94)

If the painting firms in a city sign a contract outlining a pricing plan, they are involved in

94)

A)

a legal form of business contract in the United States.

B)

price competition.

C)

price regulation.

D)

collusion.

95)

Consumers benefit from monopolistic competition by

95)

A)

being able to choose from products more closely suited to their tastes.

B)

being able to purchase high quality products at low prices.

C)

paying the same price as everyone else.

D)

paying the lowest possible price for the monopolistically competitive firm’s product.

A

96)

A prisoners’ dilemma is a

96)

A)

game that involves no dominant strategies.

B)

game in which players act in rational, self–interested ways that leave everyone worse off.

C)

game in which players collude to outfox authorities.

D)

game in which prisoners are stumped because they cannot communicate with each other.

B

97)

Which of the following is important in determining the extent of competition in an industry?

97)

A)

whether or not an industry’s product is differentiated or standardized

B)

the minimum level of the short–run average total cost of production

C)

the level of market demand for the industry’s product

D)

the minimum efficient scale of production relative to market demand

D

D

98)

A set of actions that a firm takes to achieve a goal, such as maximizing profits, is called

98)

A)

a business strategy.

B)

game theory.

C)

a payoff matrix.

D)

the Porter’s Competitive Forces plan.

99)

Patents, tariffs and quotas are all examples of

99)

A)

barriers to entry that protect consumers.

B)

key inputs.

C)

economic regulations that increase efficiency.

D)

government–imposed barriers to entry.

100)

