21

tax free to P&G because it is an intracompany transfer. If the exchange offer had not been fully subscribed, P&G would have

distributed through a tax-free spin-off the remaining shares as a dividend to P&G shareholders.

The transaction agreement outlined the terms and conditions pertinent to completion of the merger with Diamond Foods.

Immediately after the completion of the distribution, the Pringles Company merged with Merger Sub, a wholly owned shell

subsidiary of Diamond, with Merger Sub’s continuing as the surviving company. The shares of Pringles Company common

stock distributed in connection with the split-off exchange offer automatically converted into the right to receive shares of

Diamond common stock on a one-for-one basis. After the merger, Diamond, through Merger Sub, owned and operated Pringles

(see Figure 16.3).

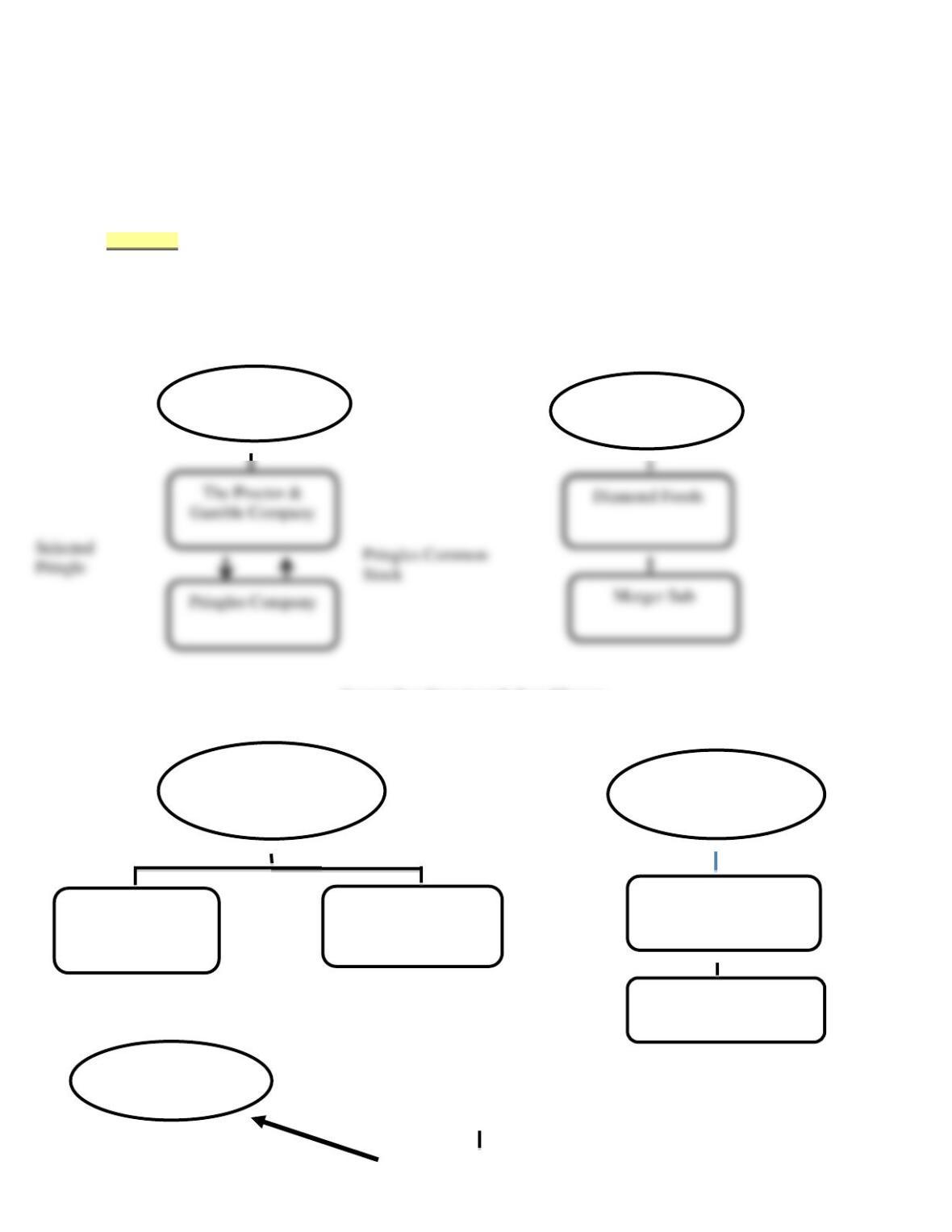

Figure 16.3

Reverse Morris Trust.

P&G

Shareholders

Diamond

Shareholders

Pre-Merger Structure

Separation Structure before Merger

P&G Shareholders

(incl. exchange offer

participants)

The Proctor &

Gamble Company

Pringle Company

(owns Pringle’s

assets and liabilities)

Diamond Foods

Merger Sub

(Acquisition Vehicle)

Diamond

Shareholders

Post-Merger Structure

Current & Former

P&G

Sharehold

22

Prior to the merger, Diamond already had formidable antitakeover defenses in place as part of its charter documents,

including a classified board of directors, a prohibition against stockholders’ taking action by written consent (i.e., consent

solicitation), and a requirement that stockholders give advance notice before raising matters at a stockholders’ meeting.

