a new budget for 130,000 units.

c. The actual results for 130,000 units with last year’s actual results for 134,000 units.

d. It doesn’t matter. All of these choices are equally useful.

57. A department has budgeted monthly manufacturing overhead cost of $540,000 plus $3

per direct labor hour. If a flexible budget report reflects $1,044,000 for total budgeted

manufacturing cost for the month, the actual level of activity achieved during the month

was

a. 528,000 direct labor hours.

b. 168,000 direct labor hours.

c. 348,000 direct labor hours.

d. Cannot be determined from the information provided.

58. Which one of the following would be the same total amount on a flexible budget and a

static budget if the activity level is different for the two types of budgets?

a. Direct materials cost

b. Direct labor cost

c. Variable manufacturing overhead

d. Fixed manufacturing overhead

59. In developing a flexible budget within a relevant range of activity,

a. only fixed costs are included.

b. it is necessary to relate variable cost data to the activity index chosen.

c. it is necessary to prepare a budget at 1,000 unit increments.

d. variable and fixed costs are combined and are reported as a total cost.

60. What budgeted amounts appear on the flexible budget?

a. Original budgeted amounts at the static budget activity level

b. Actual costs for the budgeted activity level

c. Budgeted amounts for the actual activity level achieved

d. Actual costs for the estimated activity level

61. The flexible budget

a. is prepared before the master budget.

b. is relevant both within and outside the relevant range.

c. eliminates the need for a master budget.

d. is a series of static budgets at different levels of activity.

Test Bank for Managerial Accounting, Seventh Edition

10 – 12

62. A flexible budget can be prepared for which of the following budgets comprising the

master budget?

a. Sales

b. Overhead

c. Direct materials

d. All of these answers are correct.

63. A flexible budget

a. is prepared when management cannot agree on objectives for the company.

b. projects budget data for various levels of activity.

c. is only useful in controlling fixed costs.

d. cannot be used for evaluation purposes because budgeted data are adjusted to reflect

actual results.

64. If a company plans to sell 48,000 units of product but sells 60,000, the most appropriate

comparison of the cost data associated with the sales will be by a budget based on

a. the original planned level of activity.

b. 54,000 units of activity.

c. 60,000 units of activity.

d. 48,000 units of activity.

65. Within the relevant range of activity, the behavior of total costs is assumed to be

a. linear and upward sloping.

b. linear and downward sloping.

c. curvilinear and upward sloping.

d. linear to a point and then level off.

FSA

66. Sales results that are evaluated by a static budget might show

1. favorable differences that are not justified.

2. unfavorable differences that are not justified.

a. 1

b. 2

c. both 1 and 2.

d. neither 1 nor 2.

67. The selection of levels of activity to depict a flexible budget

1. will be within the relevant range.

2. is largely a matter of expediency.

3. is governed by generally accepted accounting principles.

a. 1

b. 2

c. 3

d. 1 and 2

Budgetary Planning and Responsibility Accounting

10 – 13

68. Management by exception

a. causes managers to be buried under voluminous paperwork.

b. means that all differences will be investigated.

c. means that only unfavorable differences will be investigated.

d. means that material differences will be investigated.

69. Under management by exception, which differences between planned and actual results

should be investigated?

a. Material and noncontrollable

b. Controllable and noncontrollable

c. Material and controllable

d. All differences should be investigated

70. Best Shingle’s budgeted manufacturing costs for 50,000 squares of shingles are:

Fixed manufacturing costs $12,000

Variable manufacturing costs $16.00 per square

Best produced 40,000 squares of shingles during March. How much are budgeted total

manufacturing costs in March?

a. $640,000

b. $812,000

c. $800,000

d. $652,000

71. A flexible budget depicted graphically

a. is identical to a CVP graph.

b. differs from a CVP graph in the way that fixed costs are shown.

c. differs from a CVP graph in the way that variable costs are shown.

d. differs from a CVP graph in that sales revenue is not shown.

72. The activity index used in preparing the flexible budget

a. is prescribed by generally accepted accounting principles.

b. is only applicable to fixed manufacturing costs.

c. is the same for all departments.

d. should significantly influence the costs that are being budgeted.

73. A static budget is not appropriate in evaluating a manager’s effectiveness if a company

has

a. substantial fixed costs.

b. substantial variable costs.

c. planned activity levels that match actual activity levels.

d. no variable costs.

Test Bank for Managerial Accounting, Seventh Edition

10 – 14

74. Shane Industries prepared a fixed budget of 60,000 direct labor hours, with estimated

overhead costs of $300,000 for variable overhead and $90,000 for fixed overhead. Shane

then prepared a flexible budget at 57,000 labor hours. How much is total overhead costs

at this level of activity?

a. $285,000

b. $375,000

c. $370,500

d. $390,000

75. For June, Gold Corp. estimated sales revenue at $600,000. It pays sales commissions

that are 4% of sales. The sales manager’s salary is $285,000, estimated shipping

expenses total 1% of sales, and miscellaneous selling expenses are $15,000. How much

are budgeted selling expenses for the month of July if sales are expected to be $540,000?

a. $42,000

b. $327,000

c. $27,000

d. $330,000

76. Nikoto Steel Co. budgeted manufacturing costs for 50,000 tons of steel are:

Fixed manufacturing costs $50,000 per month

Variable manufacturing costs $12.00 per ton of steel

Nikoto produced 40,000 tons of steel during March. How much is the flexible budget for

total manufacturing costs for March?

a. $520,000

b. $650,000

c. $480,000

d. $530,000

77. Smart Manufacturing budgeted costs for 50,000 linear feet of block are:

Fixed manufacturing costs $24,000 per month

Variable manufacturing costs $16.00 per linear foot

Smart installed 40,000 linear feet of block during March. How much is budgeted total

manufacturing costs in March?

a. $640,000

b. $824,000

c. $800,000

d. $664,000

Budgetary Planning and Responsibility Accounting

10 – 15

78. In the Dichter Co., indirect labor is budgeted for $72,000 and factory supervision is

budgeted for $24,000 at normal capacity of 160,000 direct labor hours. If 180,000 direct

labor hours are worked, flexible budget total for these costs is

a. $96,000.

b. $108,000.

c. $105,000.

d. $99,000.

79. Stone Industries uses flexible budgets. At normal capacity of 16,000 units, budgeted

manufacturing overhead is: $48,000 variable and $270,000 fixed. If Stone had actual

overhead costs of $321,000 for 18,000 units produced, what is the difference between

actual and budgeted costs?

a. $3,000 unfavorable

b. $3,000 favorable

c. $9,000 unfavorable

d. $12,000 favorable

80. A company’s planned activity level for next year is expected to be 100,000 machine hours.

At this level of activity, the company budgeted the following manufacturing overhead

costs:

Variable Fixed

Indirect materials $140,000 Depreciation $60,000

Indirect labor 200,000 Taxes 10,000

Factory supplies 20,000 Supervision 50,000

A flexible budget prepared at the 80,000 machine hours level of activity would show total

manufacturing overhead costs of

a. $288,000.

b. $360,000.

c. $384,000.

d. $408,000.