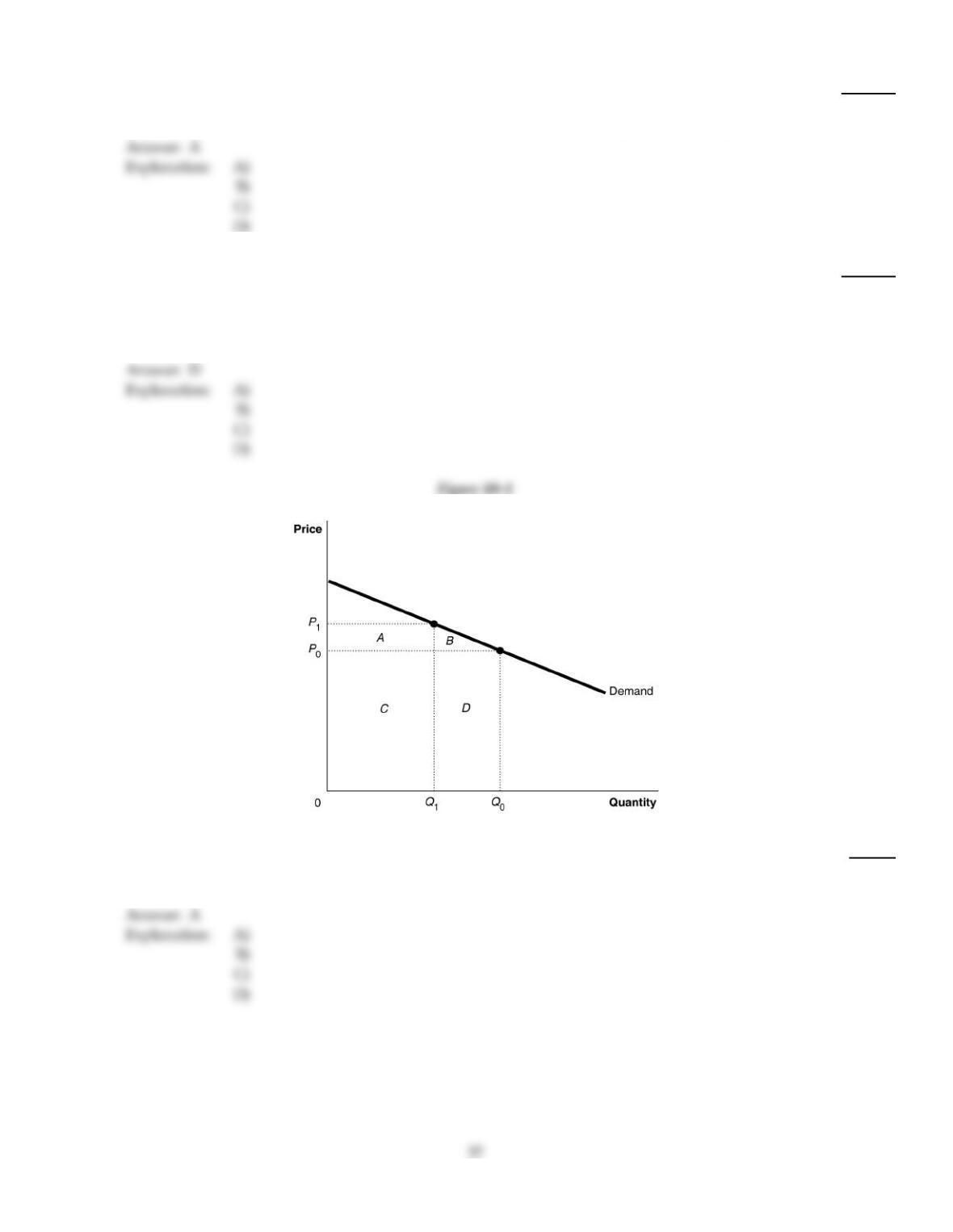

Refer to Figure 10–1. The marginal revenue from an increase in price from P0 to P1 equals

100)

A)

the area (A–D).

B)

the area (C–B).

C)

the area A.

D)

the area (B+D–A)

101)

All of the following are characteristics of game theory except

101)

A)

rules that determine what actions are allowable.

B)

strategies that players employ to attain their objectives.

C)

payoffs that are the results of the interaction among players‘ strategies.

D)

independence among players

102)

Suppose we want to use game theory to analyze how an oligopolist selects its optimal price.

The cells of the payoff matrix show

102)

A)

the profit that each producer can expect to earn from every combination of strategies by the

firms in the market.

B)

the expected profits of rival firms.

C)

the profit that each producer can expect to earn by pursuing a single strategy.

D)

the strategy that a firm must pursue to earn various levels of profit.