Following the merger, Diamond adopted a shareholder–rights plan. The plan entitled the holder of such rights to purchase 1/100

of a share of Diamond’s Series A Junior Participating Preferred Stock if a person or group acquires 15% or more of Diamond’s

outstanding common stock. Holders of this preferred stock (other than the person or group triggering their exercise) would be

able to purchase Diamond common shares (flip-in poison pill) or those of any company into which Diamond is merged (flip–

over poison pill) at a price of $60 per share. Such rights would expire in March 2015 unless extended by Diamond’s board of

directors.

Discussion Questions:

1. The merger of Pringles and Diamond Foods could have been achieved as a result of a P&G spin-off of

Pringles. Explain the details of how this might happen.

2. Speculate as to why P&G chose to split-off rather than spin-off Pringles as part its plan to merge Post with Ralcorp.

Be specific.

3. Why was this transaction subject to the Morris Trust tax regulations?

4. How is value created for the P&G and Diamond shareholders in this type of transaction?

Diamond Foods

Merger Sub

Pringle Company (owns

Pringles assets/liabilities)

Diamond

Common

Shares

23

5. Why did the addition of the shareholder rights plan by Diamond Foods following the merger with Pringles make sense

given the type of deal structure used?

The Anatomy of a Spin-Off—Northrop Grumman Exits the Shipbuilding Business

_____________________________________________________________________________________________

Key Points

There are many ways a firm can choose to separate itself from one of its operations.

Which restructuring method is used reflects the firm’s objectives and circumstances.

______________________________________________________________________________

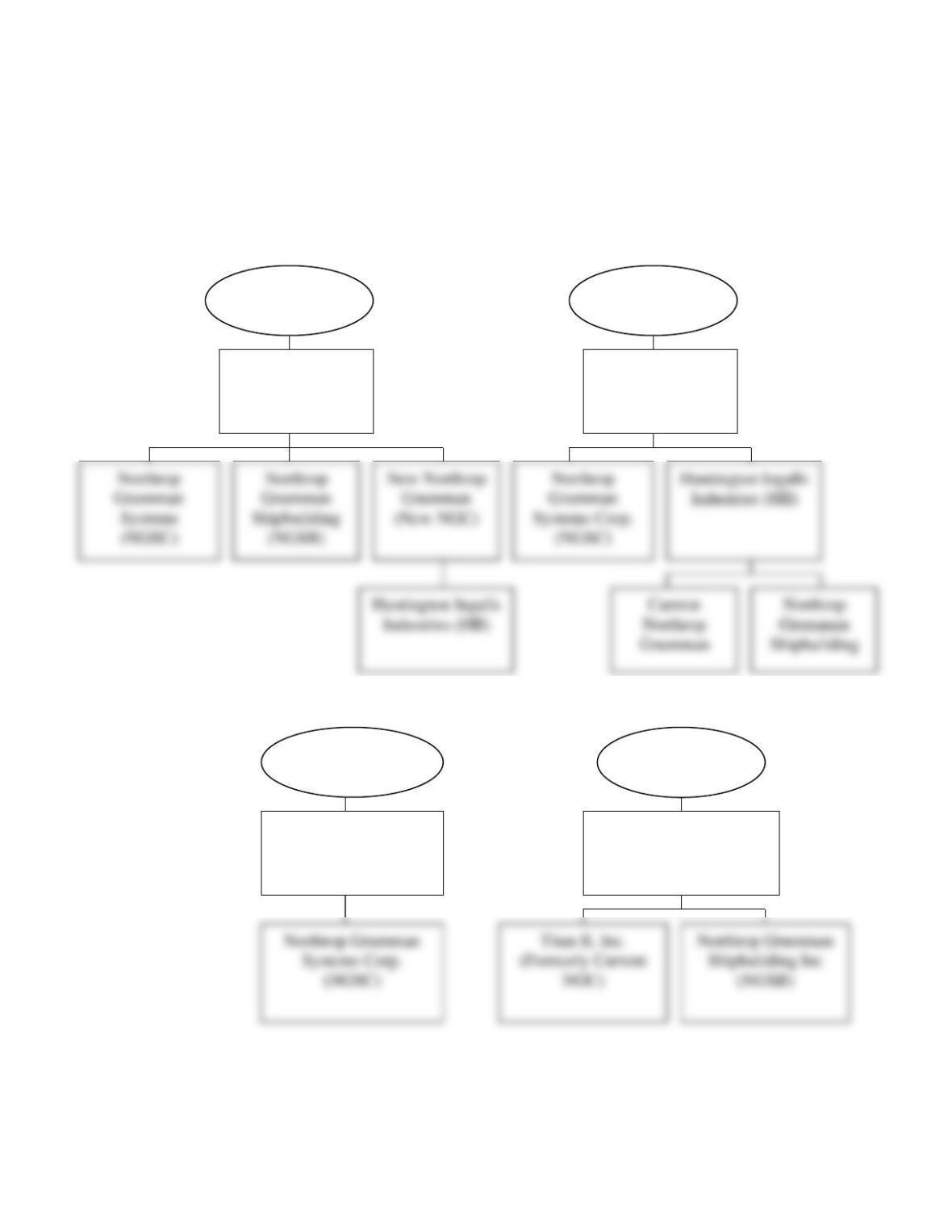

In an effort to focus on more attractive growth markets, Northrop Grumman Corporation (NGC), a global leader in aerospace,

communications, defense, and security systems, announced that it would exit its mature shipbuilding business on October 15,