81. In the Goblette Manufacturing Company, indirect labor is budgeted for $108,000 and

factory supervision is budgeted for $36,000 at normal capacity of 160,000 direct labor

hours. If 180,000 direct labor hours are worked, flexible budget total for these costs is:

a. $144,000.

b. $162,000.

c. $157,500.

d. $148,500.

Test Bank for Managerial Accounting, Seventh Edition

10 – 16

82. Chambers, Inc. uses flexible budgets. At normal capacity of 16,000 units, budgeted

manufacturing overhead is: $64,000 variable and $180,000 fixed. If Chambers had actual

overhead costs of $250,000 for 18,000 units produced, what is the difference between

actual and budgeted costs?

a. $2,000 unfavorable.

b. $2,000 favorable.

c. $6,000 unfavorable.

d. $8,000 favorable.

83. A company’s planned activity level for next year is expected to be 100,000 machine hours.

At this level of activity, the company budgeted the following manufacturing overhead

costs:

Variable Fixed

Indirect materials $120,000 Depreciation $50,000

Indirect labor 160,000 Taxes 10,000

Factory supplies 20,000 Supervision 40,000

A flexible budget prepared at the 90,000 machine hours level of activity would show total

manufacturing overhead costs of

a. $270,000.

b. $360,000.

c. $370,000.

d. $300,000.

84. Kevin Jarvis Industries produced 192,000 units in 90,000 direct labor hours. Production for

the period was estimated at 198,000 units and 99,000 direct labor hours. A flexible budget

would compare budgeted costs and actual costs, respectively, at

a. 96,000 hours and 99,000 hours.

b. 99,000 hours and 90,000 hours.

c. 96,000 hours and 90,000 hours.

d. 90,000 hours and 90,000 hours.

85. A company’s planned activity level for next year is expected to be 100,000 machine hours.

At this level of activity, the company budgeted the following manufacturing overhead

costs:

Variable Fixed

Indirect materials $90,000 Depreciation $37,500

Indirect labor 120,000 Taxes 7,500

Factory supplies 15,000 Supervision 30,000

A flexible budget prepared at the 90,000 machine hours level of activity would show total

manufacturing overhead costs of

a. $202,500.

b. $270,000.

c. $277,500.

d. $225,000.

Budgetary Planning and Responsibility Accounting

10 – 17

86. Kathleen Corp. produced 320,000 units in 150,000 direct labor hours. Production for the

period was estimated at 330,000 units and 165,000 direct labor hours. A flexible budget

would compare budgeted costs and actual costs, respectively, at

a. 160,000 hours and 165,000 hours.

b. 165,000 hours and 150,000 hours.

c. 160,000 hours and 150,000 hours.

d. 150,000 hours and 150,000 hours.

87. At zero direct labor hours in a flexible budget graph, the total budgeted cost line intersects

the vertical axis at $30,000. At 15,000 direct labor hours, a horizontal line drawn from the

total budgeted cost line intersects the vertical axis at $90,000. Fixed and variable costs

may be expressed as:

a. $30,000 fixed plus $4 per direct labor hour variable.

b. $30,000 fixed plus $6 per direct labor hour variable.

c. $60,000 fixed plus $2 per direct labor hour variable.

d. $60,000 fixed plus $4 per direct labor hour variable.

88. At 18,000 direct labor hours, the flexible budget for indirect materials is $36,000. If

$37,400 are incurred at 18,400 direct labor hours, the flexible budget report should show

the following difference for indirect materials:

a. $1,400 unfavorable.

b. $1,400 favorable.

c. $600 favorable.

d. $600 unfavorable.

89. The accumulation of accounting data on the basis of the individual manager who has the

authority to make day-to-day decisions about activities in an area is called

a. static reporting.

b. flexible accounting.

c. responsibility accounting.

d. master budgeting.

90. Power Manufacturing recorded operating data for its shoe division for the year.

Sales $1,500,000

Contribution margin 300,000

Controllable fixed costs 180,000

Average total operating assets 600,000

How much is controllable margin for the year?

a. 20%

b. 50%

c. $300,000

d. $120,000

Test Bank for Managerial Accounting, Seventh Edition

10 – 18

91. A cost is considered controllable at a given level of managerial responsibility if

a. the manager has the power to incur the cost within a given time period.

b. the cost has not exceeded the budget amount in the master budget.

c. it is a variable cost, but it is uncontrollable if it is a fixed cost.

d. it changes in magnitude in a flexible budget.

92. As one moves up to each higher level of managerial responsibility,

a. fewer costs are controllable.

b. the responsibility for cost incurrence diminishes.

c. a greater number of costs are controllable.

d. performance evaluation becomes less important.

93. A responsibility report should

a. be prepared in accordance with generally accepted accounting principles.

b. show only those costs that a manager can control.

c. only show variable costs.

d. only be prepared at the highest level of managerial responsibility.

94. Top management can control

a. only controllable costs.

b. only noncontrollable costs.

c. all costs.

d. some noncontrollable costs and all controllable costs.

95. Not-for-profit entities

a. do not use responsibility accounting.

b. utilize responsibility accounting in trying to maximize net income.

c. utilize responsibility accounting in trying to minimize the cost of providing services.

d. have only noncontrollable costs.

96. Which of the following is not a true statement?

a. All costs are controllable at some level within a company.

b. Responsibility accounting applies to both profit and not-for-profit entities.

c. Fewer costs are controllable as one moves up to each higher level of managerial

responsibility.

d. The term segment is sometimes used to identify areas of responsibility in

decentralized operations.

97. Costs incurred indirectly and allocated to a responsibility level are considered to be

a. nonmaterial.

b. mixed.

c. controllable.

d. noncontrollable.

Budgetary Planning and Responsibility Accounting

10 – 19

98. Management by exception

a. is most effective at top levels of management.

b. can be implemented at each level of responsibility within an organization.

c. can only be applied when comparing actual results with the master budget.

d. is the opposite of goal congruence.

99. Which responsibility centers generate both revenues and costs?

a. Investment and profit centers

b. Profit and cost centers

c. Cost and investment centers

d. Only profit centers

100. The linens department of a large department store is

a. not a responsibility center.

b. a profit center.

c. a cost center.

d. an investment center.

101. The foreign subsidiary of a large corporation is

a. not a responsibility center.

b. a profit center.

c. a cost center.

d. an investment center.

102. The maintenance department of a manufacturing company is a(n)

a. segment.

b. profit center.

c. cost center.

d. investment center.

103. Which of the following is not a correct match?

1. Incurs costs

2. Generates revenue

3. Controls investment funds

a. Investment Center 1, 2, 3

b. Cost Center 1

c. Profit Center 1, 2, 3

d. All are correct matches.

Test Bank for Managerial Accounting, Seventh Edition

10 – 20

104. A cost center

a. only incurs costs and does not directly generate revenues.

b. incurs costs and generates revenues.

c. is a responsibility center of a company which incurs losses.

d. is a responsibility center which generates profits and evaluates the investment cost of

earning the profit.

