Chapter 10—Forecasting Financial Statements

MULTIPLE CHOICE

1. The objective of forecasting is to develop

a.

stand-alone financial statements for future analysis.

b.

a set of realistic expectations for future value-relevant payoffs.

c.

a balance sheet and income statement that articulate.

d.

financial statements for comparison to industry averages.

2. Nichols and Wahlen’s 2004 study showed that superior forecasting provides the potential to earn

superior security returns. Nichols and Wahlen’s findings indicate

a.

that an investor could earn excess returns if the investor could predict accurately the sign of

the change in earnings one year ahead.

b.

that an investor could earn excess returns if the investor could predict accurately the

magnitude of the change in earnings one year ahead.

c.

that an investor could earn excess returns if the investor could predict accurately the sign of

the change in cash flows from operations one year ahead.

d.

that an investor could earn excess returns if the investor could predict accurately the sign of

the change in working capital one year ahead.

3. Financial statement forecasts rely on additivity within financial statements and articulation across

financial statements. Given this information forecasts of future growth in inventory will most likely

affect growth in

a.

accounts receivables.

b.

accounts payable.

c.

depreciation.

d.

salary payable.

4. Financial statement forecasts rely on additivity within financial statements and articulation across

financial statements. Given this information sales growth forecasts will most likely affect growth in

a.

accounts receivables.

b.

accounts payable.

c.

depreciation.

d.

salary payable.

5. Projecting sales price changes depends on factors specific to the firm and its industry that might affect

demand and price elasticity. Which of the following types of companies would most likely be able to

increase prices?

a.

A firm in a capital intensive industry that is expected to operate near capacity for the near

future.

b.

A firm in a capital intensive industry in which excess capacity exists.

c.

A firm operating in an industry that is expected to experience technological improvements

in its production process.

d.

A firm operating in an industry that is transitioning from the high growth to the maturity

phase of its life cycle.

6. Projecting sales price changes depends on factors specific to the firm and its industry that might affect

demand and price elasticity. Which of the following companies would most likely not be able to

increase prices in the near future?

a.

A firm in a capital intensive industry that is expected to operate near capacity for the near

future.

b.

A firm in a capital intensive industry in which excess capacity exists.

c.

A firm operating in an industry that is expected to maintain its current production processes.

d.

A firm operating in an industry that is transitioning from the introduction phase to the high

growth phase of its life cycle.

7. If a company has very low operating leverage (i.e. a low proportion of fixed costs in the cost structure)

and no changes are expected in operations

a.

percentage change income statement percentages can serve as the basis for projecting

operating expenses.

b.

using common-size income statement percentages will overstate future projected operating

expenses.

c.

using common-size income statement percentages will understate future projected operating

expenses.

d.

using common-size income statement percentages can serve as a reasonable basis for

projecting future operating expenses.

8. When projecting operating expenses it is important to determine the mix of fixed and variable costs, one

clue suggesting the presence of fixed costs is

a.

the percentage change in cost of goods sold in prior years is significantly greater than the

percentage change in sales.

b.

the percentage change in cost of goods sold in prior years is significantly less than the

percentage change in sales.

c.

low capital intensity in the production process.

d.

the percentage change in sales in prior years is significantly greater than the percentage

change in receivables.

9. To ensure that the financial statements articulate, it is important that the change in the cash balance on

the balance sheet each year agrees with

a.

the cash collections from sales in the projected income statement.

b.

the cash provided by or used by operations on the projected statement of cash flows.

c.

the net change in cash on the projected statement of cash flows.

d.

the net change in working capital from period to period.

10. An analyst using the inventory turnover ratio to calculate future levels of inventory may face the

problem that

a.

the method reduces the potential understatement inherent in average balances.

b.

the method can introduce artificial volatility in ending balances.

c.

the method results in understating inventory each year.

d.

the method results in overstating inventory each year.

Sparky’s

Sparky’s sells auto parts. Provided below is selected financial information from the company’s 2012

annual report:

Sparky’s Selected Financial Statement data

Fiscal year end

2012

2011

(amounts in thousands of dollars)

Net sales

$125,410

$106,380

Cost of Goods Sold

-104,090

-89,359

Gross Profit

$21,320

$17,021

Inventory

$31,353

$30,850

11. Using Sparky’s financial information what is the company’s inventory turnover ratio for 2012?

a.

