Chapter 11: Structuring the Deal:

Payment and Legal Considerations

Answers to End of Chapter Discussion Questions

11.1 What are the advantages and disadvantages of a purchase of assets from the perspective of the buyer and seller?

11.2 What are the advantages and disadvantages of a purchase of stock from the perspective of the buyer and seller?

11.3 What are the advantages and disadvantages of a statutory merger?

11.4 What are the reasons some acquirers choose to undertake a staged or multi-step takeover?

11.5 What forms of acquisition represent common alternatives to a merger? Under what circumstances might these

alternative structures be employed?

11.6 Comment of the following statement. A premium offered by a bidder over a target’s share price is not necessarily

a fair price; a fair price is not necessarily an adequate price?

11.7 In early 2008, a year marked by turmoil in the global credit markets, Mars Corporation was able to negotiate a

reverse breakup fee structure in its acquisition of Wrigley Corporation. This structure allowed Mars to walk away

from the transaction at any time by paying a $1 billion fee. Speculate as to the motivation behind Mars and

Wrigley negotiating such a fee structure?

11.8 Despite disturbing discoveries during due diligence, Mattel acquired The Learning Company (TLC), a leading

developer of software for toys, in a stock–for-stock transaction valued at $3.5 billion on May 13, 1999. Mattel had

determined that TLC’s receivables were overstated because product returns from distributors were not deducted

from receivables and its allowance for bad debt was inadequate. A $50 million licensing deal also had been

prematurely put on the balance sheet. Finally, TLC’s brands were becoming outdated. TLC had substantially

exaggerated the amount of money put into research and development for new software products. Nevertheless,

driven by the appeal of rapidly becoming a big player in the children’s software market, Mattel closed on the

transaction aware that TLC’s cash flows were overstated. Despite being aware of extensive problems, Mattel

proceeded to acquire The Learning Company. Why? What could Mattel to better protect its interests? Be specific.

`11.9 Describe the conditions under which an earnout may be most appropriate?

11.10 In late 2008, Deutsche Bank announced that would buy the commercial banking assets (including a number of

branches) of Netherland’s ABN Amro for $1.13 billion. What liabilities, if any, would Deutsche Bank have to (or

want to) assume? Explain your answer.

Solutions to Chapter Case Study Questions

Portfolio Review Redefines Breakup Strategy for Newly Formed DowDuPont Corporation

Discussion Questions and Answers:

1. In what way have activist investors assumed the role of hostile takeovers in influencing underperforming

managers?

3

2. Do you think that the restructuring strategy set in motion with the creation of DowDuPont makes sense? What

alternative was available to both Dow and DuPont had they remained independent? Be specific.

3. Speculate as to why the deal was structured as a merger of equals. What are the advantages and disadvantages of

such a structure? Be specific.

4. What are the key assumptions DowDuPont is making in arguing the merger followed by the spin-off of three

businesses makes sense?

5. What is the form of payment and the form of acquisition used in this deal? What are the advantageous and

disadvantageous of the form of payment and acquisition used in this deal?

6. In the deal, Dow shareholders will receive a fixed exchange ratio of 1.00 share of DowDuPont for each Dow

share, and DuPont shareholders will receive a fixed exchange ratio of 1.28 shares in DowDuPont for each

DuPont share. Dow and DuPont shareholders will each own approximately 50 percent of the combined

company, excluding preferred shares. Common shares outstanding at Dow and DuPont at the time of the

announcement were 1.160 billion and .876 billion respectively. Using this information, show how the postclosing

ownership distribution can be determined. How might these fixed share exchange ratios have been determined

during the negotiation of the deal?

7. Dow’s price per share on December 11, 2015 was $54.91 and DuPont’s was $74.55. Dow shares outstanding were

1.16 billion and DuPont’s outstanding shares were .876 billion. Assume anticipated annual cost synergies are $ 3.0

billion in perpetuity and DowDuPont’s cost of capital is 10%. What is DowDuPont’s total market cap excluding

synergy? What is the market cap including synergy using the zero growth method of valuation (see Chapter 7)?

Examination Questions and Answers

1. Deal structuring is fundamentally about satisfying as many of the primary objectives of the parties involved and

deciding how risk will be shared. True or False

2. The acquisition vehicle is the legal structure used to acquire the target. True or False

3. Such legal structures as holding company, joint venture, and limited liability corporations are suitable only for

acquisition vehicles but not post closing organizations. True or False

4. Employee stock ownership plans cannot be legally used to acquire companies. True or False

5. Form of payment refers only to the acquirer’s common stock used to make up the purchase price paid to target

shareholders. True or False

6. The appropriate deal structure is that which satisfies, without regard to risk, as many of the primary objectives of

the parties involved as necessary to reach overall agreement. True or False

7. Form of payment may consist of something other than cash, stock, or debt such as tangible and intangible assets.

True or False

8. If the form of acquisition is a statutory merger, the seller retains all known, unknown or contingent liabilities.

True or False

9. The form of payment does not affect whether a transaction is taxable to the seller’s shareholders. True or False

10. The assumption of seller liabilities by the buyer in a merger may induce the seller to demand a higher selling price.

True or False

11. The acquirer may reduce the total cost of an acquisition by deferring some portion of the purchase price. True or

False

12. A holding company structure is the preferred post-closing organization if the acquiring firm is interested in

integrating the target firm immediately following acquisition. True or False

13. The acquired company should be fully integrated into the acquiring company if an earn–out is used to consummate

the transaction. True or False

14. When buyers and sellers cannot reach agreement on price, other mechanisms can be used to close the gap. These

include balance sheet adjustments, earn-outs, rights to intellectual property, and licensing fees. True or False

15. In a balance sheet adjustment, the buyer increases the total purchase price by an amount equal to the decrease in

net working capital or shareholders’ equity of the target company. True or False

16. Because they can be potentially so lucrative to sellers, earn-outs are sometimes used to close the gap between what

the seller wants and what the buyer might be willing to pay. True or False

17. Earn-outs tend to shift risk from the seller to the buyer in that a higher price is paid only when the seller has met or

exceeded certain performance criteria. True or False

18. Rights to intellectual property, royalties from licenses and employment agreements are often used to close the gap

on price between what the seller wants and what the buyer is willing to pay because the income generated is tax

free to the recipient. True or False

19. Asset purchases require the acquiring company to buy all or a portion of the target company’s assets and to assume

at least some of the target’s liabilities in exchange for cash or stock. True or False