105. A manager of a cost center is evaluated mainly on

a. the profit that the center generates.

b. his or her ability to control costs.

c. the amount of investment it takes to support the cost center.

d. the amount of revenue that can be generated.

106. Performance reports for cost centers compare actual

a. total costs with static budget data.

b. total costs with flexible budget data.

c. controllable costs with static budget data.

d. controllable costs with flexible budget data.

107. In the performance report for cost centers,

a. controllable and noncontrollable costs are reported.

b. fixed costs are not reported.

c. no distinction is made between fixed and variable costs.

d. only materials and controllable costs are reported.

108. Of the following choices, which contain both a traceable fixed cost and a common fixed

cost?

a. Profit center manager’s salary and timekeeping costs for a responsibility center’s

employees.

b. Company president’s salary and company personnel department costs.

c. Company personnel department costs and timekeeping costs for a responsibility

center’s employees.

d. Depreciation on a responsibility center’s equipment and supervisory salaries for the

center.

109. Which of the following is not an indirect fixed cost?

a. Company president’s salary

b. Depreciation on the company building housing several profit centers

c. Company personnel department costs

d. Profit center supervisory salaries

Budgetary Planning and Responsibility Accounting

10 – 21

110. A profit center is

a. a responsibility center that always reports a profit.

b. a responsibility center that incurs costs and generates revenues.

c. evaluated by the rate of return earned on the investment allocated to the center.

d. referred to as a loss center when operations do not meet the company’s objectives.

111. The best measure of the performance of the manager of a profit center is the

a. rate of return on investment.

b. success in meeting budgeted goals for controllable costs.

c. amount of controllable margin generated by the profit center.

d. amount of contribution margin generated by the profit center.

112. Controllable margin is defined as

a. sales minus variable costs.

b. sales minus contribution margin.

c. contribution margin less controllable fixed costs.

d. contribution margin less noncontrollable fixed costs.

113. Controllable margin is most useful for

a. external financial reporting.

b. preparing the master budget.

c. performance evaluation of profit centers.

d. break-even analysis.

114. Which of the following will not result in an unfavorable controllable margin difference?

a. Sales exceeding budget; costs under budget

b. Sales exceeding budget; costs over budget

c. Sales under budget; costs under budget

d. Sales under budget; costs over budget

115. Given below is an excerpt from a management performance report:

Budget Actual Difference

Contribution margin $1,000,000 $1,050,000 $50,000

Controllable fixed costs $ 500,000 $ 450,000 $50,000

The manager’s overall performance

a. is 20% below expectations.

b. is 20% above expectations.

c. is equal to expectations.

d. cannot be determined from information given.

Test Bank for Managerial Accounting, Seventh Edition

10 – 22

116. Which of the following are financial measures of performance?

1. Controllable margin

2. Product quality

3. Labor productivity

a. 1

b. 2

c. 3

d. 1 and 3

117. Given below is an excerpt from a management performance report:

Budget Actual Difference

Contribution margin $600,000 $580,000 $20,000 U

Controllable fixed costs $200,000 $220,000 $20,000 U

The manager’s overall performance

a. is 10% above expectations.

b. is 10% below expectations.

c. is equal to expectations.

d. cannot be determined from the information provided.

118. A responsibility report for a profit center will

a. not show controllable fixed costs.

b. not show indirect fixed costs.

c. show noncontrollable fixed costs.

d. not show cumulative year-to-date results.

119. The dollar amount of the controllable margin

a. is usually higher than the contribution margin.

b. is usually lower than the contribution margin.

c. is always equal to the contribution margin.

d. cannot be a negative figure.

120. Pippen Co. recorded operating data for its shoe division for the year. The company’s

desired return is 5%.

Sales $1,000,000

Contribution margin 200,000

Total direct fixed costs 120,000

Average total operating assets 400,000

Which one of the following reflects the controllable margin for the year?

a. 20%

b. 50%

c. $60,000

d. $80,000

Budgetary Planning and Responsibility Accounting

10 – 23

121. Las Sendas, Inc. had average operating assets of $4,000,000 and sales of $2,000,000 in

2016. If the controllable margin was $600,000, the ROI was

a. 60%

b. 50%

c. 30%

d. 15%

122. Trails and Paths, Inc. had average operating assets of $6,000,000 and sales of

$3,000,000 in 2016. If the controllable margin was $600,000, the ROI was

a. 50%

b. 40%

c. 20%

d. 10%

123. The area manager of the Red, White, and Brew Restaurants is considering two possible

expansion alternatives. The required investments, expected controllable margins, and the

ROIs of each are as follows:

Project Investment Controllable Margin ROI

Phoenix $120,000 $30,000 25%

Chicago $540,000 $50,000 9.25%

The Red, White, and Brew segment has currently $2,000,000 in invested capital and a

controllable margin of $250,000. Which one of following projects will increase the Red,

White, and Brew division’s ROI?

a. Both the Phoenix and Chicago options

b. Only the Phoenix option

c. Only the Chicago option

d. Neither the Phoenix nor the Chicago options

124. Bogey Co. recorded operating data for its Cheap division for the year. Bogey requires its

return to be 10%.

Sales $ 1,400,000

Controllable margin 160,000

Total average assets 4,000,000

Fixed costs 100,000

What is the ROI for the year?

a. 4%

b. 35%

c. 6%

d. 1.5%

Test Bank for Managerial Accounting, Seventh Edition

10 – 24

125. Dingo Division’s operating results include: controllable margin of $150,000, sales totaling

$1,200,000, and average operating assets of $500,000. Dingo is considering a project

with sales of $100,000, expenses of $86,000, and an investment of average operating

assets of $200,000. Dingo’s required rate of return is 9%. Should Dingo accept this

project?

a. Yes, ROI will drop by 6.6% which is still above the minimum required rate of return.

b. No, the return is less than the required rate of 9%.

c. Yes, ROI still exceeds the cost of capital.

d. No, ROI will decrease to 7%.

126. Grown Industries reported the following items for 2016:

Income tax expense $ 60,000

Contribution margin 200,000

Controllable fixed costs 80,000

Interest expense 40,000

Total operating assets 650,000

How much is controllable margin?

a. $200,000

b. $120,000

c. $60,000

d. $20,000

127. Griffin Corp. is evaluating its Piquette division, an investment center. The division has a

$60,000 controllable margin and $400,000 of sales. How much will Griffin’s average

operating assets be when its return on investment is 10%?

a. $600,000

b. $660,000

c. $400,000

d. $340,000

128. An investment center generated a contribution margin of $400,000, fixed costs of

$200,000 and sales of $2,000,000. The center’s average operating assets were $800,000.

How much is the return on investment?

a. 25%

b. 175%

c. 50%

d. 75%

Budgetary Planning and Responsibility Accounting

10 – 25

129. Rhein Manufacturing recorded operating data for its auto accessories division for the year.

Sales $750,000

Contribution margin 150,000

Total direct fixed costs 90,000

Average total operating assets 400,000

How much is ROI for the year if management is able to identify a way to improve the

contribution margin by $30,000, assuming fixed costs are held constant?

a. 45.0%

b. 22.5%

c. 15.0%

d. 12.0%

130. The current controllable margin for Henry Division is $93,000. Its current operating assets

are $300,000. The division is considering purchasing equipment for $90,000 that will

increase annual controllable margin by an estimated $15,000. If the equipment is

purchased, what will happen to the return on investment for Henry Division?

a. An increase of 16.1%

b. A decrease of 13.3%

c. A decrease of 3.3%

d. A decrease of 7.2%

131. Monte, Inc. recorded operating data for its Sandtrap division for the year. Monte requires

its return to be 9%.

