1

CHAPTER 1

TRUE/FALSE QUESTIONS

to market.

intermediation, its residual claim is against a deficit spending units (DSU).

spending unit.

scheduled maturity.

contact with each other in financial markets.

2

units (DSUs).

corporate growth.

corporations for long-term growth.

exchange.

suppliers.

resold to the general public.

their liabilities.

3

MULTIPLE CHOICE QUESTIONS

a. income and expenditures for the period are equal.

b. income for the period exceeds expenditures.

c. expenditures for the period exceed receipts.

d. spending is entirely financed by credit cards

a. a surplus spending unit (SSU) purchasing a financial claim from a deficit

spending unit (SSU) spending unit (DSU)

b. a surplus spending unit (SSU) purchasing a financial claim from a dealer

c. a surplus spending unit (SSU) purchasing a financial claim from a commercial

bank

d. a surplus spending unit (SSU) purchasing a financial claim from an underwriter

a. commercial banks.

b. savings and loan associations.

c. credit unions.

d. finance companies.

a. Borrowers are able to finance at the highest possible cost.

b. Surplus spending units are able to receive the lowest return on their savings.

c. Transaction and intermediation costs are low.

d. Lenders will have a limited choice of financial investments.

a. eliminates search and transactions costs

b. is a mere theoretical possibility

c. promotes economic growth and social progress

d. depends on high volumes of “direct” transactions

a. higher-yielding long-term securities

b. money market securities exclusively

c. government securities exclusively

d. none of the above

a. from savers to borrowers

b. from Surplus spending units (SSUs) to deficit spending units (DSUs)

c. from the household sector to the business sector

d. any of the above

a. Business

b. Government

c. Foreign

d. Household

4

a. households

b. businesses

c. governments

d. all of the above

a. Deficit spending units (DSUs) are sometimes Surplus spending units (SSUs).

b. Every financial asset is someone else’s liability.

c. Intermediaries may own both direct and indirect financial assets.

d. The government is unable to control its federal spending.

a. $116

b. $118

c. $2

d. none of the preceding

a. issue direct claims and purchase direct financial assets.

b. issue indirect claims and purchase indirect financial assets.

c. purchase large amounts of real, tangible assets.

d. purchase direct financial claims and issue indirect securities.

a. government regulation of interest rates

b. economies of scale

c. ability to manage credit risk

d. control of transactions costs

a. issuing insured deposits and making risky business loans.

b. bringing together investors of different religions

c. issuing five $3,000 CDs and making one $15,000 loan.

d. promising liquidity to surplus spending units (SSUs) while investing the funds

long-term

a. ability to finance businesses and governments.

b. ability to achieve economies of scale.

c. ability to reduce transaction costs.

d. ability to find confidential information.

a. life insurance company

b. credit union

c. mutual savings bank

d. commercial bank

a. They are recognized on two balance sheets.

b. They are intangible assets.

c. They are IOU‘s traded for funds.

d. They represent ownership of real assets.

5

a. depository institutions.

b. contractual savings institutions.

c. finance companies.

d. the real estate market.

a. bonds.

b. money.

c. loans.

d. commodities.

a. the purchase of mutual fund shares.

b. depositing in a credit union.

c. borrowing from a friend or relative.

d. employee contributions to a pension fund.

a. lenders.

b. borrowers.

c. sellers of securities.

d. balanced budget units.

budgeting total expenditures of about $180,000. For this budget period, the Gutierrez

family is most specifically a(n)

a. deficit spending unit (DSU)

b. business

c. surplus spending unit (SSU)

d. household

a. quality.

b. risk.

c. marketability.

d. perpetuity.

a. the saver holding the lender‘s IOU.

b. two separate contracts.

c. the lender holding the borrower’s IOU.

d. several different financial institutions.

spending unit (SSU) and deficit spending unit (DSU) .

a. indirect; two

b. direct; two

c. indirect; one

d. direct; one

6

a. trades a financial claim for money.

b. trades money for a financial claim issued by a financial institution.

c. trades money with a broker who owns the financial claims of a borrower.

d. trades money for the financial claim of the borrower.

a. single financial instrument.

b. a broker, dealer or investment banker.

c. small denominations.

d. dominance of governments and businesses as borrowers.

a. a dealer arrangement.

b. a private placement.

c. an underwriting.

d. intermediation financing.

a. make commissions.

b. minimize the bid-ask spread.

c. bring sellers and buyers together.

d. underwrite new issues of securities.

a. dealers; brokers

b. brokers; investment bankers

c. dealers; financial institutions

d. brokers; dealers

selling at $67.50. The bid is _____; the bid-ask spread is _____.

a. $65.00; $2.50

b. $67.50; $2.50

c. lower than the ask price; higher than the bid price

d. higher than the ask price; $2.50

a. market

b. ask

c. offering

d. bid

in direct financial markets.

a. dealer

b. investment banker

c. broker

d. seller

a. provides liquidity to sellers

b. buys and sells from inventory

7

c. earns return from bid-ask spread

d. transforms claims

a. Taking deposits.

b. Marketing new issues of securities.

c. Underwriting securities.

d. Completing regulatory paperwork and rendering advice.

