Chapter 10: Fixed Assets and Intangible Assets

161.

A copy machine acquired with a cost of $1,410 has an estimated useful life of 4 years. It is also expected to have

a useful operating life of 13,350 copies. Assuming that it will have a residual value of $75, determine the

depreciation for the first year by the

a.

straight-line method

b.

double-declining-balance method

c.

units-of–output method (4,500 copies were made the first year)

Chapter 10: Fixed Assets and Intangible Assets

162.

On July 1, Andrew Company purchased equipment at a cost of $150,000 that has a depreciable cost of

$120,000

and an estimated useful life of 3 years or 60,000 hours.

Using straight-line depreciation, prepare the journal entry to record depreciation expense for (a) the first year,

(b)

the second year, and (c) the last year.

163.

A copy machine acquired on July 1 with a cost of $1,450 has an estimated useful life of 4 years. Assuming that

it

will have a residual value of $250, determine the depreciation for the first year by the double-declining–

balance

method.

Chapter 10: Fixed Assets and Intangible Assets

164.

Champion Company purchased and installed carpet in its new general offices on March 31 for a total cost of $18,000.

The carpet is estimated to have a 15-year useful life and no residual value.

a.

Prepare the journal entries necessary for recording the purchase of the new carpet.

b.

Record the December 31 adjusting entry for the partial-year depreciation expense for the

carpet assuming that Champion Company uses the straight-line method.

165.

Solare Company acquired mineral rights for $60,000,000. The diamond deposit is estimated at

6,000,000

tons. During the current year, 2,300,000 tons were mined and sold.

a.

Determine the depletion rate.

b.

Determine the amount of depletion expense for the current year.

c.

Journalize the adjusting entry to recognize the depletion expense.

Chapter 10: Fixed Assets and Intangible Assets

166.

Carter Co. acquired drilling rights for $18,550,000. The oil deposit is estimated at 74,200,000 gallons. During

the

current year, 6,000,000 gallons were drilled. Journalize the adjusting entry at December 31 to recognize

the

depletion expense.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Chapter 10: Fixed Assets and Intangible Assets

167.

Chasteen Company acquired mineral rights for $9,100,000. The mineral deposit is estimated at

65,000,000

tons. During the current year, 18,375,000 tons were mined and sold.

Required:

(1)

Determine the amount of depletion expense for the current year.

(2)

Journalize the adjusting entry to recognize the depletion expense.

168.

On December 31, Bowman Company estimated that goodwill of $80,000 was impaired. A patent with an

estimated

useful economic life of 10 years was acquired for $252,000.

Required:

(1)

Journalize the adjusting entry on December 31 for the impaired goodwill.

(2)

Journalize the adjusting entry on December 31 for the amortization of the patent rights.

Chapter 10: Fixed Assets and Intangible Assets

169.

On December 31, it was estimated that goodwill of $65,000 was impaired. On July 1, a patent with an

estimated

useful economic life of 10 years was acquired for $60,000.

(a)

Journalize the adjusting entry on December 31 for the impaired goodwill.

(b)

Journalize the adjusting entry on December 31 for the amortization of the patent rights.

170.

On July 1, Sterns Co. acquired patent rights for $36,000. The patent has a useful life of 6 years and a legal life

of

15 years. Journalize the adjusting entry on December 31 to recognize the amortization.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Chapter 10: Fixed Assets and Intangible Assets

171.

Identify the following as a fixed asset (FA), or intangible asset (IA), natural resource (NR), or none of these(N)

(a)

computer

(b)

patent

(c)

oil reserve

(d)

goodwill

(e)

U.S. Treasury note

(f)

land used for employee parking

(g)