Sales $1,000,000

Controllable margin 180,000

Total average assets 600,000

Fixed costs 60,000

How much is ROI for the year?

a. 10%

b. 17%

c. 20%

d. 30%

132. Betsy Union is the Pika Division manager and her performance is evaluated by executive

management based on Division ROI. The current controllable margin for Pika Division is

$46,000. Its current operating assets total $210,000. The division is considering

purchasing equipment for $40,000 that will increase sales by an estimated $10,000, with

annual depreciation of $10,000. If the equipment is purchased, what will happen to the

return on investment for the division?

a. An increase of 0.5%

b. A decrease of 0.5%

c. A decrease of 3.5%

d. It will remain unchanged.

Test Bank for Managerial Accounting, Seventh Edition

10 – 26

133. Benet Division of United Refinery Company’s operating results include: controllable

margin, $200,000; sales $2,200,000; and operating assets, $800,000. The Benet

Division’s ROI is 25%. Management is considering a project with sales of $100,000,

variable expenses of $60,000, fixed costs of $40,000; and an asset investment of

$150,000. Should management accept this new project?

a. No, since ROI will be lowered.

b. Yes, since ROI will increase.

c. Yes, since additional sales always mean more customers.

d. No, since a loss will be incurred.

134. The Fulmar Division of Jayne Manufacturing had an ROI of 25% when sales were $3 million

and controllable margin was $600,000. What were the average operating assets?

a. $150,000

b. $750,000

c. $2,400,000

d. $12,000

135. Naples, Inc. recorded operating data for its shoe division for the year.

Sales $750,000

Contribution margin 135,000

Total fixed costs 90,000

Average total operating assets 300,000

How much is ROI for the year if management is able to identify a way to improve the

contribution margin by $30,000, assuming fixed costs are held constant?

a. 25%

b. 18%

c. 45%

d. 12%

136. A distinguishing characteristic of an investment center is that

a. revenues are generated by selling and buying stocks and bonds.

b. interest revenue is the major source of revenues.

c. the profitability of the center is related to the funds invested in the center.

d. it is a responsibility center which only generates revenues.

137. A measure frequently used to evaluate the performance of the manager of an investment

center is

a. the amount of profit generated.

b. the rate of return on funds invested in the center.

c. the percentage increase in profit over the previous year.

d. departmental gross profit.

Budgetary Planning and Responsibility Accounting

10 – 27

138. Return on investment is calculated by dividing

a. contribution margin by sales.

b. controllable margin by sales.

c. contribution margin by average operating assets.

d. controllable margin by average operating assets.

139. Which one of the following will not increase return on investment?

a. Variable costs are increased

b. An increase in sales

c. Average operating assets are decreased

d. Variable costs are decreased

140. If an investment center has generated a controllable margin of $150,000 and sales of

$600,000, what is the return on investment for the investment center if average operating

assets were $1,000,000 during the period?

a. 15%

b. 25%

c. 45%

d. 60%

141. Which statement is true?

a. An investment center is responsible for revenues and expenses, as well as earning a

return on assets.

b. An investment center is only responsible for its investments.

c. An investment center is only responsible for revenues and expenses.

d. A profit center is evaluated using contribution margin, while an investment center is

evaluated using ROI.

142. The denominator in the formula for return on investment calculation is

a. investment center controllable margin.

b. dependent on the specific type of profit center.

c. investment center average operating assets.

d. sales for the period.

143. In the formula for ROI, idle plant assets are

a. included in the calculation of controllable margin.

b. included in the calculation of operating assets.

c. excluded in the calculation of operating assets.

d. excluded from total assets.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 28

144. In computing ROI, land held for future use

a. will hurt the performance measurement of an investment center’s manager.

b. is important in evaluating the performance of a profit center manager.

c. is included in the calculation of operating assets.

d. is considered a nonoperating asset.

145. Le Sud Retailers has a current return on investment of 10% and the company has

established an 8% minimum rate of return for the division. The division manager has two

investment projects available, for which the following estimates have been made:

Project A – Annual controllable margin = $24,000, operating assets = $400,000

Project B – Annual controllable margin = $60,000, operating assets = $550,000

Which project should be funded?

a. Both projects

b. Project A

c. Project B

d. Neither project

146. If an investment center has a $90,000 controllable margin and $1,200,000 of sales, what

average operating assets are needed to have a return on investment of 10%?

a. $120,000

b. $210,000

c. $900,000

d. $1,200,000

147. Which of the following valuations of operating assets is not readily available from the

accounting records?

a. Cost

b. Book value

c. Market value

d. Both cost and market value

a148. The following information is available for Halle Department Stores:

Average operating assets $600,000

Controllable margin 60,000

Contribution margin 150,000

Minimum rate of return 8%

How much is Halle’s residual income?

a. $102,000

b. $540,000

c. $12,000

d. $48,000

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 29

a149. What is the goal of residual income?

a. To maximize the amount of costs which are controllable

b. To maximize profits

c. To maximize the total amount of residual income

d. To maximize controllable margin

a150. Which one of the following is a correct statement about residual income?

a. Its goal is to maximize profits of an investment center.

b. It is less effective for evaluating investment centers than ROI.

c. It is the ratio of controllable margin to the minimum rate of return on average operating

assets.

d. It evaluates performance by comparing the return of an investment center with the

company’s minimum rate of return.

a151. Which one of the following does not impact the amount of residual income?

a. Contribution margin

b. Net income

c. Sales

d. Controllable costs

a152. For what purpose do companies calculate residual income?

a. To determine whether decentralization is possible or not

b. To motivate managers through possible termination

c. To evaluate management performance

d. To measure company profits

a153. Lew Co. had sales of $400,000, variable costs of $200,000, and direct fixed costs totaling

$100,000. The company’s operating assets total $800,000, and its required return is 10%.

How much is the residual income?

a. $120,000

b. $20,000

c. $80,000

d. $320,000

a154. Quincy Corp. earned controllable margin of $500,000 on sales of $6,400,000. The division

had average operating assets of $5,200,000. The company requires a return on

investment of at least 8%. How much is residual income?

a. $416,000

b. $84,000

c. $584,000

d. $512,000

Test Bank for Managerial Accounting, Seventh Edition

10 – 30

a155. The performance of the manager of Ottawa Division is measured by residual income.

Which of the following would decrease the manager’s performance measure?

a. Decrease in required rate of return

b. Increase in amount of return on investment desired

c. Increase in sales

d. Increase in contribution margin

156. Which of the following would not be considered an aspect of budgetary control?

a. It assists in the determination of differences between actual and planned results.

b. It provides feedback value needed by management to see whether actual operations

are on course.

c. It assists management in controlling operations.

d. It provides a guarantee for favorable results.