2010. Huntington Ingalls Industries (HII), the largest military U.S. shipbuilder and a wholly owned subsidiary of NGC, had

been under pressure to cut costs amidst increased competition from competitors such as General Dynamics and a slowdown in

orders from the U.S. Navy. Nor did the outlook for the shipbuilding industry look like it would improve any time soon.

Given the limited synergy between shipbuilding and HII’s other businesses, HII’s operations were largely independent of

NGC’s other units. NGC’s management and board argued that their decision to separate from the shipbuilding business would

enable both NGC and HII to focus on those areas they knew best. Moreover, given the shipbuilding business’s greater ongoing

capital requirements, HII would find it easier to tap capital markets directly rather than to compete with other NGC operations

for financing. Finally, investors would be better able to value businesses (NGC and HII) whose operations were more focused.

The spin-off process involved an internal reorganization of NGC businesses, a Separation and Distribution Agreement, and

finally the actual distribution of HII shares to NGC shareholders. The internal reorganization and subsequent spin-off is

illustrated in Figure 16.4. NGC (referred to as Current Northrop Grumman Corporation) first reorganized its businesses such

that the firm would become a holding company whose primary investments would include Huntington Ingalls Industries (HII)

and Northrop Grumman Systems Corporation (i.e., all other non-shipbuilding operations). HII was formed in anticipation of

the spin-off as a holding company for NGC’s shipbuilding business, which had been previously known as Northrop Grumman

Shipbuilding (NGSB). NGSB was changed to Huntington Ingalls Industries Company following the spin-off. Reflecting the

new organizational structure, Current Northrop Grumman common stock was exchanged for stock in New Northrop Grumman

Corporation. This internal reorganization was followed by the distribution of HII stock to NGC’s common shareholders.

Following the spin-off, HII became a separate company from NGC, with NGC having no ownership interest in HII.

Renamed Titan II, Current NGC became a direct, wholly owned subsidiary of HII and held no material assets or liabilities

other than Current NGC’s guarantees of HII performance under certain HII shipbuilding contracts (under way prior to the spin–

off and guaranteed by NGC) and HII’s obligations to repay intercompany loans owed to NGC. New NGC changed its name to

Northrop Grumman Corporation. The board of directors remained the same following the reorganization.

No gain or loss was incurred by common shareholders because the exchange of stock between the Current and New

Northrop Grumman corporations did not change the shareholders’ tax basis in the stock. Similarly, no gain or loss was incurred

by shareholders with the distribution of HII’s stock, since there was no change in the total value of their investment. That is,

the value of the HII shares were offset by a corresponding reduction in the value of NGC shares, reflecting the loss of HII’s

cash flows.

Before the spin-off, HII entered into a Separation and Distribution Agreement with NGC that governed the relationship

between HII and NGC after completion of the spin-off and provided for the allocation between the two firms of assets,

liabilities, and obligations (e.g., employee benefits, intellectual property, information technology, insurance, and tax–related

assets and liabilities). The agreement also provided that NGC and HII each would indemnify (compensate) the other against

any liabilities arising out of their respective businesses. As part of the agreement, HII agreed not to engage in any transactions,

such as mergers or acquisitions, involving share-for-share exchanges that would change the ownership of the firm by more than

50% for at least two years following the transaction. A change in control could violate the IRS’s “continuity of interest”

requirement and jeopardize the tax-free status of the spin-off. Consequently, HII put in place certain takeover defenses to make

takeovers difficult.

Discussion Questions

1. Speculate as to why Northrop Grumman used a spin-off rather than a divestiture, split-off or split up to separate

Huntington Ingalls from the rest of its operations? What were the advantages of the spin–off over the other restructuring

strategies.

2. What is the likely impact of the spin–off on Northrop Grumman’s share price immediately following the spin-off of

Huntington Ingalls assuming no other factors offset it?

3. Why do businesses that have been spun off from their parent often immediately put antitakeover defenses in place?

4. Why would the U.S. Internal Revenue Service be concerned about a change of control of the spun-off business such

that it might revoke its ruling that the spin-off satisfied the requirements to be tax-free?

.

5. Describe how you as an analyst would estimate the potential impact of the Huntington Ingalls Industries spin–off on

the long–term value of Northrop Grumman’s share price?