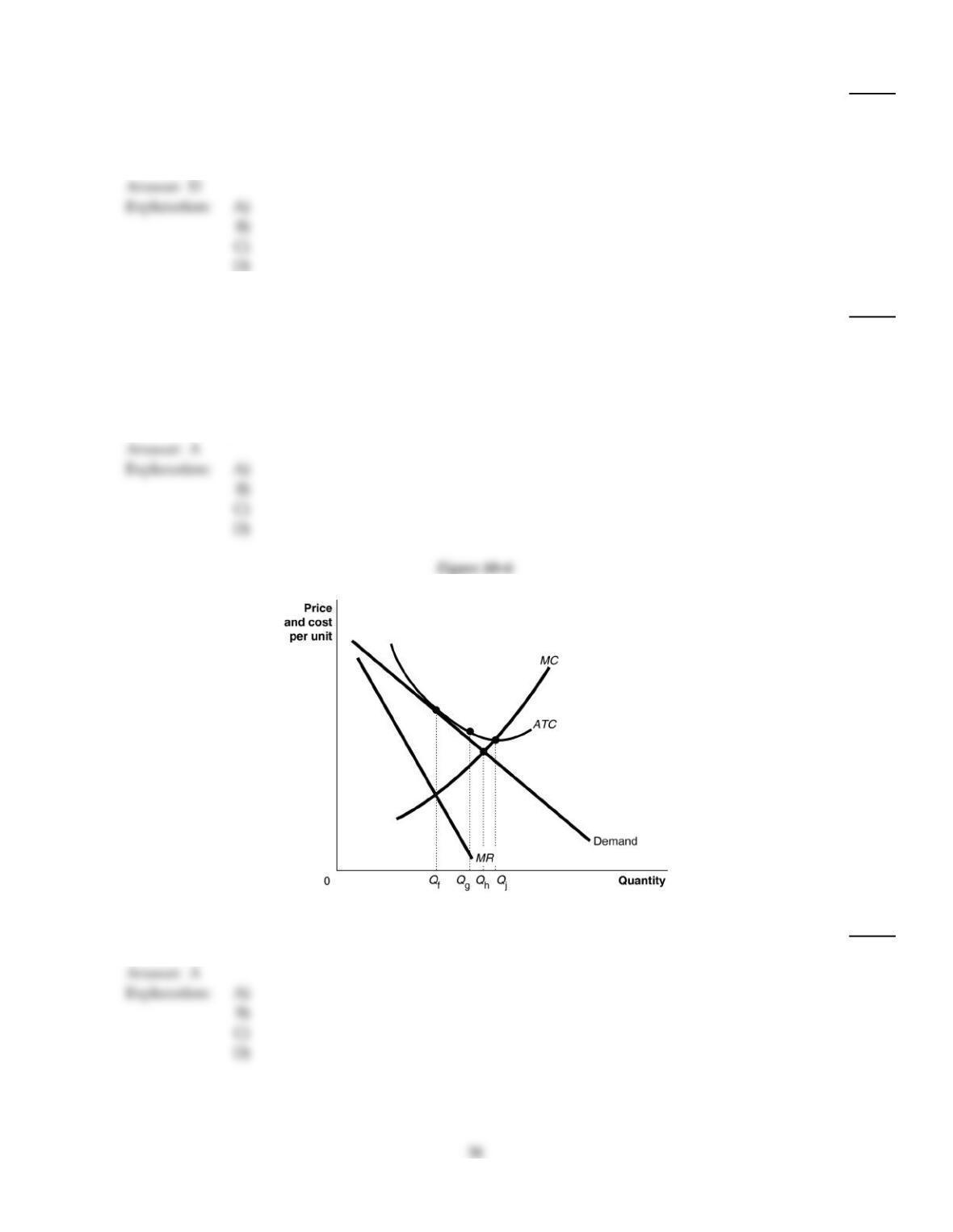

103)

Refer to Figure 10–6. What is this monopolistically competitive firm’s profit–maximizing output?

103)

A)

Qf units

B)

Qg units

C)

Qh units

D)

Qi units

104)

In the short run if price is less than average cost

104)

A)

the market must be in long–run equilibrium.

B)

there is no incentive for the number of firms in the market to change.

C)

there is an incentive for firms to enter the market.

D)

there is an incentive for firms to exit a market.

105)

For productive efficiency to hold

105)

A)

price must equal the marginal cost of the last unit produced.

B)

average variable cost must be minimized.

C)

firms must produce at the minimum point of their average total cost curves.

D)

price must equal marginal revenue of the last unit sold.

C

106)

Which of the following characteristics is not common to monopolistic competition and perfect

competition?

106)

A)

All firms sell identical products.

B)

Average revenue is equal to price.

C)

There are low barriers to entry to new firms entering the industry.

D)

There are many firms.

A

107)

If a typical monopolistically competitive firm is making short run losses then

107)

A)

other more competitive firms will enter the market.

B)

the industry will eventually cease to exist.

C)

as some firms leave, the demand for the products of the remaining firms will become more

elastic.

D)

as some firms leave, the remaining firms will experience an increase in the demand for their

products.

D

D

108)

If a monopolistically competitive firm breaks even the firm

108)

A)

should expand production.

B)

is earning zero accounting and zero economic profit.

C)

should advertise its product to stimulate demand.

D)

is earning an accounting profit and will have to pay taxes on that profit.

109)

In monopolistic competition there

109)

A)

are many sellers who each face a perfectly elastic demand curve.

B)

are many sellers who each face a downward–sloping demand curve.

C)

is only one seller who faces a downward–sloping demand curve.

D)

are a few sellers who each face a downward–sloping demand curve.

110)

A member of a cartel like OPEC has an incentive to

110)

A)

support equal production quotas for each member.

B)

abide by its individual production quota.

C)

agree to a low production quota and then produce more than its quota.

D)

argue for larger production quotas for each member of the cartel.