157. A static budget is usually appropriate in evaluating a manager’s effectiveness in

controlling

a. fixed manufacturing costs and fixed selling and administrative expenses.

b. variable manufacturing costs and variable selling and administrative expenses.

c. fixed manufacturing costs and variable selling and administrative expenses.

d. variable manufacturing costs and fixed selling and administrative expenses.

158. A static budget report is appropriate for

a. only fixed manufacturing costs.

b. only fixed selling and administrative expenses.

c. variable selling and administrative expenses.

d. both fixed manufacturing costs and fixed selling and administrative expenses.

159. Sydney, Inc. uses flexible budgets. At normal capacity of 16,000 units, budgeted

manufacturing overhead is $128,000 variable and $360,000 fixed. If Sydney had actual

overhead costs of $500,000 for 18,000 units produced, what is the difference between

actual and budgeted costs?

a. $4,000 unfavorable

b. $4,000 favorable

c. $12,000 unfavorable

d. $16,000 favorable

160. To develop the flexible budget, management takes all of the following steps except

identify the

a. activity index and the relevant range of activity.

b. variable costs and determine the budgeted variable cost per unit.

c. fixed costs and determine the budgeted fixed cost per unit.

d. All of these options are steps in developing the flexible budget.

Budgetary Planning and Responsibility Accounting

10 – 31

161. A flexible budget is appropriate for

Direct Labor Costs Manufacturing Overhead Costs

a. No No

b. Yes Yes

c. Yes No

d. No Yes

162. All of the following statements are correct about management by exception except it

a. enables top management to focus on problem areas that need attention.

b. means that management has to investigate every budget difference.

c. requires that there must be some guidelines for identifying an exception.

d. means that top management’s review of a budget report is focused primarily on

differences between actual results and planned objectives.

163. Controllable costs for responsibility accounting purposes are those costs that are directly

influenced by

a. a given manager within a given period of time.

b. a change in activity.

c. production volume.

d. sales volume.

164. All of the following statements are correct about controllable costs except

a. all costs are controllable at some level of responsibility within a company.

b. all costs are controllable by top management.

c. fewer costs are controllable as one moves up to each higher level of managerial

responsibility.

d. costs incurred directly by a level of responsibility are controllable at that level.

165. Which of the following will cause an increase in ROI?

a. An increase in variable costs

b. An increase in average operating assets

c. An increase in sales

d. An increase in controllable fixed costs

166. Costs that relate specifically to one center and are incurred for the sole benefit of that

center are

a. common fixed costs.

b. direct fixed costs.

c. indirect fixed costs.

d. noncontrollable fixed costs.

Test Bank for Managerial Accounting, Seventh Edition

10 – 32

167. If controllable margin is $300,000 and the average investment center operating assets are

$2,000,000, the return on investment is

a. .67%.

b. 6.66%.

c. 20%.

d. 15%.

Answers to Multiple Choice Questions

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

BRIEF EXERCISES

BE 168

Devlin Manufacturing makes a single product. Expected manufacturing costs are as follows:

Variable costs

Direct materials $6.50 per unit

Direct labor 2.40 per unit

Manufacturing overhead 1.10 per unit

Fixed costs per month

Supervisory salaries $13,600

Depreciation 5,500

Other fixed costs 2,200

Instructions

Determine the amount of manufacturing costs for a flexible budget level of 3,200 units per month.

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 33

Solution 168 (4 min.)

BE 169

Wind Productions uses flexible budgets. Items from the budget for March in which 3,000 units

were produced and sold appear below:

Direct materials $18,000

Indirect materials – variable 2,000

Supervisor salaries 15,000

Depreciation on factory equipment 4,000

Direct labor 10,000

Property taxes on factory 1,000

Instructions

If Wind prepares a flexible budget at 4,000 units, compute its total variable cost.

BE 170

Cyber Construction’s manufacturing costs for August when production was 1,000 units appear

below:

Direct material $12 per unit

Direct labor $7,500

Variable overhead 6,000

Factory depreciation 9,000

Factory supervisory salaries 7,800

Other fixed factory costs 2,500

Instructions

Compute the flexible budget manufacturing cost amount for a month when 900 units are

produced.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 34

BE 171

Micro Miller Company’s budgeted sales for April were estimated at $700,000, sales commissions

at 4% of sales, and the sales manager’s salary at $80,000. Shipping expenses were estimated at

1% of sales and miscellaneous selling expenses were estimated at $1,000, plus 0.5% of sales.

Instructions

Determine the budgeted selling expenses on a flexible budget for April.

BE 172

Point, Inc. produces men’s shirts. The following budgeted and actual amounts are for 2016:

Cost Budget at 2,500 units Actual Amounts at 2,800 units

Direct materials $65,000 $75,000

Direct labor 70,000 78,000

Fixed overhead 35,000 34,500

Instructions

Prepare a performance report for Point, Inc. for the year.

BE 173

Moss Corp. reported the following items for 2016:

Controllable fixed costs $ 77,000

Contribution margin 122,000

Interest expense 20,000

Variable costs 80,000

Total assets $925,000

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 35

BE 173 (Cont.)

Instructions

Compute the controllable margin for 2016.

BE 174

The data for an investment center is given below.

January 1, 2016 December 31, 2016

Current Assets $ 400,000 $ 800,000

Plant Assets 3,000,000 3,800,000

The controllable margin is $440,000.

Instructions

Compute the return on investment for the center for 2016.

BE 175

Data for the Deluxe Division of Park Industries which is operated as an investment center follows:

Sales $6,000,000

Contribution Margin 800,000

Controllable Fixed Costs 440,000

Return on Investment 12%

Instructions

Calculate controllable margin and average operating assets.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 36