20. Stock purchases involve the exchange of the target’s stock for cash, debt, stock of the acquiring company, or some

combination. True or False

21. Sellers may find a sale of assets attractive because they are able to maintain their corporate existence and therefore

ownership of tangible assets not acquired by the buyer and intangible assets such as licenses, franchises, and

patents. True or False

22. In a statutory merger, only assets and liabilities shown on the target firm’s balance sheet automatically transfer to

the acquiring firm. True or False

23. Statutory mergers are governed by the statutory provisions of the state in which the surviving entity is chartered.

True or False

24. Staged transactions may be used to structure an earn-out, to enable the target to complete the development of a

technology or process, to await regulatory approval, to eliminate the need to obtain shareholder approval, and to

minimize cultural conflicts with the target. True or False

25. Decisions made in one area of a deal structure rarely affect other areas of the overall deal structure.

True or False

26. The acquisition vehicle refers to the legal structure created to acquire the target company. True or False

27. A post-closing organization must always be a C corporation. True or False

28. A holding company is an example of either an acquisition vehicle or post-closing organization. True or False

29. The forward triangular merger involves the acquisition subsidiary being merged with the target and the target

surviving. True or False

30. The reverse triangular merger involves the acquisition subsidiary being merged with the target and subsidiary

surviving. True or False

31. By acquiring the target firm through the JV, the corporate investor limits the potential liability to the extent of their

investment in the JV corporation. True or False

32. ESOP structures are rarely used vehicles for transferring the owner’s interest in the business to the employees in

small, privately owned firms. True or False

33. Non-U.S. buyers intending to make additional acquisitions may prefer a holding company structure.

True or False

34. If the acquirer is interested in integrating the target business immediately following closing, the holding structure

may be most desirable. True or False

35. Decision-making in JVs and partnerships is likely to be faster than in a corporate structure. Consequently, JVs and

partnerships are more commonly used if speed is desired during the post-closing integration. True or False

36. A corporate structure is the preferred post-closing organization when an earn-out is involved in acquiring the

target firm. True or False

37. In an earnout agreement, the acquirer must directly control the operations of the target firm to ensure the target

firm adheres to the terms of the agreement. True or False.

7

38. When the target is a foreign firm, it is often appropriate to operate it separately from the rest of the acquirer’s

operations because of the potential disruption from significant cultural differences. True or False

39. A financial buyer may use a holding company structure because they expect to sell the firm within a relatively

short time period. True or False

40. A partnership or JV structure may be appropriate acquisition vehicle if the risk associated with the target firm is

believed to be high. True or False

41. Sellers who are structured as C corporations generally prefer to sell assets for cash than acquirer stock because of

more favorable tax treatment. True or False

42. Whether cash is the predominant form of payment will depend on a variety of factors. These include the acquirer’s

current leverage, potential near-term earnings per share dilution of issuing new shares, the seller’s preference for

cash or acquirer stock, and the extent to which the acquirer wishes to maintain control over the combined firms.

True or False

43. Acquirer stock is a rarely used form of payment in large transactions. True or False

44. The seller’s preference for stock or cash will reflect their desire for liquidity, the attractiveness of the acquirer’s

shares, and whether the seller is organized as a joint venture corporation. True or False

45. A bidder may choose to use cash rather than to issue voting shares if the voting control of its dominant shareholder

is threatened as a result of the issuance of voting stock to acquire the target firm. True or False

46. Using stock as a form of payment is generally less complicated than using cash from the buyer’s point of view.

True or False

47. The use of convertible preferred stock as a form of payment provides some downside protection to sellers in the

form of continuing dividends, while providing upside potential if the acquirer’s common stock price increases

above the conversion point. True or False

48. Bidders may use a combination of cash and non-cash forms of payment as part of their bidding strategies to

broaden the appeal to target shareholders. True or False

49. The risk to the bidder associated with bidding strategy of offering target firm shareholders multiple payment

options is that the range of options is likely to discourage target firm shareholders from participating in the

bidder’s tender offer for their shares. True or False.

50. The multiple option bidding strategy introduces a certain level of uncertainty in determining the amount of cash

the acquirer will have to ultimately pay out to target firm shareholders, since the number choosing the all cash or

cash and stock option is not known prior to the completion of the tender offer. True or False

51. Balance sheet adjustments most often are used in purchases of stock when the elapsed time between the agreement

on price and the actual closing date is short. True or False

8

52. Buyers and sellers generally view purchase price adjustments as a form of insurance against any erosion or

accretion in assets, such as plant and equipment. True or False.

53. An earnout agreement is a financial contract whereby a portion of the purchase price of a company is to be paid to

the buyer in the future contingent on the realization of a previously agreed upon future earnings level or some

other performance measure. True or False

54. The value of an earnout payment is never subject to a cap so as not to discourage the seller from working

diligently to exceed the payment threshold. True or False

55. Earnouts tend to shift risk from the seller to the acquirer in that a higher price is paid only when the seller or

acquired firm has met or exceeded certain performance criteria. True of False

56. Offering sellers consulting contracts to defer a portion of the purchase price is illegal in most states. True or False

57. Collar agreements provide for certain changes in the exchange ratio contingent on the level of the acquirer’s share

price around the effective date of the merger. True or False

58. A fixed exchange collar agreement may involve a fixed exchange ratio as long as the acquirer’s share price

remains within a narrow range, calculated as of the effective date of the signing of the agreement of purchase and

sale. True or False

59. Both the acquirer and target boards of directors have a fiduciary responsibility to demand that the merger terms be

renegotiated if the value of the offer made by the bidder changes materially relative to the value of the target’s

stock or if their has been any other material change in the target’s operations. True or False

60. Stock purchases involve the exchange of the target’s stock for acquirer stock only. True or False.

61. If an acquirer buys most of the operating assets of a target firm, the target generally is forced to

liquidate its remaining assets and pay the after-tax proceeds to its shareholders. True or False

Multiple Choice (Circle only one)

1. Which of the following should be considered important components of the deal structuring process?

a. Legal structure of the acquiring and selling entities

b. Post closing organization

c. Tax status of the transaction

d. What is being purchased, i.e., stock or assets

e. All of the above

2. Which of the following may be used as acquisition vehicles?

a. Partnership

b. Limited liability corporation

c. Corporate shell

d. ESOP

9

e. All of the above

3. In a statutory merger,

a. Only known assets and liabilities are automatically transferred to the buyer.

b. Only known and unknown assets are transferred to the buyer.

c. All known and unknown assets and liabilities are automatically transferred to the buyer except for those

the seller agrees to retain.

d. The total consideration received by the target’s shareholders is automatically taxable.

e. None of the above.

4. Which of the following is not a characteristic of a joint venture corporation?

a. Profits and losses can be divided between the partners disproportionately to their ownership shares.

b. New investors can become part of the JV corporation without having to dissolve the original JV corporate

structure.

c. The JV corporation can be used to acquire other firms.

d. Investors’ liability is limited to the extent of their investment.

e. The JV corporation may be subject to double taxation.

5. Which of the following are commonly used to close the gap between what the seller wants and what the buyer is

willing to pay?

a. Consulting contracts offered to the seller

b. Earn-outs

c. Employment contracts offered to the seller

d. Giving seller rights to license a valuable technology or process

e. All of the above.

6. Which of the following is a disadvantage of balance sheet adjustments?

a. Protects buyer from eroding values of receivable before closing

b. Audit expense

c. Protects seller from increasing values of receivables before closing

d. Protects from decreasing values of inventories before closing

e. Protects seller from increasing values of inventories before closing

7. Which of the following are disadvantages of an asset purchase?

a. Asset write-up

b. May require consents to assignment of contracts

c. Potential for double-taxation of buyer

d. May be subject to sales, use, and transfer taxes

e. B and D

8. Which of the following is not true of mergers?

a. Liabilities and assets transfer automatically

b. May be subject to transfer taxes.

c. No minority shareholders remain.

d. May be time consuming due to need for shareholder approvals.

e. May have to pay dissenting shareholders appraised value of stock

9. Which of the following is true of collar arrangements?

a. A fixed or constant share exchange ratio is one in which the number of acquirer shares exchanged for

each target share is unchanged between the signing of the agreement of purchase and sale and closing.