Hollon will pay LU $45.00 a share and offer the stock to the public at $48.00. The direct

cost of underwriting the issue is $1.00 per share. The underwriting spread is

a. $4.00 per share.

b. $3.00 per share.

c. $2.00 per share.

d. not ascertainable from the information above.

a. the household sector.

b. the business sector.

c. the government sector.

d. the foreign sector

a. direct finance

b. investment banking

c. market making

d. transformation of claims

a. speculation.

b. maturity intermediation.

c. denomination intermediation.

d. currency transformation

a. adding loans to the portfolio increases the variability of the loan portfolio.

b. loans from similar borrowers are combined in a portfolio.

c. adding loans to the portfolio decreases the variability of the loan portfolio.

d. combining loans with similar payment patterns in a single portfolio.

a. most Surplus spending units (SSUs) want to invest in more than one currency

b. all financial institutions operate internationally

c. few ordinary investors care to hold claims denominated in foreign currency

d. Deficit spending units (DSUs) can’t export unless they borrow in the currency of

the importing country

a. pays the check written by a deposit customer.

b. redeems a savings deposit upon demand.

c. makes a loan fulfilling a loan commitment.

d. All of the above.

8

a. purchase of securities.

b. sale of securities.

c. writing a broker a check to pay for a purchase of IBM stock.

d. depositing an insurance settlement with a credit union.

a. thrift institutions

b. credit unions

c. pension funds

d. commercial banks

a. depository; contractual

b. contractual; depository

c. federal ; investment

d. depository; depository

a. commercial banks.

b. finance companies.

c. property-casualty insurance companies.

d. pension funds.

a. corporate bonds.

b. U.S. Government securities.

c. federal agency securities.

d. common stock.

a. businesses that are “too big to fail”.

b. the U.S. Treasury to finance government deficits.

c. agricultural or housing-related sectors which have limited access to private

credit.

d. foreign governments

a. maturity

b. liquidity

c. availability to ordinary individual investors

d. all of the above

represent

a. credit risk.

b. liquidity risk.

c. foreign exchange risk.

d. interest rate risk.

a. common stocks

9

b. convertible bonds

c. commercial paper

d. mortgages

a. they have increased marketability of stocks and bonds.

b. they have increased the public’s access to investment.

c. they have helped investors diversify.

d. all of the above

a. create interest in stocks.

b. increase the marketability of securities.

c. provide a legal way to gamble.

d. supply money to deficit spending units.

in

a. essential nature and purpose of the assets created or acquired

b. relative cost of the assets created or acquired

c. susceptibility of the assets created or acquired to amortization or depreciation

d. semantics

a. plant and equipment

b. inventory

c. operating expenses

d. none of the above

a. directly by purchasing stocks and bonds.

b. indirectly through mutual funds.

c. indirectly through pension funds

d. all of the above

a. “primary market” activity

b. “secondary market” activity

c. “money market” activity

d. financial intermediation

a. forward contract.

b. securitized asset.

c. futures contract.

d. option contract.

a. put.

b. forward contract.

c. futures contract.

d. call.

10

a. liquidity; marketability.

b. spot; future.

c. liquidity; economic investment.

d. primary; secondary.

spending unit (SSU) sells the claim in the

a. intermediation market.

b. direct financial market.

c. federal funds market.

d. secondary market.

a. short-term to maturity

b. small denomination

c. low default risk

d. high marketability

.

a. directly; commercial paper

b. locally; their credit union

c. indirectly; negotiable CDs

d. indirectly; money market mutual funds

a. The money market is a dealer market linked by efficient communications

systems.

b. Money market transactions are seldom over $1 million.

c. Market transactions include more primary than secondary market trades.

d. Most money market transactions are conducted by mail.

a. commercial paper

b. Federal Funds

c. Treasury securities

d. agency securities

a. Treasury deposits.

b. Federal Reserve assets.

c. commercial bank deposits at the Federal Reserve.

d. overnight loans settled in immediately available funds.

a. it is the world’s liquidity market.

b. it is the market in which the Fed conducts monetary policy.

c. the federal government finances most of its credit needs in the money market.

d. all of the above

a. commercial paper.

b. federal agency issues.

c. negotiable CDs.

d. Treasury bills.

a. negotiable CDs

b. banker’s acceptances

c. repurchase agreements

d. commercial paper(d)

a. investing excess cash balances.

b. buying and selling goods on credit in international trade.

c. issuing commercial papers and short-term corporate notes.

d. all of the above

a. a place to securitize assets.

b. a source of generating fee income from trading.

c. a source of funding.

d. all of the above.

a. pay an annual listing fee and disclose important information.

b. enhance the liquidity of their securities for investors.

c. sell more securities.

d. increase the size of the firm.