BE 176

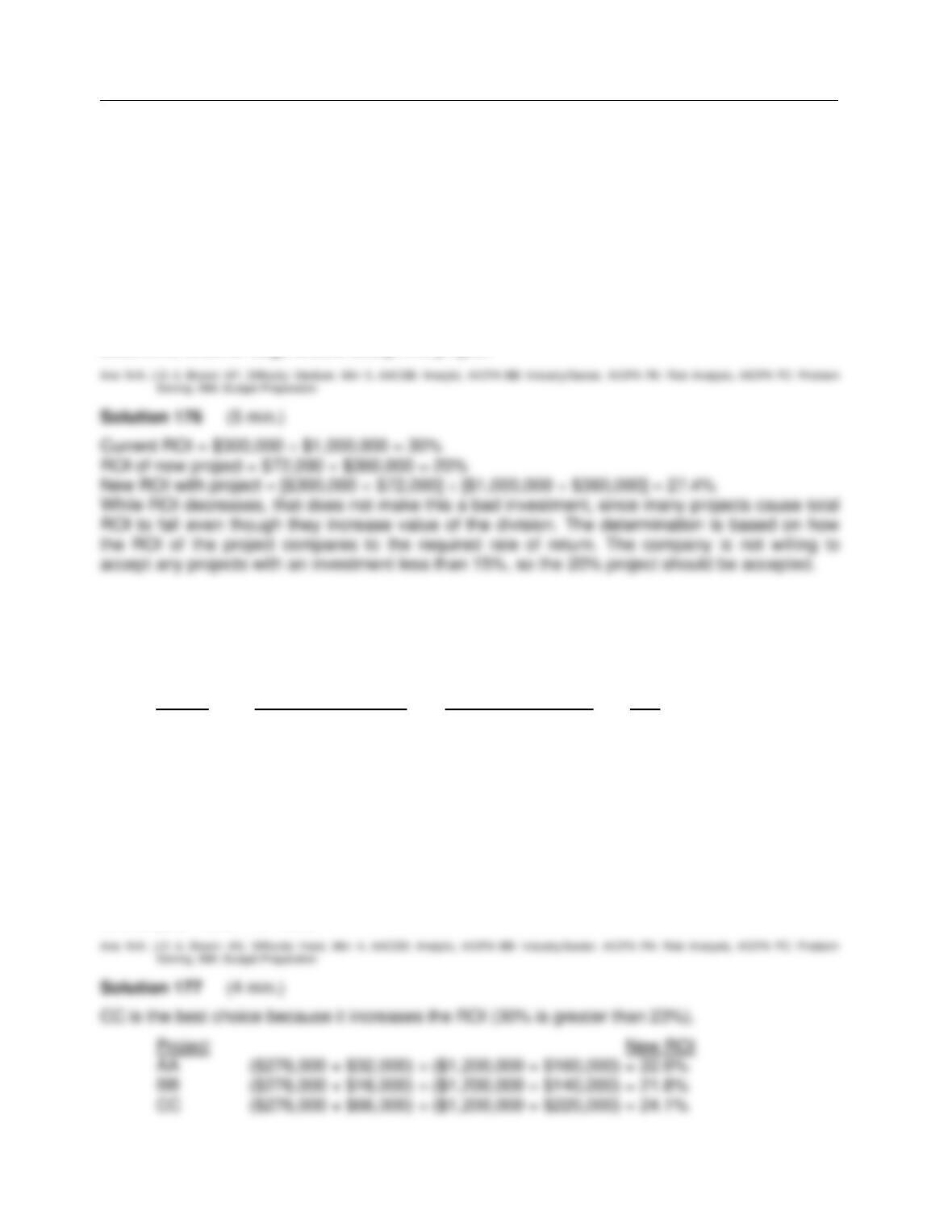

Sage Division’s operating results include:

• Controllable margin, $300,000

• Sales revenue, $2,400,000

• Operating assets, $1,000,000

Sage is considering a project with sales of $240,000, expenses of $168,000, and an investment

of $360,000. Sage’s required rate of return is 15%.

Instructions

Determine whether Sage should accept this project.

BE 177

An investment center manager is considering three possible investments. The company’s

required return is 10%. The required asset investment, controllable margins, and the ROIs of

each investment are as follows:

Project Average Investment Controllable Margin ROI

AA $160,000 $32,000 20.0%

BB 140,000 16,000 11.4%

CC 220,000 66,000 30%

The investment center is currently generating an ROI of 23% based on $1,200,000 in operating

assets and a controllable margin of $276,000.

Instructions

If the manager can select only one project, determine which one is the best choice to increase the

investment center’s ROI. Compute how much the investment center’s ROI will be if the manager

selects your recommendation.

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 37

aBE 178

The owner of Denver Toy Manufacturing Company has recently expanded his business in order

to add an additional product line. In addition to toys, the company now sells shirts. The company

has a minimum rate of return of 11%.

Toys Shirts

Sales $600,000 $200,000

Controllable margin 120,000 10,000

Average operating assets 900,000 200,000

Instructions

Compute the residual income for both investment centers.

aBE 179

Floors Direct has 4 divisions. Its hardwood flooring division’s information follows for 2013:

Sales $4,000,000

Controllable margin 250,000

Variable costs 60,000

Average operating assets 1,800,000

Instructions

Floor’s required rate of return is 10%. How much is its residual income?

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 38

EXERCISES

Ex. 180

Clark Company’s master budget reflects budgeted sales information for the month of June, 2016,

as follows:

Budgeted Quantity Budgeted Unit Sales Price

Product A 40,000 $7

Product B 48,000 $9

During June, the company actually sold 39,000 units of Product A at an average unit price of

$7.10 and 49,600 units of Product B at an average unit price of $8.90.

Instructions

Prepare a Sales Budget Report for the month of June for Clark Company which shows whether

the company achieved its planned objectives.

Ex. 181

Beal Manufacturing Co.’s static budget at 12,000 units of production includes $72,000 for direct

labor and $12,000 for direct materials. Total fixed costs are $48,000.

Instructions

a. Determine how much would appear on Beal’s flexible budget for 2016 if 18,000 units are

produced and sold.

b. How would this comparison differ if a static budget were used instead of a flexible budget for

performance evaluation?