10

b. Collar agreements provide for certain changes in the exchange ratio contingent on the level of the

acquirer’s share price around the effective date of the merger.

c. A fixed exchange collar agreement may involve a fixed exchange ratio as long as the acquirer’s share

price remains within a narrow range, calculated as of the effective date of merger.

d. A fixed payment collar agreement guarantees that the target firm shareholder receives a certain dollar

value in terms of acquirer stock as long as the acquirer’s stock remains within a narrow range, and a fixed

exchange ratio if the acquirer’s average stock price is outside the bounds around the effective date of the

merger.

e. All of the above.

10. Which of the represent disadvantages of a cash purchase of target stock?

a. Buyer responsible for known and unknown liabilities.

b. Buyer may avoid need to obtain consents to assignments on contracts.

c. NOLs and tax credits pass to the buyer.

d. No state sales transfer, or use taxes have to be paid.

e. Enables circumvention of target’s board in the event a hostile takeover is initiated.

11. The form of acquisition refers to which of the following:

a. Tax status of the transaction

b. Acquisition vehicle

c. What is being acquired, i.e., stock or assets

d. Form of payment

e. How the transaction will be displayed for financial reporting purposes

12. The tax status of the transaction may influence the purchase price by

a. Raising the price demanded by the seller to offset potential tax liabilities

b. Reducing the price demanded by the seller to offset potential tax liabilities

c. Causing the buyer to lower the purchase price if the transaction is taxable to the target firm’s shareholders

d. Forcing the seller to agree to defer a portion of the purchase price

e. Forcing the buyer to agree to defer a portion of the purchase price

13. The seller’s insistence that the buyer agree to purchase its stock may encourage the buyer to

a. offer a lower purchase price because it is assuming all of the target firm’s liabilities

b. offer a higher purchase price because it is assuming all of the target firm’s liabilities

c. offer a lower purchase price because it is receiving all of the target’s tax benefits

d. use its stock rather than cash to purchase the target firm

e. use cash rather than its stock to purchase the target firm

14. A holding company may be used as a post-closing organizational structure for all but which of the following

reasons?

a. A portion of the purchase price for the target firm included an earn–out

b. The target firm has a substantial amount of unknown liabilities

c. The acquired firm’s culture is very different from that of the acquiring firm

d. Profits from operations are not taxable

15. Form of payment can involve which of the following:

a. Cash

b. Stock

c. Cash and stock

d. Rights, royalties and fees

11

e. All of the above

16. A “floating or flexible share exchange ratio is used primarily to

a. Protect the value of the transaction for the acquirer’s shareholders

b. Protect the value of the transaction for the target’s shareholders

c. Minimize the number of new acquirer shares that must be issued

d. Increase the value for the acquiring firm

e. Increase the value for the target firm

Case Study Short Essay Examination Questions

END OF CHAPTER CASE STUDY:

DOW CHEMICAL AND DUPONT COMBINE IN A MERGER OF EQUALS

Key Points:

• Successful deal structures reflect the highest priority needs of the parties involved

• Activist investors often play a key role in forcing boards and senior management to restructure their firms

• Financial engineering often is used to restructure underperforming firms

Two of the largest and oldest firms in the U.S. chemical industry announced that they had reached an agreement to merge

on December 11, 2015. The merger would result in the new firm having a combined market value of more than $130

billion. Postclosing, the new firm would be named DowDuPont. The all–stock deal was motivated by a combination of

factors including the effects of slumping commodity prices, weak demand for agricultural chemicals, and headwinds from a

stronger dollar.

DowDuPont would be the second largest chemical company in the world, behind BASF of Germany, with more than

$92 billion in annual revenue. In an unusual display of financial restructuring linked to the merger, the deal is to be

followed by a breakup of the new company into three businesses: agricultural chemicals, specialty products, and materials.

The split-up of the new firm into three publicly traded companies is expected to increase their focus on their served markets

and in turn improve their competitiveness, sales growth, and profit margins due to expense reduction.

Both firms are among the best known brands in the chemicals industry: Dow for plastics and agricultural chemicals and

DuPont for such technical innovations as Kevlar and Teflon. DuPont has suffered from intense competition in Agriculture

from Monsanto, especially in its corn seed business. DuPont’s patents have kept a number of its products proprietary and

profitable. In addition to agriculture, the firm’s business portfolio includes electronics and communication, complex

materials, and safety and protection. Dow Chemical’s business portfolio is divided into two groups: specialty and basic

chemicals. The firm has increased its focus on specialty chemicals which carry higher prices than the highly commoditized

basic chemicals whose profitability is subject to the volatility of the energy markets.

The boards of both Dow and DuPont were under severe pressure by activist investors unhappy with the firms’ subpar

financial performance to increase shareholder value. In 2014, Dow agreed to appoint four independent directors to resolve a

dispute with Daniel S. Loeb, CEO of hedge fund Third Point. In 2015, DuPont successfully thwarted a challenge to their

board’s composition by Nelson Peltz, CEO of Trian Fund Management. In both instances, Mr. Loeb and Mr. Peltz argued

that the firms needed to trim costs and improve operating efficiency as well as to buy back shares and increase dividends.

Win or lose, the activists had made their voices heard.

The combination of Dow and DuPont was billed as a merger of equals. Under the terms of the transaction, Dow

shareholders are to receive a fixed exchange ratio of one share of DowDuPont for each Dow share, and DuPont

shareholders would receive a fixed exchange ratio of 1.282 shares in DowDuPont for each DuPont share. At closing, Dow

and DuPont shareholders would each own approximately 50% of the combined company. DuPont’s Chair and CEO

Edward Breen would retain his title at the new firm, while Dow’s CEO Andrew N. Liveris would become Executive

Chairman of the combined companies. The new firm’s board would consist of 16 directors, consisting of 8 incumbent

DuPont directors and 8 current Dow directors. The planned merger is to be followed by a breakup of the integrated

12

company into three independent, publicly traded companies through tax-free spin-offs giving investors a choice of retaining

or selling their shares in the agricultural, material science, and specialty products businesses. Each of the three businesses

will have Advisory Committees. The breakup is expected to occur 18 to 24 months following closing. DowDuPont will

have dual headquarters in Midland, Michigan and Wilmington Delaware.

The deal will require regulatory approval in several countries and is expected to face intense antitrust scrutiny due to its

huge size and scale. Groups representing various farm and agricultural interests have expressed concerns about the merger

harming competition, particularly in seeds and crop chemicals markets resulting in higher prices for these products. To get

approval, the firms may have to divest significant businesses in areas where the merger is expected to limit competition.

This could reduce the realization of anticipated synergies and the growth potential of some of the businesses to be spun off.