26

Kraft Foods Splits Up in Its Biggest Deal Yet

Current Northrop

Grumman Corp

(CNGC)

New Northrop

Grumman Corp

Public

Shareholders

Public

Shareholders

Northrop Grumman

(Formerly New NGC)

Huntington Ingalls

Industries (HII)

Public

Shareholders

Public

Shareholders

NGC Post-Spin-Off HII Post-Spin-Off

_____________________________________________________________________________________________________

Key Points

Investors often evaluate a firm’s performance in terms of how well it does as compared to its peers.

Activist investors can force an underperforming firm to change its strategy radically.

The Kraft decision to split its businesses is yet another example of the recent trend by highly diversified businesses to increase

their product focus.

_____________________________________________________________________________________________________

Following a successful career as CEO of PepsiCo’s Frito-Lay, Irene Rosenfeld became the CEO of Kraft Foods in 2006. As the

world’s second-largest packaged foods manufacturer, behind Nestlé, Kraft had stumbled in its efforts to increase its global

reach by growing in emerging markets. Its brands tended to be old, and the firm was having difficulty developing new, trendy

products. Rosenfeld was tasked by its board of directors with turning the firm around. She reasoned that it would take a

complete overhaul of Kraft, including organization, culture, operations, marketing, branding, and the product portfolio, to

transform the firm.

In 2010, the firm made what at the time was viewed by top management as its most transformational move by acquiring

British confectionery company Cadbury for $19 billion. While the firm became the world’s largest snack company with the

completion of the transaction, it was still entrenched in its traditional business, groceries. The company now owned two very

different product portfolios.

Between January 2010 and mid–2011, Kraft’s earnings steadily improved, powered by stronger sales. Kraft shares rose

almost 25%, more than twice the increase in the S&P 500 stock index. However, it continued to trade throughout this period at

a lower price–to-earnings multiple than such competitors as Nestlé and Groupe Danone. Some investors were concerned that

Kraft was not realizing the promised synergies from the Cadbury deal. Activist investors (Nelson Peltz’s Trian Fund and Bill

Ackman’s Pershing Square Capital Management) had discussions with Kraft’s management about splitting the firm. This plan

had the support of Warren Buffett, whose conglomerate, Berkshire Hathaway, was Kraft’s largest investor at that time, with a

6% ownership interest.

To avert a proxy fight, Kraft’s board and management announced on August 4, 2011, its intention to restructure the firm

radically by separating it into two distinct businesses. Coming just 18 months after the Cadbury deal, investors were initially

stunned by the announcement but appeared to avidly support the proposal avidly by driving up the firm’s share price by the end

of the day. The proposal entailed separating its faster-growing global snack food business from its slower-growing, more

United States–centered grocery business. The separation was completed through a tax-free spin-off to Kraft Food shareholders

of the grocery business on October 1, 2012. The global snack food business will be named Mondelez International, while the

North American grocery business will retain the Kraft name.

Management justified the proposed split-up of the firm as a means of increasing focus, providing greater opportunities, and

giving investors a choice between the faster-growing snack business and the slower-growing but more predictable grocery

operation. Management also argued that the Cadbury acquisition gave the snack business scale to compete against such

competitors as Nestlé and PepsiCo.

Discussion Questions

1. Speculate as to why Kraft chose not to divest its grocery business and use the proceeds to either reinvest in its faster

growing snack business, to buy back its stock, or a combination of the two?

28

2. How might a spin-off create shareholder value for Kraft Foods shareholders?

3. There is often a natural tension between so-called activist investors interested in short-term profits and a firm’s

management interested in pursuing a longer-term vision. When is this tension helpful to shareholders and when does it

destroy shareholder value?

GENERAL ELECTRIC DOWNSIZES

ITS FINANCIAL SERVICES UNIT

_____________________________________________________________________________________

Key Points

• Exiting a business can take many forms ranging from an outright sale to an initial public offering to a split-off.

• The exit can take place at a moment in time or be phased over a period of time.

• The choice of the appropriate restructuring strategy reflects an array of factors including the parent firm’s need for

cash, the availability of potential buyers, and tax considerations.

______________________________________________________________________________

Long synonymous with the word conglomerate, General Electric had skillfully managed for years its highly diverse business

portfolio profitably. GE Capital had been a major profit generator for General Electric Corporation for decades, often

contributing more than one–half of the parent firm’s operating profits. The firm’s exposure to the financial services industry

had provided sustained growth and had tended to offset some of the cyclicality of its industrial businesses. GE Capital had been

managed as a cash cow to generate new funds to finance the parent’s forays into new businesses.

All that changed with the collapse of the global financial markets in 2008. GE shares plummeted immediately following the

bankruptcy of mega investment bank Lehman Brothers, as investors expressed concern about the conglomerate’s ability to

support its financial services businesses. Huge holdings of commercial loans whose value was questionable along with its

substantial risk exposure as a subprime residential home loan lender raised the prospect that GE Capital would be forced into

bankruptcy.