111)

Which of the following characteristics is common to monopolistic competition and perfect

competition?

111)

A)

Each firm faces a downward–sloping demand curve.

B)

Firms are price takers.

C)

Firms produce identical products.

D)

Entry barriers into the industry are low.

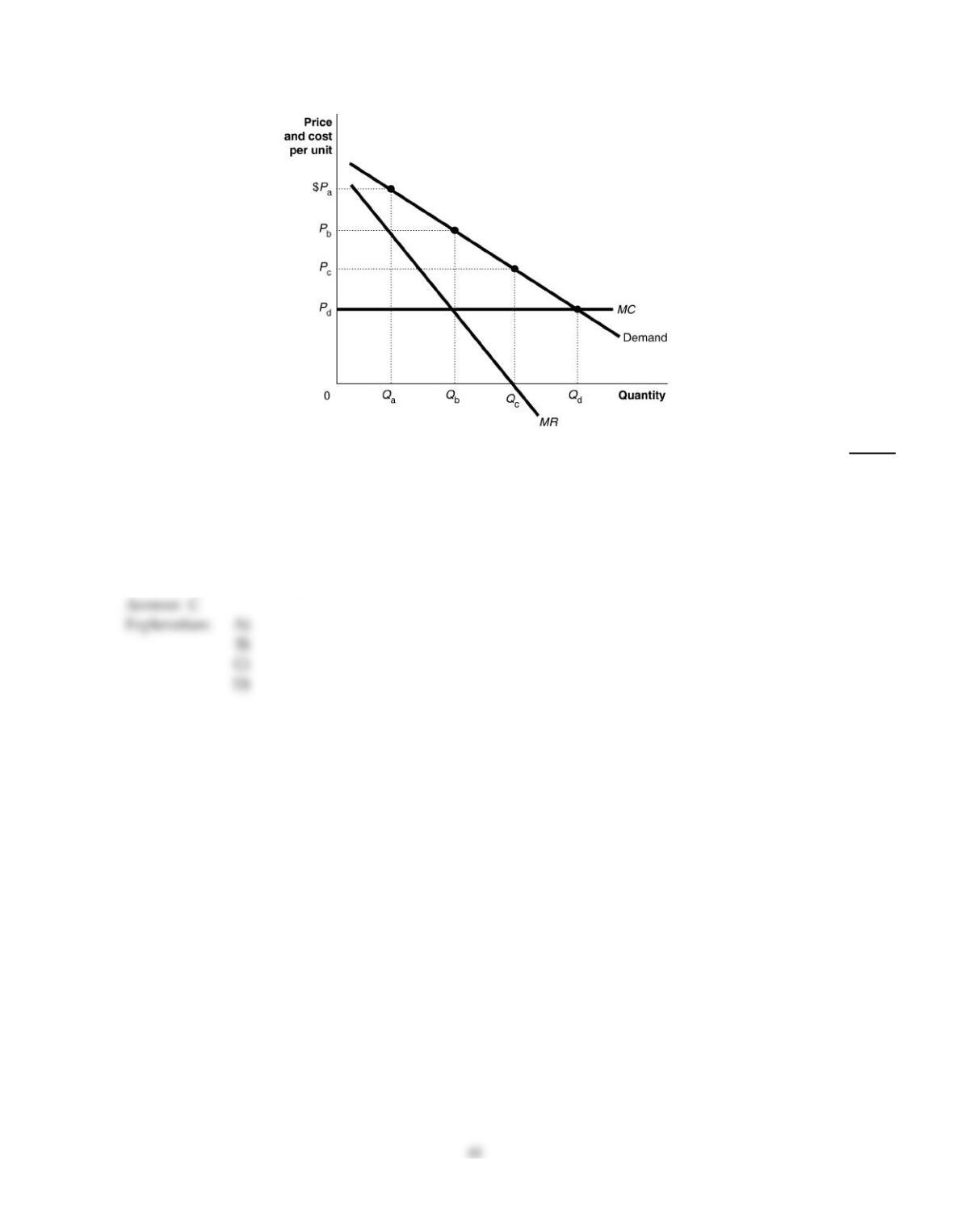

Figure 10–4

112)

Refer to Figure 10–4. The firm represented in the diagram is currently selling Qa units at a price of

$Pa. Is this firm maximizing its profit? If not, what should the firm do to maximize profit?