If approved by the regulators, postclosing implementation will be enormously challenging. Within two years following

closing, DowDuPont is expected to realize cost synergies annually totaling $3 billion in expenses. During the same

timeframe, the new firm must undergo extensive reorganization in order to create the proposed new subsidiaries that are to

be spun off to shareholders. Given the probable interrelationships between and among the various operations, this is likely

to prove to be a gargantuan task.

Reorganization involves moving people around, trimming overhead, allocating debt, renegotiating customer and supply

agreements, disentangling jointly used information technology systems, and ensuring that the eventual spun off units will

be considered tax free to shareholders. The logistics of such activities often take many months and DowDuPont is

expecting to implement three spin offs in a relatively short period of time. DuPont’s last spinoff, Chemours, a performance

chemicals unit, has been a disaster, losing three-quarters of its value in less than a year after its separation and represents

the ills that can befall a spinoff.

With a total workforce exceeding 100,000 people, the major task confronting the new firm will be in retaining and

keeping motivated talented people. While it is customary to use retention bonuses to keep those workers that will be needed

during the transition period leading up to the spinoffs, the resulting uncertainty, stress, anger, frustration, and confusion are

likely to result in significant attrition. While such attrition may be desired from a cost savings standpoint, some of those

employees leaving will be critical for the ongoing operations of the business. In businesses that have been as integrated as

Dow and DuPont, layers of management will be stripped away. Management turnover typically tends to be substantially

higher during this period leading to confusion among reporting relationships and disjointed communication. Also, it is

likely that management talent will be stretched thin as managers are asked to maintain or improve the performance of their

business units and to simultaneously implement the logistics required for the planned spinoffs.

Tax considerations are a primary driver of the deal. The tax-free treatment of the spin-offs is viewed as a highly tax

efficient alternative to selling selected businesses which could result in significant taxable gains to Dow and DuPont.

Structured as a merger of equals in a share for share exchange, the DowDuPont deal also is tax free to shareholders.

Typically, companies that have been through a change of control are liable to pay capital gains taxes on subsequent spin–

offs, under section 355 of the U.S. Internal Revenue Code (see Chapter 16 for more detail). If both companies, however, do

not formally undergo a change of control, the spin-offs can be tax-free. After their merger, Dow and DuPont plan to argue

that no change of control will have occurred by structuring their initial deal as a merger of equals. Bolstering their view that

a change of control has not occurred is that the two companies have many shareholders in common. Vanguard Group Inc.,

State Street Global Advisors, Capital World Investors and BlackRock Inc. are, in that order, the top holders of both

companies’ stock.1

Investors immediately expressed skepticism following the deal’s announcement on December 11, 2015 with Dow’s

share price falling by 2.8% to $53.57 and DuPont’s shares falling by 5.6% to $72.91. DuPont’s shares fell more

precipitously on news that its 2016 sales growth would be flat. The firm also announced plans to cut its global workforce by

10% as part of its restructuring program. Investors expressed concern about the deal’s complexity, the potential for the

deal not to close due to regulatory issues, and the potential difficulty in implementing the breakup of the company in the

time frame indicated by management.

Discussion Questions and Answers:

1The most recent precedent in which a merger of equals’ structure was employed to argue successfully that a change in

control had not taken place (and therefore there was not any actual sale) was in the 2007 merger of drug distributors

AmerisourceBergen Corp and Kindred Healthcare Inc. Once the merger took place the new company spun off its pharmacy

businesses tax free to shareholders.

1. Speculate as to why the deal was structured as a merger of equals. What are the advantages and disadvantages of such a

structure? Be specific.

2. What are the key assumptions DowDuPont is making in arguing the merger followed by the spin-off of three

businesses makes sense?

3. What is the form of payment and the form of acquisition used in this deal? What are the advantageous and

disadvantageous of the form of payment and acquisition used in this deal?

4. In the deal, Dow shareholders will receive a fixed exchange ratio of 1.00 share of DowDuPont for each Dow share, and

DuPont shareholders will receive a fixed exchange ratio of 1.282 shares in DowDuPont for each DuPont share. Dow

and DuPont shareholders will each own approximately 50 percent of the combined company, excluding preferred

shares. Common shares outstanding at Dow and DuPont at the time of the announcement were 1.160 billion and .876

billion respectively. Using this information, show how the postclosing ownership distribution can be determined How

might these fixed share exchange ratios have been determined during the negotiation of the deal?

14

5. Dow’s price per share on December 11, 2015 was $54.91 and DuPont’s was $74.55. Dow shares outstanding were 1.16

billion and DuPont’s outstanding shares were .876 billion. Assume anticipated annual cost synergies are $ 3.0 billion in

perpetuity and DowDuPont’s cost of capital is 10%. What is DowDuPont’s total market cap excluding synergy? What

is the market cap including synergy using the zero growth method of valuation (see Chapter 7)?

THE ELUSIVE ISSUE OF PRICE

Key Points:

• The acquirer’s cost often is more than what it pays target investors per share

• Additional costs include liabilities assumed by the buyer

• Assumed liabilities can be especially onerous if their future cost is difficult to estimate

• Negotiators often focus on minimizing such risk

______________________________________________________________________

The growth of cloud computing and the growing connectivity in our lives have pressured semiconductor2 makers to

achieve greater economies of scale to drive down costs and to offer a broader array of products ranging from commodity–

like to highly complex chips. These market forces have resulted in an ongoing consolidation within the industry. A recent

example of such consolidation is Intel’s (the world’s largest chipmaker) acquisition of Altera, an integrated circuits

manufacturer, for $16.7 billion. Intel’s interest centered on Altera’s programmable chips, a higher margin product whose

sales would help offset the declining personal computer market. Altera faced substantial capital expenditures to remain

competitive and being acquired represented a reasonable way to maximize shareholder wealth.

What follows is a description of events that transpired between Altera and Intel beginning in late 2014 and ending in

mid-2015 in a signed merger agreement. These events illustrate common negotiating tactics used by potential acquirers and

target boards and senior managers to hammer out M&A agreements.3

Given their long standing business relationship dating back to the late 1980s, it was easy for Intel’s CEO, Brian M.

Krazanich, to approach Altera’s CEO, John P. Daane, in late 2014 to discuss a commercial licensing deal. During the

conversation, Mr. Krazanich expressed Intel’s interest in acquiring the firm but he refrained from discussing a price range.

Aware of his fiduciary responsibility to shareholders, Mr. Daane said he would bring Intel’s expression of interest in buying

Altera to the firm’s board of directors.

Discussions during the early phase of the negotiating process are often nuanced. Any reference to purchase price by the

potential acquirer is usually verbal, vague, expressed in a range or formula (i.e., multiple of earnings), and conditioned on

performing “adequate” due diligence. The start date, length, and intrusiveness of due diligence often becomes a means for

both parties to leverage their positions. Sellers routinely move aggressively to get the buyer to state as high an offer price

with as few caveats as possible before granting the buyer the right to examine detailed financial statements, operations, etc.

Buyers use the absence of proprietary information as a reason for giving a price estimate as a range or formula or subject to

conditions allowing for revision of the initial offer price based on the outcome of due diligence.

Three weeks had passed before the two CEOs talked again. In the interim, Altera’s board hired financial advisor

Goldman Sachs. In mid-December the two met again with Mr. Krazanich willing to indicate a price range of $14 to $15

billion or $45 to $48 per share, subject to Intel performing due diligence. Mr. Daane stated that the price was too low and

that the firm would not enter due diligence unless Intel revised its offer up by at least $1 billion.