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 39

Ex. 182

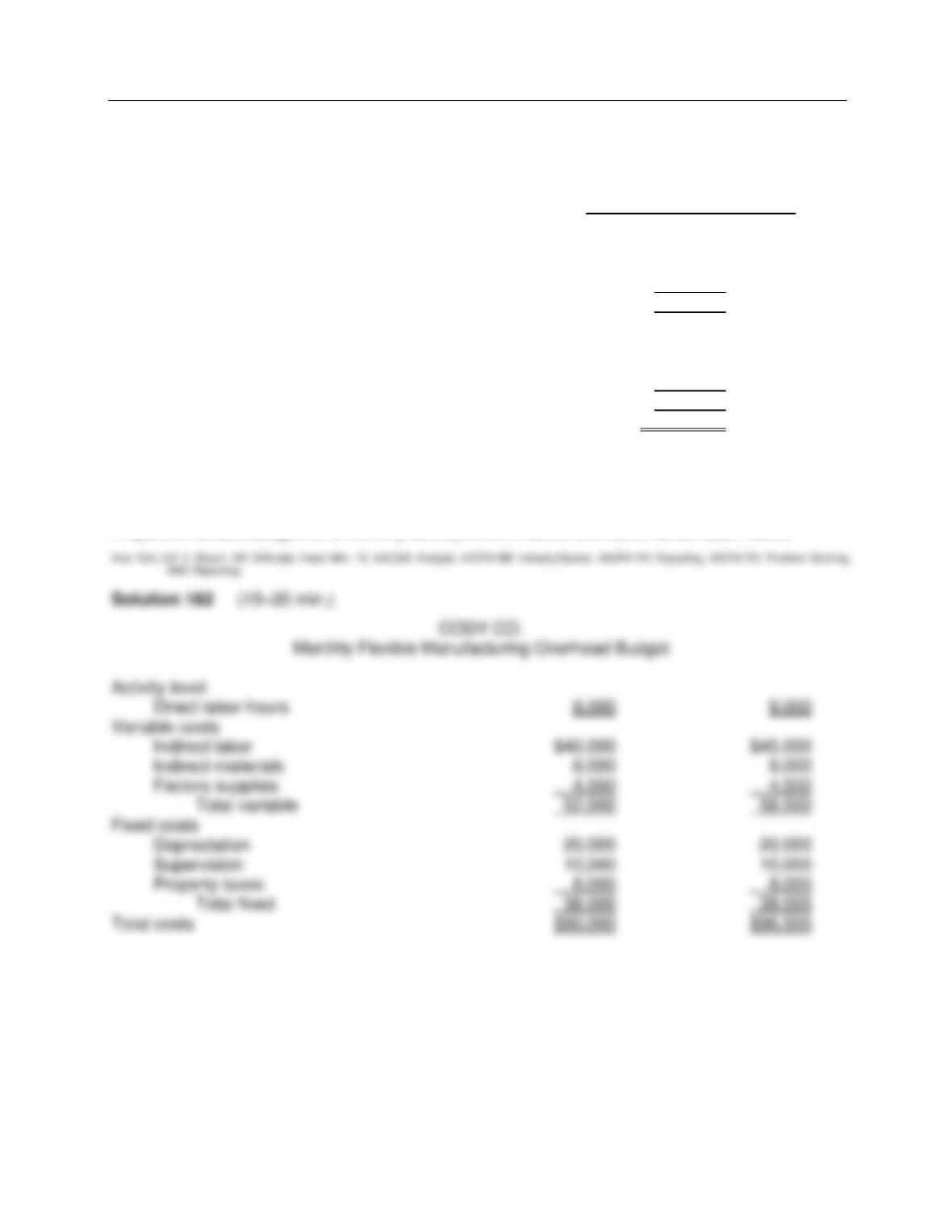

Cody Co. developed its annual manufacturing overhead budget for its master budget for 2016 as

follows:

Expected annual operating capacity 120,000 Direct Labor Hours

Variable overhead costs

Indirect labor $600,000

Indirect materials 120,000

Factory supplies 60,000

Total variable 780,000

Fixed overhead costs

Depreciation 240,000

Supervision 120,000

Property taxes 96,000

Total fixed 456,000

Total costs $1,236,000

The relevant range for monthly activity is expected to be between 8,000 and 12,000 direct labor

hours.

Instructions

Prepare a flexible budget for a monthly activity level of 8,000 and 9,000 direct labor hours.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 40

Ex. 183

Copper Manufacturing has prepared the following monthly flexible manufacturing overhead

budget for its Mixing Department:

COPPER MANUFACTURING

Monthly Flexible Manufacturing Overhead Budget

Mixing Department

Activity level

Direct labor hours 3,000 4,000

Variable costs

Indirect materials $ 3,000 $ 4,000

Indirect labor 15,000 20,000

Factory supplies 4,500 6,000

Total variable 22,500 30,000

Fixed costs

Depreciation 20,000 20,000

Supervision 12,000 12,000

Property taxes 15,000 15,000

Total fixed 47,000 47,000

Total costs $69,500 $77,000

Instructions

Prepare a flexible budget at the 5,000 direct labor hours of activity.

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 41

Ex. 184

Berne, Inc. uses a flexible budget for manufacturing overhead based on machine hours. Variable

manufacturing overhead costs per machine hour are as follows:

Indirect labor $5.00

Indirect materials 2.50

Maintenance .80

Utilities .30

Fixed overhead costs per month are:

Supervision $800

Insurance 200

Property taxes 300

Depreciation 900

The company believes it will normally operate in a range of 2,000 to 4,000 machine hours per

month.

Instructions

Prepare a flexible manufacturing overhead budget for the expected range of activity, using

increments of 1,000 machine hours.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 42

Ex. 185

Telemark Production’s manufacturing costs for July when production was 2,000 units appears

below: Direct materials $10 per unit

Factory depreciation $16,000

Variable overhead 10,000

Direct labor 4,000

Factory supervisory salaries 11,600

Other fixed factory costs 3,000

Instructions

How much is the flexible budget manufacturing cost amount for a month when 2,200 units are

produced?

Ex. 186

Webb, Inc. uses a flexible budget for manufacturing overhead based on machine hours. Variable

manufacturing overhead costs per machine hour are as follows:

Indirect labor $5.00

Indirect materials 2.50

Maintenance .50

Utilities .30

Fixed overhead costs per month are:

Supervision $1,200

Insurance 400

Property taxes 600

Depreciation 1,800

The company believes it will normally operate in a range of 4,000 to 8,000 machine hours per

month. During the month of August, 2016, the company incurs the following manufacturing

overhead costs:

Indirect labor $28,000

Indirect materials 16,200

Maintenance 2,800

Utilities 1,900

Supervision 1,440

Insurance 400

Property taxes 600

Depreciation 1,860

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 43

Ex. 186 (Cont.)

Instructions

Prepare a flexible budget report, assuming that the company used 6,000 machine hours during

August.

Ex. 187

Lapp Manufacturing uses flexible budgets to control its selling expenses. Monthly sales are

expected to be from $400,000 to $480,000. Variable costs and their percentage relationships to

sales are:

Sales commissions 6%

Advertising 4%

Traveling 5%

Delivery 1%

Fixed selling expenses consist of sales salaries $80,000 and depreciation on delivery equipment

$20,000.

Instructions

Prepare a flexible budget for increments of $40,000 of sales within the relevant range.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

10 – 44

Solution 187 (17–22 min.)

Ex. 188

Cadiz Co. uses flexible budgets to control its selling expenses. Monthly sales are expected to be

from $300,000 to $360,000. Variable costs and their percentage relationships to sales are:

Sales commissions 5%

Advertising 4%

Traveling 7%

Delivery 1%

Fixed selling expenses consist of sales salaries $40,000 and depreciation on delivery equipment

$10,000.

The actual selling expenses incurred in February, 2016, by Cadiz are as follows:

Sales commissions $17,200

Advertising 12,000

Traveling 23,700

Delivery 2,400

Fixed selling expenses consist of sales salaries $41,500 and depreciation on delivery equipment

$10,000.

Instructions

Prepare a flexible budget performance report, assuming that February sales were $330,000.

Budgetary Planning and Responsibility Accounting

FOR INSTRUCTOR USE ONLY

10 – 45

Solution 188 (17–22 min.)