112)

A)

No, it is not; it should lower its price to Pc and sell Qc units.

B)

No, it is not; since its marginal cost is constant, it should produce and sell as much as it can. It

should sell Qd units at a price of Pd.

C)

No, it is not; it should lower its price to Pb and sell Qb units.

D)

Yes, it is maximizing its profit by charging the highest price possible.

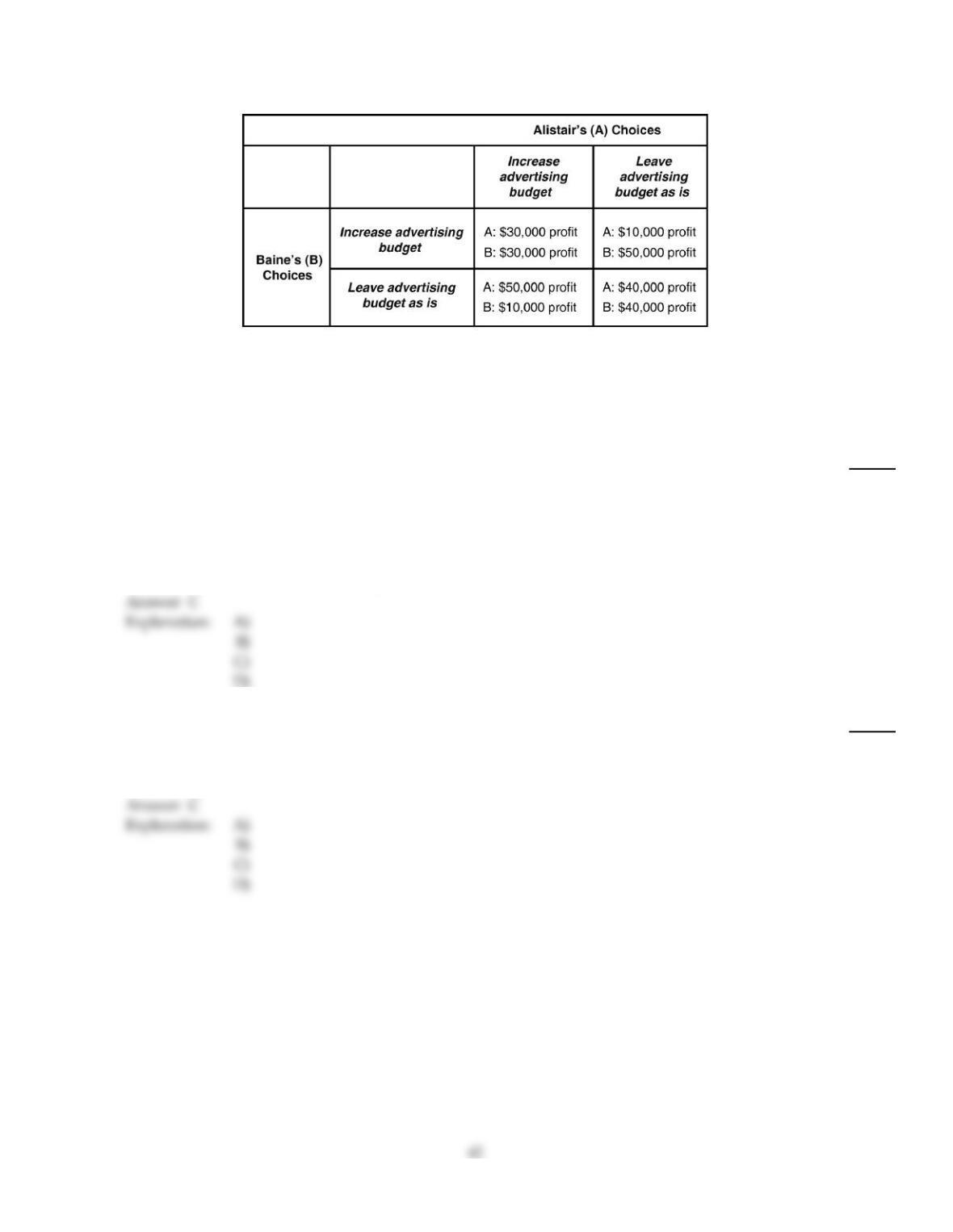

Table 10–4

Alistair Luggage and Baine Baggage are the only firms with similar products in the upscale town of Montecito. Each firm

must decide on whether to increase its advertising budget to compete for customers. If one firm increases its advertising

budget but the other does not, then the firm with the higher advertising budget will increase its profit. Table 10–4 shows the

payoff matrix for this advertising game.

113)

Refer to Table 10–4. Does Alistair have a dominant strategy and if so, what is it?

113)

A)

Yes, Alistair should keep its advertising budget as is.

B)

There are two dominant strategies: if Baine increases its advertising budget, then Alistair’s

best bet is to keep its budget the same but if Baine does not increase its spending then Alistair

should raise its advertising budget

C)

Yes, Alistair should increase its advertising budget.

D)

No, there is no dominant strategy.