a. secondary markets

b. primary markets

c. money markets

d. derivatives markets

e. commodities markets

I. Pool funds of small savers and invest in either money or capital markets

II. Provide economic protection from adverse events

III. Provide consumer loans and real estate loans funded by deposits

IV. Underwrite and trade securities and provide brokerage services

V. Accumulate and transfer wealth from work period to retirement period

1. Credit unions

2. Insurance companies

3. Pension funds

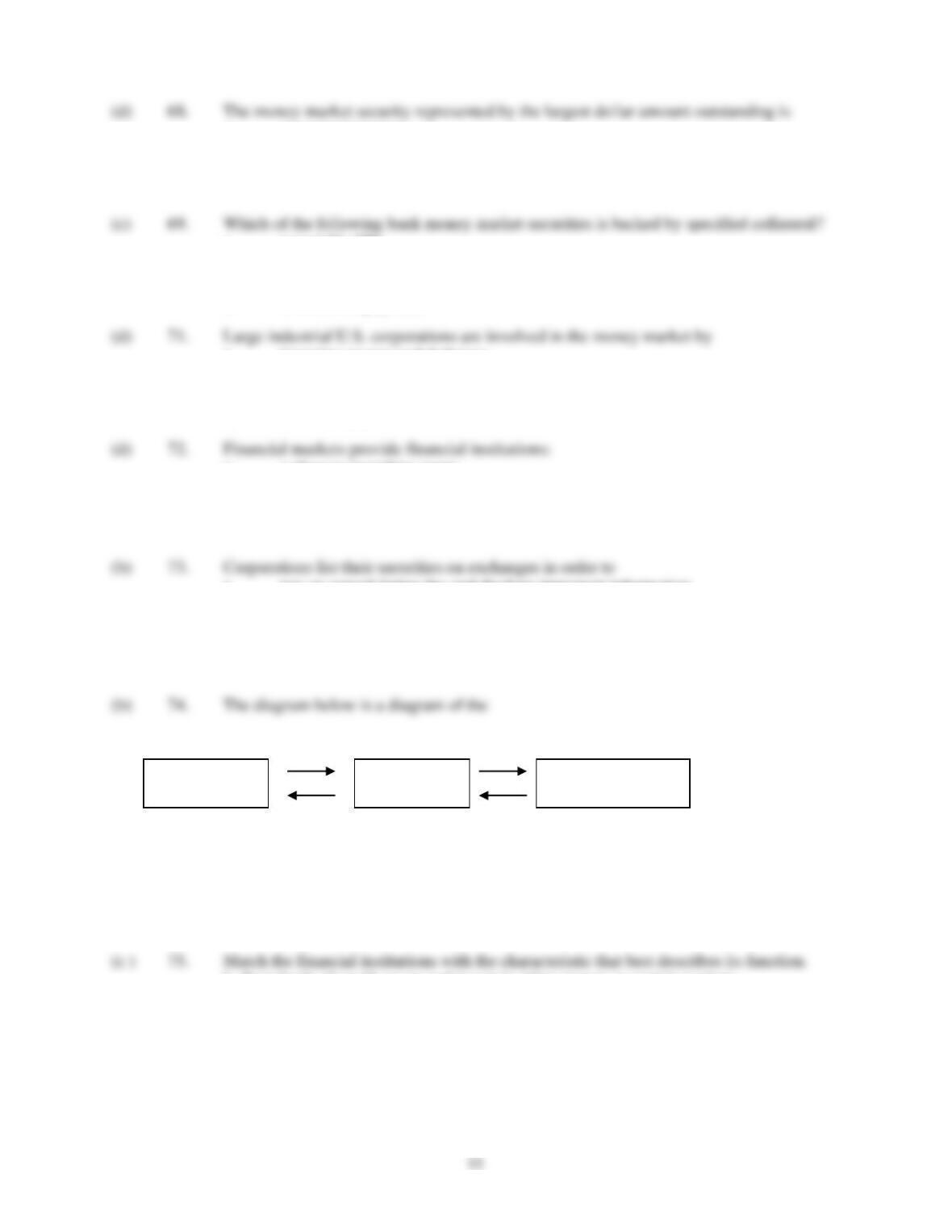

Users of Funds

(DSU)

Underwriter

Suppliers of Funds (SSU)

12

4. Securities firms and investment banks

5. Mutual funds

a. 1, 3, 2, 5, 4

b. 4, 2, 3, 5, 1

c. 5, 2, 1, 4, 3

d. 2, 4, 5, 3, 1

e. 5, 1, 3, 2, 4

a. offer primary market purchasers liquidity for their holdings

b. reduce the cost of trading the primary market claims

c. help investors diversify portfolios

d. update the price or value of the primary market claims

e. all above

ESSAY QUESTIONS

1. Explain financial intermediation and its benefits.

2. Explain how and why the secondary capital markets play an important role in our economy. How

do secondary markets assist the primary market?

3. List and briefly describe the main risks managed by financial intermediaries.

4. Discuss the major functions provided by investment banks and security firms.