2 Used in such products as computers, cell phones, appliances, and medical equipment, semiconductors (usually composed

of silicon) conduct electricity more than an insulator but less than a pure conductor.

3 The source for this information is found in Altera’s Definitive Proxy Statement (Schedule 14A) filed with the SEC on

August 24, 2015.

15

The Altera board formed a committee consisting of independent board members called the Transaction Committee

whose expressed purpose was to review Intel’s offer and to make recommendations to the full board. Such committees are

formed to minimize the appearance of any improprieties. Goldman Sachs representatives discussed strategic options with

the Altera board including contacting other potential bidders. After discussing the benefits and risks associated with a wider

sale process, the Transaction Committee recommended to the full board that an Intel bid deserved further consideration and

that Intel be told that their proposal was inadequate in an effort to get a higher offer price.

Informed in early January 2015 that Altera had rejected their $45 to $48 per share proposal, Intel raised its bid to $55 per

share, again on the condition Altera would allow an appropriate due diligence. The Altera CEO countered that at that price

his firm would not allow due diligence to begin. The Intel CEO agreed to have his board reconsider their offer and would

counter with a revised offer if his board felt comfortable with the potential synergies.

All previous offers made by Intel had been verbal. On January 27, 2015, Intel submitted to the Altera Board a legally

non-binding written proposal authorized by the Intel board to acquire Altera for $50 per share based on publicly available

information about Altera. Frustrated by Altera’s unwillingness to provide proprietary information, Intel hardened its

position by reducing the offer price from $55 to $50 saying that this was the best they could do in the absence of due

diligence. The proposal stated that the bid could be revised upward if a due diligence process were to validate anticipated

merger benefits.

The Altera Board in discussing the proposal with its financial advisors expressed concern that Intel could make the bid

public, undertake a hostile bid, or walk away, given that the talks had been underway for several months. The Altera board

decided against a wider sale, since there were only a small number of potential buyers capable of paying the purchase price

Altera demanded. They also believed that a wider sale process could result in rumors negatively impacting Altera’s

relationships with customers, suppliers, business partners and employees.

At the end of March, Altera submitted a draft merger agreement containing the restatement of Altera’s proposal that

Intel should agree to use reasonable best efforts to get regulatory approval and that Altera should be compensated if the deal

was not completed over failure to get regulatory approval. At this point, the talks stalled and the media speculated that the

deal might not happen.

On May 7, 2015, Intel sent a letter to the Altera Board containing a new acquisition proposal stating that, if Intel and

Altera did not reach an agreement by June, Intel would abandon discussions. Intel’s proposal included a price of $50 per

share compared to its earlier $58 price bid, arguing it was the best it could do having access only to public information.

However, it did make other concessions Altera had demanded saying it would use reasonable best efforts to obtain

necessary regulatory approvals and would pay a reverse termination fee of $400 million if the acquisition could not be

completed for antitrust or competition law reasons. The letter indicated that this was Intel’s final offer.

4 Termination fees are those paid by the seller to the buyer if the seller chooses to accept a better offer. Reverse termination

fees are paid by the buyer to the seller if the deal cannot be closed due to certain conditions not being satisfied.

5 If a party promises “reasonable best efforts”, everything that can be done should be done, but not to the point of going

bankrupt. It can also imply that Intel would have to “leave no stone unturned.” By contrast, “reasonable efforts” implies that

what can be done should be done, in the context and purpose of the contract, but without requiring a party to leave “no

stone unturned“. “Reasonable efforts” is a less onerous standard than “reasonable best efforts”.

16

The Altera board approved the terms of the Intel proposal but at a purchase price of $56 per share. Intel responded in

writing saying that $54 per share was the highest it would go and that it would agree to a reverse termination fee of $500

million. On June 1, 2015, the two firms announced a joint communication indicating that Intel had reached an agreement to

acquire Altera on the terms previously described. After receiving regulatory approval, the deal closed on January 28, 2016,

more than one year after Intel’s CEO made first contact with Altera’s Chief Executive Officer.

Illustrating Bidding Strategies—Appollo’s Takeover of CEC Entertainment

In a deal designed for a speedy conclusion, Richard M. Frank, Executive Chairman of CEC Entertainment announced on

January 16, 2014 that the firm had entered into a definitive merger agreement with private equity firm Apollo Global

Management. The deal was valued at $1.3 billion including the assumption of $70 million in debt. AT $54 per share, the

deal represented a 25% premium over the firm’s closing price on January 7, 2014 when first reports of the deal surfaced.

The bid was structured to include an accelerated means of obtaining shareholder approval, an exceptionally short time

period for CEC to solicit higher bids, and a poison pill intended to deter activist hedge funds and other potential bidders

from entering the fray.

Mr. Frank said in a news release that “the deal represented the best option resulting from their extensive review of a full

range of strategic alternatives.” CEC is the parent firm of the Chuck E. Cheese restaurant chain consisting of 577

restaurants in 47 states and 10 foreign countries. Known for its quirky looking mouse logo and its offering of food and

video games in a child friendly environment, the restaurant chain had been attempting to sell itself for several months.

While the board had agreed to the deal, CEC shareholders had not yet done so. Recent developments showed that

reaching closing quickly was critical. In 2013, Carl Icahn bought a stake in Dell Inc. after the firm had agreed to a $24.4

billion buyout and subsequently lobbied against the proposal to take the firm private. While the buyout eventually

succeeded, it did so only after the purchase price was increased. Hedge funds also managed to delay closing in such deals

as Sprint’s buyout of Clearwire and MetroPCS’s merger with T-Mobile. Both deals eventually closed but only after their

initial purchase prices were increased. According to FactSet, between 2005 and 2010, bidders were forced to raise their

initial offer prices to close the deal in about one-half of the transactions in which the initial offer prices were challenged as

too low. Since 2010, initial bidders in virtually all deals facing such challenges were forced to either raise their offer prices,

improve the terms (e.g., go to all cash), or to withdraw their bids.

In addition to the acceleration of the tender offer, the deal included a so-called top-up option enabling Apollo to buy

newly issued CEC shares if it failed to purchase enough of CEC’s outstanding voting shares to reach the 90% threshold

required to “squeeze out” the remaining shareholders. Apollo also adopted a “dual track” tactic made popular in 3G

Capital’s 2010 takeover of restaurant chain Burger King. This involves the inclusion in the agreement with CEC of a

provision requiring CEC to prepare and file with the SEC a proxy for a merger in parallel with the commencement of

Apollo’s tender offer. If the tender offer is delayed for any reason such as a shareholder lawsuit seeking a higher offer price

or a competing bid from another suitor, Apollo has the right to withdraw the tender offer and to pursue a merger.