114)

When a monopolistically competitive firm lowers its price to increase its sales it experiences a loss

in revenue due to the

114)

A)

output effect.

B)

substitution effect.

C)

price effect.

D)

income effect.

115)

An oligopolist differs from a perfect competitor in that

115)

A)

firms in an oligopoly do not produce homogeneous products while firms in perfect

competition do.

B)

the market demand curve for a perfectly competitive industry is perfectly elastic but it is

downward–sloping in an oligopolistic industry.

C)

there are no barriers to entry in perfect competition but there are entry barriers in oligopoly.

D)

there is cutthroat competition in perfect competition but little competition in oligopoly

because firms have significant market power.

Table 10–3

Quantity Price

(Dollars)

Total Revenue

(Dollars)

Total Variable

Cost

(Dollars)

Total Cost

(Dollars)

0$22 $0 $0 $50

120 20 16 66

219 38 31 81

318 54 45 95

417 68 59 109

516 80 75 125

615 90 93 143

714 98 112 162

813 104 140 190

912 108 180 230

10 11 110 230 280

Table 10–3 shows the firm’s demand and cost schedules for a firm in monopolistic competition.

116)

Refer to Table 10–3. What is the amount of the firm’s loss at its optimal output level?

116)

A)

$0

B)

$41

C)

$45

D)