0.69

b.

1.00

c.

3.35

d.

4.03

Sparky’s Selected Financial Statement data

For Fiscal year end

(amounts in thousands of dollars)

Net sales

Inventory

Inventory Turnover

12. Sparky’s forecasts that sales will grow by 25% in 2013 and that its cost of goods sold to sales ratio will

be the same in 2013 as it was in 2012. If these assumptions prove correct and Sparky’s inventory

turnover ratio for 2013 is 4.5 what will be the level of inventory at the end of 2013?

a.

$31,353

b.

$26,475

c.

$40,000

d.

$42,314

Selected Financial Statement data

Fiscal year end

(amounts in thousands of dollars)

Net sales

Card Sharks, Inc.

Card Sharks, Inc. sells baseball cards and other memorabilia. The company tries to maintain a cash

balance equivalent to approximately 30 days of sales. Sales in 2011 amounted to $352,412 and the

company expects growth in 2012 of 30% and in 2013 of 35%.

13. Given the information provided about Card Sharks, what is the company’s 2012 projected year-end cash

balance?

a.

$966

b.

$50,820

c.

$15,623

d.

$38,524

14. Given the information provided about Card Sharks, what is the company’s 2013 projected annual sales?

a.

$656,191

b.

$493,377

c.

$618,482

d.

$542,333

15. Given the information provided about Card Sharks, what is the company’s 2013 projected cash balance?

a.

$53,934

b.

$49,524

c.

$21,873

d.

$50,820

16. All of the following are the fundamental bases for future payoffs to equity shareholders and share value

except:

a.

earnings

b.

cash flows

c.

dividends

d.

depreciation

17. All of the following are true regarding the key principles of forecasting except:

a.

Financial statement forecasts need not be comprehensive.

b.

Forecasts should not manifest wishful thinking.

c.

Financial statement forecasts must be internally consistent.

d.

Financial statement forecasts must rely on assumptions that have external validity.

18. Which of the following statements does not apply to preventing “garbage in, garbage out” when

implementing a forecasting game plan?

a.

The quality of the financial statement forecasts will depend on the quality of the

forecast assumptions.

b.

The quantities forecasted within financial statement forecasts will depend on the quantity of

the forecast assumptions.

c.

Analysts should justify and evaluate the most important assumptions that reflect the critical

risk and success factors of the firm’s strategy.

d.

Analysts can impose reality checks on the assumptions by analyzing the forecasted financial

statements using ratios, common-size, and rate-of-change financial statements.

19. If a firm competes in a capital-intensive industry with excess capacity, all of the following are true

except:

a.

price increases will be less likely.

b.

price increases will be more likely.

c.

companies in competitive industries face high exit barriers.

d.

companies in competitive industries may experience future price decreases.

20. Using common-size balance sheet percentages to project individual assets, liabilities, or shareholders’

equity has all of the following shortcomings except:

a.

Individual assets, liabilities, and shareholders’ equity are not independent

of each other.

b.

If a company experiences changing proportions for investments in securities among its

assets, other asset categories may show decreasing percentages in some years even though

their dollar amounts are increasing.

c.

Individual assets, liabilities, and shareholders’ equity are independent

of each other.

d.

The common-size percentages do not permit the analyst to easily change

the assumptions about the future behavior of an individual asset or liability.

21. All of the following statements are true regarding ratios and forecasts except:

a.

Ratios cannot confirm whether forecast assumptions will turn out to be correct.

b.

Ratios can tell whether future sales growth was accurately captured.

c.

Ratios cannot tell whether assumptions about future cash flows are realistic.

d.

Ratios can tell whether growth rates for sales are consistent with past sales growth

performance.

22. Projected financial statements can be used to assess the sensitivity of all of the following except:

a.

a firm’s liquidity

b.

a firm’s leverage to changes in assumptions

c.

conditions under which the firm’s debt covenants may become binding

d.

unusual patterns for projected total assets.

23. Common-size financial statements recast each statement item as

a.

a percentage of the “bottom line.”

b.

a percentage using industry averages for the “base number.”

c.

a percentage using a base year number for each line item.

d.

a percentage of some “base number” on the financial statement in question.