Recognizing the key role played by the business in the U.S. economy, U.S. regulators declared it as a “systemically

important financial institution.” This meant that the government could take over the business in an effort to wind it down in an

orderly manner if it were declared to be insolvent in an effort to blunt any ripple effect that the demise of such a large

institution might have on global financial markets. The net result would be huge financial losses for GE shareholders. To

minimize this potential outcome, GE decided to reduce substantially its vulnerability to the financial services industry.

Despite efforts in recent years to downsize the operation by divesting in 2010 its commercial real estate business for $251

billion, GE Capital remained a major revenue generator for General Electric. In 2013, the unit’s annual revenue totaled $44.1

billion, about 30% of the parent’s consolidated revenue.

To accelerate its efforts to restructure GE Capital, the unit’s retail finance operation was renamed Synchrony Financial and

taken public through an initial public offering in late 2014. Synchrony processes credit card transactions for major retailers

such as the Gap and Walmart. The IPO represented 20% of Synchrony shares. By issuing only 20% of its shares, GE would be

able to consolidate the unit’s financials for tax purposes. The IPO enabled GE to establish a value for the business and to

create a liquid market for the unit’s stock, a factor that was to make the second half of GE’s exit strategy for this business

29

possible. The proceeds of the IPO were used to pay certain intercompany loans owed to General Electric Corporation and to

add to the new company’s capital base.

In 2015, GE will completely exit the remaining 80% of its retail finance business through a so-called transaction consisting

of a tax-free distribution of its remaining interest in Synchrony to GE shareholders willing to exchange their shares of GE

common for Synchrony Financial shares. Any remaining shares in Synchrony not disposed of through the share exchange will

be paid out as a dividend to GE shareholders. In doing so, GE will be totally rid of its retail finance unit.

GE decided to undertake this staged divestment of its retail finance unit because of its huge size and the inability to find a

buyer for the entire business. The obvious potential acquirers are other large financial institutions which continue to find

themselves capital constrained and as such unlikely to be permitted by regulators to undertake such a large acquisition.

Consequently, GE’s options for exiting this business were limited.

The Warner Music Group is Sold at Auction

_____________________________________________________________________________________________________

Key Points

In selling a business, a firm may choose either to negotiate with a single potential buyer, to control the number of potential

bidders, or to engage in a public auction.

The auction process often is viewed as the most effective way to get the highest price for a business to be sold; however, far

from simple, an auction can be both a chaotic and a time-consuming procedure.

Auctions may be most suitable for businesses whose value is largely intangible or for “hard–to–value” businesses.

____________________________________________________________________________________________________

In early 2011, the Warner Music Group (WMG), the third largest of the “big four” recorded–music companies, consisted of two

separate businesses: one showing high growth potential and the other with declining revenues. Of WMG’s $3 billion in annual

revenue, 82% came from sales of recorded music, with the remainder attributed to royalty payments for the use of music

owned by the firm. Of the two, only recorded music has suffered revenue declines, due to piracy, aggressive pricing of online

music sales, and the bankruptcy of many record retailers and wholesalers. In contrast, music publishing has grown as a result of

diverse revenue streams from radio, television, advertising, and other sources. Music publishing also is benefiting from digital

music downloads and the proliferation of cellphone ringtones.

By the end of January 2011, WMG had solicited about 70 potential bidders and attracted unsolicited indications of interest

from at least 20 others. As this group winnowed through the auction’s three rounds, alliances among the bidders continually

changed. In the ensuing auction, WMG’s stock price jumped by 75% from $4.72 per share on January 20 to $8.25 per share,

for a total market value of $3.3 billion on May 6, 2011.

In view of the differences between these two businesses, WMG was open to selling the firm in total or in pieces,

contributing to the extensive bidder interest. Risk takers were betting on an eventual recovery in recorded-music sales, while

risk-averse investors were more likely to focus on music publishing. Prior to the auction, WMG distributed confidentiality

agreements to 37 suitors, with 10 actually submitting a preliminary bid by the deadline of February 22, 2011. Of the

preliminary bids, four were for the entire company, three for recorded music, and three for music publishing. For the entire

firm, prices ranged from a low bid of $6 per share to a high bid of $8.25 per share. For recorded music, bids ranged from a low

of $700 million to a high of $1.1 billion. Music publishing bids were almost twice that of recorded music, ranging from a low

of $1.45 billion to a high of $2 billion.

For bidders, the objective is to make it to the next round in the auction; for sellers, the objective is less about prices offered

during the initial round and more about determining who is committed to the process and who has the financial wherewithal to

consummate the deal. According to the firm’s proxy pertaining to the sale, released on May 20, 2011, the subsequent bidding

was characterized as a series of ever-changing alliances among bidders, with Access Industries submitting the winning bid. The

sale appears to have been a success from the investors’ standpoint, with some speculating that THL alone earned an internal

rate of return (including dividends) of 34%.4

Motorola Bows to Activist Pressure

Under pressure from activist investor Carl Icahn, Motorola felt compelled to make a dramatic move before its May 2008

shareholders’ meeting. Icahn had submitted a slate of four directors to replace those up for reelection and demanded that the

wireless handset and network manufacturer take actions to improve profitability. Shares of Motorola, which had a market value

of $22 billion, had fallen more than 60% since October 2006, making the firm’s board vulnerable in the proxy contest over

director reelections.