$50

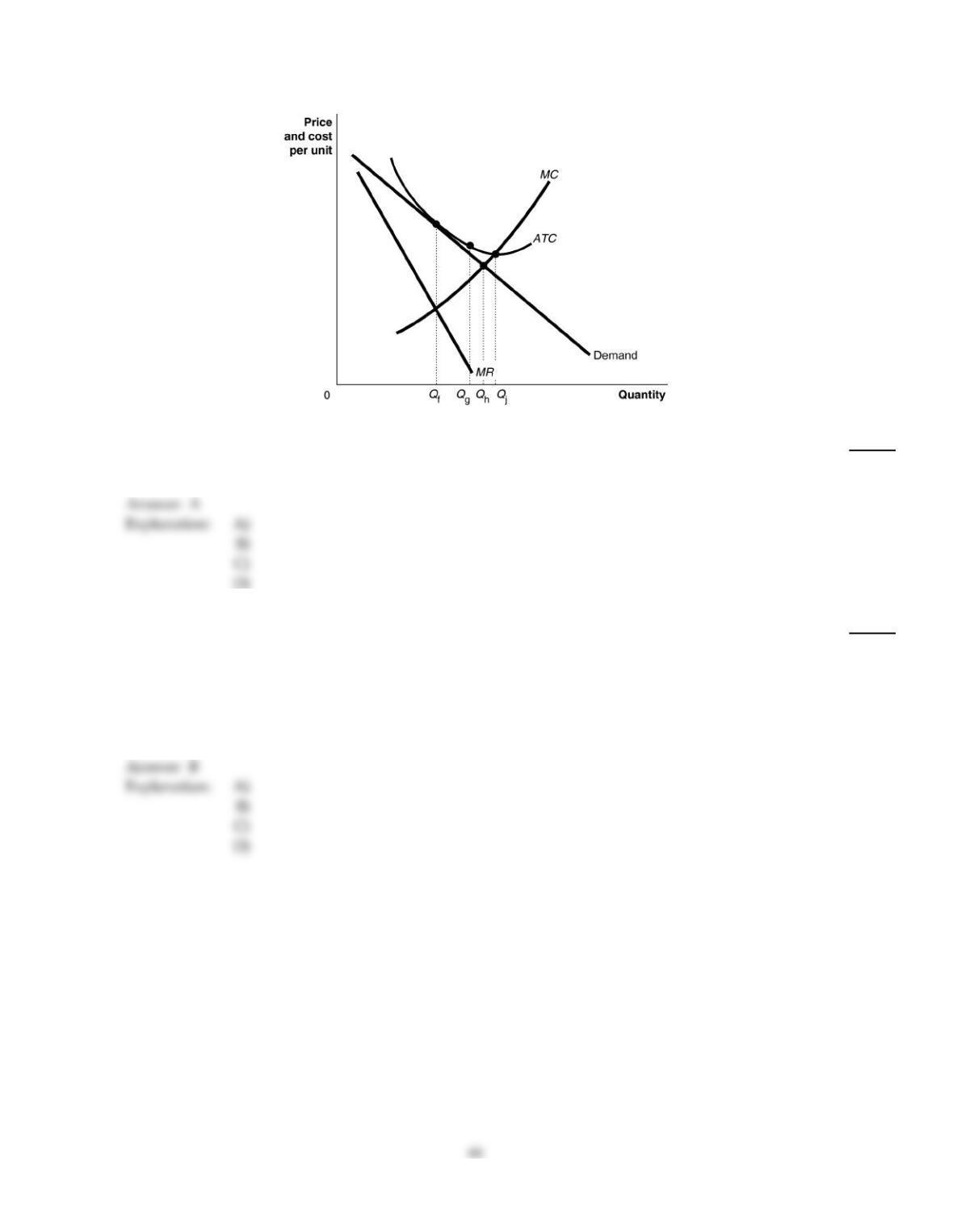

Figure 10–6

117)

Refer to Figure 10–6. The monopolistically competitive firm depicted in this diagram is

117)

A)

in long–run equilibrium.

B)

making short–run losses.

C)

in a constant–cost industry.

D)

in an increasing–cost industry.

118)

A monopolistically competitive firm earning profits in the short run will find the demand for its

product decreasing and becoming more elastic in the long run as new firms move into the industry

until

118)

A)

the firm exits the market.

B)

the firm’s demand curve is tangent to its average total cost curve.

C)

the firm is driven into bankruptcy.

D)

the firm’s demand curve is perfectly elastic.

Table 10–1

Quantity Price

(Dollars)

Total Revenue

(Dollars)

1$7.50 $7.50

27.00 14.00

36.50 19.50

46.00 24.00

55.50 27.50

65.00 30.00

119)

Refer to Table 10–1. What portion of the marginal revenue of the 4th unit is due to the output effect

and what portion is due to the price effect?

119)

A)

Output effect = $24.00; Price effect = $19.50

B)

Output effect = – $0.50; Price effect = $5.00

C)

Output effect = $6.00; Price effect = – $1.50

D)

Output effect = $6.50; Price effect = $2.00

120)

Collusion between two firms occurs when

120)

A)

announce that each will match its rival’s market price.

B)

firms act altruistically to bring about the economically efficient outcome.

C)

the firms independently pursue strategies that could hurt each other.

D)

firms agree to charge the same price or otherwise not to compete.

121)

An example of a barrier to entry is

121)

A)

increasing marginal costs.

B)

high profits.

C)

product differentiation.