CEC also had the right under a “go–shop” provision to solicit superior bids until January 29, 2014. The go-shop

provision in the agreement also reflects Apollo’s race to complete the deal. It is in force for only two weeks compared to a

more standard 45 days. Go-shop provisions normally allow the target to seek other bidders to enable the target’s board to

fulfill its fiduciary responsibility to its shareholders. However, the CEC go shop provision applies only to potential bidders

17

who were not invited by CEC to submit a bid in the second round of the CEC auction process. This effectively limits the

bidding process to firms currently participating in the auction, as the firms not invited to the second round may not have

completed sufficient due diligence to justify their submitting a higher bid than Apollo’s offer. The net effect of all of these

tactics is to force the remaining bidders in the auction for CEC to move quickly or to drop out.

CEC also announced that it had introduced a poison pill defense intended to prevent others from acquiring more than

10% of its outstanding shares. The adoption of the poison pill makes it less likely that others will seek to block the deal and

push for a higher purchase price. Another bidder buying more than 10% of CEC’s outstanding shares would allow the firm

to issue additional shares thereby increasing the overall cost to acquire CEC. Existing investors such as Fidelity

Investments and Wellington Management, who already own at least 10 % of the firm as of March 31, 2013, are exempt

from the pill.

Whether or not the poison pill is at odds with the board’s fiduciary responsibility to maximize shareholder value is

problematic. The use of a poison pill in a friendly transaction is unusual with the last deal to include such an arrangement

being Dell Inc.’s 2010 takeover of Compellent Technologies Inc. Its introduction could cause lawsuits. To minimize

litigation, the board announced its intention to search for other potentially higher bids as allowed under the agreement with

Apollo.

The deal closed on February 14, 2014, thirty days after it had been announced. The speed with which the transaction was

completed along with the phalanx of other unconventional tactics employed for a friendly deal may have proved too

daunting to other would be suitors. In accordance with the merger agreement, CEC merged with an Apollo affiliate and will

be operated as a privately-held, wholly-owned subsidiary. CEC’s common stock ceased trading on the NYSE as Chuck E.

Cheese, the cartoonish character of the restaurant chain bearing his name, was under new management.

T-Mobile and MetroPCS Complete a Multibillion Dollar Merger

_____________________________________________________________________________

Case Study Objectives: To illustrate

• How deal structures reflect the primary needs of the parties to the negotiations

• How reverse mergers enable private firms or wholly owned subsidiaries of parent firms to go public and

• Their use as a corporate restructuring strategy.

______________________________________________________________________________

Background

T-Mobile Chief Executive Officer John Legere has always been considered a maverick in the wireless telecommunications

industry. At an interview at the Consumer Electronics Show in Las Vegas in 2014 he discussed how T–Mobile had all the

momentum in the industry. “The firm,” he said,” has presented itself as the antithesis of what most people do not like about

their carriers.” Reflecting growing market acceptance of its new marketing campaign, the firm added 4.4 million new

customers, including prepaid, during 2013.

After U.S. regulators nixed a $39 billion merger between T-Mobile and AT&T in late 2011 due to antitrust concerns, the

outlook for T–Mobile, the nation’s fourth largest cellular phone carrier, looked bleak. The firm was hemorrhaging

customers to Verizon and AT&T once their contracts ended. Rene Obermann, CEO of T-Mobile’s parent firm Deutsche–

Telekom, made it clear that he was unwilling to increase significantly its investment in T-Mobile. Without a 4G LTE

network and the ability to offer high-end smartphones like its competitors because of its lack of clout with handset vendors,

the firm appeared destined to shrink amid an industry in flux.

Wireless communications in the U.S. market is transitioning to what the industry has fought against for two decades: a

commodity business in which all competitors look the same and prices keep coming down. For ten years, AT&T and

Verizon, which together have one-half of the market by number of subscribers, have been quickest to roll out big, fast

wireless networks. Their advertisements have focused more on quality than price. The basic business model in the wireless

18

industry involved attracting customers with deeply discounted prices for handsets, locking them into two-year service

contracts, and limiting their ability to switch by imposing onerous contract termination fees. With 90% of U.S. adults

having a cell phone, the usefulness of this model is fading fast. The basis of competition is now shifting from gaining

market share to retaining existing customers and encouraging other customers to change their current wireless carrier.

Sensitive to changing industry dynamics, the U.S. Justice Department and the Federal Communications Commission

(FCC), which had not supported the aborted tie up between AT&T and T-Mobile, seem focused on maintaining three or

four national competitors. This number of competitors in most developed countries appears to keep competition healthy

and to hold prices down. Since rejecting ATT&T’s proposed acquisition of T-Mobile, the Justice Department and the FCC

have approved several other deals driven in large measure to acquire spectrum. These deals included AT&T’s purchase of

Leap, a prepaid service with spectrum holdings in cities. Sprint combined with Softbank in 2013 and later bought out its

broad band partner Clearwire, ultimately giving the firm the biggest spectrum holdings among the four competitors.

Not to be outdone, T-Mobile merged with MetroPCS on May 1, 2013 in a complex deal structure designed to allow T–

Mobile’s parent Deutsche-Telekom to exit T-Mobile over time, satisfy T-Mobile’s and MetroPCS’s need for additional

spectrum, realize substantial cost synergies, and to provide a significant takeover premium for MetroPCS shareholders as

an incentive to approve the deal. Although its geographic coverage is less than its larger competitors, this deal gave T–

Mobile the fastest network in the U.S. For Obermann, who after seven years as CEO was succeeded by Chief Financial

Officer Timotheus Hoettges at the end of 2013, the deal was probably his last chance to find a solution to the U.S. business

that had long eluded him. What follows is a discussion of how reverse mergers can be used as part of a complex

restructuring strategy to achieve these diverse strategic objectives for each of the three parties involved: Deutsche-Telekom,

T-Mobile, and MetroPCS.

The Shareholders’ Dilemma

In late 2012, T-Mobile announced that it had reached an agreement to merge with MetroPCS. Dallas-based MetroPCS is a

low-cost, no-contract provider of prepaid data plans and inexpensive phones targeted at Americans who could not afford

Verizon and AT&T’s more expensive offerings. At the time, it was the fifth largest wireless carrier in the U.S. based on the

number of subscribers. According to Roger Linquist, Chairman and CEO of MetroPCS, the deal addresses the firm’s need

for additional spectrum and allows for expansion into underserved markets. The firm’s shareholders in assessing the

proposed deal were confronted with the usual dilemma: Do the proposed benefits of the combination represent a better

alternative to remaining a standalone company?

In addition, the deal structure was complex. T-Mobile, a wholly-owned subsidiary of Deutsche-Telekom prior to the

merger, was taken public through a reverse merger with MetroPCS. The deal was recorded for financial reporting purposes

as a recapitalization of MetroPCS. A recapitalization involves a change in a firm’s capital structure: a change in the number

of shares outstanding and the amount of debt relative to equity. Prior to closing, MetroPCS would declare a 1 for 2 reverse

stock split (shareholders would receive one new common share for every two shares held prior to the split), make a cash

payment of $1.5 billion to its shareholders (approximately $4.09 per share prior to the reverse stock split), and acquire all of

T-Mobile’s stock by issuing to Deutsche Telekom 74% of MetroPCS’ newly issued common stock. That is, MetroPCS

exchanged almost three–fourths of its shares for 100% of T-Mobile’s shares held by Deutsche-Telekom. Consequently,

Deutsche-Telekom would own about 74% of Newco, with the remaining 26% owned by MetroPCS shareholders.