24. Financial ratio, percentage, and trend comparisons can be distorted by all of the following except:

a.

aggressive revenue recognition practices.

b.

the timing of asset purchases.

c.

accounting for similar economic fundamentals in similar fashion.

d.

the presence of nonrecurring items among the firms being analyzed.

25. All of the following are true regarding projected financial statements except:

a.

The statement of cash flows is the most critical forecast since it reflects profitability rather

than viability.

b.

Preparing projected financial statements must incorporate a company’s past performance

records.

c.

Preparing projected financial statements must incorporate a company’s current performance

records.

d.

The income statement demonstrates immediate capability to service debt for banks or real

potential for growth in returns for venture capital.

26. As a firm progresses through the introduction life-cycle stage, what type of flexible account will it be

more likely to use to balance the balance sheet?

a.

dividends.

b.

growth related assets.

c.

issued equity.

d.

stock buy-backs.

27. As a firm progresses through the decline life-cycle stage, what type of flexible account will it be more

likely to use to balance the balance sheet?

a.

issued debt.

b.

growth related assets.

c.

issued equity.

d.

stock buy-backs.

28. As a firm progresses through the growth life-cycle stage, what type of flexible account will it be more

likely to use to balance the balance sheet?

a.

issued debt.

b.

paying down of debt.

c.

dividends

d.

stock buy-backs.

COMPLETION

1. Financial statement forecasts are important analysis tools because forecasts of

______________________________ play a central role in valuation and many other financial decision

contexts.

2. Realistic expectations are ____________________ and ____________________.

3. Financial statement forecasts should rely on ____________________ within financial statements.

4. Financial statement forecasts should rely on _________________________ across financial statements.

5. A firm in a mature industry with little expected change in its market share might anticipate volume

increases equal to the growth rate in the _________________________ within its geographic markets.

6. Firms which have differentiated ___________________________________ for its products may have a

greater potential to increase prices.

7. It may be difficult to forecast sales for firms with _________________________ patterns because their

historical growth rates reflect wide variations in both direction and amount from year to year.

8. A company that has a cost structure in which its costs grow at a lesser rate than its sale enjoys

___________________________________.

9. In developing forecasts of expenses the analyst must take into consideration that expenses can be

broken down into ________________________ or ______________________ components.

10. The formula for forecasting inventory is ____________ /365 X .

11. To develop forecasts of individual assets, the analyst must first link historical growth rates for individual

assets to historical growth rates in ____________________ and other activity-based drivers.

12. For some types of assets, such as plant, property and equipment, asset growth typically

____________________ future sales growth.

13. For some types of assets, such as accounts receivable, asset growth typically ____________________

future sales growth.

14. When projecting ____________________, the analyst should consider economy-wide factors such as

the expected rate of general price inflation in the economy.

15. A firm in transition from the high growth to the mature phase of its life cycle, or a firm with significant

technological improvements in its production processes, might expect increases in

______________________________ but decreases in sales prices per unit.

16. If a firm operates at less then full capacity then price _______________________ are not likely

17. Analysts must develop realistic expectations for the outcomes of future business activities.

To develop these expectations, analysts build a set of _____________________________.

SHORT ANSWER

1. Based on the following statement from the text,” to develop forecasts of individual operating assets and

liabilities, you must first determine the underlying operating activities that drive them”. Explain what

those underlying activities are?

2. The authors set forth a seven-step forecasting game plan for preparing pro forma financial statements.

Discuss the seven steps necessary to prepare the three principal financial statements.

3. One problem caused by using turnover ratios to calculate asset balances is that it can lead to volatility in

projected ending balances. What might an analyst do to reduce the “sawtooth” pattern caused by using

turnover ratios?

4. The first step in the forecasting game plan is to project sales and other other operating activities. Sales

numbers are determined by both a volume component and price component. Projecting prices depends

on factors specific to the firm and its industry that might affect demand and price elasticity. For the

following types of firms discuss whether it would be likely that the firm would be able to raise future

prices:

a.

A firm in a capital-intensive industry that is expected to operate near capacity for the near

future.

b.

A firm in an industry that is expected to experience numerous technological improvements.

c.