D)

ownership of a key input.

SHORT ANSWER. Write the word or phrase that best completes each statement or answers the question.

122)

Explain why OPEC is caught in a prisoners’ dilemma?

122)

123)

Explain why a member of a cartel like OPEC has an incentive to agree to a low quota and

then produce more than its quota.

123)

124)

How does the demand curve for an oligopoly firm differ from the demand curves for firms

in competitive market structures?

124)

TRUE/FALSE. Write ‘T’ if the statement is true and ‘F’ if the statement is false.

125)

Assume that price exceeds average variable cost over the relevant range of demand. If a

monopolistically competitive firm is producing at an output where marginal revenue is $110 and

marginal cost is $118, then to maximize profits the firm should increase its output.

125)

126)

The barrier to entry that allowed Alcoa to make persistent economic profits was ownership of a key

input.

126)

127)

If a monopolistically competitive firm breaks even the firm is earning as much in this industry as it

could in any other comparable industry.

127)

128)

A barrier to entry exists when firms in an industry charge the lowest price possible for their

products.

128)

129)

If economies of scale are significant, the typical firm will not reach the minimum point on its

long–run average cost curve until it has produced a large fraction of industry sales.

129)

130)

When a monopolistically competitive firm cuts its price to increase its sales it experiences a loss in

revenue due to the income effect and a gain in revenue due to the substitution effect.

130)

131)

An equilibrium in which each player chooses its best strategy given the strategies chosen by the

other players, is called a Nash equilibrium.

131)

132)

A monopolistic competitor does not earn profits in the long run unless it can successfully

differentiate its product in the minds of its consumers.

132)

133)

In monopolistic competition if a firm produces a highly desirable product relative to its

competitors, the firm will be able to raise its price without losing any customers.

133)

134)

A monopolistically competitive industry that earns economic profit in the short run will be able to

expand its market share even if the market size remains constant.

134)

135)

In a Nash equilibrium, all players select non–dominant strategies.

135)

136)

For a monopolistically competitive firm price equals average revenue.

136)

137)

In long–run equilibrium, a perfectly competitive firm and a monopolistically competitive firm

produce the output at which MR=MC and charge a price equal to the average total cost of

production.

137)

138)

In long–run equilibrium a monopolistically competitive firm earning normal profit produces the

allocatively efficient output level.

138)

139)

A prisoners’ dilemma leads to a noncooperative equilibrium.

139)

140)

For a downward–sloping demand curve marginal revenue decreases as quantity sold increases.

140)

141)

Occupational licensing is an example of a barrier to entry that improves a country’s standard of

living.

141)

142)

Consumers in monopolistically competitive markets face a tradeoff between paying prices greater

than marginal costs and purchasing products that are more closely suited to their tastes.

142)

143)

Price leadership is a form of explicit collusion where one firm in an oligopoly announces a price

change and expects all other firms to follow suit.

143)

144)

A member of a cartel earns more profits by producing more than its quota and selling at a

price lower than the cartel’s price.

144)

145)

For a profit–maximizing monopolistically competitive firm, the marginal cost of the last unit sold is

less than the marginal benefit received from the purchase of that unit.

145)

146)

One way firms differentiate their product is to find a market niche.

146)

147)

If marginal revenue is negative then the revenue lost from receiving a lower price on all the units

that could have been sold at the original price is smaller than the additional revenue from selling

one more unit of the good.

147)

148)

Firms in monopolistic competition compete by selling similar, but not identical, products.

148)

SHORT ANSWER. Write the word or phrase that best completes each statement or answers the question.

149)

Assume that two interior design companies, Alistair and Baine, are competing for

customers and if they both advertise they would each earn $30 million in profit. If neither

advertises, they each earn $50 million in profit. But if one advertises and the other doesn’t,

the firm that advertises earns $40 million in profit while the other earns $20 million in

profit.

a. Present the information above in the form of a payoff matrix. Let Baine be the row

player and Alistair the column player.

b. Does each firm have a dominant strategy and if so what is it?

c. What is the Nash equilibrium?

149)