19

A recapitalization is viewed as a financial reorganization in which Deutsche-Telekom would have a substantial

continuing interest in Newco as a result of its exchange of T-Mobile shares for MetroPCS shares. T–Mobile’s operations

are unaffected; and, as such, a recapitalization is not considered an actual sale of the business. Consequently, the deal is tax–

free to Deutsche-Telekom. See Chapter 12 for a more detailed discussion of this matter.

The Newco shares held by MetroPCS shareholders would trade on a public stock exchange. While not impacting

Newco’s market value, the reverse stock split would reduce the number of Newco shares outstanding following the

exchange of 74% of MetroPCS post-split shares for all of T-Mobile shares. The 26% of the Newco shares held by former

MetroPCS shareholders would be publicly traded. Thus, the intent of the reverse split may have been to support the value of

the publicly traded Newco shares by boosting earnings per share to mitigate any selling pressure on the stock. That is, for a

given level of earnings, EPS increases when shares outstanding decrease, making such shares theoretically more attractive.

Deutsche Telekom also agreed to transfer T-Mobile’s debt owed to Deutsche-Telekom (so-called intercompany debt)

into new $15 billion senior unsecured notes to be paid off by Newco. It also agreed to provide Newco with a $500 million

unsecured revolving line of credit and a commitment to provide up to $5.5 billion to help finance certain MetroPCS third–

party financing transactions. The latter could include resellers of MetroPCS’s prepaid services such as BestBuy and other

retailers who sign up customers

MetroPCS’s Lindquist argued that the ownership distribution in Newco between MetroPCS shareholders and Deutsche–

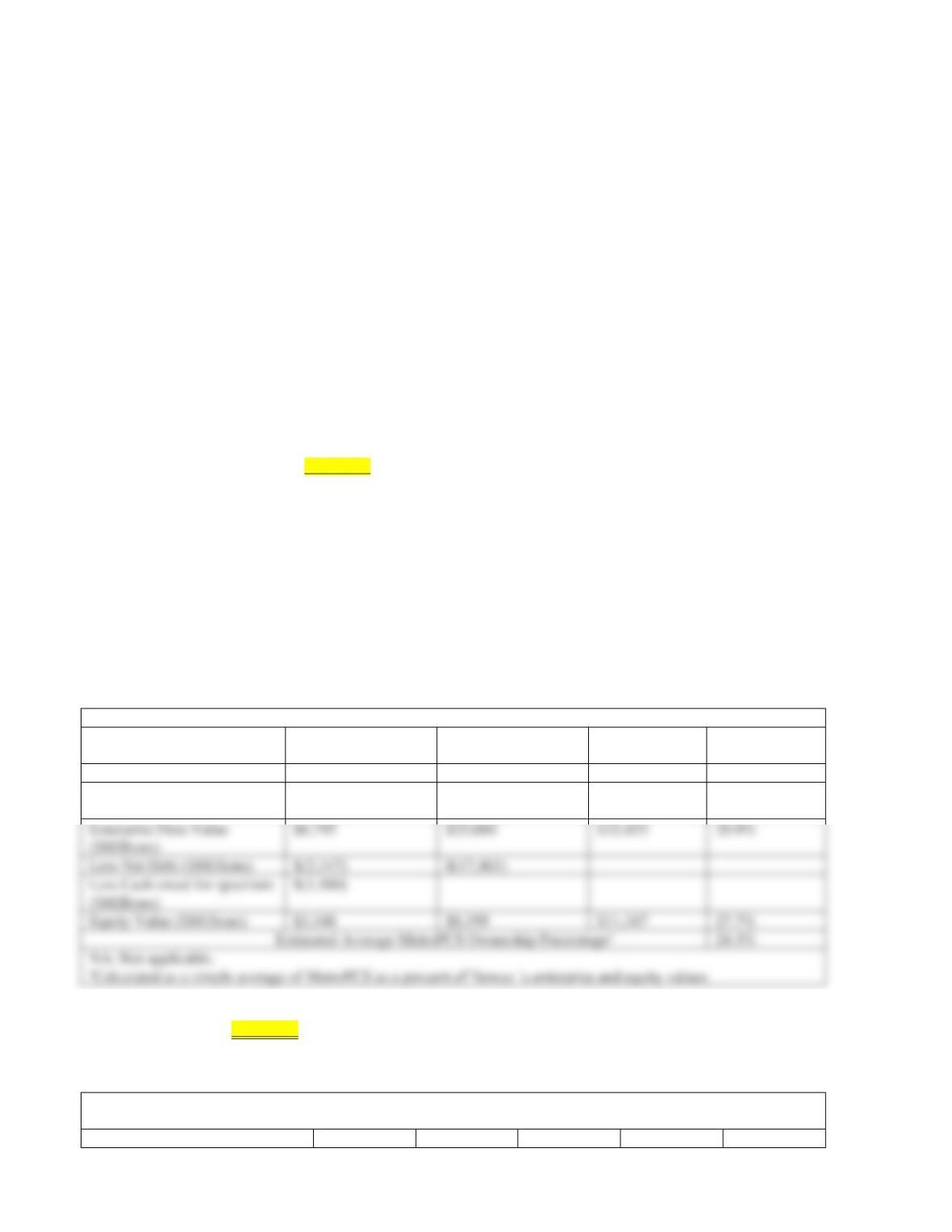

Telekom was favorable based on the relative contribution of MetroPCS and T-Mobile to the value of Newco. A simple

average of enterprise and equity values for each firm as a percent of Newco’s value indicated that MetroPCS’s contributed

24.3% of the value of Newco (see Table 11.6). Yet, the MetroPCS board of director was able to negotiate an approximate

26% stake in Newco, perhaps reflecting the perception that MetroPCS would contribute more to projected cost synergies

than T-Mobile.

Newco’s valuation depended on the assumption that industry average valuation multiples could be applied to valuing the

combined firms. At the time, wireless carriers were trading at an average of five times earnings before interest, taxes,

depreciation and amortization (EBITDA). MetroPCS’s and T–Mobile’s enterprise values (equity plus net debt) were

estimated by multiplying this price to EBITDA multiple by each firm’s EBITDA over the prior twelve months. Equity

values for each firm were calculated by deducting net debt (i.e., total debt less cash and marketable securities) from the

estimated enterprise values. MetroPCS’s enterprise value was further reduced by the cash payment made to its

shareholders, since this cash would be unavailable for transfer to Newco.

Table 11.6 MetroPCS Ownership Analysis

MetroPCS

T-Mobile

Newco

MetroPCS as %

Newco

Firm Value/EBITDA

5x

5x

NA

NA

2013 Estimated EBITDA

($Millions)

$1,359

$5,132

$6,491

NA

($Millions)

Less Net Debt ($Millions)

$(2,147)

$(17,461)

Less Cash owed for spectrum

$(1,500)

Equity Value ($Millions)

$3,148

$8,199

$11,347

27.7%

24.3%

NA: Not applicable.