Signaling its willingness to take dramatic action, Motorola announced on March 26, 2008, its intention to create two

independent, publicly traded companies. The two new companies would consist of the firm’s former Mobile Devices operation

(including its Home Devices businesses consisting of modems and set-top boxes) and its Enterprise Mobility Solutions &

Wireless Networks business. In addition to the planned spin-off, Motorola agreed to nominate two people supported by Carl

Icahn to the firm’s board. Originally scheduled for 2009, the breakup was postponed due to the upheaval in the financial

markets that year. The breakup would result in a tax-free distribution to Motorola’s shareholders, with shareholders receiving

shares of the two independent and publicly traded firms.

Motorola’s board is seeking to ensure the financial viability of Motorola Mobility by eliminating its outstanding debt and

through a cash infusion. To do so, Motorola intends to buy back nearly all of its outstanding $3.9 billion debt and to transfer as

much as $4 billion in cash to Motorola Mobility. Furthermore, Motorola Solutions would assume responsibility for the pension

obligations of Motorola Mobility. If Motorola Mobility were to be forced into bankruptcy shortly after the breakup, Motorola

Solutions may be held legally responsible for some of the business’s liabilities. The court would have to prove that Motorola

had conveyed the Mobility Devices unit (renamed Motorola Mobility following the breakup) to its shareholders, fraudulently

knowing that the unit’s financial viability was problematic.

Once free of debt and other obligations and flush with cash, Motorola Mobility would be in a better position to make

acquisitions and to develop new phones. It would also be more attractive as a takeover target. A stand-alone firm is

unencumbered by intercompany relationships, including such things as administrative support or parts and services supplied by

other areas of Motorola. Moreover, all liabilities and assets associated with the handset business already would have been

identified, making it easier for a potential partner to value the business.

In mid-2010, Motorola Inc. announced that it had reached an agreement with Nokia Siemens Networks, a Finnish-German

joint venture, to buy the wireless networks operations, formerly part of its Enterprise Mobility Solutions & Wireless Network

Devices business for $1.2 billion. On January 4, 2011, Motorola Inc. spun off the common shares of Motorola Mobility it held

as a tax-free dividend to its shareholders and renamed the firm Motorola Solutions. Each shareholder of record as of December

21, 2010, would receive one share of Motorola Mobility common for every eight shares of Motorola Inc. common stock they

held. Table 15.3 shows the timeline of Motorola’s restructuring effort.

Discussion Questions

1. In your judgment, did the breakup of Motorola make sense? Explain your answer.

2. What other restructuring alternatives could Motorola have pursued to increase shareholder value? Why do you believe it

pursued this breakup strategy rather than some other option?

Table 15.3

Motorola Restructure Timeline

Motorola (Beginning 2010)

Motorola (Mid-2010)

Motorola (Beginning 2011)

Mobility Devices

Mobility Devices

Motorola Mobility spin-off

Enterprise Mobility Solutions &

Wireless Networks

Enterprise Mobility Solutions*

Motorola Inc. renamed Motorola

Solutions

*Wireless Networks sold to Nokia-Siemens.