A firm with products which are transitioning from the growth to maturity phase of the

product life cycle.

d.

A firm that has established a well known brand name and image.

b.

This firm would probably not be able to raise prices due to efficiencies brought on by the

technological change, although sales volumes may increase.

which demand is more stable. Thus, price increases may result in consumers switching

products, etc.

d.

Firms with well known images and brand names may be better positioned to raise prices

because consumers feel such brand loyalty.

business operations.

6.

Check whether the projected balance sheet is in balance. Repeat Steps 4 and 5 until it is in

balance.

7.

Derive the projected statement of cash flows from the projected income statements and the

changes in the projected balance sheet amounts.

5. As an analyst it is important when projecting sales to make estimates about future changes in sales

volume. Compare how you might make estimates about future sales value for a company in a mature

industry and one in a rapidly growing industry.

6. In comparison of 2010 to 2009 performance, Watson Company’s inventory turnover decreased

substantially, although sales and inventory amounts were essentially unchanged.

Required:

During a corporate meeting you heard the following managers postulate why the decreased inventory

turnover ratio happened. Which statement best explains the decreased inventory turnover ratio and

why?

a. The marketing manager said: The decreased inventory turnover ratio is due to an increase in the cost

of goods sold.

b. The operations manager said: The decreased inventory turnover ratio is due to increased gross profit

percentage.

c. The credit manager said: The decreased inventory turnover ratio is due to a decrease in the accounts

receivable turnover.

d. The shipping manager said: The decreased inventory turnover ratio is due toinventory being shipped

FOB destination point which keeps those items in inventory until they reach the purchasers warehouse.

PROBLEM

1.

Bargains, Inc. manufactures and markets toys. Selected income statement data from 2010 and 2009

appear below:

Bargains, Inc.

Selected Income Statement data

Fiscal year end

12/31/2010

12/31/2009

(amounts in thousands of dollars)

Net sales

$5,320,185

$4,980,000

Cost of Goods Sold

-3,520,415

-3,340,290

Gross profit

$1,799,770

$1,369,710

998,934

Required:

a.

An analyst can sometimes estimate the variable cost as a percentage of sales for a particular

cost by dividing the amount of the change in the cost item between two years by the amount

of the change in sales for those two years. The analyst can then multiply the variable cost

percentage times sales to determine the total variable cost. Subtracting the variable cost

yields the fixed cost for that particular item. Follow this procedure to determine the cost

structure for costs of goods sold for Bargains, Inc.

b.

Bargains, Inc. projects sales to grow at the following percentages in future years: 2011,

10percent; 2012,12 percent; 2013, 16 percent. Using this information project sales, cost of

goods sold and gross profit for Bargains, Inc. for 2011 to 2013.

2. Glad Rags, Inc. sells women’s clothes. Provided below is selected financial statement information:

Glad Rags, Inc.

Selected Financial Statement data

Fiscal year end

2010

2009

(amounts in thousands of dollars)

Net sales

$47,895

$42,589

Cost of Goods Sold

(35,952)

(32,588)

Change in COGS

Change in sales

Variable cost percentage

Fixed Costs:

2010

b.

Projected Growth Rate

10%

12%

16%

Net Sales

Cost of Goods Sold:

Fixed portion

Variable portion (53 of Sales)

Gross Profit

Gross profit

$11,943

$10,001

Inventory

$ 5,548

$ 4,948

Required:

a.

Compute the inventory turnover ratio for 2010.

b.

Clothes, Inc. projects that sales will grow at a compound rate of 7% per year for years

2011-2013 and that the cost of goods sold to sales percentage will equal that realized in 2010.

Compute the projected implied level of inventory at the end of 2011 to 2013.

3. Office Mart, Inc. sells numerous office supply products through a national distribution center. The

company has focused on maintaining a cash balance equivalent to approximately 14 days of sales. Sales

in 2010 amounted to $125,980,673 and the company expects growth in 2011 of 11% and in 2012 of

15%. Given this information determine Office Mart, Inc.’s projected year-end cash balance for 2011 and

2012.