gold mine

Chapter 10: Fixed Assets and Intangible Assets

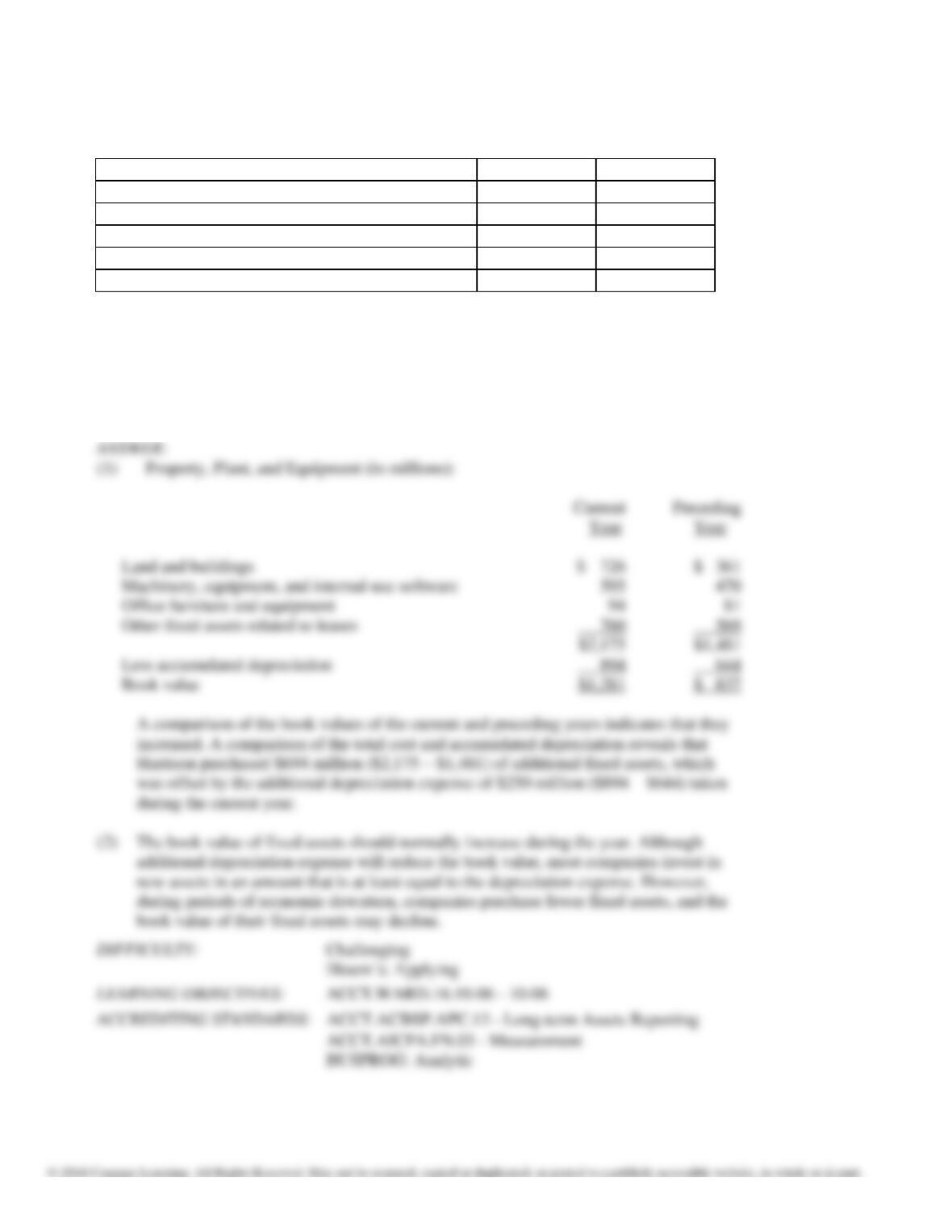

172.

The following information was taken from a recent annual report of Harrison Company (in millions):

Current Year

Preceding Year

Land and buildings

$726

$361

Machinery, equipment, and internal-use software

595

470

Office furniture and equipment

94

81

Other fixed assets related to leases

760

569

Accumulated depreciation and amortization

894

644

Required:

(1)

Compute the book value of the fixed assets for the current year and the preceding year

and explain the differences, if any.

(2)

Would you normally expect the book value of fixed assets to increase or decrease

during

the year?