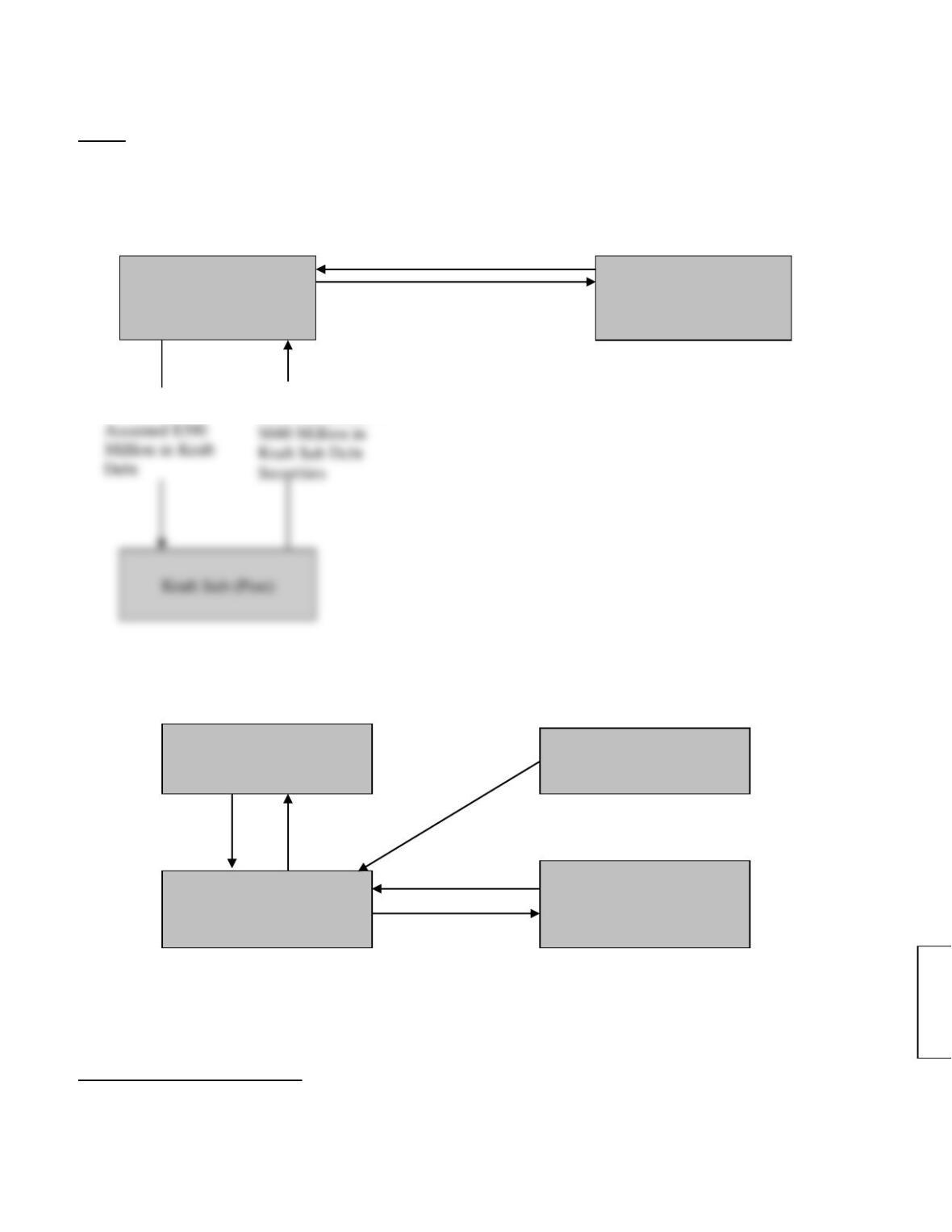

Kraft Foods Undertakes Split-Off of Post Cereals in Merger-Related Transaction

In August 2008, Kraft Foods announced an exchange offer related to the split-off of its Post Cereals unit and the closing of the

merger of its Post Cereals business into a wholly-owned subsidiary of Ralcorp Holdings. Kraft is a major manufacturer and

distributor of foods and beverages; Post is a leading manufacturer of breakfast cereals; and Ralcorp manufactures and

distributes brand-name products in grocery and mass merchandise food outlets. The objective of the transaction was to allow

Kraft shareholders participating in the exchange offer for Kraft Sub stock to become shareholders in Ralcorp and Kraft to

receive almost $1 billion in cash or cash equivalents on a tax-free basis.

With the completion of the merger of Kraft Sub with Ralcorp Sub (a Ralcorp wholly-owned subsidiary), the common shares

of Kraft Sub were exchanged for shares of Ralcorp stock on a one for one basis. Consequently, Kraft shareholders tendering

their Kraft shares in the exchange offer owned 0.6606 of a share of Ralcorp stock for each Kraft share exchanged as part of the

split-off.

Concurrent with the exchange offer, Kraft closed the merger of Post with Ralcorp. Kraft shareholders received Ralcorp

stock valued at $1.6 billion, resulting in their owning 54% of the merged firm. By satisfying the Morris Trust tax code

regulations,6 the transaction was tax free to Kraft shareholders. Ralcorp Sub was later merged into Ralcorp. As such, Ralcorp

assumed the liabilities of Ralcorp Sub, including the $660 million owed to Kraft.

The purchase price for Post equaled $2.56 billion. This price consisted of $1.6 billion in Ralcorp stock received by Kraft

shareholders and $960 million in cash equivalents received by Kraft. The $960 million included the assumption of the $300

million liability by Kraft Sub and the $660 million in debt securities received from Kraft Sub.7 The steps involved in the

transaction are described in Exhibit 15.1.

Discussion Questions and Answers:

1. What does the decision to split up the firm say about Kraft’s decision to buy Cadbury in 2010?

2. Why did Kraft chose not to divest its grocery business, using the proceeds to either reinvest in its faster growing snack

business, to buy back its stock, or a combination of the two?

3. How might a spin-off create shareholder value for Kraft Foods shareholders?

4. Kraft CEO Irene Rosenfeld argued that an important justification for the Cadbury acquisition in 2010 was to create

two portfolios of businesses: some very strong cash generating businesses and some very strong growth businesses in

order to increase shareholder value. How might this strategy have boosted the firm’s value?

5. While Kraft’s share value did increase following the Cadbury deal, it lagged the performance of key competitors. Why

do you believe this was the case? Explain your answer.

6. There is often a natural tension between so-called activist investors interested in short–term profits and a firm’s

management interested in pursuing a longer-term vision. When is this tension helpful to shareholders and when does it

destroy shareholder value?