4. The following information about Douglas Corp.’s Accounts Receivable and Sales are presented below:

Year 2012-Beginning Balance of A/R = $791M

Year 2012 -Ending Balance of A/R = $807M

Year 2012 – Sales = $3,002M

Assumptions:

Sales growth will be equal to 6% per year

A/R turnover will stay constant throughout the forecast period

Required:

a.

Using this information, forecast Douglas Corp.’s the growth in Accounts Receivable for

years 2013-2017.

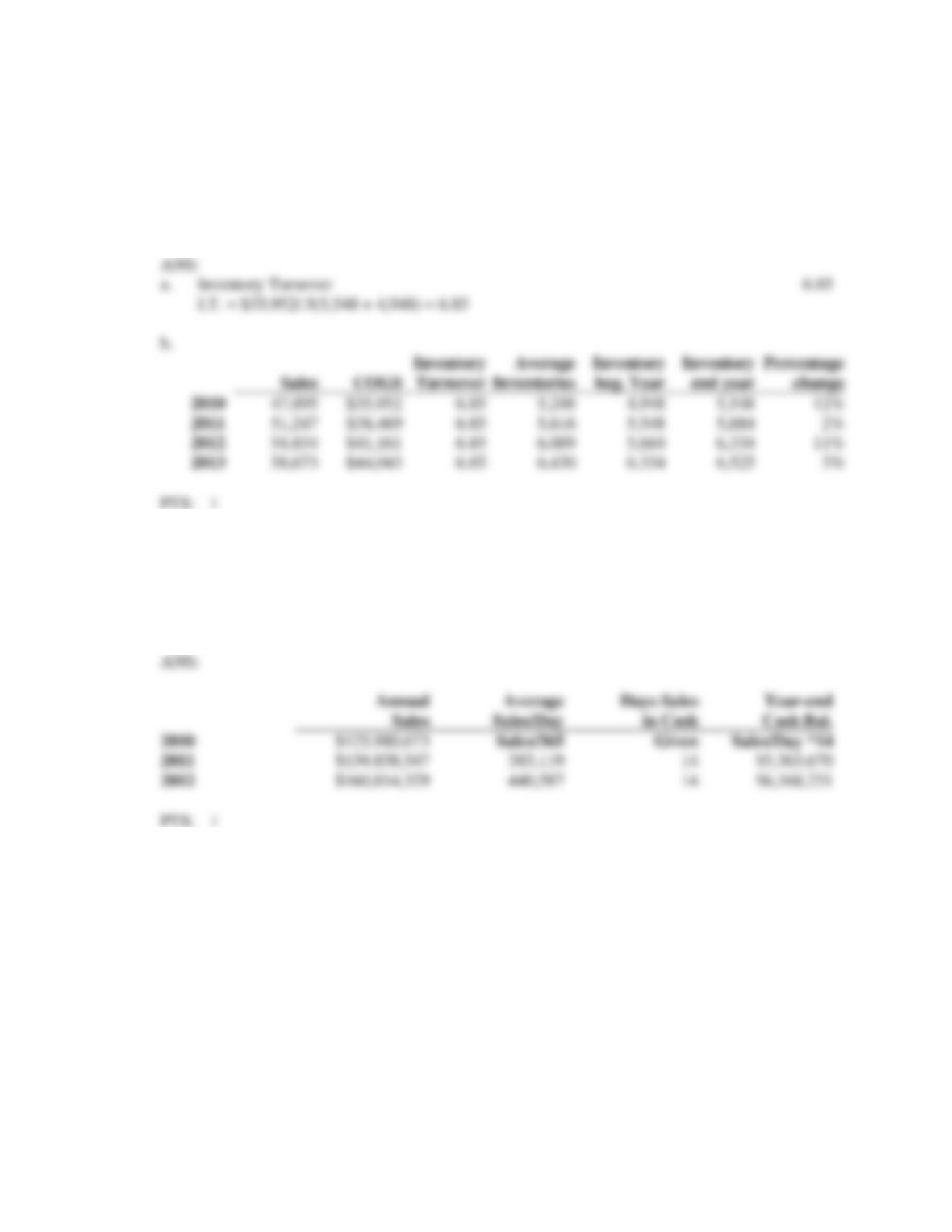

Inventory Turnover

I.T. = $35,952/.5(5,548 + 4,948) = 6.85

b.