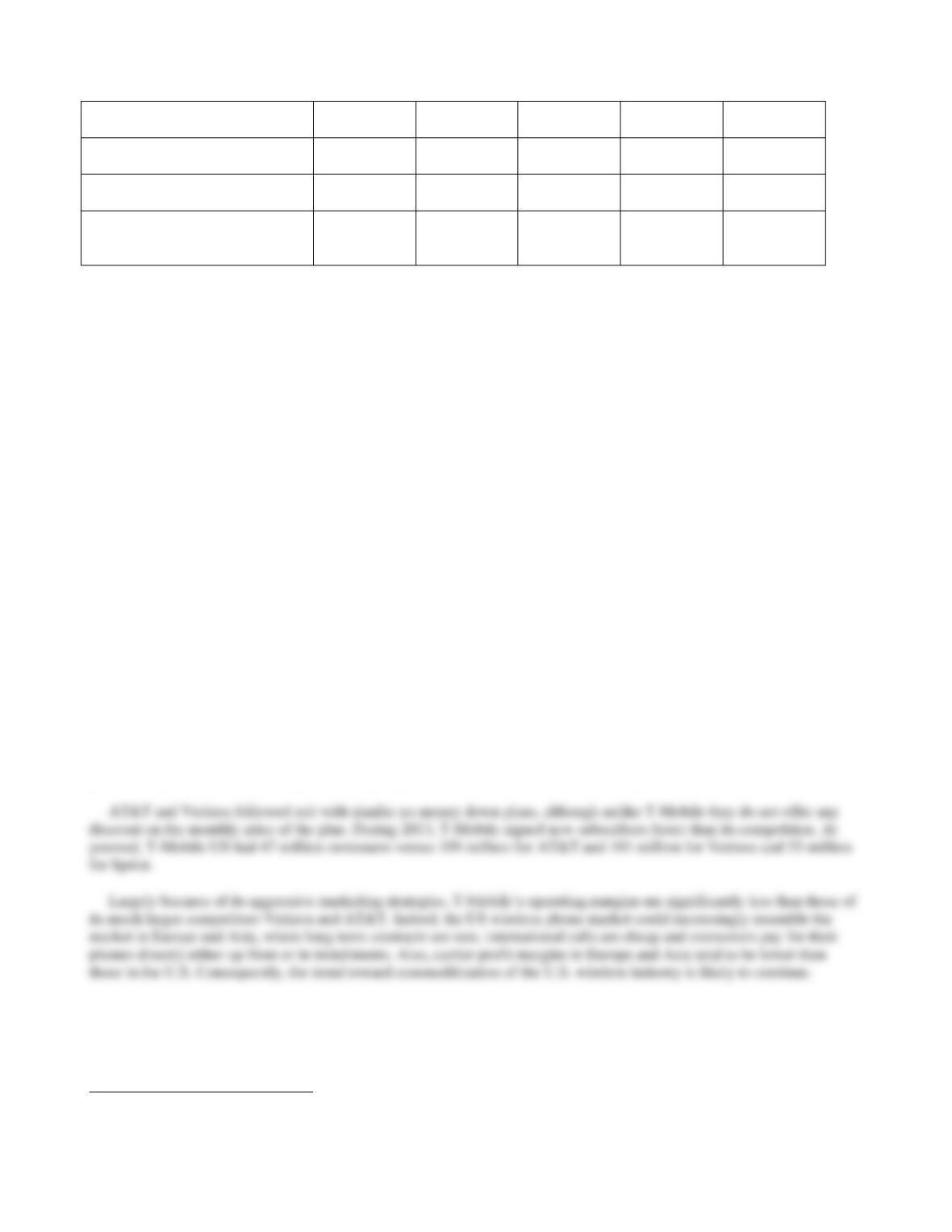

Critics of the proposed deal raised concerns about the amount of leverage Newco would have following closing.

However, as shown in Table 11.7, MetroPCS’s financial leverage following closing was in line with its peers. In addition,

its S&P credit rating of BB was higher than its peers. Note that net debt is gross or total debt less cash and marketable

securities.

Table 11.7 Comparison of Newco Peers Leverage and Credit Ratings

Based on Last Twelve Months EBITDA

Leap

Sprint

Newco

MetroPCS

T-Mobile

20

(Post-

Merger)

(Pre-Merger)

Gross Leverage

(Total Debt/EBITDA)

5.5x

5.5x

3.6x

3.1x

3.6x

Net Leverage

(Net Debt/EBITDA)

4.4x

3.0x

3.4x

2.4x

3.6x

S&P Rating

B-

B+

BB

B+

NA (part of

Deutsche

Telekom

Selecting a Restructuring Strategy

The reverse merger was undertaken in lieu of a direct sale of T-Mobile to a strategic buyer or an initial public offering.

Why? Since regulators had disallowed the proposed AT&T takeover of T-Mobile, it was unlikely that there would be a

strategic buyer big enough to buy the firm. IPOs could be administratively cumbersome and expensive.6 Furthermore, since

Deutsche-Telekom was unwilling to invest additional capital into T-Mobile to achieve the necessary size to be competitive

with Verizon and AT&T, it was unlikely that an IPO would attract much investor interest. Consequently, a reverse merger

seemed to be a reasonable option, since it would enable the creation of a new wireless company with the scale to make it

competitive without Deutsche-Telekom investing additional funds. In time, the combined firms could become more

attractive to potential investors enabling Deutsche-Telekom to exit the business at a much higher price than could be

achieved at that time.

In a reverse merger, shareholders of a private firm exchange their shares for shares in a public firm, with the public firm

surviving the merger. Although it technically is a takeover of the private firm by the public firm, the public firm becomes

an entirely new operating company and often changes its name to that of the privately held firm. That is, T-Mobile was

merged into MetroPCS, with MetroPCS surviving. Subsequently, MetroPCS was renamed T-Mobile US, Inc. and trades

under the ticker symbol TMUS on the NASDAQ stock exchange. See Chapter 10 for a more detailed discussion of reverse

mergers.

Prologue

T-Mobile US, the fourth biggest U.S. wireless company, rose 6% in its first day of trading as a public company to $16.52.

T-Mobile’s Chief Executive Officer John Legere noted “It will be fun to have people voting on the stock every day.” True

to his word, T-Mobile has been shaking up the industry. Late last year, the firm started allowing customers to upgrade their

phones twice a year and introduced no-money down plans for new phones, such as the popular IPhone, forcing competitors

to introduce similar programs.

In early 2014, T-Mobile announced that it would pay termination fees of up to $350 for Verizon, Sprint or AT&T

customers dropping their contracts with these carriers and switching to T-Mobile. Furthermore, T-Mobile offered a credit of

as much as $300 toward a new phone, without having to sign a two year contract. In place of a two year contract, customers

pay monthly installments for the phone they get up front and lower international roaming rates.

Discussion Questions

1. The Deutsche-Telekom board decided against a divestiture of T-Mobile or an initial public offering to pursue a reverse

merger. What other alternatives to merging its wholly-owned subsidiary T-Mobile with another firm could Deutsche-

Telekom have pursued? Be specific. What are the advantages and disadvantages of the other options?

6 Companies going public through an IPO must file a Form S-1 with the SEC. However, a reverse merger requires only the

filing of a Form 8-K, which is much less extensive than a Form S-1. For more information on SEC filings, see Chapter 2.