33

Exhibit 15-1. Structuring the Transaction

Step 1: Kraft creates a shell subsidiary (Kraft Sub) and transfers Post assets and liabilities and

$300 million in Kraft debt into the shell in exchange for Kraft Sub stock plus $660 million in

Kraft Sub debt securities. Kraft also implements an exchange offer of Kraft Sub for Kraft

common stock.

Step 2: Kraft Sub, as an independent company, is merged in a forward triangular tax–free merger with a sub of Ralcorp

(Ralcorp Sub) in which Kraft Sub shares are exchanged for Ralcorp shares, with Ralcorp Sub surviving.8

Sara Lee Attempts to Create Value through Restructuring

8 The merger is tax free to Kraft Sub shareholders in that it results in Kraft Sub shareholders owning a significant ongoing

interest in Ralcorp and Ralcorp owing the Kraft Sub assets. Consequently, both the continuity of interests and the continuity of

business enterprise principles are satisfied. See Chapter 12 for a more detailed discussion of these issues.

Kraft Shareholders

Tendering Kraft Shares

Kraft Foods

Post Assets &

Liabilities +

Kraft Sub

Common Shares +

Kraft Shares

Kraft Sub Shares

Ralcorp

Ralcorp Sub

Kraft Sub (Post)

Kraft Sub Shareholders

(i.e., former Kraft

Shareholders)

Ralcorp

Stock

Ralcorp

Sub Stock

Kraft Sub Assets & Liabilities

Ralcorp

Stock

Kraft Sub

Stock

34

After spurning a series of takeover offers, Sara Lee, a global consumer goods company, announced in early 2011 its intention

to split the firm into two separate publicly traded companies. The two companies would consist of the firm’s North American

retail and food service division and its international beverage business. The announcement comes after a long string of

restructuring efforts designed to increase shareholder value. It remains to be seen if the latest effort will be any more successful

than earlier efforts.

Reflecting a flawed business strategy, Sara Lee had struggled for more than a decade to create value for its shareholders by

radically restructuring its portfolio of businesses. The firm’s business strategy had evolved from one designed in the mid-1980s

to market a broad array of consumer products from baked goods to coffee to underwear under the highly recognizable brand

name of Sara Lee into one that was designed to refocus the firm on the faster-growing food and beverage and apparel

businesses. Despite acquiring several European manufacturers of processed meats in the early 1990s, the company’s profits and

share price continued to flounder.

Despite these restructuring efforts, the firm’s stock price continued to drift lower. In an attempt to reverse the firm’s

misfortunes, the firm announced an even more ambitious restructuring plan in 2000. Sara Lee would focus on three main areas:

food and beverages, underwear, and household products. The restructuring efforts resulted in the shutdown of a number of

meat packing plants and a number of small divestitures, resulting in a 10% reduction (about 13,000 people) in the firm’s

workforce. Sara Lee also completed the largest acquisition in its history, purchasing The Earthgrains Company for $1.9 billion

plus the assumption of $0.9 billion in debt. With annual revenue of $2.6 billion, Earthgrains specialized in fresh packaged

bread and refrigerated dough. However, despite ongoing restructuring activities, Sara Lee continued to underperform the

broader stock market indices.

In February 2005, Sara Lee executed its most ambitious plan to transform the firm into a company focused on the global

food, beverage, and household and body care businesses. To this end, the firm announced plans to dispose of 40% of its

revenues, totaling more than $8 billion, including its apparel, European packaged meats, U.S. retail coffee, and direct sales

businesses.

In 2006, the firm announced that it had completed the sale of its branded apparel business in Europe, Global Body Care and

European Detergents units, and its European meat processing operations. Furthermore, the firm spun off its U.S. Branded

Apparel unit into a separate publicly traded firm called HanesBrands Inc. The firm raised more than $3.7 billion in cash from

the divestitures. The firm was now focused on its core businesses: food, beverages, and household and body care.

In late 2008, Sara Lee announced that it would close its kosher meat processing business and sold its retail coffee business.

In 2009, the firm sold its Household and Body Care business to Unilever for $1.6 billion and its hair care business to Procter &

Gamble for $0.4 billion.

In 2010, the proceeds of the divestitures made the prior year were used to repurchase $1.3 billion of Sara Lee’s outstanding

shares. The firm also announced its intention to repurchase another $3 billion of its shares during the next three years. If

completed, this would amount to about one-third of its approximate $10 billion market capitalization at the end of 2010.

What remains of the firm are food brands in North America, including Hillshire Farm, Ball Park, and Jimmy Dean

processed meats and Sara Lee baked goods and Earthgrains. A food distribution unit will also remain in North America, as will

its beverage and bakery operations. Sara Lee is rapidly moving to become a food, beverage, and bakery firm. As it becomes

more focused, it could become a takeover target.

Has the 2005 restructuring program worked? To answer this question, it is necessary to determine the percentage change in

Sara Lee’s share price from the announcement date of the restructuring program to the end of 2010, as well as the percentage