Chapter 10: Fixed Assets and Intangible Assets

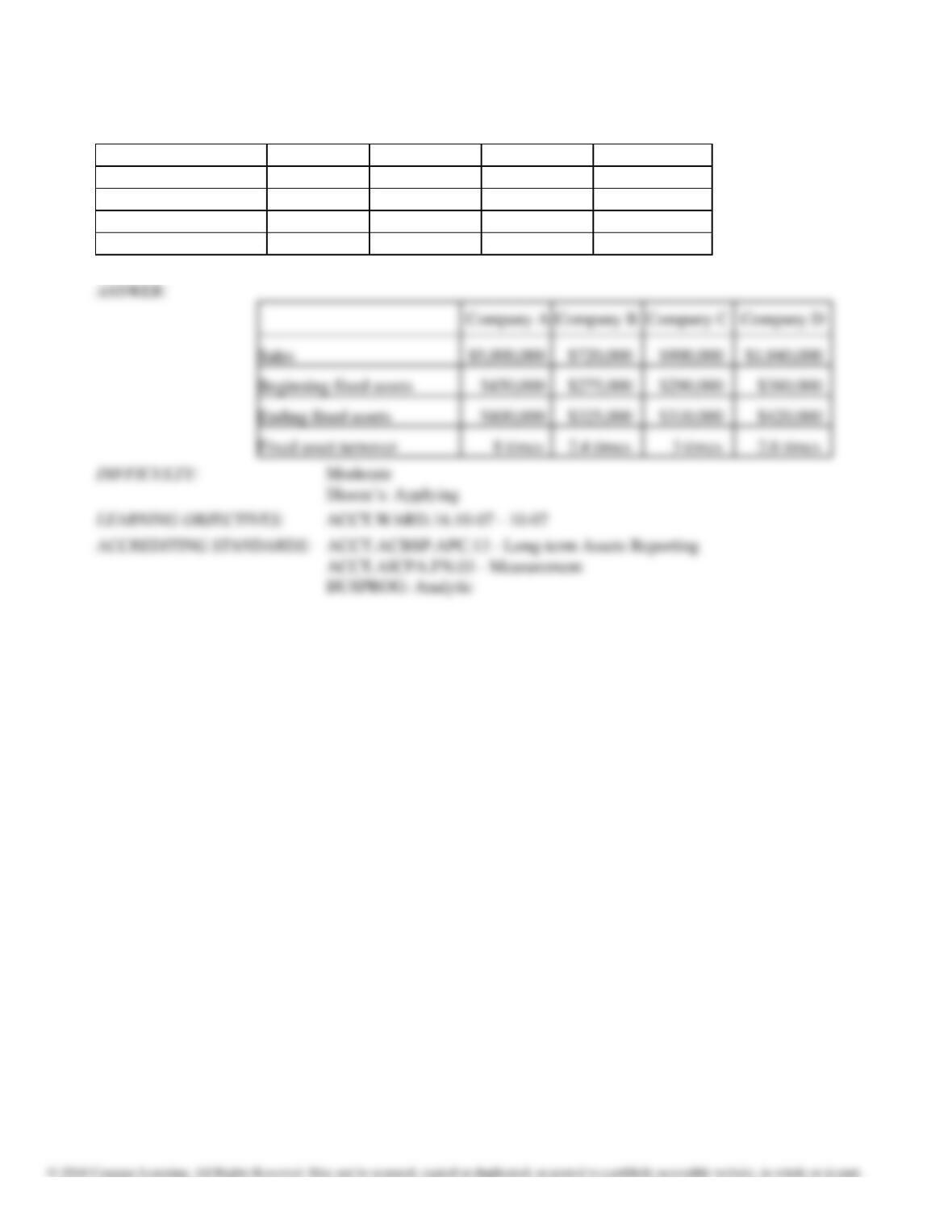

173.

Fill in the missing numbers using the formula for fixed asset turnover:

Company A

Company B

Company C

Company D

Sales

$5,000,000

$720,000

$900,000

?

Beginning fixed assets

$450,000

$275,000

?

$380,000

Ending fixed assets

$800,000

?

$310,000

$420,000

Fixed asset turnover

?

2.4 times

3 times

2.6 times

Chapter 10: Fixed Assets and Intangible Assets

174.

Financial statement data for the years ended December 31 for Parker Corporation are as follows:

Current Year

Prior Year

Sales

Fixed assets (net):

Beginning of the year

$2,595,600

$901,070

$2,409,498

$820,000

End of the year

829,330

901,070

a)

Determine the fixed asset turnover for the current and prior years.

b)

Does the change in fixed asset turnover from the prior year to the current year indicate a favorable or

unfavorable trend?

Chapter 10: Fixed Assets and Intangible Assets

175.

Computer equipment (office equipment) purchased 6 1/2 years ago for $170,000, with an estimated life of 8

years

and a residual value of $10,000, is now sold for $60,000 cash. (Appropriate entries for depreciation had

been made

for the first six years of use.) Journalize the following entries:

(a)

Record the depreciation for the one-half year prior to the sale, using the straight-line method.

(b)

Record the sale of the equipment.

(c)

Assuming that the equipment had been sold for $25,000 cash, prepare the entry to record the sale.

Chapter 10: Fixed Assets and Intangible Assets

176.

Equipment was acquired at the beginning of the year at a cost of $75,000. The equipment was depreciated

using

the straight-line method based upon an estimated useful life of 6 years and an estimated residual value of

$7,500.

a)

What was the depreciation expense for the first year?

b)

Assuming the equipment was sold at the end of the second year for $59,000, determine

the gain

or loss on sale of the equipment.

c)

Journalize the entry to record the sale.