Ex. 189

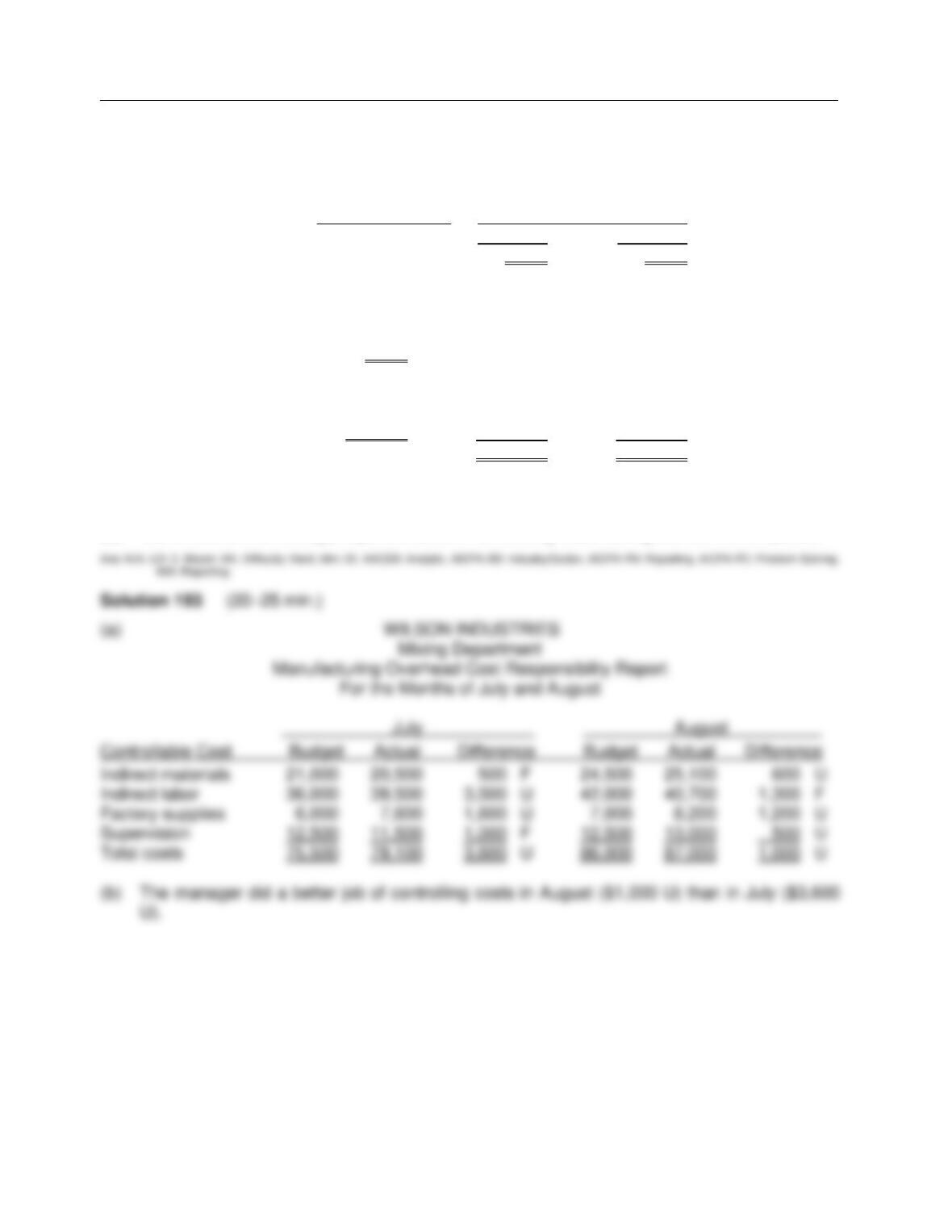

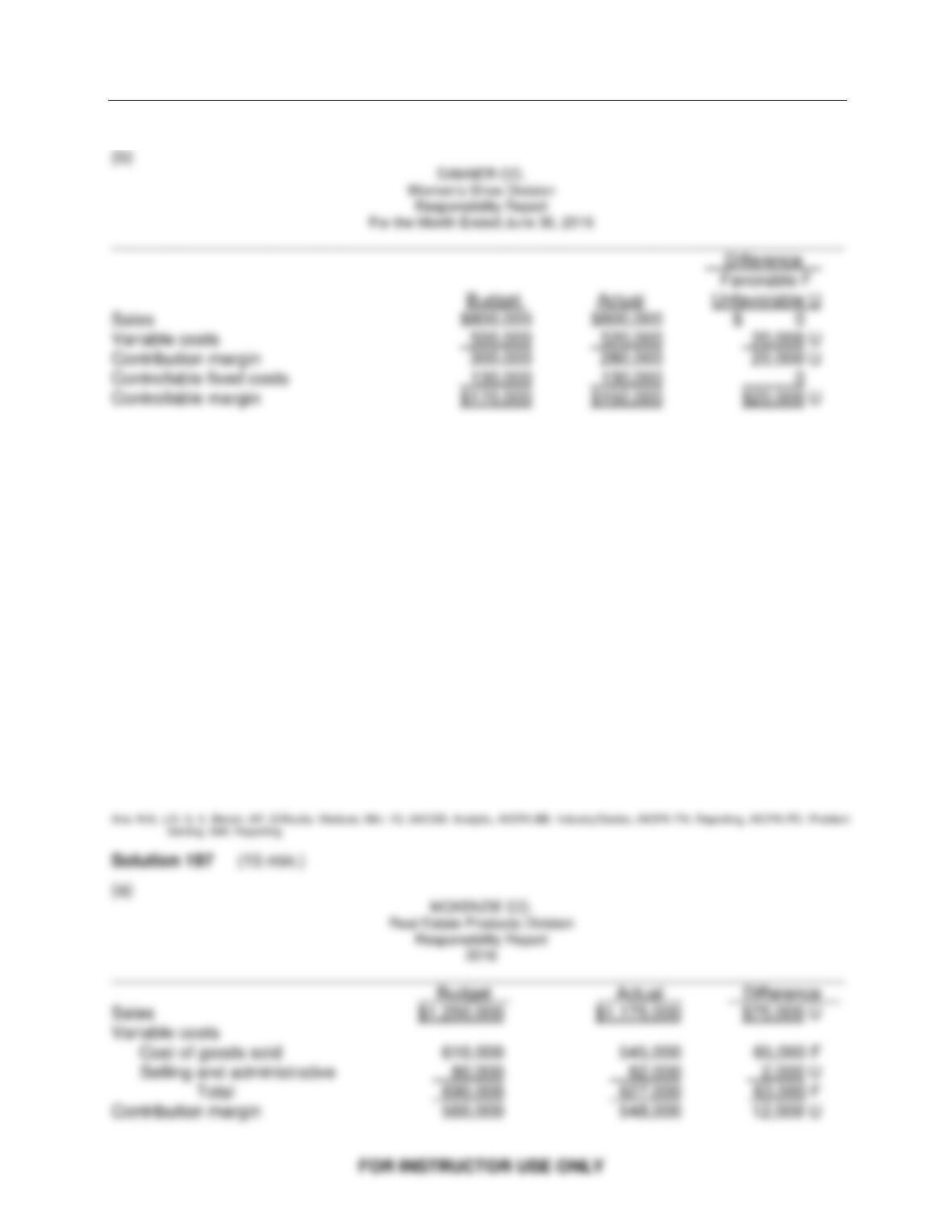

A flexible budget graph for the Assembly Department shows the following:

1. At zero direct labor hours, the total budgeted cost line intersects the vertical axis at $120,000.

2. At normal capacity of 50,000 direct labor hours, the line drawn from the total budgeted cost

line intersects the vertical axis at $360,000.

Instructions

Develop the budgeted cost formula for the Assembly Department and identify the fixed and

variable costs.

Ex. 190

Ace Production Co. has two production departments, Fabricating and Assembling. At a

department managers’ meeting, the controller uses flexible budget graphs to explain total

budgeted costs. Separate graphs based on direct labor hours are used for each department. The

graphs show the following.